We have been living off our portfolio since late 2012. Along the way I’ve made only minor adjustments – annual rebalancing, minimizing long-term taxes with capital gain harvests and Roth conversions, and adding the occasional small chunk of fresh capital as blog income allowed.

But after ~7 years of the stock market trending upward, and the conscious decision to spend more, in early 2019 we took some money off the table (sold stocks / bought bonds.)

When literally everything went to hell due to COVID-19, we sold some of those bonds to buy stock and increase our cash cushion..

After all of that… This is what our portfolio looks like in 2020.

GCC Asset Allocation

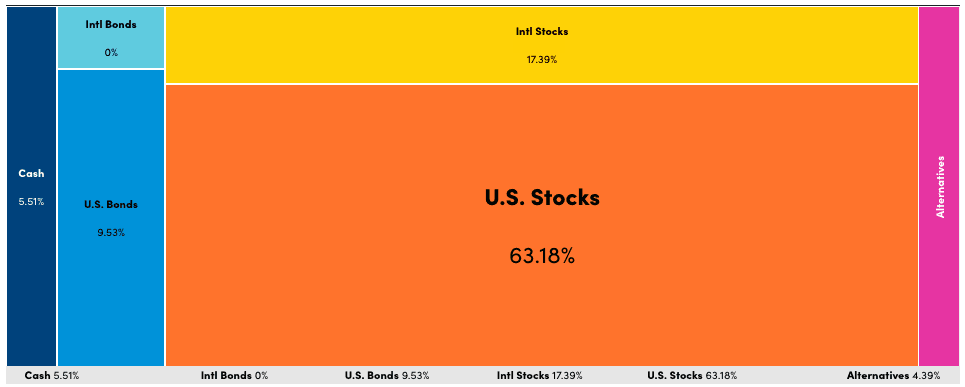

As of early April 2020, according to Personal Capital our portfolio looks like this:

Strangely enough, despite the COVID-19 craziness and 2019 being one of our most expensive years yet, total net worth is a few percentage points higher than last year.

The biggest change over previous years is a larger percentage of bonds and cash. More details to follow.

Data from previous years: 2016, 2018, 2019.

Assets and allocation

US Stocks: 63% -> ~77% VTI, plus 20% S&P500 and 3-4% Small-cap trusts in my old 401k

International Stocks: 17% -> ~93% VXUS, 7% VWO, and small holdings of Vanguard MFs in our HSA

Bonds: 10% -> ~75% Municipal bonds (mostly MUB, some VTEB), 10% intermediate term Treasuries (IEI), 15% I-bonds (not shown in the chart, about 2% of total)

Alternatives: 4% -> 100% VNQ (a REIT.)

Cash: ~6%

Some interesting ratios:

Stock / Bonds-Cash: ~ 84 / 16 (trending away from 100% equities)

US / International equities: ~ 80 / 20

Taxable / Pre / Post-tax: ~ 72 / 21 / 7 (Roth is trending up – was 0% 7 years ago)

Took Money Off the Table

About 1 year ago in March 2019 the Mrs and I were having a chat about our future – should we try one more time to have a second child, will we move back to the US at some point(?), if we end up in California should we buy a house or rent, etc… (The GCC household has amazing pillow talk.)

We also continued a recurring conversation: “Our investments have returned more than we ever expected. The market has gone straight up for 7 year… Should we take some off the table?”

Perhaps being less aggressive with our asset allocation is appropriate – We have consciously increased our spending and our life choices have reduced our geographic arbitrage and budget reduction flexibility. On the other hand, we are a year closer to Social Security income.

By taking $ off the table, worst case we reduce the odds of dying with $1 billion – Best case, we are less likely to require implementing austerity measures if the market goes against us (and wouldn’t you know it…)

Long story short, we sold a bunch of stock – I took what started as a massive capital gain harvest (~$100k capital gain) and just parked it on the side in municipal bonds. This brought our stock/bond split to ~80/20. I then put some of those bonds back into equities during the coronavirus crash, for a current allocation of ~85/15.

Thanks to ~$175,000 of tax free harvested gains from years prior (saving $26,000+ in taxes), an additional $100k gain means a significant chunk of capital with a very small tax bill. (I’ll review this in the near future when I post our 2019 taxes.)

For a step-by-step example of what harvesting a capital gain looks like, I’ve written a template based on the trades I executed in December 2016. Drop your email address in here and I’ll email it to you.

Portfolio Expense Ratio

Through absolutely zero effort on our part, the total cost of managing our portfolio continues to fall, dropping from 0.08% 7 years ago, to 0.06% 4 years ago to <0.05% last year… and now to 0.03%. On $1 million, a 0.01% drop is a savings of $100+ per year.

Some of this is because my old work 401k continues to negotiate lower prices on the asset trusts they use, and part is from Vanguard continuing to drop expense ratios. I’m looking forward to the days when they start to formally pay us instead.

Retirement Account Fee Analyzer by Personal Capital

Plus, now that many of the big brokerages charge zero trading fees, we also no longer pay $20-$50/year for cap gain harvesting and portfolio rebalancing.

Reward Points

While not a traditional asset class, we have continued to build a healthy amount of airline, hotel, and travel rewards points through credit card signup bonuses. Despite using a ton of points over the past couple years, our point hoard (and credit score) continues to be worth a healthy chunk of change.

One example of point usage: $16,000 business class flights to Europe for $300.

Alaska Airlines: 119,663 miles (+40,000 after tax season)

Amex: 0

Asia Miles: 1,200

Capital One: 133,232

Delta Airlines: 9,281

Hilton: 27,051

IHG: 37,859 (+140,000 after tax season)

Marriott/SPG: 135,219

Ultimate Rewards: 132,255

United Airlines: 19,789 (+40,000 after tax season)

Total value: $8,933+

Our pile of points will increase in the coming weeks as I make our tax payments for the year.

Yes, I’ll be paying taxes on the $100k capital gain harvest with 3 credit cards (when they are due in July.)

We don’t have any travel planned as we are quickly coming to the 3rd trimester of Winnie’s pregnancy (plus borders are closed anyway) but maybe Jr and I can do a quick ski trip late 2020/early 2021?

For ideas on how to accumulate or redeem award points, check out our Award Travel Series!

Final Thoughts

When you’ve already won the game, you can either let it ride or stop playing.

We are now older and less interesting so in Q1 2019 we did the latter, selling some stock in exchange for some bonds. When the market dropped in Feb/March 2020, I sold some bonds and exchanged it for stock and cash.

Our portfolio now stands at 85% stock / 15% bonds-cash and 80% US / 20% International. This is the least aggressive we’ve been, about a 10% shift in stock/bond ratio. If the market cooperates and tests the lows again, I’ll convert more of those bonds into stock.

Nice, agreed on changing allocations. Also, you can count your business income towards a diversification on the income scale as opposed to looking at just assets?

On the income side, I’m looking at getting a nice 33/33/33 split between dividends, bonds/fixed income and business income. At 1.5% net divi yield, 4% net fixed income yield and business income, I’ve recently reached that 1/3 income from each source, and I feel it helps with resolving the day-to-day side quite well. After these 2 years I still feel like income and production makes more sense to me, rather than potential net worth consumption for income.

Lastly, well done, just wish my home bias country had also been the US =)

I just assumed any business income was temporary and would go to zero if the bad times ever arrived.

Seems like that was mostly true – all of the big revenue sources have collapsed. We will just continue forward spending less than 4%, some dividends and interest and the occasional stock sale.

Question for you guys. Why do you buy municipal bonds? I assume it’s because it’s in your taxable accounts, but from my understanding, especially in FIRE, the low tax bracket you guys are in actually invalidates the value of tax-free bonds because all things considered (growth not just distribution) they yield less than say VBTLX.

I heard muni bonds are only worth it when you’re in the highest brackets? Love your comment on that!

Do the math.

Current yield on IEI (3-7 year treasury ETF) is 1.75%.

Current yield on MUB (Muni bond ETF) is 2.22%.

Our current marginal tax rate is 27% (credits reduce total tax burden to ~zero.)

For doing taxes what do you use? Do you download an HR Block software?

I just use Turbotax

More here.

Interesting update during interesting times.

January of this year we scaled back from an 85/15 allocation to 75/25.

This was not because of my crystal ball, we just decided, through pillow talk as well, that we were comfortable with getting less aggressive as we neared retirement.

I recall a comment in one of your posts (I honestly can’t remember which one) about Winnie stating “you already won the game why keep playing” kind of resonated with me a bit…. just a little bit.

The plan was to take off into the world this fall for our dose of geographic arbitrage. However, considering the current state of affairs we have decided to work a bit longer and pump a bit more into the funds.

Could be great timing… Maybe we will go on another decade long bull run after this, decreasing our sequence of return risk Who knows. Either way, we should be fine.

If you go on that little ski trip, be sure to post some photos of junior tearing up the slopes.

Stay healthy

I was thinking of taking more off the table this year (back to about 80/20), but didn’t get around to it before the big drop. Crazy times.

Were I in your shoes I would probably wait and see as well. The future is cloudy.

We rode skateboards for about 3 hours yesterday, so I think this winter Jr might be ready for the snowboard. He tore up the mountain this winter on skis.

Always love reading about asset allocation posts. We’re a bit conservative and are sitting closer to 60/40 as we approach our FIRE date next year. We’ll do a glide path over the next 5-10 years back to our higher stock allocation. We had been 90+% stock index funds up until a year or two ago when we started shifting into more bonds and cash (in a high interest savings account). We’re also conservative in that we’re looking to pull a sub 3% withdrawal rate. I’ve shifted over to part time work last year which has been such a game changer. My wife retired when our little one was born 2 years ago and I feel like I’m retired (only working 73 days a year) yet we’re maintaining a 50% savings rate. For us, it’s all about designing the life we want to live along the way.

Sounds like a solid approach and great life balance.

Not too different from my own. I have a bit more in U.S. stocks, none in bonds, private real estate (that I don’t manage), similar amounts of cash, but no international. Like you, I do maintain a multi-year buffer of cash for rainy days such as now. Cheers and thanks for this update!

I don’t normally keep this much cash – I just did it for this special occasion.

subscribe

good choice :)

“I’m looking forward to the days when they start to formally pay us instead”

This may already be happening :). Under the hood of those Vanguard etf’s (VTI + VXUS) they return 100% of the securities lending revenue (SLA) in the form of dividends. So, the “effective” cost (0.03% E/R + SLA revenue) may be close to zero or negative.

Also, one question: why not hold a portion of bonds in pre-tax accounts (e.g. 401k)? Then you can do a 2-step “sell equities in taxable / swap bonds in pre-tax for equities” keeping your overall AA the same. This may also open up some additional TLH opportunities and would slow growth in pre-tax to avoid larger RMDs in the future.

Yes, it is in practice. By formally I meant I would like to see the expense ratio as a negative number – make it a contractual and ongoing thing.

I do hold some bonds in pre-tax accounts (All of our IEI is in a Traditional IRA.) I do it that way primarily to eliminate the yearly tax burden on interest.

With regular Roth IRA conversions, I’m not at all concerned about RMDs being too large (or 401k being too big.) You could try to reduce growth in the IRA to avoid it, but TLT up 25% this year while equities down 25% so TBD if it works out. Careful with harvesting losses and repurchasing the same asset in an IRA – in theory that makes it a wash sale, but permanently (can never claim the loss, but unclear if IRS will enforce it.)

Well, certainly looks like you made some good moves. Just interested to know, how high of an allocation are you willing to give stocks if things get REALLY ugly? 90% -95%? 100% god forbid?

Ah guess it doesn’t really matter since you already won the game though 😉

If the yield on the SP500 went above 4% I would see that as motivation to go 100% stock. This could happen if the SP500 falls below 1500 (or whatever) or maybe stock buybacks are banned once again and more corporate $ flows into dividends.

That said, we started thinking of the “off the table” funds as possible house or kid’s college fund, so as those events come closer we’d have to start pulling funds out of equities again.

House? You?

if only to annoy certain people :)

Longtime reader, 1st time commenter. Thanks for all of the great posts over the years. Enjoy them and learn a lot. I am 7 years away from expected retirement at 59.5 yrs. Not sure what appropriate denominator is for savings rate, but still 100% VINIX and VIIIX, pumping in $90K annually into retirement accts even during the downturn. Stubbornly staying the course come what may, based on prior committment to an aggressive strategy. Will reallocate once I am closer to retirement. If still not at target, may work a little longer. Life could be a whole lot worse, and I am super thankful for what I have, financial and otherwise. Stay safe everyone.

Continuing to have a well-paying job is a HUGE asset! That was my blessing in 2008 when I was able to continue plowing into equities at lower prices

Yes, having a job is huge during times like this. My organization has committed to no layoffs or pay cuts until at least the fall. Good feeling. I will follow the same strategy until then.

Take care,

Max

$90K annually into retirement accounts! Impressive. With a savings like that are you sure you’re not already able to retire?

I follow the aggressive strategy for when you are still saving for retirement as well. Lets hope this latest bear market is the bringer of gains in the years to come. Any plan yet for when and how to reallocate?

I dunno. I actually have no idea for how to time reallocation (i.e., converting from 100% equities to bonds or REITs or whatever) close to retirement (not in 2 comma club). I suppose it will be a gut feeling thing about how the markets are doing and such. Would love to hear GCC’s opinion and experiences on that issue.

One easy way to adjust allocation is to just put new capital into the asset you are trying to grow. So maybe you stop buying stock / start buying bonds when you are 1-2 years away from retirement. With $90k/year you could have about $200k in bonds in short order.

This is exactly how I have been re-balancing my stock ETFs. I had the tentative plan to start buying bonds when I was closer to actually retiring. Being able to buy new shares of your desired instrument makes everything much simpler.

Looking at all the tax info, sorry if I don’t understand this part, in the Template Harvest Long Term Capital Gains, how do you contribute 18K to your solo 401K? I see your person taxes, not the business is that part of income, or am I missing something.

Cheers!

Sorry, that isn’t as clear as it should be.

If you have self-employment income you can contribute to a solo-401k. If you have earned income, you can contribute to an IRA. The cash for those contributions has to come from somewhere.

In the template example, I realized a tax-free capital gain by selling some stock (VTI.) I could just repurchase VTI to complete a capital gain harvest. The end.

But for bonus points I moved some of the cash from the sale into my Roth solo-401k and his/her Roth IRAs. I then bought VTI in the Roth accounts so now all future growth is also tax-free.

Didn’t you say you buy ITOT etf to avoid wash sale? I Didn’t see you mention it in your post. Would you mind explaining if you still do that?

A few times for capital gain harvests I did buy ITOT instead of VTI. I did this because my brokerage (Fidelity) had no-fee trades on iShares. Now that all trades are free, I just buy/sell VTI.

Note there are no wash sales when harvesting capital gains. That only applies for losses. In that case you could switch between a total market index and a SP500 index to avoid the wash.

Hi GCC… did you happen to read the Ray Dalio comment regarding it would be crazy to ‘hold’ government bonds in the current environment where central banks are printing money and interest rates remain at historic lows. I see you own bonds and I also own a fund that does contain some government bonds. I’m new at this, and curious what your thoughts are regarding owning a fund that includes governments bonds… and/or curious on your take on Ray’s comment. Thanks!

I think what he is saying is that negative interest rates mean you pay the federal government for the privilege of holding their bonds, so it is a bad deal. The same could be said for non-US governments with additional risk (lots of flight from EM bonds atm.) That deal is even worse because the printing presses will erode the value of the US dollar.

As alternatives, Mr. Dalio suggests bonds of US corporations with strong balance sheets (perhaps Microsoft or Apple, for example) or equities of strong companies.

That all sounds reasonable, but market timing and chasing performance often do.

“So convenient a thing it is to be a reasonable creature, since it enables one to find or make a reason for every thing one has a mind to do.” – Ben Franklin

99% of fund managers fail to outperform their target index year after year. So… pick an asset allocation and stick with it, including bonds.

Your PC AA Chart shows 4.39% alternative and you say you have 4% in VNQ. My PC AA shows something like 3.4% alternative and I own no REITs or other alternatives. It says that VTI is comprised of about 3.4% REITs so that’s where my alternative % on the chart comes from. Do you change the categorizations so that all of your VTI shows up in the US Equity category on the chart?

…..what I’m trying to say is that the personal capital asset allocation alternatives category shows roughly the same % for you and I, but I don’t hold any REITs. My roughly 3% allocation, according to PC, comes all from my holding of VTI. Since you hold 4% in VNQ I would expect you PC AA alternative section to be about 7%.

I just copied the 4% number from the chart and haven’t done anything to modify the default categorizations.

It’s strange that my chart shows 3.4% alternatives, which it says is all from VTI. My only holdings are VTI and two bond funds (BIV & VTEB). Not a big deal, was just curious regarding the difference. Thanks.

I zoomed into the Real Estate portion of the allocation in PC and it shows my VNQ is really <2% of the portfolio with the rest coming primarily from VTI.

OK. Thanks for providing that.

Good article, BTW. I always enjoy your asset allocation updates.

Our Allocations are almost identical now! Hope it works out.

Just curious how did you get PC to NOT show the dollar values in the Allocation page?

>how did you get PC to NOT show the dollar values in the Allocation page?

Photoshop

Why do you use IEI for bonds instead of BND?

I bought all of that IEI 10+ years ago when I was looking for an intermediate-term non-corporate bond ETF. The Vanguard equivalent is probably VGIT. BND is also a good option.

What are your thoughts are bonds at the moment if you were underweight them?

If I have very little bonds at the moment, shall I just wait till the yields strengthen?

My choices at the moment are between international (US) bonds that all pay 1% yield (known), versus local bonds that are paying 9% but come with potential further currency weakness (unknown).

If you were in a situation with no bond real exposure, would you look to acquire some at this stage, or when would you? Thanks!

I’m moving towards a more international allocation, excluding Europe, mostly focused on Emerging Markets.

I don’t think the US will maintain the dynamism we are used to — thus yielding the long term stock returns in the 7% region net of inflation that we see in our historical past. Or, more generally to talk in relative terms, I don’t think we will continue to outperform the world as we have for most of our history.

As the US moves towards a more European societal structure where exceptionalism is increasingly persecuted to subsidize mediocrity (this seems to be the entropy trajectory of almost all democracies) the effort-reward curves flatten and so does the incentive to careers and competencies at internationally competitive levels. Depressed growth rates inevitably follow. Case in point, unlike most of its ascending history, the US can no longer even match current longer term worldwide growth, currently standing at 4%. Our growth trendline is now already a rather anemic more European-like 2%, likely trending to equalizing with the structural European 1% as our society’s transformation to that model progresses, as most of the population desires. There is simply no future for a society that grows at 1-2% surrounded by a world that is growing at 4%. There is simply no alternative arithmetic. So, those who count on a continued 7% long term trendline from US equities might be sorely disappointed, like Japan lost decades disappointed or even Weimar Republic disappointed. Bad things can and do happen in advanced countries.

Of all people investors are the ones holding one of the most flimsy assets: essentially a societal promissory note of reward for delayed gratification. When the hordes of voters who for decades have voted themselves ever more goodies in the hopes that someone else will finance the inefficient state that will attempt to give them such goodies eventually have to face the final bill, one of the easiest ways to soften the blow will be to renege on the above mentioned societal promise given to investors and savers. Entities appointed by voters, governments and the FED will quickly find the financial mechanics to do just that.

Witness the ever rising percent of GDP that is being consumed by government throughout the developed “free” world, and the concurrent intensifying growth deficit of the developed world compared to world average. The coronavirus will intensify and bring the day of reckoning closer for these advanced democracies as the virus becomes a great opportunity for government percent of GDP to permanently expand. The opportunity will not be missed. Japanese levels of debt and stagnation are quite likely.

I am hence on a long term (inter generational time horizon) reallocation scheme to reallocate into emerging markets. As much as some of these countries are already basketcases, their low CAPE ratios seem to allow for a lot of screw ups. As you wisely said, it decreases my chance of dying a billionaire and also decreases my chances of seeing my assets going down in some sort of new world Weimar Republic. I’m probably in a somewhat more advanced and thus presumably more secure stage of financial independence than you are, hence I look at my finances (allocation etc) through the eyes of my minor children rather than my middle aged eyes.

This is of course all far from certain. Just an educated guess based on some math, some logic, and some visceral expected values.