Go Curry Cracker Going to Battle with the RMD

Over the past few years, taxes have become a bit of a passion obsession.

I had always assumed our tax rate would be lower in retirement, and therefore followed the mainstream advice to max out my 401k each year. This definitely helped to Turbocharge our Savings, and saved a ton in taxes during the accumulation phase

Then in our first years of early retirement, it became clear just how low our taxes could be. Infinitesimally low. Completely non existent. Zero

Now I’m on a mission to Never Pay Taxes Again, not for any politically or financially motivated reason… but just because we can

Beating the RMD

For an early retiree, a 401k/IRA has 3 life stages:

Accumulation, Conversion, and the RMD

The duration of each stage varies by the individual. The accumulation phase lasts at least as long as it takes to save a sufficient portfolio, and possibly longer if one decides to continue working after Financial Independence

On the other end, the IRS mandates Required Minimum Distributions in the year you turn Age 70.5 (which is why I was strategically born in the latter half of the year.)

In between is the tax saving nirvana of the Conversion stage

The Conversion Stage

The goal during the conversion stage is to move as large a sum as possible from a Traditional IRA / 401k to a Roth IRA at the lowest possible tax rate. Just as the Traditional IRA / 401k is the ideal tool for the Accumulation phase, the Roth IRA is the ideal tool for the Conversion stage

Any funds converted will be taxed as ordinary income, but thanks to tax deductions and exemptions, the first $20k +/- is tax free for Married Filing Jointly (MFJ.) Other deductions or exemptions can increase this further, which I’ll touch on later

We use a Traditional IRA / 401k during the working years because tax deductions combined with tax-deferral and compound interest is an incredibly powerful force for wealth creation. Just add time, and these accounts are bound to grow to impressive levels. But if they get “too large” then RMDs will be large, potentially resulting in large tax bills late in life. Uncle Sam wants his take

If we are able to remove a sufficient amount during the years before the RMD, we can minimize total lifetime taxes. We pay as little tax as possible during the accumulation phase, and as little tax as possible in the conversion phase, ultimately resulting in the least amount in the RMD stage

Our Traditional 401k / IRA

During my working days, with the exception of the first few years I always contributed the maximum amount to my 401k. I wasn’t as tax savvy back then, and either wasn’t aware of the option to also contribute to a Traditional IRA or wasn’t eligible. Similarly, we hadn’t contributed to Roth IRAs, with all additional savings going into our Brokerage account

Our tax-deferred accounts are no beacon of investment success. The ~6% CAGR “growth” to date isn’t so impressive when considering inflation and employer matching. Maybe the only positive thing to say is our tax-deferred accounts are a good example that a high savings rate is more important than investment returns for an early retirement

As of Dec 31st, 2014 the value of our tax-deferred accounts was ~$450k

We paid no tax on any of those assets, and my goal is to never do so

How Much to Convert

In 2013 I converted $12,028, and in 2014 I converted $5,744 from our tax-deferred accounts to a Roth. That seems like the wrong direction to be trending in, so some changes are in order

Because my goal is a 0% tax rate, the size of our annual conversion is limited to the Standard Deduction and our 2 Personal Exemptions minus any ordinary income such as Interest, Short Term Capital Gains, or Non-qualified Dividends

Conversion Amount at 0% Tax Rate = Standard Deduction + 2 x Personal Exemptions – Ordinary Income

In 2014, the standard deduction was $12,400 and personal exemptions were $3,950 for a total of $20,300

Over time, our Deductions and Exemptions will change:

- 2015: GCCjr is born. +1 Personal Exemption (+$3,950 in 2014)

- Until college graduation +/-

- Age 65: Standard Deduction increases (+$1,200/person over Age 65)

I’m also taking steps to reduce Ordinary Income

- Reduce interest income: Keep less cash on hand (-$400/year)

- Sell assets that generate Non-qualified Dividends and replace with index funds (in progress, -$3k/year)

- 2017: Private Mortgage balloons out (-$6k/year)

The combination of these factors will allow us to increase our Conversions by ~$13k/year and still pay no tax

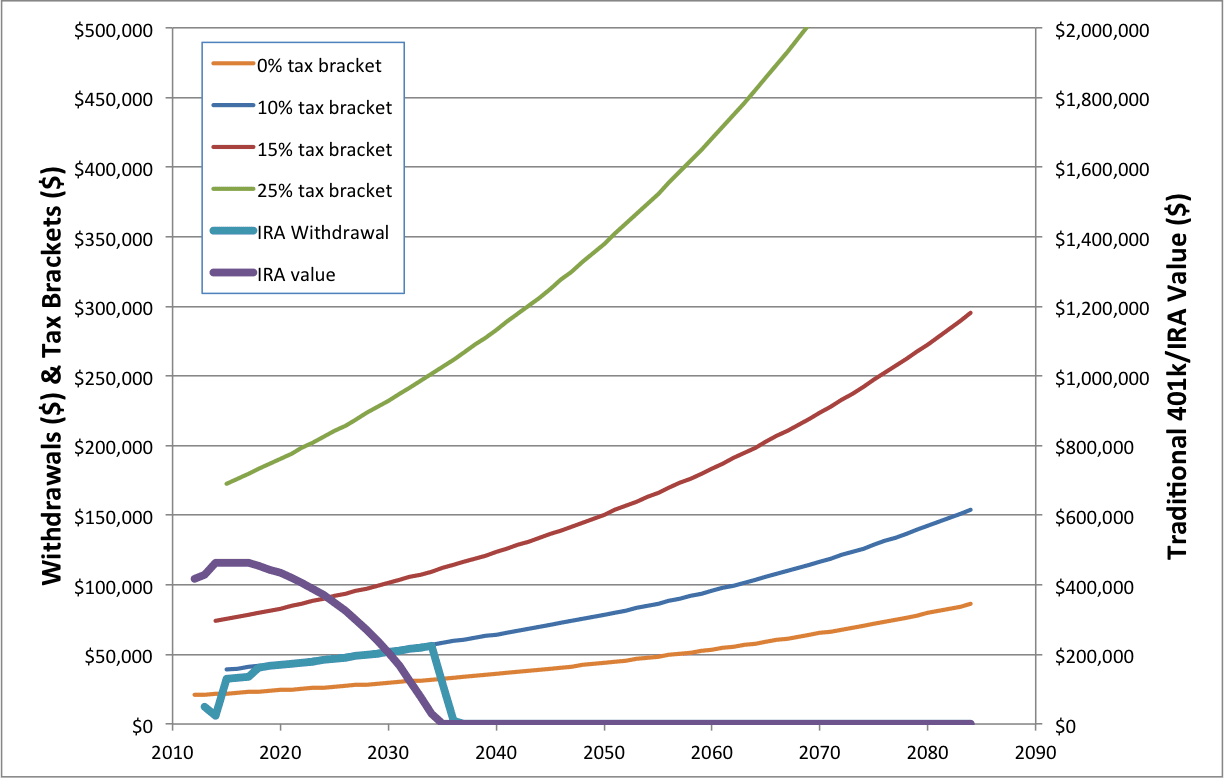

With these changes, and assuming 7% annual growth our efforts to beat the RMD look like this

Convert Maximum at 0% Tax Rate (Assumes 7% annual growth)

Because we are only able to withdraw about 3-4%/year while still paying 0% tax, and the portfolio is growing by 7%, the portfolio continues to grow at an increasing rate. That is, until Age 70.5 when the RMD starts requiring large withdrawals. In this round of GCC vs the RMD, the RMD is the victor

Even in this scenario, however, we never surpass the top edge of the 15% tax bracket (thin red line), highlighting the value of choosing a Traditional 401k/IRA over a Roth during our working years

A Compromise?

Not ready to admit defeat, I looked into other options. Maybe a compromise was in order

What if instead of paying 0% tax, I was willing to at least concede the 10% tax bracket? Using 2014 dollars, this would allow conversion of an additional $18,150 per year, at a cost of $1,815 in tax. Paying tax now at 10% and avoiding the 15% tax bracket later is better, right?

Convert Maximum at 10% Tax Rate (Assumes 7% annual growth)

But this isn’t quite right either. I avoid the 15% tax bracket, but the 401k/IRA is depleted too quickly. We pay tax in the near term at only 10%, but we lose all of those future years of 0% tax opportunity

So the right answer is probably to fill the 10% Tax Bracket a small amount. But how much of this bracket would be ideal? Use 10% of it and increase our total Conversion by $1,815? 20%? 30%? More?

And what about the rate of return? The stock market isn’t going to just go up 7% per year. It might average that over the long term, but it will be chaotic and random, up some years and down others

And since future dollars are worth much less than today’s dollars, it might be better to pay more later rather than a little now

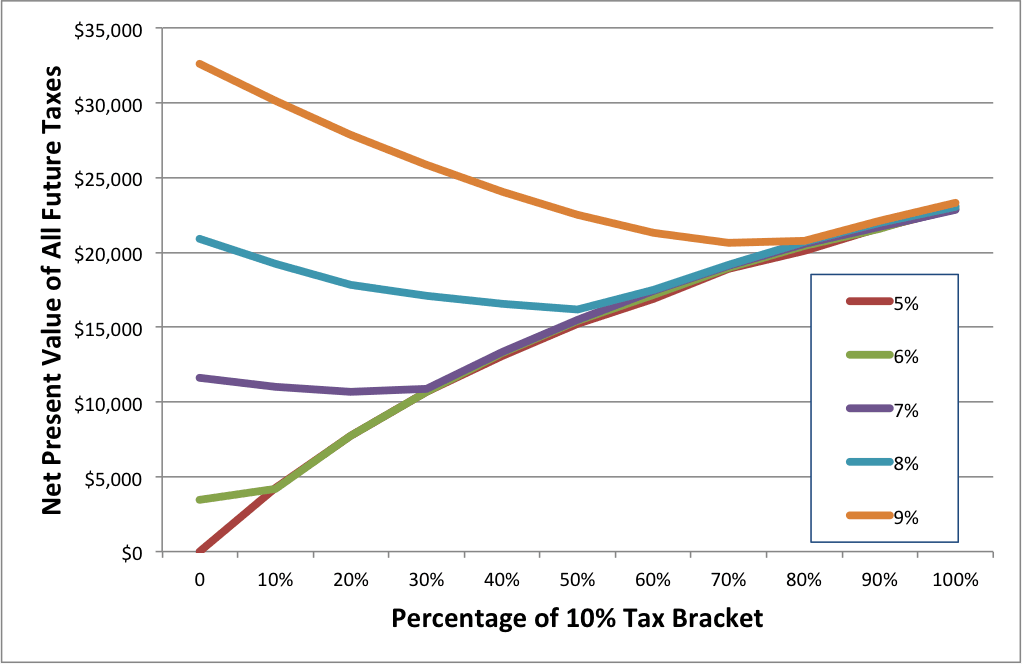

Net Present Value (NPV) of All Future Taxes

Enter the Net Present Value. This chart plots the Value of all future taxes in today’s dollars for investment returns ranging from 5% to 9%.

This is based on using only part of the 10% Tax Bracket, incrementing in steps of 10%. Since the size of the 10% Tax Bracket (in 2014) is $18,150, each 10% step represents increasing the size of our annual conversion by $1,850 which would result in a tax bill of $185

If we use 0% of the 10% tax bracket, the results are the same as in the 1st chart, growing faster than we can withdraw the funds. If we use 100% of the 10% tax bracket, the results are as in the 2nd chart, depleting the 401k too quickly

Net Present Value of Future Taxes (to Age 100)

A couple data points to clarify what this graph represents, using 2014 dollars

The purple line represents an annual growth rate of 7%, the same as in the first 2 charts. The minimum point on that line is at the 30% point.

If growth is a little higher at 8% (the blue line) then it would be better to convert more each year in order to minimize the value of total future taxes paid (minimum value at 50%)

Key Takeaways from the NPV Graph

This is a lot of data to process in a short period of time, so let me highlight a few things that can be pertained from the NPV graph

If return rates are low (5-6% per year) then there is no need to convert more quickly. The minimum NPV is actually at 0%

At the 7% growth rate, the NPV is roughly the same if we choose to use 0% or 30% of the 10% Tax Bracket

The worst case value of all future taxes in 2014 dollars is less than $35k. That means I could basically write a check for $35k now and that would cover our tax load for life (If only the IRS would accept such an offer)

Increasing the size of the annual conversion by 20% of the 10% Tax Bracket (~$3,600) is roughly equivalent to increasing investment returns by 1%

If investment returns are low, we win (pay no tax.)

If investment returns are high, we win (can make large charitable donations late in life)

Increasing the Rate of Conversion

$3,600 is not a lot of change per year to effectively gain a 1% return. Taxes are a heavy load on a portfolio

Can we do anything to try to gain additional tax free conversion space? I can think of 3 things (or 4, if you count business expenses)

- Roth IRA Horse Race

I first learned of this idea from the Mad Fientist. Done correctly, the Roth IRA Horse Race can increase the effective size of each year’s Roth IRA Conversion, in both up and down years. We can do 2 (or more) Roth IRA conversions in one year with different investments, and whichever one grows less can be recharacterized (meaning it never really happened, wink wink) - Harvest Capital Losses

Each year, up to $3k in capital loss can be used to offset ordinary income. Greater losses must be carried over to future years. I could either harvest gains each year, or harvest a large loss and use it over the next few years. I have 2 investments from long ago that pay non-qualified dividends and have an unrealized loss of $30k, so selling would have double benefit. (These losses are first offset against capital gains, so this would need to be balanced against Harvesting Capital Gains) - Harvest Taxes Paid on Foreign Investments

Any assets that invest Internationally will typically have taxes paid in the host countries. We hold the VEU ETF, and in 2014 paid $480 in foreign tax. The IRS will provide a credit against foreign tax paid on your US tax bill, so we could increase the size of our annual Conversion to harvest foreign taxes paid. Because this is a credit, we could effectively convert an additional $4,800 in the 10% tax bracket using this as an offset

Note: Neither Harvesting Capital Losses nor Harvesting Taxes Paid on Foreign Investments can be done in an IRA. These are 2 of the reasons I prefer a Brokerage Account to a Roth IRA

Through the above techniques, if on average I can increase our annual conversion amount by an additional $5k (possible from the Foreign Tax Credit alone) I can improve our tax situation further.

In this case, we are best off NOT paying any taxes now. RMDs could possibly result in us paying some tax at the 10% rate when we are 80, but only if the market only goes up. At this rate, we might even beat the Social Security tax torpedo too

Convert Maximum Using All Tools at Our Disposal (Assumes 7% annual growth)

Conclusions

The quest to Never Pay Taxes Again has inspired me to leave no stone unturned.

I outlined why the Traditional IRA / 401k is the ideal tool for the Accumulation phase, and the Roth IRA is the ideal tool of the Conversion phase

We explored all of our options for increasing deductions, replacing ordinary income with tax-friendly income, and increasing our tax space via credits, harvested losses, and recharacterized investments

The best Net Present Value of all future taxes is to continue to pay no tax now, and take advantage of multiple decades of tax free income and growth

The result is what I hope is the world’s longest Roth IRA Conversion pipeline, resulting in a lifetime of tax minimization and maximized wealth

See All of Your Accounts in One Place

Track your net worth, asset allocation, and portfolio performance with free financial tools from Personal Capital

Are You Ready to Battle the RMD?

We’re in a tougher spot with respect to the RMD’s. Our total tax deferred savings add up to $900k which represents two thirds of our investments. If we assume an 8% average growth rate, that yields the tax deferred investments growing at $72k per year and means even if we convert $40-50k per year today (to stay around 0% taxes), the tax deferred accounts will just continue to grow year after year.

Obviously it’s not such a huge deal, since by the time we’re 70.5 and face a large tax burden, we’ll have plenty of funds to pay the tax bill. Or in an alternate universe of really crappy long term stock returns, our tax deferred portfolio might be nearly depleted by 70.5 and RMDs won’t mean jack.

And I’ll take 35 years of zero (or close to it) taxation in the mean time. No matter the % return outcome over the next several decades, we’re both well positioned to mostly avoid high taxes.

Although we’ll probably end up filling the 10% bracket (or whatever lowish bracket makes sense in a decade or three) to minimize the RMD tax sting.

In your case, you might benefit from the Horse Race idea. Yes, it is impossible to draw down the IRA if the market goes up every year. But since that won’t happen, the down years can provide a great opportunity to make a big move, even if it means recharacterizing a previous Roth so it didn’t really happen

But in any case, it sounds like you still win because your average tax rate will be lower than if you didn’t contribute to tax-deferred accounts while working. And how about that 35 year interest free loan from the IRS?

I’m giving the horse race some serious thought. One could even put 10 or 12 horses into the race to really squeeze out every bit of juice (I have 11 asset classes in my portfolio).

Although I think 2 or 3 horsies will get you 90% of the way. I would probably do total international and total US market since they tend to be lesser correlated. I could throw REITs in as a third option since they often zig when one of the other 2 assets zag (see 2014, for example).

I’m also curious if a pattern of roth IRA conversions and subsequent partial recharacterizations would set me up in the “high audit %” category. Not that I intentionally mis-report anything on the 1040, but the thick envelope from the IRS is never a fun experience.

If GCCjr qualifies for the Child Tax Credit ($1,000 in 2013), you would be able to convert another $10,000 per year tax free from the IRA using the 10% tax bracket. The credit is good until GCCjr is 17 years old.

It gets better if GCCjr has siblings. :)

Wait a second, the IRS will pay us $1000 a year just for having a kid? Now they are just making this too easy

I just did a quick look at the requirements, and I think GCCjr qualifies.

Thanks Bill!

I’ve now run this through taxcaster, and it looks like the Child Tax Credit is in! In 2015 we take tax free Roth conversions to the next level!

When we started the IVF process, we were actually hoping to get twins. That would have been just too much tax goodness to handle though

Kids in early retirement really are tax magic. I just wish we could have kids while we’re SS age so the kids get a paycheck too. You can’t win them all.

Parents helping their kids with college expenses may be able to claim the American Opportunity Credit. The credit is 100% of the first $2,000 of eligible expenses + 25% of the next $2,000 of expenses. The maximum credit is $2,500 (2013). This should cover not only the 10% bracket, but also part of the 15% bracket when making IRA conversions. See IRS Pub 970 for the details.

Conveniently, this credit usually arrives just as the Child Tax Credit is expiring.

Thanks for mentioning those. I used the ed tax credits while I was in university, and hopefully I can do the same with my kids in another 9 years (and convert even more to Roths in those years).

Jeremy,

I am in process of streamlining my own portfolio to reduce taxes and simplify things in general. Thank you for your ideas and for thinking this through and sharing the results.

My pleasure earlyfi. I know an example would have helped when we were planning, so hopefully this is helpful

It was so thoughtful of your parents to consider your RMD battle 71 years before it would occur. Make sure you thank them for that. I just missed the cutoff, June birthday.

Very well done once again sir. I look forward to this battle myself, although I believe I will be closer to ROG’s deferred balance than yours, so I will have a lot of work to do. But with people like you and the madfientist blazing the trail I’m confident I will have the tools to succeed. Thanks for sharing your knowledge.

Wasn’t that nice of them?

I’ve read all the tax documents and theory and pieced it together as best I could, so I thought a real world example would be helpful for others trying to do the same.

Thanks Cheddar Stacker!

Read your article and then saw this article.. will this affect what you are trying to do?

http://www.mainstreet.com/article/is-this-the-end-of-the-roth-ira-obamas-budget-could-hurt-your-retirement-savings?puc=yahooms&cm_ven=YAHOOMS

This only affects the accumulation phase for people with high incomes. If it becomes law.

I did my first backdoor Roth IRA last year but after reading Jeremy’s posts on why a brokerage account is a better idea, I am not too worried if they take this option away.

There are so many celebrity advisers that are chanting “Roth, Roth” that even my wife told me to get into it instead of a pre-tax account. Roth never made sense to me for our situation. Looks like the best use for a Roth IRA is as a conversion ladder AFTER one retires. Paying tax now and hoping/predicting that we will be in a lower tax-bracket later seems a little iffy. Please correct me if I am mistaken.

Sounds like exactly the conversations I’ve been having with my husband these past few years while we were traveling. Lots of tax optimization happening (and happened)- but it’s great to see it all outlined in one place. And while I think it’s great that you and I and others similarly inclined can do all of this, it makes me sad that the tax system is too complex for many people to fully understand. Hopefully articles like this will help some of those people wrap their mind around their options.

Yeah, it is complex.

If anybody from Congress is reading this and would like some help refining the tax code, please reach out to me via the Contact form ;)

I share that hope. And glad you were able to blaze the trail yourself!

Would you really want to be responsible for the mass lay offs that would hit the accounting industry and the tax attorney industry? What about the poor tax lobbyists?

It would be a difficult emotional burden to bear, but I would do my best

I read somewhere that the US Tax Code, if reduced to a simple flat tax, would free up to 8% of GDP to more productive use. It would be a difficult transition period for many accountants and lawyers, but I think the world would be a better place for it

I believe it. There are armies of accountants and tax attorneys on the individual and corp side fighting to minimize taxes. Then on the IRS side there are similar armies. Then there are the second order effects of current tax laws that incentivize suboptimal consumption and capital allocation. You might break 8% if you add up all the second order effects.

It would also but savvy FI tax bloggers like you (and me?) out of business. We would finally have to retire. :)

I totally agree that the tax code is wicked complex. It favors the educated and savvy.

You lost me on the NPV chart, but I’m not going to worry about that yet. On your second chart, can you explain this comment further? ” I avoid the 15% tax bracket, but the 401k/IRA is depleted too quickly. We pay tax in the near term at only 10%, but we lose all of those future years of 0% tax opportunity”

Not sure I’m clear on the downside of depleting it quickly. As you would be rolling the money into a Roth which will still grow tax free, and once you have converted all of it, you can go back to 0% taxes. I would think the short period of paying at the 10% rate, would result in far less tax paid than the years of huge RMDs being taxed at 15%.

Let’s look at the edge case. Assume 10 years from now, on Dec 31st I can make a final withdrawal from my 401k and pay tax on it at 10%. The value of my 401k is now $0.

But if I had just waited 1 day, as Jan 1st is a new tax year I would have been able to make that withdrawal with no tax

Now extend that 1 day wait for 30-35 years. It is like the IRS is giving us a 30 year interest free loan.

I’m thinking I may have ran myself into the NPV portion without realizing it…

I was thinking that if you converted at the maximum rate, you would pay an extra 36K in taxes in the 20 year period. When RMD hits, you are going to end up paying hundreds of thousands in extra taxes.

I think what i was missing was the NPV, where the money saved now (based on the investment return) will be much more valuable than the taxes paid even with RMDs?

Yes, exactly. That’s what the NPV tells us

Very interesting GCC. Looking at your calculations, the only flaw I see is the ‘What if?’ of taxation rates changing. That will likely occur, but can it be predicted well enough to plan for it? Probably not.

At this point, I’m most interested in how you manage to get funds out of the 401k/IRA to live off of. It looks like you are doing a direct rollover into the Roth. But, do you live off any of those 401k funds? I’ve heard about SEP distributions, but never heard of anyone actually doing it.

Hi Kuma

The only thing I’m certain of is that tax law will be different in the future than it is today. I have no idea what will really happen (although I can guess, just like I can pick lottery numbers)

At present, we are only spending from our taxable accounts.

https://gocurrycracker.com/cash-flow-management-early-retirement/

I have not met anybody that is doing SEPPs. They are somewhat inflexible, and therefore not ideal for somebody retiring much younger than Age 55 or so.

In the case of the Roth IRA Conversions we are doing in this post, contributions to those can be spent 5 years after the first conversion. 5 years of spending in a taxable account could bridge the gap

Cheers

Jeremy

I’m now seventeen years into early retirement and I did do a SEPP at 54 after learning you can separate your IRA and do it with only one account and you could also ladder IRA’s with different starting dates. The rules are five years of distribution or till you are 59 1/2 whichever is greater. I still smile at having only diverted 58 cents of take home pay into my 401K when I was working that immediately became $2.00 that then also compounded, and then sweetly after ER paying zero taxes when I take it out!

At the time Roth Conversions were not such a hot topic, but I’m doing them now to continue to lower my RMD at seventy. The five year time clock till you can touch the Roth starts from Jan 1st of the year you contribute, so even if you do the conversion say on Dec 31st, 2015, the five years would be satisfied on Jan 2, 2020.

The current volatility of the market gives you opportunity to convert when one of your holdings in your tax deferred IRA has gone down throughout the year and I have found in my experience converting then has given me not only greater profits tax free but what I have paid in taxes is now in the tax free Roth so I don’t get too worried if I pay some in the 10% tax bracket. Conversions can be done more then once during the year to accumulate the total you want to have at the end of the year and once again the five year time clock starts on Jan 1st for all of the conversions.

I know everyone is saying to hold till age 70 to collect SS but I think everyone needs to run their numbers because it is not the best scenario for everyone .Because I live frugally and the SS check is more then my living expenses I stopped needing to use any of my portfolios or their dividends and interest. I project at least $400,000 more in eight years in my portfolios and after two years, I’m at $100,000 more so far, I am on target. This occurs for two reasons:You eliminate the drain on your assets, and only half of your Social Security is figured in income in the Social Security worksheet. If you stay below SS being taxed at the 50% tax limits,($32,000 single and $44,000 married) only 25% of the Social Security income shows in adjusted gross income. So the rest-75% of SS in addition to your standard deduction and personal exemptions has given a huge increase in your tax free income! And all my taxes are taken from the SS check so they are no longer taking anything from my stash just I’m getting a slightly smaller SS check. Tax Freedom! So already the $100,000 I’m ahead generates more income then the increase that most people are waiting for till age 70 and its possible by normal retirement age you triple what SS projects the increase in waiting will give you without touching the principal in your portfolio but from the interest and dividends. IMHO, If your an early retiree, and been smart to convert your traditional IRA to a Roth before age 62, not only RMD’s are not a major factor you are more likely in the driver seat to take SS early and benefit more then holding till 70.

Another thought provoking post. I honestly hadn’t thought that I would be converting from IRA to Roth IRA for that many years, but it sounds like I will want to take a look at it in 7 years when I reach financial independence. Hopefully the Roth conversion is still a viable option at that point! I do have a decent percentage of funds in a Roth already, so that may help me be flexible around how much I need to convert each year.

I think the Roth conversion will still be an option. It’s a potential short term revenue source for the IRS, and those don’t get shut down often

I hope to have a pipeline 34 years long. The longer the better

7 years will go by in a flash. Your blog posts about your plan look solid, it might even happen sooner than that

This gave me a chance to compare to i-orp.com. Not knowing exactly your situation, I put your ages in as 38, 450k in tax deferred, 100k in Roth, 10k each in SS at 67, and retirement at 38. It basically says that your spending is so low that you don’t need to worry, and when RMD’s hit, you will have spent down most of your tax-deferred (having lost ground to inflation). Obviously converting tax-deferred to Roth when you have tax-free space is a safe bet, but I’d be hesitant to ever venture in to the 10% bracket to speed up conversions, unless your tax-deferred has grown too far too fast – but then how do you know it won’t fall right after you’ve paid tax (ouch)? My situation is a bit different since there is a lot to be gained by optimizing conversions to smooth my effective taxes and limit the RMD damage, so I would be interested to hear your feedback on i-orp!

Model Error

Retirement ages must be 37 or greater. Earlier ages may make infeasible models..

I bumped up Winnie’s age, but the output was confusing to me. I’ll have to look at it another time. For some reason it is assuming we spend 2x what we do

Look at the Mad Fientist’s horse race concept for options to limit damage from a falling market after a conversion

That’s funny, 38 works but 37 is too young? It is not the most user friendly, but there is plenty of documentation (and good tax advice, like SS file and suspend) buried in there. One way to adjust the spending is to adjust the estate at the end of the model. Otherwise the model is trying to maximize total spending and minimize total tax down to the final estate value, and ignores Monte Carlo and sequence of returns (e.g. the 4% SWR).

I am familiar with re-characterizing / unwinding a conversion during the tax year, I was thinking more along the lines of paying 10% tax in 2005, -6, -7 and then having a 2008/early 2009 when large taxable RMD’s suddenly look like the least of your problems…

Thanks for looking into this, and discussing ways to go about tax planning in retirement. Good stuff!

Thanks for another brilliant distillation of complex topics into a single post with pithy words and pretty pictures! It’s official: GCC is now the internet’s #1 destination for early retirement tax nerds.

One assumption implicit in your analysis is that future tax treatment won’t change. Why in this context are you willing to give up the 0% bird in the hand today for the hope of lower taxes tomorrow? Seems a bit at odds with your general approach on Roth vs. Taxable, etc.

Step 1: Build an audience of tax nerds.

Step 2: Take over the world! Muahahahahaha

I’m interpreting your 0% bird in the hand comment in 2 different ways. Can you expand on your comment?

I meant that voluntarily opting to pay tax at the 10% rate upfront (when you have the option of paying 0%) seems a bit analogous to doing Roth instead of Traditional during the accumulation phase (in my comment, I meant to say “Roth vs Traditional,” not “Roth vs Taxable”), which you (sensibly) recommend against. In both cases, you are paying taxes today in order to (hopefully) save on taxes tomorrow. But I suppose the distinction is that as long as you assume no changes in tax law, you know you will come out ahead in one context and behind in the other context. So to decide *not* to pay some upfront taxes in the RMD race is actually gambling that tax laws *will* change (in an adverse manner). So now maybe I’ve answered my own question.

We contributed $13000 to our Roth as soon as possible. ye, we are old, catch-up is included, best part of being old and still working though. If my husband retires next year, converting will begin, my brain have to work over time, so we can minimize our added tax incursion from converting. I always enjoy your intelligent thought on any subject in this blog, especially on money.

Thank you Young

Going through the conversion the first time takes a lot of thinking, but the second time is really easy.

I barely got through the calculations my first year… last year. Now with all the tax changes etc. I’m finding it difficult my second year also. I’m in the same situation as Justin Root of Good with a large 401K and Traditional IRA relative to my taxable assets and last year I just filled up the 15% tax bracket with conversions because I didn’t know any better. I’d like to calculate the optimal amount of the 12% bracket to fill up this year. I’m a dunce as far as creating Excel spreadsheets. Have you ever made yours available for download?

I’m 57 and the wife is 40. We have two children ages 3 and 7. Currently retired and living in Thailand. Were living off cash I saved. No other income. At age 60 I get a $1800\ month fixed pension. At 62 I’ll be claiming my SS of $1800/mo and the children will be claiming their approximately $1200/mo.

Suggestions are welcomed.

We lived in Taipei in a new neighborhood on Xinfeng street near the park for two years and loved it so i understand why your so happy living there.

Hey Mike. I don’t really have a spreadsheet, I just crunch the numbers each time.

Filling up the 15% tax bracket (2017) or 12 % tax bracket (2018) is the same process. Then you can use the $2,000 CTC/kid as an offset to any tax burden.

I walk through the process in our 2014 tax return.

Awesome post! Now that we have a saving strategy and general plan set in place, I’ve been looking more and more about how to minimize taxes and also access our 401ks early. I am 90% sure we are overfunding our 401ks, but with our current salaries we can’t open a Roth, so I’m hoping between Roth conversions starting after we RE and maybe SEPP form the 401ks, we will have a plan to access that money. I’m still trying to understand these strategies, and your posts really help.

Great, I’m glad they help Mrs SSC!

Unless you are expecting a large pension and a large amount of Social Security, it is hard to overfund the 401k. Taking the tax savings now is a winning strategy

(In reply to brooklynguy)

That makes more sense. I agree with your conclusions

I updated the post to state more clearly that I think not paying tax now is the optimum solution for us

It is possible that the Roth IRA Conversion could be eliminated, or that the 10% marginal rate could be increased. I think the odds are in our favor though (More likely would be increasing taxes on dividends and capital gains, and increasing the marginal rates at the high end)

Now that I’m aware of the Child Tax Credit, combining it with the Foreign Tax Credit can allow us to convert up to an additional $15k/year at 0% over the next 17 years. We may get everything out before we even hit the RMD

Updated chart with child tax credit:

I’m curious how the Child Tax Credit is relevant to your calculations, considering that the unused portion of the credit would be refundable through the “Additional Child Tax Credit” provision.

In other words, one can increase IRA conversions to use up the “Child Tax Credit”, at the cost of missing out on the 1k refund through the “Additional Child Tax Credit” provision.

That is a fair way to look at it. The answer depends on the marginal rate of the Roth conversion vs expected future tax rates.

In my calculations above I’m experimenting with paying or not paying tax at the 10% marginal rate, and just looking at the border conditions. The choice essentially comes down to would you rather have a gift of $1k in cash from the IRS today or move $10,000 from Traditional to Roth.

If we choose to take the $1k in cash today (avoiding 10% tax) we will probably pay some tax at 15-25% in the future with the RMD. If we use all of the CTC to offset Roth conversion tax today, our Traditional accounts will be zero long before the RMD. The ideal choice is probably somewhere in the middle, at least in terms of minimizing taxes over a lifetime.

Another stimulating, terrific post! I was well aware of the recharacterization concept but had never thought of it in terms of a horse race strategy. Clever! Will need to give that more thought. I think it assumes one is investing in noncorrelated asset classes, else the difference in performance of the 2 horses won’t be enough to justify the effort. But if you can predict the winning horse, then you’d do better to keep on in the IRA stable than set them both on the track. i.e., if you insist on a stock/bond portfolio, then splitting them into 2 Roths makes sense and later keep the winner. But if you think bonds are a bad choice right now and prefer to put all in stocks, then it seems doubtful the 2 accounts will differ enough to justify doing this.

As for the RMD, I think this highlights the need to carefully think through and model the RMD effect. I sent you an email privately that includes a spreadsheet tool that can be used for this purpose as well as the purpose for which I created it (to contribute to the great 401k vs. Roth debate). For some people, it would make sense to do the conversions at 10% or even 15%, while for others, 0% is achievable. Knowing this well in advance is the key to success, so that you can have enough time to get the conversions done.

One thought that occurs to me is suppose you had a little side business that made $10k one year and lost $10k the next, and repeated in alternating years. Probably this is not kosher–I know very little about business and tax law–but I’m thinking maybe some kind of advanced sales or accounting/inventory tactic could be used. (If corporations can manage their earnings to always just beat the street by a penny…). In Year1 you book a $10k loss and take 2 years worth of living expenses out of your accounts in the form of capital gains or IRA distributions or whatever. In Year2 you book the gain but don’t take any distributions for expenses. If you have GCCjr and live >6 months in the USA, would you be eligible for EITC for that year? And, if you look at the two years combined, does that produce more headroom for conversions? I haven’t worked this out or explored the legality, but maybe someone else here can comment.

The Horse Race concept is pretty cool, no doubt.

I’m not sure about the business tax side of things, but we will never be eligible for the EITC. We have too much investment income to qualify

I’ve seen cases of people timing tax-deductible expenses with income. If you receive a big bonus one year, for example, you could pay next year’s property taxes this year for the increased deduction

I have your doc and xls and will read through it this weekend. Thanks!

You’ve been knocking it out of the park lately GCC! This is the high quality stuff I love. Usually only the Mad FIentist has stuff this analytical and clever. That NPV chart makes me a little hot.

Haha, thanks Joe! lol

Post quantity must be inversely proportional to distance traveled. Now that MF is on the road and we are nesting…

Looks like I also won the birth lottery. Now it takes a lot of time to digest your post and the related comments. This is not a compliant.

Have a few questions about the NPV graph:

(1). How many years of tax payments you are discounting?

(2). Did you include the additional $185 tax per $1850 in the tax payments before you discount them?

Due to the nature of our jobs, my hubby and I are able to shield a lot in tax-deferred retirement accounts every year, which means we will have way more money in these accounts than in taxable accounts. How to efficiently maximize Roth conversion would be an important topic for us.

Thanks for sharing the Roth IRA Horse Race post. As someone mentioned in the comment section of that post, even if you are not doing a horse race and only doing a single conversion, it makes sense to convert from Traditional IRA to Roth on Jan 1 each year. If the market goes up, great, you get more tax-free growth. If the market goes down, you can recategorize the conversion and make another conversion at the lower value. Brilliant! You guys make the world better!

GCCjr won’t be so lucky with the birth lottery, since he is due in April. But with 70 years before the RMD, he should still do well. We might hire him as a model for the blog so he has some earned income to contribute to a Roth each year too at his 0% marginal tax rate

I included all taxes through Age 100 (although exact age didn’t make much difference), and included all taxes paid (so yes, the $185 on each $1850 and also any taxes on the RMDs later in the 15% tax bracket or higher)

I like the Horse Race idea too, and am going to try to use it this year

Do you mean we can move $20,300 from our 401k to Roth IRA if we had no other income in 2014? Actually, the 401k account belongs to my husband. Does he only allow to move it to his own Roth IRA or he could move some amount to my Roth IRA too? Thank you. Amy

Hi Amy

You would have had to do it before the end of 2014. But yes, if your husband was not working, rolled the 401k over to a Traditional IRA, he could have then moved as much money as he wanted to a Roth in his name. There is no limit, although it would all be taxed. Married filing jointly with standard deduction and no other income could move $20,300 and pay no tax, any more than that and there would be tax due. Depending on the State, there may also be State Tax due

By the way, should we do the move during 2014 or we could still do it in 2015 before filing 2014 tax return?

It would need to be done in 2014

Thank you for your reply but how can I know exactly how much I can move before end of each year because some of the interests or dividends only distribute in the end of Dec. Or you just move your funds in the very end of each year? Also, should I inform Fedility that I am moving from 401K to Roth if I have both accounts with them? How does it work with Fedility? Pls advise. Thank you.

You have to estimate:

https://gocurrycracker.com/7-minute-taxes/

Login to Fidelity, select your Traditional IRA, and click the link for “Convert this IRA to a Roth IRA”

Then just specify how much you want to convert

You can call Fidelity and have them help you through the process

You would have to check with Fidelity on specifics:

https://www.fidelity.com/retirement-planning/learn-about-iras/convert-to-roth

Please clarify……

We hold the VEU ETF, and in 2014 paid $480 in foreign tax. The IRS will provide a credit against foreign tax paid on your US tax bill, so we could increase the size of our annual Conversion to harvest foreign taxes paid. Because this is a credit, we could effectively convert an additional $4,800 in the 10% tax bracket using this as an offset

When you say convert $4,800, convert in what manner? You received $480 in tax credit, was that on $4,800? Do you mean that you will convert or harvest gains? if so, would’nt you be minimizing your foreign tax credit for the next year?

I understand the rest of the post, I am wanting to know more about this topic.

Thanks.

Convert is the word the IRS uses to mean moving money from a Traditional IRA to a Roth IRA.

The $480 tax paid to foreign governments is on hundreds of thousands of dollars invested in VEU

The two are unrelated

Since we get a credit for foreign taxes paid, I want to create tax liability of an equal amount. I can do that in many ways, but in this example I can do it by moving $4800 from a Traditional IRA to a Roth.

Does that make sense?

Yes, this makes sense. I understand converting traditional to Roth. I was just reading it wrong. Thanks for the explanation. I enjoy your blog.

I’m thinking I can pull this strategy off in small quantities over the years:

$39216/year in tax free income (VA check)

$20268/year in taxable pension income

$42000/year in self-employment income (wife)

$2000/year in dividends/interest

———

~$104K/year in early/semi-retirement income

$18000—goes to solo 401k

$7806—goes in as profit sharing employer contribution

SET is $5934

$5500 Traditional IRA for spouse and $5500 Traditional spousal IRA for me (Or would Roth’s make more sense here due to all the exemptions below?)

I’m thinking I should be left with an average AGI of about $27K/year

Two kids (6 and 3), so eligible for:

Child Tax Credit–$2000

Savers Credit (I think)–$4000

EITC–$5460.

The first two are non-refundable so i don’t think they can offset the SET, but I believe the EITC can and wipe out the SET almost completely.

I know I have to be mindful of how much I transfer from the traditional to the Roth, and I also need to watch my AGI/MAGI so I don’t unnecessarily bump myself out of a credit I would be entitled to otherwise by taking a distribution which is too large. Anything else I should consider?

Saver’s Credit for MFJ is 50% of up to $4000 in contributions, or $2000. I think you were confusing the contributions with the credit amount. But your problem is bigger than that. The issue I ran into with savers tax credit was that it is a nonrefundable tax credit. But if you are MFJ w/$27k MAGI then your taxable income is less than the max amt of refund. i.e., you qualify for $2000 Savers Credit, but your tax liability is less than that, so you don’t get the full amount. In fact, you could earn the maximum income to qualify for the credit yet still not be able to actually pocket the maximum credit! That’s just the way the math works. When I first encountered this I thought I must be doing something wrong, so I called IRS helpline and asked about this and they said the published maximums are misleading because it is pretty much impossible to actually get the maximum refund, given the current tax structure. Furthermore, unlike me, you are planning to claim the EITC. That is a refundable credit. You won’t have any tax liability left, and thus no saver’s credit.

You wouldn’t be eligible for EITC based on investment income. I also believe EITC is based on your earned income not on AGI so you wouldn’t be eligible on that basis either.

You’re right–I put the contribution amount instead of the credit. from what I can tell, the refundable credits are applied first and then the non-refundable credits which should eliminate all tax liability. I imagine I’ll only be left with the SET and the EITC could cancel most of that out and possibly result in a refund. do you think Roth’s or tIRAs make more sense in this case? I’m guessing Roth’s since the tax liability is already so low and would be managed by the Saver’s/child tax credits.

Late reading this post. Curious to know how GCC will handle health insurance costs. Will Roth pipeline start before you are eligible for Medicare? If so, APTC subsidies would get reduced or vanish as your MAGI increases via Roth conversions. This effectively adds costs during pre-Medicare years that seriously compromise the savings from doing the Roth conversion. Have you posted anything about this aspect? Or perhaps your insurance costs are not being handled via ACA marketplace?

Hi Will

We aren’t in the US, so no ACA for us. I saw roughly a $0.13 reduction in subsidy for every $1 in income, a 13% effective tax

https://gocurrycracker.com/how-obamacare-saved-us-from-extortion/

Mostly likely we’ll be outside the US 30 years from now, so no Medicare for us either

Cheers

Jeremy

I’m reading this late but how are you avoiding early withdrawal penalties on your 401k? Is this a side benefit of Moving to an IRA?n

Yeah, moving funds from a Traditional to a Roth IRA isn’t considered a withdrawal. No early withdrawal -> no early withdrawal penalty.

The IRS calls this a Roth Conversion (see links and comments in this IRS FAQ.) Any un-taxed dollars in the Traditional IRA involved in the conversion are taxed as earned income in the process (0% in our case.) I assume the IRS encourages it because they prefer tax revenue today vs in the future.

It is a nice way to fill up the 0% tax bracket (standard deduction + personal exemptions) if other sources of earned income don’t.

I need to re-read this article to entirely understand it but I get the basic gist of it. Perfect timing too as i was just starting to do some research on this topic. One “off-the-wall” solution which may slay the RMD dragon might be Puerto Rico. I am having a little bit of trouble determining for sure what the tax tax rate would be there on (in my case) a beneficiary IRA. But in the right circumstances, it may be tax free. Note, you do have to fully commit to living in a tropical paradise with sub US cost of living for at least 183 days of the year.

I don’t think PR is a solution?

The IRA is still in the US, and the IRS will tax withdrawals independent of where we are in the world.

Again, wonderful information, thank you for laying this all out. This is all still new for us to think through, and would appreciate your confirming our understanding (Married Filing Jointly):

401k to Roth Conversion = Standard Deduction ($12600) + 2 Personal Exemptions ($8000) – Interest Income ($0) – ST Capital Gains ($0) – Non-Q Dividends ($0) = $20,600 available for Roth Conversion from prior 401k … is that correct?

If that’s the case, does that mean we could still fill up our 15% bracket using Qualified Dividends and/or Long Term Capital Gains and pay 0% tax on this portion of income ($95,500)? And then would we would owe the equivalent 15% tax rate on the above Roth Conversion amount? I don’t necessarily want to pull that much income, but just wanted to check my understanding of the impact.

Thank you … I wasn’t clear how to model the impact of Roth Conversions using the Tax-Caster calculator, so thought I’d ask those with experience.

Your understanding on the size of Roth IRA Conversion is correct. (Yeah!)

Yes, you can still fill up your 15% bracket using QDs and LTCGs and pay 0% tax. AND… you still pay zero tax on the Roth conversion. See our 2013 and 2014 tax returns to see this in action.

In TaxCaster, you can model the Roth Conversion using the Other Income, IRA/Pension Distributions field

—

Caveat: If you are physically in the United States, all types of income impact the size of healthcare subsidies you receive. So there is a balance between maximizing Roth conversion and maximizing ACA subsidies.

Hello Jeremy, The link above on striking the balance between maximizing Roth conversion and maximizing ACA subsidies no longer works. Is the post still up? Thanks! Weili

fixed it, thanks for letting me know

I am not sure if this is the correct post to ask for clarification, but are you saying you saved your money during accumulation phase ONLY in Traditional 401k/IRA and brokerage accounts while foregoing Roth? I thought that if I am able to max 401k and Roth while still contributing to brokerage account that would be the recommended approach. Thanks for clarifying.

Correct, I never contributed to a Roth account while working.

The best approach is the one that involves the least amount of lifetime taxes paid. If you pay 15-25% tax on that Roth contribution today and 0-10% in the future, then a deductible Traditional IRA is a better choice.

and if IRA contributions are not deductible?

Then do brokerage or backdoor Roth as you prefer. For someone like me, targeting a retirement 20+ years before age 59.5, the brokerage account is fully accessible, including earnings, whereas the Roth is not. If your retirement plan has you calling it quits much closer to age 59.5, then having some Roth in the portfolio is fine.

I think I reviewed this in the post Roth Hypocrisy.

If I want to max out the current annual 401(k) limit of $18K, and my employer matches my contributions, does that mean I should contribute $9K? Or does the $18K limit only apply to the employee’s contribution, and NOT the employer’s? I’m inclined to think it’s the latter but thought I would ask.

Interesting web page. It’s got me thinking about how to handle this. Thank you.

I will be reaching the RMD stage of life pretty soon, and I’m wondering if I can do a conversion to a Roth and treat that as the RMD. If I have to withdraw $20K for my RMD, why not just convert it to a Roth if I don’t need it to live on? That way I don’t get hit with a tax on both the RMD and the conversion.

I don’t know if IRS allows this or not. Any thoughts would be appreciated.

IRS rules prohibit putting your RMD into another tax-advantaged retirement account. So no, you can’t do a Roth conversion as your RMD.

Tax minimization is the name of the game at this point.You may choose to do Roth conversions above and beyond the RMD to the top of the 15% tax bracket if it means less likelihood of paying 25% tax rates as RMDs increase going forward.

I would willingly pay to have someone figure this out for me. This is a huge business opportunity for someone to charge a flat fee to figure out for those of us who get lost in the weeds to determine how much we can rollover before hitting the next tax bracket. I have several friends who would pay for this service also.

Any competent CPA can do this. Would it be helpful if I had a list of resources to refer to?

(I can look at building one.)

Thank you so much for providing the wonderful information. The charts you provided are really amazing. As we approach our retirement, I hope to be able to draw similar charts based on our situation. May I ask how you produced the line charts? What software did you use – MS Excel or others? Many Thanks!

Excel.

Thanks GCC! I’m also wondering how your tax bracket lines (0%, 10%, 15% brackets etc.) were produced. Are those based on some data tables or certain formulas?

The brackets come directly from the IRS tax tables

So what we can find from the IRS tax tables are the brackets in the past years. I was wondering how you predicted the tax brackets in the future years to draw the lines…for example, the 0% tax bracket is up to $50000 around year 2055. It seems that the scale at which the curves going up would need to be relatively accurate for the future years since it plays an important role in the decision making.

I projected based on assumptions re: inflation. But this isn’t so important, I could have just kept the lines flat as inflation adjusted.

More important (by far) is your assumption on future (real) growth rates, and potentially major changes to tax law.

This is why I used a range of growth values in the NPV of future taxes chart.

Okay got it. Thanks so much for the explanation!!

Hello GCC!

Is there a post of your describing what would happen if you were to withdraw funds through SEPP vs. Roth Conversion vs. early withdrawal penalty? Mad fientist has a breakdown considering early retirement and the logistical hurdles that come up for understanding what is the best way to save on taxes over long-term (and short-term too), and it seems like the early withdrawal penalty is not a bad way to go considering how it simplifies things…

What are your thoughts on the matter of paying the penalty vs Roth conversion, besides the fact that giving money to the government in the form of a penalty seems to give one the heebie jeebies? Thanks!

https://www.madfientist.com/how-to-access-retirement-funds-early/

-Sean

A penalty is mathematically the same as increasing the marginal tax rate on a withdrawal by 10%. I’d rather pay 0% myself, so would rank penalized withdrawals last.

But if you have no liquid funds, you can still come out ahead paying the penalty, say if you pay 10% tax 10% penalty but saved 21%+ on contribution.

Agreed, thanks for the quick reply!

In performing my early retirement calculations, I don’t plan on having kids, and the single payer tax brackets are much lower of course than the married filing jointly.

I am well off and am on track to early retire in 15 years with 100k income per year (long term capital gains mostly, Roth conversions). In your opinion, if I’m not trying to pay 0% tax and am simply trying to optimize the taxes I pay, I would assume maxing out my employer retirement plan and throwing every dollar at my taxable brokerage account is the way to go? With 100k income per year, ACA subsidies are still a large expense but a little easier to digest thankfully.

With long term capital gains, as long as I’m under $433k (Lol) I pay 15% only on gains and qualified dividends. That’s what I’m inevitably shooting for.

Contribute max to 401k, HSA if available, optionally also to IRA (backdoor Roth if necessary), and then save a ton in after-tax since that is only remaining option.

Unsubsidized ACA prices in your 60s can be 3x the prices in your 30s, fyi.

sorry if I missed this but did you have to pay a penalty for accessing the retirement accounts?

No. Roth conversions aren’t a withdrawal in that sense.