“Would you do anything differently if you were retiring in today’s economic environment?”

“What do you think of the 4% rule for people planning to retire soon?”

Let’s go through both of those questions.

If I Were Retiring Early Today…

Loosely and nominally, the SP500 is down 20% YTD and 15% over the past 12 months. In real terms it is down an additional ~9%.

Headlines are very doom and gloom… INFLATION! DOW JONES! WAR! HOUSING MARKET! GAS PRICES! I even saw one headline or another that said 2022 was the worst stock market performance year to date of any year in history.

Based on all of this… what would I do differently?

Nothing.

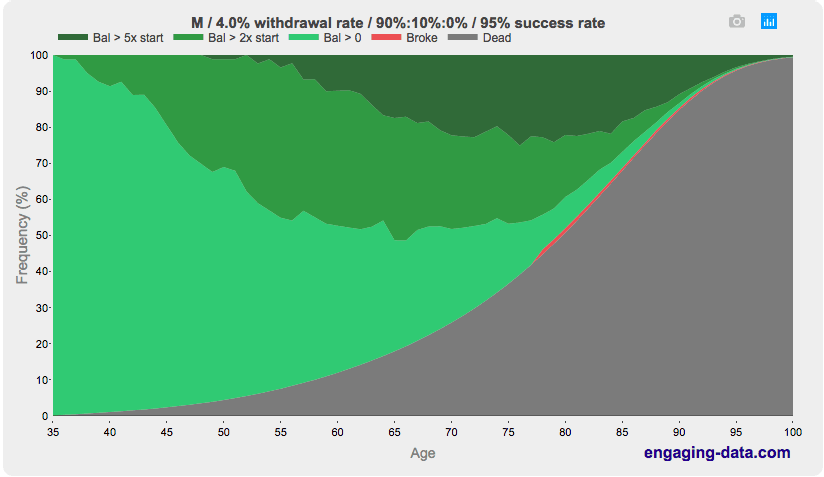

The 4% Rule

The 4% Rule is a rough guide that says you can (probably) spend 4% of your initial portfolio value each year, adjusted for inflation, and have your retirement savings last at least 30 years.

A lot of retirees (early and otherwise) use this as a planning tool.

But why is it called the 4% Rule and not the 5% Rule or the 6% Rule? Using data going back to 1871, spending 5% of a portfolio would have worked 75% of the time. 6% would have worked more than half the time. Even 9% would have worked on occasion.

But 4% worked through the worst times in economic history with a 96% success rate.

Inflation. Pandemics. World wars. Depressions. Recessions. Through all the bad times… even the worst of times… the numbers come out to ~4%.

Add in Social Security and this is the closest thing you can get to guaranteed.

The 100% Guarantee

“I don’t want the closest thing to a guarantee. I want a 100% guarantee!”

OK, no problem. With complete certainty… you will die. And pay taxes*.

This isn’t meant to be crass, we are just talking probability… read the post, You Will Die Before You Run Out of Money… for important perspective.

Death is guaranteed – Source

There are no absolutes here, but the 4% rule with Social Security is pretty dang close.

* or maybe not.

Worse than the Worst

This doesn’t mean times are good, of course. Headlines aren’t just made up nonsense (most of the time.) Maybe you personally feel the squeeze of rising prices.

So the question we need to ask ourselves is this… “Do I expect the future to be worse than the worst we have ever seen?”

Think about it for a minute…

…

…

…

…

If you answered yes… retirement probably isn’t for you. Or at least not right now. Retirement is an optimistic act.

If you answered no… we can at least be comforted by the knowledge that we agree.

Either way… it doesn’t mean things are going to be easy.

How would you feel if early into retirement your portfolio was worth half its starting value? When the markets fall fast and hard, it hurts, and our withdrawal rate doesn’t have much impact.

With 30 to 50 years to go… you have only 12 years worth of savings remaining with a current 8% withdrawal rate? (4% = 25 years of savings.)

This has happened multiple times in the past…. 1929, 1965, 2000 (See: How are the 2000 and 2008 retirees doing?)

Maybe 2022 will be on that list. We have no way of knowing until after the fact.

2012 Flashback

Back in 2012 it certainly wasn’t clear what the future would hold.

Here are some headlines from that era:

“The global economic outlook isn’t pretty”

“2012 forecast: anaemic growth in US at best”

“Debt hangover in the aftermath of the Great Recession”

“Gas prices at record highs”

“Slow recovery in the job market”

“Fiscal cliff looms.”

It seems the case is always, death on one side and doom on the other… with our retirement plans caught in the crossfire.

The Plan

10 years after the fact, it looks like most of those headlines were intentionally gloomy to drive clicks and engagement.

Maybe some of that is still true today (low unemployment, prediction markets have inflation dropping substantially, strong US dollar, US oil production at highest level since the pandemic, travel demand through the roof, the markets are not the economy, markets down but really only to 2020 levels, etc…)

But… we can only know for sure with the benefit of hindsight.

We must hope for the best and plan for the worst (or continue to work/save.)

Which is why, from my post on the 4% rule (read at least the part on a Foundation for Long Term Success), we had formulated this plan:

- Plan on a 4% withdrawal rate

- Spend less in the early years, the lower the better

- Minimize taxes

- Travel hack for free flights and hotel stays

- Minimize investment costs through Vanguard index funds

- Earn a little accidental income

- Be prepared to move bond position into stock in a severe downturn

- Be OK with going back to work for awhile

…

That still looks like a solid plan to me, I see no need to change or update it.

Retracing our steps

In late 2012 we flew to Mexico City with a plan to spend a year traveling throughout Mexico, Central, and South America. 6 months later we were still in Mexico…

The dollar is much stronger now, buying 19.x pesos vs 12.x pesos back in the day. A nice looking guest house in La Ciudad on hotels.com is $19/day… whereas I think we spent $25/day for a fairly dumpy hotel when we first started (that option also still exists for ~$25-$40.)

Mexico City guest house, $19/day (photo from hotels.com)

We then headed to San Miguel de Allende, arriving by bus with a reservation for one night in a hostel. Today that costs $25/night… I think about the same. Tuition for the Spanish school we attended is $420 for a month which also seems about what we paid 10 years ago.

I just browsed through some online menus in SMA… prices are higher but you can still get an entree at a mid-range restaurant for $6-$10 (and this is for restaurants that have websites and an online menu, which is not the norm.) Two of our favorite meals were a bowl of pazole or a torta de carnitas from little hole-in-the-wall shops. Lunch for 2 = $2. Maybe lunch is now $3, no big deal.

This has got me thinking… perhaps we should pack up the kids and head to Mexico! This looks fantastic!

In any case… “spend less in the early years” seems completely reasonable and achievable while retracing our footsteps. By continuing to LBYM we allow the portfolio to continue to grow and/or weather any storm.

But… what if it was a requirement that we stay in the US and live the American dream… pushing our budget hard to 4% with minimal wiggle room?

… in that case, based on current economic conditions I would probably continue to work for awhile longer… which is the same as in 2012 or any year.

What can I say, I’m conservative.

Summary

“Would you do anything differently if you were retiring in today’s economic environment?”

Nah – viva la Mexico!

“What do you think of the 4% rule for people planning to retire soon?”

It depends… retirement is an optimistic act. There is no way of knowing what the future holds.

The 4% rule with social security is incredibly robust. It’s walked the walk and got stories to tell, and it is still here.

If you think today’s economic environment is worse than the worst we have seen, it’s probably not a great time to retire.

If you absolutely have to spend 4.01% to meet the bare minimum standard of living you are entitled to and you are 25+ years away from social security… also probably not a great time (same as every year.)

But if you have a more sophisticated perspective and a reasonably conservative plan, as we did in 2012… I would personally be fine taking the plunge.

In early 2016 when I decided FIRE was a nice goal and the 4% rule meant $1m would spin off $40k, I figured we could be happy with that. Almost seven years later CPI calculator says $40k on 1/1/2016 is equivalent to about $50k, requiring $1.25m.

If we had a market portfolio worth $1.25m I would be writing my resignation letter (or rather, hinting strongly at my trusted boss to get me in line for a severance package) right now. Whenever we hit that equivalent — through inheritance, investment, discovering a winning Powerball ticket on the sidewalk, whatever — it’s time to retire regardless of what the market is up to.

I was also hoping for a severance package… it didn’t play out and instead I ended up working 3 more years since I had to commit to a new project.

Then I jumped ship even though the 2012 headlines were not that great.

Wow, three years is…a lot. Do you think you needed to, in retrospect?

I didn’t think I needed to at the time, although it was 2009 and thing were still fuzzy post-GFC… We basically lived just off dividends during those entire 3 years.

At the time the project I was working on was cancelled, and they gave us the summer to look for a new position in the company… It was a nice summer.

Several people from my team started moving to a new project, and I was being recruited as well. I held out as long as I could, waiting for the company to offer a package… a bit of a game of chicken.

It became clear that I had to either leave without a severance or join the new project. Guys I had worked with for 10 years asked me to do the latter. The day it was announced I submitted my resignation. No regrets – had a good time, accumulated some more $.

This was a lovely checkpount to see that the plans that I have enacted over the least four years are still relvant today.

We followed through on one of the points, and backed off on our plans to FIRE to Portugal and France. The war in Ukraine, which may limit necessary travel to Eastern Europe, injected too much uncertainty to that plan. We continued to work in our “funemployment” part time work, which we enjoy and provides us with world class wine and food, in addition to small amounts of cash. But, the effect on our portfolio is that a 3% withdrawal rate plus our income and barter, we have the equivalent of a $60,000 take home in the US. Not enough to buy a house these days, but enough to rent and get by.

Migrating to developing economies, using geoarbitrage and the strength of the US passport are important features. Above all, thether working, skiing, motorcyling or retiring, watch your environment like a hawk and adapt as rapidly as possible. Mobility, languages, forex, barter, learning, etc. The US could be a one party oligarchy like Russia within three years. How does that affect one’s plans?

Bravo! A timely and well-put summary, I especially appreciated how you stroke out the text “current market condition” and put focus on the other considerations. I feel like this is written for me! Muchas gracias! (better start learning Spanish now for future geo-arbitrage :) )

or learn spanish when you get there :)

I enjoy working, so I won’t retire just yet (@ 47 yrs old). However, I am working on our road trip from Denver to Alaska in 2023…..8,000 + miles, 144 hours in the truck, 7 weeks, and so many wonderful experiences with my wife and four kids!!! Got the spreadsheet up and running, camera ready, and 5th wheel trailer set for a great adventure. BTW, thanks for the IHG travel hacks…enjoyed a week in Washington DC over spring break using IHG and AmEx.

Nice! I love free vacations.

There are going to be some good stories after an epic journey like this. We did a week in Alaska a long time ago before we were married, hiking in Denali and camping around Seward… the wildlife is amazing. Enjoy!

I’m retiring in early January, the job got to be too much and I think my portfolio can support my barebones living expenses even if the market drops another 20% between now and then. I’m definitely nervous, but then I’m naturally anxious. I figure sooner or later, we were overdue for a major correction, and until I’ve survived one it’s normal to be scared. Thank you so much for a reassuring post!!! 😊

It does get easier, see Exposure Therapy and So That’s What It Feels Like to Lose $1 Million. Just look at a chart of long-term SP500… all of those past dips look pretty small in hindsight.

From an optimistic perspective: as of 10/2022, stocks are much cheaper than they were a year ago. As reflected in lower CAPE ratios going forward. I.e., if you have the funds now to retire on 4%, the likelihood for success is quite good.

Yessir, this is a very good point. I caution people in general… if you did all of your savings during a prolonged boom and you hit your 25x savings well ahead of schedule, it behooves you to be extra cautious (save more)… the bust is coming. And here we are.

If you still have 25X even at 20-30% down, you are in real good shape. And if you are still saving… congrats, you are getting a 20-30% discount.

Hey J, as you may recall, I quit in January. So I may be the poster child for the 21st c retire early worst timing. We’ll see. Am I bummed on the timing? Yes, given our portfolio has dropped more than 20% (we are more aggressively invested). But, am I scared? Not really, given we plan to continue our travels through Central and South America and Antarctica. The reason — to paraphrase your plan simply — hope for the best but plan for the worst. For us, it means probably adjusting the 4% down slightly for the next couple of years. And, if needed, we both know we’re fully employable when we return to the US. So in the meantime we’re really going to enjoy our travels and time together cuz life is just too short!

Yeah! Congrats Andrew.

I just checked out your blog. Looking good!

We really wanted to visit South America but we loved it so much in Mexico and Guatemala that we just never made it. (Except for that Chautauqua thing I did.)

It sounds like you have a healthy attitude towards everything.

We’re very similar, Andrew.

I also started full time FIRE withdrawals in January. And saw the nest egg drop by nearly 30%.

I’ve been researching expat FIRE and nomadic geoarbitrage since 2005. I motorcycled through Central America in 2009 and South America (not Brazil or the*guays) in 2013. I lived in Antarctica for a total of two years, supporting science.

Bad timing for the markets. But, we’ve been augmenting only a sub-3% SWD with part time work that we like.

Heading back to SA soon, hoping for a year of good living at low rates. There’s a big world out there, and you don’t need $100K a year to experience it.

Thanks for another great read. Timely and always enjoy your perspective on things.

My pleasure, Fred.

Yes, I agree with Dr. Zed. Since valuations have already fallen quite dramatically I think the 4% rule is an even better litmus test than a year ago.

Personally, I’ve tried to build up our cash flowing assets by purchasing an affiliate website. That has been both a positive and negative for me in that it has helped with cash flow, but I basically bought a full-time job for a bit.

Anyways, early retirement is all about managing risk. It’s always going to be there, but if you are flexible and optimistic there’s no reason not to give it a shot!

Thanks Jeremy, I enjoyed reading this.

I retired in December 2020, enjoyed 2021 in lockdown (I live in Melbourne, which had the most lockdowned days on Earth) and watched my portfolio drop a little over time.

I decided to pick up a few days of teaching on a casual basis, which has enabled me to leave my bucket of cash for market downturns untouched for this whole year, instead of needing to tap into it.

I’m not deprived – anyone who’s able to fly to the other side of the world to go to Antarctica is still in a very nice position. (I leave in December.)

Flexibility is key. Did I NEED to go back to work this year? Probably not, but it made me sleep a little better at night.

Your blog was where I first heard about FIRE. Thanks – it changed the trajectory of my life. :)

Sorry for being a bad influence. :)

Sleeping better at night is worth a lot! Working a bit on and off is a perfectly reasonable thing to do

Hopefully you can share some pics of Antarctica. I’ve wanted to go ever since seeing the pics from my friend Nick.

The thing about down markets is that if you have what you need to retire now, you probably had _way_ more than you needed at the recent highs. So you should probably just retire with confidence.

I think though that most people are probably more in the situation that they had what they thought they needed last year, maybe just barely, and now it’s 20% lower so they don’t have what they need. That’s a trickier question to answer but the “following the 4% rule” answer is that you should wait, even if that seems strange because you could have retired last year?

It’s not an exact science!

The comparison I like to make is this:

You retire today with $1 million. You can spend $40k.

A friend retires next year after the market has doubled. You both have $2 million.

Your friend can spend $80k but you can only spend $40k. Sorry, them’s the rules.

You make a good point – if you got to your target portfolio size way ahead of schedule because of a long bull market… more caution is warranted.

I make a similar point in this post: Lessons From Japan’s Lost Decade(s).

“Your friend can spend $80k but you can only spend $40k. Sorry, them’s the rules.” – how about the “retire again” scenario you mentioned in this article?

Spending more as the portfolio grows seems perfectly reasonable to me. The 4% rule doesn’t do that so you get these weird dichotomies.

A balanced perspective, Fine Sir!

I do try

I delayed my early retirement by 9 months and turned in my papers in March 2021, after riding out 2020 and realizing that I was OK financially to call it a career. The tax deferred accounts are in for the long haul so they will continue to be equity-heavy. Daily expenses are covered by dividends and cash. Our expenses are lower than 4% and I can sell stocks if needed to fund our vacations.

“Loosely and nominally, the SP500 is down 15% YTD and 20% over the past 12 months.”

You have these flipped. YTD the S&P is down about 20%.

Good article and something I needed to read right now as I am considering next year being my last year of “real” work.

Yes, you are correct. Thanks.

I remember thinking in 2013ish when I started following that you guys retired at a terrible time. The news was super negative!!

Thanks for the recap! I wish I would have followed your advice from the beginning. We tried a little real estate which put us back a year or two(now we look smart but it was 6 years of terrible returns) . Thank you for the good advice!

Negative news gets more clicks and views so the news is always negative. Broken clock right 2x per day, etc…

Glad to hear your RE investment is going well now… lots of people have success with it, I was not one of them.

Always good to get a little reminder that we are doing OK. Your ideas about spending less in the early years of retirement through geo-arbitrage was a lightbulb moment for me. We had not really considered perpetual international travel until I came across your blog years ago. It just made too much sense to ignore. We delayed or retirement a bit due to the pandemic. Mostly because travel was too much of a pain in the ass. Of course, this worked out well financially because we were still cramming money into the market while it was down (honestly, I wish it had stayed down longer). We finally pulled the plug June, 2021 and decided we would spend a year touring Mexico because, well, Mexico was easy. We wound up being wildly under budget for the year, spending a total of $26,200. This includes full international medical insurance for two people. Spending that little was easy and we lived very well. I point this out as an example of your advice being solid. Now, we are touring Southeast Asia and the good life continues. I recently had a shoulder consultation with an Ortho in Malaysia, which included an MRI. Total cost $260 U.S. Had a dental exam, cleaning, and X-rays in Chiang Mai, Thailand which cost a whopping $32 U.S. We just booked an nice one bedroom apartment with a pool and gym in Danang, Vietnam for a little over $400/month. We have been so far under budget every month, we have no worries about the current down market. In fact, I think we will splurge a bit on a tour of the South Andaman Sea Islands in Thailand this coming February and March. Again, all examples that your advice is solid. BTW, the wife loves all of your writing on taxes. Love your brain brother 🍻

Do you ever worry about the horror stories of US brokerage accounts suddenly being cashed out because the institution realizes the customer is not a US resident anymore and decides to not want to do business with them?

No

No

I definitely recommend the South Andaman Sea – I did a scuba trip there and spent an entire afternoon swimming with giant manta rays. Amazing! If you aren’t scuba certified there are a ton of inexpensive dive shops on Koh Tao.

This is great! It is really incredible how well you can live in many areas of the world for not much money at all.

Would you be interested in writing a guest post about how you are “wildly under budget” every year due to geo-arbitrage? Drop me an email!

I would be happy to write a guest post. I’ll drop you an email.

Thank you for this article Jeremy – it’s just what I needed to read.

I’m 59 and working part- time now with plans to retire at the beginning of 2023. I’ve run our numbers in Maxify Planner and it says we’re good to go with our 401K, small pension and future SS, but I just can’t fully commit 100% yet.

One of the issues we have is we’d like to spend more money in our early years of retirement when we can travel, gift $$ to our kids, etc…, rather than when we’re in our 70’s or 80’s and not as mobile. This goes directly against the advice given to spend less in the earlier retirement years. Figuring out how to balance that is always going to be a bit risky until we’re close to SS age.

@MarkD: I would suggest you to read a book called “Die with Zero” by Bill Perkins. It’s honestly a great philosophy and no, the author doesn’t imply that you must die with $0 in your pocket. I actually dismissed this book for a while just because of its title, but when I read somebody’s recommendation on the Internet, I decided to give it a try and checked it out at the library. I am glad I did. Very easy to read and straightens out the backwards thinking at the same time.

I liked this book, it does a good job of making you think of things in a different way.

Here is my review: Book Review: Die with Zero

Hi Mark

At age 59 you are close to SS age.

The “spend less in the early years” is geared more towards very early retirees (I was 38.)

Within ~10 years of SS it has an average effect equal to an extra $1 million in your portfolio.

When you model retirement in your tool of choice (I like cFIREsim) I would do it this way:

– plan for inflation adjusted withdrawals for your core spending, e.g. $40k from $1 million / 4%

– add extra spending for kids, e.g. $10k/year for 10 years, starting now…

– add extra 1-time spending for big things (help kids with down payment for house, grandkids college, etc…)

– add SS as an income stream that starts at age 67+/-

Then see what kind of success rate and terminal values you get. You can post details and screen shots on the forum if you want to work through it.

Thank you Jeremy. That sounds like a great plan!

Maxify Planner let’s you create multiple what-if scenarios so it it should be easy to publish a screenshot.

I semi early? retired in 2020-1ish … I like your reflection and thoughts today … I intend to also do some part time teaching of ESL (works anywhere in the world) … to keep active and shore things up … and it can be fun … I also like your idea of accidental income like you business blog or other side hustle projects to keep things entertaining … and maybe a little real estate and or some individual stocks etc … to diversify risk and keep busy … thanks for your updates and ideas – so many options :)

Well sometimes health issues require an earlier retirement. I think we have sufficient money to last until we get social security if medical bills aren’t too high. We’re pretty frugal and have paid off our house. Luckily we don’t have any debt yet. Depends on how high our medical bills become. Plus we have 2 rentals as an inflation hedge, annuities that we can start drawing on in 8 years if we are still alive, and we plan to wait 8 years until age 70 for social security. If we need more money I figure we can rent out our guest room but would probably need to put in a bathroom for the guest room as we only have 1 bathroom right now. Also probably would need to install a separate heating/cooling system for that room as we don’t have central air and we keep our thermostat low to save on heating bills.

Hi. Wondering if you could find the time to listen to the first part of this podcast about long time horizons for investing. Sounded to me that this new research debunks many commonly held beliefs in personal finance, would love to hear your reaction and thoughts. Thanks.

Prof Scott Cederburg: Long-Horizon Losses in Stocks, Bonds, and Bills

The Rational Reminder Podcast

Listen on Apple Podcasts: https://podcasts.apple.com/us/podcast/the-rational-reminder-podcast/id1426530582?i=1000584063409

My apologies… I don’t enjoy listening to podcasts in general.

Sounds like somebody selling a book.

Go directly to the paper: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3594660

Abstract: ‘… we estimate a 12% chance that a diversified [share] investor with a 30-year investment horizon will lose relative to inflation …’

That leaves 88% chance of gain. See fig 1, page 43; fig 4, page 46.

What is not included is similar analysis of low volatility investments such as best bank deposits as comparison.

Thanks! I’m not sure why this would debunk many commonly held beliefs in personal finance.

Negative returns on a monte carlo simulation aren’t surprising, nor are they if you start from extreme valuations (e.g. the example of Japan post-1990, Introduction, Line 20.)

Adds better data, still a ‘prediction’ about the past.

Would I retire early today?

Were I a USAn then I would not unless I had adequate Social Security retirement entitlements. (age 60+)

As an Aussie, birth through schooling is sufficient term of residency to qualify for the Age Pension. (age 67+)

Then I would require more than enough capital to near guarantee adequate cost of living cover until official retirement.

Only if I had greater than ~200 times living expenses (not including entertainment expenses) would I retire early.

= RATE((95 – 45), 1 / 200, -1, 1)

= 0.5% / y

= PMT(0.5%, (95 – 45), -1, 1)

= $0.05 / y

= ($1 / $200) / y

Worst case leaves capital to be consumed, better case real returns exceed worst case.

If the 4% says you need $1 million to spend $40k, you would want $8 million for the same budget?

4% nominal 90% adequate case vs 0.5% real worse / worst case (mean ~2.5%).

Just to clarify. So my experience with real estate has been awful also. We bought a huge run down building for super cheap 180k. We spent 500k fixing it up. Who knew you would need 6 new heating in cooling units in 6 years?😳 We tried another business in part of the building which has only been open for a year and it’s been a flop(although it may have helped a little with taxes. So I saved 40% on every dollar I wasted?? Idk).

Ultimately after 6 yrs, a ton of stress, skipped vacations and weird/crazy renters we are probably on track to make 8% next year after paying our new property manager.

When I look at what I could have made by just investing in VTSAX it makes me a little sick.

Three benefits 1. I know not to try it again in retirement 2.Diversification 3. Lower tax rate on the rental income

Very high risk in my opinion. Totally not worth it. I posted about it here about 6 years ago and was told it wasn’t a good idea. Totally right. Just wanted to be transparent for anyone else who’s thinking about it.

Sorry this was supposed to be a comment on my Oct 26th message

Just looked at doing a 1 month spanish immersion class in Mexico and was wondering if you have recommendations. Family stay including some meals are a great way to learn but I don’t think I can live 1 month like that. Did you guys stay in AirBnB while taking the course? Any recommendations would be appreciated. Thank you.

We weren’t huge fans of home stays in general. See this: Homestay Adventures.

Long-term rentals are great, especially if you can find them through local channels and pay in local currency. We paid $1k/month for a great place in Mexico whereas the cheapest thing we found on Airbnb was closer to $2k, for example.

OMG…I just read your home stay in Mexico blog. That is exactly the situation I’m trying to avoid if I do a 1 month immersion. Good to know. I guess the best thing is for me to hotel it for a few nights while looking for a 1 month place while I’m on the ground.

You had incredible timing for taking shares to buy a home last year.

Out of curiosity if you missed that window opportunity and wanted to buy a home now, where would you buy/what would you have done differently?

At this point in time…

I sold when the market US/World market was 10%/20% higher and (according to Zillow) our house was 5% lower. I think it is mostly a rounding error.

The main thing I would have done differently is just not get a mortgage. I borrowed at 2.75% which was a no-brainer. Borrowing at 7% is also a no-brainer on the other side.

I guess to play devil’s advocate, in hindsight 20/20, taking out the loan and buying stocks so far hasn’t worked out so well in the short term but I’m sure in the long run it will.

As someone who is still working and not yet living off equity returns, its weird to think about after the big housing boom this last decade that houses were actually the cheapest they’ve ever been in terms of # of shares of VTI last year.

My spreadsheet says the mortgage into stocks decision is down 12%

Edit: ps, thinking of things in terms of shares per house is kinda genius

Unfortunate timing so far, but it should be very easy to beat 2.75% going forward. Most people would love to have a 2.75% 30-year mortgage right now.

As far as shares per house, 2009 was actually the most expensive to buy a house per share rather than 2006 when home prices were at their highest. Obviously, it’s hard to time and jump in and out of the housing market especially with kids.