Sometime soon the American Rescue Plan Act of 2021 will become law. (See text of House bill H.R. 1319)

With a cost of $1.9 trillion it roughly matches the price tag of the Tax Cuts and Jobs Act of 2017 and the CARES Act of 2019. That’s big.

It even has some big claims, like “Will cut childhood poverty in half.” That seems good.

So… Where does all that money go? And… How will this impact retirees and aspiring retirees?

The American Rescue Plan Act of 2021

Generally speaking, the rescue plan is intended to provide a cash infusion to Americans continuing to struggle from the COVID pandemic. At present, over 500,000 people have died, 18 million people are on unemployment (pdf), and 100,000 small businesses have closed permanently. States are also facing massive revenue shortfalls, particularly those states heavily dependent on oil (Texas -10%, Alaska -40%) and tourism (Florida -11%, Hawaii -13%.)

By distributing cash to those in need and providing funding to accelerate vaccine rollout, in theory we get back to normal faster and with less pain.

At ~600 pages, it’s a big bill. The following is the most interesting to me with some colorful commentary.

$1,400 checks

This is probably the part that most people get immediately excited about. It does seem to get the most attention in headlines…

Each American will be getting a direct “check” of $1,400, with some income limitations (now including students and dependents.) As a family of 4 we will be getting $5,600, for example.

The income requirements are more restrictive than the CARES Act, so some people who previously received stimulus checks will be ineligible for this round, which seems kinda dumb. I’d much rather see just giving money to everyone for speed and efficiency, and clawing back at tax time for higher income households if that was important.

Anyhoo, based on the more restrictive Senate version of the bill, for married couples filing jointly the checks will be reduced if income exceeds $150,000 and eliminated completely at $160,000. For Single filers those thresholds are $75k and $80k, and for Head of Household they are $112,500 and $120k.

These checks will be distributed asap based on your 2019 or 2020 tax returns – because of the income requirements, we don’t qualify based on our 2019 tax return so I spent a few days last week doing our 2020 return. If you are in the same boat, file your 2020 taxes asap.

Affordable Care Act improvements

This is my favorite part of the bill…unfortunately it’s only for 2 years (2021 and 2022) with the intention of making it permanent.

There are 2 main changes –

- The complete elimination of the ACA Subsidy cliff!

- Increased subsidies for everyone under 400% of FPL, with particular benefit to those earning <150% FPL

If you can benefit from these changes, open enrollment continues until May 31st, 2021.

Many people will now benefit from a higher level of coverage at lower cost – Don’t miss out.

Elimination of the ACA Subsidy Cliff

One really ugly aspect of the Affordable Care Act was the subsidy cliff.

For a household earning 400% of the Federal Poverty Level, the cost of health insurance was limited to ~10% of adjusted gross income. But if you earned 400% FPL + $1, you were on the hook for the full cost of health insurance. (For full details, see: Obamacare Optimization vs Tax Minimization.)

When I explored the idea of our moving back to the US, this cliff would raise the cost of insurance for us as a 3-person household from ~400/month at 400% fPL to $1,000/month, costing an additional ~$8,000/year.

But now, the cost of insurance is limited to 8.5% of AGI no matter how high income goes. The cliff is now just a reasonable off ramp.

Increased Premium Tax Credits (Subsidies)

At all ACA qualifying income levels, subsidies are increased / premiums are lower. The following chart shows the difference

The benefits are particularly strong for households earning less than 150% FPL, although all households benefit. A beautiful way to look at this is a chart from the Kaiser Family Foundation (from their excellent overview of the health insurance changes in the ARPA.)

Not shown here, but of huge importance… many low income households would previously choose a Bronze plan because it came with a $0 premium. Not without price though, as those plans often had a deductible of as much as $13,000, which meant choosing between necessary medical care and paying rent or buying food. Now those same households can get a very good Silver plan with reasonable deductibles and additional cost sharing subsidies. Win win win.

(For full details on how the ACA works and how income levels impact premiums, deductibles, etc… see my overview: Obamacare Optimization in Early Retirement.)

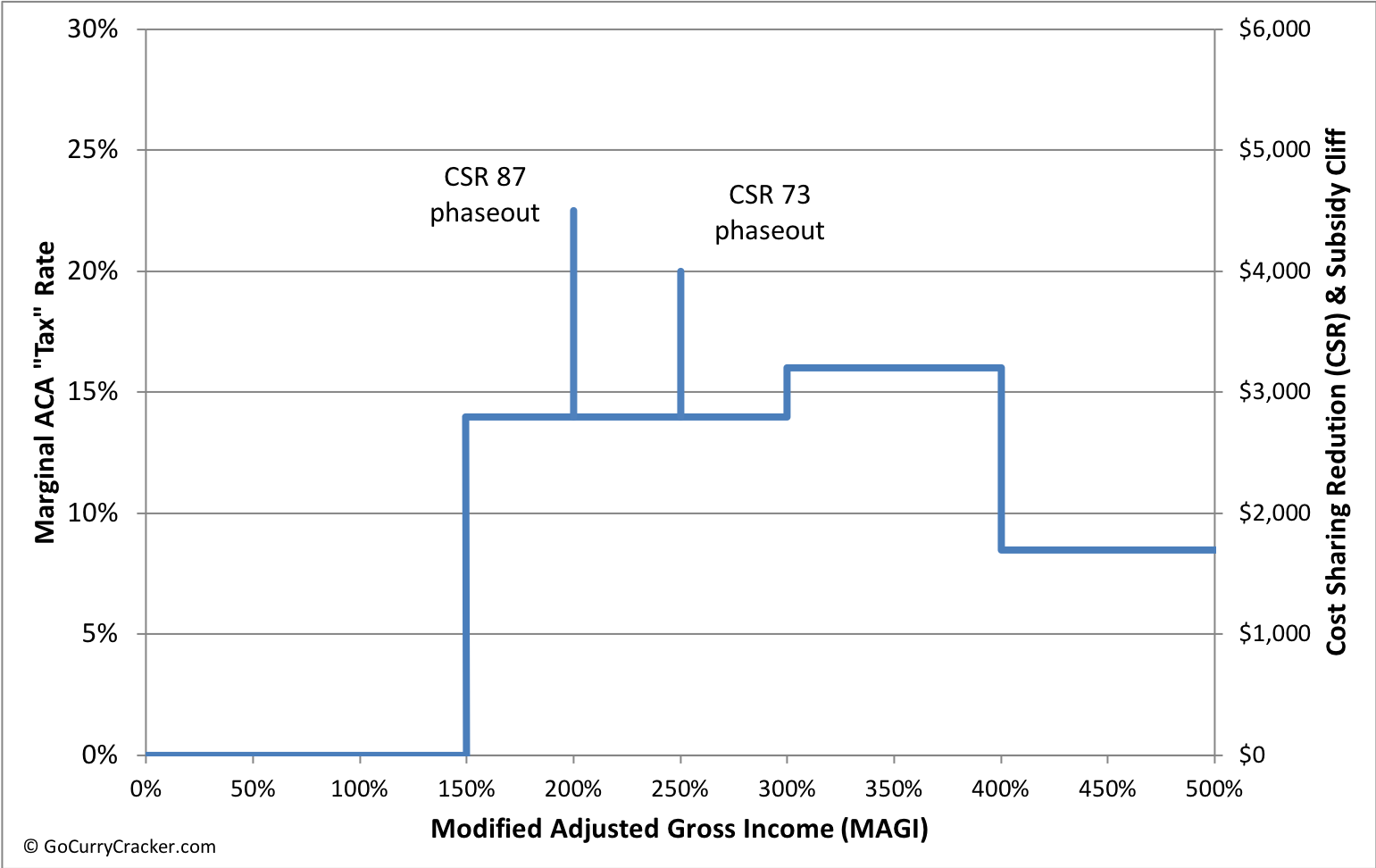

ACA Tax Optimization

With the change in premium subsidies, the way the ACA acts as a tax also changes. The following chart shows how we can model additional income as a tax, with a marginal tax rate of ~15% for income between 150% and 400% FPL. This is useful for deciding whether to do Roth conversions or IRA withdrawals in retirement. Numbers are rounded.

For more details on the prior law and tradeoffs for taxes, see: Obamacare Optimization vs Tax Minimization.

ACA Subsidy Calculator Updated

To explore how these ACA changes impact you, check out our updated ACA Premium Calculator.

Set the Coverage Year to 2021x to explore the changes related to the American Rescue Plan, and to 2021 for the default / prior legistlation.

Expanded Child Tax Credit

The American Rescue Plan massively expands the Child Tax Credit for one year only (2021.)

The CTC is increased to $3,600 for kids under 6 and $3,000 for kids up to age 17 (was 16.)

The credit phases out as incomes exceed the thresholds of $150k MFJ, $112.5k HoH, and $75k Single at a 5% rate ($50 per $1k of income.)

Additionally:

- The credit is fully refundable (will get the credit even if owe zero tax, so ACTC is basically eliminated)

- There is no earned income requirement (previously required earned income to get ACTC)

- Payments will be made “periodically” (probably monthly) starting in July 2021 (with remainder credited on 2021 tax return)

If income is high such that the CTC is reduced to $2,000, then the fall back is current tax law which allows a $2,000 credit up to higher income levels ($200k single, $400k MFJ.)

Related: Maximizing the Child Tax Credit (even without earned income)

With 2 kids, age 6 and <1 year we will get $6,600 in Child tax credit in 2021, up from the expected $4,000.

Unemployment Benefits and Tax-Free Income

Unemployment benefits have been extended and expanded again, continuing levels from previous stimulus legislation through September 2021.

New in the Senate version of the Rescue Plan is an exclusion for $10,200 of unemployment benefits for households earning <$150k. This ~$10k will not be taxed in 2020. (All unemployment income is normally taxed as ordinary income, but not subject to FICA taxes.)

I dislike this implementation in part because it is messy – changing 2020 tax law in March 2021 means anybody who already filed 2020 taxes will need to file an amended return with the time, energy, and expense thereof.

It’s also highly regressive – a household with <$24k in 2020 income will get zero benefit. A household with $150k income will benefit by $2,200… better, imho, would be to just distribute an additional $X to anybody who received unemployment benefits in 2020.

And finally, one of the things I’ve advised people to do in low income years (such as years of unemployment) is to do Roth conversions at 0% / low % tax rates to help with retirement. But that opportunity closed on Dec 31st… alas, you can’t put the milk back in the cow.

Expanded Child and Dependent Care Credit

Again, for 2021 only…

This credit has been expanded from a maximum of $3,000/year to $8,000/year for households with up to $16,000 in care expenses. The credit is 50% of expenses, up from the prior 35%.

The credit has also been made fully refundable (you get the $ even if you owe $0 tax.)

Earned income is required for this credit.

Expanded Earned Income Tax Credit

The qualifying age range for the EITC has been expanded and the maximum qualifying income more than doubled for childless households (or households with children who do not live with them.)

This will namely benefit students and low-income Seniors… who can receive up to ~$1,500 in credit.

This would have been super helpful when I was a student.

More on EITC: Hacking the Earned Income Tax Credit

Additional direct aid to households

The American Rescue plan offers additional indirect aid through existing agencies:

Rental assistance – $25 billion towards emergency assistance to renters

Energy assistance – $4.5 billion to HHS to assist low-income households with utility bills

Backing up the money truck

All of the above has been related to direct aid to households. The American Rescue Plan also offers significant aid to states, municipalities, schools, and the vaccination effort.

Schools – $170 billion to school for reopening efforts and improvements

Internet – $7.6 billion to FCC to expand internet connectivity to students

State and city aid – $350 billion to overcome revenue shortfalls

Vaccine effort – $170 billion to HHS to detect, diagnose, trace, and monitor Covid-19.

Restaurant revitalization fund – $25 billion to SBA to aid small businesses

Summary

The $1.9 trillion American Rescue Plan Act of 2021 is a massive piece of legislation.

Key provisions include direct checks to households, expansion of the Child Tax Credit, expansion of the Earned Income Tax Credit, expansion and improvements to the Affordable Care Act, expansion of the Child and Dependent Care Credit, and more.

It also includes significant funding to the vaccine rollout effort, school reopening efforts, and helping states and municipalities (which would otherwise have been forced to cut services / layoff staff / raise taxes.)

Because this was all passed through reconciliation (avoiding the filibuster) it is all temporary, limited to 1 to 2 years. This does make it difficult to plan long-term, but hopefully many of these provisions become permanent in the near future.

In the mean time, households will benefit with an abundance of direct aid.

Action required:

- Update your ACA enrollment based on the improved subsidy structure prior to May 15th

- File your 2020 tax return asap if you would not qualify for direct stimulus checks based on your 2019 return

- Amend your 2020 tax return if you’ve already filed and collected unemployment benefits in 2020

- Plan 2021 income based on the phase-out levels for the expanded Child Tax Credit if applicable

- Explore how the ACA subsidy changes using our ACA Premium Calculator (set Coverage Year to 2021x for ARPA changes.)

Do you mean as a family of 4 you would get $5600?

I sort of feel guilty getting this even though I don’t live in the States. Especially since it will only be stimulating my brokerage account.

Actually, we do need new phones this summer…

Yes, $5,600. I updated the post. Math is hard sometimes, thank you

You’re still a citizen and entitled to all benefits and responsible for all encumbrances thereof…You vote. You are required to report all of your world wide income and go through the hassle and expense of filing and paying taxes. You still have to pay administrative fees for passports, driver’s licenses / ID, etc…

Great analysis! Mainstream media misses so many of these important details, like the ACA changes.

Hi. Thanks for this. Can you clarify what you mean by “”And finally, one of the things I’ve advised people to do in low income years (such as years of unemployment) is to do Roth conversions at 0% / low % tax rates to help with retirement. But that opportunity closed on Dec 31st… alas, you can’t put the milk back in the cow.”?

Do you mean since Roth conversions for 2020 ended in 2020 so that’s why? Or is there now a downside for doing Roth conversions in general going forward? Thanks.

No issue going forward.

Yes, as you say 2020 Roth conversions ended in 2020. 3 months later they tell us about a special exemption. They say don’t look a gift horse in the mouth (whatever that means) but I did anyway.

My first thought when I heard about unemployment provision was that I was glad that we were still working on completing 2020 taxes.

My second was if I knew the unemployment provision was going to be part of the bill I would have converted 20k of traditional to Roth.

In my family’s case, we won’t qualify for the stimulus checks based on 2019 or 2020 income, but we will be eligible based off 2021 income. Therefore, I believe we can get them in the end at tax time next year by filing a Recovery Rebate Credit form with our 2021 return. Not as great as money now, but I don’t mind waiting a year to get $5600 for my family of 4!

Yes, you should see it on the backend.

We had a similar thing… the previous 2 rounds of stimulus we received was based on a 3-person household. Since kid #2 was born this year, his stimulus income was just deducted from our 2020 tax burden (or will be as soon as I click the file button.)

Wait, what say you? Our household income will be dropping substantially due to the wife retiring early in 2020. We qualify for $0 stimulus now, but will most likely fall within the thresholds for our 2021 income. How can we claim this Recovery Rebate thingie for 2021 taxes?!

Check our your 2020 tax return when you have it. Line 30 of the 1040, “Recovery Rebate credit.”

Should be similar.

Does this also apply to any lost additional CTC, or just the stimulus checks? The +$1,000/$1,600 per child?

When you file 2021 taxes if you are below the AGI limits, yes you would get the full increased CTC at that time.

$30 trillion operating federal debt, $126 trillion in unfunded liabilities. Too much spent on state and local governments who poorly managed their finances before the pandemic. A good number of people do not need these subsidies and cash infusion. We are destroying our children and grandchildren’s future. We should just prioritize on those directly effected by this disease. It is completely out of control.

I find myself on the opposite side of this. I think the kids will be fine, and the opportunities available to them will be greater for these investments.

If you are open to some reading material, The Deficit Myth is a good read.

I am glad that you sleep well at night with respect to profligate printing of paper. Your children will likely be billionaires, like most everyone in Zimbabwe. As for this money being an “investment”, it is an investment only so far as to bail out states who have not had fiscal responsibility for the last 60 years and has little to do with “investing”. You know what is missing in the “investment”? How about a bridge or overpass; maybe new water pipes for Flint; or potholes filled in the Interstate System? Not even a coat of paint is going on an outhouse for the 1.9 TRILLION being spent! Crumbling infrastructure, “zero” interest rates, and no money spent to fix a thing. Just send $$ to anyone who can fog a mirror regardless of their need. Ask yourself, 1.9 trillion dollars and you get $1,400. Each taxpayer is on the hook for almost $20K for that 1.9 trillion, so where did the rest go?

Here’s an interesting thing: I own real estate in several southern states. Every tenant has remained employed and have enjoyed a drop in rent that I provided at the very beginning, out of concern for the unknown last March. I’ve been repaid with loyalty and appreciation. Additionally not one of them has lost a dime or been shorted a single hour at work. On the other hand, my wife’s boy, living in Nirvana, CA., lives with 3 other people in a 1 bedroom apartment and none of them have worked for 9 months due to lock-downs of one sort of another. Oddly, the flu infection rates are the same per 100K people in CA and the states where I own property. One state is a total disaster, requiring tons of Federal Assistance, and the other(s) require basically “zero” assistance. For this gross mismanagement, we print $ out of thin air and reward incompetence.

Deficits don’t matter until they do.

So… not interested in learning something then.

Thanks for helping out your renters.

Scott is 100% correct. What they could not do with the climate alarmist nonsense….they are doing with virus scare nonsense. Covid has become a religion to some. Get some facts outside of the usual criminals..i.e WHO, CDC, etc.

Hmmm, very interesting.

Thank you 1st time commenter with very credible opinions from the deep web

I took your advice and just finished ‘The Deficit Myth’. Wow! That is a paradigm shift in thinking and what a refreshing way to look at OUR economy, the ‘people’s economy’. I got a degree in Economics way ‘back in the day’ and I loved reading this book and am still sorting out some of it in my mind but have an updated way of thinking about the economy now. Of course there are detractors because we are all used to mis-management of the economy. Now, education, management and courage are needed from our politicians. Trying something new isn’t necessarily a bad thing. Thanks for the reading tip!!

I agree, Eduardo. We need to start taking billionaires more, so our children and grandchildren can have a greater future. I think that’s what you’re saying. ;-)

But seriously… if sending money to lower/middle class, funding vaccine distribution and schools reopening, and helping local/state governments (who also manage public health and vaccine distribution, by the way) during a zero interest environment isn’t the time to spend, then when is?

Hello! We just had our first born in February. Do you think we’d be eligible for a direct stimulus payment on the backend when we file our taxes for 2021?

Yes

Your tax posts are the best 👍.

Oh MI

And the info about changes to the ACA may prompt me to switch from a bronze to a silver plan. Boom.

Silver plans are nice, especially below 250% FPL

When will the ACA marketplace reflect the updates that you reflect in your calculator? Can I change from Bronze to Silver now?

As a non-US citizen who’s own country is poor, I find it interesting that the US is distributing so much financial aid to it’s citizens. Do you think there will be an impact to the USD or taxes going forward?

Also, are more focused relief plans too complex to implement versus this helicopter money?

More focused relief plans have speed and efficiency issues – it’s a whole lot easier and faster to just blast the money out there. All projections show a GDP benefit so it then pays for itself, more or less. If things get too stimulated, the fed will just bump interest rates up a bit…

As long as the GDP / debt burden trend at a rate similar to other countries, it won’t have significant impact… ymmv

Great post, GCC! Thanks for all the in-depth info.

Not sure if you know the answer, but would my family get an additional $1,400 for a child that is born in the second half of 2021 if we already received our stimulus payment in the first half of the year?

Yes

Is the check phase-out of $150,000 based on total income before deductions or AGI?

AGI

Will the Child Tax Credit for a child that turns 6 in the middle of 2021 be 3k or 3.6k? Thanks!

$3k

they phrase it something like “a child who hasn’t reached their 6th birthday in the tax year”

Hi Jeremy,

In 2020 our AGI was $240,000 (married filing jointly).

In 2021, we have a 15 and 17 year old, and a 19 year old in college.

Based on this info, do you know how much our child tax credit would be?

Or a calculator to help me determine this. I want to determine how much of this credit we may lose due to our income.

Thank you!

Just back of the envelope here, assuming same income in 2021 I think it will be $4k

The CTC phases out at $50 per $1k of AGI over $150k (= 5% tax rate) but is backstopped by the existing $2k CTC which doesn’t phase out until $400k AGI

Which is still $2k more than you would have gotten otherwise, as under current legislation your 17-year-old would’t qualify

WaPo says you’ll get $4,500 (extra $500 for the 19 year old)

https://www.washingtonpost.com/business/interactive/2021/child-tax-credit-calculator/

Do you know what happens with an unemployment claim filed in July 2020 that’s now on extended benefits. My claim says the benefits end in April and I can file again in July 2021. Does this law change this?

Yes, benefits extended until Sep 2021 – the PEUC (which extends weeks of coverage by the States), the PUA (for Self-employed, etc…), and the $300 additional / week federal benefit all extended to Sept

That’s pretty massive. I haven’t paid much attention to it because I just came back from Thailand.

The ACA change is quite good. Hopefully, they can extend it somehow. My wife plans to quit work next year so our income will be much lower.

We didn’t get any stimulus check in2 020. I’m not sure why. Our income from 2019 was under the threshold. I’ll try to get it back when I file taxes.

@Joe, your stimulus cheque may have been mailed to you and then gone astray. Although the IRS had direct deposit info on file for me, and I specifically requested DD in the “get my stimulus” portal, it was supposedly made to me in Mexico. Haha! So I’ll claim the $1200 credit on my 2020 return.

Wow, I had no idea those ACA changes were happening. Thanks for the tip! I’ll check it out when it finally passes. I only understand 40% of it right now.

Currently we’re on a bronze plan paying no premiums – contributing to a HSA.

Hey does the EITC increase apply to 2020 returns or next year? thanks

2021

Thank you for this post – well summarized. One of the action points listed is to update one’s ACA enrollment based on the improved subsidy structure prior to May 15th. Any thoughts on how this will be reconciled for those who don’t submit a new application? I suppose it will shake out in the premium tax credit reconciliation on the 2021 returns. In my situation I already have the plan I intend to keep, but I do plan to load up on additional Roth conversions. Probably six of one, half dozen of the other on resubmitting the application with a higher MAGI vs waiting to file 2021 return to report the additional MAGI.

As I read it if you have the plan you want you will just see lower premiums automagically, no need to do anything

I have a family member that was below the 138% FPL for 2019 but in 2020, I worked with them to convert Roth to bring their AGI to approx. $24.5k. I expect their AGI to be about the same in 2021. Should I encourage them to go for ACA vs. Medicaid? She is a NY state resident with 2 members of her household.

Is the 8.5% cap based on one’s AGI, or on modified AGI?

Thanks!

There are several different versions of MAGI. All ACA stuff uses this one (pdf)

Thanks for the clarification and the very helpful link. I had been assuming that the MAGI used for ACA would exclude the health insurance deduction for those of us that have self-employment income, but I see now that you do in fact include your health insurance deduction, and potentially have to do some iterative calculations to get to the final ACA subsidy. A little complicated, but I’m very happy to have my ACA premiums capped at 8.5% of something…

It won’t help with the calculation of MAGI, but our ACA premium calculator is a nice way to estimate the premiums.

Yep, like the other relief plans, they just opened the spigots… Let’s hope all ends well.

So, after direct help as you listed how much is left for the infrastructure building, updating, etc. as it’s been crumbling for years? And over what time frame are they supposed to finish these updates?

Yep, I’m also curious how ACA can or will become permanent…? I’d like permanent, but this is a yanking competition in the gov’t and during elections campaigns. I think nothing is permanent except taxes and death.

Infrastructure funding comes later in a separate bill.

If MFJ and 2019 AGI $160k, you have a huge incentive to delay filing your taxes: https://frugalprofessor.com/stimulus-round-3-proposed-senate-phase-outs/

I’m pretty sure I put a more coherent comment down. Not sure what happened.

I meant to say:

* If MFJ

* and 2019 AGI is less than $150k

* and 2020 AGI is greater than $150k (especially $160k)

Then, you have a big incentive to delay filing your 2020 taxes. A buddy of mine missed out on $5.5k because he filed his 2020 taxes a couple of weeks ago. This cannot be undone.

Contribute to a Traditional IRA or two and file an amended return?

Might not get the income now but could at filing time in 2021.

Am I understanding this correctly that for an AGI of $120k with $10k of expenses for one child, the Child and Dependent Care Credit jumped from 20% of $3,000 ($600) to 50% of $8,000 ($4,000; refundable credit)?

Yessir

Twas a max 35% of expenses with phaseout starting at $15k AGI with max allowed expenses per child of $3,000. Now max 50% of expenses with phaseout starting at $125k and max allowed expenses of $8k.

So 1 kid, $8k * 50% = $4k credit. Refundable.

Applicable section of the bill here.

Thanks, I thought so. That’s quite an increase! Any guidance on how the credit interacts with a Dependent Care FSA? I’ve already contributed $3k to the DCFSA in 2021? Should I just stop contributing moving forward and “choose” the credit at filing? (I realize that as part of the bill the DCFSA contribution limit is increasing to $10.5k for 2021. However, in my situation in the 22% MTR the $4k credit > the $10.5k deduction…)

Dunno for sure, I haven’t ever used an FSA so I’m just going off memory… but I think yeah, stop contributing to FSA and get $4k credit, plus also maybe $2.5k deduction for the amount over $8k?

Does the phaseout start at 125k/individual or 125k for MFJ.

I believe it is per tax return and married couples must file as MFJ and both spouses must have earned income.

I’m in the same boat on this. Have the FSA setup currently. 2 kids in daycare spending like 30k a year, AGI 150k. We should stop the FSA then right? This is part of the bill is surprisingly hard to find good info on. Everything is on the checks and the child tax credit but this is likely to be larger than both of those?

2 kids, 16k x 50% = 8k tax credit? the 50% is for all earnings, no reduction based on income like previously where it went from 35% to 20% over 43k AGI?

Try checking the text of the bill itself, here.

Phase out starts at 125k AGI instead of 15k. Starts at 50% instead of 35%. Amount for 2 kids goes from $6k max to $16k max. Etc…

My AGI is 157,900 in 2020 (MFJ, 2 kids under 6). Me and my wife we’re maxing out our 401k already every year.

Is there anything else I could do to bring AGI down below 150k in 2021, other than donating to charity (I don’t think that would pay itself moneywise)?

Through your employer: contribute to FSA, HSA, or HRA, deferred compensation, short term unpaid leave

Personally, any of the above the line deductions: education expenses, student loan interest, etc…

Thanks. I’ve checked with HR, they don’t allow me us to open an FSA cuz our insurance is “very good”. HSA already have. Deferred compensation I’ll have to explore, not sure they or even I like the idea though.

No loans, debt or mortgage (renter for life) and nothing big enough to itemize. Thanks anyway.

An FSA is for child care so I’m not sure how that is related to having good insurance.

But I suppose the overall point is there are zero good options – your income is “high” so you don’t qualify for a lot of the stimulus benefits.

The least worst option would probably be to take 2 weeks off unpaid. If you are getting ~$3,500/week in pay that drops you to an AGI of about $150k. If you get $5,600 in checks as a result it is a bit like a free vacation.

oops, I think I’ve asked them about HSA instead of FSA.

Great point on the free vacation. I’ll see if I can do just that.

Thank you very much!

Hi Jeremy,

Am I correct to think that 2021 and 2022 are both good years to realize huge long term capital gains(or Roth Convert) due to elimination of ACA Subsidy Cliff with premiums maxed at 8.5% of MAGI. I currently have a Silver Plan and quite happy with it, as an early retiree relying purely on investment income. I’ve been making sure my MAGI is right below 400% of FPL the past few years. Thanks

Maybe, if it means paying less tax now than you would pay on the same gain in the future.

I’m not sure that would be the case for everyone

The increase of EITC investment income limit to $10,000 is going to help out a lot of people. Either they can do a little bit of tax gain harvesting (although keep in mind that 21% effective tax rate, so you should plow it back into a traditional IRA), or you could have “normal” investments that pay dividends instead of trying to manage bank accounts to keep within the artificial $3,650 limit.

The two graphs in the article must tail off somewhere to the right. Marginal ACA Tax Rate surely doesn’t go on forever. And one wouldn’t pay 8.5% of a million dollar income for an ACA plan.

If the unsubsidized retail price of the insurance is less than 8.5% of income, you would just pay that.

Example:

Retail price for silver plan for family of 3: ~$12,000

Income level where 8.5% is 12k = ~$141k (~650% FPL)

Below that $141k threshold, you still get some subsidy and pay just 8.5%. Above that threshold you pay $12k. At $1 million income you pay $12k instead of $85k.

Thanks! That makes perfect sense. Should have been able to figure it out myself. :)

No worries – this stuff is always needlessly convoluted

Thanks for the note about the expanded Child and Dependent Care Credit. I had not heard about that one. Have you seen anywhere that shows what the new table will look like that is typically on Form 2441? This helps determine what percentage is for the credit based on income. Thanks!

I haven’t seen a new table but from reading the legislation it looks like the phrase out rate (slope) will be the same (lose 1 percentage point for every $2k increase in AGI), just starting at a much higher threshold

Hmmm. Thanks for the info on the new ACA subsidies. We live outside the US, but return in the summers to work. We have a low AGI (~$60,000mfj, family of 3). I’m wondering if we could sign up for a basically free bronze plan with an HSA to have a bit of coverage (beyond our woefully inadequate travel coverage offered by our Spanish company)?? The main advantage would be to have access to an HSA where we could shelter more money thus allow us to do more Roth conversions… What do you think?

I haven’t been through any of this process myself, but this is my understanding.

If you are a bonafide resident of Spain (or whatever) then you are exempt from getting minimum essential coverage while in the US. Else, you are required to enroll in the ACA if you stay in the US more than 35 days. See: Obamacare, Expats, and Limitations on Visits Home.

As part of that mandatory enrollment, you could get a Bronze plan with an HSA, yes. If you have an HSA for 3 months, then you can contribute 3/12ths of the legal limit.

Thanks for the reply! We’d keep a free bronze plan the whole year to be able to put more into the HSA, even though we’d only need 3 months of insurance. I’m still on the fence about it though. Basically, the US government will be paying an insurance company a boatload of money on our behalf for health insurance that I can’t use in Spain. I feel dirty just thinking about it, but financially it makes the most sense for us. I wish The US would just embrace public healthcare for all and leave the greedy middlemen out of it.

I think the risk you run is that an eligibility requirement for subsidies is that you are a resident of the US and a specific State.

If the IRS decides you are a resident of <non-US country>, perhaps because you use the FEIE or FTC or you just pass the bonafide residence test or <reason>, then you could be asked to refund any subsidies. Which would be a bummer.

I was looking for the exact phrasing in the law and for lack of time to search here is one data point:

>Can I still purchase a US health care insurance policy if I reside outside the United States?

>No. In order to buy the insurance as an individual, you must be living in the US

Thanks for great information, as always. My SIL lost her job and claimed unemployment last year. Two of her dependent children also were unable to work and collected. Do all 3 each qualify for $10,200 exclusion? Or is it limited somehow if you’re a dependent? Thanks

I searched the comments and didn’t see mention of this so I will ask, what are your thoughts on the Student Loan topic? I heard that this bill also said something to the effect of IF student loan debt is forgiven, it will NOT be subject to income tax via a 1099 to the student. Clearing the way to there not being a penalty on the student (taxes) if the government decides to forgive any student loan debt, like $10,000. Thoughts?

No thoughts really. If student loan forgiveness becomes a thing it is nicer to pay zero tax on the gain.

Sometimes I feel like all of these programs are designed specifically around not paying me (I’m just over the cutoff and no dependents). Anyway, I wonder where all of this printed money will go.. stocks? crypto? processed food?

Another way of looking at it – the system already pays you really well. Congrats

I’m on ACA healthcare and responded to the recent notice sent to me to look at revising my application to save money on premiums. I did that and found that the same plan will have a lower premium, with a higher income reported (I can do a larger Roth Conversion). I was suspect about plan deductibles and OO pocket expenses so I fished around Healthcare.gov quite a bit and found that in fact there is a risk in re-applying to your insurance company, mid-plan year. My question is, if I’m happy with my monthly premium as is, can I just wait until doing 2021 taxes to work out the new benefits of the ACA/Recovery Plan? This way avoiding all possibility of getting hit with a new deductible to fulfill, as I’ve already paid it and much more.

You don’t need to do anything, the improved ARP premiums will be applied automatically for the existing plan.