The personal finance blogosphere is full of incredible success stories:

How we paid off $1,234,567 in student loans in 3 years

How my (all consuming) side hustle helped us become debt free

How we saved multi-millions by ruthlessly slashing our expenditures on housing, transportation, and food

Inspired by these fabulous accomplishments, I feel fortunate to share our most recent financial milestone:

Despite traveling and spending a ton, over the past ~4 years our net worth has grown by an additional $1+ million.

One Simple Trick

Most of personal finance boils down to one simple principle – spend less than you earn and invest the difference.

Also known as One Simple Trick. Earn More, Spend Less, or Both.

Pay off $1 million in student loans in 3 years…. by earning $1 million more than you spend – Easy!

Pay off all debt… by earning more with a 60 hour per week side hustle – Anyone can do it!

Save more by spending (much) less on core cost of living – Yeah, but I need a car, and a house, and I like caviar and champagne…

Even our own hack of paying off high interest student loans with 0% interest credit card balance transfers wouldn’t have been possible if we weren’t spending less than we earned.

All of these stories are great examples of good choices to turn a negative situation positive.

Debt & Net Worth

Unless you are the lender, debt is an insidious and pernicious destroyer of wealth. The interest burden can turn a leisurely swim into a struggle to move upstream against the vast power of Niagara Falls. Oddly, most adults have a lower net worth than the day they were born…

That’s why all of these success stories start with overcoming debt… student loans, a poor financial choice from yesteryear, an unfortunate burden from a medical mishap…

Before you can get ahead, you first have to get to zero.

Before you can get to zero, you have to trade your time to earn money for someone else.

Beyond Zero

Hitting zero is a great milestone: We are debt free, yeah!

Now we get to trade time to earn money for ourselves.

It’s good fun to see an extra $500 sitting in the checking account at the end of the month, or to build up an emergency fund that would cover a month or two of expenses.

Sadly, this is the most financially secure most people will ever be… who can resist that great deal on a new car loan, or a kitchen upgrade courtesy of the Home Depot charge card, or moving on up to that bigger home in the nice neighborhood with the great school district (and longer commute for the new car.)

But mortgage rates are so low, who can afford not to buy a new home? Back to zero and below.

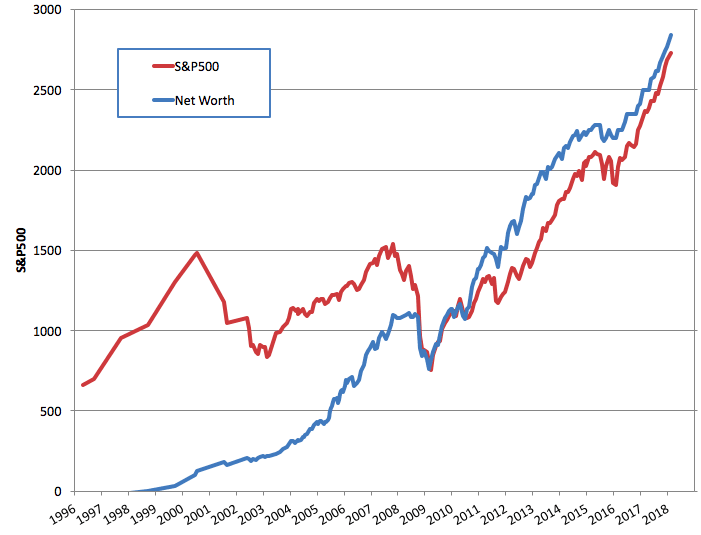

How to Grow Your Net Worth by $1+ Million in Less Than 4 Years

Now is when the magic starts to happen: your money starts to make money, which begets more money, until our time is no longer necessary.

Things get really exciting once your checking account pays you $0.06. I still shed a small tear thinking about that incredible milestone. But then that $0.06 becomes $20, and then $100, and then $1,000.

And then even though you haven’t worked for more than 4 years while spending a few hundred thousand dollars traveling through 28+ countries, you suddenly have $1 million more than when you started.

Amazing!

I even updated our net worth chart to commemorate the milestone (older version here.)

So there you have it…

All you need to do to grow your net worth by $1+ million in less than 4 years is stop working and travel the world.

Obviously.

Good luck!

Oh, I suppose it also helps if you first save more than half of your income for over 10 years, invest primarily in equities during a bull market, make a little income on the side, and continue to spend less than you earn.

Sorry, that’s all I have for sarcasm and dry humour for the day.

What is Your “One Simple Trick” to Grow Net Worth?

“Obviously.” Funny post Gcc!

It sounds ludicrous, but it’s also very true. Our family has only been at it two years and our net worth has already grown by over half a million dollars!

We have the bull market to thank for much of this, but the principles behind our massive wealth growth are sound.

I have developed an investment portfolio that allows for huge gains (over 31%) with little downside.

It has been working fantastically for me since I started implementing it in 1997. I had huge profits in 2008-09.

Life, as they say, is sweet!

Sweet! On your way to 10 figures?

Our next worth quadrupled in four years to get over $1m this past year. It also really helps when you have a bull market pushing your sails and all you have to do is dump as much money into the stock market as possible :)

Nice. Congrats!

The bull market is helpful…very helpful, but the financial discipline to take advantage of it is not very common.

Bingo!

Haha- I can’t say I have anything to contest here. I will add/emphasize that once we hit our “debt free” mark (no more student/car/credit card debt), we had to find another goal to keep us motivated. Tracking our net worth really helped us here… it gave us a monthly goal and checkpoint which helped us keep our finances in line and keep our spending lower (“do I really need all this or do I want our Net Worth to be higher this month?”)

tracking spending and net worth is a great trick.

My net worth has tripled in 9 years, but that’s mostly because of the bull market, plain and simple. While I have always been a saver, I can’t take too much credit for my ballooning nest egg. Like AdventureRich, I do track spending and net worth on a monthly basis. I enjoy looking for ways to save money and cut expenses.

We can’t take credit for the ballooning nest egg either. That’s the best part!

It’s very tempting….

However as a FIRE reader I see this strange space-time continuum shift, where people earn more or increase their net worth more AFTER they leave their jobs. Maybe we have to add ‘Leave your corporate job’ to the list of early retirement hacks.

We would still be way ahead financially if we were still working, but we are way ahead in every other measure by not.

A bit of a cheeky post :) …. but a bit of sarcasm is perhaps warranted … and can be a great teaching tool for those at various stages along the way of FI … it is great you posted some of your old links of ‘how to’s …’ … seeing they can be very encouraging to those moving along the spectrum from debt to break even to F.I and to abundance …. you and your friends are living proof that it can be done … congrats on your latest milestone! …. I also like your lifestyle posts which are fun too … we have 11 days off here for Chinese New Year and so Happy Chinese New Year to your whole crew! Michael CPO. 祝狗年吉祥,身体健康,万事如意,幸福长存!

新年快樂!!

Here I thought you were going to go all “CrytoCurrencyBonanza” on us. Thanks for NOT.

PS – Thanks again for the 529 article. I’m glad there’s bloggers like yourself out there to help us consider better alternatives.

Ha! Click here to sign up for my guaranteed crypto wealth machine!

Ha! You know, sarcasm aside, it really is beautifully straight-forward when you lay it out that way–“saved more than half of our income for 10 years,” etc. Because even though saving 50% may seem crazy to some, ten years is an amount of time you can get your head around. Not 30, or 40, or 50 years. Ten years is a decade. One decade of saving, investing, living on less. And then many, many decades of not working and traveling the world. :)

How did you cope losing half your net worth in 2008-09. Interesting to see that you wouldn’t want to prevent this from happening again by reducing your stock holdings. I have doubled my net worth from 1.2 million to 2.4 million since 2012 without new investments but I continue to work and earn 200k per year that gives me the freedom to spend as I wish, although I haven’t traveled the world as you have. I have reduced my stock holdings to 60% of my portfolio as I wouldn’t want my portfolio to go back down to 1.2 million which would be a possibility with 100% stocks.

Obviously what you’re doing is working for you and I am thinking more and more about leaving the work place as I am approaching 50; I am currently 48.

I coped well.

If the stock market crash 50% Monday I will sell my wife and kids to buy more stocks….history repeat itself…you didn’t learn that yet Ron?

Oh, I learned perfectly well, as in 2008-09 I had lots of cash available for investing which I withdrew inside my business. In 2009, I was building my retirement and today it’s fully funded so protecting it is more important for me. As I have most of my cash deployed today, and not wanting to have to take a line of credit the next time to invest, I rather be invested more conservative to protect my capital and if the market crash, re-balance my stock to bonds ratio. If your 100% invested in stocks, the only way you can take advantage of a crash you have to borrow as we both know that your humour of selling your wife and kids won’t do much for you. I prefer to protect my capital and not have to borrow and I respect others that are fully invested, to each their own.

“Financial advisers hate him!”

You can add my testimonial. Quit work, been traveling, net worth climbing faster than ever :)

I want to make a T-shirt with this in block letters on the front

I love it! So easy a child could do it, or at least understand how simple the concept is. Haha. For people drowning in debt I’m sure the light at the end of the tunnel doesn’t seem so bright, but for us, after maxing retirement accounts and paying down debt for a few years now, it really is that simple (not easy, but simple!). Now if only I could figure out when the next bull market in stocks could be?

That’s insane! The chart is great. Now, let’s see if you can do it again over the next 4 years. I think it’s going to be much tougher. Financial advisers hate us because they can’t make any money from us. I’m getting more conservative as I get older. We have 20% in bond now.

In theory it should be easier… I hear the 1st million is the hardest

“Mind The Gap” we all have a gap between in calories/dollars and out exercise/spending. Make that gap positive and keep it that way forever. This differs from an ultra-marathon in that marathons have finish-lines. This may means slowing down to extract more enjoyment from the run.

It’s that calories in vs calories out thing that I struggle with :)

Living below your means is the only way to do it. I love the below accounting exercise to confirm:

Savings_t = Income_t – taxes_t – spending_t + interest earned_t – interest paid_t

Net Worth_t = Net Worth_t-1 + Savings_t + (realized & unrealized) Capital Gains_t

Subbing first into second equations:

Net Worth_t = Net Worth_t-1 + Income_t – taxes_t – spending_t + interest earned_t – interest paid_t + Capital Gains_t

The only way you anyone will ever get richer is by living below their means. This is just as true for those making minimum wage as NFL players making millions. The above math never lies.

I love the above formulation because it specifically shows how taxes are a drag on wealth accumulation. If you want to get fancy, you can do a bunch of substitutions and arrive at the following equation for wealth T years from today:

Net Worth_t+T = Net Worth_t-1 + Income Earned over Next T Years – Taxes Paid over T Years – Spending over Next T Years + Interest Earned over Next T years – Interest Paid over Next T years + Capital Gains Earned over Next T Years

The above equation is why I think everyone should be as diligent at optimizing the tax code as you and I are. There is an (obvious) inverse relationship between taxes paid and net worth. And if you understand the tax code you can defeat it.

I love the worth chart, you can really see the accumulation phase in action, then “oh damn, the stock market crashed”, before continuing with outpacing the market! It may bean “easy” trick ;), but it also requires patience for years at a time. And patience is not something most people are good at!

Crashes and booms, and all is well.

One small note: we aren’t outpacing the market, we are tracking it ~1:1

And here I was thinking that you were going to teach me some trick with taxes that results in Uncle Sam sending you a check for $250k every year…

How to get the government to send you $250k every year:

Become a member of Congress for one day, resign, collect pension and health care for life

You messed up. Way easier to make $1M+ by inheriting massive wealth. Just need to pick the right parents to be born to! :)

Alas, we are sending $ in the other direction.

The kiddo will get it right this time around, eh?

An even easier way: start with $2M and follow Jim Kramer’s stock picks for a couple years :)

Now that is real money (badum tsss)

DH and I semi-retired about four years ago as well. We have similar gains in net worth (as a percentage.). We live fairly lean as far as total spending (earnings about poverty level, spending about twice that) but lack for nothing. Our life is more small town Midwest/kids in public school and less globe trotting (I did get my first passport stamp last month). Anyway we live different lives but are enjoying a life made possible by saving early and often and then charting our own course.

Wonderfully said. Being able to live as you wish is exactly the point.

“One Simple Trick” to Grow Net Worth? For USA citizens it has been “Uncle Sam sending you a check for $250k every year” by keeping interest rates lower for longer than seems prudent. The ‘wreckage’ has washed up on Australian shores in the form of a massive mining investment boom, high immigration, house prices, bank profits, Amazon share price and Bitcoin price. Like a tidal wave sloshing about the globe.

would you conside leverage stock ETF? say UDOW, UPRO, TQQQ to enrich your return

Consider, yes. Use, no.

Leverage will also enrich your losses. A 33% decline on 3x leverage is a complete loss, game over.

Quick question for anyone that happens to read this comment:

I have $100,000 in student loan debt owed to the Federal Gov’t w/ an interest rate of 5.84%.

Yes, it sucks and if only I could turn back the hands of time.

What is the recommendation in regards to paying this off and investing? Should I do 50/50, pay the minimum and invest my ass off, forego investing and focus strictly on getting this beast paid off?

Thanks!

5.84% * (1 – Your_Marginal_Tax_Rate) = ? Can you find a better guaranteed return?

Thanks, I will look into that!

Should read: 5.84% / (1 – Your_Marginal_Tax_Rate) = ?

Hey Matt

If you have access to a 401k and get a company match, I’d contribute enough to get the full match. A 50% to 100% immediate return on your contribution is great ROI, plus you get a dollar for dollar tax deduction.

At ~6%, I’d contribute any other $ to paying off the loan. As Bullockornis states, you get a tax deduction on the interest, but that is limited to $2,500 per year (subject to income limits) and you are currently paying about $6k. I’d also look at refinancing to reduce that rate.

Thanks for the advice everyone! I will go ahead and knock that sucker out.

I like the intentional “Clickbait” title and general sarcasm. Put that aside and this is an insightful post for those not in the know…

Love it! I’m following your advice. Just put in my notice. Now to travel the world and make millions! ;)

so easy, any one can do it. Enjoy! ;)

Congratulations. For many of us, if we just leave it alone and leave it in the market, it just grows. The power of compounding! That is what is great about achieving FI – you can now let your money work while you enjoy life.

Looking forward to getting there myself! Only 29 Months to go!

Nice. 29 months will go by in a flash!

So simple. It’s like the old adage says, time in the market is more important than timing the market.

Of course if you can retire into a bull market it helps with sequence of returns risk, but that’s a different discussion.

This post reminds me of Steve Martin’s old bit about how to become a millionaire. He said, FIRST…. get a million dollars….

I just want to say I’m new to this financial independence world, but reading your post inspires me everyday to keep on pushing. I appreciate the time you take to really show us in simple steps how we can be living a better life. Keep up the great work !

Congrats and thanks for the timely reminder that it can be done. You, GoCurryCracker, are one of the giants on whose shoulders I stand on.

We started to track our net worth 13 months ago and are up $150k in that time. I reckon, we can be FIRE anywhere between 4 more years (optimistically) or 6 years (realistically).

As to your question: What is Your “One Simple Trick” to Grow Net Worth? Simple answer, track it. As we are doing.

You are much too kind.

4 – 6 years goes by so fast. Enjoy it.

So simple XD.

What would you say to someone who has a lot of cash savings, but is hesitating throwing money into this record breaking bull market?

Also, what system do you use to track your net worth?

Look at a chart of the history of the stock market. It is always breaking records and reaching new highs.

Pick a target asset allocation and buy it. You can go all in or dollar cost average over a year or so, whichever suits your temperament the best.

I mostly track net worth in Personal Capital. You can read my review and see what you think.

One quick question, Why didn’t your portfolio go down as much as the S&P in 2008-2009? Your current net worth would be about 30% lower had you stayed in stocks for the whole crash.

It did.

Well on the graph it doesn’t.. the red line goes down a lot more than the blue line on a percentage basis.

Perhaps you were still earning money at the time?

How might one save more than half their income if they live on a poverty level income and rent consumes half of it?

Become homeless?

Earn more

I’m currently an undergrad student, and will graduate this May with $14k in student debt. I have been putting all of my income into a roth ira while I still can, before I have to it towards my debt.

I was wondering though, is putting my money (over $6k) into a roth ira smarter than putting all of that towards my debt right now? My loans have low interst rates that vary from 3-4%, and I am already invested in Vanguard’s VTSMX index fund.

Either way, I am motivated to paying off that $14k as soon as possible, but I’ve still got a lot of learning to do, and could use help weighing the pros and cons of investing now, or tackling accumulated debt now.

This kind of decision is very situational. Take a look at this article and see if it helps.

Personally, assuming you pay no income tax now and have some job prospects lined up, I’d do Roth now, LBYM until loans are paid off, and then continue LBYM until FI. See here.