Trinity University: Birthplace of Early Retirement Research

So you want to retire. Perhaps even earlier than most people.

Sounds like a great idea. But… How much (or how little) money do you need? $500k? $1 million? $10 million? What is your retirement number?

Pick a number that is too low, and you might end up begging for change, working at Wal-Mart, or worse. Pick a number that is too high, and perhaps trade years of life working for money that will benefit only your heirs

Determining the right amount starts with some basic questions

- How much does your target retirement lifestyle cost?

- How long do you expect to be retired? 15 years? 30 years? 60 years? More?

- How many dollars do you want to leave to your children or to charity?

Each person will answer these questions in their own way, with no answer necessarily better than another

“I plan to retire at the age of 57 with a cost of living of $10,000/month, mostly for golf club membership and my wine collection. Society never gave me nothing, and I’ll return the favor.”

“We will retire in our 30s to travel the globe, which we estimate will average around $3,000 per month. Ideally we will leave behind a large endowment to fund charitable hospitals”

There are other important questions that are more subtle and nuanced

- Do I have to change my shorts every time the stock market drops?

- Am I so set in my ways that I will refuse to make life changes regardless of the cost?

“Wow, 2008 was a wild ride! Stocks dropped 50%, but businesses took advantage of opportunities and made changes to enable future growth. Next time that happens, if our cash flow isn’t what we would like we can spend next year in South America instead of Europe”

“I don’t care what it costs, I’m driving the stretch RV to Florida every winter and dining on steak and lobster every night! And those Wall Street guys are crooks! No way am I putting my money in the stock market”

Somebody with low risk tolerance and great resistance to change will need a larger bank account than somebody that goes with the flow and enjoys a bit of excitement.

For better or worse, the older we get the less any of these things matter. But for somebody that plans to retire extremely early, all of these factors are of utmost importance

With all of this complexity, no wonder every bit of retirement advice in the press seems contradictory or not actionable.

Fortunately, some really smart people found a way to cut to the core of the question, “What is your retirement number?”

The Trinity Study

In the 1990’s, a key retirement planning study was published by three Professors from Trinity University, often referred to as The Trinity Study.

The Trinity Trio essentially asked the question, “Had we retired at any time in recent history, how much could we spend annually for 30 years without running out of funds?”

The original Trinity Study looked at rolling 30-year periods between 1926 and the end of 1995, and was later expanded to include data through 2009, a span of 84 years that covers a wide range of economic environments including 2 World Wars, the Great Depression, the oil embargo and high inflation period of the 1970’s, and the Boom period of the 1980’s

Their conclusions:

With a portfolio of at least 50% stock and a little flexibility, plan to spend 4% of the initial portfolio value, adjusted for inflation each year, and have a high degree of confidence the portfolio will survive at least 30 years, and often much longer

This is commonly referred to as the 4% Rule or the Safe Withdrawal Rate (SWR)

In other words, build a portfolio of 25x your target annual spend and you’ll be able to keep a constant standard of living throughout your retirement

If your target annual spend is $40,000, then your retirement number is $1 million. Want to spend $80,000 per year? Your number is $2 million

If you are extremely conservative, at most save up 33x your target annual spend (a 3% withdrawal rate.) The likelihood of joining the Forbes 400 late in life will increase substantially, but starting retirement with this level of wealth is about as close to a guarantee as one can get

For most people, that is really all of the planning necessary. Simple, effective

We aren’t most people though, so let’s dig deeper

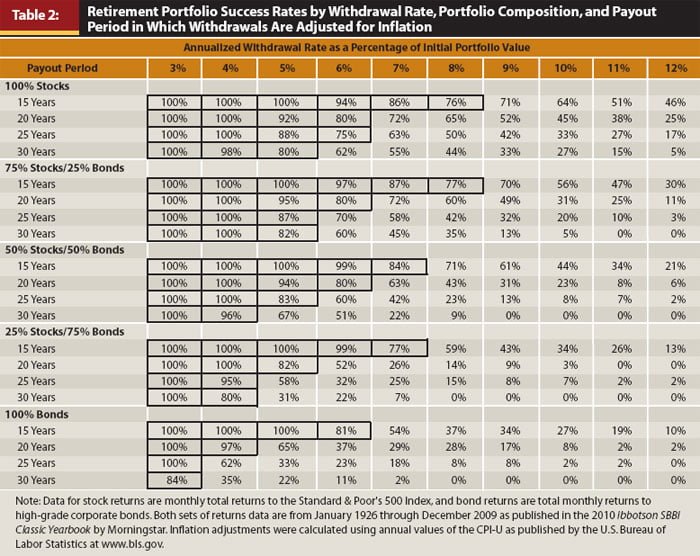

Trinity Study Data

The core results of the Trinity Study are in the Table below, which reports how many of the possible retirement periods in the 84 year study period still had assets remaining after a period of up to 30 years

One example that may help with reading the table: A retiree with a portfolio of 50% stocks/50% bonds, withdrawing 4% a year and adjusting for inflation, would have assets remaining after 30 years in 96% of the cases studied

The mainstream media took this report and reduced it to a simple sound bite. “A retiree can blindly withdraw 4% of assets every year, adjusted for inflation, and be 100% confident that they will run out of life before they run out of money”

The Trinity Trio was never as confident as the press, however:

What, then, can be done to help an investor in planning for a withdrawal rate? The word planning is emphasized because of the great uncertainties in the stock and bond markets. Mid-course corrections likely will be required, with the actual dollar amounts withdrawn adjusted down-ward or upward relative to the plan. The investor needs to keep in mind that selection of a withdrawal rate is not a matter of contract but rather a matter of planning

Sometimes people on the Internet like to argue about the conclusions, but it’s just math. This method worked in the past is just as true as I had eggs and bacon for breakfast today. Those are the facts.

But to be reasonable, remember the 4% Rule is a Rule of Thumb based on experience, not a Law of Nature. It is the base of a plan

What is Success?

But wait! A 96% success rate isn’t guaranteed, how can they call that safe?!

This is a pretty common reaction, and many people make an immediate commitment to build an extra large portfolio so they can spend much less than 4%

But how long would it take to grow your portfolio to support a 3% or 2% withdrawal rate, years of life that themselves are not zero risk? And after working an extra 10, 20, or 30, years, wouldn’t it be a bummer if it didn’t really make a difference?

If we required 100% safety in all things, we would never board a plane, never eat a medium rare steak, and would wear a helmet and life jacket 24 hours a day.

“I’m planning for a 2% withdrawal rate,” said Larry Feegan

For someone that has built wealth through living below their means, investing the difference, and patiently watching their wealth grow, the odds of a portfolio failing catastrophically is about equivalent to the odds of death by a cow falling on you while asleep in your own bed.

Sure it happens, but it is nearly pointless to plan for it (but if there is interest, I will do some posts analyzing the failure cases… #financialporn)

And worth mentioning, pretending that we are signing up for something with a 96% historical success rate is full of false confidence. Any number of unknowns could occur, ranging from an asteroid smashing into the Earth to the Simian Flu wiping out 80% of the world’s population to a terrorist setting off a nuclear bomb in downtown Manhattan. More money doesn’t save anybody from the real dangers

Even a 4% withdrawal rate will be too conservative in most cases.

Look at this other Table from the Trinity Study, which shows the median terminal value for the 55 retirement periods studied.

How would you like to spend 30 years living the good life, enjoying a constant standard of living throughout your retirement, and then look at your portfolio to find not only had it not disappeared, but it MORE THAN TRIPLED! Your children will love it even more than you do

How would you like to spend 30 years living the good life, enjoying a constant standard of living throughout your retirement, and then look at your portfolio to find not only had it not disappeared, but it MORE THAN TRIPLED! Your children will love it even more than you do

For the 50% stock / 50% bond portfolio with 4% inflation adjusted withdrawals, which had only a 96% success rate, this was the case half the time

Even at a 5% withdrawal rate, the median value of a 50/50 portfolio after 30 years was nearly 1.4x the beginning value. For a 5% withdrawal on a 100% stock portfolio, the median terminal value was over $7.2 million

Don’t get too caught up in striving for 100% safety (an impossible feat.) The only thing 100% guaranteed in life, is death (not even taxes)

Success is not a number in a Table from an academic study

Trinity Study Methodology

If you are like me (and you probably aren’t because I love data and Excel spreadsheets a little too much) then the Tables from the Trinity Study probably aren’t exciting enough. You want to see the data behind the data

So I recreated the interesting parts of the Trinity Study in Excel, using historical data from Robert Shiller, and validated against results from cFIREsim.

Viewing things graphically makes it easier to get an intuitive feel for the data, so let’s look at the source of the results shown in the Tables above

Starting with the case of a 4% initial withdrawal rate on a portfolio of 75% stock / 25% bonds, we model a 30 year retirement that begins in 1926. We withdraw the initial 4% for spending, adjust the stock and bond values based on market returns for the year, add dividend and interest income, and rebalance to the original asset allocation. Then we repeat for Year 2, but this time with a higher withdrawal amount to account for inflation. This is then repeated for each year up to Year 30

The portfolio value for the 30 year period starting in 1926 looks like this

Retiring in 1926 with $1 million, 75% bonds / 25% stocks, 4% withdrawal adjusted for inflation. Terminal value = $3.75 million

Repeating this for 30 year retirements starting in 1927, 1928, and 1929 provides the following chart

We can see that the economic conditions of each 30 year period are very different. Retiring in 1926 had several years of stock market growth before the Great Depression, whereas a retirement starting in 1929 was hit immediately with the major stock market plunge on Black Tuesday. In all 4 cases however, drawing 4% of a 75% stock / 25% bond portfolio would provide a comfortable retirement for the full 30 years. In the grand scheme of things, for a retiree living off a portfolio the Great Depression was anything but depressing

We can see that the economic conditions of each 30 year period are very different. Retiring in 1926 had several years of stock market growth before the Great Depression, whereas a retirement starting in 1929 was hit immediately with the major stock market plunge on Black Tuesday. In all 4 cases however, drawing 4% of a 75% stock / 25% bond portfolio would provide a comfortable retirement for the full 30 years. In the grand scheme of things, for a retiree living off a portfolio the Great Depression was anything but depressing

Looking at all possible 30-year periods we can get a sense of which economic periods were most challenging with an initial 4% withdrawal rate, and also which ones resulted in a ridiculous amount of wealth

Now that we can see what actually happened in the past, we can start to do some interesting analysis and figure out how to boost our success rate without sacrificing many more years to working

Hacking the Data

There are some simplifying assumptions built into the Trinity Study that result in a reduced success rate and/or reduced safe withdrawal rate. No Social Security. No future income. No reduction in spending. No flexibility

To account for the differences in individual behavior, the Trinity Trio set some rigid rules, namely that each year’s spending would be exactly the same when adjusted for inflation, no matter what. When was the last time you spent the exact same amount 2 years in a row? The concept of homo economicus was simplified to a robotic existence.

And how many people would retire in 1929, watch the stock market suffer one of the largest declines of all time, and then think to themselves, “The Trinity Study says 4% is safe, so I’ll just pretend everything is fine”

Not me, not most people. We would do what people do in life, adapt

These same adaptations apply even in good times. What young person with unlimited free time isn’t going to earn a little extra income? Even $100 a month increases the Median terminal value for a 75/25 portfolio by $150k.

Despite the scare mongering in the press, even Americans who work only 10 years will still receive some Social Security income in return for their years of paying into the system. The likelihood of some additional income is quite high

Flexible spending also has a major influence. If 2008 happened all over again, instead of vacationing in Paris that year, perhaps go to Lake Atitlan, Guatemala, one of the most beautiful places we’ve ever been (Yes, it’s safe.)

Sunrise Over Lake Atitlan

Life is full of flexible spending opportunities. Perhaps you still use a car from time to time, and can extend the replacement cycle from 10 years to 11 if the economy is suffering. Or maybe only upgrade to the iPhone 19 when the iPhone 20 is announced

And then there is Ty Bernicke’s research, which shows people naturally spend less as they age. Apparently nobody cares what brand of jeans they wear at Age 75, and even Jerry Seinfeld’s parents would dine early to get the early-bird special.

Jerry: (bewildered) Four-thirty? Who eats dinner at four-thirty?

Morty: By the time we sit down, it’ll be quarter to five.

Jerry: I don’t understand why we have to eat now.

Helen: We gotta catch the early-bird. It’s only between four-thirty and six.

Morty: Yeah. They give you a tenderloin, a salad and a baked potato, for four-ninety-five. You know what that cost you after six?

Jerry: Can’t we eat at a decent hour? I’ll treat, okay?

Helen: You’re not buying us dinner.

Jerry: (emphatic) I’m not force-feeding myself a steak at four-thirty to save a couple of bucks, I’ll tell you that!

Helen: All right (sitting on the couch), we’ll wait. (pointedly) But it’s unheard of

But all of this is secondary to one very powerful hack. Wade Pfau has perhaps done more than anyone to embrace and extend the Trinity Study, and has concluded:

…the wealth remaining 10 years after retirement, combined with the cumulative inflation during those 10 years, can explain 80 percent of the variation in a retiree’s maximum sustainable withdrawal rate after 30 years

In other words, if you can make it through the first 10 years without severely depleting your portfolio or inflation going out of control, your portfolio is likely to enter Too Big to Fail territory. I’ve never heard better news, because I’ve always wanted to be a Bank

But let’s be crystal clear. Even if we do none of these things, with a 4% initial withdrawal rate, in nearly all cases we die ridiculously wealthy

Foundation for Long Term Success

Because the early years are critical, it would be worthwhile to at least consider using that time to lay a foundation for long term success. We can’t do anything about inflation (directly), but we have great control over most everything else

If world travel is of interest, why not start traveling in Latin America or Southeast Asia instead of Japan, Western Europe, or Australia? With a possible 60 year retirement, there is plenty of time to go everywhere and see everything, but front-loading the low cost of living countries will minimize portfolio withdrawals, the lower the better. This isn’t a sacrifice or even being frugal, it is just living large where it costs less to do so. Perhaps it would even be possible to live solely from dividend and interest income

To further reduce costs, while still working we can hack Credit Card rewards to load up on Frequent Flyer miles and Hotel Rewards points, in the same way that we build up our stock and bond portfolio. Consider it another asset class. This will allow us to fly and stay for free in the early years

Because all taxes and Mutual Fund fees are part of our overall withdrawal rate, minimizing these is critical. Aggressively managing taxes and investing in a low cost way mean less of a load on the portfolio. Consider that a typical 1% fee that might be paid to a financial adviser is 25% of the total budget for somebody living on 4% of a portfolio. By contrast, our total load is less than 0.08% (based on Personal Capital Retirement Fee Analyzer)

Having grand adventures means great stories and great photos. Perhaps you might type some of these stories into a computer or allow an online travel site to use your photos. Besides being great fun, it might even generate some accidental income. There are 7 billion different ways to make a little income, unique for each individual on the planet

If a nightmarish economy and stock market collapse lays waste to your stock portfolio, be ready to sell all of your bonds and buy stocks while on sale. The bonds did their job of reducing volatility in the early years when it mattered most, and having a 100% stock portfolio has historically provided the best long term growth and largest terminal value

If things are really bad, it would even be reasonable to go back to work for a short time. Some random people on the Internet will say ignorant and hateful things if you do, but nobody will ever make a movie about them. You on the other hand are pursuing your dreams. I’ve already reached out to Brad Pitt and Angelina Jolie to co-star in the Go Curry Cracker film

Coming to a Theater Near You

Winnie: “Where should we start our world travels?”

Jeremy: “How about Latin America? We can live like royalty for pennies and let our portfolio continue to grow”

Winnie: “But isn’t it dangerous?”

Jeremy: “Don’t worry baby, we have guns”

Summary and Conclusions

Based on the excellent research done by the Trinity Trio, we have great data to use for planning an early and extended retirement. By digging deeper into the data, we know we can safely plan on a 4% initial withdrawal rate to determine our retirement number, as well as make plans to boost the already nearly guaranteed success rate and/or increased spending over time

- Plan on a 4% withdrawal rate

- Spend less in the early years, the lower the better

- Minimize taxes

- Travel hack for free flights and hotel stays

- Minimize investment costs through Vanguard index funds

- Earn a little accidental income

- Be prepared to move bond position into stock in a severe downturn

- Be OK with going back to work for awhile

If you’ve read a little Go Curry Cracker in the past, this probably seems very familiar (yes, I’m one of those conservative people I made fun of earlier)

PS

You have to have a lot of respect for the Trinity Trio, especially considering that the iPhone 6 processing power is at least 10,000x greater than a PC from the 90’s, and that most data was probably entered by hand from books.

What probably took them years, we can do now in seconds, and for a substantially wider data set. For this, check out cFIREsim and do your own Trinity Study.

Thanks for this classic post!

I’m not planning to travel, but starting with the cheaper countries is a very good suggestion.

The biggest insight for me was the first ten years period. This is also the period where one’s job skills are still fresh. So it really should be possible to earn a few extra dollars.

I like this. Thank you.

Question regarding travel hacking: do you find it’s still possible to get new credit cards for awards after retiring and showing little to no income? Or are credit card companies more interested in your total net worth than your salary?

I’ve applied for 2 (or maybe 3?) cards now where we said, Occupation = Retired. 100% approval rate so far

Even though your income is not “earned” in usual manner, you still have money coming in. I am sure that you are much more responsible in the eyes of the banks than many people who work a job to earn their money. I really enjoy your blog. Your seem to be living the dream that so many people desire. Good for you. Keep us updated.

Keep cranking,

Robert the DividendDreamer

Yeah, I’m sure we are viewed as a good credit risk. No idea what our credit score is

Love the inspiration you are giving me to think on this. For us, we hope to do the following – move/work/live in our ‘dream retirement place’ before we officially retire. Incorporate 2 mini-retirements of 12-weeks of travel, then officially retire in 12 years. Since we have 4 kids, all at various ages, this gives us a ‘live’ now ability and a reasonably early retirement by the time we turn 56 years old. I wish I’d started this journey in my 20’s like you did!

sounds like an awesome plan

Dude, excellent summary of the “4% rule”!

I’ve looked at the data pretty closely and came to the same conclusions as Wade Pfau (without realizing it) that taking a look at where you are in year 10 of your retirement withdrawals is a pretty good indicator of how things will turn out. If you don’t have around 60%+ of what you started with, then you’re probably not going to have a very successful early retirement.

Which brings us back to “flexibility”. Flexibility in what you spend the first 10 years to let your portfolio grow into a perpetual snowball able to roll over any portfolio bumps you might encounter. And flexibility in earning and spending after the first 10 years based on how you’re doing in real time.

I’d much prefer an extra decade or three of retirement at the expense of being a little flexible. Ain’t nobody got time to get to a 100% success rate (which is a fallacy anyway as you point out).

Cheers to you for pulling all this info together while simultaneously having a newborn baby rapidly filling diapers.

I wrote most of this about 7 or 8 months ago… and then this week 5 minutes at a time over 5 days. Anything that requires real thought takes a loooong time right now…

My personal goal is for net worth 10 years in to be higher than when we started, but that is just because I want to leave a large endowment for egotistical reasons. It would be cool to look down from the heavens and see people say, “WTF! Why is this hospital called Go Curry Cracker!?”

I take this as an acknowledgement that GCC Jr. made it safely into the world…Congrats!

Also, Go Curry Cracker Hospital would be hilarious. Mandatory GCC tattoos in exchange for free treatment?

there is a photo on twitter, http://www.twitter.com/gocurrycracker/

I’m working on the logo and love this idea

Cute kid, turned out a lot better than your April 1st photo mash up….thank goodness :)

Yes, fortunately for everyone he looks more like his mother

I understand and sympathize. It takes me twice as long to write anything when there is a kid crawling on me and asking me for things. Just gotta learn to hold a bottle in one hand and type 60 wpm with the other hand. :)

Or “Uhh, Winnie, can you handle this little ball of joy for an hour or two? I need to crank out some magic on the keyboard” might also work occasionally.

How’s she doing? Fully recovered from the delivery?

Still a work in progress, but we go home tomorrow

How does having money (stocks, etc.) in retirement accounts vs standard taxable accounts affect things. If retiring early, does one live off taxable accounts and then move to retirement accounts when the time comes?

I am 44 and seriously starting to think about retiring.

It partially depends on the Age of retirement. At age 59.5, access to 401k / Traditional IRA is unrestricted so no problem.

Before that, there are different strategies. The overriding theme though is just get to your retirement number. Using tax advantaged accounts helps one get there faster https://gocurrycracker.com/turbocharge-savings/

Upon retirement, if one has zero funds in a taxable or Roth account, then an SEPP can be used. Or if up to 5 years of expenses in Roth contributions and Taxable then a Roth IRA Conversion ladder can be used

http://jlcollinsnh.com/2013/12/05/stocks-part-xx-early-retirement-withdrawal-strategies-and-roth-conversion-ladders-from-a-mad-fientist/

We are primarily living off our taxable accounts, since with high income and high savings rates the limits on 401k / IRA contributions are too low

I intend to write a post about this, it is on my list

Great. I’ll keep an eye out for your post about this topic.

I too have the very same question. I look forward to the post as well.

I was just scanning your archive to see if that question was already answered. Will be eagerly watching for your future post on it. Congrats on GCC Jr! Still have quite a ways to go to retire early, but started worrying that focusing almost everything into a SEP IRA (52k contribution limit!) instead of some in taxable would screw things up.

I would like to say right now that if a cow does fall on me while I am sleeping in my bed I hope my poor family sells the movie rights and lives happily ever after. Until that does happen I plan to stick with the 4% withdrawal plan.

Oh, and stop telling people to go to Central America. It is dangerous. Just look at what happened when I went to Baja: http://www.johnpedroza.com/blog1/why-you-should-never-go-to-baja-california-mexico/

Yessir. Mexico is dangerous

https://gocurrycracker.com/mexico-_is_-dangerous/

Another great nugget. I had to add that post on Dangerous Mexico and your other post on They’ll steal your shoes! to my own Dangers in Mexico post. :)

Ah yes Central America and Mexico is so dangerous. Yup, can’t ever visit there/sarcasm off. I certainly understand that people see the news and see bad things going on in El Salvador and Honduras, but most of the countries are safe. I love traveling there and Panama is a great place to retire.

I’ve always been nervous for planning a 4% withdrawal rate in early retirement, and thought maybe 3% would be more safe. But you’re convincing me more and more that I don’t have to work those extra few years to get there! Thanks!

3% is safer, 2% even more so. But a portion of that just comes because the portfolio doesn’t need to last as long because you had many more years with an income

People tend to focus on the failure rate (4% or whatever) and ignore the part where if the Roulette wheel in Vegas had a 96% success rate then we would all be billionaires and Oceans 11 would have been a really boring movie

I am trying to figure the “rule”, so a simplistic way is to just say ok I wanna live off $30k per year so multiply that by 25, and then 33 for conservative, to get the range I should need? I feel like such a dummy trying to figure it out. But at those #s it saying I only need $750k to $990k to last 30 yr retirement. If true this is so much less than the scary news stories saying I need millions! I will reread this article and check out the links but was hoping you could see if my math is close or correct.

You got it. It really is that simple

I was considering living in Panajachel for six months to get fluent in Spanish, but life intervened and I never did.

In the time I was researching it I discovered many expats living there at a fraction of the cost of living in the USA. If you were to live in that area, you could conceivably withdraw much less than 4%, correct? I heard of some people who got by and lived like royalty on their SS payments.

I’m sure there’s a fly in the ointment someplace, because that just sounds too easy?

Life in Panajachel is pretty nice. We spent less than $2k/month while in Guatemala, and I imagine we could do it longer term for half that. We loved the area

The Kaderlis have been spending time there recently

http://www.retireearlylifestyle.com/panajachel.htm

First you give the Mad Fientist a run for his money as the most tax-savvy early retirement blogger out there. Now you’re doing the same for MMM in terms of plain-spoken demystification of the shockingly simple math behind the 4% Rule. Bravo.

One nitpick: thanks to some friends in the MMM forum, it has become clear to me that (like taxes) even death is no longer certain (perhaps within our own lifetimes):

http://waitbutwhy.com/2015/01/artificial-intelligence-revolution-1.html

If anybody is going to nitpick, leave it to brooklynguy haha ;)

I read the Ray Kurzweil book, Fantastic Voyage: Live Long Enough to Live Forever , which essentially states that if you remain healthy long enough you will still be alive for the technology revolution that will allow your brain to be uploaded to the Internet, and you thereby live forever

, which essentially states that if you remain healthy long enough you will still be alive for the technology revolution that will allow your brain to be uploaded to the Internet, and you thereby live forever

It could happen.

Great summary of the 4% rule. Most FI’ers could probably easily do with a 2.5-3% rule considering at some point their hobbies are going to produce some legitimate side income.

OK, now this one is my favorite GCC post.

Extraordinarily well done, and now an addendum to both of my own Stock Series post on the 4% rule. :)

First: this is an instant classic post. Totally foundational for a soon-to-be early retiree like me.

I’ve read that the planning is a little shakier for an early retirement, as the time period is much longer.

http://www.hullfinancialplanning.com/how-much-do-you-have-to-save-to-retire-early/

http://www.hullfinancialplanning.com/is-4-the-correct-safe-withdrawal-rate-at-retirement/

We need to dig into the planning a bit more, since the money will have to last twice as long.

A longer retirement is definitely riskier than a shorter one. Some of the successful 30-year retirements in the Trinity Study become failures if they need to last another 10, 20, or 30 years. For an extremely early retiree, it is important to stay aware. As the Trinity Trio said, “The investor needs to keep in mind that selection of a withdrawal rate is not a matter of contract but rather a matter of planning”

If you are lucky, you retire at the beginning of a bull market while committing to the GCC Live Well for Less philosophy in those early years. Then the portfolio truly can become Too Big to Fail, as actual withdrawal rates drop

I’ve previously said that I worked 3 years too long, but only became aware of that in hindsight. Those 3 years were 2010, 2011, and 2012, and it wasn’t yet clear which direction the economy was headed and if TARP and QE were going to be successful.

This is all to say, we were just extremely flexible in exact retirement date, as well as our budget and where we started our travels

When I run FireCalc I usually set it to 60+ year retirements. That should help model more of the risk I would think, as there would be multiple dips in that long of a period? Does my thinking make sense, or should I be using the standard 30 year period?

For the Monte Carlo Analysis, it is basically the same, just more random years

For the default rolling window sequence-of-returns analysis, it needs a full 60-years worth of data to do 1 cycle, so the last full cycle begins around 1955

For 60-year analysis, I typically do 30 years and look at terminal value, focusing on at least parity to day 1, although that is very conservative

At first thought parity to day 1 sounded conservative and reasonable, but then I was thinking you would have experienced 30 years of inflation, so your spending year 31 would be significantly higher than year one, but with potentially the same portfolio size. 40k turns into 97k @ 3% inflation, so I’m thinking parity to day 1 may not be enough to sustain 30 more years (although there are lots of variables such as decreased spending with age, more or less inflation, etc)

cFIREsim reports terminal values in inflation adjusted dollars, so inflation is already factored in

In essence, my splitting the two 30-year periods apart requires redefining success for the first 30 years as achieving parity. Naturally the success rate is much lower (~20% lower)

Most of those failures occur because they fail the “did well in first 10 years” test

Thinking through this is what led me to focus on the early years in the first place

FYI, “parity to day 1” is what Dr. Doom wrote about (in typically excellent fashion) (and referred to as “living above the line”) here:

http://livingafi.com/2014/06/03/drawdown-part-5-validation/

Which led to some great related discussion in the MMM forums here:

http://forum.mrmoneymustache.com/welcome-to-the-forum/when-fire-plans-go-wrong-your-experiences/msg572455/#msg572455

Great summary. I wasn’t previously aware of Wade Pfau’s work saying that the first decade accounts for 80% of your portfolio’s variation. While unsurprising, it’s also sort of crazy! Articles like these just keep making it easier for people to achieve FIRE. As you say, flexibility is key. Thanks for the write up.

Also, I love the Larry Feegan reference. Too bad ol’ Larry ended up in the 4% failure category, rather than the 96% success. Lol.

Poor Feegan the Vegan only failed because he abandoned his plan due to peer pressure. Had he continued to wear his life jacket, he would still be with us today :) Stay the course!

The first decade factor makes a lot of sense. If you’re lucky you retire into a bull market and assets continue to grow

Haha, too true. Stay the course. No one would retire early if they gave in to peer pressure.

“Just take the life jacket off, Larry. You’ll be fine!”

“You don’t need to save so much. You’re young; you’ve got plenty of time to save for retirement.”

As they say, art imitates life :)

Fantastic summary, great to have it all in one spot, and it even includes some additional analyses! Now we just need to figure out how the complex and expensive Dutch tax system is going to fit into all this……

Oh, looking forward to the Go Curry Cracker film!

Keep Cracking.

What an awesome post!

I am from India. I live Indian middle-class life with approximate expenses of $10000 per year, paid for apartment and no debts whatsoever. Looking at your post I think I will be FI if I reach $300K in net worth. Inflation in India is fairly high but so are the returns from Indian stock market.

This gives me so much confidence to do something worthwhile in my life, instead of working for money and waiting to die. I can at least take up a job that pays less but I will enjoy.

Excellent post – I’ve read about 100 articles that discuss the 4% rule and yours is one of the best. This is the first I’ve seen of the “10 year rule” and it’s an excellent comforting thought.

Thank you Jason, very kind of you. I’ve read a lot of 4% Rule things myself, so that really means a lot

Wow, well done! I always enjoy a well-written withdrawal rate post. This one was excellent.

As for your statement “(but if there is interest, I will do some posts analyzing the failure cases… #financialporn)” – I say yes, please. I froth at the mouth when reading this stuff. Results where CAPE ratios are high would be especially interesting.

I am personally shooting for a 3% withdrawal rate. Partly because expenses while raising kids and health expenses are unknown but mostly because I’m a big financial wuss.

Nothing wrong with being a big financial wuss. I’m one myself

I read a great article recently (but can’t find it) about how according to the PE10, stocks have been overvalued for the last 40 years. I’d hate to be the guy sitting in cash all that time waiting for stocks to become “fairly valued”

I’ll add high CAPE ratios to the list. I think my first in depth review will be about the failure cases of the mid 60s

Very comprehensive article.

Since getting into the PF space I have seen a lot of talk about the 4% rule. But this post has really done a fantastic job detailing the idea and expanding on the original idea.

Time to go start a new spreadsheet :)

Thanks!

Excellent post. I’m nowhere near determining my retirement number at this point, but I’ve always been fairly conservative when it comes to investing. It took a lot for me to make the plunge from savings accounts/CDs to index funds. I like your thoughts on targeting the 4%, instead of waiting for a 3% withdrawal rate. You can always adapt and be flexible with your plan, but you can’t make up for that lost time if you “over save”

Flexibility is critical

I have another post on the To Do list about why you absolutely must make the plunge from savings accounts/CDs to index funds. I think you will like that one

You should take a crack at figuring out your number, it’s enlightening. The first step is understanding your annual expenses (which is a great thing to do anyway). From there it’s just simple multiplication.

Looking for some advice from the people…

I’ll be 27 years old next Monday and currently have about $50k outstanding on my mortgage (and about $80k in equity). My assets include $45k in a taxable brokerage account invested in dividend paying stocks (with flexible reinvestment setup where I take the dividends from all of my stocks and on a quarterly basis reinvestment 50% each in the two biggest losers % wise), $70k in 401(k)s/IRAs and $10k in cash, which equates to about 6 months of expenses. Also, after maxing out my 401(k) contributions and saving up for my 2016 IRA contribution (2015 was already made) I net about $2,300 in cash from my paycheck and about $750 after monthly expenses, not including any additional principal mortgage payments.

So my questions is factoring in all areas of my situation, do I continue to aggressively pay down my mortgage at say an additional $500-$750 a month to where the mortgage would be paid off in the next 3-5 years but limit my ability to add to my taxable account or do I take my additional mortgage payments down to $0-$250 and use the difference to continue to build my taxable brokerage account? 401(k) and IRA contributions will be maxed out either way.

If I continue to aggressively payoff the mortgage and get it paid off in the next 3-5 years then at that point the savings from not having a mortgage would go towards the taxable brokerage account or possibly municipal bonds depending on how interest rates look at that time.

P.S… The goal is semi-retirement at 40. Ditch the Corporate world and join the ranks of you legends haha :)

Thanks for any advice in advance!

There is no right answer.

If you think paying off the mortgage fast is best, take your $45k brokerage account and $5k of cash and pay off the mortgage today. Done

Depending on how you respond to that idea at a gut level, you know which route to take

Appreciate the advice.

I think the standard logic is that you should compare the interest you’re paying on the mortgage and compare it with your projected investment returns. There is also the tax write-offs, and inflation to consider here is a post that may help: http://retireby40.org/pay-off-mortgage-or-not/

I like GCC’s response though, as there isn’t one right answer and his approach takes your personal feelings into account. Eight months ago my plan was to pay mine off in 7 years, current plan is to just make the standard payment and invest the difference.

Thanks for the excellent post on such tricky topic. I’ve read in some books suggesting have a more conservative withdraw number and adjust that number depending on how well the markets are doing. I think your withdraw rate early in your retirement year will have a huge impact on how long the fund can last.

Wow You really are an amazing numbers geek! And thank goodness because you translate the geeky stuff so well that those of us- like me- that get overwhelmed by all the data can really understand it.Thank you for all your work.

This might be the best compliment I’ve ever received :)

Great article, thanks!!

Great post Jeremy, you are so smart and thus help us slower people and I really appreciate your work! I am the biggest financial wuss, maybe it was my being raised by depression era parents (my Dad would make me straighten every nail I bent and use it – even when there were a 1,000 more in the bucket). I am one of those who may just be more comfortable working a few more years than worrying, although I have really relaxed more since being infused with knowledge from you and Uncle Jim (JLCOLLINSNH).

Maybe I missed it but “what if” the next 100 are no where near as good as the last 100 years? Again see the worry and conservatism.

BTW my wife and I are doing Europe each summer now while we still work and will see those “less expensive areas” once we retire. Man talk about over saving I think we will be able to get by on a 2.5% and be lavish at a 3% withdrawal rate

Once again thanks for all you do!

Hi Mark

If I seem smart, it is only because I’ve read the analysis and research of people much smarter than me, and want to be sure I’m right as the future stability of my family depends on it

Your story of hammering bent nails reminds me of my grandfather, who definitely knew how to eliminate waste and reuse anything.

As for “what if” my best recommendation is to stop watching television. If you look at all of the trends that matter (cost of food, cost of energy, human productivity, advances in medicine, computing, etc…) the world is trending towards utopia. That is boring though, so TV news shows death and destruction

Check out this TED talk, and how the entire developing world is approaching parity with the Western World. Now imagine how easy it is to make $1 in profit from 1 billion people, and the economic opportunities are endless

https://www.ted.com/talks/hans_rosling_shows_the_best_stats_you_ve_ever_seen

I could probably explain that better, but… sleep deprivation…

At a 2.5% withdrawal rate, you are at the edge of living solely from cash flow from the portfolio, and would never have to sell shares. Forbes 400, here you come. If you aren’t “safe” with that withdrawal rate, more money won’t really protect from the problems to come

Jeremy

Hans Rosling’s TedTalks sure turn conventional wisdom on it’s head. Thanks for posting the link and talking me down the rabbit hole of about 10 of his talks on the TedTalk website.

Hi Jeremy! Long time reader first time poster.

Great actionable post!

I’m considering a move to Kaohsiung, Taiwan for my early retirement and have estimated my monthly expenses to be $60K NTD for a young family of 3. I believe I can fund this based on rent and dividends alone, so I can continue to let the capital value of my portfolio grow during my absence.

I plan to work part-time teaching English or doing some freelance work online for additional income. Worst case scenario, if my portfolio tanks I don’t see why I couldn’t return and resume my corporate job (assuming it hasn’t been TOO long of an absence).

Do you see this as too risky/naive? Should I delay the move to Taiwan until I’ve built up a bigger buffer?

Hi Slothman

$60k NTD per month is some pretty good living in Kaosiung. If you can cover your cost of living from rent and dividends, it doesn’t get much less risky than that. Add some potential income, and flexibility and things look pretty good

Even if the portfolio tanks, dividend payments in 2008 (for example) were impacted only slightly in comparison to stock prices for VTSAX

Hi GCC,

Quick question on the 4% rule which still eludes me…

Assuming a pot of $1m, at the start of the first year I can withdraw $40k

At the start of the second year I can withdraw another $40k

At the start of the eleventh year, assuming I still have more than $600k in the pot then I’m golden and can continue as before.

My question is, each time I withdraw monies yearly, does the amount stay fixed at 4% of the original pot or do I increase the amount by inflation each year (e.g. $40k + inflation)? If +inflation is the case then I assume something similar to the following would ensue…

Year one – $1m pot – withdraw $40k

Year two – $40k (Year one) + inflation

Year three – Year two + inflation

Year four – Year three + inflation

Hi Yabusame

Inflation applies. For easy math, assume 10% inflation. Year 1 = $40k. Year 2 = $44k. Year 3 = $48.4k, etc..

As for the 10 year threshold, it depends. To illustrate the concept, I did some simple simulations in cFIREsim. The first column is success rate for a normal 4% withdrawal rate. The second column is for a 2% withdrawal rate during the first 10 years, and then a 4% rate thereafter

75% stocks / 25% bonds / 0.08% expense ratio

Reread your article and it answers my question early on… Add nflation each year to withdrawals.

Cheers!

Haha, lokks like you wrote your reply as I was wrote mine ;-)

This is one of the best (if not THE best) article I have ever read on this topic. I just forwarded this to a 1/2 dozen people telling them the same. Thanks for taking time to write it GCC!

PS. Congrats on GCCjr! He looks like a cute kid :-)

Thanks JT!

I think GCCjr is pretty cute, but I might be biased

Did you mean you forwarded this post to a 1/2 dozen million people? ;)

A 1/2 dozen million indeed! I’m most certainly not THAT cool ;-)

I can assure you though, that this article has locked in it’s place as my Go-To for explaining this concept. That initial 1/2 dozen was just my kneejerk reaction to the “#financialporn” contained therein. My wife humors me greatly when I turn around from my computer and exclaim “Holy Crap, this article is amazing. Such an articulate write up on SWR. It’s like i’m reading all my random thoughts in a congealed form. Look at that Data!” /Drool

As for the “failure cases” you mentioned, I would LOVE to read a good write up on that. Just as this article does so well, articulating where and when the 4% rule can fail helps me to make reasonable contingency plans to increase the chances of my success. If I can keep my SWR at 4% and obtain a 98% chance of succeeding just by coming up with $1000 a year in income, I’m game. That is a whole lot easier than lowering my SWR to 3.5%.

I must say though, reading this write up (in all it’s glory) and MMM’s post on “Work” all in the same day has not helped to lessen my paramount need to retire one iota! :-P

Thanks again GCC!

Hi, thanks for the great article.

If you do the 4% withdrawal rate, does that mean 4% of your total financial assets? If half of my assets are in home equity, would it still be reasonable to use that in my calculation?

A paid off house impacts your expenses, but shouldn’t be used to plan your withdrawal rate from the rest of your assets

If, for example, you had $500k in stock and $500k in a house, and spent $40k/year, you could be forced to get a reverse mortgage / sell the house to buy food

If someone has the house paid off, they could rent it out for rental income and live somewhere else with lower housing cost (if they are low on liquid asset). They don’t have to sell the house or take out home equity. I have seen several probate sales where the deceased left a very expensive piece of real estate. If we take the primary resident out of the 4% calculation then wouldn’t we always leave a piece of real estate behind?

For somebody that values the security of a paid for home, isn’t having a place that is yours for life part of the idea?

Leaving behind a piece of real estate in that case should be the norm, as opposed to an exception

On a personal level, if you are ok with running out of liquid assets and moving into a studio apartment while renting our your home, then it would be ok to include the residence in the calculations

You can simulate this in cFIREsim by putting only the stock/bond assets into the Portfolio field, and using a withdrawal rate of say 6%. Success rate drops from ~93% to ~50%.

Hi Jeremy, i think you did a lot of work making it easy to marry how this 4% rule works with the whole FI story. Let me try to offer some balance thoughts.

The best idea of the 4% rule is that its been load tested against 2 of the worse 30 year periods, which is the years starting in 1937 and 1969. And thus it gives people a degree of confidence in using it for the planning.

Dr Wade Pfau, Micheal Kitces and the guys that took over the job of looking at retirement planning have this to say about the 4% rule: its theoratical, and should not be followed strictly for your wealth de-accumulation spend down. even Bengen who was part of that Trinity study used a floor and ceiling wealth de-accumulation for his own clients when advising.

There are some drawbacks:

1) its tested with a 30 year period, and for FI folks who probably have a longer period of not working (strictly not working, no side income, no blog income, no going back to work for a few months) the failure rate are likely to increase

2) The data caters to USA, the powerhouse economy of the world, and i do understand that your target audience is USA citizens. However, for the folks in other parts of the world, they do not have the same instruments to reach the same financial independence. Their real or nominal rate of return will not be the 7-8% touted. Planning with the 4% rule in the context of taiwanese, singaporean, UK citizens or Canadians might reach very different results. The failure rate would be much higher.

3) the assumptions of the rule is that failure is deemed when you run out of money, or you cannot match your savings rate which in both situation fails. your spending each year WILL ALWAYS increase with an inflation, a rate that most have no idea what in the future.

with that in mind, the conclusion for me is that 4% rule is theoretical, but its not without its use.

The 4% rule or 25 times your expenses is a good milestone to charge towards, to let you know you reach a reasonable wealth to be ready for FI. As a planning and measuring tool it is good because it is easy to compute (and perhaps because it is easy that is why many uses it)

What is the solution for international folks and those that have a longer spend down duration? I think you have highlighted them.

1) Zolt and Guyton have come up with variable spending strategies. Basically in practical, most folks are likely to tighten their spending when the market isn’t doing that well and their wealth fund is cut. During these period, it is likely to be deflationary and thus increasing based on inflation is probably not realistic. So the rules are such that if its a downturn, stay the same, or do not increase based on inflation so much. Basically tighten your belt.

the good thing about this is that, Zolt shows that it works well in 1937 and 1969 scenario, and you can hit higher wealth deaccumulation % of 5 to 6%. This makes it even more helpful for folks in FI because they are the smart sort that takes time to understand these assumptions and will tighten their spending when needed, or go for part time work.

the minor problem is that you lose purchasing power, but this is less of an issue for the FI folks because their inflation rate is much lower than the average.

2) Rebalance your portfolio helps because it buy low sell high systematically. It has an effect of increasing your 4% rule success rate. Google Micheal Kitces on rebalancing.

3) base your spending strategies on more dynamic metrics such as mortality table, future CAPE ratios to determine valuation. This is complicated and might appeals for some folks

4) Have a larger security limit. perhaps 2.5 to 3% withdrawal rate. This will mean u need more money.

At the end of the day, the key thing that is different for FI folks versus the traditional retirement is that the human capital is still very productive, so there is a fall back plan.

Just trying to conceptualize and systemize the good work u have explained.

Great post, really nice discussion of the 4% rule.

For those credit cards you just applied for, can you have them delivered to wherever you will be, or will you be waiting for a return to the US to pick them up?

I’m living in Mexico, and the biggest obstacle to travel hacking seems to be physically getting the card once I’m approved.

All of our mail goes to a friend’s house in Seattle. Every once in awhile, we just have him drop everything into a FedEx envelope and send it our way

Over one 9 month period, we received no useful mail, most everything just goes into the recycle bin unopened

GCC, this is a home run. You’ve crafted timeless reference material for years to come. I’ve shared this with anyone that will still listen to me. Love it.

Great and informative post. Thank you!!! I will make sure to incorporate some of these for my early retirement.

Jeremy …something to ponder….

It’s Monday morning (and it’s my birthday woohoo) so let’s get our brains working. For a future post, can you dive into index funds vs individual stocks? Now I know right off the bat everyone is going to say index funds – case closed –end of story, but I’d like to look into it a little deeper. Now we all know the argument against individual stocks is increased volatility and fees associated with trading. However, one of the benefits from individual stocks from the passive income side is we can pick and choose which stocks to hold and yield higher returns that most index funds from a dividend standpoint. So what if we try ti combine the best of both worlds?

Instead of buying and selling individual stocks, what if we put together a portfolio of “quality” companies yielding between, let’s say, 2.5% and 5% (those amounts aren’t set in stone but more so guidelines). The Vanguard S&P 500 fund (VOO) is currently yielding 1.95%, net of fees. Let me use some figures as an example.

We take $100k in both scenarios

Scenario 1 – We buy $100k worth of VOO directly from Vanguard. No trading fee since we buy direct and we get 1.95%, net of the 0.04% annual fee. In year one, two, three, etc we receive $1,950 of dividend income (obviously assuming no increase/decrease in %).

Scenario 2 – We buy 100 “quality” dividend paying stocks, $1k each, for a total of a $100k investment. We go through an online broker and pay $7 per trade. Let’s also factor in our $7 selling fee (although we do not plan on selling for decades). Let’s say on these 100 stocks we average a dividend yield of 3.25%, which is reasonable holding the “big boys” (XOM, PG, WMT, VZ, T, etc). From a dividend standpoint we bring in $3,250 in year one – less our fees (buying and selling) – we net $1,850,

which is $100 less than we would get from the VOO index. However, in year 2 we also get $3,250 and since we already factored in our fees this is all profit. Also, since we own individual stocks we do not have any annual holding fees. Every year from now on we bring in an additional $1,300 per $100k by holding these individual stocks as opposed to the VOO.

Over a 10, 20, 30 year period this turns into some serious cash. And being early retirees we cherish every extra dollar we can produce. Now, yes, there is added volatility but how much?

Also, being that I’m 27 and 13 years from my ER age, I would use my dividend income to reinvest on a quarterly basis on my 2 biggest laggards, getting extra shares at a “discount” due to market timing and swings. If I own the VOO I am reinvesting every quarter in the same fund whether it is up, down and unchanged. Isn’t there more value, say in an up market, to take the dividends and reinvest in the companies that are lagging instead of reinvesting in the booming market?

Thoughts? Criticism? Fire away I’m open to any and all feedback. Thanks!

Hi Johnny, this is a topic I don’t plan to touch

There is a whole universe of people out there that focus on buying only dividend stocks. Search for Dividend Growth Investing and you can read about it for years

My only thought is there is nothing magic about dividends. It is just one form via which a company can return value to shareholders

This was an excellent summary of retirement withdrawal planning, best I have ever read. Great work, as a Sabermetrics dude, I love data too, I thought this was a fun and informative read. Thanks for the hard work! As for the post in individual stocks versus indexing, I think a study was just published (Stanford maybe?) that shows that indexing is the way to go, especially since most people do not purchase stocks at the right time and pay too much in load fees or transaction costs…

What a great post about the safe withdrawal rate! I really enjoyed the deep analytical evaluation. Speaking of Wade Pfau’s research, I wonder if you could share some thoughts on this more recent article by Mr. Pfau. In this article, he uses historical data to examine the SWF after retiring in times with a high CAPE ratio (like close to 27 as it is today). Basically he sees a less than 50% probability of success for a 100% equity allocation over a 40 year retirement. Thank you for your thoughts!

http://www.advisorperspectives.com/newsletters15/Retiring_in_a_Low-Return_Environment.php

I have not read Mr Pfau’s recent article, but I understand the assumptions on which it is based

If we assume that interest rates can only go up, then future bond returns will be lower than past returns. If we also assume that current stock prices are overvalued, then perhaps future stock returns will be lower than past returns

I don’t necessarily agree with at least the stock overvaluation assumption, based on CAPE / PE10 valuations. I think this article fairly summarizes why

http://www.philosophicaleconomics.com/2013/12/shiller/

Loved reading your blog, it was really awesome and inspirational. I would like to ask what happens to your calculations if the equity market goes down for 15% for 5 years in a row. Or, how many years of consecutive losses can we take using the 4% USD1m rule? (Lets not look at history, where I know such a trend has not happened in the past century).

You can play with the data using cFIREsim

There are many “what if” scenarios, but exploring them has limited value. If you believe that a depression worse than the US has ever seen is in the future, you can personally plan for that by saving more

You said, “But let’s be crystal clear. Even if we do none of these things, with a 4% initial withdrawal rate, in nearly all cases we die ridiculously wealthy.”

If most of your assets are in IRA/401K buckets, in order to die wealthy, would you just invest the difference between the 4% and RMD amounts?

You would want to keep the same target asset allocation, even outside the IRA/401k. So yes, invest the difference between the 4% and RMD amount

If the RMD amounts are large, then it is most likely because you are already quite wealthy. RMD amounts don’t start to get excessive until Age 80-85

If the IRA/401k has become very large, it can be worthwhile to pay tax at a lower rate before Age 70.5 to avoid increased taxes later. This is what The Bob’s will need to do to minimize overall taxes

https://gocurrycracker.com/reader-financial-review-scared-death-early-retirement/

James, thanks to Jeremy’s analysis that IS what we are planning to do.

He provided input to prove once they get to a certain point, the funds could potentially grow faster than can be spent and the taxman will come knocking.

This is particularly important once SS and another retirement vehicle kick in during the later 60’s.

“To further reduce costs, while still working we can hack Credit Card rewards to load up on Frequent Flyer miles and Hotel Rewards points, in the same way that we build up our stock and bond portfolio. Consider it another asset class. This will allow us to fly and stay for free in the early years”

Haha never thought of it as another asset class. It certainly doesn’t throw off income but it does result in money savings….

Loved the post. I really like the original content. You definitely delved deeper into the 4% rule than most people who just stop at a sound bite (which definitely has its place – its quite useful when you’re trying to get people to understand the big picture….but not when you’re trying to explain things to those who are already informed or those willing to learn).

We’re planning to move to the Caribbean first after FIRE so that our portfolio can grow further and leave in Europe at some point. You’re right when we have so many decades to live, there’s no need to rush it. Adapting to the situation is definitely key in making your portfolio last. Good points.

According to traditional retirement calculators, there’s no way I can retire before age 65 and I would need at least 1 million. After reading this post, I’m going to revisit those numbers, starting with my target annual spend!

I have a question about the stock/bond allocation. Most advisers recommend putting less in stocks as you get older. Do you have any thoughts on this? I cannot imagine a retiree having 100% in stocks or even 75% stocks/ 25% bonds.

https://gocurrycracker.com/path-100-equities/

Thanks Fiby

@middle_class – I’m a retiree with 90% stock / 10% bonds +/-. Most of the advice for retirees to hold a large amount of bonds is targeted at people who retire at 65, have a lot of social security, and will most likely die within 15 years

Congrats on the new baby. Fascinated by your courage to just walk away from it all. My wife and I are in a similar age/position to retire if we wish to and live the way you describe, (thank god) but wondering if having kids changes things for you? Guess you have some time to worry about schools etc but eventually do you just plan to homeschool them??

Hi Bobby

As much as it is possible to plan this far in advance, homeschooling is part of our plan. It will in part depend on GCCjr’s personality, but I can’t really think of a better place than Rome to learn Roman history, for example.

Great summary of the Trinity Study! I’m still trying to figure out how much my annual expenses vary and what I can cut from my lifestyle! Awesome that you’ve taken the leap on living abroad!

consider market is at its all time high. is 4% rules still realistic? i’m at 4% but i’m worry the market will crash as soon as i pull the trigger

The 4% Rule worked if you retired at the all time high in 1929. It worked if you retired during WW1 or WW2. It worked if you retired during the oil embargo and runaway inflation period of the 60s. It has worked at any time in recorded history.

Still reading the whole article, but in the 1926 chart, the label says: ” 75% bonds / 25% stocks,” but I believe you mean “75% stocks / 25% bonds.”

I did a bit of a double take when I saw that, but the text of the article seems to indicate the real ratio you used…

I think I’ll use 4ish% when I retire and see how much I actually spend (I’m hoping to get to $1 million, but I might bug out before that number). I think flexibility is key (Just like you emphasize). 4% initially, dropping to 3% during recessions, or maybe lower if your portfolio takes a huge hit, but then upping to 5% when your number has all of a sudden doubled itself. Knowing my spending habits, I feel like I might have more trouble spending my budget than not…

Great information and I’m learning so much from all of you!

Do you think the 4% rule applies to Real Estate Investments?

For example, if I have a 1 million condo, I could probably receive $40,000 a year after all expenses. Do you think this is sustainable for another 30-50 years? Experts usual assume Real Estate on average goes up with inflation.

I have around 1 million in equity in Condo investments. I’m wondering if I should sell all of them and then put it into index funds. Or should I simply live off the rental income?

Or maybe put half in Index funds and half in Real Estate?

It doesn’t apply to real estate investments. You can just live off rental income, many people do

Index funds or RE or both is something to think about based on personal risk tolerance and preference.

Great read. We are assuming a 40x spending target because we are ultra conservative and assume our withdrawal rate will be 2.5%, but this really struck a chord with me:

“But how long would it take to grow your portfolio to support a 3% or 2% withdrawal rate, years of life that themselves are not zero risk? And after working an extra 10, 20, or 30, years, wouldn’t it be a bummer if it didn’t really make a difference?”

I’m not quite ready to change our target, but you’ve certainly provided food for thought!

Hi Jessica

Glad to hear that this made you think! Mission accomplished :)

good job dispelling some of the fears people have with the 4% rule.

the other reality is that even in early retirement, many people will need to try hard NOT to make some sort of income. If you have a skill (and if you are an early retiree you surely do) people will want to work with you in some capacity. That opens up all kinds of money-making options to further pad your portfolio in the critical 10 years after early retirement.

You hit the nail on the head—flexibility is of utmost importance. Not only is every market going to be different, but so is every person.

Another way to look at the historical data is to plot the Safe Withdrawal Rates calculated by Bengen (predecessor to the Trinity study) vs. the market valuations at the time of retirement (Shiller P/E ratio). Because forward returns on the stock market have a good correlation with the market valuation (e.g., an undervalued market is likely to produce good returns going forward), the SWR is similarly correlated. I plotted this out explicitly in Figure 3 of this blog post:

http://plottingforjailbreak.com/safe-withdrawal-rates-for-all-markets/

The data line up very nicely, and show that the determining your SWR should be informed by the market valuation. There is of course some scatter about the trendline. Dealing with “scatter” is where flexibility comes in handy. ;-)

I like Bengen’s research much more than the Trinity Study. He is a much better writer than the Trinity Trio, and considered retirements of up to 50 years. He also used corporate bonds, which gave better results.

Your chart is a great way to look at SWR and CAPE, although my takeaway is probably different: The 4% Rule is incredibly robust, and has thrived through the worst retirement periods in history (period.)

Many needlessly want to feel safer, so even knowing that a low CAPE means a higher SWR would have been possible… few would probably put that knowledge into action. This is partially why I proposed using Withdrawal Rates to Failure and Withdrawal Rates in Perpetuity instead of for a specific duration. For a time, I considered tying CAPE into it but decided not to as it has steered people towards poor choices in other areas, e.g. Mr. Shiller has been largely in TIPS since the 1980s since stocks are “over valued” and would probably be homeless if he didn’t have multiple streams of income.

With that in mind, I would probably change CAPE values post 1980 or so. When companies started to favor share buybacks over dividends, the CAPE value became artificially inflated relative to history.

Are any of you educators? I’m 9 years away from age 55 and 30 years service. At that point, I’ll get about $3400 per month for life. As of now, I own my home and it’s worth about 900k. I have three kids- 18, 16, and 12. I want to move from here to the CLE area of Ohio. COL will reduce dramatically. I wonder how soon I can do this and use the 4% rule? I will still get retirement at age 55, but would have maybe 7 years prior to that with little income. I can rent my home for about 4K per month or sell. I’m NOT a financial person. I also have a business that I run and can net about 1K per month. It’ easy and I enjoy it. Would moving to CLE (plenty of amenities) be a viable situation and retire from teaching here sooner than later? Thanks!

4% rule is good for at least 30 years. With some flexibility, even 60+ years.

Moving to a lower cost of living area is a fantastic way to retire even earlier. That’s part of the reason why we spend time in great places like Guatemala and Thailand as well.

Jeremy, now that you’re retired, and no longer depositing working income, can you really still pull 4% out year after year even through a GFC? I mean from the Trinity study you mentioned, the 4% rule was supposed to last through 30 years, but you’re only so young… after 30 years, you’ll only be in your 60s! Another 30 odd years to go! How will you manage?

Then I found another of your article https://gocurrycracker.com/the-go-curry-cracker-endowment-fund/ So does that mean that it’s probably a 3% SWR for perpetuity i.e. the 3% rule or something like that?

In the majority of scenarios in the Trinity Study, after 30 years the portfolio wasn’t worth zero. Instead it was worth 2 or 3x as much as when retirement began.

Think about that for a minute… retire with $1 million, spend 4% every year for 30 years, and you still have $2-3 million. This is the historical norm. In other words, we’ll manage just fine.

People sometimes obsess over the worst case periods in history, or put a negative filter on the future. This is more a reflection of personality or level of conservatism rather than data. We can aim for spending less (e.g. 3% or even 2%) because in the past that did “better.” But realistically, the future will be different. 2008 didn’t become another Great Depression, because government took action based on lessons learned in 1929. Aiming for such low spend rates probably just means you end up working too long, a sometimes fatal act.

Thanks Jeremy, appreciate your feedback. I’m still trying to muster enough courage to plunge it.

I feel almost as if it’s blind faith to put significant savings into index funds, especially with 100% equities, but then it’s not really blind faith now is it? It is backed by studies. Reading your articles and other early retirees comments is slowly shifting my mind set.

I don’t know if this will work in Australia though, most of our portfolio have a home biased towards Australian equities, and I believe 3.5% SWR applies over here as well. Unfortunately, we don’t have an Aussie equivalent of GCC yet.

Thanks for this! I’ve been doing my own analysis in Excel–nice to find it’s already been done! Let’s hope this isn’t the equivalent of the late 60s.

I love this post! Reminds me of an older version of myself ;)

Question though: How are you doing on the Brad Pitt and Angelina Jolie co-starring thing?

We were all ready to sign a contract but then the Brangelina Big-D threw us a curve ball. We are now seeking a new power couple

Excellent post, lots of great information in here!

I did have one question though. You mention:

“If a nightmarish economy and stock market collapse lays waste to your stock portfolio, be ready to sell all of your bonds and buy stocks while on sale.”

What if I am invested in Target Date Retirement Funds that do automatic rebalancing, etc (such as VTTSX)? I’m assuming the volatility reduction of bonds will be inherently reflected in the price, but there isn’t really a way to sell the bonds out of these specifically right? I mean, you could potentially sell a certain % equal to the bond allocation at that point in time and rebuying VTSAX or similar fund, but you’re still selling stocks at that point right?

Do you recommend avoiding these funds entirely or potentially a lower asset allocation in these funds, or just keeping as is?

Assuming you wanted to go all equities at that point, you would have to sell your target date fund and buy a stock fund. This is (part of the reason) why I don’t like target date funds.

Yes, you are selling stocks in this example but you are also buying them back again at roughly the same price.

See this post to help decide if going all equities is something that makes sense for you:

https://gocurrycracker.com/path-100-equities/

Also see this post from Michael Kitces on why the target date fund bond allocation doesn’t necessarily make sense (my interpretation):

https://www.kitces.com/blog/managing-portfolio-size-effect-with-bond-tent-in-retirement-red-zone/

Thanks for the prompt response!

At this point, I’m sitting at roughly 90/10 stocks to bonds (ignoring my emergency fund which should stay static for the most part). I do agree that going 100% equities is a good idea during the wealth accumulation stage, and is something that I’m going to highly consider.

Also, after reading Kitces’s post, it seems he is arguing for an increase in bond holdings nearing/shortly after retirement, but I think the general idea of flexibility in asset allocation is what matters more here.

Taking both of these together, I think it is probably best to go 100% equities during wealth accumulation and then potentially shifting over to a fairly small percentage of bonds (i’m thinking 10-20%) nearing retirement and during early retirement just to hedge your bets a little in case the market doesn’t do so well. This way you can either convert your bonds to stocks if there is a large market decline, or you can withdraw from your bond stash to allow your stocks to recover. Does this make sense?

One additional question I have is whether the 10 year assessment on your retirement fund being “too big to fail” holds for retirement periods of greater than 30 years? I know it is not a hard and fast rule, but as a general assessment, is it appropriate to scale this number with your retirement period (i.e. if you plan to retire for 45 years, you would try to reduce some volatility through increased bond holds for 15 years instead of 10 years)?

The median value of the portfolio for a 75/25 stock/bond allocation after 30 years of withdrawals was 6x the initial value. For 100/0 it was 10x. The portfolio can survive forever.

See this post for benefits of different asset allocation during the accumulation phase:

https://gocurrycracker.com/financial-independence-how-long-will-it-take/

Holding bonds during the initial years of retirement is one way to manage risk. You could also earn a little money or spend a little less, or just assume that you’ll get some Social Security income. See Foundations for Long Term Success section above for more thoughts on this.

Also see this post about what happens in the worst case in history:

https://gocurrycracker.com/the-worst-retirement-ever/

This was great, thanks! Since you offered, I would definitely be interested in hearing more about the downside risks (since, after all, that is generally what we’re trying to protect against- if the modal outcome holds or improves and the 4% rule stays great, then everything’s fine- investors all win). Some of Todd Tressidder’s counter-arguments seem fairly reasonable (American cinderella story of the past 200 years), as do the arguments saying since stocks are “overbought” (high P/E) and bonds are quite overbought as well (QE, etc), that the two aren’t as good counterbalances as they historically have been. And then some of the stuff Wade Pfau has discussed more recently on his blog, Rob Bennet’s P/E-adjusted calculator, giving us currently more like a 1.x safe withdrawal rate, etc etc. Obviously anything can happen on the super-tails, so there’s only so much planning to be done for that, BUT the sample-size we have for 40+ year retirements is pretty small from a statistical standpoint, and the specific situation we’re in is far from normal, whether you’re looking at inflation, government intervention in markets, or just equity valuations vs historicals. Anyway, I know this was fairly stream-of-consciousness, but curious to hear your thoughts if you do want to write about failure cases in other countries or in non-insample times! Thanks again for all the awesome posts!

Thanks for the breakdown. I’m still confused with the multiply by 25 annual targeted spending piece. Do we need to consider inflation and length of time before I determine my retirement number? For example, if my annual spending is $40,000 now, then I will need $1,000,000 (40,000 x 25) to safely withdraw 4% or $40,000. However, saving $1,000,000 would take me 25 to 30 years. Would my retirement number increase after 30 years of saving?

For most people it is easiest to think of it in today’s dollars (2017 dollars.)

If you spend $40k in 2017, you’ll need $1 million in 2017 dollars.

You invest those savings in assets that typically grow faster than inflation.

30 years to save 25x annual spending implies a savings rate of about 25%, which is pretty good. Things get better fast as you approach a 50% savings rate.

I thought I would try to repost this question in a more appropriate blog posting. Knowing what you know now, (earning income post retirement, taking advantage of tax savings, etc.) would you have pulled the trigger and ‘retired’ earlier than what you did?

Sorry if this question has already been asked in another blog post I don’t know of a way to search all comments?!?

Hi Joshua

Probably not. I made personal promises to friends and coworkers that I would be there through the end of a project, and those relationships are worth more to me than $.

I wouldn’t be happy blogging if I needed the money. I wouldn’t plan our life based on blog income. This is also the only unknown… I knew we would have low/zero tax bill, etc…

Thanks for the response GCC, I was just trying to gauge whether the extra work was worth it or not at the end, since it seems like you’ve got to a point where there’s no concerns about running out of $$.