(This post is the 1st in a series. Subsequent posts forthcoming… soon.)

The stock market has had a pretty good run over the last 10 years or so.

If you’ve been following financial best practices by contributing to Traditional 401ks and IRAs, the odds are good that those retirement accounts are reaching lofty heights.

Is it possible that those accounts have grown too large? Is your 401k TOO BIG?

Is Your 401k Too Big?

Assuming I didn’t have to work any longer or harder for it, I’d much rather have $1 billion than $1 million. Having too much money isn’t high on most people’s list of problems.

So how could a 401k be too big?

These accounts allow us to invest for the future in a tax advantaged way. However, in some cases a 401k can become tax disadvantageous due to sheer size.

To determine if our 401k has (or will) become too large for its own good requires a bit of tax law and investment return foresight, but in this and subsequent posts I attempt this feat nonetheless. (All numbers in this post are for a Married Couple Filing Jointly. Single Filers can divide by 2.)

Beating the RMD

Maybe you read on the Internet somewhere about how you can Never Pay Taxes Again? Using that as a goalpost, a Married Couple Filing Jointly could make completely tax free annual Roth conversions equal to the Standard Deduction ($24,000 in 2018.)

Repeat for 10, 20… 50 years. An example: I previously shared our own efforts to build the world’s longest Roth IRA Conversion Pipeline.

At what level / size does the 401k become too big, such that this task become Mission Impossible? When the minimum distribution amount exceeds the Standard Deduction. See chart. (All #s in 2018 $.)

At first it appears an IRA value at age 70 1/2 of ~$650k would be a good target; those early RMD withdrawals won’t result in tax due.

Alas, RMDs are based on life expectancy, which is a nice way of saying they are designed to drive IRA value to zero before you die. This is done by requiring increasing large distributions, which are inherently tax inefficient. The IRS wants their money.

As such, if we are even close to this “IRA value” threshold, subsequent years will definitely result in a tax burden.

To avoid this, we need to determine a glide path that will coast under the RMD. This is the opposite of a large lump sum withdrawal – regular annual withdrawals of a size designed to minimize lifetime taxes.

Since this is dependent on future investment return, I implemented a series of Standard Deduction sized Roth conversions at multiple CAGRs such that total tax on all conversions is zero even as the RMD takes effect.

Here we see that an IRA value of more than ~$350k at Age 70.5 is “too big” except for low expected real return, either by design (low equity allocation) or a series of unfortunate market events.

And here it is in Table format – All numbers are real / inflation adjusted. For future use, scale all numbers: Today’s Standard Deduction / 2018 Standard Deduction.

| Tax: 0% ROI = real | 4% | 5% | 6% | 7% | 8% | 9% |

|---|---|---|---|---|---|---|

| 30 | 569k | 468k | 396k | 341k | 299k | 266k |

| 40 | 554k | 461k | 392k | 340k | 299k | 266k |

| 50 | 532k | 449k | 386k | 336k | 297k | 265k |

| 60 | 499k | 430k | 375k | 330k | 293k | 263k |

| 70 | 450k | 399k | 355k | 317k | 285k | 258k |

| 80 | 378k | 348k | 319k | 292k | 268k | 246k |

| 90 | 272k | 264k | 255k | 243k | 230k | 218k |

| 100 | 114k | 129k | 141k | 145k | 149k | 151k |

Deeper Analysis

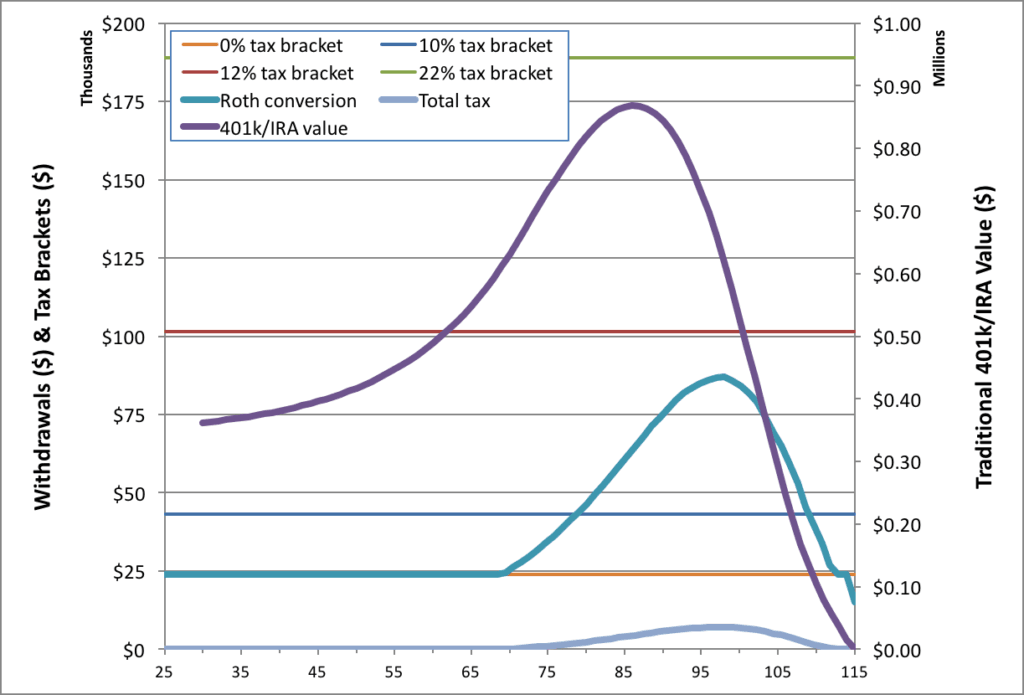

Let’s look at the case where IRA value is $650k at Age 70 1/2, the minimum IRA value that will result in the RMD exceeding the Standard Deduction in that year. What does the future tax burden look like, assuming a 7% real return going forward?

We can see that the 401k / IRA value continues to balloon (Purple line), even as withdrawals grow (Teal line), peaking at ~$865k at age 85. We can also see that RMDs cause annual tax burden to climb (Light Blue line.)

Imagine that you are 40 years of age in the 22% tax bracket, and evaluating whether to make 401k contributions for the year. “On the one hand, I want to not pay taxes in retirement. That sounds cool. On the other hand, I don’t want to pay taxes today and I get a tax deduction for contributing.”

Contributing the max ($18,500 in 2018) will save $4,070 in tax today. The NPV at Age 40 of the entire series of tax payments in the chart above is…. wait for it… $4,070. The peak tax burden starts in the late 90s, and half of total burden comes after age 97.

If we live long enough both options have equal value, but one is more predictable and immediate. Given the enormous delta in IRA values, I’d err on the side of contributing too much.

Other Income and Credits

What about other income? Many “early retirees” have some rental properties, a pension, non-qualified dividends, interest, or accidental blogging income (basically anything that isn’t qualified dividends or long term capital gains.) And most people will have some amount of Social Security income. How does that factor into this?

The math is deliciously simple in this regard, and we can just reference the Standard Deduction. Earn income equal to 1/4 of the Standard Deduction? ($500 per month.) Reduce the target IRA sizes by 1/4.

If the income is Social Security, first determine what percentage of the income is taxable (max 85%.)

For credits, we can choose to increase the size of IRA conversion / withdrawal into the 10% tax bracket. For example, if we have a Foreign Tax Credit of $600 from ownership of International Stock funds, we can convert an additional $6,000 or 1/4 of the standard deduction. Our target IRA size is also therefore increased by 1/4.

Summary and Next Steps

For extremely early retirees or late savers, no tax burden in retirement may be a natural and predictable outcome. But the IRA values that allow it are not large.

Instead, we can focus on lifetime tax minimization. Mathematically speaking, it is better to have an extra dollar and pay tax on it than to have no dollar at all. Furthermore, it would make little sense to pay more tax now (by not making additional 401k or IRA contributions) just to not pay tax later. Don’t let the tax tail wag the dog.

Are there other higher thresholds where 401ks can become tax disadvantageous?

Is there a point where it makes sense to reevaluate additional contributions?

Can we take steps to minimize the peak tax rates?

These questions and more will be explored in the rest of this series.

(This post is the 1st in a series. Also see: Is Your 401k Too Big – Part 2 )

For an aspiring early retiree in the wealth accumulation stage, if their employer provides the option to have a Roth or Traditional 401(k), is it always/usually the best option to choose the Traditional IRA? I understand everyone’s situation is different and other forms of income, such as rental properties, can have an affect. I plan to “retire” in 4.5 years and I have a Roth 401(k) and am contemplating shifting to a Traditional 401(k). Thanks

Almost always, yes. See this post to stimulate thinking on Roth vs Traditional.

Jeremy,

If you have some after tax savings in cash or bonds (as I assume a lot of readers planning for ER do), another strategy for dealing with taxes would be to use the IRA for the cash and bonds instead and buy equities with the after tax money. I am hoping one of your articles in the future will discuss the savings available by doing that tax maneuver. Good article.

Keep up the good work!

See Boglehead’s tax efficient fund placement.

But it isn’t just the tax efficiency covered in the Bogleheads article. If you plan to hold some bonds in retirement and you place your entire bond allocation in tax advantaged accounts, this also dampens the expected growth in your 401K over the long term, no?

Thanks for doing this series. Do you plan to address the case where a couple has most (85+%) of their savings in tax deferred accounts? We have access to 2 401k’s and a 457, maxing them all out. Now I’m trying to figure out how to get it back out again without screwing up ACÁ subs.

I’ll address the general case. Starting in 2019 there is no ACA Individual Mandate, which in theory means you can buy an HDHP again which has no MAGI dependency. In the meantime, you may have already read this post on the balancing act between tax minimization and ACA subsidies.

I also have the same problem. I am retired age 63 wife 64 cannot take SS or many dividends and no IRA money. I have to keep the income under $64,500.00 to keep a subsidy on the ACA otherwise the ACA will cost $27,000.00 for 2018. Would like to move money to Roth as my IRA is over 1 million. I am screwed!

You don’t think a $1 million IRA is the opposite of screwed?

Individual mandate goes away in 2019, and wife will be on Medicare so ACA subsidy impact is reduced / goes away. Odds are good that you still come out ahead vs having never contributed to IRA in the first place. I’ll explore that in this series.

I am a 58 year old disabled person on Social Security Disabiltiy and Medicare. During my career, I saved a lot. My husband and I have plenty in our after tax account to last us until my husband is at retirement age in eight years and able to draw Social Security and a pension. But I keep wondering if it wouldn’t be smarter to tap my $1 million IRA now due to special laws for disabled persons. Do you have any advice on that?

This is an important question for people pursuing FIRE. As you expand the series, I urge you to balance the two issues of taxes in retirement and taxes during the accumulation years. For my age (mid-fifties) and income, the ROTH options were not available (ROTH not invented yet), not allowed (income too high), or would generate enormous taxes at time of conversion. There is probably an earned income/ordinary income level during accumulation years where ROTH savings/conversions stop making sense.

Until recently, I put nearly all my retirement savings in 401(k)s and traditional IRAs. The ROTH accounts are not compelling for my situation. I probably should have put some percent (say 25%) of my savings into a traditional brokerage account. I would have paid taxes on the earned income that was the source of the savings, but there would little other income/taxes until selling shares later with growth taxed as long-term capital gains. This traditional brokerage approach would have given me more flexibility with retirement in my mid fifties.

The ROTH and ROTH conversions make more sense for younger people like you and my kids.

No urging necessary, that is the subtext of the series – lifetime tax minimization. See my previous work on the virtues (or lack thereof) of Roth accounts.

Reading your post today, I just had to think about Mitt Romney’s “between $20-100 mio USD” private-equity fuelled elephant IRA. Maybe he should read your blog-post too!!! Cheerio

Definitely buy the Powerball tickets and million to 1 investments in the Roth :)

The wife and I are somewhat early retired at 64 years of age; she stopped at 57 and I stopped at 60. In 2017 I finally bit the bullet and began to move traditions/deferred taxes IRA money into a Roth IRA. My intent is to shelter as much as possible before RMDs at age 70, and to also have monies that will pass to our only child tax-free when that time comes. I debated this for years and recharacterized the money the last time I tried doing this for the first time, but I let it go through after doing my taxes for the past year. Some may say it is foolish to do so at our age, but the desire to be required to take less at 70, and the desire to make it simpler on our daughter, outweighed the negative (paying taxes now).

Take a look at a past Reader Financial Review, where The Bobs are taking on a similar challenge. At this point it is a question of picking our marginal tax rate until the RMD mandates one.

Thank you, sir. Excellent write-up on the link you supplied from 2015. The financial situation is errily similar to our own, which was interesting in its own right. Thanks again for all your help.

You need to include a way to estimate the standard deduction in the future. For example in 1987 (31 years ago) the amount of personal exceptions and standard deduction was about $7,500, for 2018 it is $24,000 for a couple. If the standard deduction keeps up with 2% inflation it would double in about 35 years, so in theory it could be $48,000 in 2052.

I’m not too concerned with RMDs since we are about 20 years out and have time to roll over a good chunk to Roths after we early retire. Also I go by an effective tax rate (not the marginal tax bracket) when withdrawing. For example a 70 year old couple today can withdraw $100,000 from an IRA and have $30,000 of social security, they pay $17,000 in federal taxes (I consider this a 17% rate) which is still lower than the 24%+ marginal tax rate we are paying at the top of our incomes.

Because of the size of our traditional IRAs/401ks I’m happy if we can keep our tax rate at 15% or lower with qualified dividends/capital gains while we are working and in the future with rollovers to Roth IRAs after we early retire.

Forgot to write under the table: scale all numbers by Today’s Standard Deduction / 2018 Standard Deduction. All numbers are real / inflation adjusted.

I too am an effective tax rate guy. If you pay less in retirement than on contribution, that is a win. Still, I’ll look at how to thread the needle as it were.

My husband and I have this “problem”. I’m 58 and he is 61. Right now we are taking Obamacare subsidies, which makes it hard to do Roth conversions. I have recently started to wonder about moving IRA money to cash, just because I can’t figure out why I’m trying so hard to grow this large sum into a larger sum for taxes. I’m just now looking into Donor Advised Funds, and that will probably be the answer. A reason to be motivated to continue building those accounts. I look forward to the follow up posts.

Charitable deductions are one way.

re: growing a large sum into a larger sum for taxes – it is better to have a dollar and pay tax on it, than to have no dollar at all. More is still more.

First world problem. My traditional 401k is okay for now at a little more than $600,000. I hope it continue to grow. I’m 44 so I have plenty of time to rollover to the Roth IRA. The pesky blog income is also another first world problem. We’ll just have to figure out how much to rollover every year very carefully. I’ll start in a few year after Mrs. RB40 retires.

Thanks for this post. This part is particularly useful. Good stuff.

“Furthermore, it would make little sense to pay more tax now (by not making additional 401k or IRA contributions) just to not pay tax later. Don’t let the tax tail wag the dog.”

My life has kinda become a first world problem ;)

I love this topic! Aside from some investing in tax advantaged accounts to reduce my taxable income/taxes, I prefer to invest in other assets. As my retirement income will consist of a lot of rental income, my goal is to limit other taxable income in retirement.

I look forward to the article on minimizing peak tax rates.

I’m pretty sure we’ll get screwed by the RMD monster eventually. If so I’ll slap my 70.5 year old self on the back and congratulate future-self for winning the game and have a half million+ in assets at that ripe old age :)

In the meantime, I’m slowly whittling away at my trad IRA/401k stash but as you mention the growth offsets conversions many times.

So while I might be 0% taxed today, I’ll eventually owe the taxman something if investments continue to do well.

Tax minimization is a good game. When you win, you win. And when you lose, you win.

I too can’t wait for your future posts on this topic. We will be exactly in the situation you describe. Between dividends and capital gains in taxable accounts, trying to maintain the ACA subsidy, maximizing tax free earnings and a planned ladder of Roth IRA conversions, this is quite a puzzle to solve. So I had resigned myself to paying taxes once I hit 70.5 years.

Other than large charitable donations out of our IRA accounts by that time,I just see no way around paying taxes in our situation. We will run out of time before we run out of investments in tax deferred accounts. Not really a problem, except it makes me realize how many years I worked longer and harder than I should have.

I am very excited to see what you have come up with to mitigate/minimize this “problem”. Maybe there is hope. Thanks for these great posts. Keep ’em coming!

Enjoyed this post, looking forward to more! I too have this “problem”, with a pension coming and almost all of our savings in 401ks. I have wondered just how to approach the lifetime tax minimization problem, but I am lazy and feel like it has too many moving parts. Maybe you’ll work up a nice formula I can use.. :-D

Yes, this is an important topic. I am hitting this wall. My RMD is greater than standard deduction.

I had always thought “the more in 401K, the better” but that is not the reality of our financial lives.

Why did I not think about this when I was working?

More money in tax deferred accounts means less cash. To buy a house I really had a lot in tax-deferred accounts and not enough cash. Got the house eventually but it was tight. Cash savings also very important.

Looking forward to the other posts in this series! Thanks to the higher Solo 401(k) contribution limits, I expect RMDs to give me some heartburn down the line. That said, I prefer that to the alternative…

I’m looking forward to this series. As a not so early (semi) retiree, i’m cutting back to 50% work schedule this year at age 63. I’ve been in the 25% marginal tax rate in recent years and have maxed out pre-tax 401k contributions, traditional spousal IRA, and HSA. With reduced work income this year, my goal is to withdraw from my IRA or 401k just enough to keep taxable income at the top of the 12% bracket without moving into the next higher bracket. The amount that is withdrawn will either go into taxable investments or a Roth conversion (and some may go to living costs or tax on withdrawals). I don’t plan to contribute to my 401k this year (except my company safe harbor 3%) since I would also be withdrawing. The idea is to Withdraw IRA funds over the next few years at 12% tax in order to reduce the RMD in my 70s and 80s when We could be in a higher marginal bracket. Current plan is to take social security at age 66, although we could delay a few years if it made more sense to continue the IRA withdrawal (and/or part time work) strategy instead. I’d be interested in your take on how to make that analysis.

This is one of those “great problems to have”. At current trends (same contribution, conservative returns (5%)) I am looking at 2.5 million in my TSP (US Government 401k) by the time I am 62. And on top of that I have a federal pension that kicks in there as well ~50k…. Such a horrible place to be in, where you have too much money to play with (and of course to minimize taxes, etc). The RMD numbers are truly eye-popping when you look at it…

A good problem indeed. I’d much rather have a nice pension and pay lots of tax than the opposite.

Similar question. Age 40, Married filing jointly, two children. Current VA/military pension is $63,000/year total adjusted to inflation annually; $20,724 of it is taxable at the federal level. I will work full time two more years and my tax deferred investments should total about $550K at that point. From age 42 until I begin drawing from these investments, I would like to begin the conversion process.

In retirement, would my annual conversion amount be the $24000 standard deduction-$20,724 in pension income + the amount of child credit or just the standard deduction – the taxable pension?

nice post–thanks.

This is a timely topic and I enjoy your graphs and analysis. I’m pretty early on in the accumulation stage, but have been balancing keeping my taxes near zero even in my working years (agi around $60k, MFJ, 2 kids).

You also showed me a regular taxable brokerage account is just as good as a Roth for someone in my tax situation.

My current employer offers a pension, but I don’t know how long I’ll stick around, but I’m currently vested. In the mean time, I’ll keep my current taxes near zero and try to minimize total lifetime taxes.

Thanks for a great post.

Thanks for the detailed work on this!

Do you give any thought to diversification of the tax risks associated with policy changes?

Not really, no. 100% of the time I’d take tax deductions/benefits now vs speculating on what might be.

I hope you are going to talk about I-ORP in your series. That analysis has been a huge help in smoothing out our tax brackets. When I started looking at this “problem” we were facing a hump of very high taxes in our mid 80s. Now, we are looking at a much smoother picture, and plan to continue our conversions until age 70 so we can snuggle down a bit more in taxes owed over our lifespan.

Also please consider using an HSA HDHP tax deduction to increase IRA to Roth conversions by $3450/$6850 single/family (year 2018). HSA’s are not subject to RMDs and can be withdrawn penalty free after age 65 for any purpose (subject to taxes), and of course medical expenses are completely tax free.

Where is the second post in this series. Please get off your ass and post it:). I need this god damn info already. Its like crack-cocaine. Thinking you need to rename yourself Go Curry Crack Cocaine!!

Alas, I’m a little busy eating pintxos and drinking wine at the moment… maybe in September.

All kidding aside, are their additional articles in this series? I have read this one about 4 times and I am craving more.

Not yet

I’ve also been checking back and waiting for these forthcoming articles…

Me too. These are on my to do list, but I’m retired, sorry.

This is a lot more confusing than air quality. Thank you, though.

A lot more fun too :)

Anyway you can un retire for a brief moment one evening? Still waiting 😁

Sure, here you go.

[I did it 2 weeks ago ;) ]

Thanks very much for writing this! As a recent early retiree, I stumbled across this article as I was trying to figure out what an optimal conversion strategy would look like. Instead of trying to minimize lifetime taxes would it be more ideal to try to maximize the amount converted and subsequently grown over a lifetime? I’m not sure that these are the same, though I may be confusing things.

Yes, ultimately you want the largest after-tax value. Fortunately, lifetime tax minimization and maximizing the amount converted are one and the same for Roth/Traditional accounts except in extreme cases (e.g. you buy a lottery ticket in a Roth account and win $100 million.)

Thanks, I think I figured it out. It’s not at all what I was initially planning to do so I’m glad I came across this article albeit a couple of years after it was written. Thanks again!

One way to mitigate the impacts of an oversized 401(k) plan is to utilize net unrealized appreciation, if you own employer stock in your 401(k). By arbitraging your ordinary income and long-term capital gain rates, you can transfer out large chunks of appreciated employer stock out and potentially never pay taxes on the gains within your lifetime!

Hi Jeremy,

Should I invest my Roth IRA into different funds / indexes or how do I just let it invest itself in a retirement account?

Thanks.

Hi John. You can pick index funds and set it up to auto-reinvest dividends.