Empower – Free Financial Management Tools

Since my college days of living hand to mouth, I’ve tracked every penny I’ve earned and spent. It was a bit necessary if I wanted to have more month than money. At first I used pencil & paper, then a spreadsheet, and eventually Quicken.

Years later, after reading Your Money or Your Life, I began tracking passive / investment income with focus and determination. I added more calculations and pages and charts to my spreadsheet, and eventually started using Mint.com.

I credit this practice of tracking all income, expenses, and investment activity with our ability to optimize our spending and grow net worth. It is hard to overspend or buy frivolous things when the numbers are staring you in the face. There is no pretending and no hoping for the best.

It really doesn’t matter which method of tracking you use, as long as you do so…

After 20+ years of practice and experience, I now rely primarily on Empower to do it all for me. It does everything that my old spreadsheet did in a fraction of the time. It’s great… plus, you know… free.

Disclosure: GCC is a Empower affiliate. If you start using Empower from a link on this page, we may receive compensation. Opinions are my own, and also free. For all of our International readers, sorry, Empower is currently US only.

Empower, Free Financial Management Tools

We have 20+ bank, investment, and credit card accounts across 13+ different companies. The Empower Dashboard provides a high level overview of the last 90 days of income, expenses, account balances, and net worth across all of these accounts with a single login.

Everything is color coded and easy to read, with intuitive graphs and timelines. It is a simple and easy way to grasp our current financial status with a single glance. As a lazy and busy person, this is a dream. And more detailed information across all areas of interest and timeframes are just a single click away.

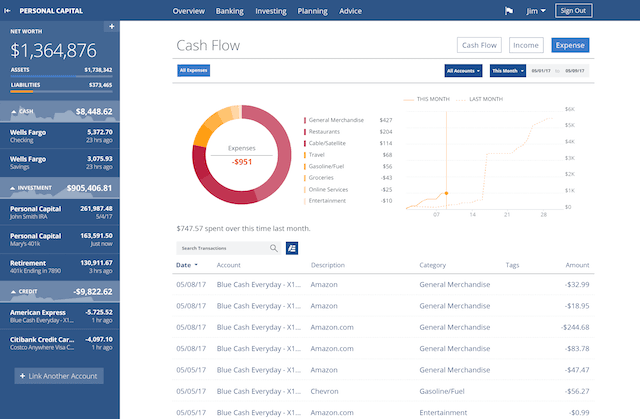

Cash Flow

Cash flow is pretty important. Just ask Floyd Mayweather. Or me.

Empower‘s cash flow page provides a snapshot of every income and expense transaction across all accounts, and the timing thereof. And each transaction is automatically assigned to standard budget categories (with great accuracy.) Zero effort Budgeting and Cash Flow Management are nice features.

Easy to read charts highlight incoming and outgoing dollars, making it clear how much is spent on avocado toast and other essentials.

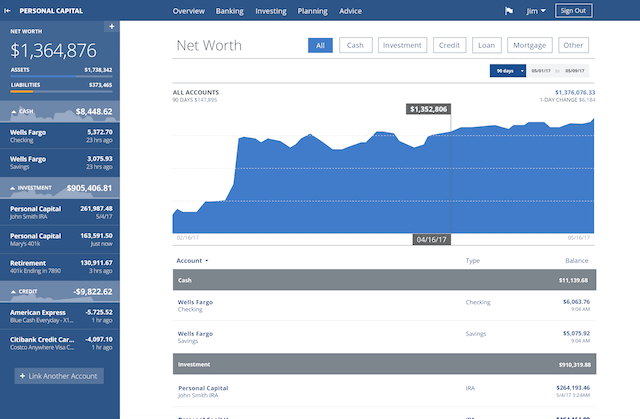

Net worth

Ideally, tracking cash flow leads to investible cash which leads to an increasing net worth. Good behavior is rewarded. The net worth page automatically tracks and updates all account values (including housing, if that’s your thing) so we can make sure net worth is trending in the right direction.

Investment Management

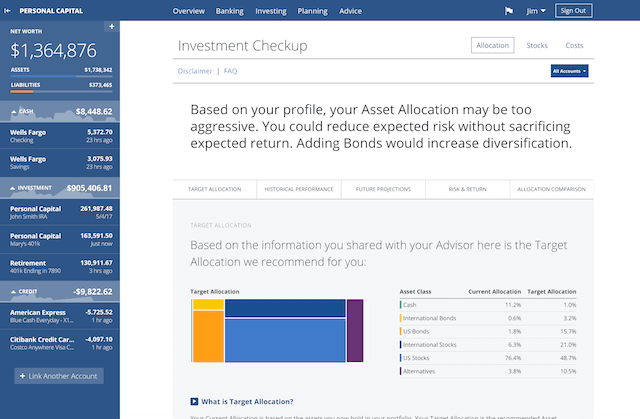

For those of us who own stocks and other liquid investments, Empower has a nice suite of tools to optimize asset allocation and minimize fees.

Through a simple series of questions Empower makes an educated guess on how well you might sleep at night and proposes an appropriate target asset allocation. (Ours is set to the most aggressive.)

Any time the target allocation is out of whack we’ll be notified. For example, due to the recent run-up in US stock prices, our total allocation has become more US stock heavy than our target.

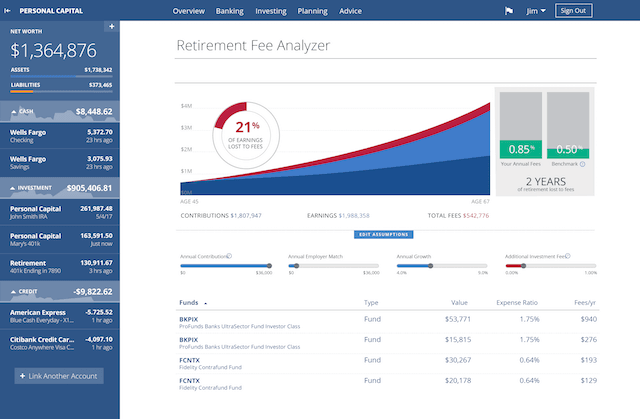

Finally, and very importantly, the retirement fee analyzer looks at your investments and compares to alternatives. If your fees are high, this tool lets you know. Shockingly, there are still too many funds charging 1%+ per year when we could be paying less than 0.05%.

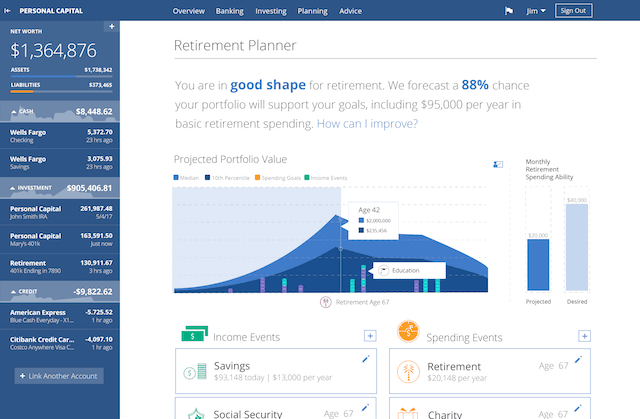

Retirement Planner

About a year or so ago, Empower added a retirement planner feature. This projects portfolio longevity based on statistics of historical returns and target spending aka a Monte Carlo type analysis. It’s pretty slick. (However, I think rolling windows based on historical data provides a more realistic outcome. See cFIREsim for this.)

This tool reports a 99% chance that our portfolio will support our goals, which is nice to know. It never hurts to get another perspective, especially if that perspective says you have some work to do.

Investment Services

I strongly advocate a DIY approach to investments with low-cost index funds. But there are people who prefer to have a person or team managing their portfolios. For this, Empower offers investment and wealth management services.

Fees are lower than traditional financial advisors, but are about 6x the cost of a robovisor and 15x the cost of our portfolio. Therefore I feel 6-15x stronger about using these services as I do about robovisors.

On occasion PC will call users and ask if they are interested in using their investment or wealth services. I haven’t answered a single one of these calls as I’m always in another time zone. Others have, and just said they prefer to manage their own investments.

Common Questions & Room For Improvement

Over the past few years I’ve heard 3 common questions from readers about using Empower

1 – Isn’t Empower a startup? What if they go out of business?

I used Amazon.com and Netflix long before they were profitable. I’m not aware of PCs financial status, but I like their tools so I use them. Hopefully their business grows, I like to see quality stuff succeed.

2 – Is this secure?

Usually this question is asked in regards to having a single login to access multiple accounts at different companies.

Yes, it is secure. There is no option to buy/sell/transfer funds from any accounts through PC, and all account access is managed by Yodlee which all of the big banks are using anyway. (No passwords are actually stored on PC servers.)

Additionally, each device that you use is individually authorized. Only my personal laptop/phone have access.

And since we now have easy and regular access to all accounts, it is easy to see if anything looks out of place. I see that as a security improvement.

3 – is there anything I don’t like?

Yes. PC works best when all transactions are in electronic form such as credit cards, debit cards, online bill pay, and transfers. For cash transactions, I would like to be able to split transactions across multiple budget areas. Example: I withdraw $500 from the ATM and spend half on avocado toast and half on toys for Jr. Currently I can only categorize this $500 withdrawal as ATM/Cash, Child/Dependent, or Restaurants. It’s a minor thing, but it is what it is.

Summary

Over the years, I’ve tried many different methods of tracking income and expenses and optimizing investments. Empower is a great option that is quick and easy to use. We are able to see our 20+ accounts across 13 different companies with a single login and a single Dashboard, with incredible detail just a click away. Plus the price is right.

Nowadays Empower is my primary way of staying on top of our financial status. Maybe you will like it too. Click here to try it for free.

Personal Capital really shines when it comes to the investment portion. I love the fee analyzer and being able to see my market allocations from all my accounts instead having to figure it out for myself.

Their budgeting tools…… yeah they need work. That’s why I still use Mint in addition to PC.

We don’t budget, so maybe that is why I haven’t had to use Mint as well. We just look at cash flow and projections and go from there, but it is nice to see the graphs of how much has been spent in various categories.

Great summary, we have been big Personal Capital fans for a few years now and I really like their offerings on the planning and fee analysis side.

I agree with Gwen- on the general budgeting/tracking expenses, I still revert to Mint, but hey, to each their own strengths :)

~Mrs. Adventure Rich

I gave PC a try and I do think it’s good to use in conjunction with my own budgeting tool. I really, really like its net worth tracker, which is hard for me to do manually each month.

Automatic updates are the best.

How about a quick mention at the start that this is only useful for U.S. centric folks. “…currently only support U.S based financial institutions (currency, USD) for linking accounts. Note that to sign up for Personal Capital, you will need a valid U.S. phone number for security reasons.”

OK

I use both Mint and PC: Mint for budgeting and transactions, PC for tracking my investments. PC has been annoying me recently though. About a month ago it decided that it no longer wants to talk to my 401k account, and I have thus far been unable to convince it to stop throwing a hissy fit and kiss and make up.

The other area where both PC and Mint become annoying is when you turn on 2FA for your financial accounts (I strongly recommend doing so for security). I still use them and pay the price of reduced convenience for additional security.

I don’t use 2FA on any accounts primarily because I don’t see much advantage. Nobody can transfer funds out of my accounts except to those already in the system, and adding new accounts requires authorization.

PC currently doesn’t display the cash portion of my HSA, but that is small so I don’t worry about it. Other than that I haven’t had any issues with their account integration. I’ve had a similar problem that you describe with Mint – sometimes they double count my 401k, other times they don’t count it at all. They also send me a warning email every time my bank reimburses for an ATM fee. They don’t seem to be able to distinguish that a DEPOSIT with the word Fee in the description is not a Fee.

” Nobody can transfer funds out of my accounts except to those already in the system, and adding new accounts requires authorization.”

I don’t use 2FA to protect my accounts from access via PC. I turn on 2FA to protect myself if the accounts themselves are compromised. e.g. if Vanguard or BOA are breached, even if someone gets hold of my credentials, they can’t do much unless they also manage to hack my email account/phone because I have 2FA set up. The 2FA then messes with Mint and PC, because they need me to provide additional credentials every time they attempt to refresh my accounts.

Right. That is what I was referring to. Even if they hack your credentials… what value does said hacker get? They can’t transfer funds.

I had to reply even if it is like a year later because there is more to this. If a hacker gets access to your BANK credentials, they can go through your statements, get your account number and most certainly make a transfer or “payment” using your account number + routing number. Most banks also allow you to transfer money outbound to others or make payments via an address. So said hacker could basically pay themselves with your checking account. Without 2FA a hacker can do a lot. Heck, they can go through all of your profile information – and change it. They could then change your address and send out a new debit/credit card to their address. You may receive a notification about this via email, but then you have to go through the process of fixing all of it – and they may have already moved money. I personally would rather have the hassle of 2FA to keep myself from having to deal with all of the possibilities.

Dear Russia, if you are listening, maybe you can try to hack into my bank accounts.

After yo hearing about PC here and on numerous other blogs and podcasts I tried it.

Weirdly, they couldn’t link to USAA. I reported the issue to them. I got a couple calls and emails from marketeers asking f they’d resolved my problem but, again weirdly, never got any communication from their technical support people to actually fix the problem.

I do all my banking with USAA and their logon protocol doesn’t seem particularly outre. I didn’t try linking my brokerage or CC accounts, but I figure if I can’t link my bank to them, they can’t help me.

So, no.

You can get them to link to USAA. Since USAA has a second check to make sure it is you, open Personal Capital in a window, then open USAA in a second window, click back to Personal Capital and refresh the USAA link within Personal Capital. Works in Mac and Windows. I link it to my USAA info once or twice a month, it catches up on everything then, banking info, USAA investments, mortgage (I have all with USAA).

I use USAA for all banking. Every once in a great while (couple of months) I have to re-do my security question for PC but otherwise have not had an issue at all. It updates like normal but does take a tiny bit more time to load than my other accounts.

I can’t get USAA to sync either. The big irony is that USAA invested in Personal Capital https://www.personalcapital.com/blog/personal-capital-news/personal-capital-raises-50-million-accelerate-industry-change/

How well does PC work for a married couple? I primarily credit cards and have several investment accounts. My wife uses checks and cash. Your thoughts on the best way to use PC in this situation would be appreciated. Also, I assume custom categories can be created, is that true?

We are a married couple and it works pretty well. We have individual and joint accounts, and they are all just linked to one common login.

Cash transactions are lumped as one category per ATM withdrawal, so that may or may not be an issue depending on how you manage things.

custom categories are supported

I am honestly interested in what finder fee PC pays bloggers for each referral?

Thanks

$100 for a qualified referral (link accounts with $100k+)

ps: looks like you commented on this multiple times which flagged the spam filter. I just saw your comments now

I just stumbled on this site and I definitely agree with the idea of tracking your income and expenses down to the penny.

In fact, I am about to do my Net Worth update for the first time. And I finished posting an article on a similar topic as you.

I would follow this site more.

Thanks.

Tried PC a year or so ago and it sucked so badly. The premise is good but the implementation terrible. Didn’t connect to my bank half the time and when it did it often, for no reason, downloaded duplicate transactions. It then proceeded to assign incorrect ETF allocations to my actual ETF’s, saying one was equity when it was in fact bonds etc. There was no way to adjust these transactions and allocations so I was left with all sorts of errors in most my accounts. Eventually it got to the point that the information was so inaccurate that it wasn’t worth using.

The software is totally inflexible and TOO automated, to the extent you are very restricted as to how much you can manually edit. It automatically does a lot of things and if it does it wrong, tough luck!

The budgeting section is laughable compared to YNAB or Mint, so yeah that’s just useless as well.

Their customer service is also dreadful. Go and check out the bugs section of their “forum”. It’s full of people reporting issues and never getting a response. I reported many issues and never got a response once.

It’s a shame, because if it worked well it would be a great company, but it doesn’t. I can more accurately track everything myself knowing there isn’t a thousand errors.

Maybe I’ll give it another shot in a few years once it has sorted out all of these kinks (hopefully)

It’s almost like we are using two completely different products. Weird

I like PC a LOT, but yeah, it often fails to update by account connection, and will auto-assign things wrongly. That would be okay if there were some mechanism to ‘adjust’ things that don’t get assigned right, but their focus on 100% passive automation makes that impossible. I actually have a separate manual spreadsheet that I keep in addition to PC that includes the various corrections. Every now and then I think “why am I doing this?” but I’m just kind of hoping something changes, because if it all starts working it will suddenly be awesome.

One thing to keep in mind is that financial institutions currently have a real distaste for aggregators like PC, Mint, etc (see: http://www.reuters.com/article/us-column-weston-banks-idUSKCN0SY2GC20151109). They actively make changes to stop these service from reporting correctly, so there is something of an arms race going on.

FYI can attest to same problem, used PC to aggregate my parents’ accounts, and mine. That part was great. The allocation tool though is bad. It wrongly assigned assets (in my parents, a large amount in a money market account was tagged as stocks, in mine it had wrong amount in cash). Not sure where their glitch is, but it seems to be more accurate with banks like fidelity. This makes all other tools (e.g analysis portfolio, or retirement planner) incorrect. I am hoping that it will eventually fix this. Agree with other comments that they should allow you to fix/reassign any glitches.

Do any Personal Capital users have concerns that their bank won’t protect them against fraud because you’re sharing your bank credentials to a 3rd party. Most banks have it in writing that if you share your account and it gets compromised, they won’t do anything to help. I know that you’re limited within PC itself, but what if the Yodlee (from what you said above) database gets compromised? Now someone has your direct bank account info. If the bank knows that your account was compromised from this method, I believe they have the right to deny compensation.

Now if your bank directly got compromised, that’s on them to protect you.

I hope I don’t come off as a crazy person that fears online banking. I use it and love it. But working in IT, I also know that given enough time, any security measure can be broken. Look at what happened to the Sony Playstation accounts. The key is that Sony turned around and protected their customers because they were at fault.

Mint does a better job a tracking expenses while pc does a better job tracking investments. With these two you have it all

Personal Capital is so easy to use! I recently started tracking my net worth on the website. Before, I was doing it all manually on a spreadsheet. It is also nice to see all of the amazing charts and graphs!

I’ve been using PC for several years now to track investments and net worth. Love it. I don’t use it for budgeting and can’t comment on that. I still use an old spreadsheet I created years ago to loosely track my very simple budget. I love playing around with the retirement calculator to try different scenarios, like how working part time after reaching FI affects our financial situation. Like you said Jeremy, easy. I think it actually makes tracking things more fun.

Hi GCC, greetings from Malaysia.

Quick question, since we, outside US can’t use PC, do you mind sharing your previous excel templates to us?

Thanks in advance:)

Sorry, PC is US only.

I’ve tried to share my old spreadsheet before but it is a real mess. It’s probably easier to follow the process outlined in Your Money or Your Life.

I’ve found it impossible to add either my 401k account (says password expired) or main brokerage (no link for it) to Mint.

Personal Capital & Yodlee (Moneycenter) are able to add and access the above just fine.

No response from Mint to repeated support requests.

I would happily delete my Mint account in favor of Personal Capital or Yodlee if the latter had better budgeting tools.

Personal Capital is always calling me to sell their service, which is annoying.

Yes, I mentioned that in the post. Just tell them you are a DIY investor and have no interest in their service. They’ll stop.

I have been using personal capital for the last few months and I love the utility of this website. I think it is a great initiative. Shout out from a newbie getting started on FI journey!

They have been trying to contact me for advisory services, which I don’t need. Willing to pay $30 year for the app since its been a life saver. Got my brothers partner to switch over to Vanguard from Voya Financial after PC showed her how much she has been ripped off on fees.