Balance

It’s been 3 years since I evaluated moving our portfolio to 100% equities, and 2 years since I last published an update on our overall asset allocation.

What’s changed since?

Updates

Over the past couple years I’ve done the following:

- Annually: Converted Traditional to Roth IRA

- Annually: Harvested long term capital gains

- Early 2018: Sold US stock to purchase Municipal bonds (enough to fund our lifestyle for 1 – 2 years)

I’ll review each in full. But first, an asset allocation snapshot:

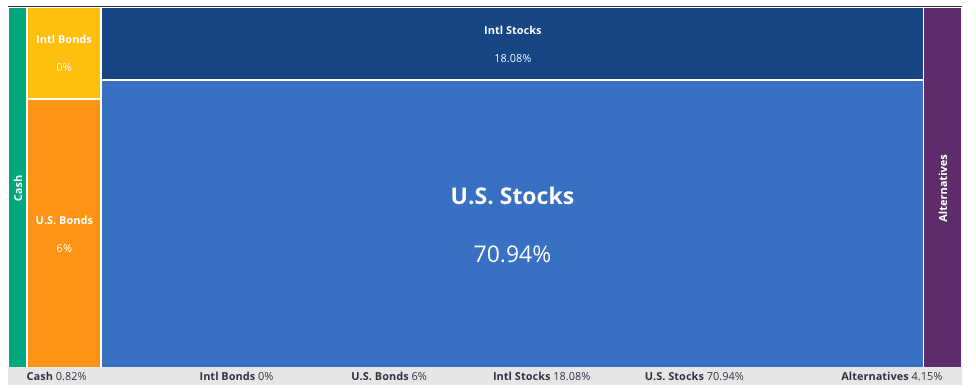

GCC Asset Allocation

As of January 31st, 2018, according to Personal Capital our portfolio looks like this:

In other words, it’s basically the same as it was 2 years ago.

Assets and allocation

US Stocks: 71% -> ~80% VTI, plus 20% S&P500 and 1% Small-cap trusts in my old 401k

International Stocks: 18% -> ~90% VXUS, 7% VWO, and small holdings of Vanguard MFs in our HSA

Bonds: 6% -> ~85% Municipal bonds (mostly VTEB, some MUB), 15% intermediate term Treasuries (IEI)

Alternatives: 4% -> 100% VNQ (a REIT.)

Cash: ~0% (Emergency Funds are over rated.)

Not shown in the chart above are some legacy I-bonds and a private seller-financed mortgage contract, which are less than 5% of total assets. When included, total weight of US Bonds is ~10% and total stock is ~90%

Some interesting ratios:

Stock / Bonds: ~ 90 / 10

US / International equities: ~ 80 / 20

Taxable / Pre / Post-tax: ~ 70 / 25 / 5

Roth conversions

A Roth conversion is the act of moving funds from a Traditional IRA to a Roth IRA. It is fully taxable in the year of the conversion, but that tax rate can easily be 0%.

In 2016 I converted ~$6k, and in 2017 I converted ~$24k. Tax paid: $0. Tax free in, tax free growth, tax free out.

When we initially stopped working for the man we had Roth accounts worth $0, and now they comprise a full 5% of our portfolio.

Capital Gain Harvesting

Capital gain harvesting is the process of selling an appreciated asset (e.g. a stock or ETF) and then repurchasing the same or similar. When all is said and done you have the same holdings but with a higher basis.

In 2016 I harvested gains of ~$29k, paying no tax on that gain. In 2017 I wasn’t able to harvest tax free, so I did nothing. This was partially due to blog income being too high.

Our taxable accounts are currently ~70% of the total portfolio, down from ~75% a few years ago. I’ve been able to raise the basis in this part of the portfolio by more than $140k over the previous 5 tax years, so that is $20k in tax we’ll never have to pay (assuming a 15% capital gain tax rate.)

For a real world example of harvesting a capital gain, I’ve written a template based on the trades I executed in December 2016. Fill out this form and I’ll email it to you.

Sold Stock to Buy Bonds

The most recent change to the portfolio is I sold a small chunk of stock and used the proceeds to purchase municipal bonds.

Thanks to previous gain harvesting, this realized only $25k in long term capital gains rather than $55k, which I should be able to fit in our zero tax plan for 2018 unless blog income grows beyond expectations. Capital gain harvesting works.

“Whoa, hold on Mister 100% Equities, what is up with this?! You are betraying your ideology, your principles, and your entire future!”

“Why would you do something like that?!”

For the drama, of course. (wink wink)

OK, no, not really. There are 2 main reasons we took some money off the table:

- Build a short term cash buffer for some (potentially) higher expenses this year

e.g. blog growth spending, Jr’s tuition, probable medical expenses, a potential foreclosure (legal expenses), and overall plush livin’… - Happy wife, happy life

I’m a firm believer in the 100% equity portfolio. Statistics are a beautiful thing. You might phrase my thinking as, “We’ve won the game, so let it ride! Woohoo!”

The Missus has a different point of view, more along the “We’ve already won the game, let’s stop playing” persuasion. And persuade, she did.

So…

5 years ago our bonds totaled ~15% of the portfolio, when factoring in I-bonds and private mortgage.

I reduced that to <10% a few years ago.

Now it is back to ~10%.

Will single digit percentage changes have any long term impact on our overall portfolio? Unlikely. But for perspective, the “off the table” dollars are enough to purchase about 1 3/4 houses in my home town or fund 1 – 2 years of our cost of living. It can therefore have minor statistical significance on our portfolio, while having an appreciable impact on emotions and quality of life. Win-win.

Other Noteworthy Updates

Portfolio Expense Ratio

Through absolutely zero effort on our part, the total cost of managing our portfolio continues to fall, dropping from 0.08% 5 years ago, to 0.06% two years ago to <0.05% today. On $1 million, a 0.01% drop is a savings of $100+ per year. Thanks Vanguard!

Retirement Account Fee Analyzer by Personal Capital

Reward Points

While not a traditional asset class, we have continued to build a healthy amount of airline, hotel, and travel rewards points through credit card signup bonuses. Despite using a ton of points over the past couple years, our point hoard (and credit score) continue to grow.

One example of point usage: $16,000 business class flights to Europe for $300.

Alaska Airlines: 141,338 miles

Amex: 55,962

Ultimate Rewards: 284,926

Delta Airlines: 8,670 (all from Airbnb)

IHG: 160,602 (mostly from Accelerate bonuses)

Marriott: 4,025

SPG: 12,724

United Airlines: 16,168

Total value: ~$11,000

We are currently debating a summer visit to the US or a return to Europe to tour the 1/3 of the continent that we have yet to visit. Or maybe both.

Final Thoughts

Depending on your perspective, this update is either absolutely fascinating or a total yawner.

Not much changed, and that is exactly how investing should be.

Pick a target asset allocation, stick with it, ignore it, and sprinkle a bit of tax management on top.

See you for the next riveting update in a couple years.

Love the aggressive attitude, guess you are still maintaining more of your ideals indeed. Some bond in this time of market valuations might not be a bad idea, but your side income makes this pretty much unnecessary. Kind of a nice safety net to have, blog income!

The blog income makes a lot of things easier, or at least more relaxed. Just think of the additional portfolio balance we would need to throw off $50k in after-tax income.

Related to the promo at the bottom, how do you cancel in time to avoid the yearly fee after the introductory year is over? I know some cards won’t let you claim your rewards until the next ywar. Do these allow you to claim within the first year? E.g. sign up for the card, earn my bonus miles in 3 months and then cancel a month later?

I always keep cards through the year, and then assess if I want to pay the annual fee or not. If it’s worth it, I’ll keep it. If not, I’ll replace it. This year we will pay maybe $800 in credit card annual fees, but will get many times that in benefit.

I enjoyed seeing this update, I’m always interested to see how folks shift or keep their strategies the same.

We also just took advantage of the IHC Accelerate to stock up… seems to be a great way to quickly get a healthy amount of points!

The Accelerate stuff is nice when it works out. I’ll take some free hotel nights just for doing what we were going to do anyway.

Not enough bloggers share their allocations, thank you! Love the last part – pick one, be smart about it and sprinkle tax management on top! X)

Thank you :)

Foreclosure? Don’t tease!

heh, teasing not intentional. The private mortgage we have has always been a bit rocky in terms of reliability. Might need to do something about that.

I am not sure why, at a time of rising interest rates, you would want to buy bonds? It looks to me that you are going to lose money because of rising interest rates. What am I missing?

80% of asset allocation is telling the “I’m so smart” part of your brain to own things that you don’t think you should own.

With absolute certainty, I can say 1 of 3 things will happen:

– bond prices will go up

– bond prices will go down

– bond prices will stay the same

Fair enough! But interest rates have been going up: this is not predicting the future or thinking that I am so smart. Don’t you want to make decisions with the benefit of the knowledge that you already have? BTW I second the compliments on publishing your asset allocation. Thanks for the service you do the the FI community. The info you publish has been some of the best and most original I read in the financial blogosphere.

This is called market timing. The Fed has been raising rates, which isn’t the same as market rates. But you know rates are going up, I know rates are going up, everyone knows rates are going up. Since everyone knows that, bond prices reflect it to a degree.

Yeah seriously. Foreclosure? Do tell!

Might have to take some extra steps to get my private mortgage $ back. Supposed to balloon out this year.

You are so solid on not paying taxes it is fantastic. I’m sure 2018 will be another great 0 for you. Glad you’re still fairly aggressive.

Spoiler alert: It becomes a bit easier in 2018 thanks to the doubling of the child tax credit.

Ahh congrats, I can understand your wife’s concern with another little. Any advice on how to avoid real estate capital gains? I’m selling two spec homes in one year by accident because one wasn’t done by December. I’m afraid at how much I’m going to have to pay the man!

Buy something bigger?

I’m glad the blog income has gone up so much – I’d like to think I had a little to do with that problem ;). If you decide to come stateside and land in LA, I’d love to meet up in person. Brad

Whoa, it looks like most of the revenue is coming from your IP address! Thanks! ;)

Always up for a coffee (or Umami Burger!) next time we are in LA. We were there in 2015 for a bit, still have friends there. Not sure when we’ll be back yet.

Great update. Always nice to hear how you all are doing. Add me to the Meetup list next time you are in LA. I’ll buy the burgers.

With the blog income how are you expecting to still pay $0 in taxes? AFAIK there’s no way to offset the self-employment tax and your blog income continues to increase. We’ll be quitting and moving overseas, but I can’t find out how to eliminate the SE tax despite having a very low income, probably <$15k once we hit the road.

With our low 6 figure income we also manage to pay zero income taxes, but the SE Tax seems pretty unavoidable indeed, at least for us! GCC, do you manage to avoid those taxes due to huge deductions on the self employment income? or are you talking specifically about income tax?

If you are in the US, you can’t avoid SE taxes. But you can think of them as a reasonable return annuity with semi-voluntary contributions.

If you are outside the US, see my reply to Ken.

For expat biz owners to avoid SE tax you need to create an overseas corp. If you are employed by a non-US corporation, no payroll taxes.

Since you spend most of your time and most of your money ex-US what’s your reasoning for avoiding a portfolio with something closer to a global market weighted (or even international tilted) portfolio? I’m a US citizen that travels full time overseas and I’ve settled at 40:60 US:INTL. Over time I’m moving towards a true global market weighting. To me the perceived risk of losing purchasing power abroad exceeds the perceived risk of losing purchasing power in the US.

Is it just that 80/20 or 70/30 US:INTL has historically yielded the best returns?

Hey Aaron, good question. Long term we’ll probably be in the US.

2 years ago I wrote this:

Maybe I should get around to writing it.

Interesting that you’re shifting some to bonds. Happy wife, happy life as you say. I’m feeling the same pressures here as the wifey is pushing to move more to bonds. She would have timed it perfectly and I almost moved somewhere between $100-500k to bonds right before this most recent dip. So now she has that to hold over my head :) Though I’ve told her we won’t regret holding all these stocks in 5-20 years.

We’re right at 10% cash/CDs/bonds at the moment with the other 90% in stocks.

I was curious about your relatively low allocation to international equities. Is that the JL Collins / Jack Bogle mindset (you’re getting your global diversification through SP500 multinationals)? Or something else? We’re at 50/50 US/Intl, and part of the thinking is that we’ll be spending $$ overseas quite a bit during retirement so I wanted to go a little heavier international so we aren’t priced out of international vacations. I figured you would be even more international given that you’re spending most of your time outside the US and spending in non-USD currencies.

After a career of working with non-US corporations, and seeing what % of revenue goes to shareholders vs politicians, taxes, the cousin’s overpriced contract business, bribes, the social contract, overly strong labor laws, etc…, I prefer to invest in the US. It’s not perfect by any means (see health care, education costs, etc…) but what can you do?

I rationalize my bias by seeing that historically a 70/30 or 80/20 US / International split was the balance point for return vs volatility.

Surprising on the asset allocation front. We’re still mostly (~95%) in equities, but that is a bit overstated since we have decent compensation that comes in February. I’ll need to decide how to deal with that cash flow this month. It likely will go into the market if the correction runs a little deeper.

How did you decide on which Bond funds to allocate to?

ok

Wow, really settling down from your wild ways! But I have to agree, I think you’ve already won :)

I’ve always respected the 100% equities position, but have been too conservative to get past 80%, which is about where we are now. Having money you plan to spend set aside is a solid argument for some bonds. At the same time that might be the a reason for us to finally get more aggressive as our portfolio grows and our potential need for cash remains the same…

If you do decide to come stateside, and end up in the NYC area, let us know! Summer can be nice in CT ;)

I never quite made it past 90/10, and here we are years later at 90/10.

Save me some cherry tomatoes

Looks good. It’s nice that your allocation stays the same. We’re a little more conservative with 20% bond. I’ll probably convert about 5-10% of US equity to cash later this year. We need some opportunity fund.

Nice job with Roth conversion too. You’ll be able to convert more in 2018, right? The tax brackets increased.

The 0% tax bracket is actually a little smaller for us (2 adults, 1 kid.) But the doubling of the child tax credit means yeah, probably a little bigger Roth conversion in 2018.

Your buying muni’s now? Wow, Mrs. Gcc really has you wrapped around her finger! Haha!

In all seriousness, it’s probably really good timing. She’s a keeper that one!

We’re about 75% equities right now, and I kinda wish it was a little higher. Oh well, I guess we’ll find out if that caution is excessive or not!

I look at it a bit differently; we are a good team. We had a good conversation:

W: How much $ has our portfolio made since we quit again?

Me: More than $1 million

W: Maybe we take some of that off the table? Whatever we can do without a big tax impact?

Me: OK

Good communication is worth more than gold (or bitcoin)

I apologize if you’ve posted this already and I missed it. Since I see you hold some of the same Vanguard ETFs that I do I was wondering where your accounts are and how easy tax lot ID is there. I’m at TD Ameritrade but since they dropped Vanguard from their comm-free ETF list I’ve been considering moving. (Fidelity, Merrill Edge, Vanguard).

We have accounts at Fidelity, Etrade (solo 401k), and Vanguard (W’s Roth IRA.) Most of our funds are at Fidelity and I just pay commissions, nbd.

GCC,

I as well use Fidelity, but I use the fidelity funds instead of the vanguard ones. For instance, FSTVX has an expense ratio of 0.035%. Not a criticism by any means but I’m wondering if I’m missing an important detail by going with the Fidelity Spartan funds instead of Vanguard through Fidelity.

Thank you for any insight,

Darren

The Fido funds are fine. They recently dropped their fees, but when I bought the majority of our portfolio holding Vanguard was lower. Recently when I did some reallocation / gain harvesting I used the ishares equivalent as those had no transaction fee.

One reason (potentially) to prefer the Vanguard funds is when they lend shares to short sellers 100% of that income comes back to the fund, which means they may actually be charging less than the published expense ratios. The other fund companies take some of that income for profit.

is there a tax calculation tool to find out how much to convert into Roth so not to trigger higher tax? thanks

I’ve not used any, but there are many Roth conversion calcs around. I just look at the tax brackets and calculate in Excel.

I think the closest I’ve come to walking through the process is on our 2015 tax return.

Judging by the Jim Cramer Cyclical chart we’re clearly in the point of maximum financial risk so why keep exposed so much in stocks? I’m doing like Ben Graham and ajusting down to 50%/50% until a correction comes where I’ll rebalance back up to 80% stocks! GBY

you lost me at Jim Cramer

Although I don’t like Jim I’m a fan of Ben and I’m 25%/75% at the moment!

I’m in the “this post is interesting” camp ;). Intriguing that you include frequent flyer miles as a quasi asset class. Why not? After all, they are worth thousands of dollars.

Curious why you are buying munis if you aren’t paying any (or minimal) federal taxes…. Why not short-term corporates, which will likely withstand the uptick in interest rates better than most bonds? Something like VFSUX.

Every dollar of interest income is one less dollar that I can convert to Roth tax free. Not so with munis

Roger. Thanks.

GCC, one follow up here. Why not have the bonds inside IRAs and then enjoy the higher yields of corporates without the worry of tax implications–keeping equities with qualified dividends in taxable accounts–rather than going with Munis.

Maybe 2 questions here – why government vs corporate and why taxable vs tax deferred?

I chose government because theoretically they are more stable in short term, and chose taxable because I am likely to spend a fair amount of these funds, also in the short term. So I need the funds in my taxable account anyway… For example, we are dropping somewhere around 15k on medical stuff this month. The delta in yield between the munis and short term Treasuries was small, less than 10%, which makes the munis better tax adjusted yield.

Technically all dollars are fungible and I could do as you say (but with treasuries), but less hassle this way.

Fair enough. You could also make the argument that you want the assets that will grow the most over time (stocks) in the tax deferred accounts as well if someone is young enough. Be well.

How has living abroad affected your thought towards international investing?

I ask because we currently do not do any other than the significant amount of international revenue our very large domestic companies earn. We have limited context from which to say we need to make a change. But you both have that and I wonder how it’s shaped your investing.

See my replies to Aaron and Justin.

This is helpful information. I loook forward to working on the cg harvest spreadsheet. I have a question though. How do capital gains impact Obamacare subsidies go? Are they considered income for the first dollar or are they also exempted?

See Obamacare Optimization vs Tax Minimization.

Income from all sources impact ACA subsidies.

We are 1+ year into our early retirement. Last week I was contemplating doing the opposite of what you’ve recently done. We’re currently at 61/39 allocation and were considering re-allocating to 70/30 or 75/25. We’re both 55 and living off of a cash stockpile until 59 1/2. I’m assuming selling some bond index funds to put more in the VTSAX while everything is tanking still matches up with a buy low/sell high mentality? As of last night our portfolio went down about $80,000 since Friday but we’re not panicking…but I did want to run this buy some folks as we still don’t consider ourselves experts despite all the learning we have done over the last few years. Would love any feedback. Thanks, Jeremy and all.

“On $1 million, a 0.01% drop is a savings of $500+ per year.”

Shouldn’t that be $100/year?

Yes, indeed. Thanks.

Happy wife, happy life is definitely key!

Hope your family has not been affected by the earthquake.

I think I slept through most of the earth shakes. We just had small aftershocks here, and all is well. Thank you!

I’m still working and have a Roth IRA instead of a traditional. Have for a long time now. Is it bad to invest in a Roth instead of a traditional while working?

Thanks for the help!

It all depends. For an early retiree you would expect tax rates to be lower in retirement than while working so a Traditional means lower lifetime taxes. See more thoughts here.

Have you looked into the performance difference between non-taxable and taxable bonds?

they behave similarly

There has to be a difference, because the tax-exempt status of municipal bonds is worth something.

According to Vanguard (https://investor.vanguard.com/mutual-funds/tax-exempt), only investors in high tax brackets should be in tax-exempt funds:

“Am I in one of the higher tax brackets? If you’re not, tax-exempt funds probably aren’t the right fit. You likely won’t save enough in taxes to make up for the lower yields you typically get from a tax-exempt fund.”

I guess even though you won’t be paying taxes, you are accepting a lower return in exchange.

Yes, this is all accurate.

A bond is a bond, so a municipal bond and a corporate bond and a US treasury will all respond to changes in market interest rates in a similar way. Similar doesn’t mean same. When people say “performance” this is usually what is meant.

Municipal bonds will typically yield less than a taxable bond, and people will often compare using tax-equivalent yield. But when interest rates are low, the delta can be quite small. VTEB yields 2.27%. VFITX (intermediate term Treasuries) yields 2.3%.

I’m ok getting 2.27% vs 2.3%.

Even though I could pay 0% tax on the Treasury income, for every $1 of interest I lose the ability to also convert $1 to our Roth tax-free. Prioritizing the Roth is better long term, because future gains on that $1 are also tax free.

WOW thanks for sharing this! its really inspirational. I cant wait to use Personal Capital! Is that a bit sad? currently dont have anything to actually track finance wise :(

Little Miss Fire

https://littlemissfireblog.wordpress.com

I still get excited to login and look through the account details. I don’t think it ever goes away.

J,

did the same thing myself in mid Jan…realized that CA Munis would be a nice way to get additional income (tax free), without disrupting Roth Conversion and being in a reg brok acct makes them very accessible. Allows me to slowly drain my taxable account if/when the next correction comes and allows the retirement accounts (almost 100% equities to grow/fall/grow over the next 25 years before i need them).

i’m at about 85% equities – 7-8% CA munis (in my taxable brokerage) and 7-8% in Vanguard REIT. not counting the equity in the primary residence in SF.

really appreciate the articles you’ve written over the years and it’s because of guys like you (and MMM, RoG, MF, jlCollins, etc) the FIRE movement became so available to the masses.

I really enjoy reading your blog and hopefully one day my family of 3 can do the same!

A Roth conversion is the act of moving funds from a Traditional IRA to a Roth IRA. It is fully taxable in the year of the conversion, but that tax rate can easily be 0%. – to pay 0% tax you can’t have a full-time job and still collecting regular paycheck. Therefore the solution is to always convert after retirement.

so you mainly invest in ETF?

Btw, why do you choose VTI, instead of VOO? thanks for sharing …

Correct

VTI also has small and mid cap, so about 3,000 stocks vs 500. Long term that should add some small perf advantage

Hi GCC. I’ve been following your blog for years. I’m 68 years old and fully retired, living off of social security, a small pension, and IRA withdrawals. Our net worth is a little under 1 million, yet we live quite well. House paid for. Maybe 3 trips a year, we saw the D’Orsay museum last year, loved your picture, we did an AirBnB for 17 days in Paris. Loved it. Did two weeks in Italy the year before. Jack Bogle recommends 100 minus your age in stocks, so according to him, I should have 32 percent in stocks, and 68 percent in bonds. With encouragement from you, Jim Collins, Mr. Money Mustache and others, I’ve settled in at 75% VTSAX, and 25% VUSFX (ultrashort bonds, yielding 1.98%). The day the Fed cuts rates, I’ll trade in my VUSFX for VSCSX short term bonds. What I love about this allocation is that I can draw 4 percent from VUSFX for up to 6 years before I have to touch my stocks component. This will allow time for any conceivable bear market to heal itself. How I execute this in practice, is to rebalance once a year on my birthday, except that I will skip rebalancing any year that the stock market is more than 8 percent below its all time high value. I just thought I’d share what old people with limited net worth are doing. I remember from your post that you said any allocation north of 60/40 stocks/bonds had near a 100 percent chance of surviving 30 years. I’ll be 98 when it runs out then, but maybe it won’t, and in the meantime, we are adding to cash savings every year also. And maybe they’ll try to sell me a reverse mortgage when I’m 98, just kidding!

Sounds like a good plan, Kenneth. Well done! For asset allocation, I would think of your SS and small pension as bonds.

hey jeromy and winnie! im set to go to greece for the second week chautauqua and am disappointed that ur not one of the speakers. I have a question though, some of ur points balances for the best reward programs are very high. for instance, ultimate rewards almost 300,000 which is much more than u could have gotten from sighn up bonuses for you and your wife unless you churned those credit cards. however, you can’t churn those cards because of 5/24. so you must have earned a lot of ongoing spending points? im just at a loss on how you got some of those balances so high? I focus on bonus earning not ongoing spending and i can no longer get far with ultimate rewards, i do some ongoing spending especially with regard to certain categories on the ink card but points dont add up for me like they have for you. maybe you can write a post sometime on how your able to get so many points especially with chase cards. im at about 500,000 but very few with ultimate rewards. i do research with travel miles 101 on fb and thats where i get most of my info.

I wrote up a little something about our UR points.

I don’t get invited to the Chautauquas anymore. They are adult only events, and I declined attending without the family. I’m sure it will be awesome though, have fun!

I created a HelloMoney visualization of your portfolio! https://hellomoney.co/portfolio/b312ad

I see you purchased some Vanguard municipal bond funds. I was thinking of purchasing some municipal bonds but buying them directly and buying zero coupon bonds. It seems like if you hold them until maturity it would guarantees no loss (unless by inflationary purchasing power). Does this strategy make sense?

Hi Rob…

GCC just answered a question on my blog at my request and in return asked me to respond to yours. Hope that’s OK by you.

You right that if you hold a bond to maturity the bond issuer will then return the principle. Unless, of course, the issuer defaults. If you are buying individual bonds this is a much great risk than if you are buying a fund with thousands of bonds.

Also, you’ll want to be sure you are in a high enough tax bracket for munis to make sense.

For more, and with GCC’s kind permission, I offer you this post:

http://jlcollinsnh.com/2012/10/01/stocks-part-xii-bonds-and-a-bit-on-reits/

Hope this helps!

I see that you have the VTI etf and assuming that you use that for most of your tax gain harvesting. I mainly have my taxable account invested in mutual funds (mainly FSTVX). Is there a difference in tax loss/gain harvesting with a mutual fund vs. a etf? Fidelity has a similar total market etf ITOT that I’m wondering if it would be better than FSTVX for tax efficiency reasons as well as tax loss/gain harvesting.

Dear Curry Cracker Family,

Regarding your bond and international stocks, where do you recommend putting them? Traditional IRA, Roth, or taxable accounts, and in which priority? I’m unclear as to what is best long term.

If you are ever in the Leavenworth, WA area please look me up, I’d like to buy you a beer.

Warm regards,

Jeff

Thanks Jeff, very kind of you. We were in Leavenworth for a visit maybe 15 years ago, it seems really nice.

Where you put them somewhat depends on your goals. If you need them for immediate use and cash flow generation, then everything goes in the taxable brokerage account. If tax efficiency is the goal, then there is a great chart on the bogleheads wiki for tax-efficient fund placement.

Hi GCC,

That is a great resource, thanks, I look forward into diving into it! Hope you had a great new year, our twins are looking forward to their first Chinese New Year which we’ll put into VTSAX ;)

Jeff