Now that is a turbocharger!

I’m not going to lie, being financially independent is nice. It enables choice and opportunity. We can choose to earn an income, or not. We can choose to remain in one location, or not. We can pretty much choose to do anything we want, when we want, and how we want.

In fact, I’m pretty sure there is only one thing better than being financially independent: Being financially independent SOONER!

How would you like to accelerate your savings, becoming financially independent years ahead of schedule? What if you could do this without saving even 1 extra dollar? Not one!

Let’s Turbocharge your Savings!

All you have to do is put every penny you can into tax-deductible accounts: A Traditional 401k, an HSA, a Traditional IRA. But what about the Roth 401k or Roth IRA? No! Not now, not ever. I’ll explain

IRS 101

First we need to understand a little about how money disappears from your paycheck in the form of income taxes. Yes, taxes are boring. So instead of reading those horrible IRS documents we are going to look at some pretty pictures with bright colors. Just like going to the museum

Let’s check out a Picasso, often simple, yet difficult to understand without the tour guide’s explanation.

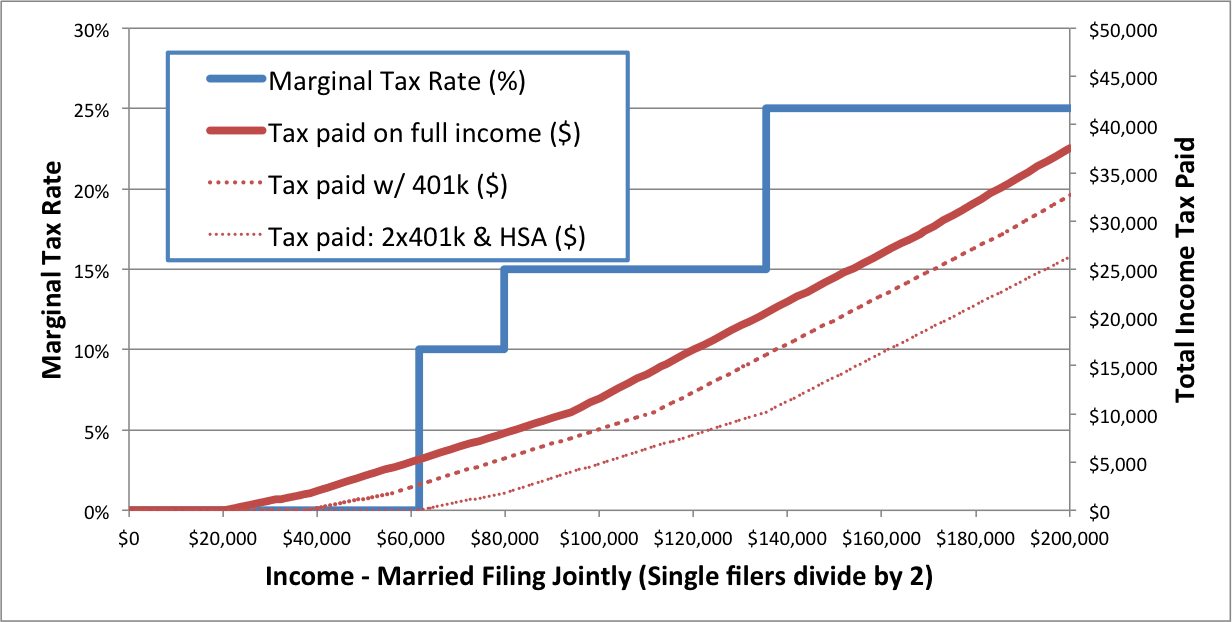

That pretty red line is the taxes paid in 1 year for different levels of earned income. See how the tax on the first $20,000 of income for a Married couple filing jointly is $0? As income increases to the right, the red line slopes upward representing more tax paid

Tax Curve by Picasso

The first ~$20k is taxed at 0%, the next ~$20k is taxed at 10%, the next ~$50k is taxed at 15%, and so on. The gradual increase in tax rate is known as marginal taxation, a fancy way of saying that the next dollar you earn is taxed more heavily than the previous dollar

At ~$200k of income, the 95th percentile of US families, the marginal rate (Blue line) is 28%. But the effective tax rate (Green line) is much lower. Even though the last dollar is taxed at 28%, the average tax rate on all dollars is less than 19%.

And that, in a nutshell, is the US Income Tax system for everybody with a job.

If you only remember a few things from the tour guide’s speech, remember this.

- A married couple doesn’t pay much tax on the first $40k of income

- 95% of income earners (<$200k/year) pay less than a 20% effective tax rate

If that isn’t clear, you can get a refund on the price of admission. Submit your refund request in the comments

Tax Deductible Savings

The government doesn’t want a lot of destitute senior citizens subsisting on cat food and refusing to turn on their AC during heat waves. Starving and dying people are bad press. It’s also bad for the economy, which probably concerns the politicians more.

For these reasons, the tax laws encourage saving and investing in the form of 401ks and IRAs

In 2014, an individual could save up to $17,500 in a 401k tax-free. A married couple with two workers could save 2x that amount.

Back to the pictures. Let’s check out a Seurat. It even has dots

Contributing to a 401k effectively shifts our tax curve. More dollars are taxed at 0%, resulting in less tax paid. For a married couple, when one of them contributes the maximum to a 401k, the first ~$40k of family income is now tax free. If both contribute the max, the first ~$55k is tax free

Other tax deferred accounts, such as an HSA, can shift the curve further, as can itemizing deductions for some people

Tax Curve by Seurat

The reduction in tax is substantial! Thousands of extra dollars are saved

More Free Money!

But it gets even better! Employers don’t want the IRS to have an exclusive on reducing the nation’s quantity of distressed Seniors. On average, US employers contribute 2.7% of salary to a 401k, but only if you contribute.

By contributing the maximum amount to a 401k, we can reduce our taxable income by $17,500 AND get a 2.7% tax free increase in pay. And this is just for saving, something we were going to do anyway

Three different working families, one at the median income level (50th percentile), another at the 75th percentile, and one more at the 90th percentile, all aspire for early retirement and have committed to saving 50% of their paychecks. This represents the majority of people surveyed expressing interest in pursuing Financial Independence. Below the median level, a focus on increasing income is also necessary

Before you get your knickers in a bunch, consider that many are already saving 50% or MORE

- We did it for 10 years

- Joe Udo of Retire by 40 does it

- Mr and Mrs Frugalwoods are doing it, and then some

- Jason Fieber of Dividend Mantra has done it for years

- Justin of Root of Good did it

- Mr Money Mustache did it, and continues to save more than 50% even after retirement

For each income level, let’s compare saving in a brokerage account vs. savings in a 401k. I promised pretty pictures…

Tax Advantages of the 401k by Van Gogh

The families that contribute to the 401k are able to save approximately 20% more! The higher the income, the better the immediate return by using a tax-deductible account

In a brokerage account, saving 50% of income it is possible to be financially independent in 16 years. Using a 401k, it is possible in 13 years! You just won back 3 years of your life!

Since it only takes 30 seconds to sign up for a 401k, that is like earning a quadrillion dollars an hour. What other activity has that kind of return?

Go ahead and do it now. I’ll wait

While you are at it, try a FREE 401k Health Check from Personal Capital

But… what about the Roth?

There are a few common myths about Roth 401k/IRA “advantages”:

- Tax wise, a Roth and Traditional IRA or 401k are basically the same thing

- Roths are good for the very young or very low income earners

- A Roth allows penalty free access to funds before Age 59.5

- A Roth is good if you expect taxes to rise or your post-retirement tax rate to be higher than today

But none of these hold up to close scrutiny

Think about it this way. When we invest $1 in an IRA, that dollar is the last dollar we earned. It is taxed at our highest marginal rate. But when we withdraw $1 from our IRA years from now, it is our First Dollar. As we saw in the pretty pictures earlier, the First Dollar is always taxed at 0%. Take the tax savings now, and Turbocharge Your Savings!

(Yes, as with any good rule (or law) there are exceptions. See why the Roth is last on our preferred list of investments when we discuss The Great Roth Controversy)

The Go Curry Cracker Way

What did we do during our working years? We Turbocharged our Savings by putting every penny we could into a 401k and HSA

As seen above in the Van Gogh picture, when saving a high percentage of income, it is inevitable that you also build savings in a taxable/brokerage account.

When a 401k and Brokerage account are combined with a powerful tax strategy and a small cash buffer, it is possible to become financially independent in the fastest possible time with the largest possible nest egg.

In this way, we built up passive income streams from dividends and interest, in our 401k and Brokerage accounts, both.

Conclusions

Want to become Financially Independent in record time?

Maximize your contributions to pre-tax accounts like the 401k, Traditional IRA, and HSA. Taking advantage of all available tax reductions will accelerate your success. This is how you Turbocharge Your Savings!

See All of Your Accounts in One Place

Track your net worth, asset allocation, and portfolio performance with free financial tools from Personal Capital

Roths sound so appealing to folks who haven’t done the tax math.

For people who are currently high paid and will live a frugal (and low tax) retirement, tax-deferred savings is a no-brainer. But even folks who will spend a lot in retirement almost always will benefit from pre-tax savings too.

The only benefit the Roth has in my mind is psychological. If the only way you can get “cousin Larry” to save for retirement is to promise him he can pull out his contributions at any time… then Roth it is! But it’s a high price to pay for the comfort of funds access. And in the long run, cousin Larry may well take advantage of the funds access to buy a jetski… :-) Thus negating the saving in the first place.

(sorry to all you Larrys out there…)

It sounds like you have been hanging out with my cousin Larry :)

I think the access to funds restrictions are typically overblown on the 401k and Traditional IRA

Let’s be generous and assume Larry already has 2 or 3 jetskis, and because he was laid off just needs some money to get him through a tough time. He could sell a jetski, but we both know that isn’t going to happen

Worst case, he pays a 10% early withdrawal penalty, which is much nicer than paying 25% tax years earlier

“Worst case, he pays a 10% early withdrawal penalty, which is much nicer than paying 25% tax years earlier”

I find this statement intriguing. Would this still hold true when you factor in that Larry would not only have to pay a 10% penalty, but also ordinary income tax on the money withdrawn from his 401k/Trad’l IRA?

I’m sure there is a fancy math formula that could answer this, but alas, I am woefully inadequate in that area.

Income tax would also be due

How much just depends on the withdrawal amount, and other potential income sources

To illustrate the point, let’s assume Larry’s time off work is voluntary (no unemployment income) and his last day on the job is 12/31. He and his spouse don’t work for a full calendar year. Maybe they use this time to work on skills for greater income opportunities in the future, maybe they go lie on a beach in Mexico to recharge

If during that year, they withdraw $40k from the 401k to cover expenses, they would pay the 10% penalty and 5% income tax (see the first chart above.) That 15% effective tax, while not ideal, is better than a 25% marginal rate paid earlier

The main point being, there are cases where it can be worth it to just pay the 10% early withdrawal penalty

Thank you for the quick response.

I would add that the growth of the pre-tax contributions over X years would further support your argument.

Your perspective has challenged my thoughts on this subject, and I thank you for that.

Keep writing, we’re all better for reading your work.

Thanks a lot SN

I too have had my perspective challenged a lot. There are a lot of very intelligent readers of GCC, and we can be sure any discussion will test assumptions. I know if I make a mistake, someone will let me know

It’s a lot of fun and helps us all be more knowledgeable.

I’m looking at the tax rate table for ordinary income.

The first 17,850 for couples is taxed at 10%.

17,851-72,500 is taxed at 15%

And so forth.

So if someone withdraws 40k, they would pay a net marginal rate of ~13%.

On the Roth vs 401k question, it seems to me that yields a better return; if a 20 year old socks away 17,850 into a Roth paying the 1785 in taxes at the 10% rate, assuming 8% annual return cashed out at 40, yields 83,198.

With 401k, that 1,785 in taxes deferred balloons into a 8,319 tax bill.

What am I missing here?

I forgot to take on the 10% penalty plus the 13% tax rate. for a total 23% for early withdrawals.

Hi Ted

What is missing is the Standard Deduction and Personal Exemptions. The first $x is taxed at 0%

See Last Dollar Principle as discussed in this post

https://gocurrycracker.com/roth-sucks/

The 10% penalty doesn’t apply if you follow the 72t rules. We will remove all of our 401k assets tax free and penalty free over next 30 years

https://gocurrycracker.com/gcc-vs-rmd/

You can see this in action if you use Intuit’s Taxcaster and enter a $40k IRA withdrawal for a married couple. Total tax is ~$2k, which is an effective tax rate of ~5%

https://turbotax.intuit.com/tax-tools/calculators/taxcaster/

Hope this clears things up

Jeremy

That was helpful, thank you.

I spaced out on the 10% withdrawal penalty exemption with 72t. I also plan to use that in the near future.

With a toddler, prolonged sleep deprivation is taking its toll on me.

Ditto with deductions; we use itemized deduction, and this year exempted $31k of our income.

Your post reminded me of those deviled details. I was assuming earlier in my 72t calculations a much higher marginal/effective rate.

This was a nice surprise after the fact.

With a newborn, I can relate on the sleep deprivation :)

I was using the 2013 table. 2014 income brackets went up by a thousand dollars each.

just remember all the money you put in has to come out at a higher tax rate. Taxes are going up trust me! My problem is I put too much in now I am saving hardly anything by taking it out.

I trust you John, but I’m also not worried about taxes going up

We plan to pay 0% on withdrawals as well

https://gocurrycracker.com/gcc-vs-rmd/

I love what you say about the ROTH IRA’s because I’ve always thought they make zero sense for us – we are in a high income field.

I do have a question please about the HSA accounts.

My understanding of them was that the money withdrawn from them can only be used for health expenses?

Is that incorrect?

Do you have a write-up further elaborating on them?

I love your blog….it is of my same mindset and I love expanding ideas!!

Thank you!

Yes and no. See this post from the Mad Fientist

http://www.madfientist.com/ultimate-retirement-account/

Withdrawals from the HSA are tax free if used for medical purposes, which we will all have. Or after age 65, HSA withdrawals can be used for other purposes, but will be taxed similar to a Traditional IRA

Thank you! That is the best information I have learned in a long time to further expand our goals. Again – I really appreciate your blog! Have a great day!

Thanks for clearing that up. I don’t believe I qualify for a HSA because my insurance is too good (really cheap through my employer) so would the traditional IRA be my next best bet after my 401k?

Yeah, take advantage of all of the tax deductible options you can

I provide a list to follow in this post:

https://gocurrycracker.com/roth-sucks/

Hey Mrs. FW, first, let me say that I love your blog and just introduced my wife to it, but second, I wanted to give you another point of view. I’m in the military, and I deploy overseas regularly. If I spend 1 day in a combat zone, the entire month is tax free (I average a lot more than that per year, though). Housing allowance and food allowance for all military is tax free, and so is the per diem we receive on work trips. In my case, because of my high deployment tempo, I normally clear over $100k a year, but I’m only taxed on about $18-23k. Between my retirement pension and investments in roth, I’ll be able to retire at the age of 41 (way older than you will be when you retire, I know, but I’m 30 now and I still really enjoy my job), but I would have to withdraw some from my nest egg to supplement the pension. I’m curious to get your thoughts on my strategy here, and anyone else, of course is welcome to critique. Thanks, and have a good one, FW

I should have mentioned a few other things: 1) Sorry FW, I called you “Mrs.” on accident…My bad. 2) I’m married with two beautiful little tax deductions, which means that I’m not paying any taxes each year.

For CZTE beneficiaries like us who ultimately pay a 0% or negative federal tax rate despite a generous paycheck, the proper vehicle for your retirement contributions is a Roth. There are no circumstances in which a Traditional IRA/401k would prove more beneficial in the above scenario, especially when coupled with your future taxable pension benefits.

Except perhaps artificially lowering your taxable income even further to exploit/maximize EITC and then attaining a 100% disability discharge/retirement to avoid those taxes on your pension, but who wants that?

Love this. What happens if as a couple you make a combined $160,000? I believe you don’t get the full tax benefits of a traditional IRA at that level. Is a Roth better at that point?

The main thing here is that a couple at any income level should take advantage of the Traditional 401k first. Assuming both are employed, this will pull total taxable income down to $125k. Add an HSA to that, and now your highest marginal rate is 15%

If the Traditional IRA is not deductible, then last in line you could put up to another $10k into two Roths

Thanks Jeremy. Just wanted to make sure. The wife and I currently max out the traditional 401k’s and the Roth IRA’s. Unfortunately we don’t have access to HSA’s but we’re happy that we’re reducing taxes as much as we can. Thanks again for the great post.

After maxing out 401-k and HSA accounts, isn’t a backdoor Roth IRA (and mega backdoor Roth IRA) a smart move for post-tax dollars vs a straight taxable investment account?

I would agree that those two methods are the next best after pre-tax accounts. It seems about 50% of folks can’t do the Mega backdoor, so at some point taxable brokerage accounts will be unavoidable.

I had started a taxable brokerage account, but since learning of the Mega Backdoor, I’m going to be trying that.

@Brad: Yes, that would be the next step, if and only if you’ve already maxed out all pre-tax accounts

@OK: Sounds like a solid plan. I’ll address this more in a future post

Maybe? Depends on how much you will be spending in retirement. If you are married and frugal, it’s highly likely that you’ll pay 0% long term capital gains taxes when you retire early. This means that pulling your money out of your normal “taxable” brokerage account is functionally the same as withdrawing roth principal (the mega backdoor).

The benefit being that you don’t have the 5 year wait to get access to those funds. The downside is that I’d consider the LTCG tax exclusions to have much higher regulatory risk (congress changing the law) than the Roth rules.

Disclaimer: I’m no accountant, I’m just some guy on the internet :-)

I think one needs to compare Roth contributions against post-tax

brokerage accounts. Roths make sense if you have maxed out your pre-tax

contributions and still have a lot of money left to invest. Part of

that money can go into a backdoor Roth IRA, which will give you tax

benefits on the growth portion in old age. It’s better than putting that

portion in a post-tax brokerage account which is taxed on the growth portion.

Or am I missing something?

Hi Fubek, that would be the correct comparison

1st take advantage of all accounts that can reduce taxes now, and then when the choice is between $5k in a ROTH or $5k in a brokerage, then go for the ROTH

I think this point is crucial for high-income earners. Of course maxing out any and all pre-tax accounts is primary goal (thank god I have a 401, 403 AND 457!).

But for someone who has maxed out all pre-tax vehicles, the comparison had to be between a roth account and a post-tax brokerage account…

I know I’m late to this party (6 years, in fact) but I’m hoping you would clarify your comment. You say if you have the choice between $5k in a Roth and $5k in a brokerage, go for a Roth, but then you also say how much you HATE Roths and that most of your money is in a brokerage account. I only ask because I have a substantial amount in an annuity, we still save all we can in tax-advantaged accounts, but now the question is what do we do with the leftover – Roth or Brokerage. Thanks!

Please look at the post, Roth Hypocrisy, which explains why I didn’t contribute to a Roth while working but I do now. I think it will answer your questions. If not, let me know.

Well, when you put it like that, it makes it sound so easy. Probably because it is easy! It’s daunting at first, but when you take it a step at a time and set up things like a 401k, IRA, HSA, etc and then let it sit there and compound on auto-invest for a decade or two, it becomes very easy (averaged over the 10-20 year period).

Like you point out, turbocharging savings and sucking up all those sweet tasty tax savings is some of the best earnings per hour you can get.

Exactly. It is amazing to me that 1 of 3 people with access to a 401k don’t contribute. And it pays better than most people’s day job

I have had discussions with fellow engineers. You know, people that are licensed to design bridges and skyscrapers. Sometimes they just don’t want to save anything and prefer to spend it all on worthless crap. Other times they think they won’t be at the firm more than a year or two so “don’t want to deal with it”. And sometimes that meant missing out on a 100% vested 4-6% match. I’m happy enough with saving 22-32% of my income (state taxes here too, boo!). And they give me EVEN MORE MONEY for contributing?

WTF man, WTF.

This is how I ended up with over 10% of all 401k assets in my former employer’s plan (with 40+ employees most of whom made more than me and many were there longer than me).

Great insights. We get screwed (admittedly in a 1st world, rich person problem kind of way) in that we are limited to maxing work related retirement plans b/c we have never had access to HSA accounts and we make too much for deductible IRA. Now my wife switched to a company w/ a Simple IRA from prior 403(b) meaning we are down to $12,000 contribution max on her plan compared to $18,000. I love reading the GCC and ROG posts to learn about your tax strategies, but we are very limited with what we can do compared to you. We max our work accounts, then Roth and then go to taxable accounts. I guess as problems go, not the worst to have. It would however be nice if we had a simplified tax code where our tax deferral options weren’t tied to what type of benefit plan our employer chose and then further limited to what investments we can choose within those plans. All the more motivation to stop working I guess!

I view the 401k options as part of compensation. If a company doesn’t have a good plan, then my salary should be higher to compensate. Taxes and cost of living are other factors. This is partially why I accepted a job offer in Seattle, WA vs Bay Area, CA. (granted, compensation is only one part of a job)

Our HSA was only available my last 2 years or so, and is mostly just a rounding error on our net worth.

In the end you’ll probably end up just like us, with most of your savings in a taxable brokerage account. It’s not a bad place to be

I agree about the compensation part. My wife took this job b/c of work from home, part-time, lower stress, etc.

I also agree about ending up in a good place where our taxable accounts will work essentially like Roth w/o the restrictions b/c of our low income.

That said, we were late to the party in figuring out these tax deferral concepts and we are seeing with our current strategies the huge difference we have made over the last 3 years compared to the first 10 years when we didn’t max deferrals. In my latest post I referred to the JLCollins article:

http://jlcollinsnh.com/2011/06/08/how-i-failed-my-daughter-and-a-simple-path-to-wealth/

and made the statement that if we hadn’t made the many errors we had made with investing with an advisor that we would have already be retired.

Factor all the money we paid in loads, annual fees and capital gains taxes investing in actively managed funds in taxable accounts and then add all of that by the increased tax savings of your strategies and compound it over time and it is amazing how simple it would have been to cut our already short careers (about 16 years) to 10 or less with no sacrifice or change in lifestyle!

Keep up the great work spreading this message!

Such a great breakdown. I agree that the tax deferred accounts are the way to go, and we max out our 401k and HSA.

The one rub with the Traditional IRA is that there is an income limit, and one that’s a lot lower than that of the Roth. So while it’s better, single people whose MAGI is above $71k and married couples whose MAGI is above $118k don’t get any tax benefit.

Thanks donebyforty!

Yeah, that income limit make the TIRA a lot less interesting. In that case I would put funds in a brokerage account instead (after maxing out the 401k, of course)

(Edited for accuracy per correction from GordonsGecko below)

Are you sure that’s right? IRS documentation seem to point to income limit phase outs even if you’re covered by a workplace plan.

http://www.irs.gov/Retirement-Plans/Plan-Participant,-Employee/2014-IRA-Contribution-and-Deduction-Limits-Effect-of-Modified-AGI-on-Deductible-Contributions-If-You-ARE-Covered-by-a-Retirement-Plan-at-Work

You are correct, the IRA is deductible as long as your income is below the threshold’s donebyforty mentioned. My statement was incorrect. I think I’ll delete it so as not to confuse anyone

Even got fuzzy edges for Van Gogh, nice paintings! Several people have mentioned this already. What if your income level exceeds the limit to get any tax-deduction for a traditional IRA account? Backdoor Roth bypasses the income limit and allows additional contribution to tax advantage accounts. I do agree maximizing the tax-deferred accounts should take the first order. After these are maxed out, other tax-advantaged savings account become attractive, such as Roth IRA, i-bonds, or coverdell ESAs.

haha, you noticed that little detail. I once spent 5 hours in the Van Gogh museum in Amsterdam, it is an amazing place. It is hard to capture the texture and nuances of his works on a 2D screen, unfortunately

Once you lose eligibility for the tax deduction on an IRA, it is less interesting. But I’d still take advantage of the tax deference and eventual backdoor ROTH

While ibonds do allow tax-deference, I find their overall return fairly poor (less than inflation currently) so they are a fairly poor investment. I’d rather have a gain and pay tax then a loss and pay no tax

The number of comments on your blog has certainly grown more than five times. :) Congratulations!

I don’t personally invest in ibonds myself for the reason you listed. However, I understand why some people might consider them for risk precautions. I had a conversation with a colleague yesterday. He pretty much has the stash already, but he cannot pull the trigger to retire. He is so scared of another 2008/2009. He stayed in the course, and his portfolio has fully recovered and went way up north. But this psychological pain just scared him so much that he cannot contemplate early retirement any more. But regardless of retiring early or not, the fact he has saved so much for a long period time has put him in a great position. Even if there is another financial crisis, he is still relatively better covered than most people. How did you guys handle the financial crisis? It was like half way in your saving journal to FI. I wonder what were your thoughts/actions at that time.

I wrote a post on that :)

https://gocurrycracker.com/reminiscing-about-the-glory-days-of-2008/

Always enjoy a good reminder that tax deferred savings plans are the way to go, I plan to pick up the pace this year for that exact reason. Thank you.

Thanks Steven. Per your comment on Jim Collins’ blog, the first chart is a quick visual on how much tax you can expect to pay on earned income or 401k withdrawals

Gross Income – Traditional 401k contributions – HSA contributions = MAGI. Correct?

Sometimes. For most people, that is the AGI and MAGI. There are more deductions than just those 2, and MAGI will add back certain deductions

See this:

https://turbotax.intuit.com/tax-tools/tax-tips/IRS-Tax-Return/What-Is-the-Difference-Between-AGI-and-MAGI-on-Your-Taxes-/INF22699.html

And also our 1040 as an example of all the stuff that goes into AGI (line 37):

https://gocurrycracker.com/the-go-curry-cracker-2013-taxes/

Not to be a downer here, but to be a downer here: Aren’t you only considering half the equation? It seems like you are only considering the effect of now.

You are supposing that people will be able to use the benefit of withdrawing 401K proceeds sans tax up to the first $40k or so. Then using this $40k to live on for the year.

Eventually, Social Security and Pension income will fill that $40k gap. Then you’ll be paying tax on the 401K anyway. (This becomes a chicken or the egg discussion because you can argue that the tax is being paid on the Pension and Social Security. However, I would posit that the 401K withdraw is optional until age 70.5 so any 401K withdraw really will be taxed for a person drawing Social Security and Pension.)

Furthermore, a person is required to make minimum distributions from the 401K at age 70.5. This was designed so the government could force you to pay taxes on that nest egg before you die.

I realize your blog is about retiring early. So, my arguments may only be relevant in the long run. However, GCC also relies on the concept of living on $40k of income (or whatever the exemption/allowance levels allow to be tax free). I think many people anticipate more income in retirement for married couples.

Maybe it’s just me, but I don’t think your strategy is as easy as you make it seem. It’s certainly not sensible for everyone. Although, everyone’s situation is different.

Yes, I am only considering half the equation: How to retire / be financially independent as fast as possible with the most assets

I’ll address the draw down phase in a coming post, with more pretty pictures

As you know, we expect to pay $0 taxes throughout the remainder of our lifetime. That isn’t the case for everybody, but it seems a good aspiration. This includes RMDs and Social Security (we have no pension)

Jeremy,

Thanks for the inclusion!

I’m actually on the opposite side of the spectrum regarding retirement accounts. I purposely forgo tax-advantaged accounts due to their relatively illiquid nature. Plus, it’ll be great to have my blog as working proof that they’re unnecessary. I admit they’ll speed the timeline up, but there are disadvantages there.

How exactly are you guys tapping your 401(k)s and IRAs? SEPP?

Best regards!

Hi Jason

The illiquid nature of tax advantaged accounts is largely an illusion. Yes, there are restrictions, but no more severe than a lid on a cookie jar. You just have to lift the lid

Between SEPP’s, a ROTH IRA Conversion ladder, and the inevitability of having funds in a taxable account after years of saving a high percentage of income, it is relatively easy to have sufficient funds for living

We personally are doing a ROTH IRA Conversion ladder, primarily for long term tax avoidance as opposed to short term spending, but the process is the same

For the ability to retire or be financially independent several years earlier, I think the tradeoffs are well worth it. Considering the BLS says 31% of people with access to a 401k don’t contribute, that is the bigger problem I’m trying to overcome

Here is a link to your post on this topic, for those interested in another way:

http://www.dividendmantra.com/2013/08/why-i-hold-100-of-my-equity-investments/

In your case, particularly now that you are self-employed, using a Solo-401k could accelerate your financial independence by many years. I know you’ve done the math

Cheers

Jeremy

Jeremy,

I have done the math, and it wouldn’t accelerate it by many years at all. Because of the self-employment income, I’ll be in a higher tax bracket down the road anyway if I go that route…meaning the taxes are just deferred. And with such a short timeline, there isn’t much to defer anyway.

Plus, you seem to be ignoring the “hassle factor” People talk about home ownership vs. rentals in the same manner, ignoring the fact that owning a house is a hassle in comparison to renting. I’d argue that SEPPs and Roth conversions are also a hassle. How much that hassle is worth is up to you and your own situation. I was actually reading about another guy doing an SEPP and it’s far from “relatively easy to have sufficient funds for living”…unless you like the idea of tracking paperwork for three decades. Just my take on it, but full liquidity and no hassle is worth some coin. Especially when we’re talking about financial independence after 10 or 12 years anyhow.

Like I said, I like that the blog is showing how it’s done without tax-advantaged accounts. They’re really unnecessary for those with a short time horizon. If I was going at this for two or three decades, I’d probably be a lot more interested in a tax-advantaged account or three.

Best regards!

I think a post on the math comparison you did would be really interesting!

The SEPP complexity piece you mention would also be really interesting if you can share the link?

What I meant to say, re: “relatively easy to have sufficient funds for living” was that because you end up with funds in taxable accounts, you have access to funds independent of any 401k/IRA. The contribution limits on the pre-tax accounts are too low to save everything in a tax-deferred vehicle

That said, we all have to do taxes every year (or in your case every quarter?) and the additional work on top of that is really only a few minutes for a ROTH IRA Conversion. SEPP math can be easier or more complicated, depending on which of the 3 methods you choose. My rate of return on that few minutes is pretty high, at least $10k/hour. Taxes are a hassle, the ROTH conversion less so

+1

And the burden of tracking tax lots in a brokerage account is no trivial matter either, and requires decades of records as well.

Another benefit of tax deferred accounts is you can go hog wild trading all kinds of stuff and not have to worry about keeping records. Not necessarily the best investment strategy, but if you want to try for some short term trades or arbitrage plays without paying ST gains, tax deferred space is a fun place to play.

One of my biggest regrets in life is not maxing out 401K/SEP IRA/REgular IRA/Roth IRA contributions earlier. I have paid so much in taxes in the first 5 years of my dividend growth journey, it actually hurts thinking about it. I used to think that these plans are bad in general, but after I researched it further, I learned I need to learn about them.

Some 401K options are poor, but mine offers low cost index funds. I invest mostly in dividend stocks, but because I have hopped around, I have been able to roll those old 401Ks into IRAs, and picked my own investments.

When I did my FI goals for 2015 and beyond, I did a very rough calculation that by maxing out all tax-deferred vehicles, I could potentially reach FI faster. For example, if it took 10 years using taxable accounts, it would take 7 years using tax-deferred vehicles. That is 3 years of your life, which one would have otherwise spent excessively working and paying tax through their nose. While I can always make more money doing something of value to someone, I can never make more time.. (I am assuming 30% Fed + State tax, and that one can defer say 18K in a 401K, 3K in an HSA, 5.5 in an IRA ( hopefully tax-deferred but Roth is ok = total of 26.5K/year). The rest could be places in a taxable account

I also plan on doing some Roth Conversions along the way in a few years/decades. I have a feeling people with networths above a certain level might end up paying more in taxes in the future – hence it is also nice to have some tax diversification and tax-deferred compounding in the tax-deferred accounts.

I am also learning about home ownership, which I think could be worth the hassle. I disagree with GCC on that, but that could be because my knowledge is mostly theoretical, whereas he seems to have had bad experience owning ;-)

Can you point me in the right direction on this concept – let’s say you want $2M in tax deferred accounts by 40 in order to retire early. Where does your income come from if all of your money is in tax deferred accounts? Can you tap these early w/o penalties?

I answered this question when you last asked 1.5 years ago.

So I keep thinking about this…

I guess if I tried to state your strategy in different terms; you are saying that you are trying to minimize any tax now by deferring as much as possible. The effect of this being that you are left to try to minimize future tax paid when you withdraw your funds.

Am I right?

The overarching concept here being that you minimizing your effective tax rate now and will likely have a lower effective tax rate when you withdraw. Thereby, saving tax now and later… and in the process saving the difference thereby saving more overall.

Have I got the hang of it?

I was going to respond to your first post, but I think you figured it out in this one. Reduce your taxes now to speed up your accumulation, and likely your tax rate will be lower in retirement, since you won’t be working for income. Longer term, RMD’s could cause higher taxes, but you are still effectively giving a larger amount of money more time to grow.

I’m following this strategy, the next question is where to put the extra money past the tax-free amount. I’m looking at Mega Backdoor Roth for that.

@Ryan: Yes you got it. Take advantage of the tax deductions now. Retire earlier with more money by saving less

Then later in life, there are other strategies to minimize the taxes on your savings

@OK: I’ll address the “where to put extra money” aspect in a future post. Mega Backdoor Roth is a good option

Jeremy,

Will your next post be about how to pull these funds out from the time period of FI/RE to Age 59.5?

Looking fwd to reading that part.

Hi Jeff

I have a post coming on withdrawing funds before 59.5. The next one will probably be more details on the ROTH controversy

@Ryan: plus you can grow the pre-tax money instead of the post-tax money. It’s not just a question of different taxation levels. If the effective tax would be the same now and in retirement, it would still be advantageous to let pre-tax money grow instead of post-tax.

Do the math on this.

If you pay 25% tax on 10,000 today, then let the $7,500 grow at 6% for 30 years…

OR

You invest $10,000 today, let it grow at 6% for 30 years then pay 25% tax in year 30…

You will end up with the same amount of money in the end. It’s exactly the same. You’re point is incorrect.

Hi Ryan,

this would be correct if you only had capital gains:

f := (1 + 6%)^30

(f * $10,000) * 0.75 = f * ($10,000 * 0.75)

The problem is that most likely you would incur dividends, which would be taxed yearly at 25%. I am not exactly sure how that math looks like in a formula, but am pretty sure it turns out as less at the end of the 30 years.

Who here has a math degree and can look into that? :-)

6% growth in my example is supposed to cover total yield of investments. Whether you earn via dividend, cap gain, or stock price appreciation, your answer is the same. Any spreadsheet model can simply bear this out. I’m a CPA. I feel this is a common misconception of ROTH vs 401k.

The truth is, as long as tax rate is the same at contribution and withdrawal, there is no difference. The argument over which is better for you revolves around your tax rate now versus your expected retirement tax rate.

Hi Ryan,

First, we’re comparing post-tax brokerage accounts vs a traditional 401k, not traditional 401k vs Roth. Maybe this is our disconnect?

Post-tax brokerage: Let’s assume that there’s no capital gains or stock price appreciation at all, the 6% are purely dividends which you get taxed at 25% each year, the remains you would reinvest. After 30 years, you would have $37453 in assets. There’s no “distribution taxes” because there’s no capital gain that could be taxed.

Post-tax brokerage: Compare this to a yearly 6% capital gains increase, which is only taxed at 25% when you sell the asset after 30 years. You will have $43,076.

401k: You would have the same $43,076 irregardless if you incurred dividents or capital gains.

The latter is 15% more than the former.

This is true mathematically. 25% tax now is the same as 25% tax later, assuming both accounts have the same return

But look at the Picasso / picture #1 above. Even with $200k/year withdrawals from a 401k the net tax is less than 25% (~18.8% actually.) While 100% of people may aspire to have $200k/year living expenses in retirement, less than 5% will do so

It would be better to take the 25% tax reduction now and pay <19% later

After reading a couple early retirement blogs, it seems from my basic understanding is the preference of the tax deferred plans over a Roth because when you retire early you have years of low income to convert to a Roth if you so choose. I’d like to retire early, but I’m not sure it’s in the cards. I don’t know yet. I had a similar thought as Ryan about Social Security and Pension filling up the lower rungs. Specifically my pension…which is also my golden handcuffs as I call them…I will have a good pension and I’ve read that those with pensions may benefit more from a Roth. I’ve been debating this issue for a while so I’m interested to clear this up.

I’m in a similar boat as you. The reason I have trouble with the GCC method is all about when you plan to retire. I think if you want to retire at age 35 or 40, it makes sense to leverage tax-deferred accounts.

However, for someone with future pension income (forcing you to pay tax) and projecting retirement at age 55 or 60 or even later, you don’t want to have all your money in tax-deferred accounts because you are forced to pay tax to get that money and once RMD kicks in, you may be in a higher bracket than you want.

You want to have money in the tax-free (ROTH) bucket, too. This way you have more flexibility over when you access your money in retirement.

I agree with decreasing your tax-rate now by utilizing tax-deferred vehicles but I don’t think you can say the ROTH is useless, especially for someone with pension income and a later retirement age.

Here is the basic comparison to make

Look at the Picasso / Picture #1 above. Where on the graph will your income lie in retirement with Pension and Social Security (85% of it taxed) and 401k/IRA withdrawals?

Over ~$90k, funds are taxed at 25%

If the Pension and SS push you over 90k, and your current marginal rate today is 25% or less, we could argue that a ROTH and Traditional 401k are mostly equivalent. Congratulations if that is the case

But if the pension and SS are less than 90k, then some of your 401k funds will be taxed at 15%, and you lose tax wise by choosing the ROTH now

Then of course at Age 70.5, RMDs kick in. See this example for a case with pension and RMD. Even with large RMD withdrawals, Mr and Mrs Bob still end up ahead by using the 401k/TSP for tax advantage while working

https://gocurrycracker.com/reader-financial-review-scared-death-early-retirement/

OK, I’ll bite. Tell me why a ROTH IRA is like taking your cousin to the prom! I’d like to hear.

I share Ryan’s skepticism, which I think is well-placed. And looks like Andrew is coming from the same place. You seem focused only on the savings side, not the withdrawal/distribution side. And there’s the rub.

Here’s a specific example (my own). Retired Age 53. Not early by your standards, and that may be the key point for the difference here. Yet, early by many people’s standard. I adhered to conventional wisdom my whole career and maxed out 401(k) when they were introduced, and maxed out spousal IRA (it was deductible). Had some savings in taxable accounts as well. Now that I’m retired, I’m living on a company pension and some of my taxable savings. My pension will actually increase in 5 years because another employer’s pension will kick in then. At Age 62 or above, I can collect SS (plan to wait until at least Age 66). The problem is that I am reasonably comfortable in present lifestyle. Don’t really need the savings now, but may at future date. Call it old age security, with some future splurges built-in. So, the big problem I now face is the mandatory Age 70-1/2 required minimum distributions. They will hit when I am drawing all pensions and SS. My SS income will get taxed at a HUGE marginal tax rate (Google “tax torpedo social security”). And if the government chooses to deal with entitlements like SS and Medicare with future increases in means-testing, this impact will only increase. Not to mention future increases in income tax rates due to ballooning government debt, which would affect tax rates on distributions from IRAs/401(k)s. So…I am now trying to convert IRA/401(k) money into ROTH IRAs. The problem is that the investments are growing faster than I can convert them (within the 15% bracket limit). It is a nice problem to have, vs. having the investments shrink. But the way things look now, there aren’t enough years left to complete the conversions–not even half the money will be converted in time. The tax torpedo looks inescapable. Had I realized all this years ago, I would have put some of that tax-deferred income into a ROTH instead of IRA or 401(k) [though of course I’d have captured all the employer matching, at least].

I agree with everything you said. I think the main issue here is the age you plan to retire and fixed income you may or may not have later in life.

I understand why there are people that get paid to do this as a full-time job. Every situation differs and thus should the prescription.

Ditto for the same situation from Bob and Mrs. Bob here.

https://gocurrycracker.com/reader-financial-review-scared-death-early-retirement/#more-3535

Will need to bump up the withdrawals and go into the 15+ tax bracket to get the money drained down out of the tax deferred accounts before the RMD’s strike. Adding in SS later is going to create havoc on the tax bill.

Almost doesn’t see fair after saving for so long to build up the wealth, only to see it confiscated at the end. In some situations, if you want to continue saving for retirement, you must use the ROTH after maxing out other options such as the 401k and the HSA. The income limit will prevent you from contributing to a traditional IRA.

Hi Bob

Your situation is a great one. A great amount of money built up over the years due to good saving practices and taking advantage of tax deferred accounts. This is certainly a better place to be than if you had never saved in a 401k/TSP

RMDs will certainly cause you to pay some taxes, but it is important to not let the tax tail wag the dog. The overall lifetime tax rate is still quite low

Cheers

Jeremy

Haha, that little comment slipped past my internal editor due to a little too much wine :)

Without knowing exact numbers, it is hard to know exactly which path is best. Converting to ROTH via ROTH Conversion ladder is a good strategy for minimizing long term taxes

With a pension, SS, not needing the savings in your 401k, you are in great shape. Had you never invested in a 401k or Traditional IRA, your wealth today would certainly be less than it is now.

As others have mentioned, panning the Roth IRA outright is oversimplying things. The Backdoor Roth and the Mega Backdoor Roth are definitely advantageous to most prospective early-retirees than contributing to taxable brokerage accounts. They are semi-liquid and of course have the massive tax advantage. My wife and I currently utilize both of these strategies after maxing out 401K and HSA options.

Hi Jake

See the discussion in The Great Roth Controversy for more on this. I don’t see the tax advantage as massive, and it comes at a cost

We hold all stocks in our brokerage accounts, and pay zero tax on dividends and long term capital gains (same as Roth.) We have 100% access to contributions AND earnings, so they are fully liquid (better than Roth.) We can harvest capital losses and use the foreign tax credit on our international funds (better than Roth.)

After reading that if you still prefer a Roth, no worries. You are saving a high percentage of income and taking advantage of all of the tax-deductible options available to you. That is a winning strategy

Cheers

Jeremy

Love the explanation, great breakdown. We can do something similar in Canada as well and this is exactly what we’re doing.

Is that the RRSP? By any name, getting a tax break for saving is a wonderful thing

Our only option for our HSA is to keep it in a checking account; we cannot invest that money. So if we don’t spend that money in-year, it gets nibbled by inflation.

My wife and I also have access to 457, 403(b), and 401(k).

Right now, we are maxing out 457, 401(k), and HSA. Don’t quite make enough to also max out the 403(b). In any case, since the HSA money is not really investable in this context, would it make more sense to put the HSA monies into the 403(b) instead? I’m trying to decide whether Pre-FICA money that’s not investable(HSA) is a better long-term play than post-FICA money in an investment account.

One more caveat, on my wife’s HDHP, your deductible is $2400… so basically any medical spending after that is “free”. Perhaps this is an argument to fund the HSA up to $2400 every year?

Does that make sense? Any thoughts? :)

We have an HSA invested only in a money market account. I’ve been too lazy to research a place to roll this over to where I can invest without excessive fees (anybody have a HSA custodian they love?)

But I like the HSA even without good investment options. It is tax free going in and tax free coming out, on both contributions and earnings. We pay for all health care expenses out of our brokerage account instead of the HSA, because we want those funds to grow, and I’ll eventually get them into stocks

What to do now partially depends on how much longer you plan to continue working for your current employer. If it is a few years, the HSA is great even if invested only in a checking account. If the answer is 30 years, then I would organize employees to put pressure on your employer to change the HSA rules to ones a little less ridiculous

I can’t be the only one to mention that there are actually two turbochargers and a supercharger on that ridiculous Camaro. :-)

If I knew anything about cars, I would have come up with some nice way to talk about turbocharging AND supercharging your savings :)

This is good. The problem we are having is that my wife is an adjunct professor and doesn’t have the benefit of any specific savings plan. When you put my income with hers, after we adjust for other deductions, I am not sure we have enough money even for a spousal IRA. Any advice? Believe me i would love to reduce our AGI. We have a future of huge tax bills because of this.

Hi Jason

The only thing I can say is take advantage of all of the tax deductible accounts available to you. 401k / 403b / HSA / Traditional IRA / etc…

But if those aren’t options, saving in a brokerage account is better than not saving at all. See this post as an example of how to minimize future taxes by focusing on qualified dividends and long term capital gains

And maybe not an option, but I considered access to a 401k as part of total compensation when comparing which job offers to accept. The next time you or your wife are thinking of a job change, maybe you can add the 401k to your list of requirements

Cheers

Jeremy

Sorry I’m a little late to comment, I read this excellent article on my phone, then came to the GCC site on my desktop and saw money on fire! (your next post on Roth IRA’s) and ended up commenting on that one first. Just wondering, have you ever fiddled around with http://www.i-orp.com (online tax optimization computation)? I’d love to hear if it compares to ‘real life’ experience (although it’s goal is to maximize spending and die w/ $0, having an optimal Roth conversion, even into the taxable regime, would be a useful guide and the visual / tabular output is helpful).

I haven’t, but I’ll add it to my list of things to check out. Thanks

I am probably missing something, but when would putting $5,500 in a taxable account be better than $5,500 in a Roth?

Even during a relatively short working career, you could see some occasional capital gains from index mutual funds, maybe you have to rebalance in a taxable account, heck, maybe you make “too much” in retirement, etc.

Once the tax deferred options are maxed out, isn’t the Roth IRA a better option that subjecting yourself to (possible) taxation on growth?

There are pros & cons. You can’t write off tax losses in a Roth, and can’t withdraw earnings (dividends) until age 59.5.

The Roth accounts will still exist as part of a Roth Conversion ladder, I just question the statement that it is always the best

This is a great post, and I am looking forward to reading more of the comments and exploring more of the links.

One question: above, it’s stated that “Contributing to a 401k effectively shifts our tax curve. More dollars are taxed at 0%, resulting in less tax paid.”

I don’t think this is entirely accurate. Wouldn’t contributing to a 401k mean less dollars are taxed at the marginal tax rate, as opposed to more dollars are being taxed at 0%?

Hi Paul, thanks.

Both statements are 100% correct, but are different ways of looking at it. The end result is the same

401k contributions are taxed at 0% (or if you prefer, not taxed.) Those same contributions are NOT taxed at the marginal rate.

I phrased it the way I did because it is more directly related to how it appears in the tax curve images

I am always trying to defer taxes on as much money as possible. I still get upset that just because my wife works with an employer that doesn’t offer a 401K that we are stuck with a limited contribution of $5,500 to a traditional IRA.

Why don’t they make the contribution limits the same? It just seems like the government didn’t think this through. Also why did the 401K limit increase in 2015 to $18,000, but the traditional IRA stayed the same???

Cheers!

I view the 401k as part of compensation. If an employer doesn’t offer one, then income should be higher to compensate

If this were the only thing government didn’t think through, wouldn’t that be great? haha

I have a theory on why the limits change differently on 401k and IRA contributions, as well as standard deductions and personal exemptions, marginal rate levels, etc… If a politician votes for a tax increase, they don’t get elected next time. But if all of these limits rise more slowly than inflation, the result is an effective tax increase but nobody revolts. Genius

I may be wrong, but I believe they only make inflation adjustments in $500 increments. Since $17500 is more than 3 times $5500, a 2-3% inflation adjustment would cross the $500 threshold faster. In other words, you’d expect the increases in the 401k contribution rate to come at about three times the frequency of increases in the IRA contribution rate.

This is great! Love this post! Would you mind extending your graph chart out to $1MM dollar income to see what it looks like for those making a lot of coin? thanks!

This isn’t 100% accurate. The 0.1% don’t benefit much from a 401k, since a contribution of $18k is only 1.8% of income, and 39.6% marginal rates, the AMT, and increased Medicare taxes set in. But then again, with 7 figure income you don’t need to turbocharge anything

I may be missing something obvious, but is the reason a married couple filing jointly pays 0% tax on their first $20K of income because of deductions (or at least the standard deduction)? My understanding is that even the first dollar earned in 2015 is taxed at 10%, up until $9,225.

Hi Paul

That’s right, the standard deduction plus two personal exemptions mean that the first $20,300 (2014) is tax free

The next dollar is taxed at 10%

Excellent. Thanks for the quick response!

That camaro in your header picture is turbocharged and supercharged! Applies perfectly for those using multiple power adders to their savings like 401k and HSA. Great post, this will help me convince friends and family the advantages in a visual format, thanks!

I am a visual thinker, so the graphs in this post really help me think through the savings. Glad they are helpful for you too!

Vroom! Vroom! Turbocharge those savings! haha

Hey there! I would love to be eligible for an HSA but alas I don’t qualify as I don’t have a high-deductible health plan through my employer. I contribute the max amount to my 403(b). Do you have any tips for becoming eligible for a HSA? In the meantime, should I contribute to a Roth or Traditional IRA? Thanks a million! :)

Hi Isabel

The only way to be eligible for an HSA is to have a HDHP. You can work with your employer to make that an option, or find a new employer. I wouldn’t change employers solely to get an HSA. They are great, but not necessarily that great

You can read about Roth vs Traditional here:

https://gocurrycracker.com/roth-sucks/

Unless you meet one of the exceptions (poverty level incomes) then as a rule of thumb Traditional is the way to go. Take the tax deduction now

Great article. Im from the UK and living in Hong Kong but some interesting facts in there for me to take in

would love to get your thoughts on when you have a sub-par 401(k) offering from your employer, whether it is still beneficial to invest in that rather than an IRA or a brokerage account. For example, my 401(k) fund has poor options–no Vanguard and the average expense ratio of the available funds is +1%. I have 100% of my 401(k) in a 2050 Target Fund (I’m 31 years old), with an expense ratio of 1.01%. Wouldn’t I be better off in an IRA then a brokerage account with Vanguard, getting charged .05% in expenses? At what point does a 401(k) become a bad deal (after the match, of course)?

Hi Andy

See this post from Jim Collins:

http://jlcollinsnh.com/2013/06/28/stocks-part-viii-b-should-you-avoid-your-companys-401k/

Generally, its worth it to get the match, and still worth it to max out both 401k and an IRA. And then petition your employer to move their 401k out of the 1980s

Cheers

Jeremy

Hi Jeremy! You and Winnie have inspired my husband and I to shoot for an early retirement. We just hope it’s not too late. We’re already in our 30’s, live in NYC (cheap rent thankfully) and don’t have children yet. I have 50k in a savings account earning a measly 1% interest and I want to make it work harder for me. It’s not all the savings I have so I’m very comfortable with investing it. I adjusted my 401K to ensure that I contribute the max this year. I can also contribute $5,500 into my traditional IRA but that still leaves me with $44,500 to invest. Do you recommend that I open a separate brokerage account and invest all of it in a Vanguard Total Stock Market Index Fund?

Awesome!

That is what I would do in the same circumstances. If you want to get really fancy, you could add a bit of Vanguard Total International Stock Index

Read Jim Collins’ stock series for more

http://jlcollinsnh.com/stock-series/

Note the disclaimer. I’m just a random guy on the internet

Hi,

yes i stack 18% into my 401k, and 10k a year in IRA account. Married. how is all that savings helping me live financially free? i can’t touch my savings until i retire. I am 32. so really, i can’t be financially free until 63?

You can access those accounts starting at Age 59.5 without issue

Before then, you can access those funds via SEPP or Roth IRA Conversion. We use the latter

This post shows one example:

https://gocurrycracker.com/gcc-vs-rmd/

Hi Jeremy,

You two are awesome! Firstly I’d like to say congratulations on having new born baby. He is adorable. And thanks for inspiring and triggering me to have this early retiring concept.

I’m from Taiwan as well. I wish I could know this concept earlier. But well, I spent some time on “extending my education journey” – studying Maters Degrees in Australia. That gave me huge debt but I completed my first dream, so I’m happy. :)

Fortunately, I could start my career in Australia and stay in this beautiful country as my second home town. That helps me to achieve my second dream more easily – to retire earlier. As the salary is great here but I’ll use it in a “more efficient way”. So I’d like to say thank you for introducing this great concept to me which has greatly changed my life plan to a better path.

All the best to you, Winnie and new boy.

Cheers,

Julie

Thanks Julie!

Working in Australia is a great move, salaries are so much higher than in Taiwan. Good luck!

I am an 35 year old married Army Officer. I have about 100k invested mostly vanguard and TSP (Federal Government 401k). This year I am set to place 18,000 into the TSP and another 11k into two Classic IRA’s at vanguard. It seems so odd that I can invest 29k without paying any taxes on it. Thanks for opening my eyes to this.

My question is what to do next year. I am deploying for a year to the middle east. During this time all of my income is tax free. I was planning on putting 11k into two Roth IRA’s, then the rest into a taxable vanguard acct. Can you think of a better idea? While deployed I should be making around 8500 a month.

CPT M

As a government employee, are you not eligible for TSP while deployed?

If yes, then Roth TSP would be the way to go while you are at 0% tax rate. If not, then Individual Roths. The rest in brokerage

I am eligible while deployed but since I do not pay taxes while deployed I figured there was no reason to put money into the TSP. My thought is to max my ROTH IRA, and my wifes. Then the rest put into a taxable acct?

Max Roth TSP (not Traditional), then Roth IRAs, then brokerage

CPT M, I believe you can contribute up to 53K into your TSP while deployed to a designated combat zone. If you just contribute to the traditional TSP they will automatically designate your contributions as tax exempt. On your TSP statement it should show a tax exempt balance of whatever you contributed in that combat zone.

I deployed several years ago and was able to accumulate a small amount of tax exempt money. When I left the service I was able to make a direct transfer from the TSP to T. Rowe Price and they were able to add the tax exempt amount into my Roth IRA.

The Roth TSP wasn’t around at the time that I deployed, but that may be an easier way to do it. Good luck and be safe.

CPT M, I just read a little further on the TSP website. It says you can only contribute up to the IRS limit of $18,000 for the year into the Roth TSP, regardless of whether the contributions are made from tax exempt money. So I would do the $18,000 into the Roth first and then the rest into the traditional TSP.

https://www.tsp.gov/planparticipation/eligibility/contributionLimits.shtml

I would also look into the DOD Savings Deposit Program. Again, if you are deployed to a combat zone you can deposit up to $10,000 and it will earn up to 10% interest annually.

http://www.dfas.mil/militarymembers/payentitlements/sdp.html

What about someone who is self-employed? A 401k is not available. What would be your next recommendation?

There are at least 3 options, a SIMPLE IRA, a Keogh Plan, and a solo 401k

Here is a link for the Vanguard solo 401k, which is what seems to be the most popular

https://investor.vanguard.com/what-we-offer/small-business/individual-401k

Hello, i just heard about you guys. I live in the Netherlands. Are you familiar with any Dutch people who have figured out how it could work in Holland?

Thank you,

Patrick

Hi Patrick

I haven’t heard of any, but hopefully somebody else has and will reply

Same here for Portugal. I really wish this blog was global and not US only. It would be so helpful. I imagine someone with a blog like that would get rich quickly just w/ ad revenue !

My employer offers a Simple IRA with a 3% match. I’m 29 years old. Would you suggest treating it like a 401k and maxing out my contributions to the Simple IRA vs. contributing 3% to the Simple IRA to get the 3% match, maxing out my Roth IRA, and putting the rest of my savings in a Brokerage Account?

Yes, take advantage of all of the tax minimization options you have. This could mean using a Traditional IRA instead of a Roth as well if your marginal rate is high

Perhaps you’ve already post an article on this, but lets say you have amassed a small fortune enough to live off for the rest of your life by age 40. If it is all locked away in your 401k / IRA, how do you tap it before age 65?

The odds of somebody having that much dough in tax-deferred accounts at Age 40 are pretty low due to annual contribution limits. Typically you would have funds in a brokerage account as well, as in our example. But it can happen.

In that case, there are two main options. Option 1 is 72t SEPP withdrawals (Substantially Equal Periodic Payments.) They are a bit complicated and non-flexible, but allow you to withdraw funds each year without penalties. This is probably best done by people Age 50 and over, since once you start… you must continue annual withdrawals until Age 59.5 or 5 years, whichever is LONGER.

For someone Age 40, the best route is probably a Roth IRA Conversion ladder. The idea is you move 1 years worth of expenses from a Traditional IRA to a Roth IRA each year (a ladder), paying taxes in the process. Those could be zero (see our example.) Once in the Roth, there is a waiting period of 5 years before you can withdraw the funds, so you need 4-5 years worth of spending in a brokerage account to fill the gap. A continuing ladder gets you to Age 59.5 when all restrictions are off.

For more depth, see this post by the Mad Fientist.

Hello! I just finished reading your suggested jcollins stock series last night and had a simple question :)

me and my husband are 27, we have $13,000 in our Roth IRAs total invested in vanguard target 2045 fund. We also have $46,000 in cash in our savings accounts..I know…not smart but we were considering buying a house in cash but have since decided against home ownership. My question/s …I wanted to open a traditional ira now since I see the benefit of tax savings but the vanguard admiral shares have a minimum of 10,000 which is more than one person can contribute to their ira in a year..so how would one go about getting them in their “tax savings vehicle”? Also, do you think it would be wise to transfer that $13,000 in our Roths to a traditional ira now or just leave it and start fresh.

Thank you so much for blogging and sharing! I came across your site at least a year ago and rediscovered it again lol!

You start investing in the Vanguard funds that will accept your minimum contribution. As the fund grows in value, they automatically move you towards the cheaper funds with higher mins.

I wouldn’t transfer funds out of the Roth. If these contributions were recent, you can recharacterize it as a Traditional, but I might only do that if you are above the 15% marginal rate and were going to invest the tax savings.

Jeremy,

Thanks for all your investment knowledge.

I have been cramming all sorts of information into my brain for the last month, your blog, Jim Collins stock series, reading Your Money or Your Life and investigating Vanguard.

I have a million questions that I am trying to get answers for on my own but I do have a question for you.

After we (wife and I) have maxed out our tax deferred accounts for the year are you suggesting that we put the rest of our money into a brokerage account over a Roth IRA?

Thanks.

Awesome, Rob! Way to make life changing steps toward FI

If you max out your tax deferred accounts, you would contribute to Traditional IRAs. In that situation, you aren’t also able to contribute to a Roth, so all additional savings would go to the brokerage account

Thanks Jeremy.

What if my income is to high for a tax deduction with traditional IRA?

Do you think I should skip the Roth and fund my savings into my brokerage account?

For very early retirement, I prefer the brokerage account to a Roth. But… the specifics are highly nuanced

https://gocurrycracker.com/roth-sucks/

If $5500/person is a small percentage of total overall/annual retirement savings, then after maxing out the 401k type accounts you could still do Roth (front or backdoor) and still accumulate savings in a brokerage. In that case, a Roth can be a useful part of the overall portfolio

What about couples who work for companies that don’t gave 401k at all? What is your suggestion in this scenario? My husband and I earn 75k only in total.

A 401k is part of your compensation. If your employer doesn’t provide a 401k, you should receive an above market salary instead, in which case you can contribute to an IRA and put the tax savings and additional savings in your brokerage account. If total compensation still isn’t fair, it might be time to find a new employer.

Your story is so motivating and I’m happy I stumbled upon your blog. Many people don’t take into account the impact of taxes and subsequently suffer the repercussions. Thanks for sharing your story!

Ok, I’m very new to this whole concept of early retirement, maximizing accounts etc. Here is my situation:

I’m 36 years old and am planning on quitting my job in the next 4 years so that I can travel around the world by bicycle for probably the rest of my life, but at least the following five years after retiring.

My finances are currently as follows: I have a Thrift Savings Account (government version of a 401k) with $88,000 and a taxable Scottrade account with $22,000. I have a home that is Zillowed at $180,000 and I owe $75,000 on it. I plan to sell the home at the start of the trip and then invest it all into the same mutual fund I already have.

At that point, my only income will be dividends on my mutual funds. I’m anticipating my annual expenses to be no more than $5,000 (yes five thousand). I would keep enough money out to have $10,000 of cash in the bank to live off of and for emergencies and then every year, I’d plan on selling $5,000 in mutual funds to fund the next year. So in addition to the dividends, I would only be paying takes on the capital gains of each mutual fund sold correct (ie, if I sold 100 shares that were bought at $35 and sold for $50, I’d be paying tax on $15/share or $1,500 total). With a standard deduction of $6,300 and a personal exemption of $4,050, that would mean I’m paying zero tax on the capital gains and that I’d still have room for ($6300+4050-1500=8850) $8,850 that I could convert from the “401k” through a Roth conversion ladder and still pay a total of zero taxes. Correct?

For what it’s worth, I guess I should add that during the next four years, I plan to max out my contributions to the “401k” at $18,000/year and add $6,000/year to the Scottrade. I’m also planning to have the house paid off by the start of the trip, just in case I’m unable to sell it and am forced in to being an absentee landlord, thousands of miles from the home and unreachable by phone for weeks at a time (I really don’t want to keep the house!)

Qualified Dividends and Long Term Capital Gains would be taxed at 0%.

So you could do a Roth conversion of the full $10,350 (std deduction and one personal exemption.)

If your working income is enough to require you pay tax even after a max 401k contribution, you could consider putting $5500 in a Traditional IRA rather than the taxable account, since you will be paying 0% tax later.

Love the blog.. I am a 23 year old single woman. I feel like a lot of this is over my head because it references married couples etc. I make over 55K, my desire is to turbo charge my savings and be able to retire early (although I likely won’t, because I love to work). There aren’t many <25 somethings that are looking into financial investing and I find myself lost reading articles all of the internet. Should I seek a financial advisor? I'd hate to go to one and they play on my youth and get me to buy a whole bunch of things I don't need…

I would read through Jim Collins’ stock series. Two hours of reading will put you ahead of many financial advisers.

In addition, a great book to read as an intro to investing is the Boglehead’s Guide to Investing, which can usually be found in your local library.

It is not a bad idea to see an advisor that specializes in advice rather than sales. they all aren’t trying to separate you from your money. i would start off the conversation with what you are looking to accomplish with the meeting and make it known that you aren’t buying any commissioned products. They usually charge by the hour and a 1 or 2 hour meeting may be worth your time. You may either find that it was a complete waste of your time and money and you are out a couple hundred dollars or you may find what you are currently doing is not the most efficient use of your money and well worth the time and expense. penny wise, pound foolish.

I’m a stay at home mom. How much income would I need to bring in to he able to add the $17,000 into a 401k? We are going to figure out to how to max this out this year. Is there a minimum income? We are just deciding to start this journey me 38 my husband 42 it’s never too late right?! So many things to consider and calculate. I just recieved from ebay “Your money or Your Life.” So many questions! Last student loan $35k @ 3.8%. Paid off $25k+ this year. Pay off or add to 401k?

Hi Joy, welcome

You are right, it is never too late. Plus, building wealth is a good idea at any age.

You can contribute either the legal 401k limit ($18k in 2017) or total earned income, whichever is LOWER.

Extra loan payments vs additional investments is always a tradeoff. Read through YMOYL and see if that pushes you one way or the other. That book will answer a lot of questions.

Good luck!

Jeremy

I’m late to the party, but I have a question.

I am at a lower income than most people pursuing early retirement. I’m 27 and am making 38k a year with a 5% 403b match. I previously was investing in a Roth IRA. I live in a HCOL area but am very frugal and try to earn extra cash in various ways.

Are you saying it’s best to max out your 401k instead of investing in stocks directly through vanguard? Is the best plan for someone in my situation trying to build wealth to invest in this way?

Yes. 401k contributions would save 15% tax now, and expect to pay 0% in early retirement.

Gocurry, have you considered retrospecting / updating some of these past articles? Maybe reposting with new tax numbers. Could be a relatively easy way to get ‘new’ posts.

I haven’t really, no. The concepts are ageless.