Big Tree on Big Island (That’s me under the tree!)

2023 was our 11th full year of wild and free livin’ domesticated living.

Life in the burbs is interesting… life largely revolves around kids and their activities. Every once in awhile when we are feeling a little wild, we might bake a pie or mow the lawn. And as the school calendar allows we mix in a bit of travel (Spring break in Vegas, early summer on the Big Island, Thanksgiving in Tahoe, and Christmas in Taiwan.)

It took some getting used to but we have now become fully acclimated to this relaxed, family-friendly, predictable environment. The only real surprise was the total cost.

2023 Cost of Living

I don’t actively track our spending anymore… so it was a bit of a shock when I opened up mint and Empower to do a 2023 post-mortem. We spent HOW MUCH on Amazon.com?!?! And don’t even get me started on Costco…

But overall expenses still came in surprisingly close to what I nonchalantly predicted last year, about $10k/month, although spending on housing and transport went down. Travel costs continue to be low for what we get thanks to extensive travel hacking.

Here is the breakdown:

| Expenses | Monthly | Annual | $/day |

| Housing* | $2,000 | $24,000 | $66 |

| Utilities | $900 | $11,000 | $30 |

| Transportation* | $275 | $3,300 | $9 |

| Groceries | $1,150 | $14,000 | $38 |

| Restaurants | $800 | $9,500 | $26 |

| Healthcare | $150 | $1,800 | $5 |

| Entertainment | $250 | $3,000 | $8 |

| Vacations | $750 | $9,000 | $25 |

| Misc | $2,250 | $27,000 | $74 |

| Childcare | $667 | $8,000 | $22 |

| Kid Activities | $500 | 6,000 | $16 |

| Taxes | $100 | $1,200 | $3 |

| Total | $9,800 | $117,800 | $323 |

Sums don’t total due to rounding.

Actual outgoing cash flow is roughly $52,000 greater due to:

- *We have debt on our house (30-year fixed 2.75%) and car (7-year fixed 2.74%.) Reported expenses reflect only the interest portion of loan payments. Principal reduction is another ~$14k.

- Minimum payments on about $50k in credit card debt at ~0% interest (with that $50k invested in short-term treasuries at ~5%.)

- Roth 401k/IRA contributions – $26,000 in total, see Legal Money Laundering

Amazon, Costco, and Target, Oh My (aka What the #^&%!!!!)

Part of the joy* of living in the suburbs is the opportunity to frequent Costco and Target and have anything and everything else delivered directly to your front door by Amazon.

Packages arrive seemingly daily… or even multiple times per day. Because who doesn’t need a Burnt Orange Cast Iron Dutch Oven Pumpkin Cocotte at Halloween, an ongoing subscription for Lavazza Gran Crema Espresso Beans, or an occasional That’s What She Said bottle opener? (affiliate links)

So maybe (MAYBE) it shouldn’t be a surprise that our miscellaneous category is so very LARGE. But still I was shocked. Winnie was shocked. The kids were shocked to see Mom and Dad being shocked.

My second reaction was to analyze where it all went… $9k on Amazon, $7,400 at Costco, $1,800 at Target…

I installed the Chrome Amazon Order History Reporter and started digging… a couple new cell phones, art supplies, an outdoor dining set, some kitchen stuff… I should definitely sort this by category because it is ridiculous to just label everything as miscellaneous.

But then I realized we were still under budget and that I would rather do other things with my time… and yet we probably have $1k/month of waste buried in there.

So we discussed… I’m going to track spending on a monthly basis for a few months and see how things look, because we would rather spend that $1k per month on business class tickets than some versatile solutions for modern living that have been completely forgotten. (February 2024 Amazon spending is only $241.93…)

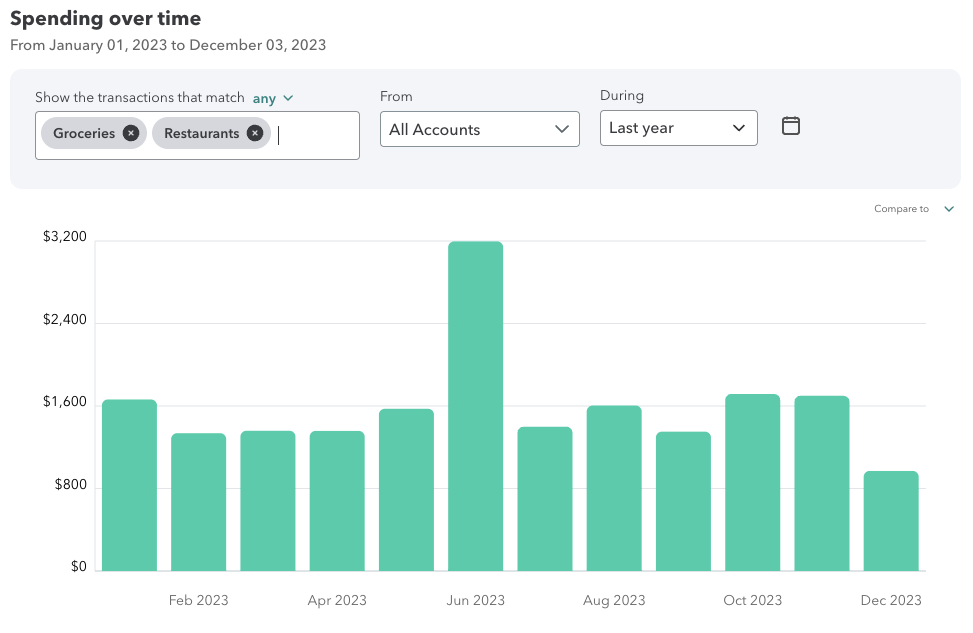

A Cool Chart

Based on the table we spend about $2,000/month on food… but looking at things on an annual basis tells only part of the story.

While reviewing our expenses I came across this cool little chart of food spending… Wow, June! What happened there?

Well… we were in Hawaii for 2 weeks in June and spent nearly $1,700 on restaurants in that time… because those macadamia nut pancakes with coconut creme weren’t going to make themselves.

mint.com is terrible at charts (it would be nice to have a separate color for groceries and restaurants, no?)

Anyhoo, moral of the story… sometimes it is worthwhile to zoom out (and be sure to order the mac nut pancakes.)

Life

We are tied to a school calendar these days but we still manage to have some fun. The kids these days say pics or it didn’t happen… so here are some pics.

A daily ritual

Another day, another package

Home eating is good eating (but no mac nut pancakes)

Tasty Eats

Homemade bbq pork

Life milestones

Biking to school

Trick or Treat – HP & Elsa

Hawaii – Big Island

Volcano Zone (Mount Kilauea erupted while we were in town)

Black sand beach

Summer Fun

On the Water

Escaping the Heat

Back in Taiwan

Jet lag

Night market – by far the kid’s favorite

Summary

Life is good. Our life these days revolves around the kiddos… school and sports, sports and school. They are doing well and enjoying the journey.

We live well, travel well, eat well. That costs us about $10k/month, which seems a little wasteful. I’ll track spending more closely to start 2024 and see if we can cut 10% or so (or at least redirect it towards things we value more.)

Thank you for reading. Please share your GCC love on Twitter, Facebook, and Instagram.

Hope everyone has a great 2024 and beyond.

Jeremy, Winnie, Julian, Jaiden

Go Curry Cracker!

* “joy”

Speaking of Travel Hacking… Get 5 free hotel nights with the Marriott Bonvoy Boundless card after $5k spending in 3 months. $95 annual fee.

This link is my referral link.

For an idea of how to use 5 free nights for HUGE value, check out our spring break 2022 trip to Waikiki – Our Suite (sweet?) Hawaiian Spring Break

If you already have this card, feel free to include your referral link in the comments!

Only $1800 on healthcare? I spent that much in January .

Always appreciate these updates and a look behind the curtain. I’m visiting Taipei for the first time in May and couldn’t be more excited for it!

Ouch. Hopefully lower bills for you going forward.

Yeah we pay about $100/month for a silver plan and I went to the ER 2x for some minor injuries w/ $150 co-pay

Is your low cost due to income-based govt subsidies?

That is correct

Obamacare Optimization in Early Retirement

Yes, it is very easy to spend $1800 just on monthly premiums. For 2 people. With a high deductible plan. I love it (not). Health care and college bills hurt FIRE ambitions. Well, I need another colonoscopy this year, so that should help whittle down that deductible! Health insurance is outrageously expensive.

Doesn’t track when 2nd lowest cost silver plan premium is capped at 8.5% of your AGI – if you’re bringing in $20K+ per month, then it isn’t the health insurance premium that is holding you back.

It is capped at 8.5% of AGI if that AGI is less than 600% FPL. For a family of 2 that is ~$10k/month

In 2026 that probably drops to 400% FPL which is only ~$6.5k/month

Also worth noting – the unsubsidized premium differences between age 30 and age 65 can be 3x

Ah – I was still on the pandemic tables. My mistake.

Big incentive to avail yourself of those traditional retirement accounts to get AGI down then.

Actually I don’t think that the 600 percent thing actually passed – the law as amended doesn’t have that level according to Cornell. Triple-checked because the case-study spreadsheet doesn’t have

https://www.law.cornell.edu/uscode/text/26/36B

And the KFF calculator agrees.

https://www.kff.org/interactive/subsidy-calculator/#state=&zip=&income-type=dollars&income=240000&people=2&alternate-plan-family=&adult-count=2&adults%5B0%5D%5Bage%5D=64&adults%5B0%5D%5Btobacco%5D=0&adults%5B1%5D%5Bage%5D=64&adults%5B1%5D%5Btobacco%5D=0&child-count=0

So I’m back to “you make a ton of money – stop whining about premiums”.

Ahh yes, you are correct. I mis-remembered, thank you.

Max 8.5%

Good post. How much of the spending is directly related to owning a home now vs renting in the past?

A lot, both directly and indirectly. No renter buys a Burnt Orange Cast Iron Dutch Oven Pumpkin Cocotte

Thanks for sharing. Cool family pics. You said you stopped actively tracking expenses for a while, do you remember about what year of retirement it was?

I believe 2018 was the first full year where I didn’t track expenses… so year 6 plus or minus.

Reflections of 2018, A Year Without Expense Tracking

Thank you for the kind response. Our tracking is based on a 20 year habit… I am curious to know if you still think about SORR?

I do not.

A few reasons for that… the main one being that I am 12 years away from collecting social security which is a bit like having an extra million dollars. Other reasons mostly revolve around having more than enough $.

I like your reasoning, it helps me to process my situation. Only 5 years from being able to draw, but if I did I would have to pay more for ACA. We have enough already as well and in 5 years that problem will only be worse. :) Do you do projections for where you will be in the future?

Sorry, I read your link after I submitted my comment. Still very hard to comprehend the ridiculous amount of money you and I will have in old age. If only I could have done this math at 20 years of age…

compound interest is a helluva thing

Love the family pics, every looks so chill! We have lived on a barrier island for the last 2 years which is very remote, and we are moving due to the lack of convenience and healthcare. I just hope we don’t have an increase in spending — just because it’s convenient to shopping. Hopefully we’ll continue to spend time outdoors kayaking & walking on the beach enjoying nature & not Amazon. But it’s hard to do!!!

I think the main thing is the house… there is always something that can be improved or made more convenient by spending $20 delivered to your door, and that adds up surprisingly fast if you aren’t paying attention. Oops.

Is a post like this the sort of thing that helps drive model income for your children so you can fund your kids Roth IRA?

We don’t have children yet, but I’d love to see some more musings on that with numbers. I’m always trying to learn the rules before being put into the game.

I guess? It would need to be a much more frequent thing to get real value out of it.

Basic details here: GCCJr for Hire

Always fun to read your updates.

I’m curious as a family with 2 kids how you teaching your kids to work.

As in regular family (no FIRE) kids see parents going to work (or getting into that room called daddy’s office) and with your lifestyle it’s a bit different.

I’m sure you guys thought about it and attend it but curious what you think.

It will be awhile before we fully learn how badly we have messed up our kid’s work ethic… but I think parents working isn’t necessarily the main driver.

The kids help around the house because that is what family members do (Jr helped me cut down a tree this weekend, for example), they know homework comes before play and that things have due dates, that they should do their best at anything they try (mainly sports), etc… We currently fund all of their main needs, but some wants get funded via cash gifts from Grandma… and there they are learning that it is better to pay for things with interest on your savings rather than spend the savings directly.

We adults are also fairly productive in non-work ways – not working a job doesn’t mean sitting on the couch staring at a television… And I still have an office even if it is only used a few hours per week

Have you seen all the electrification rebates SMUD is offering? Roseville Electric has a bunch that we’re going to take advantage of to install heat pumps all around (dryer, AC, water heater).

Yeah some good ones – we had some people offer to do a heat pump water heater install for $0 out of pocket after all rebates/credits/etc…

Oh right on! If you have those business names on hand could you send them to me? We just bought our house in Roseville but those electrification updates are high up on our list. I estimate that it should save us around $2-$3k a year in utility expenses (forgoing PGE natural gas)

There were a bunch of them.. Super Brothers is one based out of Roseville I believe.

The $0 price tag was based on a $3k-$4k credit from TECH Clean California but they already used their full budget for 2024.

Thanks so much for sharing your experiences – super helpful. I am also in CA and always wonder what healthcare premiums and out of pocket expenses would look like in early retirement (with most income coming from selling stock/minor capital gains).

With healthcare subsidies that high, were you forced to put your kids on Medi-Cal? I got spooked by an insurance broker a few years ago that told me if I was under 300% of FPL, my kids would be on Medi-Cal and it would be tough to find providers. Can you choose to opt out of Medi-Cal, or have you found that having kids on Medi-Cal isn’t an issue?

Kids are on Medi-cal, yes. We haven’t had any issues with providers – they go to the same Kaiser office we do but also have dental included

Can you provide more info about your healthcare insurance? For a family of 4, how did you find such low premium plan? Any income based subsidies applied or is it an extremely high deductible/co-pay? Also, do you and your family go back to Taiwan for major medical treatment instead?

Thanks

We are a family of four with income of about 199% FPL.

That puts our premiums at roughly $100/month with small-ish deductibles.

See: ACA Premium Calculator

When we were in Taiwan this past December three of us went to the dentist. I paid about $50 for a cleaning.

Jr needed a filling that we were having a tough time scheduling in the US due to holidays and travel plans. That actually cost us more as our US cost would have been zero.

Going back for major treatment isn’t really an option unless we pay cash which anybody could do… I’m not very knowledgable about the nuances of Taiwan system but my wife and 2 kids are citizens and are therefore eligible to enroll in the national health system, but there is a delay of something like 6 months of residency before you can (re)enroll.

I am trying to determine when to pull the trigger, so my wife and I can enjoy the life style that you and your family enjoy. You mentioned income level of 199% FPL which is around $60K for CA. Given your annual expenses is $117K. Does this mean that you have to cash out additional $60K of your principle investments to cover the “negative cash flow”?

Can I interpret as following:

Cash/income:

principle investment cashed out: $60K

earned income: $60K

less:

Annual Expenses: $117K

This would qualified your income at the 199% FPL?

thanks

I sell stock every year, yes.

Income comes from:

– dividends

– interest

– selling stock

– some blog income (in 2022 it was ~$30k, details here)

– debt – in late 2022 and early 2023 when the stock market was down I chose to take on debt rather than sell assets. Debt adds $0 to taxable income.

— see: Sweet, Sweet, Debt

When selling stock, a portion of the sale is a non-taxable return of capital and the remainder is a taxable capital gain.

What percentage is which depends on how much gain you actually have. I sell specific shares to minimize/optimize the amount of taxable gain.

More info: Long Term Long-Term Capital Gains

Can you explain a bit more?

Is it because some of the stocks you lost money? or because of 0% tax for married couple up to $83350?

If you buy stock for $1 and sell it for $3, you now have $3 to spend. At tax time, only the gains ($2) will be taxable.

Similarly I can spend $100k while having taxable income of only $60k.

In both cases that tax rate CAN be 0%. Any realized losses will reduce the amount of taxable income, but no losses are required.

Lavazza Gran Crema Espresso Beans is also available at Costco Business center (not regular retail center). Much cheaper when its on sale, plus 2% cash rewards when using Costco Citi CC.

I think you just saved me $5/month! Thanks!

edit: actually… looks like $250 minimum order to avoid a $25 delivery fee.

Really enjoyed your update – thanks for posting. We are a family of four, like you, and our food spending is at the same level. It was a relief to see that because I see so many other bloggers with really low food expenses. We did the exact opposite, moved from suburban America to SE Asia, and we noticed that our Amazon and Target spending went way down (and domestic staff and education expenses way up). Honestly it is surprising that your miscellaneous spending is not higher since you just bought the house recently, and it is so easy to find things you “need”. Anyway, thanks for posting and great to hear that life is so good.

I love mint but Mint is moving to Credit Karma. Have you decided what option are you going to use going forward to track expenses?

I am using both Empower / personal capital and a spreadsheet

Do you find the expense tracking part of empower to be useful? I can never get it to work very well. The net worth tracking is great.

I’ve been using it more the past couple of months… and I think it is 100x better than mint.

What part isn’t working? I have all of our credit cards and bank accounts linked and haven’t seen any issues (sample size of one.)

I can never get my credit cards to stay updated/linked.

Well played med insurance. We “engineer” our income to 138% FPL + $50. Limits our fun with ROTH IRA conversions, but we still manage ~$10K/yr

Only $1200 on taxes? Including property taxes? Otherwise our spending is quite similar, adjusted for the quirks of life in Canada.

Breakdown on the $1,200 from our 2022 tax return (paid in 2023)

– Federal income tax: -$3,000

– State income tax: $0

– Self-employment taxes: $4,200

Property taxes are included in Housing, ~$10k

Thank you for submitting! I love seeing the post centered on family. I am hoping to join you on hitting FI to give my kids some of these great experiences.

What are you planning on using once Mint shuts down next month?

I use Empower / personal capital and excel

Great post, appreciate it as always! One question I had is why your reported expense for housing only includes the interest portion of your mortgage payments?

The principal portion of a mortgage payment is just moving some of my money from account A (checking account) to account B (home equity.)

Unlike the interest portion which is gone forever, I can spend the home equity in the future (when I sell or via borrowing.)

Another way to think of it… each month our asset allocation adjusts slightly by reducing cash holdings and increasing ownership of real estate.

More details: Mortgages, Home Equity, and Retirement Spending

I might be biased but the burbs of Sactown are not too baad, quiet but plenty of things to appreciate. I do miss the food and bike infrastructure of CO and other states.

Oh but the summer heat!

Otherwise they are great.

That’s right, nobody move here! Summers are terrible! 😉

But seriously… it got to 104 degrees today. The pool temp was a comfortable 86. The kiddos and I spent a few hours in the water. Nice day.