At age 59.5, all access restrictions to 401ks and IRAs are removed.

Sometimes people want to retire before then. (Hard to believe, I know.)

But what if most/all of your savings and investments happen to be in a retirement account? Or you prefer to hang on to the investments in your taxable account?

Fortunately there are a few options to tap retirement accounts early and penalty-free.

Accessing Retirement Accounts Before Age 59.5

It is possible to read for hours and hours (as I have) about early IRA withdrawals and come away with:

1) it’s complicated

2) it’s risky

3) you should hire an expert to advise you – see #1 and #2

But this is all nonsense.

I have a very simple goal – I just want to make reasonably sized IRA withdrawals in a tax (and penalty) efficient way, from the smallest possible portion of our portfolio, without significant commitment or hassle.

That is not difficult at all.

Options for (early) IRA withdrawals

There are 4 main options for accessing individual retirement accounts

– WUFNaH

– JPTP

– RCL

– SoSEPP

The first option is the most common – Wait Until Fifty Nine and a Half. Almost anyone can do this so it isn’t very exciting.

The second option – Just Pay the Penalty – is almost universally frowned upon but its really not a bad solution, especially for heavy earners. Paying 10% penalty on a few withdrawals seems better than paying 22%-32%+ tax during our peak earning years.

Option 3 – Roth conversion ladder – is the topic of numerous early retirement blog posts and financial newsletters. In short, you can do a Roth conversion in Year 1 of retirement and then withdraw those funds for spending in Year 6, rinse, repeat. (This is my least favorite option, however, because if I am going through the bother of doing a Roth conversion I would prefer to have those funds grow for 50 years vs 5. This was of thinking was corrected in the comments.)

Which leaves us with our 4th possibility, a Series of Substantially Equivalent Periodic Payments, the main topic of this post.

SoSEPP

In the most concise way possible…

The IRS says:

Under Section 72(t)(2)(A)(iv), if the distributions [from an IRA] are determined as a series of substantially equal periodic payments (called a “SoSEPP”) over the taxpayer’s life expectancy (…), the 10% additional tax does not apply.

This means you can make penalty-free withdrawals from an IRA before age 59.5 as long as you follow some rules around withdrawal size and duration.

Size:

In order for the distributions to be determined as a SoSEPP, withdrawal size needs to be calculated via 1 of the following:

– Required Minimum Distribution Method (like those required at age 73+, but 20+ years earlier)

– Fixed Amortization Method

– Fixed Annuitization Method

Duration

Once the withdrawal method and amount is determined, those withdrawals must continue for 5* years or until age 59.5, whichever is LONGER.

No modifications are allowed** – Do NOT add funds to this IRA, do not rollover a 401k into the IRA, do not do Roth conversions, do not make additional withdrawals… SEPP withdrawals and SEPP withdrawals ONLY (on this specific IRA.)

If these rules are not followed, the 10% penalty applies to ALL withdrawals (since the SEPP was formed) with back interest applied to the origination date. In addition, the SEPP agreement is now null and void so any future withdrawals are subject to the normal IRA withdrawal rules (I.e. subject to 10% penalty.)

IMPORTANT – don’t F this up, current interest rate for underpayments is 8% per year, compounded daily

* 5 years from the date of first withdrawal is NOT the same as the time to take 5 annual withdrawals.

** the only allowed change is a one-time / permanent switch from one of the fixed methods to the RMD method

All of this is outlined in IRS Notice 2022-6.

SEPP Calculations

If you look at any of the most popular SEPP calculators, they offer a ton of bells and whistles and allow you to make the full suite of choices.

That is nice, I suppose… if you want people to get frustrated/confused and run into the arms of a high price financial advisor. (Or you just enjoy complexity.)

So.. out of frustration myself I just wrote my own calculator that focuses on the simple goal – maximum withdrawals, minimum nonsense.

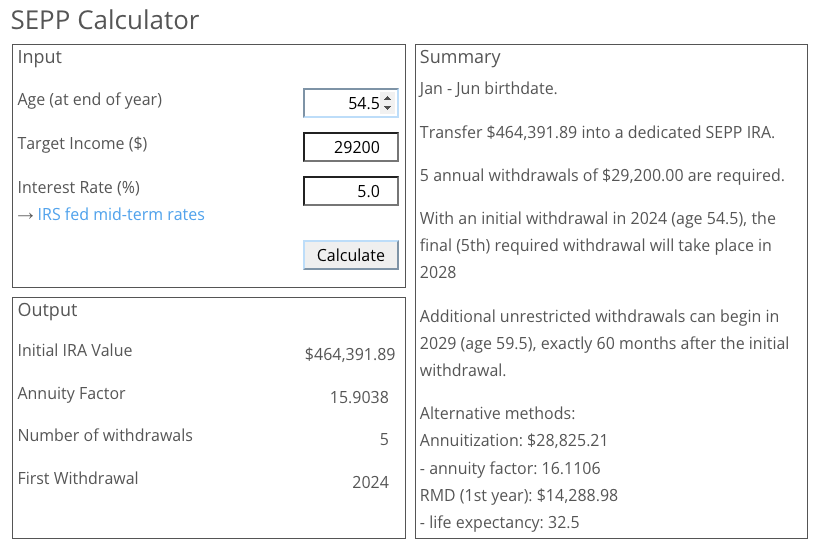

Because we really just need to know how much money we want to withdraw each year and our age upon first withdrawal.

Example:

Goal: I want to withdraw $29,200 each year starting at age 54.5.

Answer: Transfer $464,391.89 into a dedicated SEPP IRA, withdraw $29,200 per year (5 total withdrawals.)

Easy. Done.

Penalty: $0

Tax: $0 (based on 2024 MFJ Standard Deduction = $29,200)

More calculation details:

How does the math work?

Generally speaking, withdrawals are largest for the fixed amortization method:

(Fixed Amortization method > Fixed Annuitization method > RMD.)

Life expectancy is a variable in each calculation, and we can choose to go solo (single life expectancy) or include a dependent (joint life expectancy.) Joint life expectancy is always greater and therefore the permitted withdrawals are smaller… so we just use the single life expectancy tables.

Example:

RMD method

IRA size: $100k

Age: 55 (Spouse age 50)

From IRS 1.401(a)(9)-9(b)

Single 31.6

Joint and Last Survivor 40.2

From IRS N-2022-06

Universal 43.6

Allowed 1st year withdrawal

Single – 100k/31.6 = $3,164.56

Joint – 100k/40.2 = $2,487.56

Universal – 100k/43.6 = $2,293.58

Note: subsequent withdrawals (year 2, 3, …) will be either higher or lower as IRA value and age change (RMD method only.)

For the Amortization and Annuitization methods a “reasonable” interest rate is used in the calculations.

This rate is the maximum of 5% or 120% of the federal mid-term rate for either of the two months immediately preceding the month in which the first payment of the SoSEPP is made (An April withdrawal can use the rate from February or March.)

Example:

Fixed Amortization method

IRA size: $100k

Age: 55 (Single life expectancy = 31.6)

Interest rate: 5%

(Planning for an April 2024 withdrawal we can use 4.97% (3/2024), 4,79% (2/2024), or 5%. Higher rates = larger withdrawals)

First we calculate the present value of an income stream (PMT = $1) over our single life expectancy to determine a sort of annuity factor.

PV = [1 – (1+r)-n] / r = [1 – (1+5%)^-31.6] / 5% = 15.7200

Then:

Annual withdrawal = IRA size / annuity factor = $100k / 15.72 = $6,361.32

Example:

Fixed Annuitization method

IRA size: $100k

Interest rate: 5% (same “reasonable” rate as Amortization method)

Age: 55

The process is much the same as with the amortization method, but now instead of looking up life expectancy in a table, we get to derive life expectancy from raw mortality data (the same data used to derive the published life expectancy tables.)

The way that works is we do a bunch of math that ain’t nobody got time or interest for.

(Although… I did the math. Annuitization results shown in the SEPP calculator.)

And what we end up with is an annuity factor similar to or smaller than that in the amortization method, so we just use that instead.

Annuitization annuity factor = 15.9091, about 1% greater (resulting in 1% smaller withdrawals from same size IRA.)

The annuitization method results in a larger annuity factor because it includes the probability of death in the years beyond the values in the single life expectancy tables, e.g. a 55 year old has a single life expectancy of 31.6 years (age 86.6 years old.) The annuitization method includes the (very small) likelihood of living up to 120 years old.

Some thoughts

Should you use an SEPP? Probably not. But maybe you have to (because all your money is in an IRA.)

Should you hire a CPA or financial advisor to figure this all out for you (because it is complicated and risky?)

You could. This guy did… he only paid 15% in fees to avoid paying 10% in penalties (had there been an error.)

If you can use a present value function in a spreadsheet you can do the necessary math in a few minutes.

(Use my SEPP calc as a reference to double check your math.)

Practicalities / Implementation

We want the largest permitted withdrawals from the smallest possible IRA, so we use the Amortization method and the Single Life Expectancy tables.

Let’s say you have a $1 million IRA, but the SEPP calculations say you only need $250k for your desired annual withdrawals.

We can ask our IRA fiduciary (e.g. Fidelity or Vanguard) to transfer $250k into its own IRA… and then use that IRA and that IRA only for our SEPPs.

This allows us to use the remainder (e.g. $750k) if we need additional flexibility for more withdrawals (another SEPP, Roth conversions, JPTP, etc…)

Each year the IRA custodian will issue a 1099R, typically as Code 1: Early distribution, no known exception. This distribution is subject to the 10% penalty (because they are not aware that an SEPP exists.)

We must then file a Form 5329 at tax time to claim the exemption from the 10% early withdrawal penalty.

Summary

You can access funds in your IRA before age 59.5 by following a few simple rules.

The penalties for making a mistake seem a bit heavy so it is important to follow them.

An SEPP is a serious commitment, so we will do it only on a fraction of our portfolio. This begins by transferring the minimum funds required into a dedicated IRA solely for our SEPP.

We use the Amortization method using the single life expectancy tables to determine the size of this IRA because it will allow the largest withdrawals / smallest IRA size.

Try out our SEPP Calculator to figure it all out.

Enjoy.

In terms of simplicity, isn’t Roth Conversion the best idea? I am assuming one is withdrawing money to spend. So why the worry about the loss of compounding?

Also for the Roth conversion, you only transfer money you need to withdraw rather than a multiple.

Also you can choose to change your mind and not withdraw without any issues.

Hmmm, so a bit confused as to why you settled on SEPP.

Every fast food restaurant needs a chicken sandwich on the menu even if 95% of people will order the burger. There are pros and cons to each option.

To date I have personally gone with option 1 (WUFNaH.)

As for Roth compounding… early in (early) retirement it is quite easy to have a very low tax burden. Over time it becomes less so (long-term long term capital gains, Social Security, RMDs.) Therefore… having $$$s in Roth is more valuable later rather than sooner.

I retired at 53 and have been living off of my Roth IRA principle for the las 5 years. This is the simplest thing you can do no tax no penalty the money is yours. I ❤️ go curry but what he has done is to complicated for me.

Well… I haven’t done anything beyond highlight that this option exists.

Are still generating taxable income to take advantage of the standard deduction? (e.g. via Roth conversion) Is that what you mean by living off Roth principal?

3 years after a Roth contribution is made you can withdraw that $$ no penalty that $$ is your principal. I have contributed since I was 23 into a simple Roth IRA plan so I have accumulated a lot of principal. That will get me to 59.5 or older.

You don’t have to wait 3 years. You can withdraw contributions at any time without penalty. (Roth conversions have a 5-year seasoning period.)

My question is related to taking advantage of all of the tax-free opportunities.

You get a standard deduction each year which is like a 0% tax bracket (2024 – $14,600, single filer, $29,200 MFJ.) If you have no taxable income (because you live solely from Roth principal) then this tax-free space is lost. Ideally you could have some income source (such as a Roth conversion) to fill that 0% bracket.

This was very helpful, thank you very much. The simplified calculator is excellent.

GCC- Time to hang it up. This blog gad outlived it’s useful life. It was relevant when you were traveling world and living abroad, but now you’re just a suburbanite with outsized savings and routine financial tips that can be found in numerous places. Stop hanging on to the inck.e stream; time to cut the bird mate. Accept what you become: an American cliche. Sorry if the truth hurts. I’m unsubscribjng.

No.

🤣

M cubed fan boy

Probably lots of things going on here, mental health wise. It’s a bit weird to expect the entire internet to conform to your personal needs and expectations, and to have a temper tantrum when it doesn’t.

Not sure what the point of this comment was. Haters going to hate I guess. I found this blog post informational.

Good morning! You have put alot of thought into this. I have also heard something about the rule of 55 which may help some folks gain access to those funds as well.

Yessir… if you have a job until age 55, have a 401k via that employer, and that employer supports withdrawals, you can tap that 401k early without penalty.

Excellent Summary! Thank you

I did exactly that at age 55 with my Fidelity 401k.

If I’m not mistaken, you can also withdraw money penalty-free for first time home buying and for qualified educational expenses (like college). Right?

There are numerous non-retirement exceptions

https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-exceptions-to-tax-on-early-distributions

Love the chicken sandwich comment comment.

Purely to add to the chicken-sandwich crowd, i’d add two points

1. GCC points out that tax rates are lower in early retirement. I think that’s true for many for all sorts of reasons (e.g. our 10yo child’s impacts) but I’d not dissuade anyone from thinking through longer term management of effective tax rates, inclusive of indirectly affected items like healthcare costs. That may guide you to a different decision or mix of decisions. It’s complicated and few enjoy that as much as I do though.

2. I think the main knock on RCL is how you seed it. If you are seeding it by forgoing pre-tax opportunities (e.g. choosing a Roth 401k over a traditional 401k) during your peak earnings and highest tax rate years, that’s probably a mistake. If, somehow, you find your self facing the decision of SEPP or Roth ladder with an already seeded Roth, I think Roth is better because of the flexibility it offers. Pulling $X via SEPP OR pushing $X from pre tax to Roth and then withdrawing $X from Roth nets out the same. However the RCL lets you vary $X year over year which can be useful for a variety of reasons (surprise inheritance, Desire to increase make a large purchase).

Again, SEPP though is a solid default case for the Burger crowd.

I will add… you can order both a chicken sandwich and a burger (or neither.)

If you retire early (30s, 40s) an SEPP is probably a terrible idea. The commitment duration is way too long. Maybe you live off taxable accounts and some Roth conversions.

As you get to your mid-50s… the SEPP can look more interesting, especially as your IRAs have grown and you (perhaps) have drawn down the taxable accounts.

Many plan on directly accessing IRAs after age 59.5. Accessing them a few years earlier isn’t BAD or WRONG or SCARY.

It’s also optional

I’m confused. In the beginning you used Example:

Goal: I want to withdraw $29,200 each year starting at age 54.5.

Answer: Transfer $464,391.89 into a dedicated SEPP IRA, withdraw $29,200 per year (5 total withdrawals.)

All the calculations use 100K, so why the 464K?

Because those are 2 different and unrelated examples. The first introduces the calculator and how you can use it to get a simple outcome. The second shows how the math would work if you wanted to understand things behind the scenes… with different ages, IRA sizes (with a convenient size for comparison), and methods. You can explore the different options in the calc.

People are also increasingly looking to use the annuitization option of their retirement plans, especially if they are without dependents but also to keep their level of fixed income slightly greater than their needs to reduce dependence on their portfolio, or perhaps they just want to enjoy life without worrying about running out.

Not sure if I follow your logic against the Roth conversion ladder. Obviously you’d prefer to have money in a Roth as long as possible. But doing SEPPs won’t result in any more money in your Roth, and a conversion ladder won’t result in any less. The conversion ladder is like SEPPs but with a 5-year delay and less complicated rules. The money just happens to go into a Roth instead of being withdrawn directly.

With the full menu of options the SEPP is more complicated, but we should ignore 95% of it… and then it isn’t complicated at all.

I’m not presenting an argument against a Roth conversion ladder. But… I don’t see it as the holy grail of early IRA access that it is often presented to be.

There are times when it is the least worst option (you retired at age 35 and have minimal savings in taxable accounts) and times when it is not (you are age 54.5 and you have minimal savings in a taxable account.)

If I am going to go through the hassle of doing a Roth conversion (in all its complexity) then I would prefer something more than just some $ I can access in 5 years when there is a simple-enough alternative to provide funds today/now.

If you already had a Roth account for more than five years would a Roth conversion delay you from taking money out?

Or just start a second Roth account so the conversions don’t mess up the amount of contributions you can withdraw in the first account !

I don’t understand what benefit the SEPP is.

No, a Roth conversion doesn’t have any impact on when you can make Roth distributions. There are “Roth ordering rules” where contributions come out first, conversions later. But each conversion has to season for 5 years before you can withdraw those funds else the 10% early withdrawal penalty applies.

The SEPP funds can be withdrawn / spent immediately. No 5 year wait.

I was asking if you were affect by the 5 year rule but had an existing Roth that was seasoned, would you be wise to set up a new Roth for the funds that would need to be seasoned for 5 years

No. Not necessary

This is a really great summary and useful info. Thank you!

This is a great summary. I was facing a similar issue. I avoided it by delaying retirement by 2 years and socking some money way. But this is great alternative.

We’re planning to use the Rule of 55. Of course, this doesn’t help if you only have IRAs and don’t have a current 401k, but my husband is retiring the year he turns 55, so we’re planning to start emptying his current 401k first, until he hits 59.5 and we can withdraw from his IRA account without penalty.

Just wanted to encourage you to continue the blog. It will not be everything to everyone, but there are valuable nuggets for many of us on a regular basis. I learn a lot from the comments as well, some of them are even entertaining. Keep up the good work!

The comments are great, lots of good discussion here.

90% of what I write is because I am trying to figure things out for selfish reasons. When I can’t find what I am looking for in a way that is simple / easy to understand, I create it. I figure I got another year or two in me…

I get what you are saying, right now I am trying to figure out how to do a stretch with annuities. One company is helpful and straight foreword, the other company is the polar opposite and is trying to push me off on an advisor (fees) for basic questions. Apparently it will require patience. You seem to have a lot of patience based on how you deal with commenters here. When people ask me how I retired early, I tell them exactly how and their response goes something like ‘that can’t possibly be right’ or ‘It’s too complicated, I’ll just let the salesperson tell me what I need’ UGHH

I can’t help with annuities, sorry. They are not something I have explored in depth.

Patience is easy enough with strangers on the Internet… my life is exactly the same independent of their approval/disapproval. But when we have a fun conversation and everybody learns something, that is pretty nice.

This is great stuff!

I don’t follow – I think I’m missing an implied assumption. Is the assumption that the tax rate at the time of conversions will be higher than it would have been later off in retirement? Otherwise, if we assume the tax rates are the same, it would make no difference.

(maybe you used a T-bill ladder to bridge the 5 year seasoning gap helping you to drop a tax bracket while filling it out the for those first 5 years in early retirement)

my quoted text I was referencing was removed… “if I am going through the bother of doing a Roth conversion I would prefer to have those funds grow for 50 years vs 5”

No, it’s not that.

Let’s say tax on all Roth activity (conversions) is zero, for the sake of convenience, and that we start out with a small token of Roth value ($25k.)

In the roth conversion ladder case, we withdraw all contributions and conversions in order to fund life in our 30s and 40s.

In an alternative case, we let the Roth grow and fund our life via alternative means (SEPP.) When available with no tax we add a few Roth conversions, and also let them ride.

In both scenarios life is good, we have fun, and pay next to nothing in taxes.

Now we are 80 years old. Our taxable income is fairly high, thanks to Social Security and RMDs. Maybe our marginal tax rate is 32%. Our basis in our taxable brokerage account is fairly low, so any stock sales result in a large increase to our adjusted gross income.

What would be better in this situation for marginal spending, a Roth account worth $1 million (because we never touched it) or a Roth account worth $100k (because we withdrew as much as we could as soon as it was legally possible.)

I’m still struggling with this. An equivalent amount going toward SEPPs or a Roth conversion ladder would incur the same amount of taxes, so in either case you could choose to add in the same amount of Roth conversions. With the Roth conversion ladder you only withdraw the amount you converted 5 years later. So why would you end up with a much larger Roth if you go the SEPP route?

Actually… the reason you are probably struggling with this is because you are right and I am wrong. If you have funds to cover the 5 years to season a Roth conversion then the cash flow thereafter is essentially the same.

Love that you owned up that his logic was sound. 👍

Well.. he was right and I was wrong :)

I recall specifically asking you to write up your thoughts on using SEPP. So thanks! Do you ever see a scenario where you would pursue a SEPP before drawing down the taxable accounts pretty close to zero?

Can you expand on the scenario you are envisioning?

I really don’t see any downside to starting an SEPP around age 54.5 +/-.

If you are going to run out of funds in a taxable account around that time then what other option do you have?

Sorry if I wasn’t clear in my initial question. Let’s say you are 54 years old and have 500k in taxable brokerage accounts and 500K in a traditional IRA. Do you see any scenario where you choose to start the SEPP at that time (age 54) rather than just continuing to drain down the taxable brokerage? I’m trying to understand if there are scenarios for doing a SEPP even if you are NOT about to run out of funds in a taxable account.

I can think of a case

After 3 or 4 decades of growth, that $500k in taxable brokerage accounts could be from an original investment of just $100k. Selling $10k stock realizes an $8k capital gain, not very different from an IRA withdrawal (80% taxable income vs 100%.)

Those capital gains are taxed more gently at the federal level, however. Very likely 0%. As such, it would be a waste to use the standard deduction to offset capital gain income. IRA withdrawals / ordinary income would be better.

And since the IRAs have grown by a similar amount, getting more out early can help with RMDs in 20 years.

How to access the IRA funds if you are 54.5 years old? I listed 3 methods: pay the penalty, Roth conversion ladder, or SEPP. Readers mentioned Rule of 55 also.

Let’s say we like the Roth conversion ladder best (as the comments show, people view SEPP as complex and risky.)

But we still need some spending $ for 5 years and want to keep taxable income low(ish) because of ACA subsidies so we want to hold off on selling that low-basis stock.

Roth contributions are an option.

For most people Roth IRA contributions should happen early in your career (when income/marginal tax rate is low) and then later transition to Traditional.

When Roth IRAs first appeared on the scene, the contribution limit was just $2,000 (1998.) Even if I maxed out Roth IRAs for the first 5 years of my career, at most I could have contributed $10,000. Contribution limits have increased over time, but in line with inflation, so most of the value is in the earnings (see chart.)

Fast forward to age 54 and I can withdraw that $10k… but that money won’t last 5 years.

Which probably means the best option is the SEPP, as it provides immediate cash.

Summary:

– low basis in taxable account

– asset sales in taxable account would realize long-term capital gains (0% tax rate)

– don’t have significant inflation-adjusted funds in Roth contributions / seasoned Roth conversions

– Traditional IRAs are large and early withdrawals would help with RMDs

– confident that we won’t have “unplanned” income before 59.5

Thanks for your detailed response. I agree that there are scenarios where the SEPP makes sense even with assets remaining in taxable accounts–the SEPP could help especially with trying to trim down the traditional IRA so that the RMDs aren’t massive down the road. By coincidence, I read this article this morning that is exploring many of the same issues: https://robberger.com/tax-efficient-retirement-withdrawal-strategies/.

I perused the article you linked, thanks.

In the “Is your 401k too big” articles I wrote awhile back, I explored how much $ you can have in Traditional accounts before they become tax-disadvantageous.

Once they become “too big” there isn’t that much you can do… Even if we decide to start tapping IRAs early, if we aren’t drawing them down faster than they grow then we are just doing it for fun and vibes. (e.g. 15% withdrawal > 10% growth.) Most likely that means paying higher marginal rates now to avoid paying higher marginal rates later, 6 of one, half dozen of the other.

I think SEPPs can work well for some at age 50+. For younger folks it can be more dangerous. Over 15 (or 30) years many things can change in your life and your need for distributions. You only have one chance to change. Also as you pointed out, if you screw up once all the distributions are no longer SEPPs. One error can be very expensive.

This is why I setup the calculator so you can’t even enter an age less than 50

I really enjoyed this blog post and I appreciate your thorough exploration of the options Jeremy!

There is no 1 best way to manage retirement money, it depends on each individual’s circumstances and goals. This is why I appreciate reading about all the options, so I can make an informed decision as my circumstances change.

Right now I’m 40, F.I. and living off a combination of taxable accounts and casual earned income. For 2023, my capital gains were small compared to my withdrawal so I was able to do a Roth conversion for $0 tax liability. That used up my 0% tax “room” as you say. I also did a Roth IRA contribution with my modest earned income that got me a savers credit to offset a small amount of tax that would have otherwise been due on the Roth conversion amount.

I can imagine a scenario where doing a SEPP in my mid 50s could make sense, it just depends on what the distribution of my accounts looks like at that time, as well as my overall tax and income situation.

If I have depleted my taxable account by 54, but still have pretax IRA money, I might choose the SEPP over taking Roth money out.

I’ve considered the benefits of getting as much of the pretax money into either Roth or taxable, at a 0% tax rate, as possible before I start taking Social Security.

I paid plenty of tax while working!

This is the right way to think of it, imho.

Thanks to the questions from Craig, I think Roth conversions are actually the way to go unless you absolutely don’t have the funds any other way.

If you have $0 in taxable accounts at age 54.5, if you do a Roth conversion of $x and also withdraw $x of previous contributions / seasoned conversions from the Roth… the cash flow is equivalent to the SEPP but with fewer restrictions / more flexibility.

Good point.

I like to use retirement calculators for each type of money. I.e., running a calculation with just the taxable account and my current spend shows a 50% chance the taxable account is depleted before I’m 59 1/2.

Then, I run the same type of calculation to see what the chances are that I will have converted all of my pre-tax IRA balance to Roth by that date, or by various Social Security relevant ages.

If market returns are on low side, especially in the next 10 years, I might try harder to slow my rate of withdrawal from the taxable account, by cutting spending or by increasing earned income. But, if that’s not possible I’ll just have to let it ride, even if it means spending Roth contributions.

I’m grateful for a simple good life either way.

Actually, the calculator does not have that limitation.

Yes… if you manually type a lower age you can bypass the min/max of the input field. And on mobile manual entry is the only option.

Thanks for the great write-up and calculator. If you were to pursue this strategy, how would you allocate your assets in the IRA you are pulling SEPP withdrawals? Would it differ depending on which method you used?

I would keep asset allocation the same.

You could maybe put the least volatile assets inside the SEPP IRA to avoid the potential of drawing that IRA to zero in a severe market downturn.

Ten years into our retirement journey and six months into zero earned income we are still in the wait til 59 1/2 camp.

This is not because we are unwilling to do any of the other options but because realizing less income has been useful for ACA and FAFSA purposes.

We still have 10 years til Medicare.

We have two offspring. One that has completed his higher education and working full time.

The other will have a year of college completed in a couple weeks but his plan is pretty fluid at the moment except that he doesn’t plan to return to school in the Fall.

We are going to continue to just play it by ear and how we get to convert some of our trad to Roth in the next 15-20 years.

We retired in Mexico 7 years ago and and we have not withdrawn any money from our 401K yet. Cost of living here is so much cheaper than in New Jersey.

We used SEPP when my wife inherited IRAs in her late 30s. Rather than pay a high marginal tax rate on a full distribution that we didn’t need, we spread it out over her lifetime. I know you can’t do that anymore for a non-spousal inheritance but even spread over 10 years it can be a good plan.

Thank you for posting this. The SEPP is on my short list of back of plans if my current early retirement income gets too tight. Quick question that maybe I am just missing from your post. When someone transfers the funds from their IRA into the account that will be used for the SEPP those funds are then sold at the present market value. When new account is opened do those funds just sit in a money market account and gain a little interest? Or is that principal amount then locked in and doesn’t grow any further (or decline other than when when taking a withdrawal)? Hope that makes sense.

The account that will be used for the SEPP is an IRA. Maybe you start with one big IRA and end up with 2 (or more), of which one (or more) is for an SEPP.

When that money transfer happens (from the big IRA into the SEPP IRA) it is cleanest to:

– sell assets in the origin IRA

– move cash to the SEPP IRA (so it is crystal clear what the starting value is)

Then you repurchase the original assets so that your total asset allocation is unchanged before/after.

(Other strategies exist.)

Leaving a large percentage of your assets invested in cash is probably sub-optimal.

Thank you for the response! I guess the part that is confusing, even after your answer, is if you sign up for equal SEPP payments but have the funds in the newly created smaller SEP account invested back into the original, or any other market based investment, and that investment drops, then how does that affect your equal payments. Is it just based on a % of the new SEPP account value at a given time? It seems like your future payments would then have to be reduced because of the drop in the market which would not make them equal payments.

It doesn’t affect your payments at all.

What kind of investment drop are you thinking of? In the SEPP calculator example above you start with an SEPP IRA value 16x your annual withdrawal and you only have to do that for 5 years (compare to “4% rule” which expects a portfolio to last 30+ years based on 25x, and even then it will probably grow to incredible size despite decades of withdrawals.)

But… you are allowed a one time change to the RMD method of withdrawals which update annually based on portfolio size and age. In the example above the initial RMD method withdrawal was 1/2 the size of the Amortization method.

Or… if the SEPP IRA drops to zero value because you invested 100% in leveraged crypto funds and were wiped out on a downturn, the SEPP contract is considered complete (no IRS penalty will apply and no future withdrawals are required.)

Ah! That makes sense and it is clicking in my head now. Thank you for the responses! I am glad to have this option in my RE tool belt! We are living off of our rental portfolio now and our net cash flow can be very inconsistent so we are considering pulling the trigger on moving some of our SEP IRA into a SEPP plan to smooth out the ride until we can begin fully drawing from our IRA.

I was caught off guard by that NASTY comment. It moved me to subscribe. I usually don’t but just wanted to let you know that what you are and have been sharing has value. Please continue to the be the person that you are and keep helping those that are willing to have an honest discussion with you.

Thank you kindly.

I do hope that one day you too will unsubscribe, solely because you have grown financially and as a person such that this blog is no longer able to provide real value to you.