Advertiser Disclosure: This site is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CardRatings.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Advertiser Disclosure: This site is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CardRatings.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Since time immemorial, humans have used items of perceived value to exchange for goods and services. Shells, stones, gold, gems, paper, and even lines of code as a digital currency are used to establish a common medium of exchange that is predicated on trust — if everyone agrees that a $100 bill is worth $100 then the system works, otherwise it is useless.

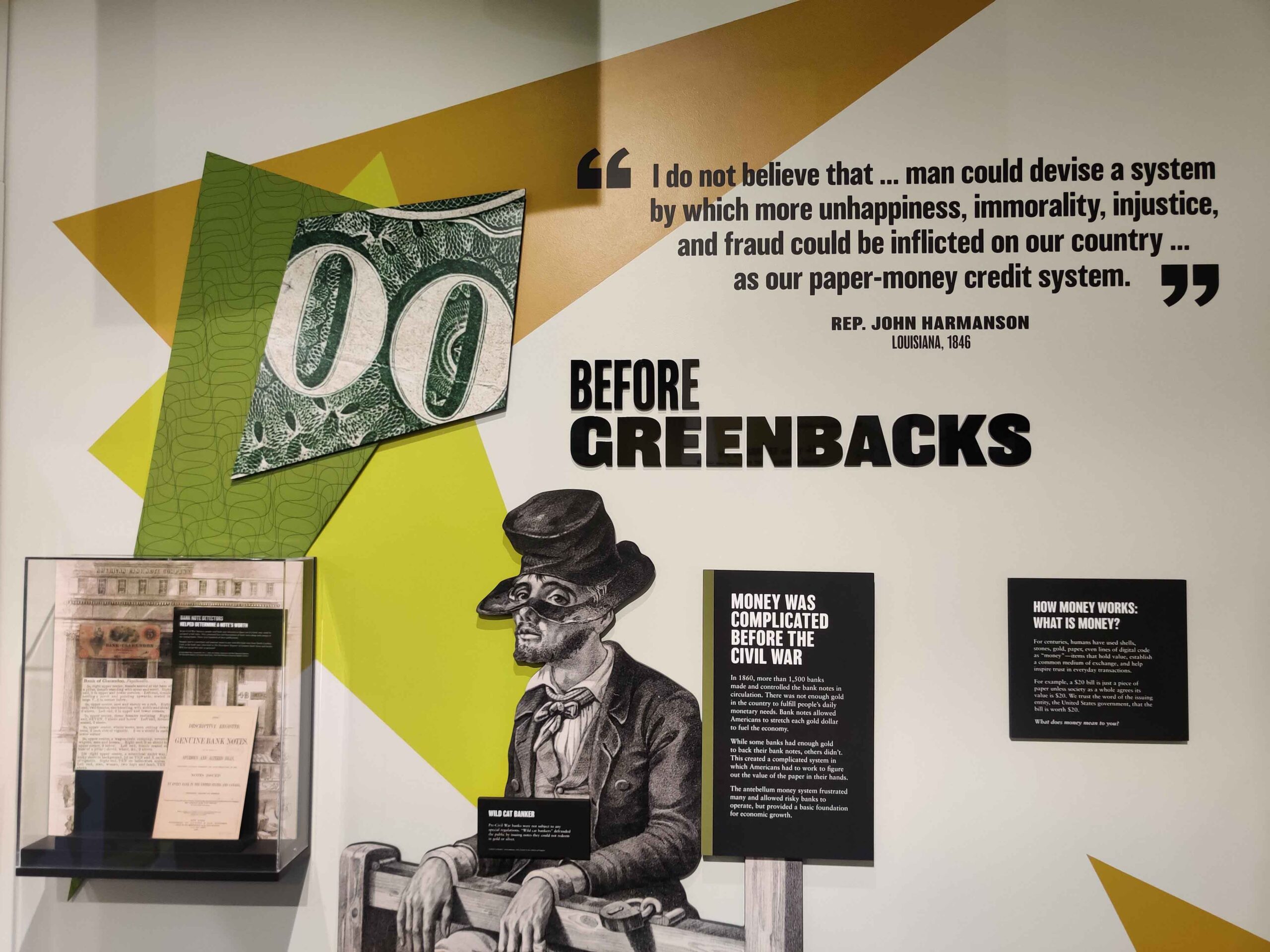

Last fall during a trip to Virginia, we stopped into the American Civil War Museum in Richmond. Among the many well-crafted displays was an excellent exhibit on the history of American money and how the currency we know and use today began as a result of the war.

The American Civil War

The dollars we use in America today are a direct byproduct of the Civil War. To raise money for the campaign, the U.S. Government had limited options: borrowing from banks, taxing citizens, printing money, and confiscating property. They settled on a mixture of taxation (3% income tax on those earning more than $8,000 per year), borrowing ($150 million from Congress in 1861), and printing money.

The U.S. Treasury soon began to issue paper bills, known as “greenbacks”, that were claimed to have a certain value (as opposed to notes backed by gold or silver). Before the war, no such currency existed and instead hundreds of different banks printed their own money. With no regulation or central authority, “wild cat” bankers often defrauded the public by issuing notes that could not be redeemed for value as advertised. This led to widespread mistrust of the banking industry and a fierce debate about the safety and fairness of the financial system.

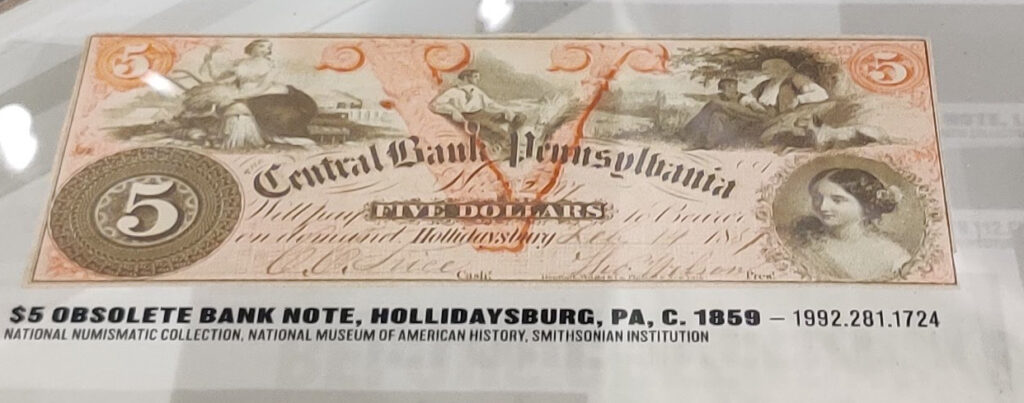

Bank note from Pennsylvania, c. 1859 – before the Treasury began issuing greenbacks.

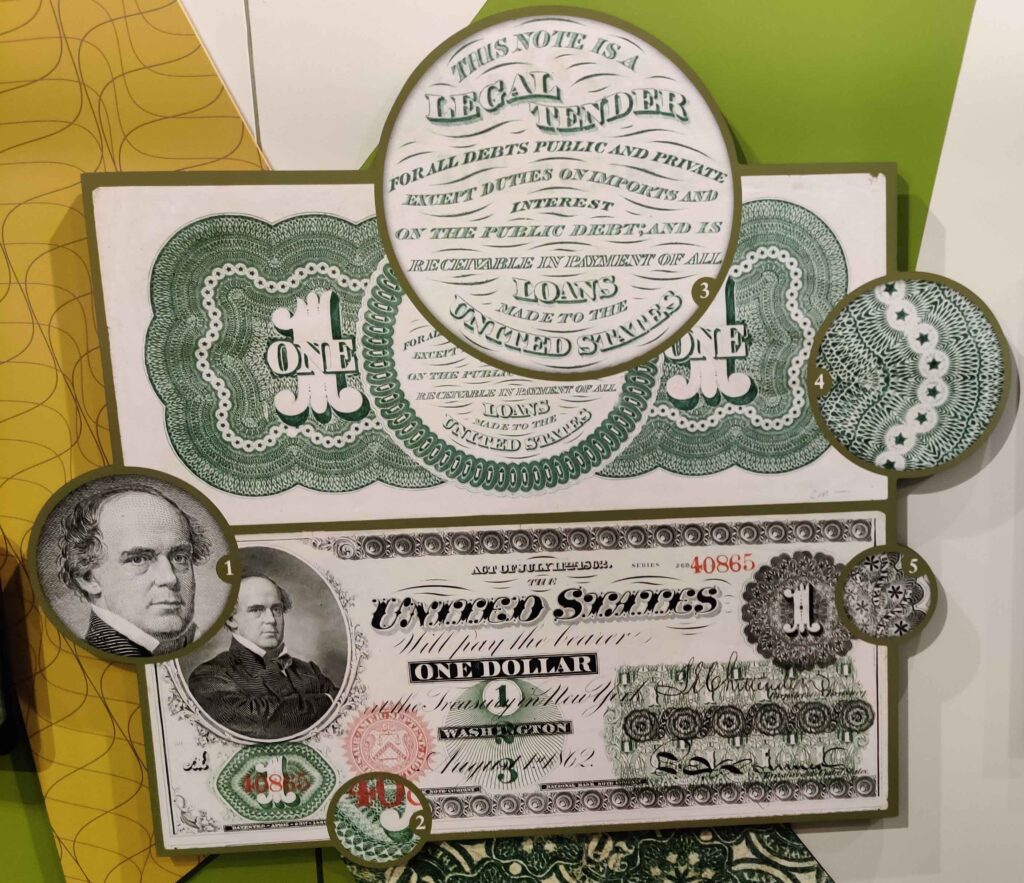

To gain public trust in greenbacks, the U.S. Treasury incorporated several features into the notes to inspire faith and foil counterfeiters including:

- A portrait of Secretary Salmon P. Chase (no relation)

- Permeating the notes with chromium oxide, giving them their green color, to prevent counterfeiting by photography

- Intricate engravings to make duplication more difficult

- The phrase regarding the note’s status as “legal tender”, which relied on the U.S. Government’s promise of its value

Original “greenback” design.

During this time, the Confederate States also felt pressure to raise money and similarly chose to print paper money, tax its citizens, and sell bonds in order to finance the war effort. By the end of 1864, nearly 60% of their income came from printing money. However, a critical mistake made by the Confederates was that they did not declare their currency “legal tender” as the United States had, and also did not regulate state-chartered banks. This led to a flood of Confederate money alongside municipal and state banknotes which caused rampant inflation that quickly devastated their economy.

1862 Confederate coin.

Post-War

After the Civil War ended in 1865, the U.S. Government continued its push for the use and faith of paper money by establishing the Secret Service, charged with deterrence and prosecution of counterfeiters. After that, a series of legislation and political happenings shaped the formation of America’s monetary policy for the next 75+ years:

- 1865: Congress begins to buy back greenbacks to reduce the number in circulation. The “Contraction Plan” ends in 1867

- 1869: The Bureau of Engraving and Printing takes over as the centralized printer of banknotes as opposed to the more than 1,500 banks that printed them in 1860

- 1875: Congress enacts the “Specie Payment Resumption Plan” which allows the public to trade greenbacks in for gold beginning January 1, 1879

- 1876: The National Greenback Party organizes to promote paper bills issued by the Government as the only form of currency

- 1896: The Presidential election revolves around monetary policy issues with Republican William McKinley supporting a strict gold standard and Democrat William Jennings Bryan supporting silver and gold

- 1900: The Gold Standard Act is passed

- 1913: The Federal Reserve Act gives the Federal Reserve System the power to create monetary policy (instead of Congress)

- 1933: Due to the Great Depression, the U.S. stops redeeming notes for gold, and gold can no longer be used as legal tender

- 1933-present: Federal Reserve Notes (fiat money) become the predominant paper currency and account for 99% of today’s circulation

Modern Day

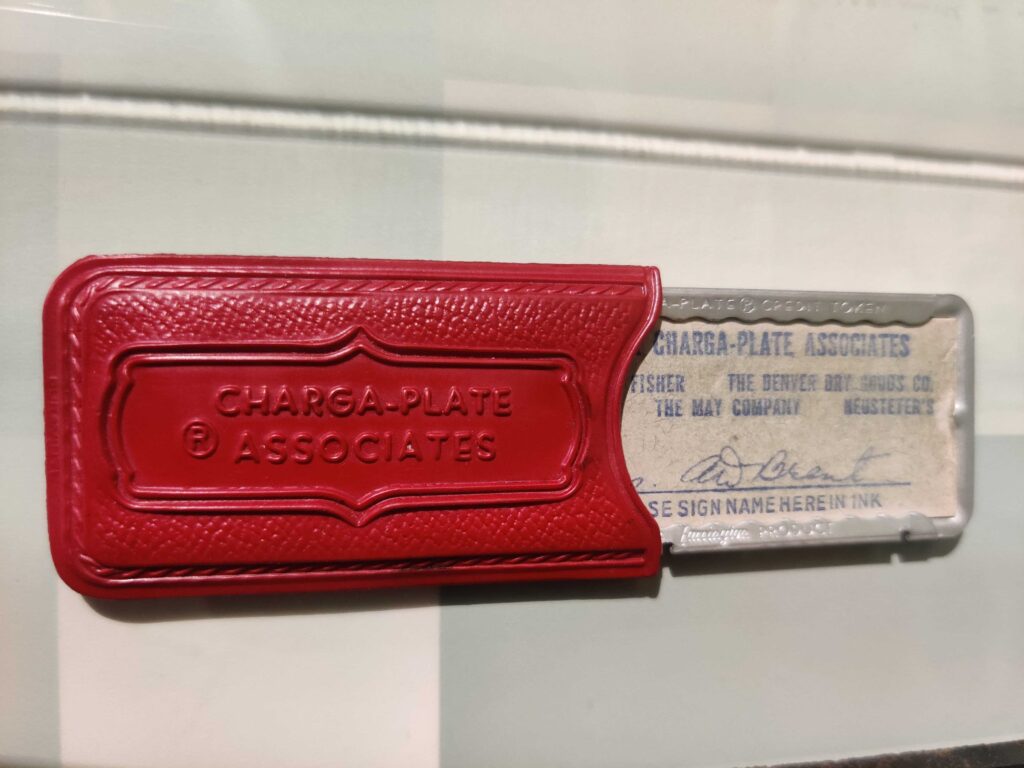

In addition to the evolution of banknotes, alternative currencies began their rise as early as the 1930s with the Charga-Plate. In use from 1935 to 1950, the Charga-Plate, a precursor to modern credit cards, was a small rectangle of sheet metal embossed with the customer’s name and address that they kept with them or was left at the store where it was issued. The device significantly sped up the purchasing process because the sales associate could quickly make an imprint of the information on the plate and charge a purchase to the customer’s account without having to record the details in a manual ledger.

Charga-Plate, circa 1935.

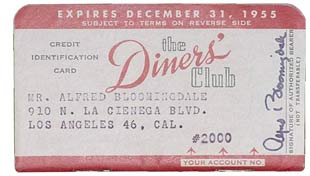

The first general-purpose credit card was issued in 1950 by Diner’s Club. At that time only restaurant bills could be applied to the card, and Diner’s Club president Frank McNamara made the first charge at Major’s Cabin Grill in New York on February 8, 1950.

1950s Diner’s Club credit card. Source.

Shortly after Diner’s Club, American Express launched its first charge card in the U.S. in 1958 and by the 1960s multiple banks were issuing their own version and beginning to institute rewards programs to entice loyalty among customers.

Debit cards also came into play around this time, with the first being issued by the Bank of Delware in 1966. Though they look like credit cards, they function like cash or a personal check as the money is withdrawn directly from a checking or savings account. The popularity of debit cards skyrocketed in the 1980s as more ATMs popped up across the country. Anyone reading this blog hopefully knows better than to use a debit card for purchases that could otherwise be paid with a rewards-earning credit card!

Today, there are countless banks issuing credit and debit cards – some with incredibly valuable rewards programs that issue transferable currencies, including our all-time favorite Chase Sapphire Preferred(R) Card introduced in 2009.

Reading the fine print on the Charga-Plate to see if their points transfer to Hyatt.

Final Thoughts

With almost 80% of Americans using credit cards regularly, there is less of a demand for paper notes these days. However, more than 150 years after the reformation of America’s banking system, the conversation about who governs money, the economy, and economic policy continues — especially as emerging technologies like cryptocurrency gain in popularity.

If you find yourself passing through Richmond sometime, I highly recommend stopping at the American Civil War Museum to learn a little more about the beginnings of our financial system.

Top offers from our partners

| Great travel card! card_name - bonus_miles_full annual_fees This is a great card for travelers! | |

| card_name - bonus_miles_full 2X miles on every purchase. Learn more here. | |

| card_name bonus_miles_full. *Rates and Fees. Numerous credits - Up to $200 in Uber Cash. $200 hotel credit with two-night minimum stay. $240 media credit. All as statement credits. (enrollment required) annual_fees. Terms Apply. | |

| card_name Small Business card. bonus_miles_full. Worth $1,250+. 3x points on travel (on the first $150,000 spent in combined purchases) annual_fees. |

Interested in getting the best and latest offers directly in your inbox? We stay on top of the best offerings so you don’t have to. Subscribe here.

Editorial Note – Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

User Generated Content Disclosure – Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

The info on the Civil War museum was interesting and enlightening–especially the glimpse at how money worked for North and South alike!

I thought so too!

Interesting read, thanks! I just recently learned that women couldn’t apply for a credit card without a man to co-sign until the Equal Credit Opportunity Act was passed in 1974! That wasn’t that long ago.