On a recent visit to the local library I picked up a random book from the non-fiction display table, Die with Zero by Bill Perkins (affiliate link.) Interesting title.

Within this book Mr. Perkins presents a life philosophy and a set of 9 rules to “get all you can from your money and your life.” At the heart of things is the idea to spend every penny you have, to die with absolutely no money remaining.

I think the ideas are worth a perusal by anybody considering retirement (early or otherwise) – worst case it will challenge some core assumptions. Best case – new thinking will enable leaving the work force years early.

Die With Zero

The idea to die with zero isn’t new. In the movie Oceans 12, Saul Bloom calmly states, “I want my last check to bounce.”

There is something a little romantic (morbid?) about spending your last dollar with your final breath. I’m a big fan of utilizing every dollar we have or will have before “skidding broadside into the grave.”

Perhaps that is why this book caught my eye.

The overarching approach to life and money management in Die with Zero is roughly as follows:

You are going to die.

But before you do, you will decline – certainly physically, but perhaps mentally. Do the things you want to do before your body rejects your ambitions. Summer in Paris is more fun at 45 than 85.

Die with zero

Every excess dollar at death is wasted time – time spent working for more that was (in hindsight) completely unnecessary. You should have retired earlier – or – spent more money creating memories. Or both.

Invest in (quality) memories

Memories pay dividends every time you think back or tell a story. Shared memories with friends and family multiply the return. Memories at age 20 pay greater dividends than memories at age 60 due to the time factor.

We retire on our memories

Reflecting on our past is the most common activity for the elderly. If you have only memories of the office, retirement may be boring and empty. Invest in memories for the long term.

I think there is a lot of benefit to this view on life.

Early retirement enthusiasts often err on the side of (extreme) caution, saving too much, spending too little, waiting too long…

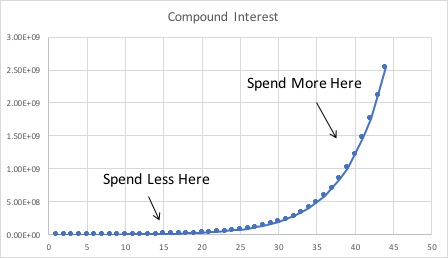

But the odds are in our favor that we will die with a great deal of money. Compound interest is an incredible thing.

Better to spend some of that sweet sweet moola on good times in the here and now.

Which leads to some of the general criticisms of this life approach discussed in the book:

Won’t somebody think of the children?!

Money planned for inheritance doesn’t belong to you, it belongs to your kids. Instead of giving a random amount of money to them on a random date (when you die) give them money now – for college, home down payment, wedding, car, etc… As a bonus, since we are still alive we get to share the experience and benefits with our children (“creating memories.”)

What about end of life care?

We may need critical care at the end of life – in that situation, one of two things happens: the government pays for it (insurance) or you die. It’s not possible to save for a bill of that magnitude, so why waste years of the best time of your life toiling away just so you can spend all that money to extend pain and suffering for a few days at the end. Many good years are worth much more than a few bad days.

Living too long

It would be scary to outlive the life expectancy tables and run out of money when there is still an abundance of vitality remaining. Sure, that would be bad. That is what annuities and reverse mortgages are for if you happen to be really into bicycles, barbells, and salads (and have incredible genes.)

My thoughts

We humans tend to like things with which we are familiar and in agreement – as a relatively young retiree who spends more than is necessary, I enjoyed seeing another approach to “getting all you can from your money and your life.”

Early retirees tend to be a conservative bunch – the more conservative you are, the more this book may benefit you.

Take a moment and find peace with your own mortality. Quit working earlier. Spend more. Sounds good!

All that said, there are a few areas where I think Mr. Perkins’ recommendations are sub-par.

The author recommends spending all of your income (and then some, maybe) when you are early in your working life, because “you will make so much more later.” This is “worth it” because the memories of backpacking around Europe at age 20 (or whatever) will create a lifetime of memories.

Thing is – you can create happy / positive memories in many ways that don’t involve getting the clap in a hostel in Istanbul and actually cost much less

For example, we took a very aggressive approach to saving early on. We treated it like a game and many of our best memories were birthed as a result – For example, is it true that our honeymoon cost $0? Yes it is. Did we also have a second free honeymoon in Hawaii? Yes, that is also true. Great memories at a great price.

And while Die with Zero is a nice catchphrase, and I’m fully on board with people working less and spending more, I think it is a terrible goal.

Why? Because the difference between dying with zero and dying with millions of dollars is extremely small. Using the prototypical example of spending $40k/year on a $1 million portfolio (i.e. the 4% rule scenario) – in some historical cases spending $39,600 per year results in runaway portfolio growth but spending $40k means no money after 30 years. In what universe are we unable to create great memories by spending 1% less?

Or… live really well for a time whilst spending a little less. Then, when the compound interest curve goes to the moon, spend more. Just because you accept that you are going to die in 30, 50, 80 years doesn’t mean that we can’t pause to do a little math.

Wait just a smidge. Spend a teeny bit less. Then go big.

Summary

The book Die with Zero by Bill Perkins (affiliate link) is a good read and worth the time investment. It’s probably available at your local library.

Taking a moment to reflect on our own mortality is always a good idea. Using that perspective to guide our saving and spending is also good – Every dollar we have at death represents wasted time is a powerful idea.

Dying with zero is a goal much like “I want to be a better person.” We get some benefit just for trying. Many can benefit from the idea to save less / spend more.

However, since the annual spending limit difference between Die with Zero and Die with Millions is often small, I think it better to let compound interest have just a bit of a longer leash… thus increasing the odds that we can have it all.

I have added Die with Zero to my recommending reading list.

“Instead of giving a random amount of money to them on a random date (when you die) give them money now – for college, home down payment, wedding, car, etc… As a bonus, since we are still alive we get to share the experience and benefits with our children (“creating memories.”)”

Growing up in a family who made sure we always knew to “pay yourself first” and to always carry zero debt, I also greatly benefited from my folks sitting down with my sibling and I and saying that instead of leaving us an inheritance when they passed, they wanted to help us out *now* while we were in our 20s and 30s and could actively build on the boost they were giving us. It was an intergenerational team effort; for example, a significant gift towards my house down payment meant I could really save more aggressively – and also did so starting at a younger age than most people can – as my monthly payment was lower.

They also wanted us to be able to enjoy our own families when we had young children, and have flexibility in those early years when the kids were young. Over the years they’ve gifted us with experiences: renting a big house for an extended family trip over everyone’s spring break for the cousins and grandparents to all spend time together.

They purposely front loaded our inheritance so that it would have the longest ripple effect on our lives. And our own kid’s lives. I’ve already talked with my teen about how they can live here post-college if they want to aggressively bank the money saved on housing and get a head start on their own wealth building.

I was in the save every penny and sacrifice group but my hubs was in the live it up while you can group. So we met in the middle with doing mini-retirements every other year and taking 3 to 4 week vacations, and doing road trips every other month. Then we did the work where you would want to retire move and still are on track to retire at 55years if we want. I am glad we did those things in our 20s, 30s, 40s, and those were different experiences than we would have today. Our kids are able to build their own wealth so we don’t feel compelled to leave them anything, we only need to sustain ourselves.

Thanks for posting this, Kate. Do you think there was any downside to your parents giving you this kind of largest earlier in life?

There haven’t been downsides, on the contrary, I think it’s made us closer as a family and we know how immensely fortunate we’ve been. Our folks both had rather catastrophic financial circumstances occur in their own families when they were children and so conversations about money, savings, and debt were regular topics from a young age at our house. In our early twenties they included us talking through long term financial decisions they were making, and we talked about the impact of these specific early gifts (e.g. house down payment) would make, versus a (likely) larger inheritance decades from now.

In their opinion (which I share), those gifts enable us to both save and invest AND have more quality time with our children and position our kids on the same “savings minded” path as well. The alternative would be my sibling and I receiving a six or seven figure lump sum in our late 60s or early 70s…which as my folks said: what would you do with it at that age, when a different amount could change your lives now?

Our family philosophy is: avoid debts, save, invest, pay it forward.

Because my sibling and I were raised with a frugal mentality, having significant help with a down payment did NOT mean we started splurging on clothes and cars and toys. Not that there were strings attached to that gift, but we all had shared values around debt, spending, and the impact that saving and investing early has.

Do I think they would have felt differently, and not made these decisions around a “front loaded inheritance” if my sibling and I were spendthrifts? Oh, I’m sure they would! I wouldn’t make a carte blanche gift to a young adult who is cavalier with money either.

Another thing that they did was fund 529s for their grandchildren with significant lump sums the month they were born. And that’s *their* inheritance. Having those amounts grow over 18-19 years means that their grandchildren will likely graduate from college debt-free, and be able to also start saving aggressively in their 20s as well. The amount of the 529 was not something that I shared with my teen until just this year, as an 11th grader, when I knew that they would fully grasp the impact this is going to have on their own life, and they had already been working hard at school all these years on their own.

And because I’ve had money conversations with my child for years, they are also well versed in credit, debt, mortgages, and investing, and they started investing a portion of their lawn-mowing and babysitting money in VTI when they were 15 – and continue to do so every time they a neighbor hires them for odd jobs.

That was all a long way of saying: there has not been a downside, rather I’m immensely grateful for how smaller yet significant amounts at key times have made it possible for me to be even more aggressive in my own saving and investing, versus thinking there will be a pot of gold inheritance when I’m retired. And it’s given me the ability to pass this mindset and method on to my own child in ways that will continue into their future as well.

Blogger ESIMoney did a 5 part book review series on this book. Link to last part of series (which has links to the previous 4).

https://esimoney.com/how-to-die-with-zero-rules-7-and-8/

We have always done a reasonable amount for our only child, and will continue to do so in our retirement years that we are currently in. She left school with no debt, we held her mortgage at zero interest (and we absolved the last $36K or so this year), give them large financial gifts at Christmas and birthdays, etc. But since the wife and I are in good shape financially and most things are paid for in our life, our assets have continued to grow in retirement. I guess this means our daughter will reap the benefits while we are alive, and hopefully even more after we are gone.

We already travel a lot, have a large house on acres of land, and so forth. Our joke is that if we ever won the large lottery we probably wouldn’t change our life at all except for going homeless and traveling all the time. The biggest beneficiaries while we are alive would be our daughter and son-in-law, our favorite charities, and maybe a few relatives. I don’t have a problem with that at all, and have no reason to die with zero. Too many unknowns for me to ever want to do that.

We won’t die with zero by a large margin, for a similar reason. Just wait a bit until the compound interest curve goes straight up and then spend whatever you want/need without the need to go to zero.

We are still TBD on the kids – I have earmarked funds for education. I do like the idea of giving $ while we are still alive, so there will probably be a house down payment, etc…

Australian Age Pension is means tested (ex-home) welfare paying $A38,000 / y for couples 67+.

Assets of $A405,000 (full pension) earning 5.43% provides $A22,000 / y.

Tax free threshold for couple is $A60,000 / y.

Cost of living for home owner couple is $A20,000 / y.

Cost of entertainment is $A-what-ever.

When income – expenditure > 0 government guaranteed (?) for life and the utility of spending is negative (too much food – health suffers, inconvenience and time wasted on unnecessary home improvements, …, etc): DON’T SPEND.

Thanks for the recommendation. Just placed a hold on an e-copy of Die with Zero at our local library. Sounds similar to Stephen Pollan’s earlier book, Die Broke, which was also good.

I also added this to my library queue, thanks

9 Rules To Live By The Die With Zero Philosophy

https://www.debtfreedr.com/die-with-zero/

Almost succinct – unlike the vast majority of books that pad pages with repetitious over elaborations.

Also free – saving the kid’s inheritance.

Hi. (We talked a year ago. I ended up buying a townhouse. I see you similarly bought lodging.) This question is only tangentially related to this post, but, as to optimizing our savings vehicles so we maybe don’t go broke too long before we die, I wonder if you have any thoughts about the potential/probable end of the backdoor Roth?

Welcome back to the States.

Number of backdoor Roths I have done in my life: 0

See: The Great Roth Controversy

I will read this one. I get a lot of fun out of building up assets. So it will be good to read this as a counterargument.

Loved your points about having fun without spending a lot as well as the power of waiting to Go Big.

A few times recently I was trying to figure out how to save small amounts of money on purchases we were going to make anyway…. which is a bit silly. So the Mrs walked by and whispered “Die with Zero” at me…

lol. I don’t think analyzing “value for the money” will ever go away. It is kind of fun anyway.

This whole post is timely as we approach coastFI. Maybe it will happen much sooner than planned. I’ve read https://www.gocurrycracker.com/you-will-die-before-you-run-out-of-money/ a few times and although I agree, the fear is still there.

Value for money is good. Sometimes it is too fun though and I can spend hours just to save pennies.

I doubt the fear will go away until you are on the other side of the compound interest curve looking back. It wasn’t until our portfolio exploded despite out spending that we really relaxed about everything and allowed our spending to increase.

The premise that spending more makes you happier is flawed. That’s not how life or happiness works. That’s my biggest argument with the concept of dying broke. And I’m not a proponent of giving significant amounts of money to grown kids. I’m fine with paying for a four year degree but after that I think you do a disservice by taking away their independence and ambition. If you help finance a lifestyle (house, cars, vacations) they could not otherwise afford you are putting them on that hedonic treadmill and dialing up the speed. And if you no longer can keep those parental welfare checks coming?

Well… all things being equal that is probably true. But all things aren’t equal at various spending levels.

In any case, let’s say spending more doesn’t change anything. The author of Die with Zero would most likely say quit working even earlier. (say with 70% as much as the 4% rule recommends.)

Definitely something to consider about giving kids money.

My parents gave me a car and it allowed me to max my 401(k) instead of making car payments. So I think first and foremost is teaching the kids financial responsibility. Giving them money just highlights what they already are. For example giving money to a child who lives beyond their means is bad for them. Giving a child who is already doing the right things with money will increase financial responsibility even more. Every child is different even from the same upbringing so you have to use your best judgement according to your family values.

I think it’s better to be frugal at the beginning of your working life as well. You can save more and let the power of compounding work for you. Yes, go backpacking in Europe. No for a luxury trip. You can still have fun without spending a ton of money.

Living like a poor college student for a few years longer than is socially acceptable enables retiring a few years earlier than is socially acceptable.

What is your perspective on this topic now that we’re in a period of a bit more economic uncertainty – still spend more/save less/quit working earlier?

I’m guessing you would put us in the “wait just a smidge, spend a tiny bit less” cycle, but what if the smidge ends up being a decade of stagnation, or worse, recession?

The 4% rule comes about based on the worst times in economic history. Else it would be called the 5% rule or the 6% rule.

Times are always full of economic uncertainty. Is this time worse than the worst we have ever seen?

Super interesting book!

A bit of a side question for your Jeremy. Assuming a significant amount of people is following the book’s advices and decide to live off their investments and stop working while still in their 30s or 40s. How will the world still function if everyone is not going to a regular job in a capitalist economy?

Dunno – odds are low though