This is your Money. This is your Money on a Roth

I recently shared some thoughts on how to become Financially Independent in the shortest possible time by leveraging tax advantaged accounts such as the 401k, 403b, HSA, and Traditional IRA. Taking advantage of all possible tax deductions Today is a great way to Turbocharge Your Savings, accelerating Financial Independence by years

I even made some disparaging remarks about the Roth IRA. Some reader’s pushed back, which is always a good thing.

I will explain the reasons that I believe the Roth 401k and IRA are the least advantageous investment choices. Furthermore, I will provide an overall recommendation for where to save for Financial Independence

First a brief comparison

Dollars saved in a Traditional 401k / IRA are pre-tax. We pay no income tax on dollars going in, an immediate savings of up to 39.6%, the highest marginal rate. The invested funds are allowed to grow tax free, so all interest, dividends, and capital gains are untaxed until withdrawn from the account. Upon withdrawal, all funds are treated as ordinary income, similar to a paycheck.

Dollar saved in a Roth 401k / IRA are after-tax. We pay normal income tax on any money put into a Roth, but this is the only tax that will ever be paid on those funds. Any interest, dividends, and capital gains are tax free, forever

Ultimately the arguments for both types of accounts come down to one question: Will your tax rate after retirement be higher or lower than it is today?

Let’s explore a few scenarios

Median Income

Let’s look at the median income earner, a family making ~$54k/year. Because they are targeting early retirement, they are saving 50% of their after-tax income. (I outlined the median income earner family in the post on how to Turbocharge Your Savings.)

They heard general advise that young people and those with low income can benefit from a Roth 401k, and they thought, “That sounds like us!” Their highest marginal rate is “only 15%”, and some of the $17,500 savings would even be taxed at only 10%. “Surely our post-retirement tax rate will be higher!”

With a $17,500 contribution to the Roth 401k rather than the Traditional 401k, the family would pay an additional $2,502 in tax, an effective tax rate of 14.3%. I’ll be generous and consider the 401k match of 2.7% ($1,444) as part of the contribution, lowering the effective tax rate to 13.2%

Fast forward 16 years to the point where they have achieved financial independence, and decided to quit their job and travel the world. Maybe they’ll even do something crazy, like retire first then have kids. Sounds like a fine plan to me

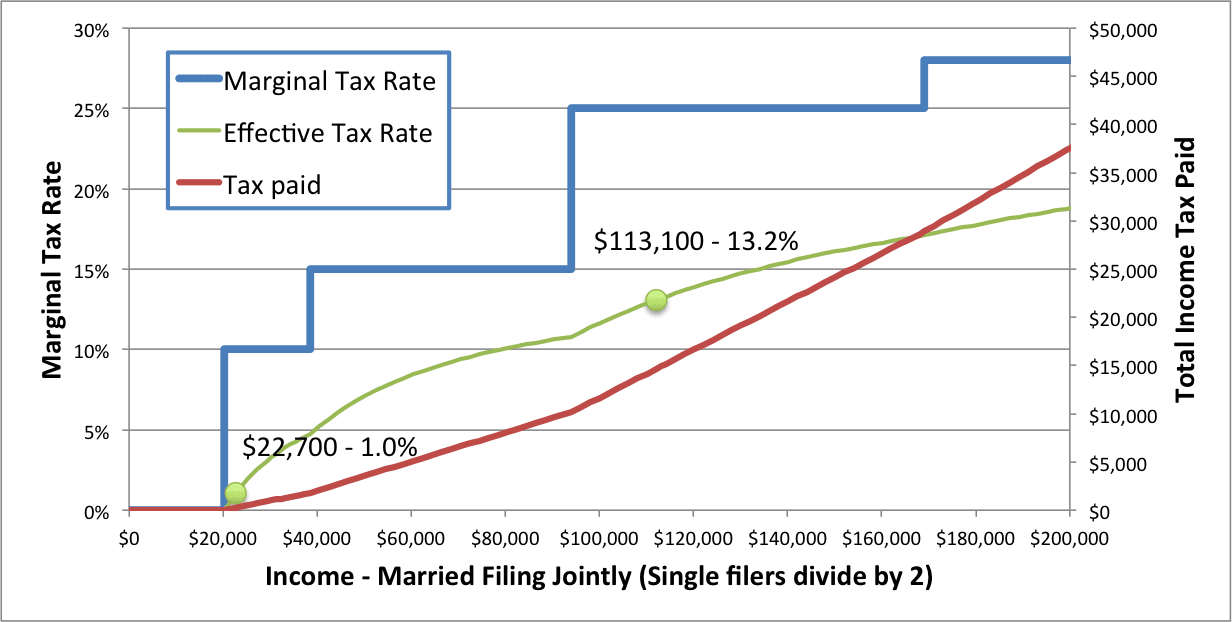

Using constant 2014 dollars, how much would this family need to withdraw from the retirement account before paying the same tax rate of 13.2%?

$113,100! 5x their entire cost of living

Withdrawing their target spend of 50% of their after-tax working income, $22,700, they would pay an effective tax rate of 1%

Why the ROTH 401k Sucks for Early Retirement / Early Financial Independence

But wait, it gets better. Remember that $2,502 that Mr and Mrs Median gave to Uncle Sam 16 years ago, instead of investing for their own use? Had they invested those funds in their brokerage account as I recommended, their total savings would be 13% larger

Using the Roth 401k cost them. They must either work longer, or be comfortable retiring with fewer assets

90% Percentile

What about somebody that earns a little more, perhaps at the 90th percentile of all US families? With an income of $118k, this family is firmly in the 25% marginal tax bracket.

Being generous once again, counting the Roth 401k employer match as part of contributions, our example family elects to hand over $4,375 to Uncle Sam instead of investing for long term personal freedom. They too targeted an early retirement budget of 50% of the working year income, a bit higher since they could afford a few luxurious due to their high earning power

How does this look come retirement time?

90% Percentile ROTH Situation

If they continue with their target spending of ~$48k, 50% of working years after-tax income, they will pay a tax rate of 6.9%. And let’s not forget, had they chosen the Traditional 401k, those tax dollars would have been invested as well

That’s a substantial haircut off the 25% they chose to pay years earlier

To pay the same effective tax rate, they would have to make a serious effort to see how the 1% lives, withdrawing $385k in one year. Kobe beef steaks and lobster tails on the yacht, anyone?

The Last Dollar Principle

In both examples, choosing a Roth 401k over a Traditional 401k resulted in less wealth and more tax. Why?

Think about it this way. When we invest $1 in a 401k, that dollar is the last dollar we earned. It is taxed at our highest marginal rate. But when we withdraw $1 from our 401k years from now, it is our First Dollar. As we saw in the pretty pictures earlier, the First Dollar is always taxed at 0%

Now as spending increases to large levels, above ~$94k into the 25% marginal tax rate things get interesting.

This is where some start to argue about mathematics. We could pull out our college algebra textbooks and prove beyond a shadow of the doubt that a Traditional 401k and a Roth 401k are EXACTLY THE SAME as long as the tax rate is the same. This is true. 25% tax paid today is mathematically the same as 25% tax paid in the future after our funds have grown tax deferred

But math textbooks make simplifying assumptions which are often impractical in the real world (Hello quadratic equation, I’m talking to you.)

The odds of our Mr and Mrs 90% earning $94k in income from other sources (the lower edge of the 25% marginal rate), and every penny withdrawn from their 401k is taxed at 25% in the future is infinitesimally small

What matters the most is the aggregate tax rate, and for both of our examples this is lower than the marginal rate.

Pensions and Social Security

But there are other income sources. I believe Social Security is here to stay, and we will certainly be able to access those funds in 30 or 40 years.

There are also a healthy number of people with pensions, although this is becoming less common

Above $44k in total income, 85% of Social Security is taxed as ordinary income. 100% of a pension is taxed at ordinary income

Both Social Security and Pensions are in proportion to working income. In other words, the more you earned while working the greater the amount received from SS and a Pension

A typical federal government pension (a very generous program) will pay 1% per year of service, so someone with 30 years of service could replace about 1/3 of their salary. A high earner that works until Age 65 could expect SS to replace about 26% of their salary.

For a federal pension and social security to pay $90k in taxable income a year, working year income would need to be greater than $185k.

As this is firmly in the 28% marginal tax rate, this family would also benefit by using a Traditional 401k

Required Minimum Distributions

Starting at Age 70.5, Uncle Sam will require that you withdraw funds from your IRA and 401k. The amount is based on life expectancy, so the older you get the larger the minimum distribution. See Jim Collins’ excellent post on this topic for more detail

How much $ would we need in a 401k for the RMD to have a punishing impact? As we saw above in the case of Mr and Mrs 90%, a withdrawal of $385k has an effective tax rate of 25%

At Age 70.5, this equates to a 401k value of over $10.5 million

An individual that made maximum 401k contributions, with employer match, for 30 years could theoretically have this amount in their 401k. All it requires is an annual return of about 16% for 30 years. It’s not inconceivable, Warren Buffett did it

(If this is you, let’s blow this Popsicle stand and start a hedge fund)

When Is The Roth A Good Idea?

I’m glad you asked

The option to pay tax today and never again is of value, no doubt. If you have an effective tax rate today of 0%, not uncommon for students and others in temporary low income situations, a Roth 401k or IRA is a great idea

It is also not a bad idea if you’ve already maxed out your Traditional 401k and have additional funds to invest. When saving a high percentage of income, this SHOULD be the case. Instead of putting an extra $5,500 into a brokerage account, you could put them in a Roth

For many, however, a brokerage account is just as good. If during your retirement years you expect to earn less than ~$90k/year, staying below the 25% tax bracket, then all Long Term Capital Gains and Qualified Dividends are already taxed at 0%. At these income levels, a brokerage account effectively has a 0% tax rate for stocks, much like a Roth

The brokerage account also has the advantage of being able to harvest capital losses, and to spend dividends or gains anytime before Age 59.5

Conclusions

We have seen that for people with median income and above, taking advantage of the tax benefits of a Traditional 401k has long term tax advantages, allowing one to become Financially Independent in the shortest possible time

We also saw that the impact of Social Security, Pensions, and RMDs also favor the Traditional solutions over the Roth

In conclusion, the preferred investment vehicle is the 401k. The HSA is also great. Only when all other options have been exhausted does the Roth start to look interesting, except for families with poverty level incomes (ideally temporary)

For a rule of thumb, I would save funds into accounts in this order during the working years:

- 401k up to company match

- HSA

- 401k up to maximum

- Traditional IRA if tax deductible (subject to MAGI thresholds)

- Brokerage account

- Maybe $5k in a Roth (subject to MAGI thresholds)

- Maybe after-tax contributions to a 401k for Backdoor Roth (pros/cons)

Addendum:

Why a Roth last? As can be seen in the comments, this is a contentious topic

What if you have already maxed out a 401k, an HSA, are not eligible for a deduction on a Traditional IRA, and have quite a bit of money remaining to be invested. Isn’t putting $5,500 into a Roth better than putting those funds into a Brokerage account?

No

Because we aspire for a long retirement, our portfolio is stock heavy. As explained in our classic post, Never Pay Taxes Again, taxes on Long Term Capital Gains and Qualified Dividends is 0% for incomes below ~$94k.

This is the same tax profile as a Roth, but with one distinct difference

We can spend those capital gains and dividends whenever we want, whereas the earnings in a Roth cannot be touched until Age 59.5 without facing a penalty and taxation (you can only access the Contributions)

Let’s look at that in numbers for Mr and Mrs 90%

Over a 13 year working career (faster due to using tax breaks of 401k), putting $5,500/year into a Roth IRA results in about $72k in contributions. Using the FV function in Excel and a 7% annual return, when we retire early the account is worth about $110k.

If we had invested those funds in a Brokerage account instead, we would also have $110k. Since Mr and Mrs 90% didn’t sell any of their stock they generated no capital gains. And since they invested in their 401k reducing their marginal tax rate to 15%, they paid no tax on any of the dividends.

Of course with that stock being in a brokerage account, they have full use of the annual dividends. At a 2% dividend rate on the S&P500, that is $2200 per year in cash flow for our use with zero tax

Fast forward 10 years, assuming the same annual growth rate, the account is now worth about $218k and continues to pay dividends (isn’t it great when the market only goes up?) Speaking of the market going up, you can’t harvest capital loss in a Roth

Assume at this point we need access to $150k in future dollars to buy a large sailboat to fulfill our dream of sailing around the world.

If we had invested in a Roth and we try to access our Roth contributions at that point, we only have access to our original $72k investment. We need more money

While full access to contributions is often cited as an advantage of a Roth, those contributions lose to inflation with each year. While we can access our $72k in contributions, those funds are only worth about $53k in Jan 2015 dollars. The earnings are much more valuable

Because we didn’t have access to the dividends in the Roth during our decade of joyful living, we’ve been spending down the Brokerage account a little faster. Maybe we don’t have enough funds there to cover the difference

Now we need to either tap the Traditional 401k/IRA or the earnings in the Roth. Both result in a 10% early withdrawal penalty and full tax on the withdrawal. Such is the price of fulfilling our dreams

But what if instead we didn’t use the Roth years earlier? We have $218k sitting there in our brokerage account, ready to use at our leisure without restriction.

And that is why the Roth is last, and why there is a big Maybe for all Roth contributions

(Post Early Retirement, creating a Roth IRA Conversion Ladder as part of our overall tax strategy, is a great practice to minimize long term taxes. This is how we pay $0 in tax on our contributions and $0 on the withdrawals)

Jeremy, I liked this post, but I can’t help but think of the problem of withdrawing money from a Traditional 401(k) (or IRA for that matter) before age 59.5. How do you avoid paying early withdrawal penalties?

The Mad Fientist has written a great article about this that your other readers might enjoy too:

http://www.madfientist.com/traditional-ira-vs-roth-ira/

You might also like this one by MF:

http://jlcollinsnh.com/2013/12/05/stocks-part-xx-early-retirement-withdrawal-strategies-and-roth-conversion-ladders-from-a-mad-fientist/

I wouldn’t so much call it a problem, as there are so many different solutions to early access that the 59.5 age limit is really just a formality. I have a post half written on this topic, stay tuned

Looking forward to seeing that post!

What if you get fired and the new company that you went to has NO benefits, what would be your solution then, saying you plan on retiring in 5 years anyways?

Small pet peeve: there is no need to capitalize all the letters in Roth. It is a last name (named after Senator William Victor Roth), not an acronym. Roth IRA.

With a name that short, the guy deserves a few extra Capital Letters

It’s a bit of a depressing topic, but there are also advantages to a Roth IRA when it comes to estate planning. Who knows what the tax codes will look like in the future, but it’s currently a more efficient way (tax shelter) the estate for your spouse / beneficiaries. So I’d still advocate diversifying into having some (backdoor) Roth IRA contributions, instead of all after-tax brokerage… Too complicated to explain in a comment, but read up on it here: http://fairmark.com/retirement/roth-accounts/roth-distributions/inherited-roth-ira/

Steve is correct. As with any of this stuff, though, rules may change over the (hopefully many) years before you die. This article says that Obama’s 2015 budget aimed to remove this advantage of Roth IRA’s. http://www.marketwatch.com/story/want-to-leave-a-roth-ira-to-your-kids-beware-of-taxes-2014-09-09

@Steve, agreed. My beef with the Roth IRA is during the working years only, when the choice is between pay taxes now or pay taxes later.

You may have seen from our posts on big picture tax strategy that our goal is to Convert every penny from our 401k into a Roth IRA, doing so at the 0% marginal rate over 30+ years in a very long Roth IRA Conversion Ladder

https://gocurrycracker.com/never-pay-taxes-again/

@Robert, thanks for sharing the link, I hadn’t seen that

Our own ultimate estate tax avoidance strategy will evolve to charitable giving, but unfortunately we can’t decide the date

Very interesting read! I need your advice please. I’m 51 years old and have a 401k at work. I am contributing 7.8k per year atm. I opened a Roth this year and am almost done funding 2019(5.5k). Our work just gave us the HSA option this year, so I am gonna max that out. My question is that I am probably gonna have to work until age 62 because I currently only have 185k in 401k, so should i stop the Roth and try to max 401k?? Will I still be able to covert 401k and lump sum pension(250k) into the roth? Trying to figure out if I will have enough time to do the conversions without paying too much taxes…Thank you in advance if you’re able to answer.

Sorry John, hard to say with the limited info here. Please post on the forum and maybe we can figure it out.

Thinking of this in a retirement early thought process, I’m not sure if I entirely agree with the HSA being second, while I understand it saves you an extra 7% or so in taxes, my thought process is if you plan to retire early and use that money by flipping from 401k to IRA to Roth, you limit yourself the income available for early retirement as an HSA can only be used at 65 or for actual medical expenses. Unless you have a HSA work around.

The argument could be made though that if you are contributing only the company match and the HSA you are probably a ways off of early retirement and this wont matter a great deal.

Hi Steven

Yeah, my argument is that you fill up these accounts in order. If you are only contributing enough for company match and the HSA, your working years will be many

On the other hand, if you are saving 50% or more, you’ll fill up the 401k, the HSA, and put many dollars in the brokerage account

Your logic is sound, and I agree access to the HSA would be a problem if you wanted that to function as a source of (non-medical) spending in early retirement

Great point!

Jeremy

Jeremy,

I love the amount of articles you are pumping out recently! Always a great read, thanks for sharing your knowledge and insights. Best.

Thanks!

My Chinese class is winding down, and this final trimester of the pregnancy means we spend more time at home. And also no travel. So I have a bit more time to write

I’m also preparing for the book I’m planning to write :)

Thanks for this, your comment made my day!

Jeremy

The discussion on the tax rate now and in the future reminds me of choosing skincare products. There is always a debate on whether a woman should start using advanced anti-aging products at a relatively young age (like in 20s or 30s) or should they wait till they are in their 50s or 60s to do so. One fear was that there will be no products left to use when you get old if you have already exhausted all the options. This argument always fails to convince me. I would rather enjoy the benefits now and for later, I am sure the technology will keep advancing new products that do wonders. What is the analogy? I would totally go for the tax-benefits NOW. I am sure the technology on tax savings (thanks to inventors like GCC, MF, etc.) will advance to help me save tax later. :)

I never knew there was a debate about skin care products :)

I love the analogy

Why would you rank brokerage before Roth? What’s the upside of the brokerage besides greater liquidity before retirement?

Hi Wh

Good question

Partially to illustrate a point. We have no Roth accounts from our working years, only since starting a Roth IRA Conversion ladder for long term tax minimization

For ourselves and many aspiring early retirement, I view a Roth IRA and Brokerage account as quite similar. We pay 0% tax on Long Term Capital Gains and Dividends in our brokerage account, the same as in a Roth

The brokerage has advantages however. In a down market, I can’t tax loss harvest in a Roth. I also can’t withdraw earnings (dividends) before 59.5, only contributions.

The Roth has its own advantages. It is a good place to hold Bonds or REITs, as payments from those are taxable in a brokerage account. But I already have a 401k /Traditional IRA that I use to hold those asset classes

Let me know if this clarifies things or answers your question

Thanks!

Jeremy

Maybe someone already raised this, but we are in our ‘working years’ and can’t quite get our AGI below that 90K threshold you’ve mentioned, so we do pay taxes on dividends, etc. in our regular mutual fund accounts. In this case, I place the value of putting something in a Roth during wealth-accumulation years slightly higher. But I could be wrong.

No, you are correct

Taxes on qualified dividends would be 15%.

If, for example, you purchased VTI / VTSAX which pays about a 2% dividend, then you would pay a tax equivalent to about 0.3% of assets (15% of 2%)

On $100k that would be $300

Alternatively you could hold a diversified investment that does not pay a dividend, such as Berkshire Hathaway

But this is probably overstated, as we are only talking about $5500 / year / person, the maximum Roth contribution. A married couple might contribute $11k to their Roths, in which case the tax bill would be $11k * 2% * 15% = $33

well, since you put it that way.. ;)

Hey Jeremy,

Just learned of the FIRE movement and been reading on it for days. Cool stuff!

Right now I have 50% in brokerage and 50% Roth. Never had 401K access (in hindsight could’ve opened tIRA). If I were to start FI journey, should I just leave as is? Or could I withdraw all contributions from Roth and put in brokerage? Have maxed the last 4 years.

Once money is in a Roth, I would leave it there forever

Will leave it as is and start adding to tax-deferred accounts then. But my Roth is in retirement and US growth funds so will move them to Total Stocks. Since I’m not withdrawing anything, I won’t be taxed correct? Not even on short-term gains?

There’s no cost in taking contributions out and moving to taxable account. You’ve said you prefer taxable before Roth, so why do you recommend leaving in Roth?

>why do you recommend leaving in Roth?

It’s not so much that I recommend leaving funds in the Roth, it’s that making any change seems premature. You are still early in the journey (both savings and learning curve.)

The asset allocation changes you are making now (your other question) would be taxed in a taxable account, and maybe this isn’t the final change. You’ve also contributed for 4 years (?) so about $20k in contributions – in the big picture it doesn’t much matter where 2% of a full retirement portfolio is located.

The post Roth Hypocrisy may explain more. Learn more, make a long term plan, and then decide if pulling funds out of the Roth makes sense.

Can you explain how you arrive at your computations? Feel free to send me your spreadsheet, if you don’t mind. I want to understand how you claim someone earning $54k per year pays 13.2% but could withdraw $113k from their 401k (both taxed as ordinary income) and still pay 13.2%.

It’s great that you show charts and your conclusions, but I’d like to see the math and numbers driving the charts if it is ok with you. As you know, I’m probably your biggest skeptic but I’m just trying to understand. I’m pretty educated on these topics and I’m not saying you are wrong but I need more convincing.

Ryan and Go Curry Cracker,

I too have been trying to understand this; it is certainly a counter-intuitive, thought-provoking concept! I’m enjoying the discussion.

Ryan, I think it works like this (you don’t need a spreadsheet). He is using his Last Dollar Principle (LDP). Thus, he is comparing a marginal tax rate for the $17,500 401(k) contribution to an overall average tax rate for the distribution during retirement. Thus, he argues that the $17,500 contribution WOULD have incurred taxes of $2502 had it been kept as ordinary savings instead of placed in a 401(k) or deductible IRA. $2502/$17,500=14.3%, i.e., this is the marginal tax rate on the “last” $17,500 earned. If you include the employer match of $1444, then he calculates this as $2502/$18,944, or 13.2%. (I think this is incorrect if you also have an employer matching option on a Roth 401(k). You should stick with the 14.3% in that case, or better, if the match is taxable income, include that tax in the numerator).

As for the distribution, he’s just saying that a family would have to have taxable income of $113,100 before their OVERALL (not marginal) tax rate would be 13.2%. From his figure, that family is already well into the 25% marginal tax bracket, though, which started in the $97k range. I question the legitimacy of the Last Dollar Principle, and this example illustrates the point. If the family withdrew only $97,000 instead of $113,100, then they would have $16,100 less in taxable income–income that would have been taxed at 25%. So if one were withdrawing significant retirement income, the LDP seems incorrect to me. Maybe Go Curry Cracker can further clarify.

One Minor Quibble: A young family during earning years may have tax exemptions for children while older retirees typically do not, so a slight adjustment to the model could be made to account for that, particularly if a lower income family where the child exemption (and maybe even EIC) is a higher percentage of the overall income. This adjustment would make the case for a Roth account slightly stronger.

One Major Quibble: Go Curry Cracker, you discuss RMDs and cite the income at Age 70-1/2 that would trigger a high tax. But, I think that you need to look at all ages, not just 70-1/2. It seems to me that the key question is whether you have reached a sort of “escape velocity” in your investment income relative to your expenses (distributions). If you are withdrawing money significantly slower than your nest egg is growing due to investment returns, then the RMDs will get to be quite large and taxed at high rates. It isn’t necessary to earn 16% for this to be true; you just have to compound the growth for a few more years, i.e., don’t just look at Age 70-1/2 but also at 75 or 80.

For example, I have created a spreadsheet which I can send if you want that illustrates this effect using your scenarios. For example, assume the 90th percentile case. Following your example, I assume $96,000 of after-tax income resulting in $48,000 of annual expenses and $48,000 annual savings into 401(k)/IRAs/HSAs (assuming they can do that much). If we assume this starts at Age 30, and they retire after 16 years, and we acrue earnings only on an end-of-year annual basis, and assume 7% real rate of return (the U.S. stock market average over long time), and conservatively assume no real salary increases during 16 years, then at the end of 16 years they’ll have accumulated $1,338,627. In that 16th year (their Age 45th), their investment income would be $84,434, already almost twice their annual expenses. If they start taking distributions of $48,000/yr, their investment will still grow rapidly because their investment earnings are almost twice their withdrawals. They have exceeded “escape velocity”. But what this means is that by Age 70 they’ll have accumulated savings of $4,229,352 and RMD will be $154,356. Ignoring tax on RMDs (which complicates the calculation but isn’t necessary to make my point) and assuming they reinvest them since they don’t need them to live on, their taxable income will keep rising. By Age 80 they are up to $7,656,585 and RMD is $409,443. At Age 85 RMD is $706,941. Even if we adjust these downwards for the impact of tax on distributions, we still are looking at a high tax rate and huge tax bill. This is why a Roth IRA or 401(k) would help. It would not require RMD (under current law) and even if it did, the distributions would not be taxable. If this family doesn’t take (all of) the 50% distributions starting at Age 46 because they also happen to have a company-funded pension, then the case for a Roth is even stronger.

Don’t forget the estate tax advantages of a Roth account either. Especially if you have grown a large nest egg as in the above example, think how much of this money would go to Uncle Sam if you died and it was dumped onto heirs as taxable income during their own prime earning years.

Second Major Quibble: The Social Security “tax torpedo” can result in significant bumps in marginal tax rates during retirement. There is no inflation adjustment either, so it will get worse. This is a good argument for having at least a significant part of your money in a Roth. http://www.oregonlive.com/finance/index.ssf/2014/10/social_security_tax_torpedo_ho.html

Final remark: As noted in my other post, Obama proposed to force RMDs in Roth accounts. That would weaken the case for Roth but not destroy it, since those distributions would still be nontaxable. However, I think perhaps the most useful idea is to diversify the type of accounts as a form of diversification protection against future congressional actions (and given current US debt levels, these are unlikely to be favorable to taxpayers). I am only in my 50’s and plan to live another 40 years, but if I think back 40 years, the tax situation in the US was dramatically different. Think of all the tax law changes during the past 40 years, including the major overhaul in 1986. It seems reasonable to assume that changes of similar scale will occur over the next 40 years. We can’t predict what they will be or what strategy will be optimal for meeting them. For that reason, diversification into both 401(k)/IRA/HSA and Roth 401(k)/IRA accounts as well as taxable brokerage accounts may provide the best long-run after-tax returns.

Hi Robert, thanks for your great comment

You nailed the 1st $ / Last $ idea in response to Ryan’s question, thanks.

You also correctly point out that a family making large 401k withdrawals would face large marginal tax rates, 25% above ~94k and point out that if they withdrew $16k less they would have only a 15% marginal rate.

That was exactly the point I was attempting to make. A family spending $23k has substantial upside in their annual spending before coming even close to a higher marginal rate than they would have paid in their working years. Even $94k is 4x their current lifestyle. While $114k was the breakeven threshold, they are unlikely to ever come close

re: mQ1

Children, increased exemptions at old age, etc… agreed this will move the 0% tax threshold around. In general, if a family is paying a very low tax rate (e.g. 0%) then take advantage of a Roth now. I think I mentioned something similar in the conclusions

re: MQ1

Agreed, RMDs will increase with age. Would you agree that the probability of having an RMD at Age 70.5 tilt taxes in favor of paying high marginal rates years earlier has low probability? (e.g. 16% annual returns for long periods)

As RMD levels increase with age, this becomes increasingly likely. I agree. The question becomes: Should people choose to work 20% longer, paying taxes now, to avoid paying more tax at 80 years old? With all of the tools available for withdrawal of funds at low or zero tax rates before age 70.5, I think the answer is no

re: MQ2

I just browsed through a couple articles on the SS tax torpedo. Clever name, I suppose. They could also just call it paying a higher marginal rate. As it so happens, I have a post coming on Social Security and will add some thoughts on this topic. The author of the article should compare to the case of if the example Senior never saved in an IRA at all

Re: final remark

Agreed, tax law will change. “The only constant is change”

Note that my issue with Roths is during the working years only, when people choose to pay tax today instead of maybe paying tax years from now

For early retirees, a Roth IRA Conversion ladder is part of the arsenal for long term tax minimization, as we do

https://gocurrycracker.com/never-pay-taxes-again/

I too am enjoying the discussion. Thanks for reading and sharing your feedback!

Jeremy

Jeremy,

RE: re: MQ1.

No, I wouldn’t agree (not convinced yet, anyway). I’m saying that it is easy to generate high marginal rates if one is in a higher income bracket (such as your 90%tile example). Even lower income brackets still run into the issue. It is the power of compounding at work. If you are living frugally and earning just 7% on your investments, but start saving early, you’ll very likely run into the problem I described. That’s what my spreadsheet shows, anyway.

What I’m proposing is that there is probably an optimum ratio of traditional vs. Roth accounts that is related to the ‘escape velocity’ I described. Essentially, you don’t want ‘runaway investment balances’ in your traditional account, but are happy if it occurs in a Roth. So, you should optimize the ratio so that you’ll spend the traditional account money as fast as it earns income, while letting your Roth grow. This optimum ratio will vary depending on your age, accumulated savings, rate of return, and spending rate. It isn’t a question of having to work longer; it is a question of minimizing the overall tax burden, including impact of RMD and SS tax torpedo etc. so as to maximize wealth, which in turn minimizes your working years (if desired).

RE: re: MQ2

For a wide-ranging discussion of how to optimize SS benefits, including minimizing the tax torpedo effect, see https://www.iscebs.org/Documents/PDF/bqpublic/bq212f.pdf.

RE: Re: final remark

I probably wasn’t clear in the remark I made a day or two ago, but my problem is that I can’t possibly convert all the money I need to from a 401(k)/IRA to a Roth IRA. The investment has reached ‘escape velocity’, so the account balance is growing faster than I can convert it. i.e., if I convert enough to take my income up to the top of the 15% bracket, that may involve a $60,000 conversion. Yet, if my investments grew by $100,000 the same year, then I have fallen farther behind on the task of reducing my 401(k)/IRA balances. I’ll never catch up. And so I’ll eventually face RMDs and a big tax liability, and this will kick in about the time I take SS, so the marginal tax rate on SS income will be huge as well.

It becomes difficult to have a continued dialogue in the comments :(

The level for RMDs driving high marginal rates shouldn’t be dependent on income, just on the 401k contribution limit. $10 million 401k value at Age 70.5 would cause any other income to be taxed at 25% or above (~$94k RMD)

I proposed a case of max contributions for 30 years with 16% return hitting that number. It could also be 40 years at 11%

Either scenario is unlikely

I’ve thought through your escape velocity scenario for ourselves. We could think of it as having too much money in a 401k, for example. I think of it as the race against the RMD

I suppose if the account grows at $100k/year, that is a good problem to have. It could go down by $400k this year instead, and you could sneak some more shares into the Roth at reduced prices. Which is better?

I think crafting a perfectly balanced triumvirate of 401k / Roth / Brokerage accounts would be challenging, if not impossible

We can choose to pay tax today to get funds in a Roth, although this does extend working years (during which we also pay more tax.) Using the 4% rule, we know when we have enough to quit working, statistically

In some cases, those funds will grow to incredible levels, causing a case of high taxation later in life. In other cases, you spend your last dollar the day you die. On the day we choose to stop working, we don’t know which case will apply. In your case it sounds like the former

I think a detailed post about your scenario and the challenges to minimize lifetime taxes could be an interesting read

Thanks for the SS link, I’ll give it a read

Yes, it gets hard to continue this dialogue as the reply is no longer linked to your response. But anyway, responding to your reply at 2:14 a.m. 1/31/2015…

I think we have a factual disagreement, which is the best kind since we should be able to easily resolve it. I may be making a mistake, or it may be you. If I understand you right, you are saying that RMD for a $10MM nest egg would be about $94,000. I calculate a much larger number. The IRS tables gives a distribution period of 27.4 for Age 70. $10MM/27.4 = $364,964. That’s several times your calculated RMD. Correspondingly, to get to $94,000 RMD at Age 70 would require a nest egg of only $2,675,600.

In the scenario I outlined above, I said, “assuming they can do that much”. I think I was a little high since max per couple in 2015 is $36,000 for 401(k) and $6650 for HSA. But let’s be more precise here, and I’ll even be liberal and ignore the HSA part, plus also I’m not counting any employer match on 401(k). If I put after-tax income at $72,000 so that the 50% savings rate is $36,000, that equals the maximum 2015 401(k) contributions for a married couple where both work and are contributing the max. Assuming spending of $36,000 as well, and still assuming starting earning/saving at Age 30 (could certainly be earlier, so this is conservative) and working/saving for 16 years with 7% returns, I calculate that the nest egg at retirement is $1,003,970. By Age 70 (assuming both spouses are same age), the couple will have a nest egg of $3,172,014 with RMD of $115,767. That will be mean a significant amount of the RMD will be taxed at the 25% rate, and their SS will be taxed at a high marginal rate too. If they have a pension, it too will be taxed at high rate. By Age 80 the nest egg is up to $5,742,439 and RMD is now $307,082. And it just keeps getting worse. (Note, btw, that I’m not assuming contributions for 30 years, but only for 16 years, and at just 7% return).

Yes, it is a good ‘problem’ to have. But if the problem can be avoided, all the better. It needn’t lengthen their required working careers; by definition, if their retirement income is growing faster than their savings, then they saved “too much” (if trying to minimize working years). There are ways to pull the future investment earnings forward. For example, if they invested in a Roth, they could have started withdrawing principle.

And, I guess my philosophy is different than yours in that I truly want to minimize the amount of my estate that goes to Uncle Sam. (Unlike you, after I die, I’ll still be upset by him taking a large take! LOL). I don’t expect my estate to be so large that it will ruin my heir’s motivation. I’d be pleased to leave grandkids or great-grandkids enough to fund college education, start a business, etc. I also want to leave assets for charity, but we can escape taxes on that part, I think.

And on your (I think) somewhat facetious comment, I would of course rather have my account grow that drop. Paying more tax is good if it means you had more income. But, if in fact you could time things perfectly (and you can’t), it would be ideal to do 401(k)/IRA to Roth conversions at market bottoms. If the market would drop 75% now, I could get all my accounts converted. I just would need it to fully recover (and then some) shortly thereafter! LOL.

I’d appreciate your comments on where I made an error, if it was me.

We are in the accumulation phase now and trying to optimize pre-tax vs post-tax money. We put about $58000 per year in pre-tax (401k/IRA/HSA). We only aim for around 20k in after tax retirement income (so roughly 500k in retirement assets). Do the growth rates above include inflation? The tax free zone (standard deduction) and spending will grow with inflation. So, the impact of RMD would lessen if you factor in inflation. I don’t think we can count on 7% return after inflation. Typically, we assume 7% total return with 4% spending and 3% inflation. Am I missing something here?

>Do the growth rates above include inflation?

Of course. Else it would just be meaningless gibberish.

>I don’t think we can count on 7% return after inflation.

The total real (meaning inflation-adjusted) return of the SP500 since 1871 is… 7%.

Thanks for the clarification! I assumed it was less since it is common to use the 4% to estimate the portfolio size required. Also, the 10% ROI may be the overall average, but how do we know that is what any given 30 year+ timeframe will yield this result? If this is the case, then can the 4% rule be increased to 5% or 6% instead? By withdrawing a larger percentage, we could retire even sooner.

We fully utilize all ore-tax accounts and shelter around 58k per year which saves us roughly 10k taxes. We spend at or less than the standard deduction, so the plan is to be at zero % tax rate in FIRE (or very close).

One main issue we are trying to navigate for the first 5 year Roth pipeline is healthcare (will likely need some cash or post tax money to keep our MAGI low enough to qualify for cheap healthcare). Our MAGI will be higher than true spending during this time since we need to start the Roth pipeline. Thanks for the reply!

>how do we know that is what any given 30 year+ timeframe will yield this result?

You don’t. Thus 4%. 4% is the worst case for sustained withdrawals in the historical record.

See example: The Worst Retirement Ever

Also see how the 4% rule was made: What is Your Retirement Number – The 4% Rule

Not sure if this is true in all 401(k)-type plans or not, but as a government worker, even if I select the Roth TSP option, the matching funds automagically go into the Traditional TSP so that they are taxed eventually. Is this different in the private sector?

Same deal in private sector. Employer matching funds for a Roth 401(k) are taxed just like funds in a traditional IRA. It is taxable income, and subject to early withdrawal penalties as well.

Hi Ryan

I welcome the skepticism and critique. My wife tells me all the time about all of the mistakes I make, so I’m used to it hahaha

My spreadsheet is a mess, as I only made it for personal use. With that caveat, here is a copy: http://1drv.ms/1vik43H

Robert’s comment just below this one explains things very well. For funds contributed to the tax-deferred account, we pay today’s marginal rate. For funds withdrawn, we pay an average rate.

Let us know what you think after having a chance to dig into it

Thanks!

Jeremy

Good post and numbers, Jeremy!

BTW, you can still contribute to a traditional IRA even if you’re contributing to a traditional 401k. You get full deductibility with married filing jointly MAGI <98k, then partial, phasing out at 118k:

http://www.irs.gov/Retirement-Plans/2015-IRA-Deduction-Limits-Effect-of-Modified-AGI-on-Deduction-if-You-Are-Covered-by-a-Retirement-Plan-at-Work

There are a few people (I happen to be one) whose MAGI is above this but below the ROTH IRA limit for contributions of 183k, so it makes sense for me to put additional savings in a Roth IRA after maxing my traditional TSP and HSA. Roth limits here:

http://www.irs.gov/Retirement-Plans/Amount-of-Roth-IRA-Contributions-That-You-Can-Make-For-2015

Thanks Kendall!

Duly noted on the TIRA contribution deduction. I stand corrected and will make a change in the post

Agreed on the Roth IRA contribution at your income level. This is effectively #7 on the list of accounts to contribute to. If you can do it, there is no harm in contributing

Note that if you use that account to invest in stock, post retirement the brokerage account has similar tax treatment, with an effective 0% tax on Long Term Capital Gains and Qualified Dividends. The brokerage account also has the advantage of being able to harvest losses when they happen, and also allowing access to earnings (dividends) prior to Age 59.5

That said, with the $5500 limit +/-, you’ll still end up with both types of accounts

Cheers

Jeremy

That has been my thinking as well. My wife and I will be able to contribute to our respective Roth IRAs for a few more years, after which our MAGI will hit $191K and we won’t be able to contribute anymore (even taking into account as and when the limits are raised, as has been the case the past few years). Even if it means not going contributing the full amount for 401(k).

Thanks for a such a great and in-depth article!

At $191k+ MAGI, financially speaking you would benefit from maxing the 401k over contributing to a Roth

I prefer the brokerage account over Roth, but the 401k first and foremost

Actually, even when your MAGI exceeds $191K, you can still contribute to a Roth IRA via the “backdoor Roth IRA conversion”. The tax implications are really complicated, unless you have no traditional IRAs or $0 in your traditional IRAs to begin with. In that case, you pay no taxes on the converted amount as long as there is no gain. Fidelity has a calculator which helps you figure out all of this:

http://personal.fidelity.com/misc/widgets/IRA_Evaluator/IRA_EVAL.html

Yes, that is effectively #6 or #7 on the list, depending on how you do it

I am generally fine with the order of 1-5, but I would switch the order between 6 and 7. Roth IRA is still better than taxable even for an early retiree. First, taxable accounts are fully exposed in liability claims, while Roth IRA is generally (but not always) protected from creditors according to the Bankruptcy Reform Act of 2005. For early retirees who saved aggressive in working years, it is inevitable to have a large taxable account. Second, for estate planning purpose, if your heir inherits a Roth IRA, he or she has the option to receive tax free distributions over lifetime (restrictions apply). Doing so can prevent taxation of the earnings (including dividends) for many decades if not longer. If the heir inherits a taxable account, he or she will get a step-up in basis, but the dividends generated could still be taxed at 15% every year if the heir is a high income earner with a margin bracket of 25% or higher. Having taxable dividends will make MAGI unnecessarily large, which could disqualify the heir with other tax credits and deductions. Third, having a Roth IRA is good for diversification purpose. If one has tax deferred (401k), tax free (Roth) and taxable accounts at disposal, one can easily engineer the type of income mix needed in order to qualify for ACA subsidies while maintaining the same living standards, since most early retirees need to purchase health insurance over the exchange. Fourth, for FAFSA purpose, Roth IRA is not considered in the calculation, while taxable accounts are. This last one is trivial, since the kid is unlikely to be qualified for any need based financial aid when the parents are FI with lots of assets.

Thank you for the thought-provoking article!

Thanks LF

Judging from the comments, many people will agree with you :)

I don’t feel strongly one way or another if GCCjr has a higher tax bill due to an inheritance, so I haven’t studied it really at all. I’ll be dead. And I certainly wouldn’t pay taxes myself at a high marginal rate to allow our heirs to pay a lower tax. Unless the death is sudden, we’ll likely give away most of our wealth before that occurs anyway. I like Warren Buffett’s comment on this: “a very rich person should leave his kids enough to do anything but not enough to do nothing”

I’m also not particularly worried about liability claims. At least not beyond the value of perhaps a simple umbrella policy, and a 401k already provides protection in this area

I agree on the value of having an account with tax free gains and such, which is part of the reason that we are creating a Roth Conversion ladder. But I view this as a secondary benefit, a side effect of minimizing our long term taxes on withdrawals from the 401k

Thanks for the great comments. I can see others prioritizing these things differently

Cheers

Jeremy

“Traditional IRA if tax deductible (not the case if you have a 401k)”

^This requires correction. Participating in an employer-sponsored plan, like a 401k, does not automatically prevent someone from deducting their tIRA contributions. A single-filer 401k participant with a Modified AGI of $61,000 or less can deduct the full amount of their tIRA contribution. For MJF, the limit is higher. If you pass the limit, it is still possible to deduct part of your contribution, up to a point. At high income levels, the deduction benefit does go away.

see: http://www.irs.gov/Retirement-Plans/2015-IRA-Deduction-Limits-Effect-of-Modified-AGI-on-Deduction-if-You-Are-Covered-by-a-Retirement-Plan-at-Work

Thanks for the correction

You covered the most common vehicles – but what about those with SEP or SIMPLE IRAs as their workplace retirement plan? or those that dont have access to the high limits of a 401k (or equivalent 403/457)

Hi Jeff

In that case, replace Traditional IRA or 401k in the text with your tax-deductible tax-deferred plan of choice. The main focus is using the tax advantage today

Loved the post. I just had dinner with a buddy of mine 2 nights ago and we talked about early retirement strategies for 3 hours.

A couple of comments:

* The 0% tax rate on dividends + LT capital gains will persist in the future. This link shows that tax rates on investments change a lot over time.

* I think your advice that taxable brokerage trumps Roth IRA is debatable. Roth is better when you consider it a hedge to tax law uncertainty (see above bullet). Brokerage is better since you can live off of interest at any age (including early retirement), whereas with the Roth you can really only draw the interest when you’re an old man (principal is ok). Brokerage is worse due to tax law uncertainty + the dividend taxes during working years at 15%/20% depending on your income before retirement.

With Obama attacking 529 tax benefits a week ago (and apparently facing much resistance for it), I don’t think it’s unreasonable to be worried about how quickly these tax-sheltered investment vehicles can be revoked. The one thing I’m really worried about in the future is a wealth tax, which luckily nobody currently is talking about.

However, the strategy of simply living like a king below the poverty line in retirement (through frugality + outright ownership of home and elimination of mortgage, for example) is a strategy that is likely to pay off no matter what the political landscape is in 40 years. No party that I’m aware of is willing to throw “poor” people under the bus. I just don’t know when the US will wake up to the fact that living on $25k/year can be luxurious.

I agree that it would be nice to see the XLS file so we can pick it apart and add improvements. Between the readers of the blog, we can totally defeat the US tax code.

Dumb typo. Meant to say “The 0% tax rate on dividends + LT capital gains **may not** persist in the future.”

I would be surprised if the tax law didn’t change

I didn’t create the xls for general consumption, but here is a link: http://1drv.ms/1vik43H

A Roth has pros and cons. In addition to those you mentioned, in a down market you can’t harvest capital losses in the Roth

Good thought provoking discussion. Do not be so certain on the topic if you have not analyzed all angles. One important advantage of Roth 401k over traditional is it effectively expands your tax shelter. 17,500 when withdrawn from traditional 401k is taxed where as Roth is not so if you contribute 17,500 or 18K in Roth you are effectively expanding the tax bracket. The finance buff did a good article and provided a test spreadsheet and concluded that even if you get a bump down in tax rate after retirement saving in Roth 401k evens out with traditional 401k IF you can manage to max out Roth 401k.

Second I do not understand why would Roth be lower than a taxable account in any circumstance. As Roth allows you to withdraw the amount contributed without any penalty you have 16 years of your contribution that could be withdrawn before 55.

Let us create a spreadsheet and play with it.

A Roth can extend your tax footprint, but can restrict it as well

Losses in a Roth are not tax deductible, for example

Please share the article you mentioned if you get a chance, it sounds like an interesting read

Here you go

http://thefinancebuff.com/roth-401k-for-people-who-contribute-max.html

Thanks Pop

Looks like a good site, I read a few of his articles. His post on why most people should choose the Traditional 401k over a Roth 401k is a good one

The xls is analyzing the marginal dollar, basically the last dollar invested, and arguing that there is an advantage in some cases for a Roth 401k because you can tax shelter a greater amount of income

So far so good

But what about the $17,499 before that last dollar? The number used for “marginal tax rate at Retirement” should be the average rate, as some of the withdrawal will be taxed at 0%, some at 10%, and so on

Or using our example, and that of many early retirees, the marginal rate, cap gain rate, and dividend rate = 0%, which results in a 20-25% loss for the Roth

re: your question, why would a Roth be lower than a taxable account: See addendum to the post above

People often cite being able to remove principle as an advantage of a Roth, but why is everybody in a hurry to remove money from a tax-sheltered account? And why restrict yourself from having access to the earnings before Age 59.5 without a benefit? If I’m going to let the IRS tell me how and when I can use my savings, I want something in return

Roth Ira is not for everyone but most people in US can benefit from it. In our case, it is a godsend. It wasn’t for high income, I would have Roth 401k for TSP. My unique investment makes me love Roth Ira even more than others. Big tax benefits forever.

Hi Young, can you expand on your comment? What are the unique investments and how big is big?

Just wanted to mention, a Traditional IRA could still be deductible even if you have a 401K. It’s based on modified AGI.

http://www.irs.gov/Retirement-Plans/2015-IRA-Deduction-Limits-Effect-of-Modified-AGI-on-Deduction-if-You-Are-Covered-by-a-Retirement-Plan-at-Work

You also mentioned a Roth being a good idea when you’ve already maxed out your Traditional 401k and have additional funds to invest. However, the max contribution amount ($18K for 2015) applies to all accounts. So if you’ve maxed out your regular 401K, you cannot contribute more to a Roth 401K.

http://www.irs.gov/Retirement-Plans/How-Much-Salary-Can-You-Defer-if-You%E2%80%99re-Eligible-for-More-than-One-Retirement-Plan

Thanks Dave

Sorry, I was referring to contributing to a Roth IRA after contributing the max to the 401k.

Good point on the Traditional IRA still being deductible below the MAGI threshold. I’ll modify the post to reflect that

Cheers

Jeremy

Dave, there may be exceptions depending on where you work. At my place of employment, I can fully fund the traditional 401k along with catchup funds totaling $24K AND up to $10K in a Roth 401k company sponsored 401k program. I called my benefits dept. specifically to confirm this question.

You can do this while at the same time funding a personal Roth IRA account $6500.00 if your 50+ years of age.

Want to add one more thing…To Jeremy’s point, I agree, would prefer the pretax traditional IRA but cannot because income is to high for a single person and the traditional IRA. My only option is the Roth IRA with additional after tax dollars. :(

Hi Bob, the catch-up contributions you’re eligible for is due to your age, not your companies specific plan. Every company plan is subject to government/IRS regulations. They may limit or restrict catch-up contributions, but they can’t allow you to go over the maximums established by the government regulations.

Here is what the IRS says (notice it states “pre-tax AND Roth”):

===

The amount you can defer (including pre-tax and Roth contributions) to all your plans (not including 457(b) plans) is $17,500 in 2014 and $18,000 in 2015. Although a plan’s terms may place lower limits on contributions, the total amount allowed under the tax law doesn’t depend on how many plans you belong to or who sponsors those plans.

If you are age 50 or older by the end of the year, your individual limit is increased by $5,500 in 2014 and $6,000 in 2015 (the catch-up contribution amount). This means your individual limit increases from $17,500 to $23,000 in 2014 and from $18,000 to $24,000 in 2015 even if neither plan allows age-50 catch-up contributions (IRC Section 414(v) and Treas. Regs. 1.402(g)-2).

===

So I’d have to say the benefits person you talked to is wrong about you being able to contribute an additional $10K to a Roth 401K if you’ve already maxed out your traditional 401K.

I’ve talked to my benefits dept several times, and they are generally clueless about the actual regulations. All they can do is read the benefits documentation and interpret what it means. This stuff confuses the heck out of most people.

Almost forgot… Your statement, “You can do this while at the same time funding a personal Roth IRA account $6500.00 if your 50+ years of age” isn’t exactly correct…

True, you can contribute to a Roth IRA even if you participate in an employee-sponsored retirement plan.BUT, eligibility is based on income (modified AGI).

Here’s the official IRS page for this year:

http://www.irs.gov/Retirement-Plans/Amount-of-Roth-IRA-Contributions-That-You-Can-Make-For-2015

If you make really good money, you might not be able to contribute anything to a Roth IRA.

Dave. Thanks for the input. I will do some more digging about the work 401k and Roth 401k. On the personal Roth, yes I can have one.

I make too much for the tIRA but come in just under the salary cap upper limit for the Roth. I’m single (due to end this year) and 57 years old.

My money is in funds that pay a high dividend. These dividends are not a qualified long term dividends unlike the ones from stocks. the yield will be taxed as income in taxable account. 9 out of 14 funds that I own pay a special dividend. Year over year, an average annual rate(9.20%) + a fat special dividend = nothing but paying high taxes, unless I have these in Roth.

1) if a family of 4 has $54,000 in income I doubt they pay any federal income tax above social security.

In which case deductions for retirement contributions are worthless and a Roth IRA is desirable.

I also doubt that a family for four making $54,000 and saving $17,500 could live on $36,500 since as a single person I spend about $30,000 / year with only about $3,600 going to housing since house is paid for, I heat with wood I cut, and my electric is from off grid solar.

I forgot to add that I believe you should

1) contribute to 401k up to match.

2) Then max out a ROTH IRA. If a 401k Roth is available maxing that out is ok also.

3) Then contribute to a taxable account.

4) I would NEVER contribute above the match to a regular 401k.

You can spend down a taxable account tax free up to about 40,000 ( single) to 80,000 ( married) in GAINS before withdrawing from 401k / traditional IRA and then Roth.

You are welcome to use our income tax calculator to ease your doubts.

I forget to tell you what investments I have and how big that you asked. I will just give you a few examples. I own PDI 1200 shares, as of now pays 7.56% annual div. and $1.8362 paid in 2014 as a special div. PKO 800 shares, as of now pays 9.24% annual div. + $1.5939 paid in 2014 as a special div. PTY 1518 shares, as of now pays 9.28% annual div + $0.6498 special div. JRI 232 shares, now pays 8.06% annual rate + $1.1791 paid as special. DMO 1428/SH, as now 7.81% annual rate + $1.2161 special paid in 2014. I made a little over $7000 as a special dividend alone last year. JRI is in my Roth, I just didn’t have money to buy more shares, I could buy more in taxable account but I didn’t. 1/3 of our Roth is in CDs that are ready to be matured soon. I enjoyed having our Roth in CDs that paid over 5% annual rate for 7 years through all those tumultuous years of 2008,2009. As time goes by, Roth is going to be bigger but investments in taxable will be smaller. special dividend for 2015 will doubled of 2014, if it is not more. I invest most of our money in CEF(closed end fund) that are invested in long term bonds only and pay dividend monthly. I hope that I answered your questions.

Definitely holding these kind of funds in a tax advantaged account is the way to go.

Jeremy, thanks for another excellent article! I second the cheers for the increased posting volume — keep churning them out!

One question: In your ranking, why are after-tax 401k contributions for Backdoor Roth (#5) and direct Roth contributions (#7) ranked differently? These two are functionally equivalent, so on what basis did you draw a distinction between them as far as priority over taxable brokerage investing?

One possible answer is that with after-tax 401k investing, you can let the earnings grow (tax-deferred) inside the 401k for the duration of your working career and then, upon retirement, split them off into a traditional IRA to become part of your Roth conversion ladder. But I wasn’t sure if this is necessarily what you were getting at…

Thank Brooklynguy!

I suppose part of the answer is because I thought I was going to get enough flack for putting the Roth at #7 :)

My initial thinking was that the limit on after-tax contributions to the 401k is much larger than for a regular Roth contribution, but all of the comments made me think about this a lot more and now I think I’m more inclined to moving backdoor roth to #6.

Yeah, I think you either have to bump up “brokerage” one spot or give in to the flack and push it down one spot, because there’s no principled distinction between # 5 and #7 — it doesn’t matter whether you take the “front door” or the “back door”, both options take you to the same place (unless, as I described above, you hold off on using the back door in the after-tax 401k option–i.e., you don’t take in-service distributions–for the duration of your working career, which allows you to fold the earnings into the Roth conversion ladder instead of keeping them locked inside the Roth account).

Also, on the Roth’s benefit that others have raised of protection against future changes in the tax laws: just to be clear (and to put it in the same terms you used to describe your preference for Roth over Traditional during the working years), in exchange for the benefit of guaranteed penalty-free early access to the funds, you are choosing to “maybe pay taxes later” instead of “definitely not paying taxes later” (because the Roth insulates you against changes in tax laws that have the effect of defeating the purpose of all your careful tax planning, such as elimination of the 0% rate for LTC gains + dividends and/or the other features of current law that promote leisure over labor).

I agree, and have made a change to the order, putting the back door Roth at the bottom

re: tax law, I think there is only one thing we can be certain of, and that is that future tax law will be different from present tax law

We could certainly make assumptions about what changes are likely. I think it fair to assume that taxes on “the wealthy” will increase. This could include increases in taxes on dividends and capital gains. But it could also include taxes on “too much” in tax-deferred accounts, including a Roth

I would also assume that there will be efforts to not increase taxes on the middle class, so taxes on dividends and capital gains for those who Live Well for Less, as we do, is less likely than for the 1%

But anything is possible. Taxes today are at historical lows, and deficits and debt load continue to increase. The government will need to get funds from somewhere

Excellent points, thanks brooklynguy!

Although I would never call anything impossible, I think the possibility that a future version of Congress will cause the government to effectively renege on its obligation to hold up its end of the deal being entered into with today’s Roth account-holders and retroactively deny them the core benefit of the bargain is *far* more remote than the possibility of the realization of any of the myriad potential changes in tax law that would have the effect of rendering taxable accounts the suboptimal alternative.

One additional consideration that I don’t think has been raised so far is that for people who live (and plan to stay) in a state with income taxes (especially high income taxes) that does not provide the same favorable 0% tax treatment for low income brackets as the current federal scheme (like my home state of New York), the state (and, in my case, local city) tax benefits of Roth investing may also tip the scales in favor of Roth accounts even assuming no changes in tax law.

Finally, now that you’ve moved Roth investing to the bottom of your hierarchy, it may make more sense to simply remove Roths from the list altogether and add a note at the bottom that the rule of thumb rankings recommend no Roth investing at all (that’s essentially what they’re doing now, since there is no limit on the amount of taxable investing a person can do and nos. 6 & 7 will therefore never be reached).

Thanks for the excellent discussion! You’re giving the Mad Fientist a run for his money as the most tax-savvy FI blogger out there.

Wow, that compliment is a big one, MF is a very intelligent guy and I really like his blog. Thanks Brooklynguy!

I agree an outright elimination of the contract is unlikely, but means testing on SS could have the same effect for example. Recent conversations around eliminating the Roth backdoor are underway, it wouldn’t surprise me if more were to follow.

I agree, State taxes need to be considered. I found moving to WA to be much preferred over my home state of MN, but I guess some people like snow (and high taxes) and somehow continue to live there quite happily

Can you explain where the 385k numbers came from?

With no other income, if a Married Couple Filing Jointly were to withdraw $385k from a 401k, they would pay an average tax of 25% on that withdrawal

This comes from the tax table. The first ~$20k is taxed at 0%, due to standard deduction. The next ~$20k is taxed at 10%, the next $50k at 15%,and so on. Some of the funds are taxed at the 33% rate, but the average comes to 25%

I’m new to this blog so forgive me if you (likely) already address this, but how is the first $20k per person 0% taxed? The standard deduction is much less than $20k. What am I missing?

Hi Susie. It wasn’t stated as $20k per person, but as $20k for a married couple filing jointly. Standard deduction in 2014 was $12,400 + 2 personal exemptions of $3,950 each for a total of $20,300

Saving within a concessionally taxed environment should always be preferred. We have a similar approach here in Australia, where superannuation contributions are generally only taxed at 15%, compared to up to 46.5% for income tax.

Definitely an incentive to contribute!

Great article, Jeremy. It definitely made me rethink my strategy of stuffing my Roth IRA with as much of my investable dollars as possible (through mega-backdoor as well as backdoor contributions).

One question for you… Even if in early retirement, I plan to be in the 15% tax bracket and not pay taxes on capital gains, while I’m working (which I will be for the next 10 years), I’m in the 28% tax bracket. Doesn’t keeping my money in my Roth prevent me from paying taxes on the dividends? If I were to put these funds in my taxable accounts, I would owe lots of taxes now. Also, rebalancing can be difficult in a taxable account, since it can trigger capital gains taxes, but no so in a Roth. Though I definitely hear your argument for tax loss harvesting, unfortunately(thankfully?) there hasn’t been much of an opportunity to do so lately.

Maybe I’m missing something? Thanks again for the great article! Really love all your posts on taxes as well as the MF’s. You guys are the best.

Thanks Emanonrog

Everything you said is true. You will owe tax on dividends and if you re-balance by selling, you will also owe tax on the gains. Also if you choose to own bonds or investments that pay non-qualified dividends, those will be taxed at your marginal rate in a brokerage account and 0% in a Roth

Maybe we can compare with some numbers

If you are at the 28% marginal tax rate, and can’t lower it any further then any qualified dividends or long term capital gains will be taxed at 15%.

Assume you purchase VTI/VTSAX as your investment vehicle, and it pays a dividend of 2%. A 15% tax on that 2% would equate to a load on the fund of about 0.3%. If you have $100k invested, this would be about $300/yr or about $25/month. Don’t forget to include State tax

It is more than $0, but $300 probably isn’t going to derail your early retirement plans. Many Mutual Funds have larger expense ratios. It is a tradeoff

For Capital Gains, since you are continuing to save a large percentage of income, you could fix your asset allocation by using new funds to purchase the asset that is currently below your allocation target instead of selling an accumulated asset

I agree, there haven’t been a lot of opportunities to harvest capital losses recently. For somebody saving aggressively this is probably negative, as the best thing that could happen to accelerate your early retirement is a major market correction

https://gocurrycracker.com/reminiscing-about-the-glory-days-of-2008/

Thank you very much for reading and your very kind comment. It is hearing things like this that inspires me to keep writing, I appreciate it

All the best

Jeremy

On tax loss harvesting (TLH), don’t forget that TLH only really benefits you during the accumulation phase. Once you’re in retirement, continuing with the assumptions that you are “living well for less” and tax law remains as is, TLH won’t save you any money because you’re not going to have any tax liability anyway (TLH can help you manipulate your income and allow you to withdraw more of your funds tax-free and/or accelerate your Roth conversions in the Roth conversion ladder, but it won’t actually save you dollars the way it will during the working years).

Agreed. My primary motivator is for TLH to help us in the race against the RMD. While it won’t save us any $ in the year of the loss, it may save us $ from Age 70.5 and beyond due to accelerated Roth conversions

Thanks for your quick reply!

You make a great point on rebalancing through new contributions. I’ve always set my contributions equal to my target asset allocation, and rebalanced at the end of the year. But since I’m early in the accumulation phase, my contributions are large relative to my portfolio and I could easily maintain my target AA through new contributions.

Here’s hoping for a repeat of ’08!

Happy travels.

Jeremy,

I can’t thank you enough for your blog. I just wish I had the information you and

your commenters present when I was your age. You are definitely wise beyond

your years. I wish I knew how to get your blog in front of every 30 something I

know and all the ones I don’t. Your two cents is worth millions!

This kind of discussion should take place in the financial press, which is, for the

most part, devoid of useful information.

Wow, thanks Warren! I really appreciate your very kind comment

I wouldn’t mind if you tried to share GCC with everybody via reddit, twitter, etc… :)

I think the best part of this post and several others is the conversation that happens in the comments. It’s a constant learning process

Now stay tuned for a nice guest post from Jim Cramer! lol

Hi!

Thanks for this post! I’ve also read through the comments, but still have two unanswered questions I was hoping you might be able to clarify. First, is there a limit on the IRA conversion from 401k? Can you rollover any amount you like per year? Second, does your employment status impact this at all? After FI, I may still do some freelance work for the current employer. I wasn’t sure if you are required to leave employment in order to do a 401k rollover?

Typically you would rollover the entire 401k to a Traditional IRA, there is no limit. I’ve seen some cases with a TSP (Federal employee 401k account) where they do a partial rollover, but can’t think of any real advantage of doing the same with an employer. It is best to have your employer transfer the funds directly to the IRA Custodian and never touch the funds yourself

Once you terminate employment, you are free to do a rollover. Doing freelance work after the fact you are likely a 1099 employee, i.e. a self employed contractor (I presume.) But yes, you must terminate employment to do a 401k rollover

Thoughtful post for sure. I’ve been struggling lately with most efficient way to reach FIRE. I keep going back and forth on whether I should devote my savings (above 401k max and HSA max) to taxable or Roth accounts.

Being 39 and having only ~ 20k in taxable investments currently, I’m really going to need to crank up the taxable account contributions in order to reach early retirement between 50-55 years old. Question is whether I do that at the expense of Roth accounts. I will need access to the funds to bridge the gap between retirement date and age 59.5.

I’ve also been thinking that perhaps I don’t need to be maxing out my 401(k) for too much longer. While I only have 20k in taxable accounts, I have ~ 8x that amount in a mix of 401(k), IRA and Roth accounts.

I am in the 25/28% tax bracket now and plan on beginning the Roth conversions as soon as I retire. By the time I’m old enough for RMD’s, I either want all of my balances already converted to Roth or to have the balances so small that the impact is minimal.

I currently have the ability to save ~ 70% of my take home pay, adding back 401(k) deposits. Now is the time to make hay, as they say! But, I’ve just not decided where to park those funds!

Thanks GG. Great name!

There is a middle ground, perhaps. Since you are saving 70% of income, you can likely contribute full amount to 401k, HSA, Roth, and still end up with a lot of funds in a taxable account.

Since the gap between your target retirement age and Age 59.5 is relatively short, you could consider doing an SEPP to access your 401k funds without penalty.

As discussed here I would recommend continuing to fund 401k and HSA to reduce tax paid at 28%. Basically, take the tax deduction now

Just a couple quick question regarding SEPP and FI since I have never heard of a Roth Conversion Ladder used at the same time. If I was to set up a SEPP would that prevent me from pulling money out of my 401k and into the Roth without increasing my tax liability? I am currently 35 and just started my journey to FIRE. I plan on having $600k in 401k, $55k in Roth IRA, and $125k in Vanguard to help float me the 5 years for the ladder once I hit FI in 9 years. Unfortunately my income is too high for a traditional IRA and my company doesn’t allow for after tax contributions or in-service disbursements. So if I am correct in your explanation, Getting that $55k into the Roth won’t really help me in any way in starting my conversion ladder at FI?

This article is fantastic and I click on your website multiple times a day hoping for another one of your adventures. You both are an inspiration.

Warmest Regards

Thank you kindly, Thor! It always brightens our day knowing that people benefit from reading GCC

Money withdrawn from a tax-deferred account is taxable no matter how it is done. So if you were to setup a SEPP you probably wouldn’t want to do a Roth Conversion as well. They are just 2 different strategies for accessing tax-deferred accounts before Age 59.5, each with their own pros/cons

In your situation, you can do the conversion ladder whether you have another Roth or not. We had no Roth when we retired, and only created one for our ladder

The question is would you want to have access to the earnings on that $55k or not? The tradeoff is paying tax on any dividends during the next 9 years

If you have $55k invested in VTI / VTSAX at a 2% dividend, and pay 15% tax on those dividends, you would have a tax load of $165/year in the brokerage account and $0 in the Roth (plus any state tax)

But then after you stop working, you can use the $1100/year in dividends federal tax free if in the brokerage, but can only withdraw contributions from the Roth

Awesome! Thanks for the response! I find this all incredibly eye opening. I would gladly pay $165 a year in extra tax to have access to those additional funds once I retire at 45. It looks like you have successfully won your case with me as I will be opening a Vanguard traditional IRA and a taxable account this week. Wishing you all the best and congratulations on the baby.

“Since Mr and Mrs 90% didn’t sell any of their stock they generated no capital gains.”

Executing a basic fixed-asset allocation investment strategy requires regularly selling stock. At the income levels of Mr. and Mrs. 90%, wouldn’t this mean they pay some capital gains?

Hi Caleb, I would rephrase

Executing a fixed-asset allocation investment strategy SOMETIMES requires selling stock

Depending on how much your asset allocation is out of whack, and the overall size of your assets, it is often possible to adjust the allocation just by using new funds to buy the down asset

An overly simplified example:

Target allocation is 50% stock / 50% bonds. On Jan 1 you have $100k total, and at year end Stock is up 10% and Bonds are down 10%.

You’ve saved $10k during the year and want to adjust allocation, so you buy $10k worth of bonds and you are now back at a 50/50 split.

Alternatively, Mr & Mrs 90% could adjust allocation in the tax-deferred accounts, bringing total assets back into alignment with the target allocation while leaving the assets in the taxable account untouched

If the situation is more complicated than that, then any long term capital gains would be taxed at 15% and short term capital gains at the marginal rate

Lots of discussion around this topic for sure!