A Fully Depreciated Asset (photo credit)

Bloggers, digital nomads, side hustlers, and business owners have more opportunities for tax savings than the average employee. One of my favorites is the ability to turn stuff you already have or were going to buy anyway into beautiful tax deductions through depreciation.

Have an extra room in your house? Write it off. That computer you once used for Facebook but now use to write blog posts and manage investments? Write it off. The smartphone you use to populate your Instagram feed? Write it off. The new SLR camera and lenses you plan to use to share details of the nomadic lifestyle? Write ’em off!

There is nothing better than having Uncle Sam help pay for the stuff you need for your business.

Naturally this ability to write it all off is a superpower that is rife for abuse, so the IRS has a whole mess of rules to follow. But as with all rules, there are always ways to optimize to your advantage. In this post I walk through the opportunities, gotchas, and strategies for depreciation write-offs using some common side hustle tools and equipment.

Opportunities

Depreciation for Side Hustlers

To “write it off” simply means to deduct expenses from taxable business income. Small items such as the pen and notebook I use to make notes have a short lifespan and can be expensed, meaning to write off their whole value at the time of purchase.

Tangible items with longer life span (computers, desks, cameras) must be capitalized and depreciated, meaning to write off the expense over time as its value is reduced due to wear, tear, and obsolescence. Because a computer or desk provides value over many years, and can be sold to recover some cost, we can only write off a portion of its worth each year.

The IRS provides a 114 page rule book that outlines the method and madness for calculating depreciation, called Modified Accelerated Cost Recovery System (MACRS). Underneath are two subsystems, the GDS (General Depreciation System) and the ADS (Alternative Depreciation System.)

Who reads this crap? Well… me :$. And in my mind, this is the most overly-complex / nuanced / stupid part of the whole tax code. So let me simplify it. (Part of simplification is this post does not apply to automobiles or real estate.)

Depreciation 101

To calculate depreciation you really only need to know 3 things:

- Cost / basis (lower of purchase price & fair market value)

- Asset class per IRS (from a Table)

- Date item was placed in service (1 of 3 Conventions)

An example will provide clarity:

On August 1st, we start a new blog. Yeah! We use a laptop we bought last year for $2,000, and plan to use it 60% for blogging, 20% for managing our investments, and 20% for personal use. (Hot tip, as long as the laptop is used at least 50% for business, you can depreciate time spent managing your personal investments, an “income seeking activity.”)

From Ebay and Craigslist we deduce that the fair market value is $1,250. Our depreciable basis in the laptop is thus $1,000 (80% * $1,250, personal use is not deductible.)

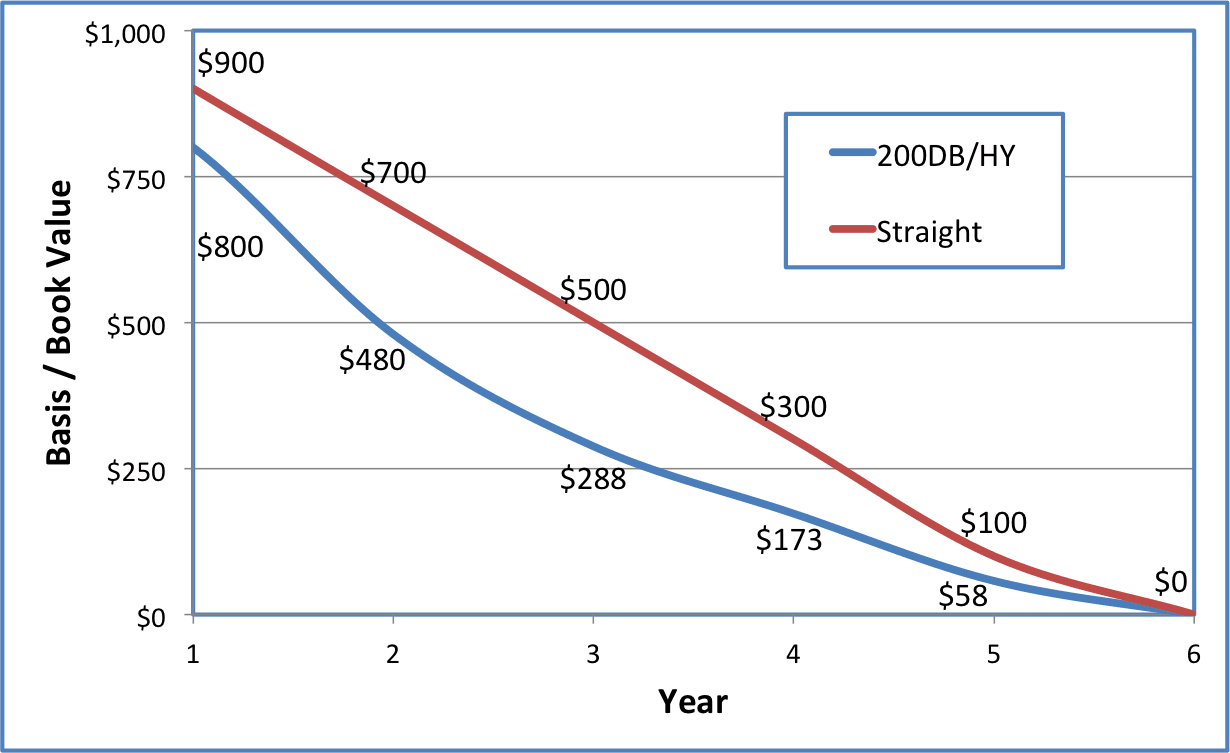

From the IRS asset class table we learn a laptop has a 5-year recovery period. We also learn that a default Half-Year convention applies (more on convention later.)

We can choose the method of deprecation (math here) based on our tax goals, either a Declining Balance or a Straight Line method. A DB method results in greater write-offs in the early years ($200 in Year 1 vs $100 for Straight Line.) This chart shows the possible depreciation. The numbers comes directly from another IRS provided Table, and TurboTax does all of this for you.

In Year 6, the book value is $0. Our laptop has been fully depreciated.

In Year 6, the book value is $0. Our laptop has been fully depreciated.

But wait, there is more…

Exceptions

The rule that a capital asset must be depreciated has two exceptions, the Section 179 Deduction and Special Depreciation (aka Special D.)

Section 179 Deduction

The Section 179 Deduction allows a complete deduction of the cost of purchasing tangible items, as long as the item is used at least 50% for business purposes.

Buying a $5,000 camera for 80% business use? You can deduct $4,000 (80% of $5k) of that purchase today. Write it off!

There are limits to total Section 179 Deductions, but most people won’t have issues (Max: $500k)

Special Depreciation

Special D allows a substantial depreciation allowance in the year an item is placed in service, currently 50%. (This is reduced to 40% in 2018, 30% in 2019, and 0% in 2020 and beyond.)

To qualify for Special Depreciation an item must be purchased NEW by you (“original use.”) An used camera from Craigslist is not eligible, but converting your old camera to business use is.

Buying a $5,000 camera for 80% business use? You can deduct $2,000 (80% of $5k x 50%) of that purchase today. Write it off!

The Section 179 Deduction, Special Depreciation, and normal MACRS Depreciation can all be used together / combined to create powerful tax optimization opportunities.

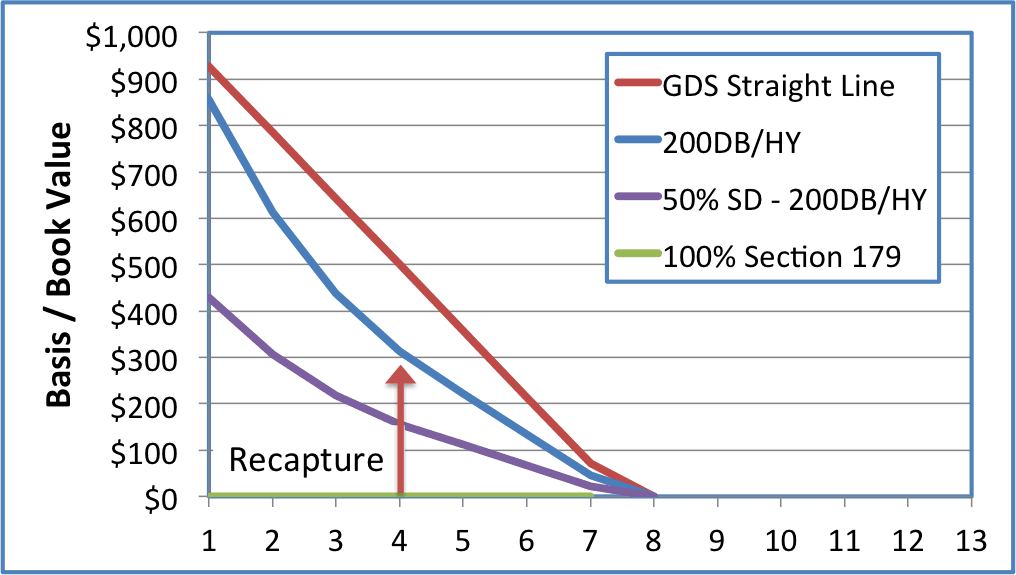

This chart shows a few different options available to us for a $1000 desk. Office Furniture has a 7-year recovery period. In Year 1 we can choose to write off anywhere from ~$100 to $1,000, depending on our tax needs and goals.

A $1,000 deduction at the 15% Federal marginal rate will reduce the tax bill by ~$300 (15% Federal, ~15% Self Employment.)

Gotchas

With something this powerful, it behooves us to plan in advance.

Recapture

If at anytime during the recovery period we dispose of a capital asset, we must recapture any deprecation up to the point of depreciation previously allowed or allowable.

That is a mouth full. But all it means is that if we sell something for a price different than current book value, we may have to pay back (recapture) some of the depreciation.

Again, an example makes it clear:

We bought a $1,000 camera 100% for business use, and in July of the 4th year of use we sold the camera (7 year recovery period) to a stranger on Craigslist for $312.40.

If the sale price is different than the book price we have an ordinary gain or loss. The book value will be different depending on if we claimed a Section 179 deduction, Special Depreciation, or normal MACRS depreciation (or all 3.) It also depends on which depreciation method we used (1 of 4.)

If we expensed the camera entirely using a 100% Section 179 deduction, our book value is zero (the Green line.) We must recapture the entire sales price of $312.40 as ordinary income.

If we used normal 200DB/HY depreciation (Blue line), our book value and sales price are the same ($312.40.) We have no gain or loss.

If we used Straight Line depreciation (Red line), our book value is $500. We have an ordinary loss of $187.60 ($500 – $312.40.)

In all of these situations, the amount of depreciation / write-off is exactly the same. The only different is the timing. (For another good example, and more on Listed Property, see thismatter.com.)

In all of these situations, the amount of depreciation / write-off is exactly the same. The only different is the timing. (For another good example, and more on Listed Property, see thismatter.com.)

So recapture isn’t that big of a deal, it is just something to be aware of and plan for… but in some cases it can become a big deal.

Recapture of Listed Property

Listed property (aka mixed-use) property is anything that has both personal and business use. Two examples are Computers and Cameras (but also cars.)

Because depreciation is such a powerful tool for tax avoidance, there is a tendency to overstate the amount of business use or to claim personal use items as business use. So the IRS has strict rules for Listed Property. (Special warning: Document with ridiculous level of detail the amount of usage on these items for business & personal use.)

If at any time the business use of listed property is less than 50%, immediate recapture is required, and in an almost punitive form: we must use straight line recovery under the ADS (Alternative Depreciation System.)

Expanding on the Camera example from above:

We bought a $1,000 camera 100% for business use, and in July of the 4th year of don’t travel much so our business camera use drops to 40%. This is cause for immediate recapture under the ADS system. GDS can only be used for property used at least 50% for business.

Under GDS, a camera is a 7-year property. Under ADS, the recovery period is 12 years. Twelve. And while we could use accelerated depreciation options under GDS, now we have only straight line.

Since we drop to 40% business use in the 4th year, we can claim 3 years of straight line depreciation at 100%. This is a total of $208.33. If we had used a 100% Section 179 deduction, we now add $791.67 to income for the year ($1k – $208.33.)

For the current / 4th year (and subsequent years), we can still claim straight line depreciation of $33.33 ($1k * 40% * 1/12.)

The recapture amount can be significant, especially if you weren’t expecting it.

The recapture amount can be significant, especially if you weren’t expecting it.

This table highlights some of the other recovery period differences for other common side hustle usage.

| Item | Asset class | Recovery period (GDS) | Recovery period (ADS) |

|---|---|---|---|

| Laptop & peripherals | 00.12, Information Systems | 5 | 5 |

| Printer | 00.13, Data Handling Equipment | 5 | 6 |

| Desk | 00.11, Office Furniture | 7 | 10 |

| Camera, lens, flash | Personal Property With No Class Life | 7 | 12 |

Digital Nomads and Travelers

Now that we’ve seen the ADS subsystem at work, there is another major gotcha.

The GDS subsystem which allows Section 179 expensing, Super D, and accelerated depreciation is only allowed for items used in the United States. Any items predominantly used outside the United States (defined as more than 50% of days in tax year) must use ADS, unless you are drilling for oil in the Arctic or another obscure exception. (Isn’t lobbying great?)

So if you are in the US and buy a $1,000 camera for business use, you can immediately write off 100%. If you are like me, you can write off $41.70. (Super lame! Seriously, we need a Digital Nomad lobby group.)

Year End Shopping

The default for personal items is a Half Year Convention (only 1/2 year of depreciation is allowed in first year.)

But if at least 40% of total depreciable property is placed in service in Q4, then the first year deduction is reduced. In other words, if you buy a lot of stuff at the end of the year the normal MACRS write-offs will be smaller. And this applies to ALL property of the same recovery period.

A 5-year property like a laptop with 200DB/HY depreciation would get a 20% depreciation allowance, but under 200DB/Q4MQ the allowance is only 5%.

Section 179 deductions and Special Depreciation are still fully allowed.

Strategies

Now that we have a handle on depreciation, how can we use these tools for maximum goodness?

Besides being able to turn stuff we already own and business things we were going to buy anyway into tax deductions, depreciation allows us to time shift our income.

Because some of these ideas represent buying and selling of assets, I should caution not to let the tax tail wag the dog. Don’t buy or sell something just because of the tax benefits. But be aware of the benefits if you are going to buy or sell an asset because that is what makes business sense.

Time Shift Income

Because we can choose depreciation methods under GDS, we have some control over the timing and amount of depreciation in any given year.

Maybe we expect next year’s income to be significantly higher. In which case, we can:

- Choose a slower depreciation schedule (e.g. Straight Line)

- Buy assets on Jan 1 next year and expense (Section 179)

- Sell assets that have a Fair Market Value above book value this year (gain is ordinary income)

If income next year is expected to be lower, we can:

- Choose a faster depreciation schedule (e.g. Declining Balance)

- Expense assets (Section 179)

- Take bonus depreciation (Special D)

- Sell assets with a Fair Market Value below book value this year (ordinary loss)

At a minimum, this time shift in income can be thought of as a 0% interest loan from Uncle Sam. Best case, we can reduce our average effective tax rate.

Special Depreciation

Special Depreciation has an amazing feature.

You can deduct any amount of bonus depreciation, and if the deduction creates a net operating loss (NOL), you can carry that amount back to offset previous year’s income and also carry any unused loss forward to deduct against future income.

This can be especially powerful for financially independent types who are transitioning from a high income career to a lower income side hustle. Why not carryback a NOL to an earlier tax return with a high marginal rate?

Section 179 Deductions

With Section 179 deductions, the total deduction may not exceed the net taxable income from all businesses you actively conduct.

Examples include your blog and your day job. (Don’t have a blog? Start one!) Yes, wages from a job are consider a “business you actively conduct” for the purpose of figuring your taxable income limitation. This makes Section 179 deductions a good tool to use while still working but side hustle income is low.

Converting to Personal Use

We saw in a camera example above that converting an asset to personal use requires immediate recapture. Because this can generate ordinary income, it can make sense to align this with a low income year.

Even after a business item becomes a personal item, it still retains book value in the business. When you eventually dispose (sell, recycle) that item, that generates a potential loss for the business. Be sure to document and claim that loss (perhaps at a time of high business income… But note, if you sell to a relative, you lose the ability to claim the loss.)

Other Tax Optimization

All tax optimization tools work together. For the big picture, see our plan to Never Pay Taxes Again and how we realize this via our actual 2015 tax return.

Summary

Bloggers, side hustlers, digital nomads, and business owners have the ability to deduct the cost of their tools of the trade from their taxable income.

The numerous rules and options provide the ability to time shift income and expenses. Worst case, we get a 0% interest loan from Uncle Sam. Best case, we get a reduced effective tax rate.

Overall, through depreciation we can take stuff we already own or were going to buy anyway and turn them into tax deductions for our business. Write it off! Write it all off!

NOTE: I’m just a random guy on the Internet who has no idea what he is doing. Tax laws change periodically, and you should consult with a tax professional for the most up-to-date advice. The information contained in this article is not intended as tax advice, is not a substitute for tax advice, and could just be wrong :).

Been thinking of Starting a Blog? Our step-by-step guide will have you up and running in 30 minutes for less than the price of a monthly latte.

It is nearly midnight where I am. I was sleepy, about ready for bed, and then I stumbled upon this gem. I’m wide awake now, super stoked and the lack of sleep is going to make me _such_ a grump at office tomorrow. Well worth it though. What a fun post! I’m especially excited because you highlighted the fact that I can use depreciation even if I have a day job.

I think for most people, this one will have the opposite effect. Insomnia cure! Zzzzz

Thanks for putting all of these together in one place! That said, I feel more than a little nauseous thinking about actually claiming any of this stuff… but then we’re still working, and so are in that special and fun “super high audit risk” category. (It doesn’t help that I witnessed two audits up close as a kid, and saw the IRS essentially tell my parents, “You’d win if you went to court, but that will cost you a fortune, so it’s cheaper to just pay this penalty we’re imposing, even if it’s not above board.” Definitely scarred by that.) But I’ll refer back to this after we ditch the high incomes and can treat our taxes as something other than an exercise in abject terror. ;-) xo

Wow, that doesn’t sound pleasant.

Unfortunately, now you are paying the fear tax… not taking deductions that you are fully and legally entitled to. Even paying a penalty later may cost less than the lost savings and growth.

I’m studying tax this semester and my professor just said that the chances of being audited are ridiculously low, like less than 0.5% and the trend has been consistently downward. Why? Lack of funding. Not exactly what I could call super high risk.

Interesting stuff. There was a bunch of things in the post I was not previously aware of, so I’d give it a big educational thumbs up.

I’m curious how much the likelihood of an audit increases when you start using different depreciation strategies like this.

You’ve been really focused on tax-saving strategies these last few posts GCC. Your blog must be “rolling in it” these days if saving on taxes is that important!

You are probably aware, I’ve always written about taxes.

About 1% of total returns are audited. About 70% of those are correspondence audits (done by mail.)

I like this quote from an article on Forbes:

“…statistically speaking, you have a better chance of being abducted by aliens or dating Taylor Swift than being audited.”

Things are getting serious! Thanks for all the insight on the business end of the tax code, things certainly start getting more interesting here. A little more complicated but deducting those expensive purchases like laptops and cameras is pretty significant.

Just to clarify, if you do not have enough business income, you can use section 179 losses against regular job income?

This one is a little deep… but working through it definitely helped me figure out my own depreciation plans. Maybe it will help others too.

Yes, you can use section 179 losses against regular income. From Pub 946:

The total cost you can deduct each year is limited to the taxable income from the active conduct of any trade or business during the year.

Net income or loss from a trade or business includes the following items.

– Section 1231 gains (or losses).

– Interest from working capital of your trade or business.

– Wages, salaries, tips, or other pay earned as an employee.

You can also carry forward any unused Section 179 deduction, but with $500k annual limits that probably isn’t too useful.

Let me know when you want to sell that computer!

I was thinking of getting a new laptop this year, but because of the stupid “predominantly outside the US” clause I’m going to wait.

Instead I bought a $6 tax-deductible mouse to replace the broken track pad, so I’m good for another few months at least.

This is a GEM! It will require a few “read-overs” (the way I learn) – but well worth it! I was pretty confused by the different kinds of depreciation and your examples have cleared that up. As Ms. ONL said above – the audit risk scares me and we are totally paying a “fear tax”. Your link and comment to Mr. Tako (along with all of your amazing posts on taxes) are moving me to take action and consider taking more deductions. This is the first year (other than having our rentals) – where I have business income from educational consulting. I was going to stick to the basics (mileage, etc.) but there is a lot more to it! As always – thanks for the education and the push and Happy Thanksgiving to you, Winnie & Julian!

Thanks Vicki. This required a few “write-overs” for me. I had to correct several of my misunderstandings and false assumptions.

Other than the hassle factor, there is no reason to be afraid of an audit. Al Capone had reasons to fear one, but you are just following the rule and letter of the law. My opinion, anyway.

I learned in law school* to be very aggressive on deductions and credits. In the event of an audit, you’ll probably pay 20% underpayment penalty plus some minimal interest, and you might not even owe anything or get a refund (if you messed up something else uncovered by the audit).

The odds of you facing a more severe penalty for fraud and/or facing any real jail time is near-zero as long as you try hard to get it right and have some basis to back up your filing. If you’re off by a $100 or $200 because of some small error you aren’t going to federal prison, you’re just going to owe the tax plus 20% + 5-20% interest.

* standard “this is the internet and I know nothing” disclosure: not currently an attorney and certainly not the attorney of anyone reading this on the internet. :)

Many, many years ago, when I still owned rentals, I had a tax accountant who prepared my returns. His philosophy: “If you are not being audited, you are not taking enough deductions.”

Indeed, every year he did my taxes I was audited. Most times I had to pay a bit more, but overall far less than if we’d been less aggressive.

I was amazed at what the IRS was willing to accept even when they had us under the microscope.

Once the rentals were gone and I went back to doing my own taxes, I was never (knock wood) audited again.

I think I would get along well with your accountant.

That’s how you do it right there! I’ve found the IRS to be nothing but reasonable the couple of times I’ve been “audited” which were really clerical errors on 1099s prepared by other people (but led to the IRS flagging my returns since it looked like I underreported income by many tens of thousands). Oddly enough both times I was audited it was a missed decimal place on the 1099s that made $600 in income look like $60,000. Easy to resolve by phone call (once) and a quick letter (once).

Exactly!

If you are committing fraud, yeah the IRS is something to be feared. And, as you are shifting your burden to me, I hope they get you.

(not you personally RofG, but the collective you) :)

But if you are aggressively seeking every deduction you are untitled to, while you may have some quibbles to resolve, the IRS is not there to punish you.

Gonna have to bookmark this one for February or March when it’s time to file. :) I’m looking to acquire a new phone and ultrabook for my business and might as well have Uncle pay for a third or a half (ACA subsidies make my effective marginal rate pretty high).

Just be sure to place the phone and ultrabook in service before the end of the year.

Big 10-4 on that one. Hoping to make some Black Friday purchases if I can catch a good deal (and silly me, booking a cruise that’ll have me internet-less on Cyber Monday… not thinking like a good consumer).

Just consume extra at the seafood buffet.

That’s a given.

I woudln’t be capitalizing anything less than $2,500 under the de minimis safe harbor election.

Tim, I think you just made my day.

I was under the impression that the limit was $500, but Google tells me it was increased to $2,500 as of 1/1/16. This election may be the solution to the “predominantly outside the US” exclusion I was facing.

There are still reasons to capitalize assets for time shift reasons. Maybe you are currently at the 0% or 10% marginal rate, but expect to be at the 25% rate in years to come.

This all seems pretty complicated. I find it hard to believe just about any blogger or side hustler accurately keeps track of depreciation unless they always do 100% right off the bat.

It seems even more unlikely the IRS would be able to verify any of it.

This may be completely inappropriate, but the message I kind of get from this is that we can deduct anything we want and it is almost guaranteed we can get away with it.

I take back my earlier comment that there is no need to be afraid of an audit ;)

TurboTax takes care of all of this for you, so for the most part there isn’t much tracking to do. When I do 2016 taxes, TurboTax will pull in all of last years depreciation data and crunch the numbers for this year.

If anything, thinking about this would just happen when it is time to buy a new laptop and dispose of the old one. Or if anybody is interested in optimizing further (e.g. me), the knobs are there.

TurboTax to the rescue, as usual. I love that software.

This is great, thanks! Since you’ve read so much of the tax code, hoping I can drop my scenario on you and see if you have any advice. I work full time (salaried) remotely and travel 100% of the year (airbnb, etc mostly domestic US) so I am a “nomad”. I also have my own legitimate side business (web dev). In this situation, besides physical equipment, can I deduct any living/travel expenses for my side business? e.g. I require an office environment with internet + desk so can I deduct an estimated portion from the airbnb rental?

I’m not completely sure, but I think the answer is no.

To deduct travel expenses, the primary purpose of that travel must be business related. If you are nomadic with no home base / tax home, then the IRS considers you to be “Itinerant.” Travel is just part of your life, not a business need, and is therefore not deductible.

But if you happened to be nomadic outside the US, you could potentially avoid US taxes altogether.

Thanks, just wanted to double check. I do spend 3-4 months abroad out of the year and could easily claim Paris, FR as my residence (parents live there, I’m dual citizen, etc.) but I’m not sure if that works out for me since I wouldn’t meet the FEIE requirements…but I would get rid of state taxes (currently in NY).

A risk of claiming residency in Paris is that France may want to tax you.

To eliminate NY tax, you could reestablish residency in a non-tax State (Alaska, Florida, Nevada, South Dakota, Texas, Washington and Wyoming.)

This article was equal parts fascinating and amusing for me. I’m in Canada, so absolutely none of the information contained in it is relevant to my life, but I am an accountant, so reading the explanations and comparing them to the Canadian tax code was fun.

Depreciation for tax purposes is called CCA (Capital Cost Allowance) up here, and I remember it being one of the most tedious and confusing parts of my tax education. However, the U.S. tax rules around depreciation appear to be even more tedious and confusing! All the same components are there, but we don’t get to choose from various methods, the rates and methods are dictated entirely by the class the property falls into. I never thought I’d be heralding the Income Tax Act for simplicity, but there you go.

Great job breaking down the details of this in a user-friendly way, and I love that you included this paragraph:

“Because some of these ideas represent buying and selling of assets, I should caution not to let the tax tail wag the dog. Don’t buy or sell something just because of the tax benefits. But be aware of the benefits if you are going to buy or sell an asset because that is what makes business sense.”

I’m always surprised/confused by people who talk about buying things “for the tax deduction.” Even my spouse, who is self-employed, has asked me if he should buy things for work to reduce his taxable income. My response is always “Do you NEED it? If you do, buy it, who cares about the tax implications. If you don’t, don’t spend $1 to save $0.30.” With the caveat that “who cares about the tax implications” only applies to small supply purchases that will just be expensed, not any capital purchases (he doesn’t really have any).

Tedious and confusing are good adjectives for this topic.

Because US people (sometimes) get tax deductions for mortgage interest, we also hear all the time how people are buying a bigger house for the tax deduction. Hello! A friend told me his accountant suggested that once, and I told him to fire the accountant and trade me $1 for a Quarter.

I love deductions, I run a mobile DJ business and have been depreciating equipment for a long time. One other thing to add is mileage, which I have a lot of. I find super tedious to itemize every little thing like gas and % I use my vehicle for work, so for the past few years I have made it less of a headache and just took the standard deduction for miles, which is down to .56 cents a mile. I use this app called MileIQ, which pretty much does the work for me, then sends me a monthly report of how many miles I drove and what I can conduct. Also, thanks Uncle Sam for that free loan on my laptop, that came in handy.

Cheers!

Nice! Since you are using an app for tax purposes, that is now business use of your smartphone and data plan too.

Congrats on (almost) making depreciation interesting! OK, I kid, I was genuinely interested, especially in the bit about depreciating against total income. I’m considering starting a business when I buy my next “slow flip” house and I’d love to convert all of my tools to “business tools” and write them off.

Happy Thanksgiving to you, Winnie, and Julian! Do they sell whole turkeys in Taiwan?

Almost interesting is one heck of an accomplishment! haha

Costco probably sells turkeys… we are just going to roast a chicken.

Happy Thanksgiving!

Regarding determining what percentage of your computer use is business versus personal, how do you make that determination? Do you keep a log of every minute you use the computer for business use? Similarly, how do you determine what percentage of your cell phone plan should be business use? For auto business use, using mileage as a way to determine % business use is straightforward. But for a personal computer, a camera, etc. not so much. Obviously, if it’s 100% business use that’s easier to deal with.

Thanks for the blog. I really enjoyed the ACA subsidies chart that you did some time ago. It is excellent.

There are no hard and fast rules. Certainly 100% usage is easier, although unless the items is physically located in an office it is hard to justify that truly 100% use is business.

Documentation is key. If you have no documentation, you have no legs to stand on if the IRS challenges a deduction. Even estimates will fare better than nothing.

For a computer, if you work 8 hours/day and surf the web 2 hours every night, then 80% of use is for business. For exactness, you could use a site blocking app that keeps logs (I use SelfControl to help focus.)

For a smartphone, you could take a screen shot of data usage by app every month. If 80% of data is for Facebook, then you have 20% business use.

For camera, when you import photos, you could segment them into personal and business folders / tags. If 90% of photos are of your kid and what you ate for dinner, then only 10% is business use.

Doing tax by ourselves is a great starting point to take advantage of the tax system. There is so much room for optimization!

BSR

This was a great article. I’ve owned a business for almost 10 years. After 3 or 4 years I switched accountants. The best advice he gave me was don’t spend money to save on taxes. I would take out a loan to pay for equipment then “save” 30 cents on every dollar I spent. That being said I happily take all the deductions on things I have to purchase.

I just assumed the best tax advantage you would receive would be for travel. Not to get into too much of a grey zone but is that considered 100% business expense? What about the rest of the family? We do a percentage when we travel but yours seems more legitimate. I’ve been trying to come up with side hustles that could be used as travel expenses. My ideas have been a little costly but we are going to SMA to try again. (I wanted to do furniture import but the shipping was crazy so we may look at drop shipping of small items)

On a side note my accountant told me you could save up expenses if you weren’t ready to start the business now, then claim them in the first year you opened. Not sure if there is a time limit.

Thanks again for the blog and great info!!!!

One thing to add. You can deduct expenses you incur to generate your income up to the amount of your income. If you have more expenses than income, then you need to be sure you have a business and not just a hobby. I agree that in general you have a low chance of being audited, but the more deductions you through out there the higher your chances.

How much greater chance of an audit? Should we pay the fear tax instead?

We always declared the office space in our house but thanks for reminding me of depreciation! This is a great way to minimize our tax burden.

I’m curious if you do your own taxes, ever outsourced until you felt competent, or always used one.

I’m curious about the above comment designating the difference between hobby and business, and when you can start taking advantage of business expenses. I’ve made zero so far, so is it a hobby even if I have business intentions?

If your intent is to make money, it is a business. Starting day 1.

I do my own taxes.

A few questions here are close to my question, but I don’t think any of them specifically hit the nail on the head. To be clear about deductions with side hustles:

Let’s say I have a regular 9-5 that pats $50k per year, plus a side hustle that pays $1k per year. Are there any issues with having $5k in deductions from the side hustle? No, right? Theoretically the IRS only has a fundamental problem if I try to claim more than $51k in deductions, right? (Although I’m sure some red flags would also come up if I tried to claim like $49k in deductions, but at least that’s technically legal, right?) Thanks for the informative article!

It’s been awhile since I wrote this so my memory is fuzzy.

Any investment to build a legitimate business is a write off, but whether your income for the year is -$1 or -$1,000,000 you still have the same tax bill. You can carry forward the losses though – so you write off $51k in year 1 and then carry forward.