(GCC: Taxes and college tuition are 2 of the greatest expenses parents will face. But what if there was a tax hack that could reduce the cost of both? Today’s guest post shares the details… Read on!)

Hi Go Curry Cracker readers! I’m Kim from The Frugal Engineers. We are a family of three retiring in our thirties in Wyoming, and I’m here to talk tax hacking for college!

Over the last nine years of running our own engineering businesses, we’ve been tracking various tax optimization strategies. One of our favorite tax hacks is using our health savings account for college funds. By lowering our tax burden and maximizing our eligibility for college financial aid, we’re able to retire earlier and enjoy more time with our daughter. This post details part of our overall strategy for college planning in early retirement.

We max out our health savings account (HSA) each year that we’re eligible based on our health insurance. For a family of three in 2019 with a qualifying high deductible health insurance plan, that’s $7,000 a year. We pay cash for any medical, dental and vision expenses that we incur right now and save the receipts for reimbursement during the college years.

In fact, I refer to medical receipts as “future college tuition vouchers” in our house.

Enjoying early retirement

The Flexibility of Using an HSA for College Savings

My husband I both attended top colleges for engineering, and each school also has their own formula for calculating financial aid. Based on our research, this is an area where early retiring families can really shine with enough planning in advance.

By making plans a decade ahead of time, we’re able to maneuver our finances in a way that’s favorable for financial aid calculations.

A downside to traditional college savings plans is the penalty on using the funds if your child doesn’t go to college. Our daughter might choose to be an entrepreneur, a homemaker, enlist in the military, or any number of paths outside of college. By locking those dollars up in a 529 college savings account, we’d be looking at a 10% penalty to withdraw money for non-college expenses.

(GCC: And, you convert low/zero taxed long-term capital gains into highly taxed ordinary income! See why GCC Jr doesn’t have a 529.)

By earmarking our daughter’s college money in the HSA, it’s tax-deductible, able to grow tax-free, and able to be withdrawn tax-free at any time (as a reimbursement for previously incurred medical expenses).

Future College Graduate

How the HSA Wins the FAFSA Game

We just outlined how the HSA is triple tax-advantaged, but did you know it’s also double FAFSA-blind?

The Federal Application for Student Aid (FAFSA) is the application used to determine financial aid eligibility for college students. Based on your income, assets, and other factors, the calculations produce your Expected Family Contribution (EFC). This number is then used to determine how much “need” you have, which schools use to award aid. The EFC is also the number used to award federal grant money like Pell Grants.

By keeping college savings dollars in the HSA, you are not penalized for saving money in the eyes of the financial aid calculations.

The tricky thing about the FAFSA is that it looks at certain buckets of money differently. For example, home equity is not included as an asset in the calculations. This was another reason why we chose to pay off our mortgage early (in 2.5 years!) rather than investing the extra money in a taxable brokerage account.

(GCC: A clear example of when imputed rent is super to rent.)

The HSA dominates these calculations based on two notable rules:

- Health Savings Accounts are counted as “retirement” assets, which are excluded from the parental asset calculations.

- Withdrawals from HSAs to reimburse previously incurred medical expenses are not included as income on the FAFSA.

This means the HSA is double FAFSA-blind.

It’s worth pointing out that withdrawals from a Roth IRA are counted as income. Additionally, the assets inside a 529 plan are counted in the FAFSA calculations, while assets in IRAs (and other retirement accounts) are not.

Example of the HSA vs. 529 Impact on Financial Aid

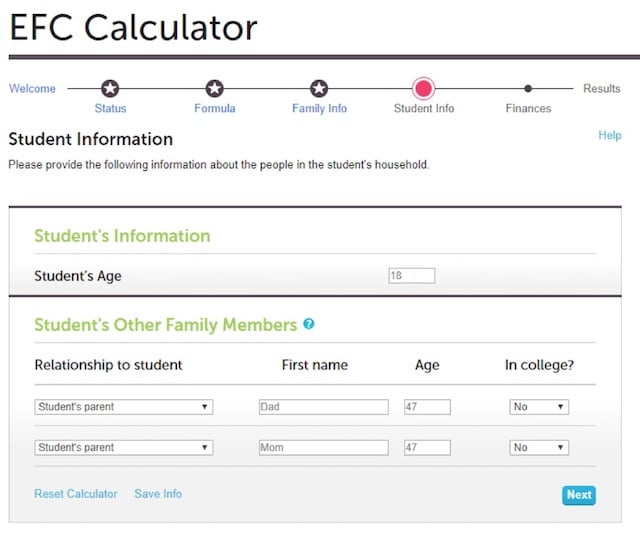

Let’s run an example of an early retired family applying for federal financial aid. Our fictional FIRE family has one child, a paid-off home, and $1,000,000 in investments. This is broken out as $800,000 in tax-advantaged accounts like 401Ks and IRAs and $200,000 in an after-tax brokerage account.

Their annual spending is $40,000 (hence the 5 years of expenses in a brokerage account for the Roth IRA Conversion Ladder). The parents are 47 years old when their child enters college.

Additionally, this family has earmarked $84,000 for college savings (separate from their 25x spending for FIRE).

Using the EFC Calculator from the College Board, we can run the numbers on two different scenarios.

Scenario 1: $84,000 in a Health Savings Account (aka contributing the maximum $7,000 per year for 18 years of the child’s life)

Scenario 2: $84,000 in a 529 College Savings Plan

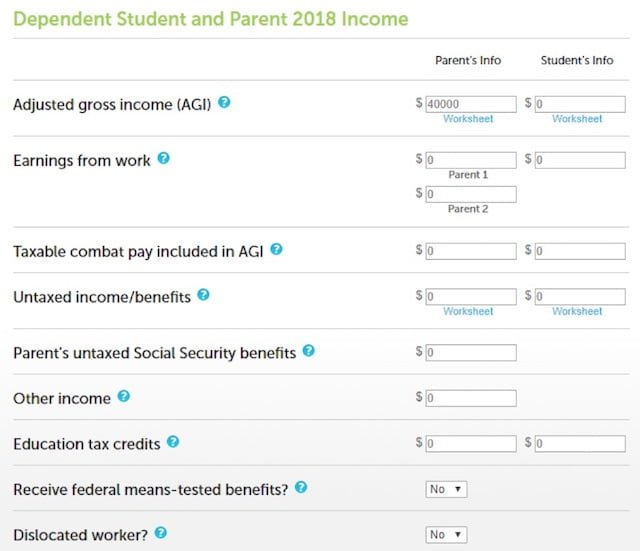

For the income calculations, we use an Adjusted Gross Income (AGI) of $40,000, which consists of converting money from a pre-tax IRA into a Roth IRA (aka Roth IRA Conversion) to cover one year’s living expenses.

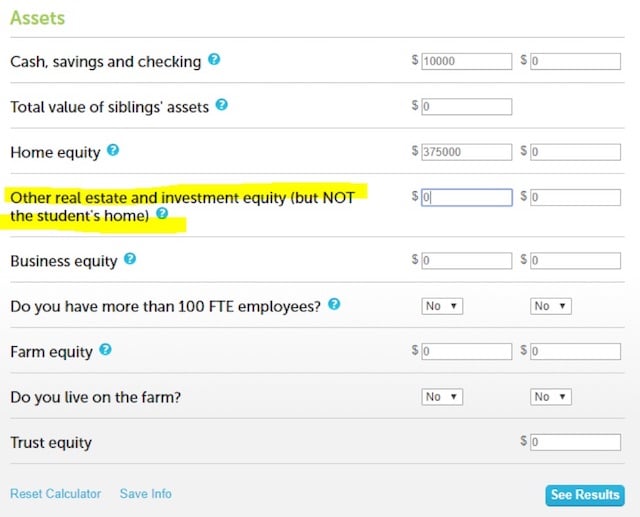

For assets, let’s assume a buffer of three month’s expenses is held in cash/savings/checking ($10,000).

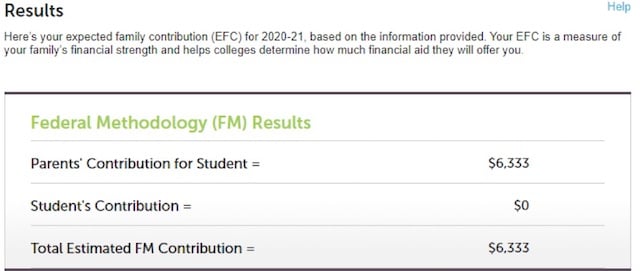

Here’s where we input savings.

For Scenario 1, the money in the Health Savings Account is not reported in this calculation.

For Scenario 2, the money in the 529 college savings account IS reported in the calculation.

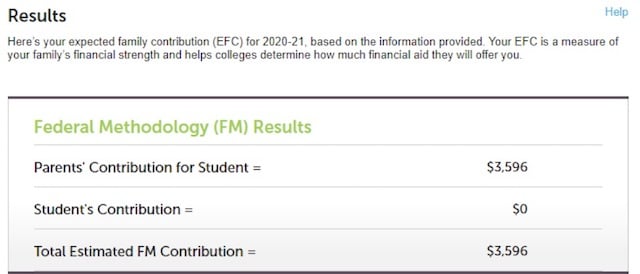

For Scenario 1, we come up with an EFC of $3,596 each year.

For Scenario 2, the EFC is $6,333 each year.

By stashing the college savings in an HSA, we’re able to lower the Expected Family Contribution by $2,737 each year. Over the course of four years, that’s $10,948 in savings! Think of this as a $10,948 grant available to your child because you invested their college money in the best type of college savings account.

These calculations also don’t account for the tax savings throughout the parents’ careers from saving money in an HSA compared to a 529 (that’s funded with after-tax money).

HSA Best Practices

Bookkeeping for HSA Records

We keep both paper and digital copies of medical bills. For every doctor/dentist/pharmacy visit, we keep the original paper receipts (explaining the services rendered and confirming actual payment). Each receipt gets their own individual page protector and goes into a binder labeled “HSA”. This is so the paper receipts don’t fade as quickly and the ink doesn’t bleed in-between pages. We also keep a digital copy with a backup in case the paper receipts get lost. To tally all the receipts together, we use a spreadsheet listing the dates, healthcare provider, description of the service and the dollar amount paid.

Health savings accounts are great because you have the ability to use the funds to invest and grow even more over time. For example, Fidelity offers a free HSA option where you can invest in their zero-fee index funds (instead of keeping the money in cash for 18 years). We chose to use a total stock market index fund for our HSA to maximize growth since we have a twelve-year timeline until our daughter starts college. Depending on the market performance in high school, we may choose to reallocate some of these funds to cash (i.e. the funds which have receipts to back up withdrawals) in the years leading up to college.

What If You’re Healthy?

What happens if your family doesn’t incur the full $84,000 of medical expenses between birth and college age? There are a few things to note about this approach. First, count your blessings for 18 years of good health. Up to now, our family has not incurred as much in medical expenses annually as we contribute to our HSA, so we do have leftover money. That’s why the health care receipts themselves are the valuable “college tuition vouchers”. For example, if our HSA has a $12,000 balance but we only have $6,000 of receipts, we’d only plan to use $6,000 for college. If you have multiple children, you can keep the HSA dollars for the subsequent children’s college educations.

Remember, there are lots of things that count as IRS-Qualified Medical and Dental Expenses (pdf) and these small purchases can add up quickly. For example, prescription drugs, contact lenses and solution, dental treatments, doctor’s office visits/co-pays, eyeglasses, IVF, flu shots, laser eye surgery, orthodontics, pregnancy tests, special education for learning disabilities, speech therapy, and vasectomies.

(GCC: we keep digital copies of all of our IVF and childbirth receipts, which now exceed the total value of our HSA. The Office Lens app is amazing!)

The interesting thing about an HSA is that if you don’t use the money by the time you’re 65, it then gets treated like a traditional IRA and you can withdraw the money for any purpose without penalties (i.e. no need to back up withdrawals with medical receipts), although it would be taxable income at that point (just like an IRA withdrawal)

Summary

By prioritizing HSA contributions during our working years, we’re able to minimize our tax burden and increase federal financial aid for college by almost $11,000.

If you have college-bound children, I encourage you to run the numbers for your future family situation and get an idea of how moving money into various forms can impact the numbers. This advanced planning can save time and money down the road and help set your child up to graduate from college without a hefty student loan package.

*Note that I’m not an accountant, I just read a lot about this topic. If you want to read more, here are some links for details:

Filling Out the FAFSA with an HSA

Wow! Thank you for this enlightening post! I got into the FIRE game a little late so I’m in the bittersweet position of having $45,000 in a 529 and a HS sophomore at home. My parents have a similar amount in an ESA for him too.

We have a paid-off house and another $75k or so in taxable non-retirement investments. Retirement assets approximately $700k and an HSA of about $16k.

I’d love to know what could be done about asset reallocation to maximize the FAFSA opportunities. Any ideas? I’m fully aware of how fortunate and lucky we are!

The big things for the FAFSA are to look at who has the assets (parents vs. kids) and what types of accounts they’re held in (i.e. retirement vs. taxable). Also income counts for more than assets, so scaling back work is also a strategy.

Wow I save my receipts in a folder and also scan them. But I didn’t think to use page protectors for each receipt. I also have an excel spreadsheet which lists each medical/dental expense.

In the posted scenario, wouldn’t it be better to pay for college from the taxable accounts first? Thus lowering EFC in future years, and allowing the HSA funds to continue to grow.

This theoretical FIRE family is using their taxable accounts for regular living expenses via the five year Roth IRA conversion ladder, so those taxable dollars are already earmarked. Plus the taxable accounts are being replenished via IRA conversions each year.

That’s very clever! Thanks for sharing. We treat our HSA as future retirement funds, opting to pay with cash for medical expenses incurred today. I never considered keeping our medical receipts to apply for reimbursement in later years. I will now!

With 3 kids, the HSA college hack won’t work for us in full, but every little bit helps. Thanks again.

Genius. The smartest blog on the Net has the smartest readers in the Net!

“withdrawals from a Roth IRA are counted as income.” Contributions to a Roth IRA can be withdrawn tax- and penalty-free.

It is absolutely tax and penalty free from federal income taxes, but it counted as income for the purposes of FAFSA

Yes, for federal income taxes, but the FAFSA still considers distributions from retirement accounts as income in their calculations. https://www.kiplinger.com/article/college/T042-C001-S001-how-roth-iras-affect-financial-aid-eligibility.html

The problem is that lowering your EFC by $10K does not mean that you will get $10K more in aid. Besides determining if your student is eligbile for a Pell grant, the EFC is simply a number that represents what the federal government thinks you can pay for college. What a particular college does with that number is up to them. And unless the college is a “meets need” college, the EFC number may not make a difference. “Meets need” colleges are not that plentiful and are mostly more competitive. Also, many competitive schools use the CSS profile in addition to FAFSA to determine how much need you have. The CSS profile goes into much more financial detail than FAFSA does.

Yes, each family should do research on how their desired colleges meet financial need. In our case, our in-state university meets 100% of your unmet need if you have a 3.5 GPA and a 1200 SAT. Our alma mater also awards 100% of the unmet need without student loans. College choice plays into this equation.

College choice is really important- some CSS schools treat HSA the same as a taxable account (even though health care receipts are needed to withdraw without penalty). Thanks for sharing your plans for utilizing a HSA! I will hold receipts for paying those future college bills (forced savings) – yay!

How do you guys get HSA? My employer doesn’t offer an HSA. Is there any other way to get to it?

Various institutions offer HSAs. First you must determine whether your health insurance is a “high-deductible health plan (HDHP)”.

You have to also have a qualifying high deductible health insurance plan, which some employers don’t offer in their benefits package. Since we buy our own health insurance (self-employed), we chose an HSA-eligible plan.

Had to chuckle. You know you are dealing with engineers when they write, “Each receipt gets their own individual page protector…” ;). Love the HSA as well!

We have one receipt for $6,380 (braces) – you better believe it gets its own page protector!

Great article. I’ve been saving digital copies of receipts, but what you guys are doing is on a different level.

Question: If one has dental insurance that covers a small portion of the braces, then would the HSA reimbursement still be good for the entire cost of the braces or would it be the cost of braces less the amount covered by insurance?

Your actual costs only.

Can you REALLY use medical bills from PAST years against the HSA account this year?

As someone else posted, why not deplete taxable accounts first leaving HSA for future medical Expences and retirement accounts for last.

You can use medical receipts from past years to withdraw from an HSA in future years – until Congress changes the rules. Hopefully this will still be in play when their daughter goes to college.

Yes, to using previous receipts. You don’t have to take the distribution the year the expense occured.

Per the IRS the only test to qualified distributions is the Qualified Medical receipts is they must have been incurred AFTER the HSA was established (“You can receive tax-free distributions from your HSA to pay or be reimbursed for qualified medical expenses you incur after you establish the HSA.”) So, if by PAST, you mean before you set up the HSA, then no, but if you mean what is meant by the post’s author, setting up an HSA, then saving up receipts for years, then submitting them for reimbursement then yes.

Always a good idea to check the IRS website for yourself though, it really is a great resource – https://www.irs.gov/publications/p969

This is great. I know of many of the major FAFSA hacks, but this is one I hadn’t heard of yet.

I do want to point out the 10% penalty and taxes on 529 money used for non education purposes is only assessed on the gains. So if you put in $20k over the years which grows to $30k, and you withdraw all of it for non educational purposes, the 10% penalty + taxes (it’s added to income and taxed like any other income) is assessed only on the $10k of gains, NOT the full $30k withdrawal.

And lastly, the HSA quacks like a tIRA post 65 years of age….until you reach the inheritance laws by non spouses

Not judging, but how do you feel about the ethics of ‘sheltering’ assets from FAFSA?

I love being aggressive with the IRS, but college financial aid is a limited pool of money. This may help out our kids, but it will take away from another student who may not have resources.

BTW, I applaud your research and creativity of this ‘loophole’.

i had the same question

The underlying premise is false.

“The Pell program has had a discretionary surplus over the past six years, estimated at $7.4 billion at the end of AY 2018–2019.” (source, pdf)

I have both 529 and HSA account. I use 529 to fund my childern’s education and HSA for future medical purpose. I pay medical bill by credit card to get reward point. let HSA to compund. Or as EM fund in case I would need it.

I think HSAs are great and should definitely be prioritized over 529’s and taxable brokerage accounts. But, I see issues with the plan of tagging HSA funds specifically for college. First, in order to tally up $7,000 of medical receipts per year you’d likely need $20’s of thousands of dollars in billed expenses each year. I doubt that’s common for most families, with the exception being families with medical expenses that aren’t covered by insurance, like IVF. Second, even if you are an unlucky family that racks up $84,000 in receipts over 18 years, if you withdraw those funds over 4 years for a $10k education grant*, you miss out on the potentially >$100k in tax-free gains those funds could achieve if you treat the HSA as a retirement account instead and take withdraw 20-years later.

*As Michele noted above, the calculated aid (“grant”) does not equate to distributed funds, at least at most colleges.

Remember, this family is already early retired, so they don’t need to add another $100k to their portfolio for the future. The HSA funds are separate from their FIRE fund (25x expenses). Regarding medical expenses, we haven’t had a year yet where we incurred $7,000 in expenses, but every single dollar we do incur, we keep the receipts. If I had $20,000 in expenses (not including monthly premiums), I’d keep $20,000 in receipts. For families on an HSA-eligible high deductible health insurance plan, we’re paying out of pocket the first $9,000 anyway (because it’s got a high deductible).

Why are the HSA funds separate from the FIRE fund? Money is fungible.

For preferential tax and FAFSA treatment.

I get that the HSA shelters an asset from the FAFSA calculation. That’s great. But I don’t see any accounting for the lost opportunity cost of withdrawing the HSA funds earlier than may be necessary. According to the EFC Calculator, increasing your income from $40k to $60k increases the EFC from $3,567 to $10,054. If you do that for 4 years it costs you $25.5k. Of course, you’d have to pay tax on those conversions, but even if you pay 22% tax (doubtful) on the $20k every year for 4 years, that only adds up to $18k. So the total cost of funding $80k of college via the Roth conversion route is $25.5k + $18k = $43k. The opportunity cost of taking out $84k of HSA money when you could let it sit for 15 years is ~$100k, assuming 5% real return. What am I missing? I’m genuinely curious.

Nevermind, it just clicked! Please disregard my ramblings. It’s not really fair of me to claim a lost opportunity cost for tax-free gains in the HSA, because you’d lose the same amount if you convert the Roth! What I really learned was how sensitive FAFSA is to income.

This is an OK strategy but you will depend on the regulatory environment not changing for 15 years and that seems highly unlikely. HSA’s could go away and something better like M4A will take their place hopefully.

Hello how much of this strategy matters to a household making about 150K in income at the time of applying and about 200K in taxable brokerage acct (not retirement)? I’m guessing very little, but would be interested in your confirmation.

You can run the numbers in the EFC calculator, but I’d imagine that unless you’ve got a large family, an income of 150K isn’t likely to result in a lot of financial aid.

Genius! Great post Kim! Us FIRE weirdos are ALWAYS looking to maximize our accounts! Kudos to this strategy and it makes sense to me as long as you can rack up that much in medical expenses prior to your daughter heading off to school to have the receipts to back up the withdrawls. As a dual US/CAD citizen who grew up in the States and now living in Canada I have to chuckle at the health related spending that is required to make this strategy feasible and the fact that there is a strategy regarding medical bills in general :) I honestly can say I don’t think my family will ever incur up to half of the required $84,000 of health related costs over the course of our entire lifetime.

$84,000 is only about a dozen sets of braces :)

Is there any scenario where someone who likely WON’T retire early, that is, before the child goes to college, can make use of this strategy? More specifically, does it make sense for me to use after tax dollars to pay for medical expenses now and use the HSA for college later? Are there ANY breadcrumbs remaining for normal retirees?

I’d say it’s the same argument for an HSA whether you use it for college or not. Triple tax advantage is hard to beat.

Yes

I had an HSA for a few years and am now retired. I am spending down my taxable brokerage account first and still paying no taxes.

Another way to use the HSA account is if you have medical Expences that are not deductable. Especially if you can’t afford to max out a ROTH IRA. Use the HSA money for the medical Expences but then contribute to a ROTH IRA.

In general contribute to a 401k to extent matched, then Roth IRA ( OR BACKDOOR ROLLOVER), then HSA, then taxable account ( in index funds you try not to trade by doing trading in sheltered accounts)

I understand concepts and fully take advantage of all HSA opportunities, but does anyone wonder what it will be like trying to submit receipts that are 20-30+ years old? I can just see the IRS questioning this. This seems ripe for fraudulent activities. What is to keep someone from submitting a receipt today, and then doing it again 30 years from now. How in the world would IRS be able to realistically keep up with this. Any thoughts?

You buy a house. 20-30 years from now, you sell it. Upon move-in, you remodeled the kitchen, added a bedroom, installed landscaping, and a few other things which increased your basis. Are the receipts for those capital improvements valid?

There are a lot of ways one could commit fraud – this one probably has a lower ROI than the others.

Almost everyone with a HSA will incur medical expenses and immediately benefit from saving their receipts. Very few will ever sell their home for more than 250k(single) or 500k(married) profits to even begin to take advantage of lowering cost basis. If people “recycled” their reimbursements for HSA’s over the decades, these numbers could get into the 10’s of thousands easily over a lifetime with an extremely messy paper trail.

Either way, will be interesting to see if a timeframe is ever placed on the amount of time someone has to reimburse themselves to eliminate this possibility of fraud, especially since I do not believe an HSA was ever intended to be an additional retirement savings vehicle like most of your readers, and myself, are currently using them.

See Q & A 39 in IRS Notice 2004-50.

“there is no time limit on when the distribution must occur”

“must keep records sufficient to later show that the distributions were exclusively to pay or reimburse qualified medical expenses, that the qualified medical expenses have not been previously paid or reimbursed from another source and that the medical expenses have not been taken as an itemized deduction in any prior taxable year”

Kim, could you please share where are you are investing your HSA dollars? I’ve had a bit of a time trying to find a firm that offers the HSA money in equities.

Fidelity is great

Thanks. I have my retirement accounts at Vanguard and last I checked they did not offer HSA accounts.

Hi Kim, GCC!

Loved the article, this is great. Now, even if someone doesn’t plan on having kids, or their kids don’t go to college, would it always be beneficial to save receipts and withdraw from an HSA for the tax savings?

For example, even if one let’s the HSA rollover to a traditional IRA during “retirement” age, they would still need to pay taxes on withdrawals as it is in regards to ORDINARY income (depending on one’s tax bracket that year). If they withdraw the $$$ before retirement and have the health expenditures to prove it, then wouldn’t it be in one’s best interest to withdraw and then deposit this money in a brokerage account, where tax expenditure could be long term capital gains tax instead of income tax?

Not sure if I’m thinking this through correctly, but wanted to ask the question :-)

Thanks!

We will all have medical expenses in our 60s 70s 80s. Letting the HSA grow is always going to be a better tax option* than withdrawing funds and letting them sit.

* the exception is when you die – if all the funds are in a taxable account they will get a step-up in basis. It doesn’t help you but does help your heirs.

Often FIRE folks keep referring HSAs are triple tax advantaged. I call HSAs – possibly as Quadruple advantaged !! (mainly applicable for folks working for large Employers especially)

Many folks don’t fully understand the fact that – HSA contributions – may already be FICA tax-free (Employer AND Employee contributions;; especially if such contributions are made directly via payroll) . This adds another layer of TAX-Free-ness to HSA contributions. This/HSA is especially relevant if you participate thru large employer., employee-contributions are also FICA/FUTA free ! (“HSA contributions made directly through payroll, you likely won’t be paying FICA taxes on those contributions.”). HSA is ever more relevant if your W2 wages already crossed SS maximum wage limits.

This FICA-free-ness may not apply to already/post-FIRE or retired folks, since they can’t possibly make direct payroll contributions to HSA (using cafeteria plan). Instead – FICA-free-ness applies more to working-bees (especially of larger employers).

Ref: https://www.biglawinvestor.com/sneaking-around-medicare-and-social-security-tax/

Great article – whether or not use HSA for college (using saved medical receipts as tuition vouchers); or simply letting HSA compound for much better/later use — you figure depending on your scenario and ‘then-in-future’ applicable laws !

Has anybody thought and posted possibly about: say, take a low-interest education (or home-equity) loan for the first 3/3+ years; then you can realize FAFSA income to pay off that loan (Roth basis withdrawals or brokerage selling to fully utilize tax-free bracket (108K with standard deduction MFJ?), or possibly more?

Again – Kudos to GCC and The Frugal Engineers !

This idea sounds great, but I want to be eligible for the “simplified needs test” on the fafsa; if I have an HSA deduction as an adjustment to income on schedule 1 of IRS 1040, I will not be eligible for the simplified needs test, which would greatly increase my EFC. Any way around this?

HSA’s are wonderful vehicles and we max both out whether or not we have the medical expenses. If you fall into the place where you don’t spend enough on healthcare so you can take it out tax/penalty free, there are some creative things you can do. I researched this a bit and found out you can use HSA money for Medicare premiums, so this can shave off money from you “old” retirement money requirements. In a year, you are looking at several thousand bucks for healthcare from age 65 and beyond that this HSA can be used for. With this in mind, the optimized solution is to not touch the HSA until it is absolutely needed to let it grow tax/penalty free as long as possible (or to reduce the EFC to hack the college expenses). Thanks for the post!

Kim, love the hacking idea! We max out our HSAs each year and plan to reimburse ourselves someday, whether it be for educational expenses or early retirement. I would love to hear if the changes to the 529 plans to cover grade school expenses have changed your views on the 529 plan or if you still avoid them?

Jeremy,

We are working overseas. Our medical provider plan through Cigna is a High Deductible Health Care Plan, as per the deductibles we have pay (and stated in the tax code) each year. Do you know of anything in the tax code that prohibits ex-pats from contributing to an HSA if they meet the criteria listed in the tax code? For example, some people have indicated that if one lives overseas contributing isn’t allowed; however, this isn’t stated in the tax code. In fact, nothing about living overseas and contributing to an HSA is in the tax code. Thoughts?

I believe the answer is no – it needs to be a “qualifying plan” (amongst other things) which a non-US plan most likely is not. But… if you find out otherwise, please let me know!

Jeremy,

So appreciate your willingness to kick this around with me. This is a bit long (sorry I could not be more concise) but necessary.

Question: Is your medical plan a qualified plan? Said another way, What is a Qualified Plan.

Healthcare.gov provides a list of what constitutes a qualified plan. Among the list, is ANY job-based plan, including Retiree plans and COBRA coverage.

Our school-sponsored plan is a JOB-based plan AND we offer Cobra. Based on these criteria, we have a qualified plan; however, this does not answer the question of contributing to an HSA. For this, we have to go to the tax code.

The tax code lists the following criteria: in order to be an eligible individual and qualify for an HSA contribution, one must meet the following requirements.

-You are covered under a high deductible health plan (we are/Cigna).

-You have no other health coverage except what is permitted under Other health coverage later.

-You aren’t enrolled in Medicare. You can’t be claimed as a dependent on someone else’s 2021 tax return.

deductible$1,400 $2,800Maximum annual deductible and other out-of-pocket expenses $7,050-$14,100

I could not find anything in Pub 969 suggesting a problem with living abroad. As long as one has an HSA through one’s insurer or other trustees and meets the other requirements, living abroad does not present a problem.

Our school-sponsored qualified plan seems to fit this bill.

https://www.healthcare.gov/glossary/qualified-health-plan/

Examples of qualifying health coverage include any of the following:

-Any health plan bought through the Health Insurance Marketplace®

-Individual health plans bought outside the Health Insurance Marketplace®, if they meet the standards for qualified health plans

-Any “grandfathered” individual insurance plan you’ve had since March 23, 2010, or earlier

Any job-based plan,

including retiree plans and COBRA coverage Medicare Part A or Part C (but Part B coverage by itself doesn’t qualify)

Most Medicaid coverage, except for limited coverage plans

The Children’s Health Insurance Program (CHIP)Coverage under a parent’s plan

Most student health plans (check with your school to see if the plan counts as qualifying health coverage)

Health coverage for Peace Corps volunteers

Certain types of veterans health coverage through the Department of Veterans Affairs

Most TRICARE plans Department of Defense Nonappropriated Fund Health Benefits Program

Refugee Medical AssistanceState high-risk pools for plan or policy years that started on or before December 31, 2014 (check with your high-risk pool plan to see if it counts as qualifying health coverage)

Thoughts on this? Jeff

A somewhat similar college-savings hack would be to set up an SEPP from a taxable IRA for the years remaining until the child finishes school for an annual amount close to what you expect the average HSA maximum contribution to be, and then use the SEPP distribution to fund the HSA, and finally to use the HSA (+ past unreimbursed medical expenses) to fund college. This is useful if (like me) you have very low cash available but large balances in the Regular IRA.