![]() In all likelihood, an early retiree in the United States is going to purchase ACA (Obamacare) compliant Health Insurance on the Federal or a State Health Insurance Marketplace.

In all likelihood, an early retiree in the United States is going to purchase ACA (Obamacare) compliant Health Insurance on the Federal or a State Health Insurance Marketplace.

Even though the ACA has provided common standards, Health Insurance is still a complex topic with numerous trade-offs. Coverage levels and premiums vary. Every insurance company has a different approach to cost sharing. Each State has a slightly different implementation, maybe a different website, and wildly different prices.

Subsidies may pay nearly all of your premium, or they may cover nothing. It isn’t always clear which will apply until after the fact. As a result, some will get an extra large tax bill at the end of the year, while others will pay too much each month. They may even provide a disincentive to earn a higher income.

But much like the Income Tax, those who understand the the system can optimize their income and investments. Knowledge is power. Optimizing Obamacare starts with understanding the system. Then we can make choices to minimize costs and maximize coverage.

The Affordable Care Act Basics

Simply stated: the ACA requires everyone in the US to buy health insurance. Nobody can be denied coverage or charged more because of pre-existing conditions.

Policies are standardized in name and level of coverage: Bronze, Silver, Gold, Platinum. The only difference is how much you pay for health services versus how much the insurance company pays. The metal levels don’t indicate a level of quality or amount of care you can get.

A Bronze plan is expected to cover 60% of the total cost of care. This increases to 70%, 80%, and 90% for Silver, Gold, and Platinum plans, respectively. Premiums (prices) increase accordingly.

Each policy will be unique in how it covers the cost of care. One silver plan may have lower premiums but higher deductibles. Another silver plan may have a lower co-payment but a higher out of pocket maximum.

It is important to evaluate these differences against personal medical needs. As every kid who is forced to wear an over-sized Christmas sweater knows, bigger isn’t always better.

To ensure access to a quality level of coverage for everyone, subsidies (Premium Tax Credits) are provided. In practice, this means every household in America that qualifies for subsidies will pay the same price for a quality health plan as other households of the same size and income, irrespective of age, where they live, or level of health.

Premiums and Premium Tax Credits (aka Subsidies)

For a household that qualifies for Premium Tax Credits (PTC), only two pieces of information are required to determine maximum insurance prices for a Silver plan:

Households earning between 1-4x of the FPL qualify, which is the majority of households as seen by the high incomes in the table.

| FPL (2015) → Household size (↓) | 100% | 200% | 250% | 400% |

|---|---|---|---|---|

| 1 | $11,770 | $23,540 | $29,425 | $47,080 |

| 2 | $15,930 | $31,860 | $39,825 | $63,720 |

| 3 | $20,090 | $40,180 | $50,225 | $80,360 |

| 4 | $24,250 | $48,500 | $60,625 | $97,000 |

Below 100% of the FPL (or 133% (or 138%) in some States) assistance programs such as Medicaid are (generally) available. (See brooklynguy’s comment for more.) Above 400% of the FPL, you don’t need subsidies for health insurance to be considered “affordable.” Congratulations.

FPL numbers change every year. Most recent Federal Poverty Level data here.

Premium Tax Credits (PTC)

Premium Tax Credits (subsidies) are a direct function of household income.

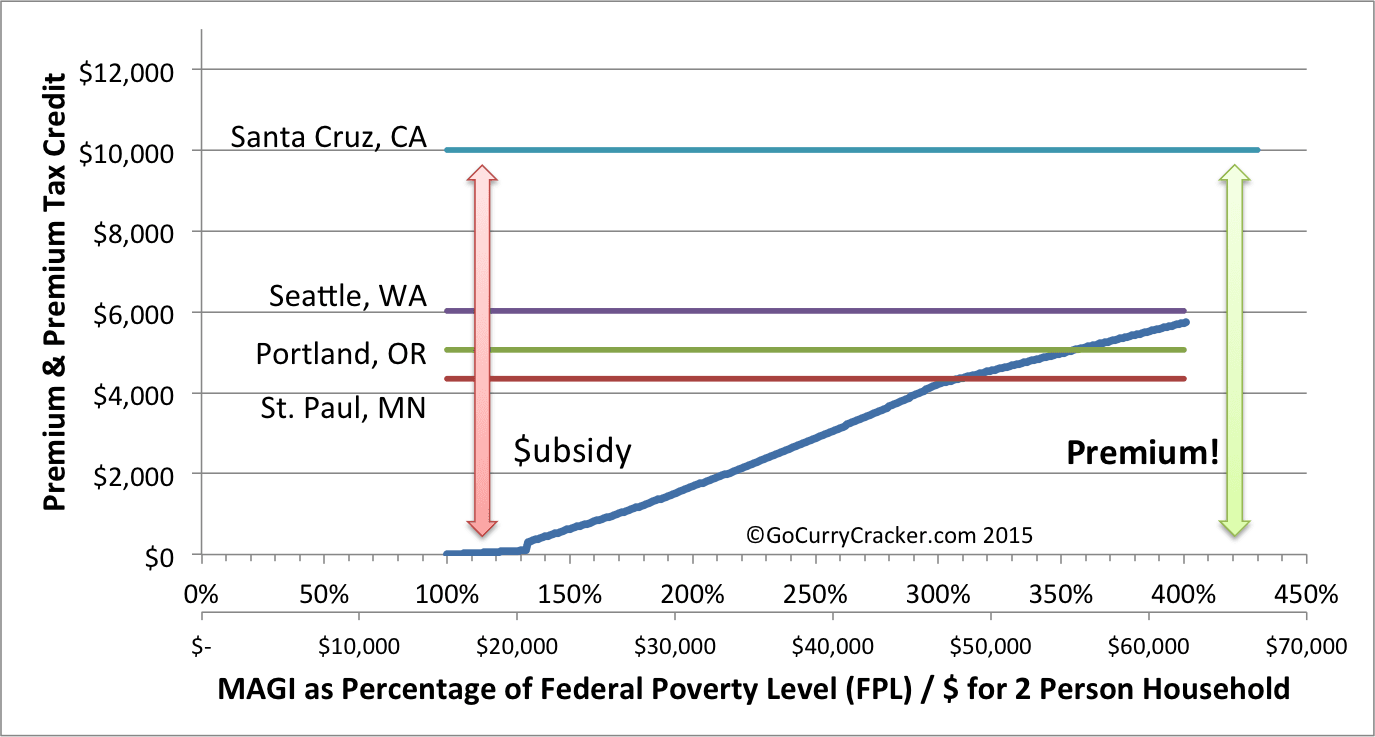

The following chart shows an example for a 2 person household. The blue line shows the maximum cost for the Second Lowest Cost Silver Plan (SLCSP) available on the Marketplace, and comes directly from the IRS. In this example, the unsubsidized premium is ~$6k for my wife and me in Seattle, WA.

If income is exactly 100% of the FPL, the max we can pay is 2% of Income or ~$300/year. The PTC would fully cover the remaining ~$5,700. Thanks Obama!

If income is higher at 400% of the FPL, the max we pay is 9.5% of income or ~$5,950/year (~$500/month.) The PTC would cover the last $50.

If the SLCSP had a higher price tag (maybe $7k instead of $6k) the Premium Tax Credit would be larger. We would still pay the same fixed percentage of income, regardless.

But maybe we want a Silver plan with a lower deductible but a higher premium. Or we want a Gold or Platinum plan. In that case, we can apply our Premium Tax Credit to those other plans and we are responsible for any additional expense.

The method by which the Premium Tax Credit is reduced with income could be thought of as a tax. For each additional $1 of income, the PTC is reduced by $0.02, $0.15, or $0.095, or effective “tax” rates of 2%, 15%, and 9.5%.

The method by which the Premium Tax Credit is reduced with income could be thought of as a tax. For each additional $1 of income, the PTC is reduced by $0.02, $0.15, or $0.095, or effective “tax” rates of 2%, 15%, and 9.5%.

Above 400% of FPL, the subsidy is eliminated completely. If the SLCSP is priced much higher than $6k, this can result in a very substantial increase in annual Premium. This is sometimes referred to as the Obamacare Premium Subsidy Cliff.

Obamacare Premium Subsidy Cliff

In the example above, earning more than 400% of the FPL wasn’t a big deal. The elimination of the PTC only causes our premium to rise by ~$50/year.

But the impact can be severe. To illustrate, I quoted ACA SLCSP prices for a few cities where we would consider having a home base.

Minnesota has some of the lowest insurance prices in the nation (Red line.) Even with the lower prices, our monthly premium is still the same as in the other states. We just receive a smaller subsidy.

Minnesota has some of the lowest insurance prices in the nation (Red line.) Even with the lower prices, our monthly premium is still the same as in the other states. We just receive a smaller subsidy.

Because of the lower cost of insurance, at ~300% of the FPL we would already be paying the full unsubsidized price. More income wouldn’t increase our costs. In Oregon (Green line) this same thing happens at ~350% of the FPL. But in California (Teal line) the annual price is an incredible $10k! If we earn more than 400% of the FPL, when the subsidy is eliminated our costs increase by ~$4,000!

And this could occur with even $1 of additional income.

That would be a rude wake-up call if we weren’t paying attention to our income throughout the year. In States with high cost of insurance, or if we choose a plan that costs much more than the SLCSP, it would be fiscally responsible to keep income below 400% of the FPL if at all possible.

This isn’t to say that it is all nice and easy in the other 3 locations. These quotes are based on our ages today. Barring some advances in anti-aging, the cost of insurance will rise as we age.

The following graph shows the lowest cost Bronze plan and the Second Lowest Cost Silver Plan for Seattle, WA for the two of us for ages from 30/25 to 60/55. Barring any change in the law, above Age 50 the danger of the cliff increases significantly. If premiums rise faster than inflation, it could be even worse. But as long as we stay below 400% of the FPL, our premiums stay roughly the same regardless of our ages. Subsidies just increase over time.

During the course of the year, the US Treasury transfers our expected PTC directly to the insurance company. Any discrepancies are taken care of when we file our taxes the following year. If these advance payments were too large, we would pay a little more on our tax bill.

During the course of the year, the US Treasury transfers our expected PTC directly to the insurance company. Any discrepancies are taken care of when we file our taxes the following year. If these advance payments were too large, we would pay a little more on our tax bill.

If we fall off the Obamacare Subsidy Cliff, not only would we have to pay a massive increase in premiums ($4k in the California example), but we would also have to pay back all of those advance payments transferred to the insurance company.

In a totally different tone of voice this time, “Thanks Obama!”

Cost Sharing Subsidies

For households with income between 100% and 250% of the FPL, Silver tier plans come with additional Cost Sharing Reduction Subsidies (CSR subsidies.)

Normal Silver level plans are expected to cover about 70% of the total cost of care. With the CSR subsidies this is increased to as much as 94%, meaning deductibles, co-pays, and co-insurance will be reduced.

Most importantly, this shows up in reduced out of pocket limits. While this may be of limited value for households that don’t have a lot of medical needs, it can be the most valuable component of insurance for those that do.

Effectively, at incomes between 100% and 250% of the FPL, Silver plans can provide lower premiums and lower out of pocket maximums than even Gold or Platinum plans. Note that the out of pocket limits here are the legal limits; some plans could offer lower.

Effectively, at incomes between 100% and 250% of the FPL, Silver plans can provide lower premiums and lower out of pocket maximums than even Gold or Platinum plans. Note that the out of pocket limits here are the legal limits; some plans could offer lower.

Optimizing Obamacare in Early Retirement

Obamacare optimization is essentially income optimization. Too little income, and you may end up on Medicaid or uncovered. Too much income, and you face a potentially serious subsidy cliff.

The maximum Premium Tax Credits and Cost Reduction Sharing Subsidies are available with incomes between 1-2x of the FPL. Even up to 2.5x is still a great deal.

Here is the 2015 FPL table again. Keeping income below $40-$50k (or even $60k for the unmarried couples out there) shouldn’t be terribly difficult for early retirees. It would certainly be easier than while working. Spending more is possible as well; cash, any basis in a brokerage account, and Roth IRA contribution withdrawals aren’t considered income for purposes of the MAGI.

| FPL (2015) → Household size (↓) | 100% | 200% | 250% | 400% |

|---|---|---|---|---|

| 1 | $11,770 | $23,540 | $29,425 | $47,080 |

| 2 | $15,930 | $31,860 | $39,825 | $63,720 |

| 3 | $20,090 | $40,180 | $50,225 | $80,360 |

| 4 | $24,250 | $48,500 | $60,625 | $97,000 |

Of course, keeping income low for the sake of increased insurance subsidies might not be rational. It wouldn’t make sense to earn $100 fewer dollars to save $15 in insurance costs. But it may make perfect sense for households on the edge of the Subsidy Cliff or in years with high medical needs.

Being aware of income is critical!

Income Optimization Example

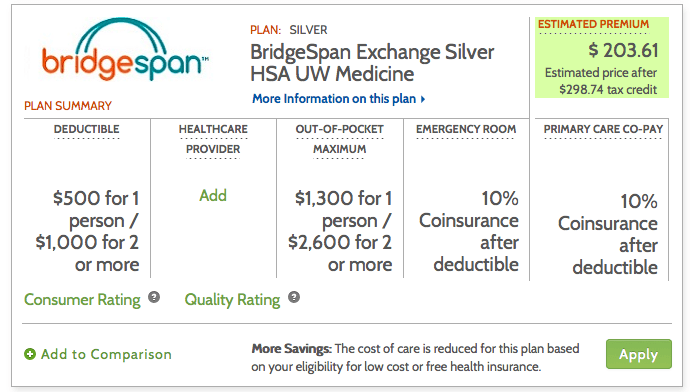

At 200% FPL we can get a Silver plan with 87% cost sharing for ~$200/month in Seattle, WA (and every other state) for all 3 of us. On this specific policy, out of pocket maximums are only $2.6k with deductibles of $500/person or $1,000/family. And it includes an HSA!

Using our 2014 tax return as a reference, there are challenges for us to stay below the 200% FPL threshold, even with the addition of a 3rd household member. Our choices are to earn less or take advantage of deductions.

Using our 2014 tax return as a reference, there are challenges for us to stay below the 200% FPL threshold, even with the addition of a 3rd household member. Our choices are to earn less or take advantage of deductions.

Total MAGI in 2014 was $96,968 (Line 37 + Line 8b on our 1040), far surpassing even the 400% FPL threshold. (See how MAGI is calculated here.)

By contributing to the max allowed to an HSA, I can reduce our MAGI by $6,650 while also saving tax free for future medical expenses. Win-win.

The Business Income (Line 12) could be added to a Traditional IRA, reducing MAGI by another $1,987. Or the Self-employment health insurance deduction (Line 29) would allow me to deduct the monthly premiums, which would also eliminate the full amount of Business Income.

At this point, I would also need to eliminate the $46,725 of Capital Gain income. This was optional income generated by Harvesting Capital Gains at the 0% tax rate, part of our plan to never pay taxes again. By harvesting $3k of capital losses instead (the maximum offset), our MAGI would be reduced by a total of $49,725.

This now brings our MAGI to $38,606, a couple thousand dollars below the 200% FPL level. We now have great heath insurance at a very reasonable price.

Conclusions

In all likelihood, an early retiree in the United States is going to purchase ACA (Obamacare) compliant Health Insurance on the Federal or a State Health Insurance Marketplace. Guaranteed access to insurance can help many cut the employment handcuffs.

The Premium Tax Credits are a direct function of income, ensuring families of a same size and income have the same cost of insurance, regardless of age, where they live, or health care needs. Just stay below that 400% of FPL subsidy cut-off. By optimizing our level of income we can maximize our health insurance benefits.

Tracking income is critical to ensuring that at a minimum we don’t hit the Subsidy Cliff, which can have severe financial repercussions. If you aren’t currently tracking income from all sources, Personal Capital is a great free tool for doing just that, automatically.

It is possible to maximize benefits by keeping MAGI between 1-2.5x FPL and choosing a Silver plan. There are obvious trade-offs between income optimization now vs future tax savings from Harvesting Capital Gains and Roth IRA Conversions. This will be explored in a future post (Coming soon: this post was originally research for that larger topic)

Great detailed write up about Omamacare, thank you for this!

Thanks Jim! I hope you like Part 2 even more

You piqued my interest Jeremy. I can’t wait for part 2!

No pressure :)

This is by far the most complicated series of trade offs I’ve worked through. Every time I think I may have a way of expressing it clearly, I find a flaw… still working through it

Just to add one more data point about the ACA and it’s quirks. I live in Alaska and the silver plan monthly premium for my wife and I is $1500 and the bronze plan premium is $850. The 400% of the FPL for Alaska is $82,000 so my maximum premium per month is $650. The price difference between silver and bronze is $650 which i receive in a subsidy. To I just end up paying $200/month with an AGI of $82,000. These numbers are all rounded but last year I paid $150/month and this year I am supposed to pay $179/month. It’s another quirk due to our high health care costs in Alaska that works to our benefits for the ACA subsidy.

Substantial difference!

Great article, trying to understand how this works, how do look at the plans and is there any agency to sit down with ask specific questions?

A bronze plan high deductible would be like having a cat policy?

I’ve looked at the ACA costs quite a bit too, for the purposes of understanding our future expenses. We’ve already discussed how every year we are going to have to do some optimization and planning to make sure that we stay in the right ranges. But – even if it is a hassle, I still think that in the end it makes ER a little bit more feasible than before. I appreciate your analysis of looking at it with age and how it changes – I hadn’t thought that far into the future yet!

The main thing that makes ER easier is probably the elimination of pre-existing conditions clauses. No longer does a person need to stay with a job just for insurance, or pay astronomical premiums to get coverage. There is a lot that could be done to improve the ACA, but one step at a time

If you are just a few dollars, few hundred dollars or a couple of thousands dollars, can you just donate to charity and be on the lower bracket? Rich people do this all the time on a bigger scale.

It’s great to have the number lay it all out there so you can literally decide which bracket you want to be in. Thank you for doing all the leg work.

My other concern is the GOP could come in and cancel out what Obama and Co. has done over the past 7 years. It might very well change the game for ealy retirees.

Charitable contributions are only deductible if you itemize your deductions, which many people won’t be doing around 400% of FPL.

at the 400%, according to the chart, it’s like $90K for a family of 4, don’t have to do the long way to deduct your property taxes, work expense (if you have a travel blog), etc.

Charitable deductions don’t count. See this for all that is included.

Great article. I am considering going on Obamacare this year now that I am retired. If the marketplace subsidy calculation was right, I can get a bronze plan for my family of 4 for about $350. Currently I pay about $598 per month for a high deductible plan.

Be sure to see if you qualify for the Silver plans with cost sharing reduction subsidies. See Travis’ comment below as an example

As a British resident of Japan, I am very glad I don’t have to deal with this :)

How do you like the healthcare system in Japan and the UK? I assume Japan is single payer?

When you see American politicians bashing the ACA on television, what do you think?

I agree! We have universal healthcare in Australia (called Medicare) which provides everybody with free (ish – sometimes there is a small gap between what is covered and what the doctor will charge) health care. Private health insurance is a completely open market, you cannot exclude or discriminate on the basis of pre-existing health conditions and premiums are reasonable. It’s not tied to your employment at all, so you’re free to move between jobs without fear of losing health care and you’re not stuck with the policy and provider your employer uses. Nobody goes bankrupt due to medical bills.

From what I understand of it, Obamacare is finally a positive step forward for the US to make things fairer and more accessible and reasonable. I can’t understand the negative rhetoric at all! (Well, I can, it’s just political point scoring).

Excellent post. You mention this in the post, but I would emphasize that the minimum MAGI threshold could actually be up to 133% of FPL (really, 138% of FPL, because of the income-calculation methodology imposed by the ACA), instead of 100% of FPL, if your state expanded Medicaid (as every state in this post’s examples did, so the charts are a bit misleading at the low end of the income scale, given that subsidies are really zero at income levels below 138% of FPL in each of those states).

This is important because it’s very unusual for there to be a tax cliff at the low end of the income scale; people are not used to thinking that too little income could ever be a problem from a tax-minimization perspective (and too little income is probably a more common “problem” among frugal early retirees than other population groups).

This ACA subsidy calculator put out by the Kaiser Foundation is very helpful: http://kff.org/interactive/subsidy-calculator/

Thanks brooklynguy. I linked to your comment from the main post to highlight the low side cliff. Great point

It’s especially important to avoid falling off the low side cliff if you’ve already purchased coverage on the marketplace in reliance on income assumptions projecting MAGI to be above the cutoff. If the end of December rolls around and you suddenly discover that your MAGI for the year turned out to be below the cutoff, then you won’t be getting the tax credits you were counting on when you purchased the coverage (and you can’t go back in time to instead receive any Medicaid coverage for which you thought you did not qualify but for which you now know you did in fact qualify).

For early retirees with Roth conversion pipelines or other ways of managing their reported income, this is pretty easy to control as long as you don’t fall asleep at the wheel.

You wrote: “If the end of December rolls around and you suddenly discover that your MAGI for the year turned out to be below the cutoff, then you won’t be getting the tax credits you were counting on…”

This could be a problem if you don’t take Advance Premium Tax Credits. But if you do take APTC (rather than just waiting until tax time to get PTC), and the marketplace estimated when you enrolled that your income would be between 100% and 400% of FPL, then if your income turns out to be under 100% FPL, the APTC that you received is not clawed back. You get treated the same as anyone whose income is “less than 133% FPL.” See Instructions for IRS Form 8962 Line 6, “Household income below 100% of the Federal poverty line.” https://www.irs.gov/instructions/i8962/ch02.html#d0e1088

FANTASTIC analysis and a wonderful illustration of how steep the cliff is.

I would, however, caution people about their fear of Medicaid. Aside from (possibly) suffering from the low income necessary and (possibly) from the associated stigma, it’s actually great insurance. It beats most private insurance for any pediatric issue, especially developmental. It’s accepted by nearly all academic medical centers. There are no billing hassles and you can go to the doctor or ED as much as you want with no or minimal co-pays. You may not be able to see a fancy private doctor, but those are fast disappearing and may don’t accept any insurance (and probably not ACA.) It’s better than most private insurance of any kind and it seems unfair that (most) fiscally responsible early retirees are ineligible. I would take it over nearly all the different private insurers I have had.

If all that’s keeping you from living on less is fear of Medicaid, make sure your state offers it and dive right in.

This is great, thanks for sharing this perspective. If that is what a single payer health system looks like, I’m all for it

I agree with Snowcanoyns comment, but wanted to add on to it

I work for a large non-profit healh center that has 15 sites (medical, dental, and behavioral health). We have doctor’s from Harvard and many other prestigious programs. The model is changing from a private practice to an employment model due to many factors including reimbursement changes (and has been changing for a while now).

There is still a stigma from both patients and some private providers, but medicaid covers most everything (and I agree it is really great coverage for kids).

Thanks Vawt. If you wouldn’t mind, what are your thoughts on the comments on this post:

https://gocurrycracker.com/spa-day-at-the-health-clinic/

I’ve definitely recommended the ACA as a way to get healthcare for some of my early retiree clients. Done right, they can basically get healthcare for free.

I have, however, heard some complaints as well – namely that there are a lot of medical facilities that don’t want to accept patients because they are on the ACA. I understand if they’re on a Platinum plan because of the loads of paperwork and delay in getting paid, but not if they’re on a Bronze or Silver plan – both of which are HDHPs.

Also dig the Bronze because of the HSA. Hello backdoor additional retirement plan.

I wonder how many medical facilities are operated by people who politically oppose the ACA, and if that is a factor.

The HSAs are awesome. And you don’t even need earned income to contribute! It almost makes we wish we had insurance so I could have one again

I’d like to assume the best and go the road of ignorance of how ACA paperwork handling occurs, but I am deep in the heart of Texas, so politics may well play a role (though one client in very blue California reported a similar problem).

BTW, good analysis about the 100% floor. Seems similar to Habitat for Humanity problems.

Hi Jason, I’m surprised at your comment that some medical facilities don’t take ACA patients. When you buy an ACA plan, it is from a private insurance company. I don’t think the medical facilities know whether you bought your (example) Blue Cross plan from the exchange or from Blue Cross directly. I have one of the ACA plans and my insurance card doesn’t look any different. Maybe there’s something I don’t know?

I think what happened is that these people were trying to determine who would take ACA a priori so were calling around to check to see if it was accepted. I didn’t get into deep details, to be honest.

Yes, you can tell if something is an exchange plan (at least in California). I think from a combination of the product name and billing information.

In fact, in early 2014 I recall many patients being referred out to specialists and being denied after already being in an exam room once that office realized they had a covered california (exchange) plan! It was a mess, but eventually most of the specialists got higher reimbursement contracts and signed on.

Excellent summary of the ACA subsidies and potential pitfalls. To echo what brooklynguy said, there’s also a very important and critical subsidy cliff at the lower edge of the ACA too. In the 36 states that didn’t expand Medicaid, you get nothing under 100% of the FPL. No subsidies, no medicaid, just bare lack of coverage unless you can afford the unsubsidized policies (that might exceed 50% of your income).

It’s a silly subsidy cliff, but one that my mother in law got caught in last year. Just under 100% of the FPL, not working, drawing only the husband’s SS and the MIL isn’t quite 65 yet. So health insurance is expensive, but there’s no money to cover it.

From my own analysis, I’ve determined the 100%-200% of FPL range of income is the sweet spot where you still get the “gold plated silver plans” with 87% to 94% cost sharing. We’re personally hoping to stick right around the 199-200% FPL range unless it makes sense to increase our income now (while healthy) in order to front load our Roths through the conversion ladder.

I’m interested to see your upcoming analysis of the trade offs of low income now to maximize subsidies versus tax gain harvesting/Roth IRA conversion front-loading. It’s an issue we’ll be tackling since we have 50+ years to optimize our income stream, and I bet making the right choice could save tens of thousands or possibly $100k+ in taxes/subsidies over our lifetimes.

Justin, very good point. If I’m not mistaken, though, 30 states *have* expanded Medicaid. Full list here: http://kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/

Sorry, you’re right. 19 states haven’t expanded medicaid. Since I’m in one of the non-medicaid expansion states, it’s a huge deal here for those near the 100% of FPL line.

You also have State income taxes on the Roth IRA conversions? Although with a 5-person household you are probably still seeing some low effective tax rates

It’s a bum deal for the States that didn’t expand Medicaid for people that fall in the gap. It’s pretty stupid considering the state ends up paying in the end for the care for the uninsured anyway

Yes, we have a 5.x% state marginal tax rate on Roth IRA conversions over $15000. Unfortunately, North Carolina ditched the concept of personal exemptions so having 5 or 15 or 5000 kids doesn’t matter. :(

They overhauled the tax code a couple years ago to give a tax cut to high earners and pretty much F’ed all the families. Fortunately we’re not hurting for cash. :)

For a $40,000 roth conversion, we’ll owe around $1400 in state taxes. I budgeted $1000/yr for taxes so not too far off, and there’s a good chance the tax code will be overhauled again in my lifetime.

This is a great analysis! Our current employer health insurance is insanely good and cheap and covers everything, so insurance is one of the things that makes me nervous about planning early retirement. Also, if you actually earn the income you mention, couldn’t you also get the “earned income tax credit”?

EITC isn’t available to anyone whose investment income is more than $3400, for 2015.

https://www.irs.gov/Credits-&-Deductions/Individuals/Earned-Income-Tax-Credit/EITC-Income-Limits-Maximum-Credit-Amounts-Next-Year

Although I don’t know CC’s finances, it’s probably the case that many early retirees are going to be pulling in more than that just from dividends.

Great analysis. My experience with the ACA so far has been helping my mom (age 62) get set up on a plan. She was originally going to get a Bronze plan, but after showing her how the cost sharing subsidies worked with the Silver plan, she went with that one. Since her income is low (just working part-time as something to do), we were able to get her a “Beyond Platinum” plan for under $2/mo.

The combination of PTCs and CSR subsidies is incredible. Nice find for your Mom

I note that your strategy of tax gain harvesting (selling when LTCG tax rate is 0% and rebuying to essentially raise your basis at no cost) now must be re-examined in light of that cliff.

However, I would point out that not only do you have to think about not doing as much because it might put you over into the realm where you lose all subsidy, but there is an implicit 13%-15%ish “tax” on doing this even if you aren’t going to reach 400% FPL. So in effect, what you expected would be 0% capital gain tax rate does become taxed at something close to 15%.

I think this also has an impact on whether to do gradual Roth conversions (pipeline) in early retirement years. It would be great to stuff a Roth by converting trad IRA in chunks and take advantage of paying 0% or 10% or tax rate in years of low income. But Roth conversions (like tax gain harvesting) are considered as income for ACA MAGI. So what formerly might have been a “tax-free” conversion is now effectively further taxed by virtue of APTC or PTC being reduced as your income grows — again, that effective 15% tax.

Are people going to stop doing Roth pipeline conversions and wait until after Medicare kicks in before shunting money into Roth IRA? Or will they do extremely small Roth conversions taxed at 0% and just accept that they’re locking in a 15% effective tax on the amounts?

This post is the foundation upon which I can build the tax analysis of Harvesting CGs and doing Roth conversions. I’m mostly done, and hope to publish it soon

In many cases, it isn’t nearly as bad as you allude to. In other cases, it is much worse.

Stay tuned

+1 for Medicaid. In our state it pays 100% of everything with no copays. When I quit my job in June the biggest thing I was worried about was how to get health insurance for my family. We tried to sign up for ACA, but they told us our income was too LOW. I told them the truth, that we have investments and savings and a little rental income, but the guy was like, “What is your income? How much do you make every month?” Based on that they signed us up for Medicaid. Basically, it’s the same as the full coverage insurance we were getting through my former employer, just better, because we pay absolutely nothing. It’s surreal but true…

Yup. Unless one has a highly remunerative job and a Cadillac plan, work often just doesn’t pay. It has not been lost on me that Cadillac plans for high earners are going away, but Medicaid for everyone from early retirees to the chronically lazy can have the best and cheapest plan. It amazes me that workers don’t rise up….

Interesting Snowcanyon and Shane…I didn’t think about the Medicaid option but would like to know more about it. Do either of you know if there is a resource to find out what the Medicaid service / coverage is like in various states? Thanks!

Sorry, I don’t know of any comprehensive resource where you can find information on Medicaid in various states, but I’m sure you could easily look up what Medicaid benefits are available in your state or any other states you may be considering moving to.

This shows how disgusting the US fascist system is. You have other choices you didn’t cover which are essentially refusing to be part of this bs: 1. don’t pay. Young people, healthy people and those who follow alternative health practices don’t need it. What happens if you don’t pay? 2. use a health sharing plan–there are three of them that I know about–and 3. get out of Dodge and live where you don’t have to pay.

Frankly, we live in a world of the brainwashed who believe the nonsense that “modern medicine” is sound and worth the cost and that gov’t can save us. Both are false. We should all act accordingly.

What about vaccines?

Oh man, way to pull the pin on the grenade GCC! Brace yourself!

Oh, and I like to throw this at the anti-science crowd: https://en.wikipedia.org/wiki/Life_expectancy#Variation_over_time

Completely amazing if you ask me. Go science!

Don’t need them because you can use your free will to not be born at all.

You mean the modern medicine where the doctors fixed my broken wrist? Or the modern medicine who reversed my moms stroke with clot busting drugs when I thought she was going to die? Or the mothers march of dimes for polio back in the day and the vaccinations that reduced the risk of ending up in an iron lung? Ya, it’s a bit of a scam isn’t it???

“Or the Self-employment health insurance deduction (Line 29) would allow me to deduct the monthly premiums, which would also eliminate the full amount of Business Income.”

If you choose to go this route, you should be aware of this hilarious loop in the tax code:

http://thefinancebuff.com/irs-guidance-on-circular-reference-in-obamacare-premium-subsidy-and-deduction.html

The gory details of how to do the SEHI iterative calculation and the simplified version (which is less optimal) are now in IRS Publ 974, pages 31-end.

It’s quite challenging, but does allow part of your SE income to get devoted to your portion of monthly premiums.

The examples given in the IRS note “Rev Proc 2014-41” are also worth looking at, as they are at least a little easier to follow (although they use earlier year cutoffs for FPL that make things a little tricky to follow).

You just know that an ACA or IRS Intern had their Excel spreadsheet report circular reference errors all over the place, but didn’t know how to fix it. Fortunately the Goal Seek function solves this every time

I wanted to love Obamacare I really did, but my experience with it was pretty terrible. It was easy enough to sign up by telephone. The CA exchange website was too glitchy to mess with. But the real kicker was when the CA exchange decided to cancel our coverage without warning or notice after insuring us for the previous 6 months. One day I got a check in the mail for $700- the amount of our premium- from the insurance company. No note, just the check. Cool! Free money! When I called the insurance company to ask why they sent it they said the CA exchange had cancelled our coverage. So I called the exchange and they had no idea why. It took almost the entire month to straighten it out and finally on December 29th we’re told they’ve fixed it, would we like to pay $700 for retroactive coverage that we didn’t use? No thanks, I said and our coverage started January 1st. I looked around online and turns out a lot of people got randomly cancelled without notice, some of them now on the hook for $1000s in medical care.

On a positive note (sort of), the exchange botched our tax forms and the IRS gave us back $3000 too much, but since it was the exchange’s fault we didn’t have to pay it back. I’m hoping the glitches get fixed before I have to be on Obamacare again. It’s a far cry from universal healthcare.

What a mess. Thanks for sharing your experience with the sign-up. We had some really weird letters from our insurance company around the transition to the ACA, and it was all written as doom and gloom.

I really like the idea and I’m hoping that when I need it in a few more years it’s improved. I’m sure Medicare didn’t run smoothly initially either.

Thanks! Grade A Stuff here. I’m glad you started posting some very detailed guides instead of just net worth updates like everyone else.

Thanks Ryan. I hope to do more detailed stuff in the future

What a timely post as we are about to start a mini-retirement in 2016. It looks like we need to stay below 250% FPL income. Our child may be eligible for free healthcare in Oregon but it might be easier to just be all in one plan. Simpler and less paperwork.

Were we in Seattle, GCCjr would most likely be on Medicaid as well. The WA state exchange didn’t even give us the option for him to be on the same plan, and would enroll him in Medicaid automatically

We’re on Obamacare now because of the nature of my work. We’re fortunate/unfortunate to be on the completely unsubsidized version.

In retirement, I’ll live off of proceeds from stock sales. Long term capital gains don’t count as income, do they? If this is correct, then we’ll be on Medicaid. It seems strange and not right, but unless we buy rental properties or the blog income increases tenfold, I have no other choice.

For the purposes of the ACA version of the MAGI, basically everything is income.

It’s Line 37 on your 1040 plus some stuff added back in.

But your basis is not income. With specific share stock sales you can tune the amount of gain vs basis

So well-timed for us! We’ve been crunching a lot of different scenarios on budget and ACA coverage, and have basically concluded that we’re best off reverse engineering our retirement budgets around the ACA subsidy cliff. (And, I admit, we’re also toying with trying to get into the low, low “super silver” bracket — which would mean paying no tax and getting super cheap 97% coverage insurance. This would be a double bonus, if we can swing it, because our state has above average premiums. Fun.) Thanks for talking about this — more FIRE bloggers need to be doing the same, or they’re missing a crucial piece of budget and planning info.

This is such a balancing act and if you are $1 over the limit, you lose a major subsidy. Combine this with doing a Roth conversion and I can tell that the spreadsheets will be burning up toward the end of the year. I really like the ACA, but it has not made life simpler. However, I think one can either bellyache about the rules or one can learn how the rules work and play within them.

In response to wijwij being concerned about not getting the 0% tax on the Roth conversion. I think there is a middle ground which is to be paying less than 15% but more than 0%. For example, I’ve worked it out that I’m paying about 8% on the amount I’m converting this year. The way I look at it is that I know I’m never going to be in that low of a tax bracket. (FI but not necessarily all that frugal.) I need to move a bunch of money out of IRAs into Roths mainly because the RMDs are going to kill me later. So paying a modest tax now rather than at least twice as much later seems to be a pretty good deal. The balancing act is to make sure my conversion amount which is counted in MAGI is still under the ACA cutoff. My head hurts…

From what little I could find, it appears that 401k to Roth IRA rollovers do not apply to MAGI – does that sound right to you? Most our money will by tied up in our 401ks (and HSAs and Roth IRAs and a little in 529s) – our taxable investments are tiny so our MAGI will be quite low – and we have 1 kid with several more on the way (IVF embryos), raising the FPL level. Anyway, my point is that even reaching 100% of FPL completely unachievable for us – actually 138% in our state. So we will definitely be on Medicaid. I would think this would be a more common situation for most early retirees than needing to reduce income – there are just so many tax shelters…

Traditional 401k to Roth IRA Conversions are definitely part of MAGI. Line 15b of the 1040, IRA distributions

I ER’d last year and went on Medicaid. UHC Medicaid Managed Care plan. All my doctors from the work plan are on this plan, but without the co-pays, and other expenses. Three Rx’s for $1 each, not bad.

New York is starting a program in 2016 for $20 a month for 150-200 FPL, and $0 a month for 138-150 FPL. The $0 a month plan has no co-pays! Very sweet.

Also NY does not permit age ratings for insurance premiums, so the cliff does not steepen with age.

Those are some sweet insurance and healthcare prices

The premiums for young people must be higher than for similar aged people in other states?

“people are charged the same health insurance premiums regardless of age, sex, health status or occupation.”

http://www.healthcarereform.ny.gov/summary/

The young subsidize the old to a greater degree in NY than elsewhere.

This is the kind of stuff the anti ObamaCare crowd will have a field day with. Wait till someone sends Shaun Hannity and Fox News a link to this blog thread. I can see it now. “Early Retirees with seven figure net worth quitting jobs and scamming ObamaCare system”

Yeah, maybe. But there is already so much in this world to feel anger and hatred towards, I’m sure a small blog would only generate a small amount of mock outrage

Or maybe a few people will read a few posts around here, discover that there is another way to live, and move on towards a better life

Feel free to send Mr. Hannity a link

Sounds like you might be thinking I took a negative shot at your blog. That is not the case. I early retired and a key factor in that decision was because the ACA removed the preexisting condition screen from health insurance policies, not so much the subsidies, although I will take advantage of the subsidy too.

My point was, I can see how the anti Obama Care crowd could lock onto the fact those with high net worth can qualify for subsidies, just by managing to keep their “income” reported on their tax returns low. While I believe there is little chance the ACA will ever be overturned no matter who is in the White House or Congress, I believe it is realistic to expect the program to be “improved” and “tweaked” over time. One those tweaks could very well be subjecting qualification for subsides to a “means test” where net worth is a factor too, not just income.

Sorry Dave, my comment was meant in good humor

I agree. A means test / asset test could be applied in the future.

I hope that one of the tweaks focuses on reducing the cost and cost transparency of healthcare itself, which in turn will reduce the cost of insurance and subsidies.

Great post and great detail that I think is great for the FI community. My hesitation comes from anything where you need to earn less money to be helped by the government. This was a couple years ago but just getting a high deductible insurance plan was in the $300 range is this something that you have come across for non-aca care?

This isn’t a case of earning less. It is a choice of pay taxes now or later, and how much. It is no different than choosing to do a Roth IRA conversion post-retirement, and choosing the $ amount such that it is taxed at the 0% or 10% marginal rate, and not 25%

While working and accumulating, there is almost never a case where earning less is beneficial unless we are talking about a few hundred dollars to avoid the 400% subsidy cliff. Otherwise, sure you’ll pay more tax, but that tax is never 100%. More money is more money

What do you mean about an HDHP plan for non-ACA?

In this example, you are correct in determining if taking out more or less money regarding tax benefits. I’m just in the group that would prefer to not use a government program if at all possible, but it certainly seems mandatory from what I have seen.

I thought there would be health coverage not tied to the ACA at a reasonable rate. I could have still been looking at ACA rates and not realized it though.

You are required by law to participate

I believe you are just required to show you have coverage. If your income is too high to qualify for any subsidies you can buy directly from the insurance company and not go through the ACA Marketplace.

https://www.healthcare.gov/apply-and-enroll/income-too-high-for-tax-credit/

Yes, by participate I just mean you have to have insurance. But all health insurance sold in the US has to meet the Minimum Essential Coverage requirements, and the unsubsidized prices will be the same if you buy the same plan from the marketplace or directly from the insurance company. You may be able to get some pricing advantage shopping off the marketplace in some cases, but you won’t be able to buy a catastrophic only policy such as we had before the ACA.

Jeremy,

We too are considering a variety of locations for our ER. Do you have a link to where you found the differences in premium prices by state? Also, we are thinking of living in one part of the country for part of the year (for mountain environment) and another for the other portion (to be near family). Do you have any ideas on using a geographical arbitrage strategy or do you know if you have to purchase in state where you have primary residence?

Thanks in advance for any info/insights you can offer.

EE

I just used healthcare.gov and quoted policies on the respective marketplaces. It was a big hassle. This link also had some relative pricing between states from a few years ago.

I’m not sure how splitting time between states would impact things. I believe you would be required to get a policy at your legal residence. Please let me know if you figure it out!

Thanks for the link and doing all the leg work behind this thorough post. I work in healthcare (physical therapist) and other than my general desire for more free time, dealing with all the unnecessary complexity of our shitty system is the biggest driver for me to want to retire early from my otherwise rewarding job. It is a bit depressing to think that with the ACA that my biggest headache in my working life will be my biggest headache in ER figuring this all out every year until (if) the dust ever settles. I guess at least it is much better than having no system as we had before.

Thanks again!

Thank you SO much for writing this post! Medical care has been one of the greatest mysteries for me when thinking about how to retire early. I had absolutely NO idea what it would cost to get insurance outside of a job. Now much of the mystery is gone and I feel a lot better. I’ll have to re-read this a few times just to wrap my head around it, but I’m sure with your way of laying things out simply, I’ll get it. I just hope ACA gets to stick around, with many improvements to come!

Jeremy, thanks so much for pulling this data together in a cohesive and understandable fashion.

If the ACA was not in place which included the removal of the preexisting conditions clause, there is no way we would have been been able to consider ER due to health insurance funding. I feel managing your income during the year is a small price to pay in order to track your subsidy eligibility and make sure you don’t go over the cliff. $10.00 could be a thousands of dollars mistake.

I understand the Roth conversions will impact the MAGI but withdrawals from a funded Roth IRA will not? If this is the case, it may be an option to withdraw from 401k’s and tIRA’s up to a certain FPL level and then use the existing ROTH fund withdrawals as a supplemental income since it won’t impact the MAGI bottom line?

Savings does not contribute to MAGI.

So you can spend cash, Roth IRA distributions (Contributions only before Age 59.5), and any basis in stock held in a taxable account.

Jeremy,

Thanks for the great Obamacare post. As a number cruncher by trade I am thoroughly impressed by your analyses. I am diabetic and am glad to see the elimination of pre-existing condition restrictions under Obamacare, though we were planning to self-insure in our own fast approaching ER as perpetual travelers. Your analysis has given us something to think about relative to potentially maintaining insurance if we can manage income to allow for a subsidy.

Thanks TF, I’ve spent way too much time in my life using Excel.

I’m currently self-insured since health care prices have been low and predictable. This may change. I haven’t seen an ACA policy that provides non-emergency coverage outside the US, so I’ve been looking at low cost expat policies and just haven’t made a decision yet.

Nice post overall. I would caution you against making HSA contributions with the example plan you describe. Remember that to qualify for HSA contributions, you need to have valid HDHP coverage, which means the plan must have a minimum deductible of $1,300 for an individual policy or $2,600 for a family plan.

The plan you show above advertises a deductible of $500 for an individual or $1,000 for a family, well below the HSA eligibility limit. Perhaps the plan qualifies as an HDHP for people who are over 250% of the poverty level and thus don’t have cost sharing subsidies applied to their plan?

I’m not aware of any IRS guidance that would suggest that you can determine whether a plan is an HDHP or not based on its pre-subsidy deductible. I would love to see someone in authority issue a ruling on that question.

That is an excellent point. More research required

You can’t contribute to an HSA if your plan has cost-sharing reductions that bring the deductible down below the required amounts. So it’s technically possible to be participating in a Silver plan that has “HSA” in its title, yet not be able to make contributions because the CSR mean the plan is not HSA compatible. You have the choice to not take the CSR when you sign up, but then you have higher deductible.

>A8: If an issuer seeks to offer a QHP designed to be eligible for pairing with an HSA in 2014, the issuer must comply with the cost-sharing reduction standards described in 45 CFR 156 subpart E. CMS recognizes that certain plan variations of a QHP may require a low or zero deductible, or that certain services be exempt from the deductible. This may result in the plan variation not meeting IRS standards for an HDHP and therefore not being eligible to be offered in conjunction with an HSA. We recommend that issuers and Marketplaces educate consumers about this issue, both during open enrollment and when an individual has a change in eligibility for cost-sharing reductions. An individual who would not be eligible for the tax advantages of an HSA because the plan variation to which he or she would be assigned does not qualify as an HDHP may purchase the plan without cost-sharing reductions.

Source:

http://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/Downloads/marketplace-faq-5-14-2013.pdf

Sorry to be late discovering this thread, but it’s this procrastinator’s tax-planning season and I’ve been desperately trying to track down advice/truth about my situation – which I have found mentioned NOWHERE on the Web (and I’ve Google’d mucho and I am also a Bogleheads subscriber [nada there]). So please help/advise, if possible:

Jan through July 2015, my Mrs. and I were ACA Silver with a sizable subsidy. In August, we both became Medicare eligible and began that coverage.

Do 7 months of ACA subsidies again restrict our possible Roth conversions as a full year of subsidies did in 2014?

Put another way: If in the next week or so we do Roth conversions to the top of the 10% bracket and blow well past my “estimate” for this year’s MAGI (on which ACA subsidies for us were based), will we be penalized?

If yes, a penalty, what would be the maximum?

Thanks for any help or advice,

Chaz

Chaz — Depends on if you got any APTC (or were waiting until tax time to just claim PTC). If you did get APTC, the answer to your question is found in Instructions for Form 8962 on page 11, Table 5 Repayment limit. If your *actual* FPL percent for the year is less than 200% FPL, you would have to repay but never more than $600; if between 200% and 300% FPL, never more than $1500; if between 300% and 400% FPL, never more than $2500. If you were above 400% FPL, there is no limitation to the repayment (meaning you pay exactly what you “should” have paid based on your income). See the comparison of lines 27 and 28 on Form 8962.

Regarding your “7 months” issue — the form 8962 has you fill out a separate row for each month, so you would only fill out 7 rows for the months you were getting APTC. The form essentially has you calculate a reconciliation for those months only — you don’t pay for the other months. On the other hand, the “repayment limitation” isn’t pro-rated. If $600 is the repayment limitation, it doesn’t become 7/12 * $600. But remember, the limitation figure is *not* necessarily what you need to repay. What you need to repay depends on the calculations in the form. It’s the lesser of line 27 or 28 that gets used on line 29.

Thank you, wijwij. Your kind replies are very helpful (although, sigh, not what I was hoping, of course).

I am seeing that 7 months of APTC (yes, we did do the advance-pay credits) will prevent us from doing any Roth conversions – other than what we did last year in order not to fall into Medicaid territory (which means no healthcare coverage in our “progressive” state).

Thanks again,

Chaz

This is my third year on ACA and I also appreciate the data and analysis you’ve provided here. I am a single father with multiple chronic disorders trying to put my daughter through college by taking funds from my traditional IRA and paying the 10% penalty on top of regular taxes.

While I am grateful for the financial benefit, my experience with ACA on every level has been horrific.

My subsidies (as well as my coverage) were cancelled in April of last year without notice. The IRS determined that the “proof of income” I provided was wrong (I had provided actual statements showing my withdrawals from my IRA) and instead used previous year’s tax returns (where I had been forced to take a lump sum retirement plan disbursement). Because I had no coverage for a month, I had to face $7K in uninsured medical coverage. My insurer insisted that to re-start my coverage, I would also have to zero my already fully paid deductible and out-of-pocket expenses (more than $2K). My State’s Insurance Commissioner would not reply to my complaints (virtually all Insurance Commissioners come from the insurance industry). I started with CMS in Washington and eventually went all the way to our Secretary of HHS. It took me months but eventually it was resolved with a net loss of a few thousand dollars and I am grateful for the help of HHS and CMS personnel.

The number of doctors and facilities that do not accept EPO plans is enormous and growing. Many of the doctors I must see are over an hour’s drive away.

The insurance “summary” documents do not provide full disclosure of every detail of their policies and they are not required to provide complete details (its called “buying a pig in a poke”). While receiving monthly injections of a biologic drug, my insurer (without any documentation) would not pay for the “labor” for the injection ($220/month). Because it wasn’t covered, its not included in deductible or out-of-pocket maximum.

Over the past 3 years I’ve received rebates from my insurance carrier due to the MLR or 80/20 rule within ACA. In 2014 carriers sent out over $469 million in rebates according to CMS. Sounds great, except for the fact that they are using American’s money to make more money (they aren’t required to pay interest on these overcharges). And what’s funny is every year my premiums, deductibles and out-of-pocket maximums INCREASE! In some States they have asked for 85% increases in premiums!

Then there is “balanced billing”. This is where a provider orders lab tests performed in their offices, but they are sent to a third party. That third party may be out-of-network! The provider posts signs all over their walls that YOU are responsible for any bills not covered by your carrier. This year’s plan summary from my carrier states that they won’t be responsible for balanced billing. Last year I was hit with over $10,000 in balanced billing. How is a patient supposed to know what third party is going to be used, let alone whether they accept ACA or not? My doctor charged me for surgery in his facility but I’m responsible for the anesthesiologist who doesn’t accept ACA? $960 in denied claims.

ACA required minimum coverage – My daughter had a head injury last Fall. Taken to the nearest trauma center, she received a CAT scan as part of her treatment. According to ACA “You cannot be penalized for going out-of-network or for not having prior authorization”. Not according to my carrier! NO out-of-network coverage for emergency treatment. Guess the ambulance personnel should ask where the nearest ACA covered emergency room is! $3,450 claim declined.

The truth is that ACA has benefited health care insurers tremendously. We, as Americans have never had a MANDATE (with penalties) to purchase anything on this scale before. For those truly in poverty, they may receive minimum essential coverage. However, it will not be affordable. With my Premiums (they don’t count towards deductible nor out-of-pocket maximum) and deductible I’m paying almost $6,000 per year before my carrier spends a penny! How many people living at the poverty level can afford this? For that matter, how many at the poverty level can afford the more than $2,000 penalty?

In the end, I believe the ACA law will be effective in getting all Americans covered by insurance. However, I also believe it will significantly increase the cost of healthcare and pad the pockets of insurance carriers. I also believe it has and will continue to diminish the quality and accessibility of healthcare to all Americans. Now United Healthcare, the nation’s largest healthcare insurer has announced they plan to abandon most of the exchanges in 2017.

Financially, ACA represents a savings for me. I would gladly give it up so that someone can truly REDUCE the cost of healthcare without diminishing the qualify of service. Not a political statement, just real-world experience that you should consider when planning early retirement using ACA.

If you are concerned about this, then go with a group model HMO like Kaiser or Group Health. You will pay more per month (it is rare that Kaiser is the lowest or second lowest cost provider on the exchange) but with Kaiser the doctors are the insurance company. This can be good or bad.

Has anybody come up with a strategy if only one of the spouse’s is retiring early?

It seems that as long as the working spouse’s plan is deemed affordable (less than 9.5% of MAGI), and the employer allows adding family members to the plan, the household as a whole is disqualified from any subsidies. This is true even if adding a family member costs in excess of 9.5% of MAGI.

Therefore, it might be worth it to sign up for a non-renewable annual plan; for a fraction of the cost.

If anything major happens during the year, one could switch to “Obamacare” the following year, and will have the pre-existing conditions covered that would otherwise be excluded. If nothing major happens, sign up for another non-renewable annual plan.

Non-renewable plans normally trigger the health care penalty, EXCEPT if enrolling to a compliant plan would cost more than 8.13% of MAGI.

Any thoughts?

I’ve already made the tax decisions for the year and it looks like I fell off the cliff. But I think the subsidies would not have helped me because I took the cheapest bronze plan and I only started in May (unless I am missing something) or the cliff doesn’t matter for single pleople?

As complicated as it is, you still have to evaluate whether maximizing subsidies this year might get you in trouble in the following years if you do so leaving on the table some gain harvesting or even IRA/Roth conversions? You could fall into a local optimum… Man, retirement is a lot of work! May be I should just get a job (kidding)

Everybody with MAGI below 400% FPL gets a subsidy, even single people with the cheapest Bronze plan.

The next post evaluates if there is a local optimum.

I didn’t understand it all but my income is above the 400% of FPL. I thought the tax sweet spot was right under the 15% bracket so I tuned income to around 51k (single filing, includnig exemption, deduction and maxing out HSA) and since 4*FPL is 44k, I went over. But since I took the bronze plan (cheaper) and only enrolled for a few months my mistake was not as bad. I even made a newbie mistake assuming I was going to be able to deduct donations, not realizing I cannot do that because I will take a standard deduction this year… so I will be in the 25% bracket. I think my tax bill will be around 10% of income, lower than when I worked but still sky-high compared to yours. I have a lot of learning to do.

Yes! I found the next post in the archives. I am reading your blog from the beginning and this was the first post I read in the new format which does nto include links to the previous and next post.

Thank you

10% effective tax rate is great for the first year. You’ll do even better next year.

Thanks for the heads up about the missing previous/next post links. I dug through the code and added these links to the top and bottom of each post.

Thank you!

Thanks for the post. Can you expand (provide actual numbers and calculations) for the statement below?

“By harvesting $3k of capital losses instead (the maximum offset), our MAGI would be reduced by a total of $49,725.”

I was assuming (wrongly?) that the $3K of capital losses would simply reduce the capital gains by $3K and thus reducing MAGI by $3K.

Thanks.

Capital losses offset capital gains, yes. But if you have more capital losses than gains, you can use up to $3k to offset earned income (if you have more than $3k, that is carried forward.)

When he says “I would also need to eliminate the $46,725 of Capital Gain income. This was optional income” GCC is implying that he would NOT realize those $46,725 in long term capital gains at all.

Thanks wijwij and GCC.

With ACA insurance, is there a problem with earning no income in a particular month, or multiple months, although you still show income between 100 and 400% of FPL? Does this force you to take Medicaid instead?

This is normal for a lot of people – quarterly dividends, seasonal work, etc… annual income is what ultimately matters, but big life changes are supposed to be reported to the exchange – a permanent or indeterminate period without income could push you onto Medicaid.

Great summary and helpful even a few years later! Perhaps you can answer or point to a more recent source. If I exit the workforce and am living largely on cash savings for the first few years (read no w-2 and minimal 1099’s) how would this be handled on a MAGI for premium/subsidy? Would I want to harvest small amounts of capital gains for spending in future years to smooth this out? I am trying to map this out because my employer changed my retiree medical eligibility in my 11th hour!

Cash is just cash, not income. So it is $0 of MAGI.

If your income is too low to qualify for ACA premium subsidies, then you either end up on Medicaid or (in states that haven’t expanded Medicaid) in no-man’s land (not eligible for anything.) You can realize gains to get your AGI up to 138% of FPL or so to insure you will get subsidies.

Can you provide an update with the recent changes to ACA?

Which recent changes?

ACA enhancements from the ARP discussed here.