Physically Present (photo credit)

A great number of world travelers utilize the Foreign Earned Income Exclusion to keep up to $102,100 in income out of the paws of the IRS (2017 tax year.)

For those who aren’t bonafide residents of another (non-US) country, this requires passing the Physical Presence Test (PPT) by being in a foreign country or countries for at least 330 days.

2017 is the first year we tried to pass the PPT, and getting it wrong by even one day could cost $20k or more in tax. Needless to say I wanted to get it right.

Physical Presence Test

As with most things in the Internal Revenue Code, what could be simple and elegant is… not. The IRS even uses the phrase “physical presence test” in the definition of the Physical Presence Test. Nice!

Here is the definition and nuances from Publication 54: (emphasis throughout is mine)

To pass the physical presence test requires being physically present in a foreign country or countries 330 full days during a period of 12 consecutive months. The 330 qualifying days do not have to be consecutive.

Full day. A full day is a period of 24 consecutive hours, beginning at midnight.

Travel. When you leave the United States to go directly to a foreign country or when you return directly to the United States from a foreign country, the time you spend on or over international waters doesn’t count toward the 330-day total.

Passing over foreign country. If, in traveling from the United States to a foreign country, you pass over a foreign country before midnight of the day you leave, the first day you can count toward the 330-day total is the day following the day you leave the United States.

Change of location. You can move about from one place to another in a foreign country or to another foreign country without losing full days. If any part of your travel is not within any foreign country and takes less than 24 hours, you are considered to be in a foreign country during that part of travel.

In United States while in transit. If you are in transit between two points outside the United States and are physically present in the United States for less than 24 hours, you aren’t treated as present in the United States during the transit. You are treated as traveling over areas not within any foreign country.

I tried sorting through this using our own travel.

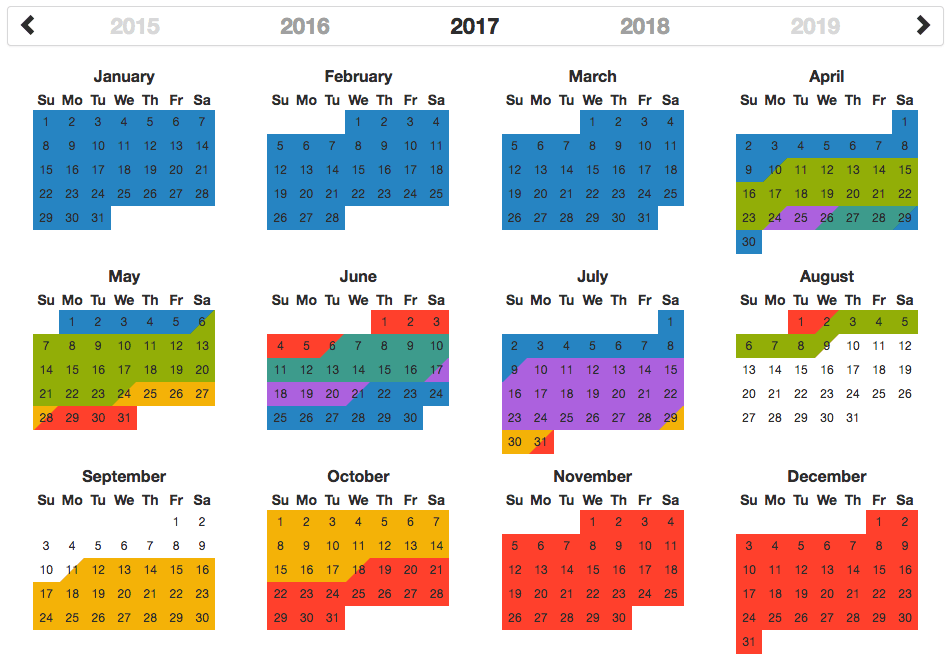

GCC 2017 Travel

We used the calendar year for our period of 12 consecutive months, since it conveniently aligns with the tax year.

We were physically present in Taiwan to start 2017 and flew from Taipei to Paris on April 10th, via Hong Kong. (With miles, of course.) We were traveling from one foreign country to another, and total travel time was less than 24 hours, so we were considered to be in a foreign country throughout the trip. Our first full day in France is April 11th (starting at midnight on April 10th.)

For the next 4 months we bounced around Europe, spending 90 days in the Schengen region before moving on to Croatia, Bosnia & Herzegovina, and Montenegro. All border crossings were within a foreign country, aka valid transfer days.

On August 9th we flew from Dubrovnik to NYC, via London. Sadly, I had to pay for this flight. Again, travel time was less than 24 hours, but this time we were flying to the US so time over International Waters doesn’t count. Even though we arrived at 8 pm, August 9th counts as a day in the United States / NOT in a foreign country.

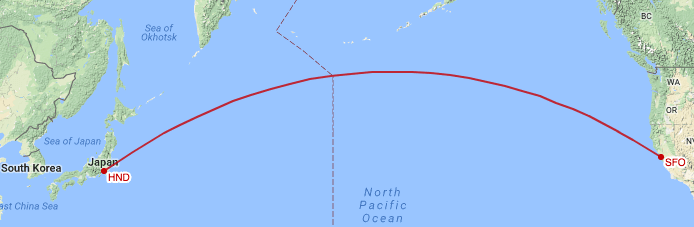

A month later on September 10th we left the United States for Japan, flying from SFO to Haneda. (Total cost: $5.60 per person.)

The entire flight was over International Waters, so we didn’t benefit from flying over another country before midnight. Even though we arrived in the afternoon on September 11th, our first full day in Japan was September 12th.

Great flight route map from greatcirclemapper.net

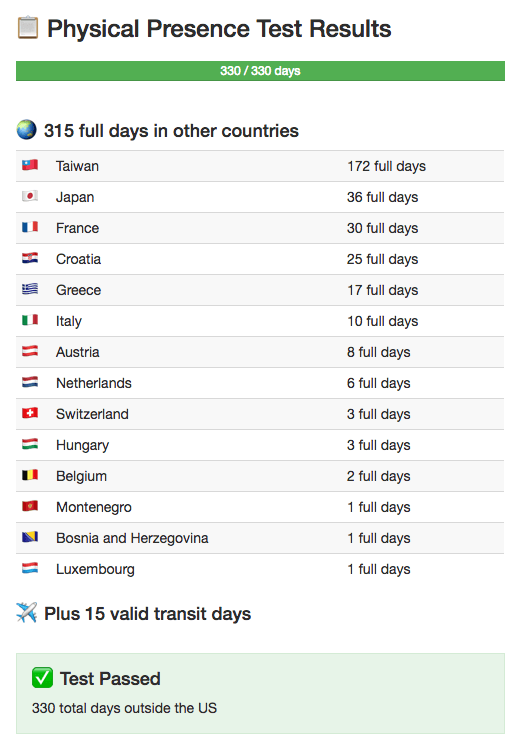

Adding up the days, we were physically present in foreign countries for exactly 330 days. Good thing our flight wasn’t delayed…

FEIE Calc

In the process of trying to figure this all out, I discovered my new favorite web tool, FEIE calc. It makes cool primary color calendars of your travels and calculates PPT days.

Test passed!

A Minor Freak Out on The High Seas

Whilst crunching the numbers on the PPT I spent a few hours convinced we failed the test and were doomed to pay a ton of taxes this year.

See, we went on a 10-day cruise to Alaska. Last I checked Alaska is in the United States, but cruise ships like to spend time in International Waters so they can get casino revenue. After much googling, it turns out International Waters start just 12 miles offshore.

Transit time from SF to Ketchikan, Alaska is 2.5 days (over 24 hours) so we were effectively not in the US and not in a foreign country for a few days. “Oh no! We lost PPT days!”

10 day Alaska Cruise

International Waters = Outside Territorial Waters @ 12 miles

Fortunately we had already reached our 330 days based solely on the inbound / outbound dates to the US.

Had this cruise been traveling between 2 foreign countries, however…

Had I royally screwed the pooch, we could choose to segment the year as highlighted in this post on how nomads can avoid ACA penalties. This would just limit options if we chose to visit the US over the coming 12 months.

Notes to Self

Since I’ll be working to pass the PPT again in the future, here are the things I want to remember for 2018 and beyond.

- Westbound trans-Pacific flights lose 2 days from West coast.

- Departures to Asia from Minneapolis (near family) cross the Canada border, saving a day (I assume)

- The flight from SF to Japan was more stressful than it needed to be. Plan a buffer day or two in case of flight problems / delays.

- Don’t go on cruises. We aren’t cruise people, and International Water days are annoying.

- Don’t connect in the US if it can be avoided.

- Don’t do math at 2 am (see A Minor Freak Out.)

Over the Canadian Border and Across the Sea to Grandmother’s House We Go

Summary

Nomadic people need to pass the Physical Presence Test in order to claim the Foreign Earned Income Exclusion. This requires being physically present in a foreign country or countries for at least 330 days.

There are numerous minutia related to crossing borders when flying into and out of the US, as well as spending time in International Waters. It is important to be aware of these details, as even a 1 day error can cost major dollars. Using a tool like FEIE calc can help with planning while avoiding undue math related stress (and taxes.)

Do you file taxes in your home country (taiwan)

Not really related to the PPT, but yes, we will this year as we have Taiwan sourced income.

This is so cool – so I get to travel the world and not pay taxes up to ~100k? Sounds like a blast.

Is it 50k for single people and ~100k for married?

Sounds better than the LTCG 15% rule for 0 taxes in a year, plus you get to visit so many cool places!

Kinda… the 0% tax rate on qualified dividends and LTCGs is separate from the potentially 0% tax rate on earned income, although they do overlap.

It’s $100k per person

Nice job. I also—carefully—spent exactly 330 days outside the US in calendar 2017. The rules are a bit of a headache to figure out but once you’ve done it once it’s not so bad. I like to make sure that all my outbound flights pass over Canada before midnight.

The more time-consuming part every year is parsing out just what income was earned during the days spent in the US, because that income is not tax-exempt.

I’ll do that calc a bit for this year’s tax post, but it would also be reasonable to visit the US solely for vacation

Those of us still in the rat race get paid vacation, paid as it’s taken. ;-)

I’ve seen people justify that vacation pay is separate. Consult your CPA blah blah blah

We tried the 330 days out of the country to avoid the (n)ACA (non Affordable Care Act) to avoid the mandate penalty. We’ve been traveling home free since 2011. The mandate avoidance rules seem to be the same as you describe. However the good news and bad news is I’m where you may ultimately wish to be. Retired and dividend income alone well exceeds tax brackets for zero taxation. I have zero earned income and no Roth IRA. I read all your fine financial posts to see if I’m missing something.

South Dakota residents now in Chile.

If you aren’t claiming the FEIE, then you have a lot more flexibility to avoid the ACA mandate. You should be able to visit the US about 6 months every 2 years. Of course this won’t matter starting in 2019 since the TCJA eliminated the individual mandate. Or if you are bonafide residents of Chile, you really have no limitations.

I had no idea the calculation was so complex. Which other countries are you paying tax to in 2017?

Aside from the Various countries that withhold tax on our International Stock ETFs, none.

Wow, you cut it close. This is very interesting. I’ll have to keep it in mind when we become nomads. Unfortunately, it’ll be many years in the future. Happy New Year and good luck in 2018!

Not too many days nor too few. Just right.

HNY to you all too!

Question. This doesn’t apply to NRAs right? Only Us persons not present in the Us for more than 330 days correctly?

Correct

Wow, I didn’t realize that the rules were this complex. I wonder how the IRS would even audit something like this. Very interesting. I’ll need to keep this in mind for the future.

You have to provide your travel schedule when filling out the FEIE forms if you are claiming the exemption due to the PPT.

Presumably, they also have access to your entry/exit dates from Customs, but could just look through your passport at an in person audit.

So fucking tired on the big brother on my life…why the heck modern society submit to something like this…damnit!

Mayhap this will help.

Clueless question: Is it true that this exemption only applies to foreign ‘earned income’ and not income from interest and gains from investment funds like Total Stock Market fund at Vanguard? ie these would be taxed in the US regardless if you pass the PPT?

Correct

I’m curious to see what percentage of digital nomads have exactly that range of income where PPT applies. Many of the guys (mostly guys) I’ve seen online keep their incomes low enough that they actually don’t have to worry as much about taxes anyway.

Great job!

All it requires is income exceeding the standard deduction & personal exemption, ~$10k single / $20k MFJ.

Btw, would there be any financial advantage if you became a Taiwanese citizen?

The opposite I think

I’m curious how you stay in Taiwan without establishing residency? And what are the advantages of keeping your U.S. residency?

We are looking at moving to Portugal and the Schengen has a strict “90-out-of-180” rule that requires me to either establish Portuguese residency or live somewhere outside the Schengen for 1/2 the year. I would prefer to just avoid the hassle and live in Portugal full-time but keep my U.S. residency and claim FEIE but I don’t think it is possible.

What does it mean to you to keep US residency? If you aren’t living in the US, you aren’t a US resident, by definition.

I have Taiwan residency, through marriage. Prior to that I did visa runs to Hong Kong, out and back in the same day. The Schengen rules are much more strict.

If you want to live in Portugal, apply for a residency visa. You will be subject to their tax laws, and also have to file US taxes.

What effect does having Taiwanese (Portuguese in my case) residency have on your ability to do a Roth conversion ladder, capital gains harvesting, tax-free dividends, etc… Additionally, many European countries don’t recognize a Roth and will charge tax on the gains. Maybe I’m wrong, but it would seem that maintaining a U.S residency would make things easier by only dealing with one set of tax rules.

If you aren’t living in the US you don’t have US residency. The IRS still taxes you though, so it is just a question of nomenclature.

1 set of tax rules is definitely easier than 2, but that just has a cost associated with it. Some people prefer to live in SF or NYC vs small town USA. It costs more, but they like it.

If tax minimization is more important than where you live (or for how long), then you can choose to be itinerant (never stay in one country long enough to be considered a tax resident) or to live in a country that is tax friendly (see “taxes foreign income of resident foreigners” column.) Some countries have no income tax, and others only tax income that is sourced from within their own borders (territorial tax system.) Taiwan is one of the latter, and also has no tax on dividends or capital gains.

For Portugal, look at their non-habitual residency scheme. It provides for no taxes on dividends and pensions for a period of 10 years. Whether a Roth IRA is a pension is up for debate.

Jeremy,

Thanks for all the info. It is great having your template to apply to my very similar situation. Yes, I am already looking into the NHR scheme in Portugal and will likely go that route…..it seems to be the best option. As an added bonus, we would qualify for the national health care after getting our residency status. Due to the insane U.S. healthcare costs, I think I can fund our entire life in Portugal on what our health coverage premiums would be in the U.S.

Wow! All this seem so complex. I will be retired in 6 months as I am opting for early retirement and I have the option to apply for American citizenship in 3.

Seeing that you have to jump through so many hoops just to avoid taxes, would it even be worthwhile for me to apply for citizenship?

Would it make sense to stay as a green card holder and be subject to staying on US soil for 180 days to retain my residency or just give it up altogether?

Your blog has been an inspiration for me for the longest time and I am hoping to emulate your world travel in a year.

Happy New Year to you and your family.

US citizenship tradeoffs are far more complex. I would give that decision a lot of thought.

Just one factor: dividends on assets kept in the US are subject to a 30% tax for nonresident aliens vs likely 0% for US citizens

Hello. Your blog has been a huge inspiration for us. Now we have lived and seen world outside the US since October 2019.

However, I face the life-time question: keep or give up my green card. I think we are in the same situation with you guys since my husband is a US citizen and I am a green card holder.

Yes, I am worried about tax and wonder how you guys handle it. As long as all asset held by both of us, tax rate for US citizen would be applied? How about 401K under my name only? If you have an article lecturing these, please indicate me there?

Thank you very much :)

A non-citizen spouse to a US citizen can choose to be taxed as a resident alien… that phrase just means you choose to be taxed like a US citizen on worldwide income, no green card necessary.

You can also choose to not be taxed as a resident alien, and then your husband would file his taxes as Married Filing Separately. Your US assets would be taxed as a non-resident alien (withholding/taxes on dividends, no tax on capital gains, tax treaties may apply.) Separation of assets would probably make things easier here… (I have no experience with this.)

Pros/Cons to both approaches. We do the former as shown on our tax returns.

Great to know. Thank you so much :)

Seems like the first leg of a long journey for someone looking to satisfy this test is a short hop to Canada, spend the night, then take the transoceanic flight from there.

I probably wouldn’t do this just for a day. It would be a good option for transatlantic cruises though

wow this is really interesting. I dont think the UK do anything like this but I haven’t really looked into it. I’d have been way tpo scared to have gone for this but ot worked out really well for you!

Little Miss Fire

LittleMissFire

The UK doesn’t tax its citizens when they are outside the country, so there is no need to have anything like this.

When you’re filing taxes do you need to list out your flight times and itineraries or can you just check a box to certify you’re good to go?

You provide entry/exit dates for the US on Form 2555

so, in theory, even if you didn’t hit 330 days, you could list your flights as if you did, and hope you don’t get audited …

You could try it, but tax fraud is only lightly punished for extremely wealthy, well-connected people.

Yup, that’s exactly what i was thinking. I’m not running for President yet, so I should probably steer clear of coming even close to tax fraud!

Your anxieties while on the Alaskan cruise (and on that flight) piqued my curiosity, which is why I asked – almost made it seem like the IRS was literally with you on every trip! I reckon they do follow us to our graves …

Thanks for the quick reply! P.S. Love the website name (though i could never go camping without running water, I’m a total Dude-Princess)

I retired a month ago and have three months to exercise stock options. I’m planning to pass the PPT for 2018. I’m under the impression that the exercised options will be considered earned income. By passing the PPT, do I effectively increase the deduction from $24k to $104.1k (married filing jointly)? That’s… a lot.

Depends, but if you were living/working in the US when granted the option, then no.

From Pub 54:

(Earned income) is considered received in the year you disposed of the stock and earned in the year you performed the services for which you were granted the option. Any part of the earned income that is due to work you did outside the United States is foreign earned income.

Ah, thanks. I earned them over the last decade working in the US. Sounded too good to be true!

Jeremy, since you are Taiwanese residents, why wouldn’t you qualify as bonafide foreign residents?

Potentially, but the PPT is completely objective and thus easier, imo.

The Bonafide Resident test is subjective and nuanced, and assumes a reasonable person would believe that you have moved to a new country and setup roots. This would typically involve things like opening bank accounts, registering to vote (if applicable), getting a driver’s license, etc… I’ve done none of those things, and haven’t actually been in the country more than half time.

Thanks for the explanation. I should point out that based on my reading there is also a subjective side to the PPT – specifically the definition of your tax home, as well as the nature and duration of the travel (i.e. “temporary” doesn’t count). In your case, clearly the permanent side is not a problem, but it is technically not enough just to be in a foreign country for 330 days. (Again, this is according to my reading of the IRS publications, which I recently brushed up on since I was trying to help a friend who is planning a sabbatical year abroad). As always, I’d be interested in your thoughts.

Plus you already have a lease, so how much more trouble can a library card etc. be? :-)

There is a clause about your travel being indefinite and for more than 1 year, but that is also objective. A sabbatical contract can be a problem because it shows intent to return. This is discussed somewhat in the comments on this post.

Tax home is just where you work, and itinerant is a valid tax home.

If I really wanted to I could probably pass as a Bonafide Resident for 2018. Maybe. The advantage of that route is I could stay in the US longer than 35 days or whatever. Harder to argue that for 2017 as I didn’t have a lease until end of the year, and was in Taiwan less than 6 months. It was more like we just were moving around and happened to hop in and out of Taiwan. For people with no or low incomes, it doesn’t matter anyway since no need for FEIE. (this will be 1st year I use it.)

One of the big questions for the BFR is Line 13b of Form 2555:

Are you required to pay income tax to the country where you claim bona fide residence? Yes or No.

Our answer has been no (not in country more than 6 months, no Taiwan sourced income in territorial tax nation, etc…)

But that is the ultimate commitment, eh? Are you really a resident if you aren’t a taxpayer?

That’s why I say the PPT is easier.

Gotcha, thanks.

Depending on the country, it might make sense to go the BFR.

Here is a bit more info about how to show proper intention:

https://www.taxtake.com/blog/post/the-12-bona-fide-residence-test-factors/

These things were natural for me to accomplish given I really did intend to live in my new home country. :)

For anybody who intends to live in one place, the BFR is more flexible. No doubt.

Hi Jeremy,

We spent the summer in Europe as well and love following your family adventures.

I have a question regarding the new tax law. I have read that it includes a change to a territorial tax system but I’m not seeing much mention of this on blogs such as yours, is this because this change has only been targeted towards corporations (like much of the new law) and individuals are still held to the previous worldwide system you discuss navigating above?

Thanks for the time you dedicate to this blog, happy travels.

Thank you Jesse.

You got it right: The territorial change is just for corporations. Individuals are still taxed on worldwide income.