It’s April 15th again, time to play with taxes!

2018 is the first tax year under the Tax Cuts and Jobs Act, our 6th tax year as early retirees, and our 1st retirement year paying income taxes.

I guess it was good while it lasted… even if it was optional.

The Go Curry Cracker 2018 Taxes

I heard I was supposed to be able to do our taxes on a postcard-sized form this year, which turned out to be untrue. The 2-page 1040 was replaced with a 1-page 1040 and 6 additional forms, which makes the total tax picture less clear at a simple glance.

As in previous years, we had multiple streams of income: Interest, Dividends, Capital Gains, and Business income. All told, this year income was $136,866 with an income tax burden of $1,187, which is an effective tax rate of 0.9%. We paid about $250 less in taxes than we would have without the TCJA. I guess I would still prefer a little actual reform with my tax reform. (My review of the TCJA here.)

We also paid $9,663 in Self-Employment taxes. (This could be eliminated through the use of an Overseas Corp, but since we will probably be moving back towards the US I’ve been content to accept a larger future SS income instead.)

Here are the details:

Tax-exempt interest: $2,831

Taxable interest: $2,616

Qualified dividends: $32,606

Nonqualified dividends: $4,591

Net long-term capital gains: $25,850

GCC profit: $67,201 (details here.)

Winnie’s blog: $1,191

Total income: $136,866

The Foreign Earned Income Exclusion allowed the exclusion of $57,775 of business income. Combined with the standard deduction, this reduced our taxable income to $46,548.

The Child Tax Credit ($2,000), Foreign Tax Credit ($660), and Child and Dependent Care Tax Credit ($221) reduced the total tax burden to $1,187.

This is shown here on the new postcard 1040.

100% of the $11,200 in tax payments were made using credit cards. For about $200 in business expenses, we earned over $7,000 worth of airplane tickets. (AAAAA+++++, would do again.)

Foreign Earned Income Exclusion

Through the FEIE, we are able to exclude our foreign earned income. We are outside the US for more than 330 days/year so we qualify via the objective pass/fail Physical Presence Test. (We probably also qualify via the subjective Bonafide Residence Test.)

Business revenue and expenses are classified as either US or Foreign sourced based on where we are physically located at the time the income is earned, so money earned while in the US cannot be excluded although the division of US/Foreign income/expenses is an exercise left to the reader. I published 51 blog posts in 2018, 4 of which were published while I was in the US, so I split everything with a ratio of 4/51 (7.8%.) Seems logical.

Business income/expenses: (full details here)

Revenue: $79,856 –> Foreign: $73,593 / US: $6,263

Expenses: $12,655 –> Foreign: $11,425 / US: $1,229 ($257 definitely related to the US.)

Profit: $67,201 –> Foreign: $62,167 / US: $5,034

Any deductions that are directly related to Foreign Earned Income are also excluded – no double deductions. For our purposes, this is only the Deductible part of self-employment tax, which is determined on Schedule SE and reported on Line 27 of Schedule 1.

Deductible part of self-employment tax = Blog Profit * 92.35% * 15.3% / 2 = $4,392

All of this info ends up on Form 2555, Foreign Earned Income, where the FEIE amounts to $57,775. When combined with the SE tax deduction, this eliminates taxes on 100% of foreign profit. The relevant portion is shown below.

Relevant section of Form 2555

We could also elect to use the FEIE for Winnie’s income, but choose to keep it as US taxed income and contribute to a Roth IRA since this has no impact on the amount of taxes we pay.

Determining Tax Burden

Determining tax burden is a process that generates a lot of questions every year, so let’s walk through it.

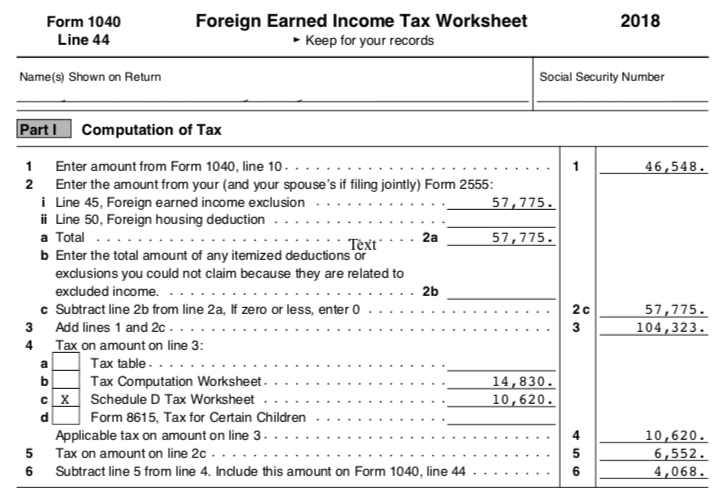

With the FEIE and the Standard Deduction, we have total Taxable Income of $46,548 (Line 10 of Form 1040.) Because we are claiming the FEIE and we have income from qualified dividends and long-term capital gains, we are asked in the instructions to use the Schedule D Tax Worksheet and the Foreign Earned Income Tax Worksheet. (Always read the instructions; TurboTax does this automagically.)

The Schedule D Tax Worksheet is really ugly looking, but what it does is separately determine tax on ordinary income and qualified dividend/long-term capital gain income. This process ignores the FEIE (for now.)

If 100% of our income was earned income (e.g. from a job) then we would have a total tax burden of $14,830 (Line 44). Because a chunk of income is from qualified dividends and long-term capital gains, some of which is taxed at 0%, total tax burden is reduced to $10,620 (Line 45.)

Final section of Schedule D Tax Worksheet

These numbers are then transferred to the Foreign Earned Income Tax Worksheet.

Here, the tax burden on the FEIE amount is specifically calculated on Line 5 (From the Tax Tables, the total tax on earned taxable income of $57,775 = $6,552.) This is how much tax the FEIE saves us this year!

Mathematically speaking, the FEIE filled the entire 10% bracket (19,050 * 10%) and much of the 12% bracket ($38,725 * 12%) = $6,552

This is then subtracted (excluded) from the tax burden calculated on the Schedule D Tax Worksheet to yield the actual tax burden of $4,068.

(Line 6 of Foreign Earned Income Tax Worksheet and Line 11 of Form 1040.)

Back on Form 1040, our total tax credits of $2,881 are applied (Line 12), reducing the actual income tax burden to $1,187 (lucky Line 13.)

Good times.

Improvements and Other Options

This is our 2nd year using the FEIE, and I feel like I finally really understand it. As with anything, every step is a learning process and it is always possible to do better.

Here are some things I could have done differently:

- Realize fewer long-term capital gains – realizing just $7,913 fewer long-term capital gains (a reduction of ~1/3) would reduce our income tax burden by $1,187 (so by 100%.) I made this sale in March 2018 and underestimated blog income for the year. Oops.

- Bring forward business expenses – I paid for 3 years of web hosting in January 2019, and I plan to get a new laptop and cell phone this year. I could have made any or all of these purchases in December 2018 instead, which would have reduced total blog profit by $3,500+. This would have curtailed 2018 SE taxes by $535 and income taxes by $525.

- Increase spousal income up to $3k to max childcare tax credit – Both spouses need earned income to benefit from the childcare tax credit, which maxes out at $600 at our income levels (20% * $3,000.) Were we to formally compensate her for the occasional photo work and social media stuff for GCC, we could increase this credit by $379.

- Contribute to Traditional IRAs – this year we made contributions to Roth IRAs in the amount of $5,785. We could have contributed to deductible Traditional accounts instead (solo 401k for GCC income, Traditional IRA for Winnie.) This would have saved up to $868 in tax (15% marginal rate.)

With a few minor changes, I could have reduced our 2018 income tax burden to zero.

So why didn’t I?

Well, I’m lazy.

But the main reason is that I plan to realize a massive amount of capital gains in short order as preparation for returning to the US. In other words, I’ll be paying a whole bunch of tax at 15% sooner or later to avoid paying even more tax later. This year seems as good as any to start.

Rushing my laptop purchase might help maintain my zero taxes street cred, but all it is doing is shifting tax burden from 2018 to 2019. Instead, I’ll time my acquisitions to meet the minimum spend requirement on a new credit card. A few free plane tickets will provide greater value.

Whenever I pay SE taxes, we get a commensurate increase in our future SS income. Whenever Winnie pays SE taxes, it is a total loss (since she never worked in the US.) Formally paying Winnie for blog services this year (2018) would allow a small boost in the childcare tax credit… but what about next year (2019) when we don’t plan to be in the US at all? (so no US income for me and thus no eligibility for this credit.) In the end, generating some 1099s and so on seems like a lot of work just to save $379 one time.

As for contributing to Traditional accounts, if I saved 15% today… would I pay less than 15% on withdrawal? If we are in California and the ACA still exists, the answer is definitely No. So this is probably the lowest tax rate I will pay on IRA contributions/withdrawals in my lifetime. I’ll just pay 15% now, as perhaps our 401k is already too big.

Summary

There are a lot of great tax minimization tools available to the early retiree.

This year the FEIE saved us $6,552 in income tax. Tax credits provided another $2,881 worth of savings, and we had a 0% tax rate on $19,425 worth of qualified dividends and long-term capital gains. We also contributed $18,500 to my Roth solo 401k and $5,785 to his/her Roth IRAs, which will grow tax-free forever. Nice.

In the end, we did pay a little income tax, which was about $250 less than it would have been pre-TCJA. We could have achieved a $0 tax bill, but paying a little tax seemed like a good value relative to the deferral and minimization options. An 0.9% effective tax rate isn’t so bad. (Albeit higher than the 0% rate on previous years’ tax returns: 2013, 2014, 2015, 2016, & 2017.)

We also paid some SE taxes again this year ($9,663), which will increase our future SS income. It’s kind of an interest-free loan.

Overall, I’d say it was a good performance in the tax minimization game.

Reminder: if you are looking for assistance with your expat taxes, check out our tax resource page.

It was my third year of retirement, paid nearly $20,000 in federal taxes and my tax filing was 78 pages long. But I did pay my CPA to prepare it for me.

This will be me next year (except for the paying a CPA part)

Well done! We had about the same dividends and LTCG and we paid no federal income taxes but paid 5k in SE taxes. Diminishing return for sure for SS income but still. No Roth conversion this year, maybe in 2019. No CPA expenses here.

SS has diminishing returns, especially since we are paying both employer/employee portions, but still not as terrible as I thought it would be.

In my solo 401k I was able to make about $17,000 in after tax contributions which got immediately rolled over into the 401k Roth.

And I still was able to do a traditional IRA

Nice.

Thanks for the breakdown, I’m still W2 but it’s nice to see what options might exist, I also love that you pay for taxes on CC.

Do you time opening the credit card before Taxes? Or do you pre-pay taxes before filling season?

Thanks!

I have to pay quarterly estimated taxes, so I aim for a new credit card every quarter.

J, do you have a blog entry specific to this? I’m finding I’m already running out of card options so I must be missing a recycle step or something.

I don’t have a specific blog post… we do his/her cards and haven’t run out of new options in past n years. I don’t hit every quarter, but most.

Are you using business cards as well? Might need to start a blog or something ;)

how do you go about estimating that? I have several accounts in a dozen countries and can never accurately estimate what I’ll owe uncle sam. Any tips?

I just track all income – no special tricks.

Lucky you. Once you have accounts in South Africa, Brazil, Estonia, HK and Switzerland, + US you can’t really track all the income. Most of them won’t even show that in the statements. They don’t send me a 1099…all guessing game at this point

Thanks for the summary!

Two questions:

1) Why do you need US income for the childcare tax credit? In the instructions it just says earned income.

2) Why did you use the schedule D tax worksheet. THat is for precious metals and 1250 recaptures. I think you needed the qualified dividend and LTCG tax worksheet: https://www.irs.gov/pub/irs-pdf/i1040gi.pdf#page=40

1) Un-excluded earned income, and therefore US income.

2) Because that is what the instructions say – special case when using the FEIE

1) Thanks for the clarification, so if I’m understanding correctly because you excluded all your income, the minimum earned income between you and Winnie was 0 for the childcare credit.

2) If i’m reading page 39 correctly: https://www.irs.gov/pub/irs-pdf/i1040gi.pdf

you can use either the qualified dividend tax worksheet or the schedule D tax worksheet whichever is applicable.

However, it doesn’t make any difference since the Qualified Dividend worksheet is a special case of the Schedule D Tax Worksheet (where precious metal profit and section 1250 recapture are 0).

1) Not this year. Next year. This year it was as I reported above.

2) It’s probably a special case due to capital gain excess. But, doesn’t really matter.

So… you’re definitely returning to the US? I’m a big tax nerd, but for me that was the biggest bombshell. Yes, I know you’ve mentioned it when discussing the “forever home”, but I’d still love to learn more about the decisions for choosing the US. Is it really that much better of an option, even given all the other places you’ve seen?

Well… probably. We want Jr to be able to read/write Chinese, which is a rarity amongst the ABCs, so need to stay in Taiwan for awhile. But then we’ll likely end up on the US for cultural reasons.

There are a lot of great places in the world, we just haven’t been able to pin down a place that we want to live and raise kids.

Thanks for sharing. But I still wonder – why choose any place? Is PT just not doable with kids?

Lots of people do it.

Jr has expressed a strong preference to stay in one place, so part of it is respecting the wishes of a 4-year-old… We were hoping to have 2 children, which would have provided more of a mobile social network, but that didn’t work out…

We could still do it and thrive, I’m sure, but we are finding that we are happy to stay in place as well. Maybe a sign of maturity or wisdom, or perhaps just we are getting older ;)

Again, thank you for your candor. As someone who isn’t hoping to pursue a more nomadic lifestyle with kids in tow, hearing about your experiences is much appreciated.

No worries, I’m happy to share our thinking. We still haven’t made any decisions.

Care to elaborate on the cultural reasons?

We’re still a few years out from having the freedom, but we’ve tossed the Taiwan vs Canada choices back and forth quite a bit. The main differentiators that stood out to me are (1) school in Taiwan is brutal for kids, especially as they get further along, (2) there doesn’t appear to be much work-life balance for parents (this mostly applies to peers), (3) kids of mixed heritage stand out quite a bit and get a lot more attention particularly around appearance, which could be negative imo

Mostly #1. The school system seems pretty good at suppressing curiosity and risk taking. We hang out with a lot of mixed families – all of the kids get the “Oh wow, they can speak Chinese!” comment (Well, yeah, he’s Taiwanese…) or 他是混血嗎。 Generally speaking this is mostly positive (“mixed kids are so handsome…”)

As adults, we enjoy life in Southern Europe, but a common refrain from local friends is money is bad and entrepreneurialism is frowned upon (“Why are you Americans always thinking about money?”) Work/Life balance might be tilted too much in one direction.

The US is far from perfect but it is my cultural baseline. There is a certain sense of anybody can make it and trying new things is rewarded – I credit that common optimism for most of my own personal success and would like to see Jr internalize it… which probably means life in the US.

Poverty of the mind is the biggest obstacle one can face, so wherever Jr. will be able to have the most enriching life is the place to live.

Got it. That makes a lot of sense. It’s definitely very obvious to me that there’s a lot of pressure to ‘succeed’ academically, which appears to mean ‘become yet another cog in the system’. Definitely not encouraging risk taking behaviour. eg: when visiting a friend in Taipei a few weeks back, she was telling us that her 14 year old daughter is in school from approximately 730am-900pm – no time or energy for anything outside of academics at that point.

As to the comments on the appearance of mixed kids, that’s roughly congruent with our experience. The comments were pretty much all positive (he’s so cute, she’s so pretty kind of stuff). The concern from our standpoint was mostly that the obvious focus on appearance and the sheer amount of comments might not teach a young kid the best attitude. Living in Vancouver, kids of mixed heritage are increasingly the norm, so standing out in this way isn’t as normal for us. :)

Is it possible to utilize FEIE and spend more than 35 days in the US ? The physical presence test is objective and the FEIE is guaranteed if you are outside the US for over 330 days. However how do you claim FEIE if you still spend for example 70-90 days in the US? In my case, I am a resident in a foreign country (with resident permit) and will be getting their citizenship this year. I rent and my place of work is in that country. Will I be eligible to claim FEIE under the Bona fide test if I spend more than 35 days in the US visiting friends, parents, etc? Keen to hear your views.

Yes. But any income earned while you are on US soil is US income. (possible to exclude “vacation time.”)

WTF! We only made a little more and paid $22,000 in Federal tax. That really bites.

I even contributed $36,000 to my solo 401k. Next year will be a lot better, though. I’m not making nearly as much in 2019 so the IRS will get a lot less from us. HA!

That will show them! ;)

Maybe you can work from Thailand?

Another question. Does it really make sense to use credit card to pay taxes given that IRS charges around 2 per cent of the credit card is used? Thanks

Sure. Pay $4000 in tax, pay 1.87% or $74.80. Get 50,000 points worth $500+.

Check out the options.

Why did you not take the Qualified business income deduction (line 9)?

It only works with US income, and a 20% deduction isn’t as good as a 100% exclusion.

I’m pretty sure a laptop is a depreciable business expense? I think you have to depreciate it over 7 years (write off 1/7th of the cost each year for 7 years). No? I had a small business for a few years and tracking depreciating assets (office chairs, computers, some equipment) was a PITA. Then when I shut down the business and sold them I had to figure out how much I had depreciated them and owe/write-off taxes on the gain/loss.

It can be. You can also use de minimus safe harbor election or Section 179 deduction to write it all off in year 1.

“Whenever Winnie pays SE taxes, it is a total loss (since she never worked in the US.)”. If Winnie gets around $6k a year for 10 years (from blog and/or GCC), wouldn’t she get the 40 credits required for SS benefits?

She’ll probably get more by making the choice to get half his ss payments.

Eventually. She might have 10 credits or less now. But even if she qualifies for SS on her own, it will almost certainly never pay higher than 50% of my SS, ergo paying SE taxes is a total loss.

I love these posts. Please keep doing them. Super interesting, and I learn a lot. Speaking as someone who managed to pull a negative effective tax rate this year when factoring in ACA subsidies….

Nicely done.

Question regarding your Credit Card usage for points- when you open a new card for the bonus points, do you cancel your other cards? Or do you just leave them sitting there with zero balance when you move to a new one? Really cool how you maximize the bonus points- wasn’t sure if opening all those new cards negatively effects credit score. Thanks

It all depends: The Credit Card Annual Fee Debate.

Credit scores often go up when you open cards, but the score is largely irrelevant.

What about Taiwan income tax?

$0

I’m curious how it can be $0 if you had foreign income of $57,775? Understanding your Taiwan taxes would be as interesting as the US ones.

It’s not that interesting. Taiwan is a territorial tax country and only taxes income that is sourced within its borders.

There are a whole lot of countries with similar tax systems. (see “resident foreigner = no”.)

Could you elaborate on that?

Does US and Taiwan really have such a hole that you can spend most of the year in Taiwan, and be only resident for tax purposes of US?

In Poland, when you spend >180 days in here, you are resident for tax purposes and you need to tax your worldwide income. There are some double taxation deductions.

Also, if you spend 180 days in one country, and therefore are on tax resident in the US, which exempts a lot of foreign income, even if it was not taxed anywhere else – is that the case?

30% of countries either have no income tax or a territorial tax system. Taiwan isn’t unique here. (see link in comment you replied to.)

This is also the US system for corporations.

If you have locally sourced income in a territorial tax country, you pay local tax. If you don’t, you don’t.

It is strange that more countries don’t go this route. The cost and time required to track, verify, and process non-local income/tax in many cases exceeds any increase in tax revenue.

You mentioned that you had to pay quarterly estimated taxes. Does that mean you figured out all the numbers in this post (approximately) by the end of the first quarter of 2018?

No, I have no idea how much blog or dividend income we’ll get until it happens. Estimated taxes are just a rough guess.

I know this is hypothetical, but how do you think you’d handle your taxes if you didn’t have the large blog income? If all your income was from passive streams? I think this would be helpful to many of your readers who are FIRE but don’t have a large pool of earned income each year.

Probably the same way I did before we had blog income. See 2013, 2014, 2015 as examples.

In a way, it would be nice to have no earned income, as I could replace all of the Schedule C income with Roth conversions.

Very happy this year to get over $5,000 in cold hard cash from Uncle Sam which was then put into a Roth. (EITC + CTC)

It’s nice to be subsidized by all you tax payers ;)

We finally achieved paying no federal income tax other than part of my husband’s SE tax! Of course, it was because it’s my first full year of working halftime and a good chunk of his income will be on next year’s taxes (final payment on a project completed in 2018 was received on 1/7/19 and his commissions for 2018 sales haven’t been paid yet). With the refundable child tax credit (we have 2 boys), his SE tax due was reduced by more than half and we got almost all our estimated payments back. We were finally in such a low tax bracket that when I almost forgot to include our HSA contributions, it barely made a ripple in increasing our return. I also elected to contribute to a Roth as the tax savings wouldn’t have been much.

The only mistake I made was not realizing in time that our income would be low enough to do some tax gain harvesting in our brokerage account.

Thank you for the encouragement and example you provide, I appreciate it!

Foreign income is pretty amazing — something we ought to consider if we end up earning money post retirement.

Weird and good problem to have though, right?

Thanks for these posts, Jeremy. They’re always eye opening. My big takeaway every year is that taxes get way better post-retirement.

My pleasure.

It can be worth just going abroad for a couple/few years – step up basis and convert some Roth, thus having Uncle Sam help pay for the trip.

What are the restrictions around contributing foreign earned income to Roth IRA, Traditional IRA, and Solo 401k?

Thanks for the great post.

You need US earned income to contribute to an IRA of any type.

Contributions to a solo401k are referenced differently in the tax code. See this comment and following links.