The United States has very generous tax rates for investment income such as qualified dividends and long-term capital gains, as low as 0%. This is a key component of the Never Pay Taxes Again strategy.

But sometimes you want (need?) to realize some large gains – say, if you are paying cash for a boat or a house, or if you are moving from a low-tax to a high-tax residence and want a massive step-up in basis. Or maybe you think the market is hot and you want to take some off the table.

In these cases you may come across the Net Investment Income Tax, a nice little 3.8% extra tax surcharge.

Net Investment Income Tax

The Net Investment Income Tax shouldn’t be an everyday or every year thing, it applies to investment income above a fairly large threshold.

Tax status – NIIT Threshold

Married Filing Jointly – $250,000

Head of Household – $200,000

Single – $200,000

Married Filing Separately – $125,000

The tax applies to passive / investment income only, which includes things like dividends, interest, capital gains, royalties, and rental profits. Income from a job or self-employment, qualified IRA distributions, Social Security, or municipal bond interest (for some reason) are not subject to NIIT. (This pdf from Ameriprise is a pretty good summary of how each income type is taxed.)

Only the investment income above the NIIT Threshold will be subject to the NIIT.

Some examples

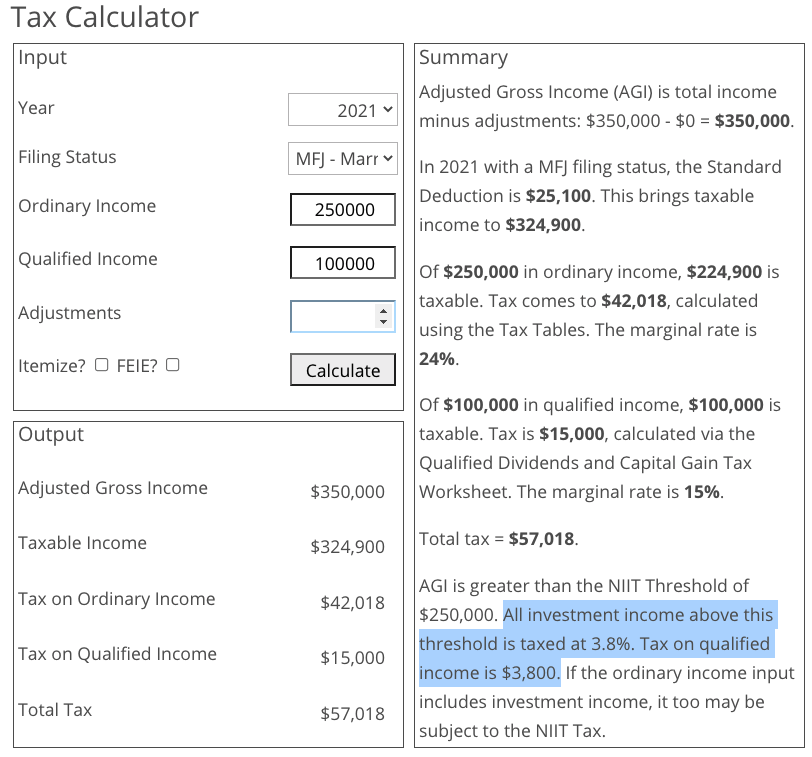

A Married Filing Jointly household has $250,000 in income from various sources. This is at or below the NIIT threshold so NIIT = $0.

This same couple realizes an additional $100,000 capital gain, for total AGI of $350,000. The investment income above the $250,000 NIIT threshold is taxed at 3.8%. NIIT = $3,800.

A Married Filing Jointly household has $300,000 in income from self-employment and $10,000 in dividends. All of the dividends will be taxed at 3.8% for a total of $380.

You can explore various options for your unique situation using our (new and improved) income tax calculator.

If you are subject to NIIT, this all gets sorted on Form 8960 (pdf.)

Avoiding the NIIT

Most people will have no problem avoiding this tax simply by never having an AGI of more than $250,000 (or respective threshold.) Super easy.

You can also avoid it (or at least minimize it) by spending 8 or 9 years harvesting tax-free capital gains before you decide to make that big boat or house purchase.

If you can’t avoid a large realized gain, try to split it across 2 years if possible. Buying a house in January may be better than buying a house in, say, July, as you can sell half of your investments on December 31st and the other half on January 1st, thereby splitting the gain across two tax years. (This can also be accomplished by borrowing – using a mortgage or asset backed loan to realize gains over multiple tax years.)

You sell your blog for a big capital gain. If the buyer is a reliable entity (e.g. a large corporation) consider an installment plan where you get paid over 2 or 3 years instead of all at once.

If none of the above are possible, then just pay the tax. 3.8% is a small price to pay, albeit important for it to be intentional vs accidental.

Summary

The Net Investment Income Tax is an extra 3.8% tax surcharge in years with big investment income.

If you can’t stay under the fairly large thresholds, just be aware that you have to pay a wee bit more tax.

Our income tax calculator now calculates a simple form of NIIT to aid in your tax minimization efforts.

My sister keeps getting dinged with this. A high-class problem.

Thanks for demystifying it a bit.

NIIT was one of the more common requests for the tax calc… and I’ll have to pay it this year, so I finally got the motivation to put this all together :)

Not sure I can follow the example. Is the $250k ordinary income (W-2 or self-employment) and $100K cap gains?

$57k in taxes would be 16% and then add state taxes and shoot way above 25% rate in aggregate. Yeah, I can see people living in high SIT locations being moving to low SIT locations, but those are getting CROWDED too.

Have you finally lined up a house to by and that’s why you came around to NIIT calculation?

It would be timely considering China’s intentions towards Taiwan.

What is SIT?

Yes, $250k of work type income, $100k of investment income.

GCR – Looks like SIT is his acronym for State Income Tax.

Retired but had a good 2020 in a taxable account. Had to pay it. Glad that Jeff Bezos and his ilk did not :(

We had a good 2021 and will have to pay it this year. Unfortunately I wasn’t also able to ride a dick-shaped rocket into space.

Ha–I was not even aware this existed. Thanks for the education!

The NIIT not the rocket!

Never knew about it and got burned by it last year. We never crossed the income hurdle until last year. I assumed it was always there and I never had to worry about it until now. Between not witholding enough and this extra tax, we ended up owing just shy of $9k. Really sucked. Need to plan better.

The first time we got hit by this, I was sure I’d made a huge mistake somewhere and scoured the net to see how I could fix it. 🤦🏻♀️ I was hoping you had more insight for future reference but it looks like what you have is what I found too. That’s some sort of comfort anyway. 🙂

What are your thoughts on using a low interest (margin) loan on your assets instead of a large cap gain harvest? M1 has a 2% loan and MMM did a 1% (ish) loan with interactive brokers.

You could harvest capital gains over a few years to pay down the “debt” and thus avoid some tax consequences?

We’re still stashing away and I find your musing really helpful in thinking through future problems:) So thanks!

There is definitely merit to borrowing instead of realizing gains. There is a breakeven point. I have this on my list of things to write about.

Thanks for the great tips here.

I am a long way away from this being an issue, but it will be important to plan for eventually.