(GCC: A few months ago, today’s guest post author reached out with the desire to share knowledge about a unique option to accelerate early retirement. Thanks to a deferred compensation plan, this post was written between retirement activities in a sunny zero income tax State. Maybe this is also an option for you…)

Does your financial freedom plan include maximizing both earning and savings? Mine did, but one of the challenges with this approach was higher marginal taxes. I discovered the (GCC: subjectively) brilliant Go Curry Cracker tax avoidance strategies years ago, but filing a 1040 with a $0 federal income tax liability was impossible as my earned income increased.

My income soared as I advanced my career, and the typical tax deduction tools were already maximized. Deductions (itemized or standard), exemptions (when they existed prior to 2018), credits (usually child and foreign tax), and cafeteria plan elections (those employer deductions like 401(k)s, HSAs, health insurance premiums, etc.) shielded less and less income from taxation. As income is subject to higher marginal tax rates, the IRS adds insult to injury by phasing out IRA contribution deductibility.

If you’re earning enough to lose this benefit, your earnings are AT LEAST into the 22% tax bracket! Imagine paying an extra $1,320+ to the IRS just because you can’t deduct a $6,000 IRA contribution. Your employer giveth, and the IRS taketh… Maybe the average high earner brushes it off as a “death and taxes” situation, but if you’re aligned with the Go Curry Cracker approach to taxes you find this unacceptable.

I did too, and now you may be thinking, “there must be a way to be a highly compensated employee AND have an IRA tax deduction.” Not only is it possible, but you can also shield even more money from your taxable income. I just “stumbled” into a savings plan that allows this, but maybe some of you GCC readers can more purposely take advantage of this.

Enter the NQDCP…

Non-Qualified Deferred Compensation Plans

You can enjoy a large compensation package, claim the IRA deduction, and lower your tax liability if you appropriately engineer your employment situation. This requires a deferred compensation program, which is more technically defined by the IRS as a 409A Non-Qualified Deferred Compensation Plan (NQDCP).

According to the IRS a NQDCP is “an elective or non-elective plan, agreement, method, or arrangement between an employer and an employee… to pay the employee… in the future.” This is the key. The employer merely promises to pay you at a future date for earnings you could receive now. When the plan is structured by the employer correctly, money deferred through the NQDCP avoids income taxes during the year the money was deferred. However, deferred compensation may still be subject to payroll taxes (although that is not a significant concern as we’ll see later on).

How it works

My filing status is married filing jointly, so the 2019 IRA contribution deductibility phases out from $103,000 to $123,000 of modified adjusted gross income (MAGI) (the phase out for those filing as single is $64,000 to $74,000). Although my wife has no earned income, the tax code has provisions for spousal IRA contributions that allows her to contribute to her IRA based on my earned income and deduct those contributions. Her contribution deductions are phased out from $193,000 to $203,000 of MAGI.

To gain the deductibility back at MAGI above the phase out limit, I simply elect a deferral amount in my NQDCP that reduces my earned income below $193,000 to deduct my wife’s IRA contribution or $103,000 to deduct both of our IRA contributions! It’s also worth noting that simply reducing my MAGI below $193,000 would allow me to contribute directly to a Roth IRA if desired, without the hassle of the Backdoor Roth procedure and its pro rata rule limitations. As long as my wife and I can live off this lower income, we’ll avoid significant taxes liabilities.

Why this works

According to IRS publication 957, deferrals under the NQCDP reduce the pay reported in Box 1 of the W-2 by the deferral amount. Box 1 on the W-2 is reported on line 1 of form 1040, Wages, salaries, tips, etc. These along with interest, dividends, capital gains (or losses), and IRA deductions compose Adjusted Gross Income (AGI). IRA deductions are added back to calculate MAGI. This is how the NQDCP allows you regain eligibility to deduct IRA contributions. (NOTE: Other items can increase or decrease MAGI, but I consider them too obscure for my example.)

Let’s look at a simple example with the 2019 IRS W-2 and 1040 forms using the following assumptions:

- A married couple that filed jointly in 2019

- Their only income was reported on a single W-2

- The gross salary of the employee was $250,000

- $19,000 was deducted for 401(k) contributions

- $10,000 was deducted for employer sponsored healthcare premiums

- They use the standard deduction and have no other deductions

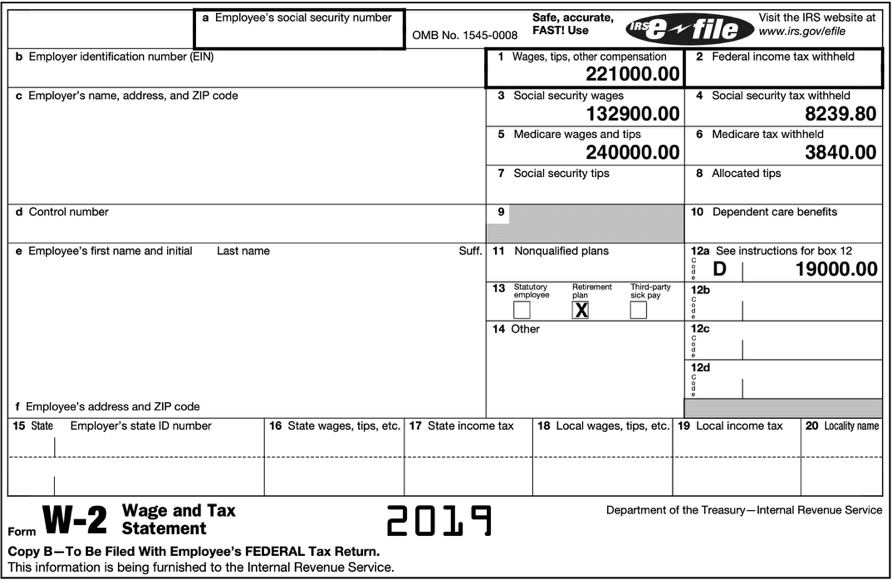

The W-2 from the employer would looks something like this:

(Note: Fields that are not relevant to this NQDCP example are left blank)

The wages reported in box 1 were reduced by $29,000, which corresponds to the employee’s 401k and health care plan deductions. The 401k deduction is also noted in box 12a and 13. We’ll discuss boxes 3-6 later, so scroll further down or just wait if you’re confused by those.

Now let’s look at the couple’s 1040 form. The $221,000 from box 1 of the W-2 is written into line 1 of the 1040. Their adjusted gross income is also $221,000 because we are assuming no other deductions. At this level of (M)AGI, neither the working spouse nor the non-working spouse can contribute to a Traditional IRA.

Next we see the standard deduction as the only reduction in income. This makes the taxable income $196,600, and results in an income tax liability of $35,533! Hopefully the withholding was enough in box 2 to cover most of this so our couple avoids a hefty penalty for under withholding this large tax bill.

Now let’s examine what happens when our fictional couple leverages a NQDCP. Let’s use most of the same assumptions, and make some adjustments and additions:

- A married couple that filed jointly in 2019

- Their only income was reported on a single W-2

- The gross salary of the employee was $250,000

- $19,000 was deducted for 401(k) contributions

- $10,000 was deducted for employer sponsored healthcare premiums

- The couple is frugal lives off $75,000 year, so they can participate in the employer’s NQDCP

- 50% of the salary, or $125,000, is deferred in the NQDCP

- They use the standard deduction

- The couple will contribute to both their Traditional IRA’s if allowed

Here is what the W-2 would look like with the same $250,000 salary. It looks exactly like the previous W-2, EXCEPT for box 1:

So now let’s look at how that affects the 1040:

What a difference that makes! The couple now has a MAGI of $96,000. They both can contribute to a Traditional IRA, and they did. This is shown on line 8a, so their AGI is $84,000. After the standard deduction they have a taxable income of $59,600 compared to the prior example of $196,600. This leaves the couple with an income tax liability of $6,764, which allows them to legally avoid $28,769 in taxes!

That’s a big win for the couple on the income tax equation, but those NQDCP contributions are still included in Box 3 and 5 of the W-2. Those lines are for wages subject to Social Security Insurance (SSI) and Medicare taxes, respectively. Unfortunately, I’m not aware of a way to completely avoid payroll taxes on earned income. Remember how I mentioned that is not significant, there is some great news here.

If you’re in a position to contribute to a NQDCP like our example couple here, your deferred compensation is likely over the SSI tax wage limit anyway, which was $132,900 in 2019. So while wages up to the limited are taxed at 6.2%, wages over have an effective SSI marginal rate of 0%!

The Medicare tax has no income limit, but that will only be taxed at 1.45% (or 2.35% for income exceeding the Additional Medicare Tax Rate thresholds set by the Affordable Care Act a few years ago). Medicare taxes will be relatively small anyway.

Since the deferred compensation is subject to payroll taxes when deferred, they will not be subject to them when received!

The Risks

The IRS’s wording about paying the employee in the future is a key distinction from qualified plans like 401(k) and 403(b) plans that you are likely familiar with. Deductions into a qualified plan are made with actual salary received. Deductions into a NQDCP are not. The employee and employer are agreeing to defer today’s earnings until some point in the future. This is an important distinction. Your promise of future payment is not an asset in an account you own like a 401(k). It’s a liability on the employer’s balance sheet.

This means the ultimate payment of your deferred compensation is subject to risks from the employer’s financial mismanagement and bankruptcy. Your employer can structure the NQDCP to mitigate these risks for the participants, but it cannot entirely eliminate them and be compliant with the IRS’s regulations. Be warned, a black swan event could wipe you out.

The Rewards

Ideally this liability also has an associated asset on the company’s balance sheet, and this could be a positive risk. An employer’s NQDCP liability could be invested, potentially with you controlling the asset allocation of your deferred compensation, and subject to the risks and returns of the market. Then the ultimate payout of deferred compensation would be based on the total returns of those investments and not the original amount deferred.

How much you can defer can vary by employer, but my experience has been up to 100% of bonuses and up to 50% regular salary can be deferred.

Even better, NQDCPs are not subject to non-discrimination rules like qualified plans. Those are the rules that can prevent you from maxing out your 401(k) because not enough of your coworkers participate or contribute enough to the 401(k). To allow companies to offer NQDCPs to only a handful of employees, the regulation for NQDCPs simply excludes any non-discrimination rules. So defer as much as you like without worry of a non-discrimination test capping your deferrals.

But my employer doesn’t have a NQDCP…

Are you sure? Remember how I mentioned that I stumbled onto the NQDCP. I did not know my last employer had a NQDCP until I was promoted to a level where it was available. These things just don’t seem to be advertised to people who aren’t eligible. You have to ask if your company has one and what levels are eligible. If you’re making enough money to have this problem, you may not be that far off. Now may be time for a discussion with your boss about NQDCP eligibility.

What if your employer really doesn’t have a NQDCP already defined? You could simply ask for one, or find another employer that will give you one. The regulation’s intent was to provide saving opportunities beyond qualified plans to an exclusive group of highly compensated employees. Yet, the regulation doesn’t actually restrict these plans to those people. You don’t need a certain minimum income, you simply need a written agreement with the employer to defer compensation to have a NQDCP.

When do I actually get my deferred compensation?

The IRS requires you to start receiving deferred compensation at a predetermined date in the future or when you separate from the employer, whichever comes first. The duration of future distributions is between you and your employer. Large companies will generally have pre-defined options. I’ve seen a plan that allowed a lump sum distributions or quarterly payments for 5 or 10 years and another that allowed annual payments from 1 to 15 years. However, the IRS imposes requirements on NQDCPs for when an initial deferral decision can be made and how changes can be made. Existing plans will have these requirements covered for you.

A few exceptions to these distribution elections are available. The original deferral decision can be overridden by disability, death, or a change in the ownership or effective control of the employer. The IRS code also allows for deferred compensation to be paid upon the occurrence of an unforeseeable emergency, but only an amount that covers the emergency.

The IRS places some additional conditions on people that meet the definition of “specified” or “covered” employees, but this doesn’t limit the availability of a plan. For example a specified employee must wait 6 months after termination to receive a distribution instead of immediately after. Some plans may just make everyone wait the six months so they don’t have to maintain two records of plan participants. This can be a good thing. For example, pull the FIRE trigger with employer in July or later, so your first distribution arrives in the next tax year.

In summary

The tax benefits of these NQDCPs may be questionable for the normal people working until retirement age. Also, deferring all those taxes, switching employers (possibly with a higher salary), and receiving distributions from your previous employer’s NQDCP could be a recipe for much higher average and marginal taxes in the future! However, I think they make a lot of sense for the FIRE crowd! These can be important savings tools when you know you will retire early from your current employer. They can also provide a penalty free income source that bridges the time between FIRE and traditional retirement.

I deferred a significant amount of money in my employer’s NQDCP. This allowed me to deduct IRA contributions again, avoid thousands of dollars of income tax liability, invest more money because of the tax savings, and ultimately shorten the time for me to become FIRE’d. It was an important part of my FIRE plan, and it could part of yours too.

Is there any way to set this up for yourself if you run your own company? Or own your own S corp?

Can I hire *myself* with an NQDCP?

Good job LinkW, already stumping me with the first question! The NQDCP regulation is written in a manner that assumes a W-2 or possibly a 1099 relationship. I don’t think that precludes self-employment, but do income recognition rules for a S-Corps and pass-thrus preclude a NQDCP? Perhaps, but I don’t know for certain. There may be better strategies for the self-employed.

No state tax is great. But typically these states have higher property tax 😇

Aren’t you eroding the value of future payments due to inflation and did you perform a study on just paying taxes on higher income and investing it? Depending on time you may be able to just make up the money by investing.

I was curious about this too, but he says somewhere in the article that your employer’s NQDCP liability could potentially be invested. That would make it just like a 401k (etc). I agree that it would only make sense to do this if you could invest or if you’re close to retirement (and the amount in tax avoidance would likely be greater than the missed opportunity of investing for a year or two). I wonder how flexible employers generally are with allowing you to invest the NQDCP liability. I think that’s the big question…

You nailed it. Those are the key issues. I hope the guest blogger responds to your comment and fleshes this out a bit.

But for someone in a very high tax bracket not far from retirement (assuming they can invest the deferred compensation in the meantime), this could be gold….

My deferred compensation was invested by my employer in much the same way I would invest my own money, and the payments are based on the investment performance. Therefore my primary TVM consideration was avoiding marginal tax rates when working vs paying average tax rates when receiving payments.

If the Plan deferred a specific dollar amount regardless of when it is payed, then I think an analysis like you suggested would be appropriate to consider.

If you earn the income in a state with income tax and FIRE in a state without, does California still come after the taxes on deferred comp?

There is no single answer on this, and it’s based on each state’s tax regulations. An HR admin at my former company told me payout duration determines state tax treatment. The max duration would have payments reported to the state of residence at the time of each payment. Any shorter payout duration would have all payouts reported to the state where you worked.

So if I worked in California before retiring to Texas or Florida, a 5 year payout would subject me CA taxes for the next 5 years. However, there is still the possible benefit of those deferred dollars being subject to a lower tax bracket in CA .

This is why I like GCC. Brings up crazy strategies that I would otherwise never know about. Good stuff!

Thanks Mighty Investor, glad you like it.

Lots of wild stuff out there. At one point in time the 401k was considered crazy.

Very common strategy among saavy sports figures & top entertainment stars…

I was offered this option when the start-up I worked at was bought by a big established tech company and I was classified as “an executive”. I worked a bunch of numbers and had some thoughts:

1) At first, it seemed like a total no brainer to put all $$ in the top tax bracket into deferred compensation since, logically, the worst I could ever pay would be the top bracket. However, I live in a no income tax state (very much on purpose) and have plans to move to a higher tax location in the future.

2) Much like a regular 401k, the growth is going to be taxed as regular income. Assuming decent capital gains as a buy and hold index investor, you might be taking a lot of the money out at 35% tax that could have been at 0% or 15%. The plan at work required something like taking the money out of at most 10 years.

3) My conclusion was that the plan was mostly set up so the SVPs and CEO could defer most of their compensation while living in California with the plan to move to a place like Florida once they leave the company.

Agree with you on the last part/

1-This benefit is only for execs- Executive Director, VPs and up….

2- it is great at shielding significant income from taxes – right now

3- you can avoid CA state taxes if you move and don’t cash out until some specified time window. There is a tax law that is not mentioned in this article that outlines this. I forget what it’s called unfortunately. But I set up my disbursement schedule for when o plan to live in a tax free state

4- there is risk with these plans and you need to be with a stable company to make a choice to put your money in these as you can lose your money if the company goes bankrupt. Makes me wonder about the exec money at places like Newman Marcus or JCP or soon coming the airlines now…. their deferred compensation money is at risk of being lost entirely

Really nice post. I had no idea strategies like this even existed as I was never offered this option before.

Thanks Max!

Why complicate all this? Just max out your 401k and Roth, LBYM, and call it a day. Extra money can be dumped in a taxable account… Plan trips, and spend time with family… Life is too short to stress over/complicate these things.

Why? To avoid taxes and invest more money. I don’t want to overcomplicate things either, nor do I want to trap myself in a false dilemma. The US tax code is complex, but learning how to minimize taxes through that complexity earned me a year of travel with my family that otherwise would have been spent in an office.

The least complicated option is to just put everything in your taxable brokerage account.

Why complicate things by limiting access to your funds before age 59.5, restricting investment options (only what is available in your 401k), having forced withdrawals after age 70.5, and spreading your savings across 3 or 4 different companies. And on top of that we have government managed health insurance and annuities? Life is too short for that nonsense.

You do no have to wait until 59.5 to access these funds. My disbursements begin at age 50.

Age 59.5 is for the 401k and IRA that were highlighted as uncomplicated.

I worked for a company that offered this to certain levels of management. Essentially, it is unsecured debt held by the company and it paid 8% per year.

Fast forward a few years. Crappy management, greedy Russian oligarchs, banks that couldn’t price risk. Company declared bankruptcy. All this was a “pre-petition claim” Some folks lost over $1million.

Never again. Take the money. Pay the tax. Invest it yourself. Then only YOUR bad decisions can sink your future.

This is spot on. I don’t have this option, but my wife does and we decided against it for similar reasons. If you’re making enough to qualify for one of these, chances are you’re working your butt off. Take the money.

James, that seems like a very, “interesting,” work environment. Probably a great story, except to the people living it.

But it made me think about ESPPs (Employee Stock Purchase Program). If your company offered an ESPP and you thought it was too risky, then the NQDCP is definitely too risky. If you would take the ESPP, then the NQDCP may STILL BE too risky for you.

It is hard for me to automatically put this tool into a good / bad category.

If I worked for the money laundering arm of the Russian mafia I would probably make different choices than if I worked for Amazon/Apple/Microsoft with $1 trillion in cash.

I would also have to consider timeline – will I touch these funds in 30 years or 3?

I know you are USA citizen, and most reader probably from US. But do you mind writing an article for international Retire early/FIRE nomads? on tax implications? which ETFs to hold? where? etc… etc? Basically, similar to all your excellent articles, but also one piece for the people who hold Non-US status. Thanks a lot for all your great work in behalf of all of us international non-us readers. We love your work.

Thank you Martin

I would like to write about those things, but I know so little about them. Perhaps a non-USA reader would be interested in sharing via a guest post?

“Be warned, a black swan event could wipe you out”. Like COVID-19?

Ironic timing isn’t it?

My experience was similar to what the author mentioned: deferred compensation was not advertised and is only available after a few promotions.

My employer offers two flavors: stock and cash. In the stock deferral, you can defer up to 30% of gross pay and company will match 25% of every dollar deferred. All dollars go into a company stock fund. You can defer for 1 to 5 years.

In the cash deferral, you can defer up to 25% of gross pay. No company match on these dollars and they are put into a bond(esque) fund at around 3% to 4% annual return.

I participate in stock deferral but mainly for the match and less for tax purposes. As I get within 3 years of FIRE, I plan to do the cash deferral to utilize the tax savings. My calculations show that within that 3 years (or less) horizon, it’s likely that the tax savings on deferral outweigh the foregone gains of investing the post-tax alternative. But beyond 3 years, you’re likely better off taking the tax hit and investing the post-tax dollars.

A few years into our FIRE journey, I realized that my spouse had a DCP option with her employer. She was in a particularly fortunate position because she worked for a state hospital, which offered a 401a DCP plan, which has a big advantage over the 409a NQDCP (which is what this guest post is referring to) in that it is a qualified plan and can be rolled into an IRA after leaving the employer. This means that the risk of losing this money due to employer bankruptcy was a non-issue. That difference aside, we used the same strategy as suggested by the post author – we lived off of my income and maxed her 403b, her 457, and stuck the remaining into the DCP so that her take-home was effectively zero, which definitely helped with taxes. When she made the call to her HR to set that up, they were definitely confused!

My wife worked as a teacher for years before we realized that she qualified for a 457 plan (deferred compensation for gov’t employees).

457 contribution limits are equal to 401k (or 403b in her case) and you can contribute to both in the same year (sum of $39k in 2020), tax deferred.

Her 457 account is invested in the S&P 500.

These government 457 plans should be more stable than non-government NQDCP (or maybe I’m naive)…

Yes, 457s are great. Tax deferral, funds are your asset upon deferral, and withdraws once employment ends regardless of age. It’s like combining some of the best features of a 401k and a NQDCP, but leaving in place the contribution limits.

My company offers this. It was attractive for me because you could invest the money in the same funds offered in the 401k. And the big one, they offer a small match.

My strategy is to defer up to the match and invest it the same as I would my 401k money. I set the predefined withdrawal date as early as they would let me (2 years I think?) so it becomes mine as soon as possible. Then gets thrown into my regular taxable account.

So if the tax benefits aren’t reason enough for you, check if they offer a match.

Aus: section 323 of the Fair Work Act 2009 – an employee must be paid “at least monthly”.

Employees: ‘Negative Gearing’ allows individuals (including employees), to deduct business costs from their gross wages. Typically mortgage interest and depreciation on a residential investment property. That converts current wages to future capital gains which might be realised as increased future rent or taken as capital gain when tax rate is lower due to not receiving wages.

Businesses: ‘Dividend Imputation’ allows companies to retain after tax earnings / profits and pay amounts of dividends, together with tax credits for company tax paid, that are lowly taxed in shareholders hands. Thus otherwise higher taxed income can be deferred and paid when the shareholder’s tax rate is lower.

Aus: Examples closer to USA Deferred Compensation Plans:

https://iknow.cch.com.au/document/atagUio567014sl17284409/td-93-242-income-tax-treatment-of-a-deferred-salary-payment-agreement

https://employsure.com.au/guides/annual-leave-and-other-leave/long-service-leave/

Thanks for sharing Bullockornis. That’s an interesting option. It appears to have less risk since one example describes the deferred amount held in a savings account, implying that it’s the employee’s/contractor’s asset.

“interesting option”:

… but where ‘the deferred amount is’ … ‘applied, accumulated or invested for the benefit of the taxpayer’ then the amount is taxed at that time.

Example 1: taxed over full 5 years = tax deferred..

Example 2: taxed over first 4 years = not tax deferred.

Good post. From what I learned: The key to such plans is “reasonable risk of forfeiture” as I understand. And companies using them as retention tools by writing tenure conditions (say, 3/5 years). If your employer is a Microsoft or Google, there is no issue but for smaller organizations, it is a risk if the employer goes bankrupt. Technically, the deferred income belongs to the employer until tenure is satisfied and then it gets paid to you.

Thanks TFR. In my experience, I haven’t seen these plans used as retention tools. Across several companies I have seen a completely separate stock grant program used for retention. These will have the 3 to 5 year vesting periods, where quitting early wipes out the unvested shares.

Hey Matt,

Awesome article, I never knew this existed. I am asking my company now if they participate.

What if you work for a private company instead of a public one? Can they change the terms of an NQDCP on a whim compared to a public company?

The reason why I ask is because I have been blessed with professional success where this would make sense, however I am less nervous about my current company going bankrupt (they’ve been around since 60’s and have large amounts of cash) then I am in them trying to withold one’s earnings for other reasons (laying employees off, legal loopholes, etc.).

They are a stingy private company who hold grudges and have sued past employees under less than ideal circumstances for leaving and taking better opportunities so I’m just a little nervous if I went down this path…

Thanks!

I took part in my employer’s deferred compensation scheme. There was a good choice of low cost funds in invest in, and the payout was set for five years out, 20% a year for five years, with an option to defer each upcoming payout for another five years. Fantastic! Then I resigned my position to move to another firm and… there was no choice but to receive immediately the whole amount in a single lump sum.

On the upside, there was capital gains which had grown tax free. On the downside, the tax bill was absolutely horrendous, and it was disconcerting to have large salary deductions which I couldn’t alter for the entire financial year (unlike a 401k or taxable investments).

Although it might be suitable for some people, I wouldn’t do it again.

This is the best article I’ve ever seen on the 409a. I personally used this to help accelerate my early retirement. I put almost $300,000 away and set the plan up to pay me out monthly for 15 years. I now get a steady paycheck coming in that covers around 1/3rd of our early retirement spending.

Thank you for such a helpful article. It prompts me to make changes for next year. My husband’s job offers NQDCP. However, we have not taken advantage of it due to our ignorance, fear of the company’s bankruptcy, and the false belief that the money in NQDCP just sits there. Now I’m no longer ignorant about the subject since I have read your article and done research. In my assessment, the company’s bankruptcy risk is <3%. The NQDCP offers 15 investment options, one of which is the Fidelity Total Market Index Fund, FSKAK. At open enrollment in October, we will elect to start NQDCP next year. The plan allows to defer up to 100% of base pay and 100% of incentive bonuses. At open enrollment, we also must elect distribution start time (in 5 years or later), frequency (lump sum or quarterly installments), & duration (over 3, 5, 10, or 15 years). Our plan is to reduce the net earned income, line 1 on form 1040, to $120K. That would allow us to contribute $12K to the 2 Roth IRAs and to save $55K in federal tax & $18K in CA state tax. We would continue to maximize contributions to Roth 401k & Roth in-plan conversions ($35K). My question to the author is why contribute to IRA instead of Roth IRA. Isn't tax-free growth preferred over tax-deferred growth?

>Isn’t tax-free growth preferred over tax-deferred growth?

No – which of the 2 results in the lowest tax rate is preferred.

Thank you for your answer. That made me think about our income & tax rate now versus income and tax rate in retirement.

I also have another question about the case. Assume the fictional couple retire next year; 5 years later, they collect the annual NQDCP distribution of $80,000 over 10 years. Would this $80,000 be wage & reported on Line 1 of form 1040? If yes, can the couple contribute $12,000 to their IRA or Roth IRA annually for these 10 years?

I found out the answer to my own question by reading the 2019 Publication 590-A, page 5, http://www.irs.gov/pub/irs-pdf/p590a.pdf. Correct me if I’m wrong: compensation for the purposes of an IRA does not include “deferred compensation (compensation payment deferred from a past year).”