The end of the calendar year is quickly approaching, and that means it is time to run through our year-end tax checklist. The simpler the better.

Here are a few important items to review and actions to take.

Year-End Financial and Tax Checklist

Estimate total annual income

Q4 dividends, interest, and capital gains are not yet on the books, but Vanguard (and others) usually publish an estimate in November / December.

For 2022 Vanguard has shared this calendar:

(VTI – $0.93, VXUS – $0.63.)

With a preliminary year-end fund distribution estimates out on Dec 8, 2022, I can start my 2022 tax calculations for total income, qualified dividend income percentage, and US / Foreign earned income split, and then adjust as necessary / as new information is available.

The actual distributions come in the last week of the year so there are still a few days to adjust before the ball drops.

Determine Your Marginal Tax Rate

From income, we can quickly determine our marginal tax rate. (See our full overview of the federal tax brackets.)

The marginal tax rate is what guides us in most decisions related to tax optimization.

For 2021 we will have a high marginal tax rate, so I am aggressively making deductible contributions to 401(k) and HSA. Deductible IRA contributions would also be good at lower income levels. In years past with a low marginal tax rate, we instead pointed that aggression towards Roth contributions and conversions.

Income Tax Calculator! (reports marginal tax rate)

For assistance with tax calculations, be sure to check out our simple yet powerful tax calculator!

Ensure SEPP and RMD distributions are complete

SEPP / 72(t) IRA withdrawals and Required Minimum Distributions have rather unpleasant penalties if the necessary withdrawals are not completed accurately and timely. Review SEPP and RMD distributions to avoid this unpleasantness.

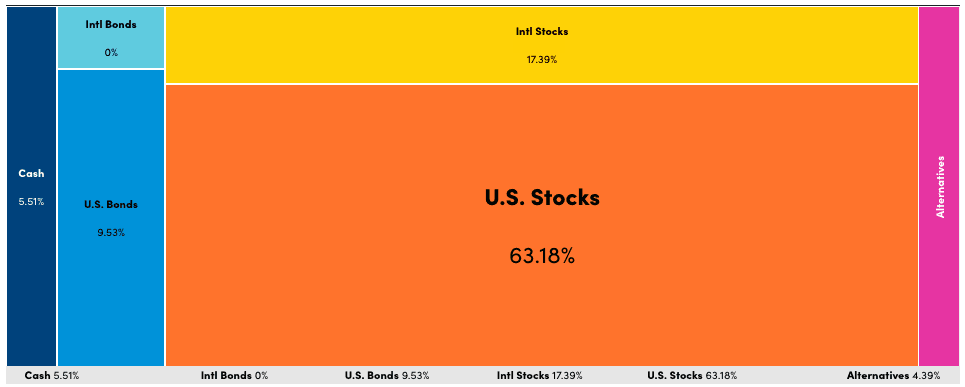

Review Asset Allocation & Rebalance

A good asset allocation stands the test of time through periodic rebalancing. I include Roth Conversions, Capital Gain / Loss harvesting, and cash flow management as part of the rebalancing process.

Our target asset allocation has been about 90% stocks / 10% bonds and 75% US equities / 25% International for as long as I can remember, even with the cash accumulation I did as part of pandemic response.

Our 2020 asset allocation chart

Now is a good time to review and rebalance if necessary. I use a combination of a spreadsheet and Personal Capital (affiliate link) for this process.

Finish All Roth Conversions

Any Roth conversions must be completed by Dec 31st. Since Roth conversions can no longer be recharacterized post-TCJA, I will schedule these after I know our “final estimated” total income and amount of unqualified dividends (taxed as ordinary income.)

The actual distributions and qualified dividend income percentage of Mutual Funds / ETFs may be different from the early-December estimate, so some educated guesswork is sometimes necessary.

- Our tax calculator also helps estimate appropriate Roth conversion size.

Harvest Capital Gains / Losses

Similar to Roth conversions, all capital gains/losses must be realized by Dec 31st. I will schedule these after I’ve completed a Roth conversion (if applicable), although I already realized some capital losses earlier this year (This is a good time to remember why to harvest capital losses.)

Related: see thoughts on how to prioritize Roth conversions or Gain harvesting.

I also have a template that shows the step-by-step process for harvesting gains. Submit the form here and I’ll email it to you.

- Our tax calculator also helps estimate appropriate capital gain harvest value.

Make final 401k contributions

Ideally, 401k contributions are on auto-pilot and you are able to contribute at least enough to receive a full match from an employer (if applicable.) See the current and past year 401k contribution limits.

Verify all is well, and make necessary adjustments including desired Roth / Traditional allocation.

We make solo 401(k) contributions manually, and the final “employee” contribution must be made by Jan 30 (I’m with Etrade and this may have changed this year), so December is when I ensure we have the requisite cash on hand. (If you are self-employed, the new solo401(k) docs need to be in before end of year!) Your solo 401k administrator may enforce a different schedule, just be sure you know the contribution deadlines and ensure the cash is available.

Our solo-401k contribution calculator can help with the math.

Plan for IRA and HSA contributions

IRA and HSA contributions need to be completed by the tax deadline, often April 15th of the following year.

See IRA contribution limits and HSA contribution limits.

If we haven’t already made full contributions for the year, I plan to ensure we have the cash available. This might mean selling stock now or Q1, realizing a capital gain in whichever tax year is more favorable.

Be Sure to get the Full Child Tax Credit

With the expiration of the wonderful child tax credit enhancements that came during the pandemic, it may be necessary to jump through some hoops to get the full child tax credit.

A portion of the Child Tax Credit (CTC) is refundable, but only if you have earned income. If you don’t, it is necessary to ensure a positive tax burden and use the CTC to bring total tax back to zero rather than get a refund. A Roth conversion or capital gain harvest can solve this problem easily but must be done by Dec 31st.

For more details, see Maximizing the Child Tax Credit (even without earned income)

We likely won’t get the full Child Tax Credit this year because increasing our taxable income (via Roth conversion, for example) would result in higher ACA premiums and State taxes that would actually cost us more than the CTC benefit. Bummer.

Schedule Healthcare, Enroll in ACA coverage for next year

Most ACA and employer health insurance plans have a deductible. If you are close to hitting it for the year, December is a good time to schedule Doctor visits and planned care. Free knee surgery in December is possibly preferred to expensive knee surgery in January (or it may be better to meet the deductible in January. The key is planning ahead.)

FSA and HRA dollars may also need to be spent.

For ACA enrollment, results from these end-of-year health checks can inform what level of health insurance coverage we may want for next year. Healthy as an ox? Bronze with HSA. Something isn’t quite right? Silver plan with high CSR subsidies combined with income optimization for the year.

ACA Premium / Subsidy Calculator!

For assistance with ACA planning, be sure to check out our simple yet powerful ACA premium calculator!

Make Tax-deductible Purchases & Donations / Shift Income to Next Year

For business owners / self-employed, December can be a good time to make necessary purchases. Or it can be a good time to shift income into the future if you expect lower income next year (e.g. bill you clients with a due date of Jan 15 instead of Dec 31.)

Last year I purchased a new laptop as a Christmas gift to myself because our marginal tax rate in 2021 was higher than it will be in 2022. Were it the other way around, I would have gotten myself a Januarymas gift instead.

If you are itemizing (rather than claiming the standard deduction) you can also deduct charitable donations (also by Dec 31st.) Gifting appreciated shares means no capital gains taxes for the gifter or beneficiary.

Alas, the above-the-line charitable deduction changes during the pandemic have expired (can only deduct charitable contributions if itemizing.)

Consider getting an (almost) free vacation for paying your taxes

Either through paycheck withholding or via quarterly estimated tax payments, the IRS collects their money upfront.

For the self-employed, it is a simple process to pay those taxes with a credit card (or four) to get free vacations. (See how Uncle Sam paid for our Hawaii trip. I paid $56 in fees to get over $1,000 in free hotel nights and free breakfast with beach view.)

For employees, you can reduce withholding with an updated W4, and then make quarterly payments as the self-employed do to square up.

Consult with your CPA or Tax person

Tax and investment management are superpowers that anyone can develop, but it takes some time and experience to get there. I learned it all one step (and mistake) at a time.

A good CPA or tax guy/gal who also enjoys the role of educator can really help. December is a good time to meet with them for the first or umpteenth time. You can even bring this list.

I’m sometimes asked if I can help – I do my best to take on that educator roll through this blog and also on the forum. I created a consulting page for those who want something more.

Also this year (2022 tax year), in addition to volunteering for tax assistance for low-income households, I am considering personally helping a few GCC readers do their taxes for a competitive fee. Drop me an email if that sounds of interest.

Summary

- Estimate total annual income

- Determine your marginal tax rate

- Ensure SEPP and RMD distributions are complete

- Review Asset Allocation & Rebalance

- Finish All Roth Conversions

- Harvest Capital Gains / Losses

- Make final 401k contributions

- Be Sure to get the Full Child Tax Credit

- Schedule Healthcare, Enroll in ACA coverage for next year

- Make Tax-deductible Purchases & Donations / Shift Income to Next Year

- Consider getting an (almost) free vacation for paying your taxes

- Consult with your CPA or Tax person

Use online tax calculators to help:

- Federal Income Tax Calculator

- ACA Premium Calculator

- Self-Employment Tax Calculator

- Solo 401(k) Contribution Calculator

Enjoy the Holidays

We may spend a lot of time thinking about money and taxes on this blog, but they are small topics in the grand scheme of things.

Have a great holiday season with friends and family, wherever you may be.

We spent Thanksgiving in Tahoe (snowboarding) and have a few hotel nights booked over the school winter holiday (free night certificates! instead of $500/night)… 56″ of new snow in 24 hours this weekend at the place we have season passes… it is going to be epic.

Happy Holidays!

Actual photo of me in our hot tub.

I thought the employee contribution for the solo 401(k) wasn’t due until you actually filed your tax return?

Maybe for an S corporation it is due by January 30 but if you’re just a sole proprietor it’s not due till the tax filing deadline.

Yeah, I believe that is the rule, depending on plan documents. My solo401k provider (Etrade) requires it be in by Jan 30. It’s supposed to be paycheck deduction

I had the same understanding as David Ann Arbor–though my provider is Vanguard.

Thanks for this useful write up by the way.

Yes, he is correct.

What the plan documents allow is typically a subset of what the law allows.

The overarching message there is to just plan for the cash flow. Jan or Apr or Oct are more or less the same when you have a lot of assets, but you need to decide in which year you will realize a capital gain (if applicable) and to ensure you have the cash on hand.

Actually I had it wrong about the Etrade solo 401k contribution deadline for employee contributions. It isn’t Jan 30, it is Jan 15. Good thing I checked!

Thank you for this post.

Thanks for putting this all together in one place.

It will be very helpful for me over the next month.

I probably made some optimization mistakes again this year,

but reading your posts has helped me get a lot better at it.

You do deserve a new laptop!

I do, don’t I! :)

I make optimization mistakes too. It happens, but every year it gets easier.

Just wondering, what are your 4.46% alternatives? Gold? Crypto? :)

Yes! Lots of gold and crypto!

Narrator: actually, it is just VNQ (REIT fund)

Great list. We’re in the process of updating our estate plan as our youngest turned 18 this year, and we thought it would be a good milestone to look at what we had and what needed to change. While you don’t want to update your entire plan each year (it’s quite a process) one thing I’m doing as part of this is making sure our estate attorney has updated beneficiary forms for all of our investments and also making sure all of our bank accounts have a backup person who can access the accounts immediately should we die or become disabled. The beneficiary and bank forms don’t need to be updated each year, but every time you add an account you need those forms, and tax time, where you’ll pulling together all your paperwork anyway is a good time to check these things.

This is a good one. I should sit down and formalize our estate stuff this coming year.

At the moment, we mostly just have joint accounts and TOD forms.

Awesome Job!! Thank you again!!😁👍👍

Great article, as usual!!!

Do you have in mind any ideas how to shield some pretax $ in my case? : (tax return: joint (120k salary/year/family (one earner only), no 401k offered by employer, IRA contribution – 12k, HSA – 7k).

Do you think it’s worth exploring the idea of splitting 120k in 100k salary and 20k as self employed (as an example) in order to contribute to solo 401k?

Many thanks!

If you have a legitimate profitable business you can contribute to a solo 401k, as long as the formation documents are filed by Dec 31. W2 income from a job isn’t business income, nor can it be.

Between IRA and HSA contributions you are already using all of the options at your disposal. If you have significant itemized deductions (mortgage interest, property taxes, medical expenses, etc…) you could look at also making substantial charitable contributions

This year is special (SECURE Act) and the plan can be setup up to your filing deadline in 2021.

https://www.mysolo401k.net/the-secure-act-extended-the-deadline-to-establish-open-a-self-directed-solo-401k-self-directed-401k-solo-k-individual-401k/

Somewhat of an off-topic question in how it relates to taxes, but I’m looking at putting a down payment on a house coming up soon!

In order to minimize my taxes, I’m still working a full-time gig and don’t want to pull from my Roth IRA just yet. Would a Fidelity brokerage account allow me to withdraw just “my contributions” these past few years to minimize taxes, or is this only a ROTH thing? I don’t have much dispensable cash because I invest (and save!) a lot. Thanks.

You can’t withdraw just the basis from a brokerage account (unless it has just been sitting in cash this whole time.)

If you sell some stock, you’ll get some return of basis and some capital gains.

GCC,

If you withdraw the most recent trades though in the brokerage, these should have the least amount of capital gains all things considered right? I am pretty sure you can withdraw certain shares depending on date.

Yes, you can do specific shares. Most recent or not, you can pick the shares with the least amount of gain. Be sure to choose shares that have been held for 1+ years to ensure long-term gain tax status.

Or even better shares that have some losses.

“The CARES Act waives required minimum distributions during 2020 for IRAs and retirement plans, including beneficiaries with inherited accounts.”

https://www.irs.gov/newsroom/irs-seniors-retirees-not-required-to-take-distributions-from-retirement-accounts-this-year-under-new-law

Yeah, this is a special situation for 2020 due to covid. Was happy my mom wasn’t forced to “sell low” when it looked like this year would be a particularly nasty down year.

Thank you, I added this point to the post.

Hi Jeremy & Winnie, this was helpful and timely. After reading,I realized I was on the verge of crossing into the 32% bracket, so I boosted 401K contributions for the rest of the year. Probably will save me a good chunk of taxes. Thank you!

Do you have any recommendations for finding a good tax advisor?

Alas, I don’t… I’ve had some good email exchanges with a company called Taxes for Expats but for US residents I don’t know anyone.

https://www.gocurrycracker.com/tax-services/

I believe the CARES Act deduction for charitable cash contributions is $300 per return, and not $300 per individual.

Yes, thank you. I’ve updated the post.

Hi there! Long time reader, first time commenting.

Just FYI, the CARES Act specifies that the $300 deduction is only “per tax filing entity”. Meaning that it only $300 if married filing jointly.

I read this on the government document (cannot find the page anymore), but here’s this other blog post as a resource. https://thefinancebuff.com/cares-act-charity-donation-deduction-married.html

Thank you, good link

I believe the cash contribution deduction of $300 per person, $600 per couple (for those not itemizing deductions) expired after the 2021 tax year. Here’s a link:

https://giving.stanford.edu/stories/cares-act-not-extended-for-2022/

That’s right. The comment you are replying to is from 2020

You rock! I love reading your blog and learning from your experience. A giant thank you!!

GCC,

Now that you are back in the U.S. and possibly going to be using an ACA health plan, does this complicate your future tax gain harvesting and Roth conversion plans? Both of those strategies would increase your income in terms of calculating ACA subsidies.

Personally, I have avoided Roth conversions and tax gain harvesting to focus on maximizing ACA subsidies, but you might have a different take.

I welcome your thoughts on how you approach this.

It’s different yeah, albeit the same thought process – if future peak RMD marginal tax rates exceed today’s marginal tax rates, then do Roth conversions now. Else not. It’s just that “today’s marginal tax rate” now includes the ACA subsidy reduction rate. That is a long way of saying that I don’t plan to do any Roth conversions going forward and will instead prioritize ACA subsidies.

There are some graphs of this in these posts:

Going Back to Cali…? – looks at combined tax rates for Federal + California + ACA

Obamacare Optimization vs Tax Minimization – outlines the tradeoff between ACA subsidy and future tax minimization

Reassuring to know we are on the same page.

I assume you also won’t do tax gain harvesting for the same reason?

Thanks for the link to the graphs.

Most likely no capital gains harvesting.

Context: We will be around 200% FPL for MAGI which is a bit of a sweet spot for ACA subsidies. If we were lower than that I would probably still generate some taxable income via Roth conversion or cap gain harvesting.

Thanks. I don’t mean to drag this out, but why do you see 200% FPL for MAGI as a sweet spot and superior than, say, 150%.

Also, would you prioritize first Roth conversions or capital gains harvesting if you were going to bump up your MAGI a bit.

I’ve been keeping MAGI as low as possible while not dropping below the requirements to qualify for ACA subsidies. Thinking I must be missing something if you think 200% is better. I could easily bump it up by changing solo 401K contributions between Roth vs. Trad or doing cap gains harvesting or a Roth conversion….

There is a window on the bottom end between eligibility (100% or 138%) and when total cost of the plan starts to ramp up (200%) due to loss of CSRs.

For us, a family of 4, at 200% FPL we can get a silver plan for ~$75/month with a family deductible of $1600/year. Or a free Bronze plan. But if we chose Bronze (say, to have an HSA), the cost of the plan is actually less than the subsidy we qualify for, leaving $ on the table. Maybe that is OK, but if we have unplanned expensive circumstances the deductible is now $16k.

Were we to try to get a lower AGI, say 150% FPL, then that same silver plan costs $0/month and the family deductible is $150. Copays drop from $15 per service to $5. Total out of pocket difference over a year is probably $1k for lowering income by $13k or a ~7.5% tax rate. That seems like a lot but I struggle to care about $1,000 in the context of the hoops I would have to jump through to realize $13k less in income.

Were we in the situation where income naturally came to be 150% FPL would it be worthwhile to do a Roth conversion up to 199% FPL? Or just to the top of the 10% tax bracket?Maybe. If I was in a no tax State then paying 17.5% “tax” on a conversion would be better than paying 22% or 24% down the road. Add a few % for the state and it still might be a good trade.

Makes sense and thanks for your perspective.

I’m guessing the large deductible for a family of four on the bronze plan is giving you pause. For me (being single) the gap between the silver plan HSA and bronze plan HSA deductibles is only a few thousand dollars–which I make back fairly quickly by having lower premiums on the bronze HSA plan.

The bronze HSA plan comes in at exactly the same figure as maximum possible HSA subsidies (no coincidence, I’m guessing). So not leaving money on the table. Confess I haven’t even looked at the CSR angle. Glad you mentioned that.

Thanks again for sharing your perspective, Jeremy.

The cost sharing subsidies are where the real value is in these policies, but only applies on silver plans

Thank you for the article. I bookmarked it as I know it will be very useful to me. I have a question though. My understanding that capital gain harvesting will increase ACA MAGI and as a result will reduce premium subsidy. How do you optimize this? Thanks

Higher AGI does mean higher ACA premiums.

I walk through the tradeoff here: Obamacare Optimization vs Tax Minimization

Also see my reply to Mighty Investor here.

Hi, I see you live in California now so you have a quandary similar to my own.

I was thinking of doing a $50K capital gains harvest with no federal tax, since we have low enough income this year to take advantage of the ~$80K capital gains at 0% tax.

But since we live in California, I’d get hit with ordinary California income tax on that $50K. I think it would be something like 6% CA state tax, so let’s say $3,000 to CA.

I’m guessing our earned income will be a bit higher next year.

Does it make sense to do the federal tax harvest, but pay CA $3,000 for the privilege?

Thanks.

I do not plan to do any cap gain harvesting (or Roth conversions) while living in California – but due to ACA subsidies not the CA income tax. But this is because I have a clear path to no/low tax between now and age 59.5.

For your specific situation, paying some tax now might be a good choice – but it is hard to say without context of what you plan to do with these funds in the future. I generally don’t consider cap gain harvesting above 0% tax rate unless I plan to use those $ in the near future (1-3 years.)

Thanks. I myself was also worried about how much ACA subsidy I might lose. I’m unclear on how much the subsidy is affected by capital gains income. My tax program (Taxhawk) does not seem to calculate that. I guess that since capital gains is counted as ordinary income by California, I would lose on that subsidy as well as paying CA income tax. So no harvesting for me while I’m on the ACA.

My plan for the funds in the future is simply continued early retirement. I’m in my 50’s and did manage to retire early with help from the ACA and from this site. You’re providing a great public service here.

My pleasure.

To understand how ACA premiums are impacted by income, see these 3 posts:

– Obamacare Optimization in Early Retirement

– Obamacare Optimization vs Tax Minimization

– The American Rescue Plan Act of 2021

This is a great list of reminders! One question about ACA. I have a 2022 silver plan and when I signed up for 2022 I figured that my 2022 income would be low enough to use the lowest deductible. (as income increases the subsidy lowers and premiums increase quite a lot but the deductible skyrockets). So, if I go over the income limit for the lowest deductible I know my premium will increase (and I know how much) BUT will I be on the hook for the higher deductible??? I did use some medical care and that higher deductible scenario is worrisome although it seems like it would be tough to go back and re-adjust all my medical bills. Any idea what would happen?

CSR subsidies (which lower deductibles on silver plans) do not need to be repaid (although you are technically supposed to notify the exchange when your income expectations change.)

APTCs do (to a point.)

My question is about the change in deductible in my silver plan (which I noticed when using the premium estimator by inputting different incomes). I saw the premium increased, but also the deductible jumped way from $1k to $4k at a particular income figure. So, I’m questioning if I am going to get this higher deductible applied to me. I called Healthcare.gov to ask and basically the person didn’t understand what I was asking. I think it is a legitimate question but maybe I’m wrong.

That is the question I answered.

You get a lower deductible on silver plans at lower income levels thanks to CSR subsidies. If you end up with higher income, you don’t have to repay the CSRs and you don’t retroactively have a higher deductible.

However… when you know your income is going to be higher, you have to call the insurance exchange and tell them. They will change your plan to the correct one, and your deductible would be higher going forward.

Thanks, definitely will do better planning next time, with this info.

Great checklist. Thanks for putting it together. Happy holidays.

Great site, great posts.

For the flip side of paying taxes with a credit card:

What credit card do you use for non-bonus/everyday spending?

Thanks,

Jim

I am always working on a bonus so I almost never have non-bonus spending :)

But here are some examples from Q4-2022:

– working on bonus on new CSR (Chase Sapphire Reserve) for Winnie, so everything goes on here

– new bonus on Citi Premier card for me – paid property taxes with this

– paypal spending is a bonus category for Q4 for Chase Freedom cards, so all other spending goes on these (probably including my Q4 estimated taxes before 12/31.) (~7.5% back)

– except groceries, which are on my Amex Blue Everyday (6%) (because they offered a $150 bonus and no annual fee for one year if I upgraded)

– and also I need to spend another ~$1k on my Marriott Bonvoy card to get my 50th Elite Night Credit (Platinum) for 2022 (1 ENC for every $5k spend.)

–> as a bonus here, they gave me 18 months zero interest and zero fees on a Chase Pay Over Time plan on a recent $2k hotel stay on this card (Tahoe Thanksgiving)

Thanks Jeremy another quality post.

Think you’ve mentioned it in the past…the Taxcaster app is very easy and quick to use.

Gives a good idea of how various changes like contributing to an IRA, paying student loan interest, etc., will affect your Fed taxes.

Has definitely saved me tax dollars using it to plan year end.

I haven’t used Taxcaster in quite a long time… they “improved” it quite a bit at one point and then I liked it a whole lot less so I just made my own calculators instead ;)

I can never really estimate my income for the next year. Fortunately I get until the Following October to make my solo 401k contributions.

Hi Jeremy,

How do I figure out how much of a Roth Conversion I can do without the information of qualified and non-qualified dividends from Vanguard?

I see the preliminary year-end fund distribution estimates, but I don’t know how to go about figuring that stuff out. Please help.

In that same document that shows distribution estimates they also provided qualified / non-qualified percentage estimates. It looks like that document has been removed (temporarily?)

What I have done in the past is use previous year information and call that “good enough.”

Thanks for the great reminder post!

As a general question is it possible to tax gain and tax loss harvest in the same year to maximise the benefits?

Assuming MFJ income falls under the threshold for LTCGT but is enough to actually pay federal taxes on income.

Worked example:

MFJ couple only VTSAX earning 100k gross leads to a suggestion on your calculator of harvesting capital gains up to AGI < 109250 leaving around 9250 to get the 0%.

Could you also sell the same investment at a loss up to 3000 in order to reduce the federal tax on W2 income?

No, not possible.

If you have any gains, losses are first applied as an offset against those gains. There is no way to have both a large amount of capital gains and a $3000 loss.

Very nice check list. Thanks.

A question that is wondering my mind lately. As an employee, do I need to have some withholding on my paycheck or could I fill out a W-4 in a way that I don’t withhold anything but make quarterly payments with a credit cards to get the most points? Do you know if that’s possible and if anyone you know is doing it?

Yes, you can do this.

Just make sure you meet the withholding requirement to avoid penalties: What’s worse than paying taxes? Paying tax penalties

That’s a great idea to pay with credit cards, if you can. However, I did look at paying a quarterly payment with a credit card (as opposed to direct withdrawal from my bank which has no fee) and there are fees with the lowest being 1.87% (and a minimum of $2.50) for that service. You can find the optional services on the IRS website if you click on ‘pay by credit or debit card’.

Pay $3,000 in taxes on new credit card. 1.87% * $3000 = $56.10

Get x points worth $600 – $1000.

I’ll do that every chance I get.

Most CA counties can extend their tax payment due date until October per https://www.cpapracticeadvisor.com/2023/03/09/irs-and-state-move-tax-deadline-to-oct-16-for-most-californians/77630/