Going back to Cali, stylin, profilin

Growlin, and smilin, while in the sun

Paying taxes and health insurance premiums

Driving to the mountains in the vintage Escort– LL Cool J ft. GCC

We have been having the Forever Home discussion for some time now… Is there somewhere we love that would be a good place to raise a kid or two?

We have a few International destinations in mind, but several places in California rank high on our list of criteria.

I hear California is an expensive place to live, with high taxes, costly health insurance, and sky high housing prices. I figured I should at least crunch some numbers before we consider putting some California cities at the center of our radar.

Going Back to Cali

Setting up a home base in California would be a big change in our lives, no doubt. What would it look like, financially speaking? How would it impact taxes, health insurance, and overall cost of living?

Taxes

California has a State income tax which treats all income types equally. Dividends, Roth IRA conversions, capital gains, and earned income are taxed exactly the same.

This means the end of tax free Roth IRA conversions and capital gain harvesting.

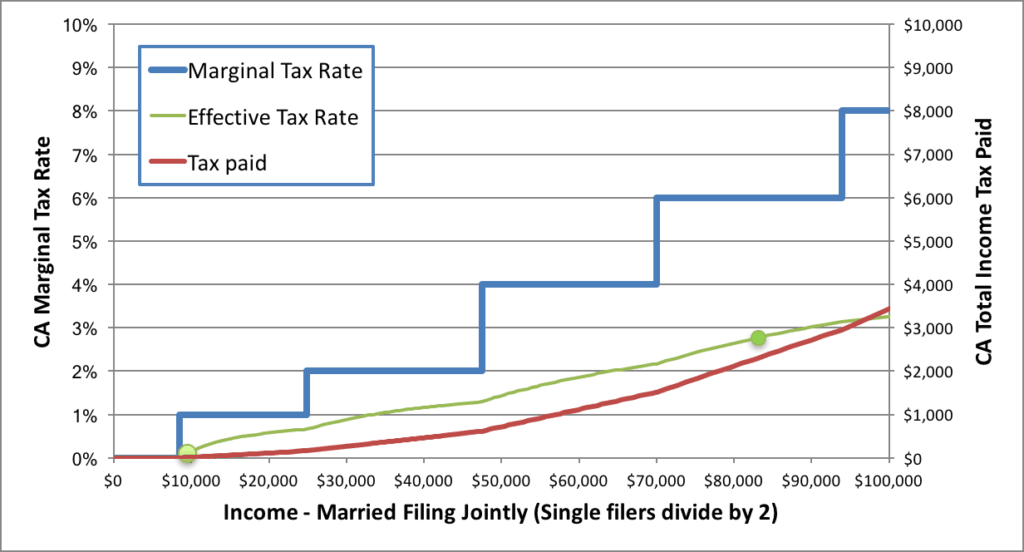

California tax brackets and burden (2017) – Green Dot is 400% FPL for family of 3 (2018)

With taxable income for the past 5 years of our retirement and world travel of $100,000+, we have had zero Federal tax burden. At similar levels of income, California would want about $3,000/year or $250/month.

$250/month seems a small amount for a good quality of life.

(Other States for comparison – WA: $0/mo, MN: $375/mo, OR: $600/mo.)

Health Insurance

There are 7 States without an income tax, but we would need to purchase health insurance in all 50 of them.

The ACA long ago largely killed the Roth IRA conversion pipeline for US residents (unless exempted), by implementing an income based subsidy aka a tax.

Technically, the TCJA eliminated the ACA individual mandate, so one could choose to self-insure or purchase a non-ACA compliant HDHP like we had pre-ACA. Self-insuring in a system such as exists in the US would be a losing strategy due to unpredictable and fantastical healthcare costs, and I haven’t seen good alternatives.

Therefore we would purchase an ACA health insurance policy on the California exchange, aka Covered CA.

ACA insurance premiums are a function of family size and income, so I explored the premiums for a few Bronze and Silver plans on Covered CA at different income levels. The Bronze plan qualifies as an HDHP and offers a Health Savings Account (HSA.) The Silver plans potentially have CSR subsidies (details here.) With income less than 266% FPL (~$55,000) children are covered by Medi-Cal, so prices go down and coverage goes up if our income is below that level.

| FPL $20,780 for family of 3 (2019) | Income | Bronze ($/month) | Silver ($/month) |

|---|---|---|---|

| 200% | $41,560 | $2 | $184 |

| 250% | $51,950 | $47 | $319 |

| 300% | $62,340 | $107 | $457 |

| 400% | $83,120 | $278 | $628 |

| 400% + $1 | $83,121 | $919 | $1,269 |

These price points are just the beginning though.

If any real issue were to come up, for the Bronze plan we would be looking at a $6000/person deductible and 40% co-insurance on everything thereafter up to an individual max of $6,550. (Family deductible of $12,000 / max of $13,300.) Covered CA estimates the total annual cost for “medium usage” to be $3,300 at 300% FPL and $5,375 at 400% FPL. This translates to an additional ~$170/month above and beyond monthly premiums, in the form of payment at the time of care.

For Silver plans, instead of an individual deductible of $6,000/person, it is $650/person at 200% FPL and $2,220/person at 250% FPL. Max out of pocket is lower and copays are much cheaper too. At higher income levels the lack of CSRs mean max out of pocket levels similar to Bronze plans with much higher premiums, so which is better really depends on how much care we would really need.

For incomes above 400% FPL + $1, the ACA subsidy cliff means premiums increase by ~$640/month.

Adding this all up, with annual income of $100k it seems like health insurance and care would run at least $1,000/month for a Bronze plan, and an extra $300/month ($3,600/year) for a Silver plan.

By comparison, we currently spend $75/month for all 3 of us for better coverage and better care (with great dental too!) via the Taiwan National Health System (like Medicare for All.) When we brought Jr to the Dr for flu-like symptoms we paid $3. When Winnie went to the emergency room we paid $30. A dental filling is $10.

Cost of Living

We have lived large across quite a few different countries, with total cost of living ranging from ~$2,000/month in places like Mexico/Thailand/Guatemala, $4,000-$6,000/month in Taiwan and the US, and $8,000/month in Europe and Japan. How would things be different with a home base in California?

Housing / Transportation / Food (aka the Big 3) are where we focused during our accumulation years, so I started looking there.

Housing

I have heard housing is expensive in California, but this is primarily in cities where we would hate to live. (Hey Bay Area, what’s up?)

I’ve been using Zillow and WalkScore to understand the housing market in a few cities we are considering, using the same process we used to find our ideal home back in Seattle.

Roughly, we can rent a 2 to 3 bedroom SFH in the 1200-1500 sq. ft range for about $2000 – $2500 per month. Some with garages, some with basements. Apartments with amenities like a pool are similarly priced. Prices drop (sometimes significantly) if we are willing to be dependent on a car, which we are not... walking to the library, grocery store, farmer’s market, coffee shops, and restaurants is important.

The same houses that rent for $2,000/month sell for around $750,000.

That is a price/rent ratio of 31. (Other data points: SF & Manhattan ~50, Austin, TX ~25, and Detroit ~6. Data from here.)

Even with no mortgage, property taxes and home maintenance would still be $1,000+/month. Imputed rent helps a small amount with cash flow, but I could get better ROI in my savings account. Buying a home in this environment would definitely be a luxury purchase / lifestyle choice, probably because we deserve it. Fortunately, we avoid the whole mess by being Renters for Life.

Overall this is a about a wash compared to our current rental in Taipei.

Car / Transportation

For easy access to outdoor adventure like National Parks we would probably get a vehicle.

A shiny new Tesla X would set us back around $150,000. Good times. But we would just pick up an used Ford Escort or similar for $10k or less, and drive it one day per week or so.

A few bicycles and shoes would be our other major transport expenses, along with the occasional Uber. Guesstimate: $250/month.

Food

Farm to table restaurants and great farmer’s markets are our life blood, and eating well is one of our core values. As such, we end up spending roughly $1,000/month on food.

This summer we spent a few days in a nice town in California and visited a couple farmer’s markets. We scored some great deals on produce, including a small flat of figs for $3. A week later we bought a smaller amount of figs at a farmer’s market in Seattle for $8. Being near where the food is grown reduces costs and improves quality.

I wouldn’t be surprised if moving closer to the food epicenter reduced our total food spending, but since it has been consistent across several years and numerous countries, I’ll go with $1k for margin.

Total Budget

| Cost of Living | Monthly | Annual |

|---|---|---|

| Rent & Utilities | $2,500 | $30,000 |

| Food | $1,000 | $12,000 |

| Transport | $250 | $3,000 |

| Entertainment | $500 | $6,000 |

| Vacation | $500 | $6,000 |

| Taiwan (annual trip) | $250 | $3,000 |

| Misc | $500 | $6,000 |

| Gifts/Charity | $250 | $3,000 |

| Taxes | ??? | ??? |

| Health ins/care | ??? | ??? |

| Total | $5,750 | $69,000 |

Without taxes or health insurance, we could potentially spend $69,000/year or $5,750/month. This includes summers abroad and annual visits to Taiwan to see family. We often fly for free so some or all of this $9,000 travel budget could be zero.

With annual income of $100,000, Health insurance/care and California income tax would add $15,000/year, bringing the total to ~$84,000. That is only 4x what we used to spend in Seattle.

But wait a second… if we are spending so little (relatively speaking) why do we need this much income in the first place?

Income & The Downward Spiral

Since we don’t need to save for retirement or pay off debt, with a total cost of living of $84,000 we only need an income of $84,000. Seems legit.

But, if we just dropped income by $880/year to $83,120 (exactly 400% of FPL) then we are on the more budget friendly side of the ACA subsidy cliff and our expenses drop $7,700/year. (That is a nice 870% tax rate.)

Roughly $40,000 of our annual income is from dividends and interest. With blog income equivalent to 2017, I could shelter 98% of it in 401k/IRA/HSA. I could get another $40,000/year by selling some stock, after which we have $80k to cover our cost of living and then some.

This isn’t income though. If I sell $40,000 worth of stock, and that stock has doubled since I bought it, then only $20,000 of the sale is actually income (a capital gain.) The other $20,000 is a return of basis.

Between dividends and stock sales we now have $80,000 in cash, but only $60,000 in income (~300% FPL.) With lower taxable income, health insurance premiums drop by another $2,000 and CA Income tax drops by $1,000, bringing total cost of living to ~$73,000.

But we can do better. I could instead sell stock at full basis (zero capital gain), withdraw some contributions (or aged conversions) from our Roth IRAs, or use some of our existing cash. None of these count as income, so we can cover the full $73,000 budget with only $40,000 of taxable income (~200% FPL.)

Now CA income tax drops by an additional $500 to a measly $12.5/month ($150/year.) We also have a free Bronze health plan or a great Silver plan with $600/deductible for $184/month ($2,200/year.)

Now subtract the $2,000 Child Tax Credit from the IRS and $500 or so of Foreign Tax Credit from our international stocks, and we effectively have free health insurance and zero tax burden (State + Federal + ACA = $0.)

Total cost of living: ~$70,000.

Summary

Thanks to years of boosting basis in our stock holdings and building our tax free Roth IRA Conversion pipeline, about $250k total, we are able to strategically source spending money without generating significant taxable income. And we still have a year or two before we would possibly return to the US.

This is something any early retiree could implement – retire, travel the world for a year or more, harvest capital gains, convert some Roths… and then return to the US if you so desire. (Alternative option: opt out of the ACA and live in a no-tax State.)

To answer my original question: Would returning to the US have a significant impact in terms of taxes and health insurance?

hmm, I don’t think so.

How is y’alls life in Cali?

—

Pre-emptive Rude Question Rant: “It’s people like you that are the problem with this country, taking these government subsidies when they were supposed to be only for poor people.”

Polite response: This is a false premise. Subsidies were intended for households up to 400% FPL, which is ~60% of all households, because an insurance system with full enrollment means lower costs for all. If Congress wanted to add an asset test, it is easy to implement (See EITC.)

Less polite response: It’s fine to attack me, I already forgot all about it. But instead, maybe you could be a great role model. Please give up your subsides, which are some of the biggest tax breaks for the wealthy (5x the cost of ACA subsidies.) Add to that Medicare and tax deductions on your house and 401k. Deal?

Well, at least you did your homework! Seems like you are in a good position to move back if you wanted to, question is, do you want to? Guess you are not in a rush either, so plenty of time to think about it.

Probably still a year or two before we decide.

Crunch numbers for Roanoke, Va!!! We used to live in California, alot of my family and friends have moved over. We bought a modest, “inexpensive” home near downtown. I can walk or bike to work, our bus system is not extensive but it’s decent and even takes you to nearby Virginia Tech for $4! We have a new Amtrak station that takes you into D.C for cheap.. I could go on a walking tour of all the cool new breweries that are within walking distance to my home. Mountain biking is huge here.. and we are extremely fortunate to live near the beautiful blue ride mountains!! Best of all are little town is diverse!! In recent years we’ve seen a huge influx of immigrants starting over and I love the impact it’s made. Our food scene may not be as good as NYC but boy do we have some cool spots!! Google us, it’s worth the 5 minutes! 😊

Thanks for sharing this good info, Michael. I second that nomination, and also recommend my nearby area of Lynchburg, VA.

I live in Lexington, VA. But miss Minneapolis, which has gotten better over the years. A new 14 mile light rail extension will start construction in the winter, which will extend the blue line that currently ends at the Twin stadium to the southwest suburbs. You won’t need a car, has plenty of bike share kiosks with lots of outdoor amenities. You can roller blade literally around the city.

Sounds nice, but I can’t live anywhere that it snows. (I grew up in Minnesota…)

Nice analysis. Although since you have earned self-employment income it would get radically more complicated. And you could deduct your ACA premiums. I think you might be happier with Corolla all the Midwest Escorts rusted to death a long time ago😀

Corollas are a’ight too.

It’s not much more complicated:

“With blog income equivalent to 2017, I could shelter 98% of it in 401k/IRA/HSA.”

But stay tuned for next week…

What are the tax implications of repatriating mid-year if you take FEIE? Is this something you’ve explored? Also, where in Cali you lookin’? You might want to take a peek at Nevada City (yep, it’s in Cali, not Nevada).

It’s prorated. The FEIE applies up until your entry date.

Just looked at pics of Christmas in Nevada City, and it looks very nice. For a place to live we prefer something about 100x larger.

Wow. Love your math. And California is worth every penny and more. Where exactly are you considering? It’s such a diverse state.

That’s your opinion, of course. Mine is this state sucks the big one, and I can’t wait to get the hell out. Only four weeks until we’re free at las, free at las, thank god almighty, we’re free at las.”

Out with one, in with another :)

Where is the holy land you are headed to?

Solid article! You always introduce some technique that I would not think of on my own. I guess that’s why I read all your articles. Any consideration given to Christian health sharing programs for healthcare or do you not consider them because your faith is not in alignment with them? I remember reading that WhiteCoat Investor runs the numbers each year and compares Christian health sharing to traditional health insurance. I know there are large differences between the two. Just curious since I didn’t see you mention them as an option. Thanks!

What were the techniques that you hadn’t thought of?

The health sharing ministries are interesting… the biggest one (Liberty?) is apparently paying out more than it takes in, so that isn’t sustainable. I’d hate for them to realize that while considering whether to pay my bills or not.

I thought the technique of systematically ratcheting down taxable income through return of basis (which doesn’t count as income) was brilliant. Makes perfect sense but it didn’t occur to me.

Two years ago we (family of 4) switched from Anthem to Medi-Share and saved over a thousand a month in premiums. I’m trying to decide whether to stay with a non-insurance plan like Medi-Share as my wife just had genetic testing and tested pos for Lynch which increases her odds of cancer. That’s why I was interested to know if you’d looked into the health sharing ministries. I think we’ve saved about $30k in just the past two years by leaving Anthem two years ago but increased odds for a future serious health issue gives me pause when deciding whether to continue with a HSM.

I’d be interested in a link to that info re Liberty/Other ministry that is over-paying out. I couldn’t find any information that indicated this with the top sharing ministries. I use Medi-Share (got to love the name), and it appears financially sound based on the last financials I looked at less than a year ago. With the influx of people due to ACA, I could see that shifting though as they expand beyond their traditional conservative Christian demographics.

re: details on sharing financials… I read this on at least 2 of the reviews of one share program or another, but didn’t look as deeply as I do at other financial stuff… I mostly discounted them due to my wicked sinful ways.

I think I googled something like health sharing ministry problems and Liberty won’t pay my bills.

The health sharing ministries appear to be a Ponzi scheme. They don’t have to meet any actuarial standards and there’s little outside oversight. Avoid. You are paying for nothing- better to bare and save your pennies. So many otherwise savvy early retirees get sucked in- I don’t get it.

My understanding is that the health share ministries pay out what they take in, therefore there is no actuarial “standard” that applies. They are NOT insurance. If they have to pay out more than the yearly contributions, they go back to the members for more $$. That’s stated in their docs, anyway. One of Liberty’s problems is that they stupidly cover pre-existing conditions. The other ministries do not.

The real key is to stay healthy, which means eating organic, getting good sleep and exercise, detoxing regularly and staying very far away from MDs. It’s not that hard, we’ve done it all our lives. You will not need doctors. And btw, you don’t need dentists either for the most part, barring accidents. Cavities do NOT have to be filled. They heal themselves and it’s better that way.

How about them there vaccines, Mary?

Thank you, GCC, for being evidence-based.

I’m a fan of math and science. Jr has all of his vaccines.

Yay math, science, and vaccines. Thank you!

You’re joking, right? Vaccines are toxic, part of the big pharma plan to make the population chronically sick. NEVER GET VACCINES.

Staying healthy is important, but I’d be nervous having that be your primary insurance coverage or a condition for the solvency of your insurance carrier. Insurance is supposed to cover the big expected unexpecteds in your life and an insurance company that isn’t able to cover you when push comes to shove isn’t really an insurance company after all. One nice aspect of the ACA is that we are no longer concerned about the old insurance company games to dodge/avoid paying on claims that used to be so common. Maybe the alternative health share ministries are significantly cheaper for a reason?

My wife and I are members of solidarity healthshare with a monthly premium of 299 vs 1440 for 2018. For 2019 the

monthly cost of sharing will be again 299 and with an ACA plan (silver ) being over 2000 / month . The put option cost

is just too much for the ACA plans and there is no way at this time to get under that 400% FPL.

The numbers are wild. I would be tempted to go with the lower cost option and bank the difference just in case.

Aus Couples Health Insurance:

https://www.medibank.com.au/health-insurance/couples/

$500 excess, monthly:

Accident Cover $A129.30 ($USA93.10)

Top Hospital Essentials and Basic Extras $A284.60 ($A 3,415.20 / y)

Ultra Health Cover $A614.00

Bulk billing GP free.

Medicare levy 2% of taxable income > $A42172.

Cool. Don’t come to the ER when you break your leg. Fix it at home. Brilliant. You know, people get sick, and it’s not their fault. Don’t blame sick people for their illnesses. It’s not nice. Nor is it accurate.

You are right on snowcanyon. I work in an ER and everyday I see people who’ve done everything “right” (which changes daily, btw), who have a catastrophic illness or injury through no fault of their own. Broken legs, cancer, heart attacks, etc. Not to mention the whooping cough I now see regularly in the unvaccinated….. We don’t have universal health care, so you need insurance. And if you don’t have insurance, you’ll get care – that the rest of us pay for.

I always though Cali would be bad for early retirees because of the taxes, but it’s really not. I think I pay more in North Carolina with our 5.7% flat tax vs the progressive CA taxes that start out much lower. COL is obviously higher in CA than NC but we would probably save a small chunk of state taxes.

That said, I usually don’t worry about state taxes since they are fairly flat here and don’t come with a bunch of phase out gotchas like the federal tax code (400% FPL cliff for ACA as you noted, for example). We typically spend $1300 on state taxes and it might be several thousand if we harvest some big CGs (like we’ll potentially do this year). Large in dollar terms, but tiny in long term tax planning terms.

Ha, yeah, in MN I pay about $1000 in state income taxes, $0 Fed, for single filer AGI $25K. Qualified dividends and LTCG’s are taxed as ordinary income. If MN would adopt the Fed standard deduction, it would drop my state income taxes to $700.

California taxes are only high for the tech workers and other high income earners. Combined with the generous property tax limits, it can be a pretty good place for long time retirees.

Really curious to know what locations you are considering in California?

Roughly speaking, the coastal areas between Santa Cruz and San Diego, skipping LA and Orange County. Also like Sacramento. We are a couple years away from any real decisions but starting to look closer.

Love the coast, but Sacramento is hot for like 5 months a year and has terrible air quality. Also, floods, but if you are renting less of an issue. Curious what you like about it? Sacramento is up there with Chicago as a place I’d never want to live.

If you want sun and cars, then you get ozone. For a few days each year that equals poor air quality. Those are the days we would probably be in the mountains or somewhere around the globe anyway.

100F in Sacramento is perfect. No humidity, and comfortable.

But the pollution isn’t just just the summer- that’s my point. Sacramento has pretty bad air quality year round (check out airnow.gov). Summer is eight months a year there, and there’s agricultural, car, and, and home heating (including wood-burning) pollution all year round. The Central Valley is one of the most polluted places in the US with some of the worst year-round air quality and sky-high rates of asthma and respiratory illness. It’s why we crossed it off our list.

The coast has nice summers with better air quality. If you like warm, you’ll breathe easier in SD, western LA, or the northern coast. Unlike those areas, Sac has universally poor air quality no matter what area you live in. There’s no coastal breeze to clean the air, and the Delta breeze just locks in the smog.

We live in a sunny area in the west, and picked it specifically for its cleaner air after having lived in an area with climate and air quality similar to Sacramento. It just wasn’t healthy. You only get one set of lungs, after all, and there’s more and more evidence of cardiac and dementia risk factors from air pollution.

I have looked at airnow, etc…

Looking at it from the other side, I looked at a list of the 50 cleanest cities in the US. With one exception, I don’t want to live in any of them.

So then you look at the list of worst places, and Sacramento is high on the list. But only for ozone… and San Diego ranks no better. Particulate matter is fairly low, and has greatly improved over the past decade. The bad ozone days are in peak summer and peak auto hours.

When I pick one of the worst days from the historical data, (Aug 1, 2017) the region scores poorly but the city of Sac is more or less fine.

I also spoke with 3 friends who are Sac residents for the subjective perspective. They all said the air is fine, more or less, except when there are forest fires.

How do you read the data? Thanks!

I like (not love) a couple of those cities. Agreed that subjectively Sac may not seem smoggy, but it is. Airnow seems to list it as pretty smoggy most of the time, but I am admittedly a clean air nut. City of Sac is better than some surrounding areas (like the foothills), but still scores too badly for my personal taste, and there is chronic, moderate to high level ozone in the area. Particulates have improved, but still not great. It’s a valley, after all, and the nicer downtownish areas are ringed by freeways, so the microclimate might be worse.

I think the difference is that in San Diego or LA you can live right near the coast, mitigating much of the air issue. Santa Cruz and the north are cooler and breezier, so less ozone, and you can live right near the beach in a lower smog microclimate, and they seem to me to better more fun places than Sac in every way, but of course that’s personal.

Sac to me has never been a particularly appealing city, aside from COL, so it wouldn’t inspire me to put up with poor air quality. I’m surprised with family in SC that isn’t the clear winner!

Curious what appeals about Sac more than SC, OC, Capitola, Soquel, or the coast in general? We have family there so I’m always trying to like it and failing :)

I can’t be snowboarding in less than 2 hours from the coast, and while family is nice… you can have too much of a good thing. And rent in Santa Cruz is 2x+ over Sac.

I wouldn’t say Sacramento has any one thing that is overwhelmingly amazing, but its parts add up to something quite nice. And I guess I question the idea of putting up with poor air quality for the times of year we would be there.

Global measured air quality: https://aqicn.org/map/world/#@g/4.0392/8.6133/2z

Shocked by air pollution in central valley 2016. Surprised by bands of pollution when ascending Sierra Nevada 1981. Disappointed by obvious blue haze through much of US. Definitely a factor influencing perceived quality of life.

I think that area is a winner! Having lived there a long time I’d say the one negative of anywhere between Santa Cruz and Santa Barbara area is lack of a bigger airport. In that way Santa Cruz is the winner, only 45 minutes or less to San Jose airport. If you aren’t flying that often it is not a big deal to take a shuttle a few hours though. But it might get annoying if you fly several times a year and have to go four hours from San Luis Obispo to LAX or something.

I didn’t have a car when I lived there and it was totally easy to get around by bike or on foot. If you get an electric bike it even makes the hills a non issue too 😁

I guess the one other quandary is the school systems. That seems to be a big issue for parents when considering housing locations in the USA.

Ventura/Ojai is heavenly. Ojai has a better school district. Rent is high though for the priviledge. To be honest, I was much more in FIRE until I moved here. Now, I really don’t care as much because my travel bug softened considerably and we never want to leave. SLO is sweet but probably small for you. Super far from airports. From Ventura , LAX or Burbank are fairly close, although Santa Barbara is my favorite airport in the world. Easy. Small, and with flights that connect to major hubs. Happy home finding!

It is nice to have a major International airport nearby. I’ve flown into the Santa Barbara airport, and it is great. I’m also a big fan of the Bob Hope airport in LA… easy in easy out.

Great areas. Wife and I are settled a couple blocks from the beach in Huntington Beach, renting a small 2-bedroom apartment. I couldn’t imagine it much better. One area I’ve also been interested in is the San Luis Obispo area. Beach, good art, yearly classical music festival, excellent food, and an outdoor active community. Really fits what we like.

Most of my OC experiences involve huge traffic jams and strip malls. We also aren’t big beach people, although it is nice from time to time.

Did I miss the good parts?

If you aren’t beach people then I could see this being a hard pass. We hardly drive anywhere so avoid any traffic issues. The overall vibe here is similar to areas of San Diego county which I also like a lot. The weather is about 5-10 degrees cooler than even a few miles inland year round, which is a big deal for me.

Maybe I would have to pickup surfing…

Great idea! Strangely I don’t surf yet, still need an acl surgery. Meh, gotta do that soon, missing snowboarding. Well if you’re ever in the area, feel free to hit me up — happy to show you around town.

Top 2 places I’d recommend- San Luis Obispo (and areas around) and Encinitas / Carlsbad (North San Diego)

Funny, these two specific areas are at the top of my list too. Amazing areas.

Brilliant!

What about long term? Eventually you’d run out of Roth and stock sales that are 100% cost basis.

Excellent observation, sir. Check back next week when I explore this in depth :)

Have you looked at Dallas? I know you mentioned Austin; they’re similar demographics. Cost of living is quite manageable and no state income tax. Property taxes are a bear, but as renters for life, that’s a pass-through expense. Balancing walk/bike friendly and good schools might be a little trickier (Highland Park maybe?), but there are surprisingly good public transportation and farmers’ markets here. We live in Uptown, and aside from my 1 mile/day commute to my WeWork office, we rarely drive anywhere. Our projected retirement CoL is roughly what you’ve outlined.

You drive 1 mile?! ;)

All of my Texas experience is with work travel, which may have tainted my Dallas memories a bit.

I KNEW you’d give me crap about that. It’s a time trade off. 30 minutes for free trolley or 7 minutes for the drive. Time > $.

Or 4 minutes to bike. Or 15 minutes to walk.

Where are you thinking about in CA? I really love the South Central coast region. San Louis Obispo, Santa Barbara, and around there. The COL is very high from what I understand. In reality, we probably will have to move to the Palm Spring area at some point. Mrs. RB40’s parents are there and they will need help when they’re older. Palm Spring is expensive, but the COL is quite cheap if you go out a bit. I believe there are lots of retirees in the cheaper San Jacinto valley area. Not too exciting lifestyle, though…

Interesting to see that taxes aren’t that bad. We’ll have to take a closer look at it.

I live near SLO (Pismo Beach area). COL is only high in regards to home-ownership (home price, prop tax, etc). If you are a renter, that can be avoided as GCC mentioned in his analysis. The weather here is so mild our utilities are virtually nil. Never run the AC, almost never run the gas heat. Electricity bills around $50/month, gas $25/mo for a 2100 sq/ft house, year ’round. Little in the way of “nightlife” entertainment options, but if you are into outdoor activities(golf for us) this is the place to be. If you need big city life occasionally – LA and SF are 4 hours away in either direction. I was originally planning on moving out to a zero tax state (NV) when it is time to pack it in at work, but my number crunching has come up with about the same results as GCC, likely to stay since the house is paid off.

Good idea about renting. I’ll need to check the price out. Maybe we could live in the area for a few years to see how it goes. We went to college at UCSB. It was great and I’d love to live in the area again.

It is still wide open.

I was largely looking at mediterranean climate zones around the globe. My Mom and sister are in Santa Cruz… I was checking out coastal towns south of there all the way to the border, skipping LA and Orange County. I used to spend a bit of time in Long Beach. Some of the housing and insurance prices in this post are from Sacramento. We spent a few days there this summer and really liked it.

Foothill areas around Sacramento are really nice. Auburn, Amador County, etc. Nicer summer climate and out of the main city, but really close to Sacramento. Easy access to the Sacramento Intl Airport.

I second San Luis Obispo County. House prices, and thus rent, are high in San Luis Obispo (SLO), but the surrounding cities have much more reasonable prices. 20 minutes to the beach, 4 hour drive to China Peak for skiing. Excellent weather all year round. Bikeablility for SLO is rated at “gold level” by the league of american bicyclists. Surrounding cities aren’t nearly as bike friendly. SLO has a FANTASTIC farmer’s market, and there are farmer’s markets in the surrounding cities as well. I am a SLO native, feel free to email me if you have any questions about the area.

Thanks Drew! I’ll take a closer look at it.

I have only had one experience with SLO, when I randomly popped into a drive-in movie theater when I was heading from Seattle to LA via Highway 1. (I can’t remember what the movie was.)

Josh Kennon recently moved to Huntington Beach from Missouri and loves it. He put days and days of quantitative analysis into the decision and considered all U.S. cities that made sense. You can Google Josh Kennon blog to find it. Fascinating guy and blog he has put together. All of his writings are great.

I just did a quick search and didn’t find his analysis. Do you have a link?

Perhaps it’s this one? https://www.joshuakennon.com/its-official-we-are-moving-to-newport-beach-california/

Right you are. Thanks!

Interesting that were it not for some specific legal challenges they would have moved to Seattle.

Being a California native, I have a special place in my heart for this state. And there are plenty of FIRE people here making it work. It is expensive, but when its 80 degrees in November and you’re at the beach, you can’t beat that.

Very interesting proposition! Numbers don’t look too bad either, I’d be curious what cities you are thinking. CT is a higher cost of living, but we still managed to FIRE here and found ways to keep our COL low while still taking advantage of the area.

Love visiting CA. I just keep telling myself the traffic and cost of living isn’t worth it, because all that sunshine is tempting ;)

If we end up in Cali you are always welcome to visit. We would look for a place with limited traffic :)

About 45 deg and rainy here, we need to fly out to LA :) But it was sunny, and prime leaf peeping season in the Northeast this last weekend. So we have that..

This is why we left Seattle :( If there is a bad time of year in our forever home, it needs to be summer when school is out so we can go somewhere else.

I didn’t know Cali taxed all income the same…is that why they tax my HSA? I live in expensive San Diego and have given living in Tijuana somewhat serious thought, but commute would be horrendous and I want to bring my disabled parent and brother with me and they only get Medicare if they live in US. They live in the cheap rural desert, far away from my job with a sweet pension. East of SD, Imperial County is also cheap. I have wondered about Nevada, Arizona and Oregon once I can retire, but still stuck on the nomadic van life…Class C for a fam?

We moved from Seattle to San Diego several years ago and everyone told us how expensive it was going to be. Turns out, we spent less in San Diego and were way happier. I can confirm that food is MUCH less expensive in California. I remember paying $2 for a single bell pepper in Seattle, in California, you can get six bell peppers for that price. Entertainment is also free, or at least cheap, and plentiful. Nowhere is perfect though, which is why we travel :).

It’s great to see you analyzing ACA and states with income taxes! Are you using CA standard deduction? Some states haven’t adopted the new Federal standard deduction amounts.

I just used an online tax calculator for CA taxes. I think it used CA standard deduction of $9k or around there. Precision isn’t too terribly important at this point as long as in the right ball park. If they adapt Federal standard deduction that will save a bit more.

GCC,

Can you help me understand the Taiwan medical system/plan? As context, I’m a US citizen but was born in Taiwan along with my spouse. I’ve been considering getting Taiwan citizenship for my two boys (7 & 4) along with paying any back medical premiums for me and my spouse so that we can have Taiwan healthcare as an alternative healthcare for when me and my spouse are older (post retirement)

I’m not an expert. If you are a resident you can enroll in the health system after 6 months. I’m not sure how it works for citizens away from the country for extended periods.

My wife and I live in San Diego too. It isn’t the cheapest place around, but we don’t want to move into the desert in order to get costs way down. Not a good trade-off IMHO. My brother’s family lives in San Luis Obispo. Cost of living is roughly the same between the two places. We’ve been on a bronze HSA for years and have been happy with it. Costs weren’t very high either until this upcoming year when they go up 30+%. We knew it was coming ever since the Kaiser Family Foundation came out with their report early this year that the White House cutting the CSR reimbursements would result in significant rate increases, but I must say it was still a shock. Love that you have a way to get the subsidized pricing! We are lining up our *hopefully soon* early retirement and will be under the limits then too, but for the time being are in the not too bad position of making enough money to not get subsidies. Wherever you move to in California, I have no doubt that you’ll love it. It is an amazing state!

I’m sure you can find an even cheaper place. Charlotte North Carolina is where my in laws retired. Raising kids, well that can be done without settling.

There are definitely cheaper places, but cost isn’t our primary concern. I can’t deal with the humidity – I once had a job interview in RTP and rejected the offer before I even got off the plane. It was crazy humid in March already.

If cost isn’t a concern, Santa Barbara, Capitola, Soquel, San Diego, and I actually like Orange County. Great weather in all of them, minimal smog, minimal humidity, yummy food. Way more fun than Sacramento, and more culture, wine, fresh air etc. The icky month (if there is one) is June, and that’s easy to go away!

Sacramento does not compare IMHO.

Cost isn’t a “primary” concern, but I also am not going to pay $6k/month for a 3 bedroom house the size of a shoe box.

I loathe OC… so different lens. Traffic blows and hanging at the beach isn’t fun for more than a couple days per year.

Sacramento is probably a decent compromise, then, and the COL is low. I see your point about the OC and it’s further from the mountains.

My guess is you won’t really be aware of the smog is mostly invisible ozone. My view has always been that you can control your diet, your exercise, your lifestyle and even your water quality, but that air is a community resource so it’s always been a huge priority, and as I said, I’m a clean air freak. You can’t have everything, though.

Sacramento to me is a large, hot, smoggy, generally unwalkable, highly congested (just as bad as the OC IMHO) uncultured city which is two hours from where I’d rather be (I’d rather live at the beach, in the mountains, or in a more city city like SF), but we have relatives who love it and are really happy there. I totally get the insane COL in Santa Cruz, but I’d rather work a few days a month and live in Santa Cruz, Soquel, Santa Barbara, Pacific Heights, west LA, Oakland etc than work no days a month and live in Sacramento. But it sounds like it might work for you.

I think I have figured out my favorite part about Sacramento… if you tell anybody that you are considering moving there, (literally) everyone says, “WTF! That is a terrible idea!” Except the locals.

I think schools might be a problem though. There are fantastic schools in the burbs, but the city center less so.

Because I’m “Down With GCC” ( who isn’t?! )…I give you my two cents. I moved to Las Vegas @ 8 years ago and find it mostly enjoyable in particular the “tax treatment”. Now…the summer’s are extremely hot & dry…and may wreak havoc on Jeremy’s light skin tone and insistence on wearing jean shorts as an early retirement wardrobe staple.

I could go elsewhere for summer. Most of my LV experiences are through heavy inebriation and the cover of night, so I’m skeptical ;)

Vegas is underrated- it’s not all the strip!

There’s great hiking right there (not obligatory 2 hour drive), a good food scene, decent air quality, and Summerlin and Henderson are nice areas and there’s very little traffic. Zion NP is close and the coast is a few hours drive. I know you are renters for life, but RE is very cheap there. Good airport with direct flights everywhere and you can’t beat the income tax, either. There’s some skiing nearby, but you’d have to hop over to Utah or Tahoe for better slopes, but it’s a short flight and a moderate drive.

The negatives include a historically lacking school system, and the medical system has historically been poor but these are both getting much better with more investment in the schools and a new medical center and medical school. And, it’s not Cali! I’d say it gives Sac a run for its money and is way cheaper if COL is a concern. Many Bay Area and LA transplants.

Hi from San Jose! While we still both commute to work, it’s not too bad at ~30 minutes. We did find a great place to buy with lots of things within walking distance. A couple weeks ago we walked to the library and got Black Panther and Princess Mononoke on Blu-ray. There are two small grocers a few blocks away and some good restaurants. Also a small farmers market on Sundays. There’s a parkway along the river a little less than 0.5 miles down the road where we like to take the dog. We’re about 1.5 miles from the downtown core and 3 blocks from a good transit hub.

We have 7 fruit trees (avocado, peach, fig, lemon, pear, persimmon, pomegranate) and two fruiting vines (passion fruit, grapes) that mostly fruit at different times of the year. The avocados are almost ready! Our neighbors on both sides have chickens, which we trade fruit for eggs. There was a small time where one of them had a couple bee hives and we got (very) local honey.

There are some downsides of course. High cost of housing, income disparity, homelessness (due to the previous two points), property crime. I have hope those issues are fixable.

A good friend has also built a nice oasis in San Jose in the foothills. We eat well when we visit.

One option for healthcare. If you want to completely avoid the Subsidy Cliff issues and you spend some time outside of the US is Global Individual insurance from CIGNA. It offered up to six months of family coverage in the US and global coverage for the other six months. It was less than half of the cost of healthcare through the ACA website, even with subsidies at the 400% level ! It’s cheap enough that you could supplement it with a health share policy, like Liberty health share. The two combined would still be less than some of the rates you mentioned and may be good for a transition year, or if you still plan to travel a good bit. It’s worth checking out for anyone who spends some time out of the country, you don’t even need a visa or foreign residency.

Thanks! I looked at them as an option when we first left the US, I’ll have to look at it again.

Recent transplant to CA here (and in the bay area chasing tech $$$ so maybe not your exact target audience :-P). We came from the East Coast. It’s hard to believe this weather is real, and this area is far more family friendly than where we came from. And the farmer’s market/food situation is pretty amazing. Since we came from a fairly hcol area, the change is not dramatic to us besides housing. Housing will prevent this from being a permanent move for us which in some ways is definitely a little sad, and I guess speaks to our enjoyment out here :).

Like everyone else, wondering what your California short list is.

Going to vote tomorrow to keep ACA – our top FIRE issue. Hoping to lure GCC back in the states for more applicable tax hacks.

We engineer our income to 139% FPL to work the opposite side of the ACA cliff – that is, falling into medicaid (IL is an expansion state). We played the medicaid game for a year, just for fun. Saved nice money, but suffered the uncertainty of coverage the first 6 months while the paperwork was shuffled/reviewed/accepted. Then, when the coverage/benefits proved to be real – it felt a bit skeezy to utilize…

So now we skirt the minimum income for max ACA subsidies and CSR. And in metro IL this year – same silver PPO plan as last year – our premium is down 25%. Lucky bonus, thanks actuaries. We actually need to generate some MAGI this year, so we are converting TIRA to Roth to make up the balance.

BTW, the only $10k Escort you’ll find here is in the Ford museum.

What was the skeezy factor? That you were using a low-income benefit? Or something else?

I’m a proponent for single payer healthcare (and, conceptually, universal basic income). But until we get there, I kinda felt like we were taking something away from someone that could really need/use it.

There were other operational difficulties that shaded our medicaid experiment. They track income monthly, and you are “supposed” to notify them with changes, possibly ping-ponging in/out of compliance throughout the year. Being “self-unemployed” with residual work, my income/expenses fluctuate all the time. I simply reconcile at year end (and shelter excessive income into an individual roth 401k). That was how I “pitched’ my income number for the application, and my plan for the year.

Until I made an imprudent move into bonds (panicky wife) that yielded more income than I could offset/shelter. Reconciling too late, our year ended up about $900 over 138% FPL. I was worried about clawbacks/penalties/claims of “cheating”/re-applying – jeopardizing the whole experiment.

In sum, we decided it was too stressful/restrictive to maintain ultra low-income year-to-year just for cheap healthcare. The uncertainty of consistent coverage (initial application 6-8mo lag, month to month, year to year), limited doctor network, perceived social stigma – all changed our perspective. The game is now “clear the bar”, with much less disruption/penalty/stress for “achieving a bit too much”.

Thanks for explaining. The administrative hassles sound terrible.

Curious to see where you might move to in CA. In my experience (which is mainly limited to larger CA cities) everything does tend to be more expensive. Not absurdly so, but just enough that I notice. $5 here or there for everything.

It all adds up I guess.

Canberra comparison: all in cost of living ex international holidays & external entertainment; accounted cost of owned ‘single family’ home, (4 bed, 200 m^2, 900 m^2 block + rates + 4×4 vehicle + health insurance + home entertainment) = $A32,000 (~= $USA 23,000). City household incomes: median ~$A 110,000, average ~$A 130,000. Separate bicycle / foot path network. ‘Farmers markets’ not significantly different to supermarkets. Direct flights to Singapore & Doha.

I’ve heard great things about Canberra and Melbourne.

We’re on the verge of FIRE’ing next year and live in the Bay Area. Our plan is extremely similar to your proposed scenario. We’re a family of three (adults are 43 and one 4 year old child.) One thing I’d point out is that we’re going to ensure that we manufacture enough income to push our MAGI above the threshold required to keep the child off of Medi-Cal (for a family of 3 in 2019, this is >$55,275.) In my research, the options for physicians who accept Medi-Cal are greatly reduced. And the quality of those practices is a bit of an unknown. Avoiding Medi-Cal means we all can continue seeing our established physicians.

Medi-Cal is way better for kids than private insurance. Medicaid pays for EVERYTHING.

I enjoyed this write up. I’m in a similar situation looking for “the place”. There hasn’t been a perfect answer and there are trade offs everywhere. Want low cost of living? The southeast is cheap for a reason. Want incredible climates or to live by the water? It’s more expensive.

It may not be my first destination, but I understand the appeal of California. Water, perfect weather, and have friends who can wake up at the beach and be snow skiing in the afternoon. That’s incredible

The place is elusive, but it probably has a mediterranean climate.

I think that in another year or two, maybe look at the cost of living again, along with the other financials that are going on. Things-are-a-changing in the USA, so you never know what to expect as far as new taxes/fees on capital gains/insurance costs, etc.

Keeping track of your money in/out and what’s going on in every state will help guide you.

Buy a tesla 3 when they sell the base model for $35k next year instead of a used gas car. Then you will drive more ofrtn and save thousands a year in gas and help improve poll.

I don’t want to drive more often. Why pay $35k for a car when I can spend less than $10k?

Regarding cost of living, Oklahoma is a great place. Despite its reputation of the dust bowl mid west, it actually has a lot to offer. Dirt cheap housing costs and low taxes. We also have some great farmers markets and co-ops. Just make sure to dodge those tornadoes!

Definitely not the result I expected when I read the title….Most people flea California when FIREing or regular retirement.

How did you go about raising your basis in your stock holdings?

Cap gain harvesting raises basis.

Thanks for teaching me this. My wife and I are taking advantage of our lower tax bracket with this. This is probably the most powerful tool I’ve leaned in the FI community besides the Roth conversion.

Enjoy! :)

Awesome! Put Davis on the map for your consideration (our hometown and where we live now). It has one of the best public school systems in the country (K-12) and a great green belt for cycling/walking, and is really close to Sacramento.

Why are Davis property taxes, and values, high?

Because of UC Davis, a top 10 public university in the tiny city of Davis. That’s the same reason why the k-12 public schools are so good, you get a disproportionate amount of faculty and staff children affiliated with the university.

Btw – to Justin I forgot to mention I’ve also lived a few years each in Santa Cruz and San Diego, both awesome cities. I love exploring the little towns that surround SC too like Bonny Doon, Felton or Capitola. I would choose SC if I were childless but with kids it would be a tough choice bc it would have to depend heavily on the school district for me.

Hints that land is ‘corralled’, government pensions ‘padded’:

https://www.businessinsider.com.au/philip-greenspun-davis-california-2011-5?r=US&IR=T

Hmmm I wonder if anyone has figured this out for Canadians repatriating?

We moved from San Jose to Monterey early this year. So far surprisingly cheap. Wife and I rent a 2 beds 2 baths condo for $2k, central to everything. Bike around town and the beach everyday. Our foods expense is surprisingly low; fresh vegetables at Marina farmer market are cheap; fruits and vegetables at Moss Landing stalls are super cheap all year round. The anchovies and sardines at the Fisherman Wharf are cheap and fresh. We ate well for $300- $400 a month, including trips to Costco twice a month. The negatives: water is very expensive. $150 a month, with a base cost of $100 a month even if we don’t use a single drop. Summer is cold and foggy. Falls and Winter days are great. Healthcare is not so good here. We still keep our San Jose doctors. We initially planned to live here short term until FIRE and move elsewhere. The plan may change.

Another thing to consider with health insurance is which, if any, hospital systems take the ACA. We live in NYC, and we pay over $1k more per month in coverage instead of opting for the ACA b/c all the major hospital systems in NYC don’t take the insurance plans available on the exchanges. For this reason, as soon as we can change our full-time living status we will look at other states that don’t have this issue, and of course, Costa Rica has excellent and accessible healthcare. We’ll keep a base in NYC b/c we love it here, but it doesn’t have to be a primary residence.

Can you tell me more? Not a single one is accepted by Columbia, NYU, Sinai, or Montefiore? Not one? I’d heard rumblings, but hoped things weren’t that bad.

I watched in horror this year as the Trump administration tried to destroy Obamacare and it was just so awful to watch and think about. It’s nice seeing that it has been resilient and that you can still get good coverage even if you’re retired/have pre-existing conditions and I’m hoping it’s here to stay.

I always love your case studies because it’s about living a great life but still being able to be retired. 400% fpl actually isn’t too low, even for a single person, if like me, you’ve only got the total stock market as dividend income. It’s kind of nice that it’s such a cliff because, even if I don’t minimize my income, I could still get good subsidies, even if I hang right at the edge of the subsidy cliff.

On an unrelated note: one thing that stuck out to me in one of your previous posts was that you can neglect your finances a while and still come back back you can’t do that as long for your health. For someone like myself that is in a challenging but high paying job and saving well for early retirement or financial independence, what’s the first steps or recommendations you have for improving health. Mainly, I don’t want to decline and cause irreparable damage.

Thanks again for your wonderful posts. You don’t know how inspiring and helpful they can be.

Avoid addictions and sedation. The rest is up to fate. (I’m clearly not a health expert.)

Sorry to ruin the excitement but if I was you I won’t do it.

CA is one of the most expensive place on this planet…until it will become iper-expensive if you will need some serious medical care ( it’s in the USA…)

Why not staying in Taiwan few more years (anyhow your baby is still young so no need of College yet) or moving to better places like South of Spain, France, Portugal (do you know you can move in Portugal and get permanent EU card and citizenship after few years…)

Why not Costa RIca, or Mexico where you can live with a fraction of money and few hours away from USA?

To be fair, 99% of the world would make different life choices than we do.

I like American culture.

I like American culture.

You answer my question in one short sentence…:-)

Congratulations again for your blog, family and life!

I like the places you mention also, but not sure if we would make one of them a permanent home base.

edit: (adding this later) if you live in Spain, France, etc… you have to pay tax in those countries. Many of them have a wealth tax in addition to a steep progressive tax system. This can make these places far more expensive than California.

I moved from California to Colorado this year. There were a variety of reasons, but two big ones were the personal income tax rate and the cost of living. San Francisco was INSANE for the quality of life there. Anyway, I posted this yesterday (seemed timely) and I thought you might find it useful. Enjoy! https://thesterlingreport.com/best-places-for-americans-to-move/

By my math we would pay more tax in Colorado than California.

I wouldn’t live in SF either.

I have a ‘soft spot’ for the 4 corners area region. Where is Santa Fe on the GCC home index?

I haven’t been there so I’m not really sure. I just looked at some pictures and it looks nice. I assumed it was super hot like Phoenix but actually looks pretty comfortable.

Milder summer due to altitude. If the climate does not suit on the day, change altitude. Grand vistas and myriad hidden canyons. Rich history. A seemingly comfortable blend of American, Spanish, Mexican and USAn cultures.

Hi GCC!!! I’ve been a big fan for a couple years… I just have one word for you: SACRAMENTO! It’s close to the mountains, close to the ocean/Bay Area, it’s cheap, it has bike trails, close to Yosemite, Amtrak, an International Airport. And, it is about 100x bigger than Nevada City :-) (but close enough to visit for a day)

What is your perspective on the air quality discussion?

GCC, was eventually leaving Taiwan always part of your plan, or is there a Taiwan-centric reason(s) that you’re considering moving elsewhere? (I ask b/c I’m considering moving there)

Also, you mentioned in a reply to Nita that you wouldn’t choose to live in NC b/c of the humidity there. How have you been managing then with the considerably much higher humidity in Taipei?

I haven’t been managing. Humidity is terrible and I have to leave for the summer

Question- rents in Sacramento and environs have been on a tear for the past decade as the area receives more and more Bay Area transplants. I don’t believe there is any rent control. What happens if rents go up to $4k a month, or even higher?

I’d pay more?

Rent history in Sac is pretty interesting – basically flat for past decade. Trendy areas, notwithstanding.

1.9 [yr] Breakeven horizon [number of years after which buying is more financially advantageous than renting]

https://www.zillow.com/sacramento-ca/home-values/

Try before buy is best when uncertain.

Zillow has improved their methodology from the early days.

I enjoy life as a renter.

Aren’t the trendy areas also the walkable ones? Land Park etc? Are there non-trendy walkable areas?

Sacramento’s AQI today is 169. And it’s not summer. Or wood-burn winter. It happens here, too, but for a month a year, not months on end.

Isn’t all of California on fire at the moment? Biggest wood-burn in history…

We would likely live in the trendy areas, school quality permitting, which is why I budgeted more $ than the avg. That the avg and median haven’t budged in a decade is a good indicator of ability to absorb more inhabitants. Lots of construction going on too.

Yup. And more to come. It’s all enfuego all year round now. I guess eventually the trees will be gone and scrub-savannah just doesn’t provide as much fuel.

Agreed Sacramento seems willing to build, which will hopefully keep prices moderate, and the ensuing traffic nightmare won’t be yours if you live in walkable, central areas. I know you are RFL, but does Sac allow, and would you potentially be interested in, a house with MIL quarters or a duplex? Would provide tax benefits, another income stream, and diversification.

Good point on the sunscreen. That stuff is not cheap!

I haven’t done any math on Sac rentals.

Well, you could get a sunbrella and nix the sunscreen (which is definitely not cheap).

It’s not our current situation, but there’s nothing more satisfying than having someone else pay off your mortgage (or most of it) while living for free. Works best with a duplex in an urban area, and the numbers have to work, but when it does it’s extremely satisfying and remunerative, and my guess is you would be doing a happy dance over the tax bennies.

It’s hard to find the right property and place to do this, and American zoning makes it hard, but when it works it’s sweet.

Snow isn’t too bad: ) At least it isn’t here in Michigan. The only thing that I don’t like about snow is driving in it. We were out in California 2 summers ago and it is really nice. One of our favorite places was the the Redwoods National Park area in Northern California along the coast. Hardly anyone was there and we didn’t even get cell phone reception. Kind of cool! Good luck with your decision!

Hi! Long time reader/lurker, California native. As I was reading this post I had a gut feeling Sacramento was on your list and your bit about finding a flat of figs for $3 made me scroll through the comments to confirm.

I really wanted to share my two cents:

– If you can survive Taipei in the summer, summer in Sacramento will be a piece of cake.

– You really really get the biggest bang for you buck here. Eight years ago, I moved from San Diego to Sacramento with my sole criteria being a metropolitan area with a lower cost of living.

– I’ve enjoyed frequent trips to Tahoe, exploring the Shasta Cascade and Mendocino Coast, and the many many places within a two hour drive to stand in awe of the redwoods. Oh and wine, so many wine regions a hop and skip away.

Please continue to share your breakdown as you plan your move, I find so much encouragement in reading numbers from California residents. Wishing you and your family the best!

Sounds very nice :)

What do you think of our target budget?

How is the air quality?

If you don’t mind sharing, what neighborhood do you live in? How car dependent are you?

Thanks!

Your target budget sounds reasonable, I think the state of healthcare will be your wildcard. As far as your expectations on rent, it is pretty spot on but variable due to neighborhood.

Rents have been steadily rising. To give you an idea, I started renting my 3 bed/2.5 bath townhouse in 2014 and rent is $1300. Market rate for the same property will probably run you closer to $1800 now, so still fairly reasonable.

I am out in East College Greens, closer to Sac State. I am within walking distance to a park, elementary school, a lightrail station (though it is not the most safe/comfortable station) and the bike trail. Due to the lightrail station, I could get away with not having to drive to work, however, I would still be car dependent for running basic errands.

Coming from San Diego, the air quality is a little subpar and spring allergies obliterate me every year. But it’s definitely really easy to head out to the foothills or even Tahoe for a breath of fresh air every now and then!

Jeremy, little sad you’re “hating” the Bay Area…when you factor in everything (weather, people, jobs, things to do, etc) I still say it’s the best place in the world. Plenty of decent areas that are affordable with great weather year round (Pacifica along the coast, San Carlos in the peninsula, and Santa Clara in the South Bay). All within 15-20 minutes of major downtowns (SF, SJ).

Sacramento really can’t compare to the Bay Area other than being a lil bit cheaper…honestly what is it about Sacramento that is better than the Bay Area??

BG

Agreed that the Bay Area has much more to offer and much better schools, although I’d say it’s a lot more expensive, not just a bit.

I’m not hatin’. My favorite color is just different than yours.

I don’t want jobs or people, but would like it if the people who have jobs making median income can thrive as my neighbors.

Median income in Bay Area is almost $97,000 (quick google search – SF Gate source). Any married couple or college buddies earning that could afford to rent in a LOT of places in the Bay Area. Sure maybe they wouldn’t want to buy right now! But that seems to shoot down the argument against the Bay Area over Sac.

And I’m not really hating on Sac compared to tons of other places…and to be fair there are some drawbacks to the Bay of course, but neighbors not being able to thrive…not buying it…people should rent remember?!?

and you say you ain’t hating but these are your words “but this is primarily in cities where we would hate to live. (Hey Bay Area, what’s up?)” …seems like a lil hate to me : )

you guys are still welcome to come hang out anytime

I also dislike the color orange, but am glad to hear that you like it :)

A google search of bay area commute times for teachers is a good metric (90+ minutes 1-way, teachers moving away each year unless married to google employee, etc…)

Jeremy, you’re killing me here. Of course average people will commute 90 mins + each way but that’s not you or smart readers of this blog. There are areas in the bay area that ARE affordable where you don’t need to commute 90 min….these are the people that WANT a 4 br house and backyard..one could find a small 2br townhouse or duplex and rent and still be affordable and live within 15 min of work. And avg teachers salary for SF is $71K…not bad for 9 mos. work and definitely possible to find places to live and not commute 90mins. Add a roommate or spouse and now you can really start saving $

And yes I do like the color orange and if u don’t like it here that’s cool, but it’s not because some teachers don’t know how to house hack.

>if u don’t like it here that’s cool

agreed

If “house hacking” is mandatory, it is no longer a hack.

When i read you were moving to CA, I thought you guys were crazy. It is just too damn expensive! However I am in the Los Angeles area, so my perspective is skewed.

The only thing i know about ACA amd subsidies is that the paper work can be a headach and confusing, especially if you have variable income. A friend was subsidized for 4 years and now they are saying she did not qualify and taking money back.

On a somewhat related note, my family receives state benefits due to my child’s serious health issues.. When people complain about taxes, I understand. Not all money is being used well, but i want people to know there are families that really, really need and appreciate the assistance!

I lIve in So Cal-I wouldn’t trade it for anything…20 minutes to JWA and the beach. Perfect weather :)

I think the Manhattan price/rent ratio of 50 must be skewed by all the absurdly priced new luxury apartments. I own a condo in the village that would sell for around $900k which I recently rented out for a year for $3650/month. Not a great return if it were an investment property, but that’s a much lower ratio of 21 which is more reasonable for a primary residence. Am I missing something?