(GCC: I am often asked, “Do you know any good CPAs?” and “What are some good tools for doing my taxes?” I never thought both questions could share a common answer – Kathryn from Making Your Money Matter is a CPA (who gets it) who has developed some very cool tools for doing taxes (and more) that cost less than an hour with a CPA. Disclaimer: links in this post are affiliate links.)

I remember the first time I found Go Curry Cracker and read one of Jeremy’s blog posts going through his tax return in detail. It covered his then-recently filed 2015 tax return, with over six figures of income and still no income tax due (only a small amount of self-employment taxes).

I’d like to say that I—a CPA—was intuitively able to do a quick review of the numbers and figure out pretty fast how this worked out. However, I had to pull out a pen and paper and calculate it by hand just to make sure it made sense.

Each spring since, I’ve looked forward to the annual tax return reveal. (GCC: 2021 tax return coming soon!)

If you have ever wondered, How can I optimize my taxes in the same way… without all the hassle of becoming a tax nerd first, well… have I got a tool for you.

Optimize Like a Tax Nerd

I’m always looking for ways to completely optimize my life, and especially my personal finances. This was one area I knew there was room for improvement. And while I’m not able to completely eliminate my own income tax liability as Jeremy manages to nearly every year, I’ve created some in-depth resources to help optimize my entire financial life, and of course, taxes are a huge part of that.

When I said I liked optimizing my finances, what I really meant was that I was crazy enough to spend thousands of hours over the past few years putting together an Excel-based personal finance software because I couldn’t find anything that was as comprehensive and tax-optimized as I was looking for.

Each of the main areas I focus on has some type of tax impact:

- Cash Flow Analysis

- Net Worth

- Debt & Credit Management

- Federal & State Taxes

- Insurance

- Saving & Investing

- Retirement Planning

- College Planning

- Estate Planning

They say you learn more when you teach than when you’re the student, and I would say it’s 10 times even more true when you build something from the ground up. I’ve learned more about optimizing taxes creating this workbook than in my entire career as a CPA.

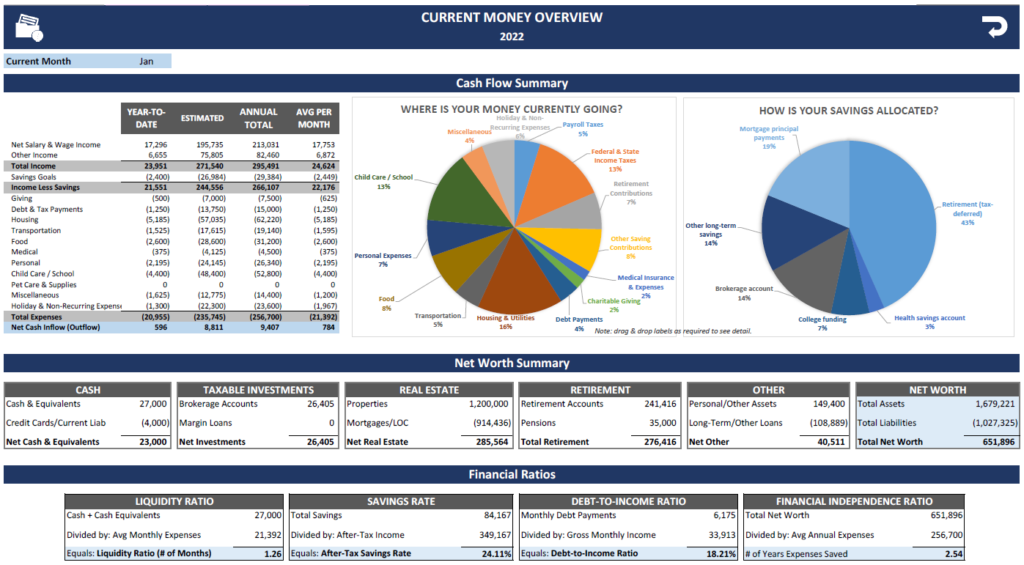

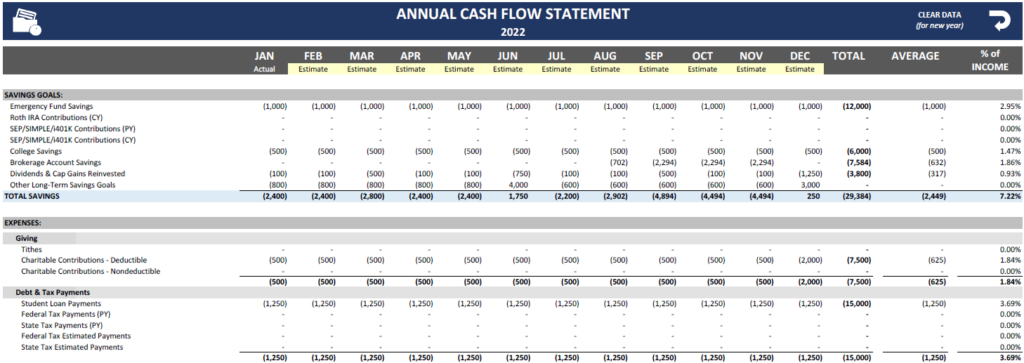

Here are some tips on how you can optimize your taxes this year by taking a comprehensive view of your personal finances. This shows my own tax planning tool, but these will all apply regardless of how you choose to manage your finances.

START WITH TRACKING YOUR INCOME & EXPENSES

Have you ever filed your tax returns and then remembered another deduction you forgot to include (don’t do this to your CPA, mkay!)? Or scrambled at the end of the year to try to get your charitable contributions together finally just figuring you’d total up what you could easily find and hope it was pretty much all of them?

The best thing you can do to make sure this doesn’t happen is to track these things throughout the year. I’m a firm believer in tracking expenses anyway (budgeting is optional). Aligning my income, spending, and saving categories with the information I need for tax projections and tax filing has saved me a considerable amount of time (and money!).

Note: You can get a list of my tax-optimized budget categories for free here.

In addition to identifying tax deductions separately, I also believe that it’s essential for employees to break out payroll deductions as well. This gives attention to what are often some of your biggest expenses (tax withholding, health insurance, etc.) and allows you to easily pick those key numbers out for tax planning purposes.

MONITOR YOUR ADJUSTED GROSS INCOME THROUGHOUT THE YEAR

You’ve likely heard the saying “don’t let the tax tail wag the dog”. I mean, most people (ahem, I guess myself excluded) aren’t constantly thinking about money and taxes. Daily life is first, then a whole lot of other things, then trying to optimize their taxes.

But, at the same time, information is knowledge and with a little tax planning, you may be surprised by the opportunities available to pay less to Uncle Sam.

Consider the following tax credits (and there are others as well) that are directly affected by your income:

- Stimulus payments

- ACA Subsidies/Premium Tax Credit

- Earned Income Credit

- Child Tax Credits

- Dependent Care Credits

- Retirement Saving Credit

- Education Credits (American Opportunity Tax Credit & Lifetime Learning Credit)

If your income is close to the thresholds to take advantage of these credits, it’s possible for that extra income to actually cost you money overall like a couple of the situations described here.

A few simple ways to lower your taxable income include:

- Switching from Roth to Traditional 401K contributions

- Contributing to a deductible IRA account (if your income allows it)

- Tax-loss harvesting

- Accelerating business deductions (for those filing Schedule C)

By completing tax planning throughout the year, you can monitor your situation to make better tax-optimized financial decisions.

TAKE A LONG-TERM VIEW OF YOUR TAXES (GCC: Lifetime Tax Minimization!)

Don’t focus solely on your current year’s tax situation, though, or it could cost you many thousands of dollars over your life. Here is a short checklist of things to review:

Passive Investment Income

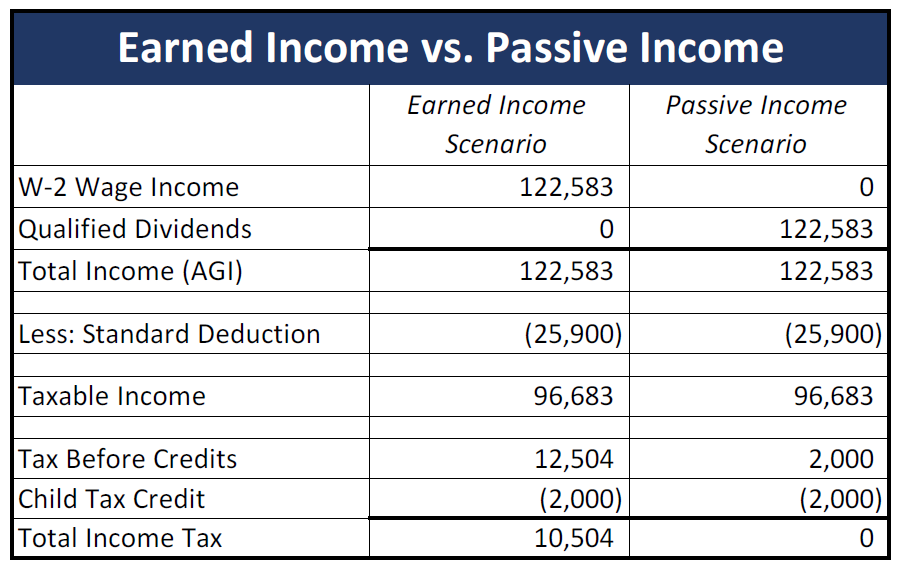

Do you know how Jeremy is able to achieve a zero tax liability? It’s the nature of the income. Certain types of investment income are preferentially taxed in the US. There’s a 0% tax rate (it doesn’t get any better than that!) on qualified dividends and gains on investments held for more than a year if your income is under a certain amount.

Here’s an example: Assume Bob has $122,583 of taxable wages for 2022. Betty also has $122,583 of income, but it’s entirely qualified dividends from her portfolio (coincidence, I know!). They’re both married with one dependent. How are they going to be taxed on that income? Well, I’m glad you asked.

Not only does Bob pay $10,504 more in income taxes than Betty, but he’ll also have at least $9,378 of FICA taxes on those wages.

This supports having a high savings rate so that you can shift your income from the least efficient (earned income) to passive investment income, which is taxed at a much lower rate.

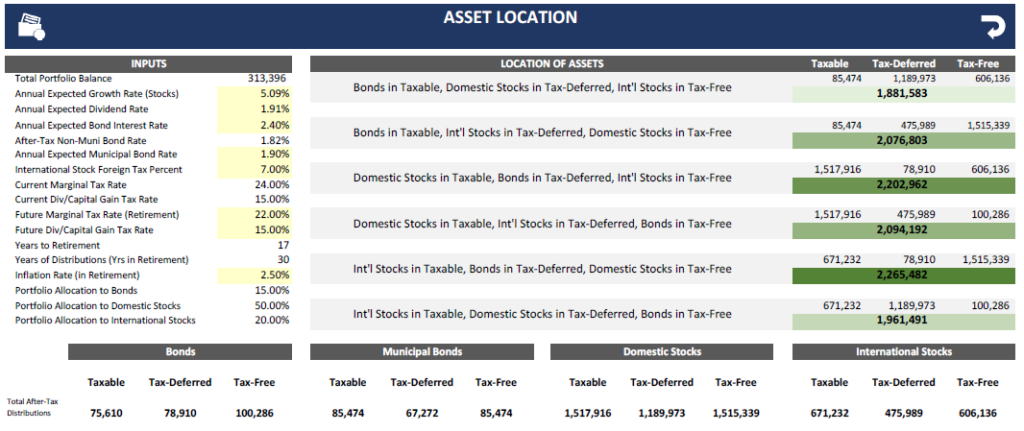

Tax Location

Where you keep your investments matters. Even in a modest portfolio, it can make a difference of nearly a hundred thousand dollars.

Of course, the ideal situation is to have as much money in Roth accounts as possible as they grow tax-free and are also tax-free when withdrawn after age 59 ½. Generally, your highest expected growth assets (in the past this has been stocks) should be kept in these accounts.

Roth Conversions

Roth conversions are an important tool to give you more of this valuable Roth space where you can keep some of your highest expected growth assets.

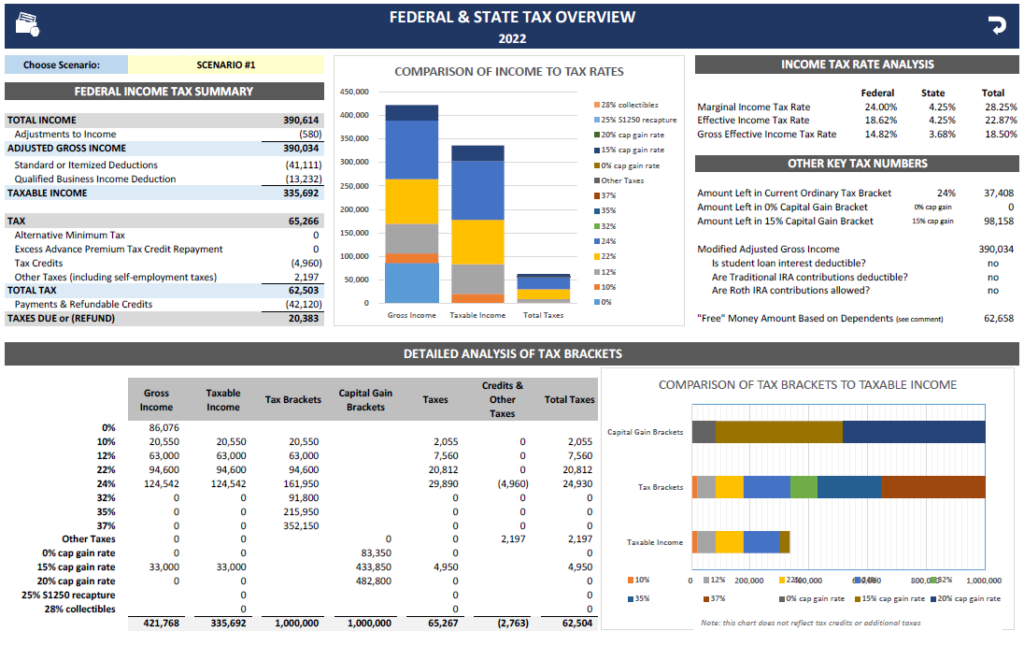

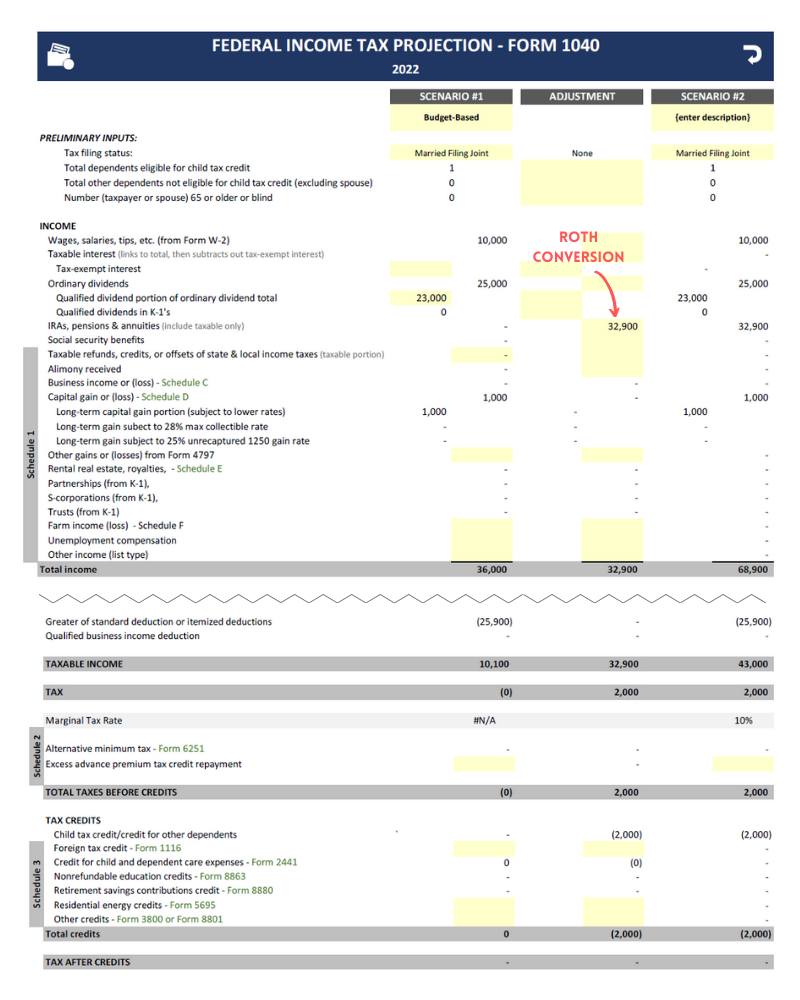

Let’s go through a quick example of someone optimizing for Roth conversions for the year that wants to pay zero taxes. We’ll assume Fred is a married, early retiree with one dependent that only has wage income for the first month of the year. He has $10,000 in wages, $25,000 in dividends ($23,000 qualified) and $1,000 in long-term capital gains this year.

The first step would be to run a base scenario without that additional Roth conversion income. This is shown in Scenario #1 in the image below. The result is zero tax due, but there’s some money left on the table for sure.

We can then add an IRA adjustment to reflect the addition of a Roth conversion that populates Scenario #2. Through some trial and error (or Excel’s solver function), we can easily figure out that Roth conversions of $32,900 are the sweet spot for paying zero taxes and optimizing the full child tax credit.

Retirement Distributions

Contributing to tax-deferred retirement accounts is another great way to reduce tax drag on your investment returns in the long term.

However, it’s not uncommon for super savers to approach retirement age and realize they have way too much of their savings in tax-deferred accounts. Often, if they want to keep up their current lifestyle, they’ll be at the same tax rate, or potentially even higher rates when required minimum distributions kick in at age 72.

With some decent planning, you can optimize both your taxes now and your future retirement income to avoid this problem. And, the sooner you start the better!

This is another place where Roth conversions come in, so you can ideally have most of your tax-deferred account distributions covered by your standard deduction and sell investments at a capital gain rate of 0%, all while being able to meet your cash flow needs by buffering those additional distributions with tax-free funds.

A FINAL NOTE

If you’re looking to optimize your financial life, and especially your taxes, you can check out the following links for more information about the Personal Finance Bundle:

- Details, screenshots, and FAQ’s

- Tutorials that show each section individually (currently a work in progress!)

- Additional free resources like financial goals and creating a financial plan

For less than the cost to hire a CPA for an hour of tax planning, you can get this tool to help guide you in your 2022 tax-optimization decisions.

How does passive income effect the MAGI? And will this impact the ability to obtain ACA credits?

Great question! MAGI is defined in different ways depending on the purpose of the calculation (Social Security, ACA, IRA contributions, etc.), but passive income is a component in essentially all calculations of MAGI. Yes, it will directly impact your ability to obtain ACA subsidies. Here’s a great source that shows income included for ACA purposes:

https://www.healthcare.gov/income-and-household-information/income/

Assume the same for Royalties (as part of MAGI and therefore affecting ACA)?

Yes

I’d be interested in a tool that would let me calculate the optimum drawdown/Roth conversion strategy (total tax burden as the years go by, investment return differences depending on where we take money from first, that sort of thing).

I’m retiring in a year with a lot of moving parts (pension, retirement accounts, spouse still working), and this is one area where I know I don’t have an optimized strategy.

I tried to purchase this but the coupon code GCC2022 didn’t work for me. Any ideas?

Also, is V4 for 2022 tax year?

The coupon code expired at the end of January, sorry.

v4 reflects current legislation, so 2021 and 2022 tax returns.