2X the Contribution, 1/2 the Work

Earning a little income in your retirement years is becoming increasingly common.

Some choose to work part-time for benefits or socialization or fun, and others accidentally make a little extra while pursuing their hobbies or passions.

With a powerful investment portfolio behind these (early) retirees, this income is often just added to a Roth IRA for further tax-free growth.

Now, what if there was a way to double those Roth contributions without working or earning more? Turns out, there is.

Double Dip Roth Contributions

Total compensation

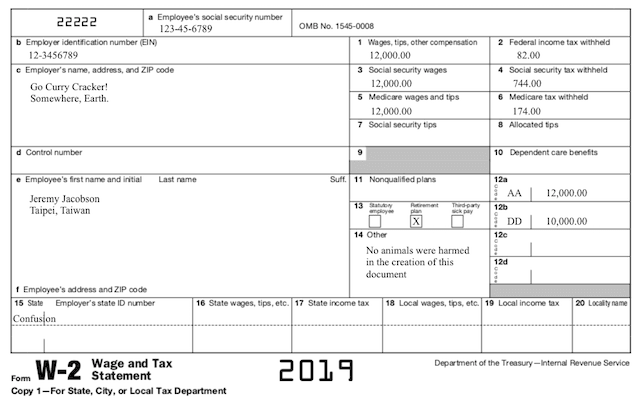

As an employee, every year we receive a Form W-2 Wage and Tax Statement from our employer. This form shares all of our income, benefits, and tax withholding for the year, which we dutifully report on Line 1 of our tax return.

It looks something like this: In this fictitious example, I earned $12,000 working part-time for a company called Go Curry Cracker! (What a weird name!) This is shown in Box 1, Wages, tips, and other compensation.

In this fictitious example, I earned $12,000 working part-time for a company called Go Curry Cracker! (What a weird name!) This is shown in Box 1, Wages, tips, and other compensation.

As required, the employer withheld taxes throughout the year, $82 in federal income tax (Box 2), $744 in Social Security tax (Box 4), and $174 in Medicare tax (Box 6.) All together, $1,000 in taxes were withheld from my paychecks, resulting in take-home pay of $11,000.

401(k) Contributions

With $11,000 in after-tax income, how much can I contribute to the company’s 401(k) plan?

The IRS states that annual 401(k) contributions are limited to the lesser of 100% of the employee’s compensation or the annual contribution limit ($19,000 in 2019. Employee’s age 50+ can make an additional catchup contribution.)

100% of our compensation is shown in Box 1. Thus, we can contribute $12,000.

In this example, I choose to make $12,000 in Roth contributions. This is shown in Box 12 with the AA code – “Designated Roth contributions under a section 401(k) plan.”

Had I instead chosen to make $12,000 in Traditional (pre-tax) contributions, these would be shown in Box 12 with code D, and would also be subtracted from the amount reported in Box 1 (See IRS W-2 instructions pdf.) In this case, Box 1 would be changed to zero dollars ($0.00.)

Any matching / employer contributions to the 401k are not shown on the Form W-2.

IRA Contributions

Now that I have made $12,000 in Roth 401(k) contributions with take-home pay of $11,000, how much can our household contribute to IRAs?

IRA contributions cannot exceed the lesser of the annual limit and total earned income. In 2019, the individual IRA contribution limit is $6,000. (Individuals age 50+ can make an additional catchup contribution.)

Total earned income is shown on Box 1 in the amount of $12,000.

As such, I can make a contribution to an IRA in the amount of $6,000 (the individual limit.)

As a married couple, my spouse is also able to make an IRA contribution in an amount equal to the lesser of the individual limit and total household compensation minus any IRA contributions that I make. Or $12,000 total compensation minus my $6,000 IRA contribution = $6,000 spousal contribution.

Total IRA contributions (either Roth or Traditional): $12,000.

Had I elected to make Traditional contributions to my “work” 401(k), reducing the number on Box 1 to zero, we would be unable to make any IRA contributions.

Self-employment

Self-employed individuals don’t receive a Form W-2, and their income for the purpose of determining retirement account contribution limits is based on net earnings.

The difference is due to a deduction for the payment of 1/2 of self-employment taxes (the “employer” half.)

To contribute $12,000 to a solo Roth 401(k) and an additional $12,000 to his/her Roth IRAs, we would need net-earnings from self-employment of ~$12,912 (and 25 cents.)

(To see how this is determined, check out our Self-employment tax / Net earnings calculator.)

Bonus

Combine with the Saver’s Credit for extra oomph. (Up to a 50% tax credit on retirement account contributions!)

Summary

Sometimes IRS math is funny math. That is the case with Roth 401(k) and Roth IRA contributions.

Roth 401(k) contributions are not deducted from W-2 Box 1 total compensation, which is a safe harbor value for determining individual IRA contribution limits. This effectively means we can double contribute.

As such, with as little as $12,000 in gross earned income, a married couple can contribute up to $24,000 to Roth retirement accounts. (More if you are age 50+.)

Double your Roth retirement account contributions without working or earning more! 2X the contribution or 1/2 the work.

Love your blog Jeremy especially on cap gains harvesting and IRA conversions. Since retiring several years ago, I have been maxing out on my Roth IRA contribution as a spouse since my wife still works and I earn zero. Got to love those spousal IRA rules.

Also got to love having a working spouse! :p

Would conversions of traditional IRAs to Roth IRAs count as a substitute for box 1 earned income? That is, convert $12,000 instead of earning $12,000 from a job and then still be able to make the $12,000 in Roth contributions?

No. Earned income is job income, self-employment income, etc…

Hi Jeremy!

This is probably a dumb question

but I can’t figure out your calculations.

How can you contribute $12,000 to solo 401k after paying at least 30% in taxes as self-employed and then contribute $6,000 to regular Roth IRA when you made total of $12,912 for the year and your contributions total $18,000? Won’t you be short?

You would have only $8,400 in net income after paying taxes but you are contributing $18,000 (solo plus regular Roth).

Wouldn’t you be short almost $10,000 to make your contributions?

And also what would you be living on?

I second this question.

How can you contribute more money than the money that came in?

Does the extra contribution money come from your taxable account? But then I don’t see the point of doing that because you’d be tying up your money until 59.5.

See my reply to Elena.

Yes, the extra contribution comes from your taxable account.

The point is you are retired and have 25x+ your annual spending in investments. You don’t need $12k today or before age 59.5, but you would appreciate having all future growth on those funds be entirely tax-free. (Technically the Roth contributions can be withdrawn any time tax and penalty free (the growth is locked up until age 59.5.))

Not a dumb question at all. As I said in the summary, sometimes IRS math is funny math.

First, you don’t pay 30% taxes as self-employed, especially not on income this low. On $12,912 of self-employment income, you’ll pay $0 in income taxes, $1,824 in SE taxes, and have an above-the-line deduction for 1/2 of the SE taxes ($912), bringing net earnings from self-employment (nefse) to $12,000. (See the calculator.)

IRS rules for contributions to solo 401k and individual IRAs are based on nefse, and function as described in this post.

Yes, you will contribute more $ than you earn. Yes, you will be short. That’s the point.

This allows you to move some of your cash or money in your taxable brokerage account into a Roth for tax-free future growth.

You live off your retirement assets. The “job” income is extra; you are already retired / financially independent, or at least well on your way.

As a married couple, my spouse is also able to make an IRA contribution in an amount equal to the lesser of the individual limit and total household compensation minus any IRA contributions that I make. Or $12,000 total compensation minus my $6,000 IRA contribution = $6,000 spousal contribution.

I’m confused

Wouldn’t the math be the lesser of the individual limit ($6000) and total household compensation ($12000) = $6000 – my individual IRA contribution ($6000) = $0??

How are you coming up with a $6000 contribution limit for the spouse?

total household compensation is Box 1. 12k – 6k = 6k

I love the way you think. I didn’t know this option existed. Thanks for sharing!

Wow, I never knew about this loophole. It sounds like a great way to beef up your Roth. I’ll keep it in mind for when Mrs. RB40 retires. Our income will be lower then and might sneak into this sweet spot.

Jeremy, the IRA contributions in your example aren’t specifically called out as Roth but based on the post title I assume they are. Do they have to be because making traditional IRA contributions would have eliminated the earned income needed to make the Roth 401k contribution in the first place, the same as making trad 401k contributions would have eliminated the option for a Roth IRA contribution?

Thanks for always looking at the different angles and sharing your experience.

You can make Traditional or Roth contributions to your/spousal IRA. This has no impact on what you can contribute to your 401k.

Could you also contribute 12,000 to a traditional IRA and then use the backdoor conversion to make this a 3x win?

Nevermind, looking into this it seems it’s a 6k max of combined Roth and traditional contributions.

Correct, it is $6k total for all IRA contributions. There is no way to get around that limit.

Better do those Roth conversions ASAP! Time’s a tick’n. 31Dec19 is the deadline.

So this is pretty much like a mega back door Roth?

No, this is something else entirely.

Here you earn $12k and contribute $24k.

To contribute $24k to your work 401k you would need to earn $24k. Then you could contribute the full amount, $19k as regular contributions and 5k as after-tax non-deductible non-Roth (to be converted to Roth as part of backdoor.)

This is a GREAT post!

I am very interested in leveraging the Roth 401K. We have a small income from our online activities (Less than $7,000) I’m using TurboTax and it shows the qualifier below for a Solo Roth 401k versus a Solo 401k. Am I reading this correctly: You need employees for a Roth 401k???

We’re over 50. So, we’re qualified for $25K of elective contributions. This seems to not be tied to our business income. Is it correct that we can contribute the entire $25K even if our income is only $6,000?

Blurb from TurboTax:

“The Roth 401(k) plan is also a retirement savings option for those who are self-employed. The advantages are the same as individual 401(k) plans, except there are more paperwork requirements.

Unlike individual 401(k) plans, Roth 401(k) plans are for businesses that have employees.”

You don’t need employees for a solo 401k (and actually can’t have them.) Look at Vanguard or Etrade solo 401k docs, and make sure the plan is open before Dec 31st or you won’t be able to contribute at all.

Solo 401k contributions are limited to your net earnings from self-employment, so less than $7k. (about $6,500, see math.)

Then as highlighted in this post, you could also contribute that ~$6.5k to his/her Roth IRAs..

Does not seem as exciting if you are single.

Earn $6k, contribute $12k to Roths. 1/2 as exciting as a married couple.

You are so flippin’ clever! Your posts make me strain my brain but I love it. Thank you for your hard work putting these ideas out there for all of us to benefit from. Health, wealth & happiness to you & your family in 2021!

You are too kind. A wonderful 2021 to you as well

Okay, this is a bit mind blowing. I am single, only made 15K, 1.5k went into company 401k pre tax and post tax dollars, which isn’t much. I did just do a Vanguard Roth max 7k. But, if I’m following you, I could go back to my company and add 15K to my Roth 401k?? (It’s now April 2021 but taxes have been delayed until May 2021). Confirmation would be golden! Thank you!

Technically, yes. But it depends on your 401k rules – they may be unable to accept prior year contributions. Check with HR or whomever manages your 401k

Yes, it seems that my company’s plan won’t allow this (has to come from your “paycheck”) to fund accounts. :( That said, this was still some empowering information. Found you from the book, The Simple Path to Wealth, and like the book, your information is fantastic. Thank you!

Just want to make sure we aren’t leaving any money on the table here : )

I know we are on the hook for FICA, but either way, we are getting back a refund for our $82.00 from line 2 through our standard deduction, correct?

Let me know if I am thinking about that correctly because I have a few more things on my Christmas list.

Max

Yes, that $82 withholding will be refunded if you don’t have taxes due from other income. I just included it here because it made for nice round numbers and unless you file a W-4 with “exempt” status your employer will probably still withhold something.

Awesome.

Have you ever found a calculator that shows how they calculate what they take out of our check based on allowances/income? Seems like I tried to back into it a few times without much success. I should probably just ask our payroll department.

Max

See IRS Pub 15, or try their withholding estimator.

Wow. Great post. I made a mistake this year with hubby’s income. He works just so we can get health insurance. I switched his retirement contribution from 401k to Roth 401k based on the above math. Thanks for some great advice!

Jeremy,

Thank you for your continued work in supporting learners. I think I’m going to ask an obvious question, but it’s not to me…Where will you “get” the additional 12,000 to contribute to your IRA’s. If you have contributed the 12,000 to the 401 where does the other money come from? Learner…

It comes from your brokerage or bank account. You are just moving $ from point A to point B (the Roth.)

The maximum paycheck deduction any of my previous employers would allow was 50%. Part timers are often not eligible at all. For anybody self-employed it’s a great option.

Yes, that is a plus for self-employment. Google part-time jobs with 401k -> Costco, Starbucks, Home Depot, REI, etc… they still probably don’t allow 100% contributions

My company allow aft-tax 401k. IRS 2019 limit is $56,000. So I do mega aft-tax and convert to Roth every year. My wife is doing the same. So total family mega Roth IRA is 112000 per year plus over 50 catch up $6000×2. So we do $124,000/year Roth. Doing this for 30 years. Assume 0% gain, we will accumulate 3.72 million, we bought our house 5x leveraged with 5% annual gain (with 3% APR mortgage). In addition, we max out HSA, 529. Still have pension at $50000+$40000=$90000 at 65. Will delay SSI till 70 with zero RMD. We have paid vacation 25 days each year. Enjoy our 8-5 working schedule plus something business paid traveling vacation. We established a family trust, so the total Roth will go to heir tax free. Wife just bought a fairly used Porsche macan at 1/3 of the MSRP. Couldn’t be happier with our life.

Aus: $25,000 per individual ‘concessional’ (=tax deductible) contribution to ‘superannuation’ taxed at flat 15% – not rational if individual taxable income less than $20,500 (senior $29,600) when marginal tax rate is 0%. $100,000 per individual ‘non-concessional’ (=already taxed’) contribution – not taxed.

Pension is tax free. Can re-contribute required pension withdrawals within said limits if work for 40 hours in any 30 consecutive day any time in a year to age 75.

Its incorrect to state that if you a typical 401k contribution to your 401k, that you couldn’t do a Traditional IRA. Anyone with earned income can contribute to an IRA ( they may not get a deduction though)

Nope. You can contribute whatever is in Box 1 to an IRA. If Box 1 is zero, you can contribute zero.

Thank you for this info. It was exactly what I was looking for, since I’m in the same situation.

In your example, you grossed $12,000, netted $11,000, yet contributed the full $12,000 to your 401k. How did you get your company to contribute the $1000 that was already taken out for taxes?

Before I retired earlier this year, I earned about $9200 in gross, $8200 net. I asked HR to put the entire amount in my Roth 457. They put in $8200. I didn’t have any way to add the extra $1000.

Thanks!

You are dependent on what your company will allow, which may be more restrictive than what the law allows.

This seems off. If you gross $12k, and net $11k after taxes, but still put $12k into Roth accounts, then you aren’t paying taxes. Rather, the employer is paying your taxes for you. And if the employer is paying your taxes, that would be more taxable income.

I understand and agree that if you have outside money, you can use that to fund the 6k in the Roth IRAs. But I don’t think you can contribute $12k to the 401k. (you could end up there if the employer is doing an employer match/contribution). Help me out if I’m missing something.

The law allows you to contribute whatever is in Box 1 of the W2 ($12k.)

What your 401k plan allows may be more restrictive

How would this look with tax filing as MFS?

Conceptually the same. But if you lived with your spouse at any time during the year then maybe you can’t contribute anything (due to $10k MAGI limit.)

Somehow I missed this article when first released. Maybe because I was internet-less sailing in the middle of the Caribbean Sea at the time ;)

Anyway, good write up. I don’t think I’ve seen anyone else talking about this online. I’ve been doing this for a couple of years now myself. Instead of doing bigger Roth conversions, I do the double whammo Roth 401k + Roth IRA contributions to get some additional $ into the Roth space.

My tax planning spreadsheet I use every year has a big bold note that says “DON’T FORGET ROTH 401k CONTRIBS DON’T REDUCE INCOME!”. Every year I pat myself on the back for figuring this out. Or maybe you or someone else told me about this a few years ago? Anyway, neat method to juice the Roth space :)

I probably learned it from you. Thanks for being a bad example.

This is a great post!

I previously had this idea and this is the only place online that suggests it is a viable strategy.

I have 1 important question though:

Has it been vetted by a CPA?

(I apologize if you are a CPA)

Same question and reservation as Matt’s. Sounds too good to be true. Could you provide IRS publications/references for this strategy? Thanks.

Try IRS Pub 590-A. Go through worksheet 2-1.

Pub 590-A shows how to calculate taxable portion of the Social Security benefits, if you have any. It uses IRA contributions in the process, but they assumed to be legitimate. How is this related to the topic of this blog?

What you are describing sounds like Pub 915.

Pub 590-A is Contributions to Individual Retirement Arrangements (IRAs)

Hi Jeremy,

Should I invest my Roth IRA into different funds / indexes or how do I just let it invest itself in a retirement account?

Thanks.

So I really wanted to use this cool post to double my Roth contributions after retirement but I encountered a hurdle so thought I would get your expert opinion.

I have a Solo 401k at Fidelity but it is pre tax. It seems that Fidelity doesn’t have a ROTH Solo 401k which I was quite surprised to learn.

So if I wanted to do this as someone without a W2, my only options would be to do a custodian transfer of my 401k to Vanguard to other institute which allows ROTH 401k contribution, correct?

Just wanted to see if I am missing something.

Yes you need a Roth 401k option and earned income. E*trade or Vanguard have Roth solo 401k.

Hi, do you have any tips on which ROTH IRA stocks, ETF’s REITS etc. should I invest in?

I only have one tip. Take a few hours and read The Simple Path to Wealth by JL Collins.

Thank you and appreciate all your helpful articles.

Great article and great idea! Is this Roth “double dipping” still allowable in 2024? And would there be anything different if instead of a Roth 401k it’s a Roth 403b?

Box 1 of W2 is a safe harbor for IRA contributions in 2024.

Contributions to employer Roth accounts don’t reduce box 1

Very late to the game, but this is amazing! Thank you for some great ‘news you can use.’

Question- does any of this impact your ability to do Roth conversions? That is, can you do what you did here AND do some Roth conversions the same year?

Roth conversions are taxable so there are no limitations… do them whenever you want, as big as you want.

Can you also contribute the 20% employer matching after putting in all $12,000 into solo Roth 401k employee contribution?

No. Solo 401(k) Contribution Calculator