It is that time of year again. Time to pay the tax man. At least for most people.

It is that time of year again. Time to pay the tax man. At least for most people.

For the past two years we have shared our tax returns (2013, 2014), showing investment income of nearly $100,000 and a Federal Income Tax bill of $0.

This year is a little different because we violated Principle #1, Choose Leisure Over Labor, and this little blog accidentally earned a few bucks. Apparently I’m a business owner now. While that opens up all kinds of interesting tax opportunities, which I certainly capitalized on, having earned income changes the game a bit.

So earlier this year I shared how International nomads like us can have earned income over $100,000 while still paying zero Federal Income Tax. Which is pretty cool.

But you are probably thinking, “Yeah, yeah, they earned $100k and paid zero income tax. Again…” *yawn*

I agree, that is sooo 2013. Which is why this year, I had the IRS pay us.

Using actual tax documents, let’s go through line by line and figure out how.

Income

Income in 2015 came from multiple sources. Multiple streams of income!

We received interest from a savings account, a seller financed mortgage, and tax-free municipal bonds.

Long term capital gains were realized while rebalancing the portfolio to our target asset allocation.

Dividend income was up 9% over 2014 and 30% over 2013, with zero effort on our part. Thank you business leaders of the world!

And still a complete shock to me, this little blog earned nearly $100/day. Thank you!

Filling out the 1040 Form:

Interest (Line 8a): $5,747

Tax-free Municipal Bond Interest (Line 8b): $1,335

Qualified Dividends (Line 9b): $33,967

Non-qualified Dividends (Included on Line 9a): $2,793

Blog profit (Line 12): $36,419

Capital gain (Line 13): $23,737

Total income (Line 22): $102,663

2015 Form 1040 Income

Adjustments, Deductions, & Credits

Before calculating tax we subtract adjustments and deductions.

Some of these are fixed entities, such as the Standard Deduction (Line 40, $12,600) & Personal Exemptions (Line 42, 3*$4,000.)

Others are based directly on income or actual expenses. For the self-employed (Hey, that’s me!) health insurance premiums are deductible (Line 29.) Also a deduction, the “employer” portion of FICA taxes (the Self-Employment tax, Line 27) is a fixed percentage of blog income.

Still other deductions are optional, such as contributions to a Traditional IRA (Line 32) or to a qualified plan for the self-employed like the Individual 401k (Line 28.) We will tune these contributions to optimize our tax bill.

2015 Form 1040 Adjustments, Deductions, & Credits

Once we calculate our total tax, we apply tax credits.

Since we hold most of our International stock index funds in our brokerage account, we can claim the Foreign Tax Credit (Line 48) for any tax withheld by foreign governments. In 2015, this was $469.

In addition, because we are the parents of a happy little tax deduction we qualify for the Child Tax Credit. This is a whopping $1,000! (Line 52.) We also paid a small amount for child care, so we get another credit of $39 (Line 49.)

All credits total $1,508; any tax due will be reduced by up to $1,508.

A detail worth understanding on Line 56, which reports the total tax bill after credits: “If Line 55 (total credits) is more than Line 47 (total tax), enter -0-.” In other words, if you can’t use all of your credits, you lose them.

IRA & 401k Contributions

With earned income we are each able to contribute up to $5,500 to an IRA.

I can also contribute up to $18,000 to my Individual 401k, and my business can make a profit sharing contribution of up to $6,769 (20% of net business income minus half of self-employment tax.)

IRA contributions and employee Individual 401k contributions can be either Traditional (pre-tax) or Roth (post-tax), but business profit sharing contributions are always Traditional (pre-tax.) If we choose to make Traditional contributions of $6,769 or less, these should go to the Individual 401k, so 100% of our IRA and employee 401k can be Roth.

With up to $35,767 in potential contributions, we have a classic Traditional vs Roth trade off.

Traditional vs Roth (vs Brokerage)

The standard Traditional vs Roth argument goes as follow:

– If today’s marginal rate is higher, than a Traditional IRA is the better choice.

– If the future marginal rate is higher, than a Roth IRA comes out ahead.

With no Traditional contributions, Taxable Income (Line 43) is $74,989. This is $89 beyond the upper edge of the 15% marginal tax rate ($74,900.) The effective tax rate on this $89 is 25%.

Will our future tax rates be less than 25%? Considering we’ve paid 0% the past two years, I think it is fair to say yes. We should definitely contribute at least $89 to Traditional accounts, after which all of our Qualified Dividends and Long Term Capital Gains ($57,704 total) are completely tax free.

All of our regular income is now firmly in the 10% tax bracket, and an additional $2,146 +/- Traditional contribution would completely eliminate our Federal Income Tax obligation, as determined by experimentation in Turbo Tax.

But will our future tax rate be less than 10%? This is a harder call. I forecast that we could easily convert all of our Traditional accounts to Roth with zero tax over the next 30 years, so the odds are good that our future marginal rates are lower. But then again, if we spend time in the US the ACA makes even small Roth conversions subject to 25% marginal rates.

Since $2,146 +/- is a negligible percentage of our existing Traditional accounts, and I like paying no tax, I decide to make this contribution. Hello zero dollar tax bill!

Additional Child Tax Credit

But wait, we can do better.

The Additional Child Tax Credit (Line 67) is a refundable credit. If the Child Tax Credit (Line 52) is greater than the amount of total income tax owed, then some of the credit becomes a refund.

We could make Traditional retirement contributions up to an additional $10,000 and receive the maximum ACTC of $1,000 as a refund. Or we can make an additional $10 smart ass contribution, and have the IRS pay us $1. Which is what I would do.

But thanks to the IRS using Tax Tables rather than math, and the tax tables implemented in $50 income / $5 tax increments…

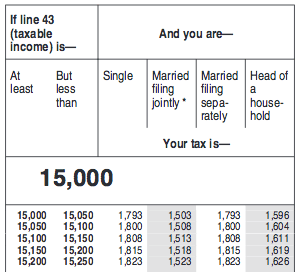

2015 Tax Table ($1503 or $1508 due)

…all I had to do was increase my contribution by $1 and we get a refund of $5. Attention to detail earns a 500% return.

Final 2015 Tax Forms

Our 1040 Form 1040 as it appears in Turbo Tax.

And the Qualified Dividends and Capital Gains tax worksheet, which is used to calculate total taxes.

And the Qualified Dividends and Capital Gains tax worksheet, which is used to calculate total taxes.

Not shown on the 1040:

Not shown on the 1040:

– we contributed $5,500 each to two Roth IRAs

– I contributed $18,000 to my Individual Roth 401k

This is exactly how to use a Roth; we pay 0% tax on $29k in contributions, and all growth will be tax free.

Self-Employment Taxes & Other Potential Improvements

aka, things I wish I had done sooner / differently.

Self-Employment Taxes

Someone will comment that we didn’t really have the IRS pay us this year, because we had to pay self-employment taxes.

Indeed. However, whereas income tax payments are gone forever, the self-employment taxes proportionally increase future Social Security income.

I could eliminate the SE taxes as well, by employing myself at Go Curry Cracker, a Belize company. Initial discussions I’ve had with the legal types suggest this isn’t of sufficient value (yet.) (i.e. the tax savings don’t outweigh the costs and management overhead.)

– As a redeeming feature, I paid all of the self-employment taxes on two new credit cards to meet our minimum spend requirements, and the fee is a tax deductible business expense in 2016. This is part of how we are getting $10,000+ of free European travel (tax free.)

Health Reimbursement Arrangement

By formally employing my lovely spouse and providing her with a Health Reimbursement Arrangement (a IRC Section 105(b) plan) we could make all health care and health insurance costs pre-FICA. In a year like 2015 with child birth costs, this would save thousands of dollars instead of just hundreds.

Ask: If anybody has expertise in this area, please email me.

Tax Penalty

You may have noticed that Line 79 includes a tax penalty of $6. With self employment income we are supposed to make estimated payments throughout the year.

I didn’t do that… something to do with starting to earn blog income around the time GCCjr was born. $6 isn’t a lot of money, but I’d still rather use it to buy lunch.

Although… with SE tax of ~$5k, by not making quarterly payments to the IRS, and instead keeping those funds in our Capital One 360 account earning 0.75%, we made at least $36 in interest. Maybe I’ll have lunch after all.

After-tax Contributions to Individual 401k

I opened my Individual 401k with E-trade, since they are one of only two custodians I found offering Roth accounts (the other being Vanguard.) Unfortunately neither of these plans allow non-Roth after-tax contributions (although the E-trade plan docs are so sparse, maybe…)

Had I instead decided earlier* to be my own administrator, I could have contributed an additional several thousand in after-tax dollars to the Individual 401k. This is known as the Mega Backdoor Roth. And since our tax rate is 0% (actually negative) this is an ideal match for Roth contributions. Although I’m quite happy saving these dollars in the brokerage account, since clearly gains and dividend income are still tax free.

* I didn’t get around to opening the Individual 401k until late December, and Ascencus had already stopped processing new docs by then. Full credit and thanks to The Finance Buff for figuring this all out.

Final Thoughts

Overall 2015 was a great tax year. We continue to live beneath our means in part thanks to a zero/low/negative tax load.

In addition to a negative tax rate, we contributed $29,000 to Roth accounts for tax free growth and harvested ~$24,000 in tax free capital gains. Thanks to the self-employment tax, we will also receive increased Social Security income in about 20 years.

While there is always room for improvement, we have a negative income tax bill today thanks to mistakes of yesteryear. I now have a short list of things to learn and new potential optimizations for the future. Doing our own taxes all of these years has had great return.

So there you have it… even with accidental income in early retirement, Taxes are Optional.

—–

See All of Your Accounts in One Place

Track your net worth, asset allocation, and portfolio performance with free financial tools from Personal Capital.

Very nicely laid out. Now that Mrs. Root of Good no longer has an income in 2016, I’ll be doing the same thing you are doing. That is, using my blog income to max my solo 401k on the Roth side for $18,000 and two IRAs for $5,500 each (assuming I actually net $29,000 throughout the year…).

This answers my question I posed to you on twitter perfectly, and lines up with what I was thinking. It’s basically a free $29k Roth contribution without paying any tax.

I’m also in the sweet sweet spot of having the IRS pay me for being awesome. $81,200 in Total Income in 2015 (Mrs. RoG was still working) but zero tax owed and a $3,000 refundable Additional Child Tax Credit. Another joy of procreating frequently (beyond the obvious joy).

Would you consider doing an additional Roth conversion and having the CTC wipe out the tax bill, including ACA credit and State tax? Or would you rather have the cash?

ACA credit phaseout + state tax + student loan IBR payments put me at a 39% marginal rate even while in a 0% federal income tax bracket, so I’m very reluctant to exceed $42,000-ish AGI right now.

What I can do (with enough 1099 income) is max out the employer portion of solo 401k and then use the lowered AGI to convert more from Trad IRA to Roth. A tax free way to “launder” money from my taxable investments into Roth.

Nice!

You should give this a read: http://thefinancebuff.com/irs-guidance-on-circular-reference-in-obamacare-premium-subsidy-and-deduction.html

This doesn’t apply (we don’t have Obamacare.)

Oh right. And I read those posts too. I just saw self employed and health insurance and my mind immediately jumped to this.

I still find this loop in the tax code amusing :)

As do I. You can always rely on the IRS for entertainment ;)

Your interest income is pretty high ($4.4k after subtracting the tax-free portion). I’m curious what is the source of that, if not cash? My understanding was that you didn’t keep a large cash balance.

A seller financed mortgage

https://gocurrycracker.com/rental-hell/

Thanks for giving the insights into y’alls income/taxes. The big benefit to doing your own taxes is that you know your complete financial situation and can research ways to optimize/reduce your taxes. My own SE/blog income isn’t enough to really worry about making any major moves that would just complicate things and add more accounts to track. But that doesn’t mean I’m not trying to boost up my side income. I look forward to the day that we need to complicate things a bit.

I understand the preference for simplicity. I only added the additional account this year as the income grew.

Maybe of interest, I shared some ideas for blog monetization.

Hi GCC,

Could u explain to me how you are not paying taxes on the roth 401k contribution or the roth ira contributions? My understanding was that Roth accounts are on after tax income.

Also, in order to make an employer contribution to the 401k, is there any qualification on type of company? Ie does it matter if ur sold proprietor, s-corp, or llc?

Thanks and love the blog :)

Maybe think of it this way:

We are paying taxes. We just happen to have a tax bill of $0 (plus the IRS gave us an extra fiver.)

There are nuances to the different types of qualified retirement plans and it depends if you have employees. See this as a start:

https://investor.vanguard.com/what-we-offer/small-business/compare-plans

Cool! May I ask how you arrived at the tax number of $1503? I understand the credits equaled or were greater than the tax owed, and therefore it was a wash. But I’m wondering how the $1503 figure was computed. Thanks :)

Read the Qualified Dividends and Capital Gains tax worksheet above, and/or look at our 2014 tax return where I walked through this in more depth.

Gotcha. Very financial ninja-like?!

Not that you needed to but the link at vanguard said employer contributions could be made up to 25% of income (minus half self employ tax).

So helpful to see it all mapped out like this. Thanks for sharing your tips — and your actual tax return! Right now we’re only planning to have dividends, interest, long-term capital gains and rental income in retirement (and no child tax credits), and are factoring in how to optimize all of that to maximize our ACA subsidy. We appreciate your past breakdowns of the ACA and taxes for those calculations, btw. But not having earned income means losing out on some of those retirement account opportunities/tax deductions, so thinking about finding some small side hustle that would open up options… or maybe we finally bite the bullet and monetize the blog! But since we’ll be in the U.S. for the foreseeable future, we certainly won’t be able to get anywhere near $100K income without owing taxes — LOL. But glad you guys get to enjoy it!

ONL – I don’t believe the fact that they live overseas has anything to do with their low tax liability. It’s due to the fact that a majority of their income comes in the form of qualified dividends and long-term capital gains. This strategy would work the same for you in the US!

Correct, nothing at the Federal Income Tax level is dependent on being outside the US.

However, with ACA subsidies factored in, the Traditional retirement accounts may look more appealing. We would want to keep MAGI below 4xFPL certainly, and 2.5xFPL probably.

It is interesting to me that this is one of the situations where claiming the FEIE (for the Schedule C income) could possibly provide a negative effect. While tax owed would still be zero (ignoring SE), the retirement contribution is shielding some small part of future growth. With FEIE there is no income support that contribution. The one hope had been if you could use 8812 to get a refundable portion of the CTC, however that is barred for FEIE (2555) claimants.

This is in great part why we didn’t claim the FEIE this year. I’d want biz income to grow 3-4x before going down the FEIE path.

It is still possible to get the ACTC while claiming the FEIE, but it requires having earned income above and beyond the excluded amount.

Simplified comparison for Australia:

Company:

Income 111,084.16

Tax -33,325.24

Dividends -77,758.92

After tax 0.00

2 x Individuals:

Dividends 77,758.92

Super (pension) -70,000.00

Tax 0.00

Tax credit 33,325.24

After tax 41,084.16

Super (pension):

Income 70,000.00

Tax -10,500.00

After tax 59,500.00

Overall:

Income 111,084.16

Tax -10,500.00

After tax 100,584.16

Super-annuation pension is tax free after 60.

The dividend tax credit is great. Although a lot of the biggest US corporations pay no tax either. Nicely done

Tax-wise, the company is there to retain passive income based profits [non-personal exertion, ie work] in excess of that which would be taxed at greater than 0% for the individuals. Should income be less than the maximum taxed at 0% for the individuals then dividends can be paid from retained profits [if any] with the attached tax [franking] credits.

The shareholders of the biggest US corporations pay taxes on the dividends and cap gains on sales of appreciated stock. I get what you mean but I just hate when the occupy wall street crowd uses that line.

I don’t begrudge anybody using that line. It is a good one.

Out of curiosity, why not make further traditional 401(k)/IRA contributions, which would reduce your tax due, which would transfer more of the CTC to the Additional CTC, which would offset more of your self-employment tax?

Good question. I was going to comment on this in the post but it was already getting long.

– It would take another ~$10k in Traditional contributions at the current 10% marginal rate to get the full $1,000 ACTC. 10% is a low rate, and I’m not 100% confident that we will always be at such a low rate in the future (income grows, we spend more time in the US and get ACA health insurance, tax laws change, etc…)

– I’ve already contributed $2,236 to Traditional accounts this year, using 1/3 of the possible $6,769 employer profit sharing space. I could add another ~$4.5k to this and get $450 in ACTC, but beyond that I would have to reduce Roth contributions to increase Traditional. Would I rather have $5.5k in Roth or Traditional when the savings is only 10%?

– I did no Roth IRA conversions this year due to having earned income, and my analysis that we would convert our whole 401k to a Roth tax free was based on annual conversions. With continual income, paying future tax at 10% is likely, and it really make no difference if we pay 10% today or in the future.

I’m still not fully convinced, so reserve the right to change my mind between now and April 18th.

Another great tax post, thanks!

One question: with $34k of qualified dividend income you must have either: 1) north of $1M in taxable accounts with typical S&P yields, or 2) less money and something kicking off higher yield dividends. What are you using to generate that $34k?

It’s a little discouraging for me as probably 85% of my invested assets are in tax advantaged accounts and so don’t have that nice 0% tax on dividend advantage. How did you manage to get so much money in taxable accounts? What is your taxable/tax-advantaged ratio?

> How did you manage to get so much money in taxable accounts?

Saved 70%+ of after-tax income for 10 years. Legal limits on 401k contributions mean most savings are done after-tax.

Other questions are probably answered in this post:

https://gocurrycracker.com/2016-gcc-asset-allocation/

Okay, so about 74% taxable, nice! As I said I’m about 85% tax-advantaged at this point. Is there anything I can do to minimize tax impact when withdrawing the money (through 72t or Roth conversion ladder), or am I doomed to pay regular income taxes because not enough of my money is in taxable accounts?

You will have to pay some tax, but presumably at a lower marginal rate than while working.

Impressive that you’ve accumulated a sizable amount in your taxable accounts in order to kick out the dividends. Mostly from index funds, I might add. Great work! One day I’ll hope to get there!

Man I was reading the article the entire time thinking hmmm when are they going to get to SE taxes really want to see how they tackled this..and then :(.

Disappointment is just one of the services we offer here at Go Curry Cracker ;)

Good stuff. We still had to pay tax in 2015 because Mrs. RB40 is still employed. Once she retires, then we will be in a very similar position to you. We still didn’t pay much tax even with her earned income. We were able to stay in the 15% bracket and avoid paying tax on dividend and capital gain. I also contributed $24,500 to my solo 401k and $5,500 to my Roth. It’s great to have multiple streams of income.

Very nice. Tax burdens of <15% are pretty low by historical and world standards. America is already great.

Very impressive. For next year’s feat, I expect you to pull off negative tax liability with blog income of $1000/day.

That’s where the Belize corporation comes into play

Can you elaborate a little on how that would work? Also, was it hard to set up a belize company?

I have not created a Belize company.

This would require a long blog post to explain. Which I will do if/when I get to that point.

How would employment at a Belize corporation eliminate self employment taxes? Is that part off a totalization agreement? I was under the impression that the totalitarian agreements just eliminated double payment requirements.

Not related to a totalization agreement.

Belize (and several other countries) don’t tax foreign source income, and non-US corporations are not required to pay or withhold FICA.

But you are still required to pay on your earnings. And, theoretically, IRS would seem to declare that you can’t take 100% of your earnings out as dividends. So you will personally be liable for FICA on your pay unless you expatriate, as I understand it.

Foreign Earned Income Exclusion for income.

I am outside the US.

FEIE for income, but not for SE Tax. Totalization agreement is the only thing that can wipe out SE Tax, afaik.

In my situation, I am outside of the US and have three sources of income. 2 are US source (a W2 and a 1099) and 1 is foreign source (country of residence). Ignoring my country of residence tax issues (I am here > 183 days per year and therefore tax subject), I still have to contend with US SE taxes.

The totalization agreement between my residence country and the US states that foreign employers do not pay US SS, they play in-country equivalent.

The totalization agreement also states that for a period of 5 years or less, I can make an election on my US source income as to whether to pay US SS or resident-country equivalent. I cannot eliminate the US requirement without being here for more than 5 years.

As I understand it, if you have no tax resident country that has a totalization agreement with the US (and Belize does not) then you are still liable for US SE.

I do not know how that affects foreign W2-style employment … but I suspect there are rules somewhere. Have you got a reference?

Also, unrelated, if you did establish a tax residency, do you have a pointer for using 1116 and a tax treaty to tax carry-forward (and applicable) credits?

re: 1116, I don’t, sorry

Because your main method of generating an income is to sell services you personally perform, you can’t avoid FICA.

If you have a business that doesn’t involve trading hours for dollars, but instead sells products or the services of people other than yourself via a non-US corporation, you can.

That non-US corporation would be in a country that does not tax foreign sourced income, and you would live elsewhere. We don’t live in Belize, Panama, HK, etc…

This is my understanding from speaking with an American tax attorney living in Belize. We had discussed him writing a guest post for this blog which might lead to some interesting discussion.

I’d love to see this guest post. I understand the idea of a foreign corporation operating this blog and therefore not having a US connection. Belize not taxing the income is the bonus. I also understand that the blog generates the income without directly selling your services. However, it still has to pay you to write the content. I suspect IRS would frown up your “donating” your services to a foreign corporation you happen to own. This salary would generate SE unless under $400. I doubt you could get away with a figure that low for the same reason. However, I am prepared to be educated in a future blog post :)

If he’s paid by a foreign company, how is that self-employment? Wouldn’t it be wages like any employee?

Regardless of whether the work is done as 1099-style self-employment or as an employee, The equivalent of SE taxes must be resolved. In both cases the Totalization Agreement, if any would drive whether there is US SE (or equivalent) due or not. In the case of Belize, there is no Totalization agreement so there is, as I understand it, a requirement that contributions be made to SS/MI. I believe in the case of employment the only requirement is for the individual’s contribution. In the case of self-employment, both halves must be paid.

re: salary

Many who write for a living get paid by the world. I’ve written guest posts on other sites for $0, but $0.03/word is not uncommon. This post has 1771 words so is worth maybe $53.

Research for this post was just doing my own taxes. The IRS thinks this is worth $0.

Thanks for the questions, it has made me think through this in more detail.

I’ll add overseas corp guest post to my to do list.

I look forward to that guest post.

While I agree that you could come up with a rate, for example $0.03/word on the effort, if you also own the corporation that is far from “arms length.” :)

I just love how you lay it all out. Provides a lot of transparency that lets your readers see how the knowledge on tax-free living translates on paper ( and real life). I would probably never do that.

But love your dividend income even more. Given your historical cost of living, can it be safely said that your dividends essentially cover your expenses?

Good luck in your journey GCC!

DGI

Thanks DGI.

Dividends did not cover our expenses this year, but it does cover most of our core cost of living (excluding child birth, etc…) Post coming soon.

Wow, congrats on another no-tax paying year! You continue to inspire us to look for loopholes to minimize our tax bill.

Hola Sr. Enchumbao

I don’t think loopholes is the best word for this. We are following the tax law as it is written, and more importantly as it is intended.

The backdoor Roth on the other hand is a real loophole.

My point being, no need to find loopholes! Just design life in the way that Congress, in their infinite wisdom, intended ;)

As an accountant it’s refreshing to see someone actively pursing a $0 tax bill by diving into the details of the system and sharing it with others. This should be something that all CPAs should learn from the start to help clients save as much taxes as legally possible. Out of everything that I’ve learned in my career when it comes to taxes, by peeking into your tax situation gives me something to aspire to and want to learn more about. Thank you GCC!

Awesome, thanks Jeff!

Thanks for the update. As always very thoughtful

In the future, you could also consider writing off business expenses, such as blog hosting fees, buying equipment (laptop, etc.), home office, traveling to conferences (that just happen to take place at very nice touristy spots). The possibilities are endless!

One other thought: if your business becomes large enough (maybe it already is) you might consider putting it into an LLC wrapper to shield yourself (and your assets) from frivolous lawsuits. You never know who you might insult or otherwise run afoul with. Especially, since you have assets in taxable accounts. Costs to set up are only a few hundred dollars (tax deductible!) and ongoing costs are pretty minimal too.

Blog income is net of expenses, aka all of that stuff is already taken off the top.

LLCs for single person businesses aren’t nearly the shield people think they are.

I would love reading about business expenses you were able to deduct. This seems like an area with lots of potential for lowering taxes for small business owners but also an area with some confusing tax language. Your detailed analysis on this topic would be really appreciated if it fits your blog post schedule at some point!

I’m also interested in your comment regarding LLCs (especially since that’s the route I went for my business!) Thanks.

I have a post planned about business expenses.

Google “when doesn’t an LLC provide asset protection” or something similar. Most of the links are provided by law firms trying to sell you an LLC, always a warning sign. But in general if you are personally providing services, such as in a 1-person LLC, you are personally liable for any negligence. There isn’t much of a corporate veil.

The LLC may help for separating debt in case the business fails, but we have no debt.

Looking forward to the post! And bummer about the negligence stuff. Makes my registering as an LLC seem a bit wasteful (it’s a simple DIY process at least, so I didn’t have to spend much). And thanks for the quick response as usual. Really impressed with your website.

I like to hear more of your thoughts too. There are obviously two ways of setting this up:

1: the blog is in the LLC

2: your unprotected assets (non retirement) are in the LLC

Under (1), it’s easy to see how a smart lawyer will argue that when your blog posts something offensive, he/she will go after both and your blog inside the LLC. The LLC has no assets, but you you do. Probably there is no protection at all through the LLC.

Under (2), the lawyer can sue you and your blog (same entity essentially), but your assets held by the entity are harder to crack for lawyers. Usually an LP with multiple partners (you, your wife, your kid, your mother-in-law with a symbolic 1% share) could all be parters. If the LP is properly set up and has no business relationship with your blog (LP only holds financial assets in brokerage accounts and other investments through their own LLCs), lawyers will have a tough time getting assets out of your LP.

If you use a single person LLC you probably still run the risk that a lawyer goes after the LLC in a lawsuit, I agree.

I don’t have anything to add.

Maybe put everyone’s feelings in an LLC so they don’t get offended.

To clearly distinguish my personal income from personal exertion [work] from passive income my company and I make work contracts for me. The contract letter states the task to be performed, the outcome to be achieved, the time frame, the minimum hours of work to be performed and the salary or wage to be paid. The hourly rate is what would be considered fair compensation. I define what is fair to be something significantly more than the minimum wage. My company pays me the [modest] salary at least annually and I declare the salary on my Australian tax return.

How are you able to write off half of your self employment tax? I’ve been self employed for 13 years and have never written this off. Is it because you are set up as a sole proprietor and the money flows through to you directly? I’m set up as an LLC, file taxes as an s-corp…and so pay self employment tax through a monthly pay check I cut myself. Wondering if that’s the difference…

The deduction in question is, as I understand it, allowing a Švédské C filer to deduct a business expense for the employee portion of FICA/MI. A similar deduction should be reflected in your Scorp filing.

Your business would deduct it as an expense on the S-corp taxes

You have the amazing gift to even make taxes interesting :-)

Great post!

More of a curse, really ;)

Thanks Karl!

Wow, you guys really hit it out of the park this year GCC! Good job.

I love that you’re still so open about your income. Most bloggers, once they “hit it big” stop posting things like tax returns, and start hiding the fact they make a huge chunk ‘o change from their blog.

Love your transparency GCC! You set a good standard.

Thanks Mr. Tako

This is still a little blog, so no big time for us. Maybe one day though.

1. Why not add your spouse to the business and bring it to 53769 tax advantaged space.

2. I think 401k vs roth 401k is not the normal argument at your income level, because if pretax 401k brought your income under 11K through pretax contributions (might be 5500 not sure if spousal iras can be eligible based on the same income or each needs its own 5500), I believe you would not have IRA eligible income.

Tax advantaged space can’t be greater than earned income minus self-employment tax, so can’t be higher than ~$34k. We used $31k of it, so not much room for improvement

I thought 401k contributions (at least ones that don’t reduce income in the case of self employed) does not reduce income eligible for IRA – so you could basically use the same income both for 401k and ira. Was always unsure of this, so would be useful to know if you do? – Basically on 20K of business income – you would have the ~20% piece + 18K Roth 401k + 11K IRA/Roth IRA. Let me know if you are sure this is incorrect.

Ahh… yes, you are correct. Or at least I think you are; I’m not sure where specifically in IRS docs to confirm for certain.

We still couldn’t contribute more than 100% of income to the solo 401ks, but could double dip contributions to the IRAs. Total contributions would be $51,617 in that case, assuming 50/50 split on the income.

Too late for 2015, but something to plan for next year. Thanks!

I’m a little confused on some basic points. It seems like your capital gains, ordinary dividends, and interest – passive income – is added along with your “earned income” from the blog to figure your marginal tax rate. Why isn’t your marginal tax rate based only on your earned income, i.e., the $36,419? I thought a married couple filing jointly could have earned income up to $74,900 and pay no taxes on any amount of long term capital gains. For example, suppose you had $80,000 of income from long term capital gains, and no other sources of income. Would you owe any tax at all on that 80K? Thanks.

marginal rate is 0%. He’s only paying self employment taxes.

Effective rate is 0%. Marginal rate was 10% on earned income, but tax obligation was eliminated due to credits.

Wouldn’t the Foreign Earned Income Exemption have wiped all of the blog income away anyway since it covers about 100k? You lost me in the need for the child credit to wipe away the $89.

Oh and awesome job again this year! I’ve been trying to find ways to reduce our tax liability while working, but have so far come up empty handed.

It would have. It was an option, but not the best one.

Getting $5 back and putting $29k into Roth accounts is better than paying 0 income tax and the same Self Employment tax.

The combination of earned and investment income is used, but they are taxed at different rates.

If you had earned income after deductions of $74,900 (Line 43) + investment income, you will pay 15% or greater tax on all of your investment income and the earned income would be taxed, some of it at 10% and some at 15%.

If you had only investment income (QDs & LTCGs) of $74,900 (Line 43), all of it would be tax free. The next dollar would be taxed at 15%.

The charts on this post might make it more apparent than looking at the 1040

https://gocurrycracker.com/obamacare-optimization-vs-tax-minimization/

Great information as always GCC, can you consider have a search option in your website. There are so many great posts I like to save as notes, but really hard to find after going back. Thanks.

Thanks Yu Shao.

There is a search box in the right side bar, sorry if it is hard to find.

Also take a look at the archive page.

Thanks for all of the great content you guys produce.

I am getting ready to possibly embark on a year or two (maybe more) of actually pursuing my passion and seeing if I can turn that into a way to “pay the bills”. Where would you recommend someone start reading to fully understand what you guys are accomplishing with your taxes?

Thanks for any help. – Joe

The post Never Pay Taxes Again explains all of the fundamentals.

It’s amazing that the IRS is so gracious with taxes considering your total “income”. Don’t get us wrong, this is great for you guys. But as a government, it is unbelievable that they are leaving a lot on the table.

We are also doing our taxes, but due to a international move last year we have to file taxes in two countries on paper! We can’t file electronically, go figure. The good thing is that because we dumped a portion of our home sale proceeds into RRSP accounts, we are slated to get a massive (5 digits) tax refund for the year. However, next year we will be paying roughly 30-40% taxes on our incomes without any possibility to lower this any further. This is the inevitable downside of living in a “social” country.

Keep cracking ;-)

The upside being that you live in a social country.

On a related note, could you use your beautiful daughter as a model for the blog (think picture on home page, etc.), then pay her (flat out, stipend, retainer, etc.) for that service. With that income could you then start her (continue, more likely) on her merry way to retirement fund (IRA, Individual 401K, etc.) fun?

He is a boy. But yes, there is a possibility there.

We could in theory pay our son for services rendered. He can earn up to $6.3k/year tax free (the standard deduction) which would be fully deductible as a business expense.

Because he is a child in a family business, he is not required to pay FICA taxes. With earned income, he could contribute $5.5k/year to a Roth IRA, and by the time he was 18 would have a Roth IRA balance of $250k +/-. With these funds in a retirement account, they probably wouldn’t impact his FAFSA applications.

Income needs to be fair and reasonable though, and for real work. If I wouldn’t pay $6.3k/year in royalties for the right to post a pic of the Kardashian spawn on our site, then it wouldn’t be reasonable to pay our own child the same.

If anybody has real world examples of a child working in an online business though, please share them.

Sorry about the gender goof. I knew I should have checked when posting. Thanks for the clarification, and I hope to see real world examples of a child working in an online business as well. Safe and happy travels to you. Thanks for your work on this blog.

No worries, Doug. People often guess he is a she.

Hey CGC,

Very impressive. We have some rental properties. I am deciding whether to sell them or keep them as part of our retirement income. I am curious as to how this would affect our taxable income and income bracket. Will my rental income be the same as qualified dividend, which would great. Or will it eats into the 12,600 standard deduction and $12,000 exemptions?

Thanks!

Rental income is regular income. But it does already have special treatment through deductions, depreciation, etc…

Depends on the yield you are getting with your rentals. Why give up a safe and stable 5% rental yield in exchange for 4% annual withdrawals from an all-equity portfolio that can fluctuate wildly. Even after 15% marginal taxes the real estate gets you more than 4% tax free (not even counting the preferential tax treatment of being a landlord, due to depreciation etc.).

As much as we hate paying taxes (currently while working and in the future when retired), we plan to have some diversification of income. A lot of it will come from equities (dividends and capital gains), but we’d like to have some rental income as well as a consumption floor when equities drop.

In summary, don’t let the tax tail wag the dog.

Thanks earlyretirementnow.com and GCC! Lots of think about. Landlording isn’t too bad most of the time :). Currently, we do have about 50% of our money invested in real estate. In the next year or two we might just sell one off to cut down risk a bit.

If the properties are highly leveraged with mortgages , maybe that gets a bit risky.

But according to the federal reserve stats: https://www.federalreserve.gov/releases/z1/current/z1r-5.pdf

Net worth in real estate is more than corporate equity plus mutual fund shares combined, so 50% real estate is not totally crazy. But retirement is only fun if you don’t have to deal with needy tenants all the time, so that’s something to consider too! To do the travel life style like GCC you probably can’t have any rental properties at all.

Hello GCC,

Avoiding tax as much as you can sometimes is a good thing. But I just wonder what will happen to the less fortunate people: homeless, orphanage, elderly, disable people, environment, and other society issues. Have you ever think about those people? And who will care for them? Or you just shrug your shoulder and says: “who care?”

Just imaging, the entire world fills with lucky people like you, no wars, no terrorists, everyone financial successful and enjoy all the leisure things like living in a utopia; then who will produce food, perform all labor work, provide all services for you to enjoy, defend our country so you can be proud to say “I am an U.S. citizen”?

Of course, you can go through all the loophole to find the crack in taxes and avoid them, but as a tax payers, I share our society’s burdens because of the compassion toward other humankind and to protect the freedom that our ancestors fought for it.

So paying a little tax, from rich people like you, will not hurt.

I was raised on food stamps. My wife spent 2 years in an orphanage. So yes.

Something to google:

What percentage of your tax dollars helps orphans?

What percentage of your tax dollars creates them?

Moral of the story: just because you pay taxes, doesn’t mean that you are net total helping people or improving society.

Anna, your complaint should not be directed at the GCC family; they didn’t write the tax code. You should talk to Congress, who did. Also, both Jeremy and Winnie worked hard for years to build up their net worth, and I’m sure they paid taxes along the way. The reason they are “rich people” is because they made conscious frugal choices all along the way, and instead of squandering their incomes, they found ways to save and invest them. So by trying to shame them into paying taxes out of the goodness of their hearts you are really trying to punish them for their prudent financial decisions over the course of years.

Also google “iraq war expenses”.

The money saved on taxes could be redirected directly to charities rather than expect the government to do the right thing.

I fully agree with Sam, and would add this for consideration Anna. A more prudent use of money “saved” on taxes would be to make charitable donations. (Which coincidentally is tax deductible in many cases.)

Uncle Sam has never had the reputation of spending money wisely especially when it comes to social services. So Anna I applaud your concern for the less fortunate. I only suggest there are better ways to do it then paying more taxes than legally required.

Good point, Anna. Most people who target an early exit from the labor force have already paid a whole lifetime’s worth of taxes (or multiple?) by the time they retire. My wife and I will likely not be able to completely avoid income taxes and we will still pay sales taxes and local property taxes (either as homeowners or renters via the landlord). No guilty feelings here!

Anna,

Perhaps you need to familiarize yourself with the tax system in US and you will see why taxes are total rip off for all of us.

Good info,,, very smart….. wished my hubby had known about this many moons ago. Congrads! on your wonderful blog. You are helping a lot of people I am sure of this….That what life is all about!

I don’t see mentioning of S-corp, so I am assuming you are filing as sole proprietor?

I was hoping to read about strategies on how to reduce SE tax through S-corp. :-)

When do you think is worth it to incorporate to reduce SE tax burden?

Income would maybe need to go up 4x or so.

Gotcha. I currently have mainly self employment income from two sources(one passive, one active), it’s not at that threshold yet, but I do see it growing to that in future, so I am looking forward to your writing on how to cut down SE tax, the IRS intended ways. :-)

I appreciate the transparency also! It’s one thing to say you can live on 25 or 40k a year as an early retiree when you are earning 400k in blog or other income as a nice fat cushion. It’s another proposition entirely to earn a respectable but modest 36-50k a year beyond investment income and still be comfortable. I guess I appreciate that your blog is full of nuts and bolts and less fluff!

+1. Looks like GCC will do fine even without the blog income for now. I am following and tracking FIRE bloggers to see how they are doing with the 4% rule and I am especially interested in how they will do if and when another 2008 hits. Post-retirement income from blogs and other sources tends to muddy the waters.

Retiring in your 30s… it would be weird to never earn another dollar.

Its not retirement per se then is it? If blog income comes close to 4%, tracking you guys is no longer prudent.

I am only saying that for myself in the context of using FIRE bloggers as benchmarks. Your blog is a great resource regardless of your income.

I think a blog can be considered passive income to the extent that earnings are not directly dependent on the amount of personal time expended to create or maintain it – ie to the extent that a blog is a product for sale. The time spent then being more like ‘capital investment’.

Retirement or not-retirement, I think you should call it whatever makes the most sense to you. I’ll continue to call it retirement, because we just live the way we want without concern for dollars and without time restraints.

I don’t think tracking us has ever been prudent for understanding the 4% rule in action. We’ve never spent anything close to 4%, even during the first 3 years when this blog made $0.

And really, nobody follows the 4% rule like a robot. Sometimes you spend a little less, sometimes you spend a little more. If the market is doing well, people tend to spend more. If it isn’t, they spend less. And nobody is sitting at home watching Netflix. They are doing stuff. And at some point, that stuff will earn an income. We have to constantly turn down opportunities to earn more of it.

I wouldn’t be opposed to this blog earning 400k ;)

With the way Internet traffic seems to work, the bigger you get the more opportunity you have to grow. So with no more effort than I’ve been making (which is little) I can see the possibility. I don’t see it changing out day to day life though.

Absolutely killing it. One day I hope to be in your shoes, the dividend income alone is impressive! Keep up the great work.

Hey GCC!

So depending on how much interest received from self-employment savings, you can potentially outweigh the tax penalty for foregoing estimated quarterly payments? I would be curious to analyze break-even points for that. Obviously if you need the self-employment income to live on it’s not earning interest in savings, but I still think it would make an interesting analysis. I couldn’t find anything on Google about weighing the penalty for use of your month throughout the year. Perhaps that’s an article people would be interested to read? ;)

The IRS charges 3% interest on underpayments for 2015. If you can earn more than 3% after-tax, it can make sense to wait rather than make estimated payments. I didn’t really look into the Turbotax estimate, but I think we missed out on the lions share of interest/penalties because last year’s tax liability was $0.

I plan to make estimated payments this year.

I think I read most of the blog contributions from GCC and they were all really good. I skimmed though the comments sections before and liked them but the comments here in this discussion were beyond anything I had seen before, anywhere and even here at GCC. I learned a lot! It would be nice if GCC could create a summary blog posting on some of the advanced tax avoidance techniques:

1: What are the tax write-offs for retirees running a blog, including 401k, profit sharing, travel expenses, etc.

2: What are the ex-pat tax breaks

3: How can you pay your under 18 year old kids?

But I’m sure you already though of that :)

Keep up the good work!!!

Ernie

Hey GCC!

I’ve been living in Mexico for around 3 years (naturally not going back to the States for more than a month in a year due to working here) now but this year, I was in the States for 36 days so if it’s by the tax year, I would barely not qualify…

On the physical presence test for the FEIE, the 330 days don’t have to be within the tax period right?

I probably wouldn’t have looked into this tax savings if it wasn’t for your post!

Thanks for all you do!

330 days can be in any 12-month period. Not required to be the calendar year / tax period.

Although if you are living/working (and thus paying taxes) in Mexico, you probably qualify under the BFR test and don’t need to worry about the 330 days.

And also in that case, best to calculate taxes with the FEIE and with the Foreign Tax Credit, and see which one produces the best results.

Good point about the BFR test and comparing between the FEIE and the Foreign Tax Credit. Always more IRS stuff to read… ;)

Thanks again!

Amazing job on the blog income. What tax minimisation opportunities will being a business owner create for next financial year?

I’ll let you know next year! ;)

Great job GCC! I have also been paying zero Fed taxes but for a different reason. I live and work in a highly taxed country where it is more beneficial for me to take the foreign tax credit instead of FEIE. I pay high taxes to the country where my earned income is. The FTC gives a direct dollar for dollar offset on US taxes and allows you to build up a reserve of credits up to 10 years to shield against future Fed taxes when you return back to work in US or even if your passive income in US exceeds the no tax threshold. So, whether to take the FEIE or FTC depends on where you live and where you earn income.

But looking at your dividend entry on tax return, you must have a lot in taxable accounts. At this level of asset base, you don’t need any blog income at all to live ‘happily ever after’! Great work in life planning and finances!

Hey PMV

Indeed, we don’t need any blog income. It was kind of an accident.

I’ve mentioned to a few people in comments to calculate taxes with the FEIE and the FTC and see which provides the best outcome. Thanks for sharing an example of how the FTC can be superior! Bummer about the big tax bills though

Thanks for sharing your returns and philosophy–I learned a lot!

Hu, I was satisfied enough doing my own taxes this year (first year in the US), didn’t even tryo to optimize anything… I guess this will have to come later.

Thanks for the detailed explanations here!

I’m a total dork when it comes to taxes! I love doing them. Nice work on yours!

Curious about the CapitalOne360 checking account. You mention a 0.75% return on these assets and that you keep 3 months cash on hand. However, to get the 0.75%, it looks like you need to be keeping >$50k in the checking account. Am I missing something here? (looking for a place to open a better checking account for my small business, currently with Schwab). Thanks.

The savings account is 0.75%. The checking account is a different product.

Some incredible work you’ve done here and it really has me rethinking my savings strategy. I intend to funnel a lot more money into traditional accounts now.

One question I have though is, prior to the blog income this year, where does your money come from for living expenses? My fear is that if I am shoveling all my money into traditional 401k/IRA/HSA that I won’t have access to the money until 59.5. I believe my spouse and I will be able to contribute the maximum this year.

It seems that you also have significant sums in brokerage accounts. Is that the solution?

Saving significant sums in a brokerage account is a solution, albeit not necessarily the best one, depending on your current marginal tax rate.

You can access funds in a Traditional IRA before Age 59.5 via SEPP withdrawals, Roth IRA Conversion, or simply by withdrawing funds and paying the 10% early withdrawal penalty.

Here are a couple posts that explain the concepts:

http://jlcollinsnh.com/2013/12/05/stocks-part-xx-early-retirement-withdrawal-strategies-and-roth-conversion-ladders-from-a-mad-fientist/

http://rootofgood.com/roth-ira-conversion-ladder-early-retirement/

I almost mentioned this yesterday in one of my rambling comments but here I see it in action.

I loved how you put $89 in a Traditional IRA in order to meet your tax threshold. and then socked the other away in a Roth. I was going to suggest that! But aside from the 0% rate on cap gains, are there any interesting thresholds you would look for if you can’t get that low? I’m eyeing the savers tax credit, but it’s pretty hard for me to hit.

Wow. This is a lot to know in order to do a little to save a lot. I’m impressed.

You can definitely use Traditional to Roth IRA conversion to create income to qualify for ACA subsidies right? If so, that seems like one of the best early retirement tax hacking situations to be in

Right. If you are below the 133% FPL threshold that may be the way to go.

I’ve devoured your blog over the last week or two, it’s awesome.

What would you recommend I read to really understand my taxes (US), including the ACA, so I can optimize mine like you do? I’m considering the Ernst & Young Tax Guide, the JK Lasser Tax Guide, or just plain old IRS documents.

Background, if it makes a difference: I’m 43, early retired, with about $40k earned income and about $5M in taxable accounts, holding Vanguard funds generating dividends & cap gains distributions of at least $80k/year. Almost nothing in retirement accounts – just $29k in a solo 401k (I will contribute the max possible each year going forward). No Roth accounts. No state income tax.

> What would you recommend I read to really understand my taxes

This blog?

Thanks for sharing the 2015 tax document guys! Fascinating stuff.

To simplify, is the basic goal to limit household income to ~$100,000, have a business for expense deductions, contribute to the max for all retirement accounts, and have a no state income tax state? A $100,000 household income is definitely a healthy income anywhere, and especially in Asia.

Hypothetically speaking, do you know how a household who makes a higher income, like $500,000+ could pay no taxes either?

Thx!

The amount is only part of the equation. Different kinds of income are taxed in different ways. Go Curry Cracker maximizes their income to be in types that have low to no taxes or that can be excluded in other ways. They also leverage geo-arbitrage. There is no single formula.

Excellent comment, bexelbie.

Sam, for a hypothetical $500k earner in the US… I would assume they would consult a high powered attorney and CPA for tax advice :)

But… it does depend on type of income. If it was all advertising and affiliate income from a blog with some product sales, you could put all blog / book assets in an S-corp and pay yourself a reasonable management salary of ~$40k with some additional dividend distributions. It wouldn’t cut the tax bill to zero, but it would reduce it significantly.

If the hypothetical household moved abroad, there are more options. Guest post coming soon.

Can’t afford a high powered attorney on that hypothetical income. :)

Here’s the thing, so you pay taxes on a $40K income w/ an S-Corp. You still have $460,000 in distributions where you still need to pay the normal income taxes. Yes, you can max out $53,000 to a SEP IRA or Solo 401k, but that still leaves $407,000 in distributions that face a effective tax rate of roughly 30% = ~$120,000 in tax liability.

Yes, the $407,000 in income after SEP IRA max doesn’t have to pay the FICA tax of 12.6% or whatever it is, but $120,000 in income taxes is still a FAR CRY from $0 taxes.

What am I missing here?

Sam

Why are you distributing all of the earnings?

I can let the earnings sit on the company’s balance sheet or distribute them. It’s just accounting. The earners in an S-Corp pass through to an individual’s tax returns, so there’s no escape paying income taxes.

In this hypothetical situation, what would you do with the $407,000, and how would you avoid taxes on that annual income after SEP IRA max and business expense deductions?

Yeah, sorry, I was thinking of something else.

If you are earning income via freelance and real estate profits, there is not much you can do. You’ll pay tax.

If income is from financialsamurai.com and you are willing to move outside the US… my next guest post will address that.

If not, moving out of California to a no-tax State…

Options are limited as income exceeds the couple hundred K mark.

Cool, I’m looking forward to the guest post!

If you have the time, do you mind highlighting line by line how someone with a $500,000 income can pay no taxes or very little? Check out my comment below.

So, if I am reading this correctly (even being conservative with annual dividend yields) you have somewhere upwards of $1,000,00 (if not north of that figure) in equities to be producing annual dividends in that amount. Or am I missing something? Just curious since transparency doesn’t seem to be an issue for you :-)

Sure. You can read this post or practice fiscal voyeurism on the master list of finance bloggers net worth. (I’m not on it.)

Hi, I’m struggling with one detail. You show your final 1040 in Turbo tax Line 78 as owing $5147 in taxes and I’m not understanding how that went away? I understand that the 1040 did not include contributions to Roth accounts but that would not eliminate the balance. Can you or anyone help me with this. Thanks!

It didn’t