What if somebody gave you an interest-free loan for a year? Say, the government, maybe. And then instead of requiring you pay back all of the loan, they only wanted half?

This situation actually exists within the Affordable Care Act / Obamacare in some circumstances. Throughout the year, Premium Tax Credits are paid directly to the insurance company based on our estimated income for the year. Then come tax filing season, we reconcile any differences – if our actual income is greater than estimated, we repay the excess on the advanced credits.

For the self-employed, seasonal workers, and retirees living off variable investment income, estimating income accurately can be next to impossible. As such, to provide some protection against unexpectedly large tax bills, as long as total income is less than 400% of the Federal Poverty Level (FPL) the amount of repayment is limited.

And those limits can have profound implications.

Obamacare Advanced Premium Tax Credit (APTC) Repayment Limitation

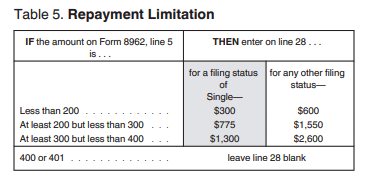

In the instructions for IRS Form 8962 (pdf) there is a nice table that outlines repayment limitations for excess advanced premium tax credits.

Here is the table for tax year 2018:

(2019 numbers slightly higher, but documents are still only in draft form.)

Line 5 of form 8926 translates total annual income to a percentage of the Federal Poverty Level. A non-single filing household with income of between 300% and 400% FPL might have to pay back at most $2,600, even if they underpaid premiums by $5,600, for example.

These repayment limitations mean there is an effective 0% ACA related tax rate on a range of incomes.

Here is a chart I’ve shared before, showing ACA premium reductions with increasing income for household size = 3 (2018 numbers.)

ACA Tax for a Family of 3 (dollar amounts different for other family sizes, but shape the same)

And here is what it looks like when the repayment limitation for the “At least 200 but less than 300” row in the table is reached around 250% FPL.

At 300% FPL, the repayment limitation jumps by an additional $1,050, which is a sort of additional subsidy cliff (shown as a $1,050 impulse in the chart.)

ACA Repayment Limitations create an effective 0% tax rate for a wide range of income

The repayment limit means additional income results in no reduction in tax credit (not required to repay the APTC), which is equivalent to a 0% tax rate.

(Hypothetical) Repayment Limitation Example

When I was exploring the tax / health insurance premium impact of moving to California, I estimated we would have income from dividends and interest of about $40,000/year, which is roughly 200% FPL for a family of 3. The remainder of our budget would come from selling stock, which could increase taxable income via realized capital gains.

If during annual health insurance enrollment in Q4 we estimated our annual income for the following year at just under 400% FPL, we might pay ~$7,600 for a Silver level insurance policy with high copays and a high $12,000 deductible.

But if we estimated our annual income at $40,000, then our insurance premiums would be only ~$2,000 and we would have a deductible of only $1,300.

Then, maybe on December 31st, I realize a capital gain of ~$40,000.

Since income was much higher than estimated, nearly 400% FPL instead of 200% FPL, we would be required to repay some of the advanced premium tax credits. But the ACA repayment limitation would cap this at $2,600. The cost-sharing subsidies never need to be repayed.

This chart has been shown before (in the post Harvesting Massive Capital Gains), where additional income beyond $40,000 for a family of 3 is taxed 3-fold (US Federal tax, California State tax, and ACA tax.) In most of the range of $40k to $80k income, taxes are 17%+.

And here is the same chart again, this time with the repayment limitation. The effective tax rate and total tax lines from the first chart are included for reference. In this case, tax rates above $40k are less than 15%

In this second chart, pay attention to the purple “Tax w/ APTC limits” line… as income increases above $40k we repay some of the advanced premium tax credit, up until the 200-300% limit is reached. At 300% there is a jump of $1,050 to the next threshold. (Throughout this range, California tax of 4% – 6% would apply.) Going over 400% FPL would require 100% repayment of all subsidies.

In Option A, we pay $7,500 in insurance premiums with a deductible of $12,000.

In Option B, we pay $2,000 in insurance premiums, $2,600 in premium repayment, and have a deductible of $1,300.

Option B saves $3,000 in premiums and over $10,000 in deductible, if applicable.

Option B is definitely the way to go then, right?

Well…

Rules, Requirements, Implications, & Penalties

I’ve been asked about this topic numerous times:

“I’ve had some unexpected income late in the year, and now my annual income will be significantly higher than I estimated due to:”

- an additional client,

- dividend increases and special dividends,

- unplanned expenses that required the sale of stock

- side hustle accidentally made extra income

- etc…

“What do I do?!”

No worries here at all. Our best plans change. The rules were followed, so everything is fine.

Report the change to your State or Federal Exchange as soon as you know that income will be higher. This can be done as often as you want. They will respond with a redetermination notice, which is basically an adjustment to premium tax credits.

The implications can be long-lasting. Higher income this year might increase expectations on the part of the Exchange for higher income (and higher premiums) next year, thus preventing you from benefiting from cost-sharing subsidies. (In theory, I’ve not seen an example of this having happened.)

There is definitely a (perverse) incentive to estimate income on the low side.

Therefore, expectedly, the penalties for abusing the repayment limitations are severe: (legal text)

- knowingly and willfully providing false information.. may be subject to a maximum civil money penalty of $250,000 for each application

- Failure to provide correct information … where such failure is attributable to negligence or disregard of any rules or regulations may be subject to a civil money penalty for each use or disclosure of not more than $25,000

So, it is best to avoid giving the appearance of anything untoward.

But if income was going to go above a threshold anyway (so repayment is already limited), I wouldn’t hesitate to harvest gains up to the next beneficial threshold. But I would definitely avoid doing this repeatedly or making a pattern of it.

Summary

Obamacare / ACA tax credits are paid in advance based on estimated income, then reconciled the following year at tax time.

If actual income is higher than estimated, repayment of the advanced credits may be limited. This has the effect of creating a 0% tax region up to 400% of FPL.

If income is going to go above a repayment threshold anyway, there may be some opportunity to harvest some gains at a 0% Federal / ACA tax rate.

In practice, it is probably best to estimate income a little high, but in the event that income is significantly higher than expected report changes to your Exchange to redetermine ongoing advanced premium tax credits.

—

For a detailed exploration of the ACA / Obamacare, and how tax credits are related to income, be sure to explore these two classic posts:

Request for Real-World Examples

Have you had some interesting experiences with health insurance premiums, tax credits, and fluctuating/unpredictable income?

A hypothetical here…Say a person was 55 years old, had a brokerage account of 2 million with about 800,000 in basis. I’m wondering if a person could pull 100,000 per year in basis out of their account (zero income earned), would they still be able to qualify for the entire tax credit given they have no income? If so, they could do this each year until age 63 before starting to draw out capital gains income as well as medicare. Thoughts on this?

Unlikely. Any time you withdraw from the brokerage account, unless the funds are just sitting there in cash, a portion of the sale will be basis and another portion will be a realized capital gain. If the stock has doubled since purchase, half of the sale is a capital gain, for example, so 50k basis 50k capital gain on a 100k withdrawal.

There is a good reference chart in the post Long Term Long-Term Capital Gains.

We did this exactly in 2018. Started out the year at our normal 40k-ish AGI like we’ve had for the past several years. Got the subsidies, cost sharing reductions, etc.

Then late December I realized I needed some cash and wanted to bump up cost basis while I was at it so that my CGs are lower when the kids are in college. Oops – busted right through the 40k AGI target and ended up with an AGI of 299% of FPL. I had no problem when certifying income for 2019. They didn’t even question it. And so far we are on track to hit 40k AGI this year (as long as I do some conversions to generate enough income to get up to that threshold!).

I imagine if you did this every year (certify low income, end up with much higher income) then you might run afoul of their rules. Also can’t act in bad faith knowing what you’re doing. But even the best of us tax geniuses can’t plan out our financial moves several years ahead with any high level of detail as you don’t know what the market will do, how tax laws will change, what unexpected income you’ll receive, etc.

It would probably be weird if you didn’t hit the repayment limitation at least once every 2 to 3 years, right? I mean, who knows what will happen at the end of the year.

What happens if your income is lower than estimated? If you fell below the limits to get subsidies for an ACA plan, do you have to switch to Medicaid?

Yeah, Medicaid. But there is a weird spot between 100% and 133% FPL where some States have expanded Medicaid and some have not.

For an early retiree, doing a Roth conversion to force income sufficiently high to qualify for subsidies is probably a good choice.

Yeah, we’re early retirees, so planning on a Roth conversion if needed. Do the rules require you to switch to Medicaid mid calendar year if your income falls below the FPL limits? I can’t seem to find a reliable answer.

Not sure what you mean… If you estimate in Nov for enrollment, and then somewhere in the following year you realize you won’t hit the minimum income required to be eligible for subsidies, then yes you are supposed to notify the Exchange and switch to Medicaid.

Great, that’s what I was wondering, thanks!

I’ve got a good one. Retired client didn’t understand sign up process and claimed $0 income with decent coverage so claimed a $9,000 advance of PTC. End of the year comes and mutual funds have larger than usual distributions this year. Income goes to >400% of FPL for 2018 by $200, has to repay the entire $9k. September comes and we receive a corrected 1099 with $500 less income. Saves him more $6k in tax.

That is a serious emotional (and financial) roller coaster.

I only hope the Affordable Care Act stays in place. We could really use it, my husband could quit his job, and we would be okay…but in this political climate, I’m terrified of them taking it away….because odds are we will NOT be able to find another job where we live with good healthcare benefits. (he works for local government right now) I’ve literally been looking for a full time job (clerical) for over a year, and not gotten anything except a few interviews. We’re both in our 50s…..that may have something to do with it…I’m ready for FIRE, I have a nice part time job for supplemental income…..but it’s all about health insurance

Sorry :(

The health insurance system in the US is really messed up… I too am unsure what is going to happen, but I’m not optimistic in the short term.

Very interesting – thanks for sharing. Moral of the story: To avoid the $25K fine, notify the feds as soon as you know you know you’ll make more income than estimated.

Probably, but I imagine this has a low enforcement rate. It’s also a little weird if the income comes on December 31st, for example. You only have one day of coverage remaining on the existing plan, and you’ve already enrolled in the following year’s plan based on estimated income.

Great article, as always!

Let’s say someone were to early retire in, say, the month of April of a particular year and then look to purchase a plan on the Exchange. Being the previous fall enrollment would have past, and the individual didn’t predict his/her income for the current year to support the ability to obtain subsidies, what would then happen?

Specifically, how would subsidies/the cost of plans be determined?

Subsidies are based on the calendar year income. So if 4 months of work pushes you above 400% FPL, no subsidy this year.

Leaving a job means loss of other health coverage, presumably. This qualifies you for a Special Enrollment Period under the ACA, so you would just enroll at that time.

This is absurd. It’s analogous to the government rewarding the underwithholding of taxes. If, when filing in taxes in April you find out that you underwithheld $10k, it’s like the government saying “you only owe us $5k because you were bad at guessing.” Unsurprisingly this would create a massive incentive to underwithhold taxes.

As an aside, when I compute the marginal tax rate on $1 of income that puts you over 400% of FPL, I compute something on the order of 1,800,000% (=1500 subsidy / month for large family * 12 months / $1 of income). I tried to write a research paper using IRS data understanding people’s behavior around a 1,800,000% marginal tax rate but the IRS didn’t select my proposal. Oh well.

It is weird, yeah…

Super interesting article. I don’t know how good the ACA plans are in California, but the plans in Texas don’t seem to be worth much. My daughter was looking at plans, so I called about 15 pediatrician offices in the DFW metroplex and not one accepted any ACA plans. I also couldn’t find any hospitals that accepted them either. Ultimately, my daughter stayed with COBRA, but will have to find an alternative soon. The best alternative appears to be the medical cost sharing programs.

Good luck. I recommend more research.

Re: medical cost-sharing. Spot on. We live in Brownsville, TX. I’m self-employed with a family of 5 and we have had a good experience with Altrua Healthshare. There are several options so make sure you do the research for your specific situation. If you squint, our plan is catastrophic coverage with a per person deductible of $2750 and we pay $260/month. I say “squint” because it’s not technically insurance hence that amount isn’t called a deductible.

I had heard different things about ACA plans and was concerned because all of the plans in my state are the same companies that have Medicaid plans – no standard commercial payers. But after checking with our current medical providers, we had a couple of options that included our primary care, specialists and hospitals. So definitely something that varies and should be explored.

I have the ACA in CA and I’ve had no problem with finding providers, there were lots of different plans to choose from, and I didn’t even have to change my OBGYN, although oddly enough under my prior plan she was also my PCP, but under my new plan I have to have a GP as my PCP. I do have the option of changing to one who is only 5 minutes away instead of 30 minutes away, but I’m sticking with the one I know & like and have been going to for many years. It has never occurred to me to call offices and ask if they take the ACA – before I select my plan, I go to that insurer’s website and search for which doctors/offices near me take it. SO much easier that way!

For folks just starting out on ACA–with a big ‘ol income from 2019;)–do you know if they evaluate your previous year’s income to determine your subsidy OR do they ask for a 2020 estimate of income, now that you are self-employed/retired?

We’re financially planning for premiums next year(our first retired year)–so if they look at 2019 we wouldn’t get a subsidy, but if we estimate for 2020…we sure would:) Appreciate your help here!

2020 estimate of income.

Yay and thank you:)

We have been playing this game for the last few years. Engineering MAGI to 136% of FPL to maximise silver plan cost sharing reductions (excellent deductibles!). We have an established/consistent tax record of low income (<$24k/yr) – but it comes down to what you estimate upon ACA enrollment year. I tease out the specific $ cutoff by ratcheting down my income estimate until it shunts me into medicaid, then round up a few hundred bucks.

Speaking of Medicaid, we played that game for a year – and deemed it not worth the effort/reporting, instability, and stress of "trusting" that the coverage is actually there. Most of this is do to understaffed bureaucracy, outdated monthly reporting methods, and slow communication. The whole process feels punitive and insecure, certainly not preferred for savy FI'ers. I'm a proponent for a robust and easily administered safety net for all citizens – and by my minimal experience, medicaid is not. I'll leave it for those that have no other options.

Thanks for the discussion of how to handle/report an unplanned gain – I expect my parents will not zero-out their estate and there will be some leftovers that upset my current strategy.

It’s interesting that ACA subsidies are based on calendar year income, but Medicaid only looks at monthly income. For example, you could earn $20K/month, for the first 11 months of the year, and if you quit your job on November 30 and applied for Medicaid on December 1, all the Medicaid people would want to know is, “How much is your income?” To which, you could truthfully reply, “$0,” or if you had investments in taxable accounts, you would have to estimate dividends and interest, but that’s it. So far, our experience using Medicaid during FIRE has been great. It costs $0/month, and when we’ve needed to use it, it’s paid 100% of our medical bills. No co-pays. No deductibles. It seems too good to be true, but so far it’s working for us. If things change in the future, we’ll adapt.

A problem with using Medicaid is finding a provider that is in your particular state’s Medicaid provider network if you are out-of-state due to travel. I believe that Federal law says that’s not a problem but the reality is that there is a lot of paperwork involved in a provider enrolling in Medicaid and so they’d rather just bill the person if they aren’t already enrolled with that particular state.

Last summer, before spending three months traveling across the country by car, we contacted our previous state’s Medicaid office to ask about coverage while enroute from one state to another. They told us we would be covered for emergencies only. In the event of an emergency, they recommended we go *only* to a hospital emergency room, not an “urgent care,” and they said Medicaid would pay. Luckily, we never got to test that out. As soon as we established residency in our current state, we applied for Medicaid. When we got the acceptance letter and medical cards in the mail, we called our previous state and cancelled our Medicaid coverage there.

Thanks for your comment, Shane. My state’s Medicaid office said they would try and work something out if I were out-of-state but I may have to pay. Not sure if that includes ER visits. I wish I could get a written policy on this and information on the likelihood. So a worry.

This is from an AAPC billing forum:

If you send a bill to an out of state Medicaid, they will require you to fill out all the paperwork to become a participating provider before processing your claim. I know we went through this with Medicaid of NY. They kept sending the paperwork back for various reasons, taking months to process it and reject it and return it to us. By the time we finally got it all settled, they denied the claim as past timely filing. We have never, ever billed an out-of-state Medicaid successfully. We bill the patients. All of our charges for these are inpatient so we have no choice but to see the patient and the physicians have no way of knowing the patient has out-of-state Medicaid anyway.

GCC, since you are planning to (maybe) move to California, you may or may not have heard that the state passed a new law that boosts the ACA subsidy to 600% of the federal poverty level 2020, 2021 and 2022. Basically the state covers the difference between the 400% federal subsidy and the new CA 600% limit. There’s no guarantee the state will extend that program beyond 2022, but the they love to spend money when they have it.

Hopefully, the expanded subsidy is good at least until the next recession when then state’s tax receipts take the typical nasty dive (since they rely heavy on taxing the highest earners and the new governor is angling to eat up the ‘rainy day’ fund that the previous governor protected).

Thanks Bill!