The US tax code includes an Estate Tax for inherited wealth. Oligarchs and other opponents of such a tax like to refer to it by a more ominous title, The Death Tax. Ooh, scary.

After the passage of the Tax Cuts and Jobs Act of 2017, this tax applies only to households with more than ~$11 million per adult (~$22 million per couple.) Fewer than 0.2% of US households qualify. (*)

I’m personally more concerned with the tax that will apply to the other 99.8% of us. The real death tax.

The Real Death Tax

Throughout this blog, I’ve shared countless tax reduction and tax minimization scenarios.

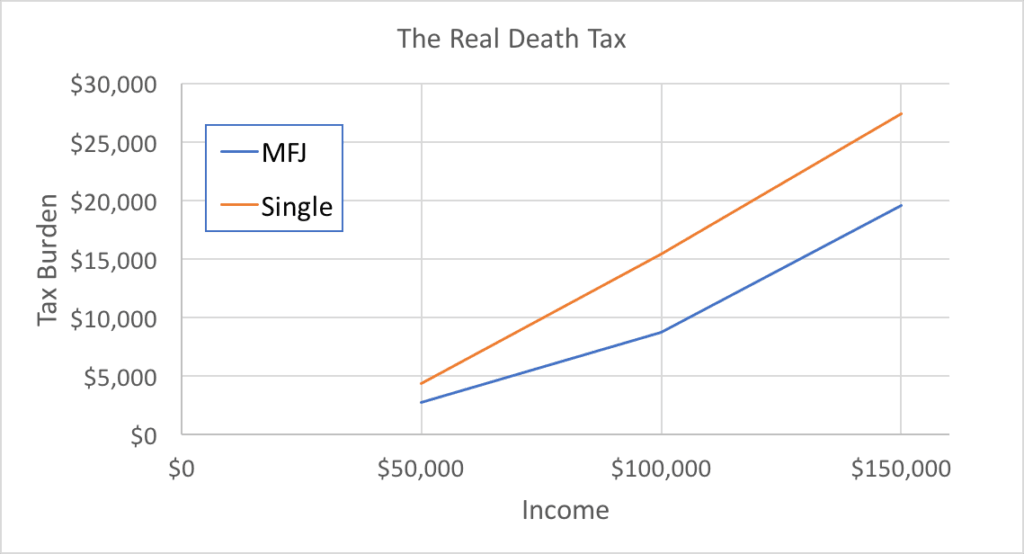

Every one of those examples includes a nice little phrase, “for a Married Couple Filing Jointly (MFJ)… Single filers divided by 2.”

The truth is, we won’t live forever. Often, that means one spouse will continue on without the other.

With significant assets. As a single filer.

Making the simple assumption that retirement income will continue as normal, involuntarily, due to RMDs, pension & SS, and dividends, then the tax burden of our beloved widower will increase significantly. Using the single filer tax brackets, each dollar of income is taxed more heavily. This could also apply at the State level.

Planning

I’ve heard it’s been said that everybody should have an estate plan. Even without an estate tax, that seems wise.

Upon the death of a spouse, reducing involuntary income is warranted. The levers we have the most control over are IRA size and Dividends, and the sooner we can start, the better.

Minimize Traditional IRA Value

Once we hit age 70.5, we will be making Required Minimum Distributions from our Traditional IRAs/401ks. To avoid an increased tax bill, it is best if the IRA values for the surviving spouse are independently below key thresholds (See Is Your 401k Too Big?)

Naturally, our Traditional accounts will already be as small as possible thanks to annual Roth conversions throughout our non-working lives.

But that may be insufficient. in which case we can:

- bequeath our Traditional IRA, in whole or part, to a non-spouse (children, grandchildren, etc…)

- ramp up our charitable efforts via Qualified Charitable Donations (QCDs) which satisfy the RMD requirements

Fortunately, a spouse can decline to inherit an IRA, but an up to date last will and testament or a Transfer on Death (TOD) registration with your brokerage will help with a seamless transition.

Reduce Dividends

Our taxable brokerage accounts have been spitting off an increasing quantity of dividends, as they do. As RMDs increase, our dividend income is likely to increase with it (where else are we going to park those funds?)

Single Filer tax brackets and Social Security, with or without an RMD, could mean most or all of our dividends no longer benefit from the 0% tax bracket, instead facing rates of up to 23.8%. (Dear S&P500, please stop paying so many dividends.)

To minimize the long-term damage, we can:

- Reduce the percentage of net worth invested in high-yield assets (individual stocks, high-yield funds)

- Increase the percentage of net worth invested in non-dividend paying assets (e.g. Berkshire Hathaway)

- Gift assets to friends and family (although this keeps basis same for the recipient)

- Donate (appreciated) assets to charity

I’ve already taken option 1 and will increasingly rely on options 3 and 4, with perhaps a sprinkle of option 2.

Summary

Reflecting upon my own mortality has got me thinking… everyone needs an estate/inheritance plan, not just the top 0.2%.

Married couples benefit from larger tax brackets which cease to apply when one person passes. Without proper planning, this can result in a significant increase in tax burden for the surviving spouse. (*)

A lot of income late in life is involuntary (SS/pensions, RMDs, dividends) so options are limited. Using the non-working years to minimize RMD size/impact and total dividend income will yield the best results.

I’ll be working on formally implementing our own estate/inheritance plan over the coming weeks, because everyone needs a hobby. (TODs already in place.)

(*) This is even more relevant to us, as the estate tax exemptions don’t apply to non-resident alien spouses (NRAs.) At present, our estate plan includes the important (albeit unlikely) requirement that I am not allowed to pass first.

For a non-resident alien spouse, besides the estate taxes at the death of the US person, there are also taxes to be considered when the second spouse dies (i.e. when transferring the remainder of the marital estate to GCC Jr.). In this case, trusts might be an option. There’s a Qualified Domestic Operating Trust (QDOT), which is really more relevant if you have assets that exceed the marital exclusion. But you can also set up a trust where the trust is the inheritor of the assets. The surviving spouse is entitled to income from the trust throughout the remainder of her life (and potentially the principal if/as needed), and upon her death the surviving (presumably US person) children become the beneficiaries, thus sidestepping the greatly reduced exemption for NRAs upon their death. The trust could also be set up that if both spouses die when the children are young, the trustee administers the assets for the benefit of the minor children.

The usual caveat: I’m not an estate lawyer (though I suggest you talk to one if this is of interest to you. It will cost you a bit, but you can consider it a peace of mind or insurance expense).

Good luck!

Thank you. A trust is probably something we set up, even if Winnie eventually becomes a US citizen (assuming we end up back in the US.)

I am currently working with an estate attorney on establishing a trust to be created at my and my wifes death to benefit our 14 yr old daughter. I learned that the tax law for trusts changed in 2019. Originally the advise was to set it up so that the trust pays out all the gains annually because the trust was taxed at 37% while the beneficiary would be taxed at normal income tax rates. Now the law applies to unearned income for children under the age of 19 and college students under the age of 24. Now it is taxed at the 37% regardless of whether it is paid out to the minor beneficiary or kept within the trust.

I don’t want to deal with it right now. We’re too young for that.

There is 25 years left to reduce our RMD. I’m not sure why we have to rush in now.

I’m not aware of a reason to rush either. But something to think about when considering Roth vs Traditional and comparing marginal rates now vs future.

Don’t spouses get a stepped up basis on taxable accounts? If so, you could do some mayor reshuffling at death without paying any taxes.

Yes and no.

Basis is stepped up 100% if it is community property / accumulated during the marriage. Any stock you bring into the marriage is separate property. Or in common law States, basis is stepped up by percentage ownership… say half each.

But with basis stepped up, you could sell your VTI/VTSAX and buy Berkshire Hathaway without capital gain tax impact.

Woah. I did not know that. It looks like I’ll need to plan things a bit better. Thank you.

I’m still figuring this stuff out, but as an example, let’s say you enter a marriage with some assets (stock, rental property, etc…)

You do nothing with regards to your pre-marriage assets and they remain separate.

Sadly, your spouse passes. You get no step up in basis.

Or…. after marriage, you commingle all assets / add spouse’s name to title/brokerage account, etc… now it is community property, and upon death there is a step up in basis.

One is clearly better for capital gains taxes. The other is better if the marriage doesn’t last, or if the value of the asset declines during the marriage (reset in basis goes both ways.)

To “Retire by Forty” – Death doesn’t ever think anyone is too young to visit. Get your stuff in order or your heirs will curse you.

This is a great post on the widow/widower tax slam. I deal with this each year with mom/mother-in-law having half the tax bracket. There is a Ed Slott term for “Tax torpedo” related to this/social security. Shrinking forced income (RMD Required Income Distributions) is one way to help. I love our current “low income” years right now to Roth link crazy and stay in the 0% LTCGs. The surviving spouse has it rough–partner loss, tax bracket hit, and no life-care partner, etc.

My mom died a few years back, and last year dad hit 70.5 and needed to start taking RMDs from his TSP. He’s fortunate in that he can afford to not care; he lives simply and idolizes Thoreau, his ideal vacation is camping in the mountains, the cushy pre-1987 CSRS pension system is generous, and mom was the big spender in the relationship anyway. That said, he dumped all his large assets into a revocable living trust a year ago while setting up powers of attorney for me and my brother, and we all sleep a lot easier now.

Sorry for your loss :(

The trust will smooth the transition. It’s something I’m looking into as well.

Thank you. It was dealing with her ‘estate,’ such as it was, that made dad realize he needed to do something; for peace of mind alone, he’s convinced it was well worth a few grand. I hope your investigation and implementation go smoothly!

“Reflecting upon my own mortality has got me thinking… everyone needs an estate/inheritance plan, not just the top 0.2%.”

Good point and interesting post. I think this one is hard to deal with because not only does it not benefit the planner personally (unless judgment day comes in the form of an estate planning audit) but death is also something that we don’t like to think about (there is a great book called The Denial of Death about the implications on this in our lives). However avoiding probate through planning is like spending a dime to give your loved ones a dollar when you are in the great beyond. I admit that this is something I need to give more attention to personally as well. Thanks for the reminder

Reflecting upon your own mortality is a good thing to do from time to time. I came at it just from thinking about the aging process… seeing older people struggle with stairs and heat while on their big retirement vacation, personal challenges with injuries that don’t seem to heal as quickly, feeling tired more easily than before… it helps to remember what this early retirement thing is all about.

I live in a community property state. Part of my estate plan is to sell all rental real estate and brokerage holdings as soon as one of us dies. All are way to appreciated for us to want to sell now. Appreciated as in stock/mutual funds/rental real estate thats been owned for 30+ years. All do now is donate appreciated stock to my DAF. Also long ago directed that dividends/internal capital gains of mutual funds get paid out rather than reinvested.

We both retired several years apart in our mid-50s. The first few years I harvested capital gains up to the 0% capital gains limit. When involuntary income* gains took that option away and I realized that my first year RMD would likely be 80K* I switched to Roth conversions. I filled the 25% bracket for several years and now the 22% bracket. Glad I did since even with the conversions my RMDs could still be close to 80K.

When one of us dies, 80K RMD on top of uncontrollable income will be a a tax shit storm. Be glad you’re dealing with this in your 40s (30s?) rather than 50s and 60s.

*talk about first world problems!

Definitely a 1st world problem. It’s like when you order a cappuccino and they give you a latte.

Sounds like you have a solid plan.

I know you play by the rules as they are currently, however does anyone think perhaps in the future the RMD age will be later ? I know it hasn’t changed yet, and I know the government wants there money, but i do think it will change before I get to 70.5

With longevity ever increasing forcing people to take money out at 70.5 seems honestly dangerous for people that don’t have the savings most of the readers of this blog do. I realize they don’t have to spend it but, I do wonder since I’m 20+ years away if perhaps they change this age which changes a large variable in the equation.

I think any shift would be minor. RMDs are already fairly small (*) until age 85 or so.

If people live 10 years longer, on average, Congress might consider shifting the RMD by 10 years. I’m doubtful, but it could happen.

Then we would probably start withdrawing a smaller amount at age 70. Maybe 3.5% instead of 3.65%.

* Interestingly enough, the RMD table for inherited IRAs is much more aggressive:

70.5 normal RMD table – 27.4 (3.65%)

60 inherited IRA RMD table – 25.2 (3.97%)

70 inherited IRA RMD table – 17 (5.88%)

Interesting post that I think about from time to time.

As much as I love the tax articles, being a single filer makes the threshold so much lower. I’ve realized, in my late twenties, that my 401k is already too large but there’s no real alternative to funding it fully each year at a 32% tax rate.

As a single filer, you start to realize you’ll never fully optimize things (0% tax forever) but you can try to optimize as best as possible.

If you were a single filer now, do you think you’d do things much different? I think probably the feie is the best tool for single early retirees in the you can make good income, convert to Roth at 0%, and have 0% dividend/capital gains rate.

I was a single filer for most of my career.

If that was the case today, ignoring blog income I would still be at a zero or near zero tax rate, in part because cost of living would be so much lower.

If using the FEIE is valuable to your personal situation, then you are unlikely to also be able to have 0% div/CG rates, as those are taxed as if the FEIE wasn’t used.

Thank you for this article. I’m so excited you’re researching estate plans and trusts. We are in the process of doing that too. Our son is similar age to GCCjr. I’m looking forward to reading your articles on this topic.

I know I am a bit late to the party here, but I am 46 years old. Looking at current SS life expectancy tables, I am only going to live 3 years less than my wife, who is age 45.

We will have , in theory, 4 years of her filing single, which will include less income due to her having one social security check instead of two.

But wait, for surviving spouses, she will get a full two years after my death to file jointly per law, and also the year of my death, so really two plus years (1-11 extra months).

https://www.1040.com/tax-guide/taxes-for-families/filing-as-a-widow-er/

It is, therefore, my opinion that although I will keep RMD planning in mind, I don’t think it’s a major issue if both spouses are near each other in age, or even apart by a few years.

This is more an issue of probability and it is more pronounced the longer you live because of the steep rise in minimum withdrawals. If you are average and your spouse is 1 sigma outside of average then she could live to age 91+, about 16.5 years longer than you.

The SS table says if you are a 46 yo male you will on average live another 33.37 years. A 45 yo female will live another 38.08 years. The gap is small.

But if you go out to ages 79.37 and 83.08, respectively, a full 56% of female births are still alive. The 44% bring the average waaaay down. At age 83, a woman is expected to live another 8.09 years (again, on average.) At age 91, 26% of female births are still living and expected to live another 4.52 years.