Balance (photo credit)

Optimizing Obamacare vs Minimizing Taxes presents a classic trade-off.

On the one hand, it would be nice to maximize Obamacare subsidies. Easy! Simply don’t generate a lot of income.

On the other hand, we want to minimize taxes. We do this by offsetting income with standard deductions and personal exemptions, and generating (a large amount of) income that has preferential tax treatment.

But for the ACA, there is no preferential tax treatment. There is no standard deduction, no personal exemptions.

In this post, I explore how to navigate this complex environment in order to optimize health insurance premiums, out of pocket medical expenses, and taxes. Can we find the balance?

Tax Minimization

As part of my quest to Never Pay Taxes Again, I’ve read a lot of tax documentation. What can I say, everyone needs a hobby.

The process is simple. We convert our tax-deferred 401ks and IRAs to Roth IRAs at zero or low marginal tax rates, invest in index funds that pay Qualified Dividends, and Harvest Capital Gains to increase our basis. Doing this, it is possible for a Married Couple Filing Jointly in 2015 to have $95,500 in income and pay $0 in tax. (See a real world example for 2014.)

In some cases, it might make sense to pay a little tax now to avoid larger tax bills in the future, a real possibility with Required Minimum Distributions. We might then double the size of our Roth IRA Conversion to occupy all of the 10% marginal rate (or even part of the 15%) and harvest a little less in capital gains. Same $95,500 income, but with a reasonable tax bill of only $2,000 or so and smaller RMDs down the road.

An example is shown below for a Married Couple Filing Jointly / 2-Person Household. For Single, divide by 2. For 3+ Person households, shift tax curves right by $4k/additional dependent

Tax Minimization for Federal Tax Profiles

Now with the Affordable Care Act, the process is no longer so simple

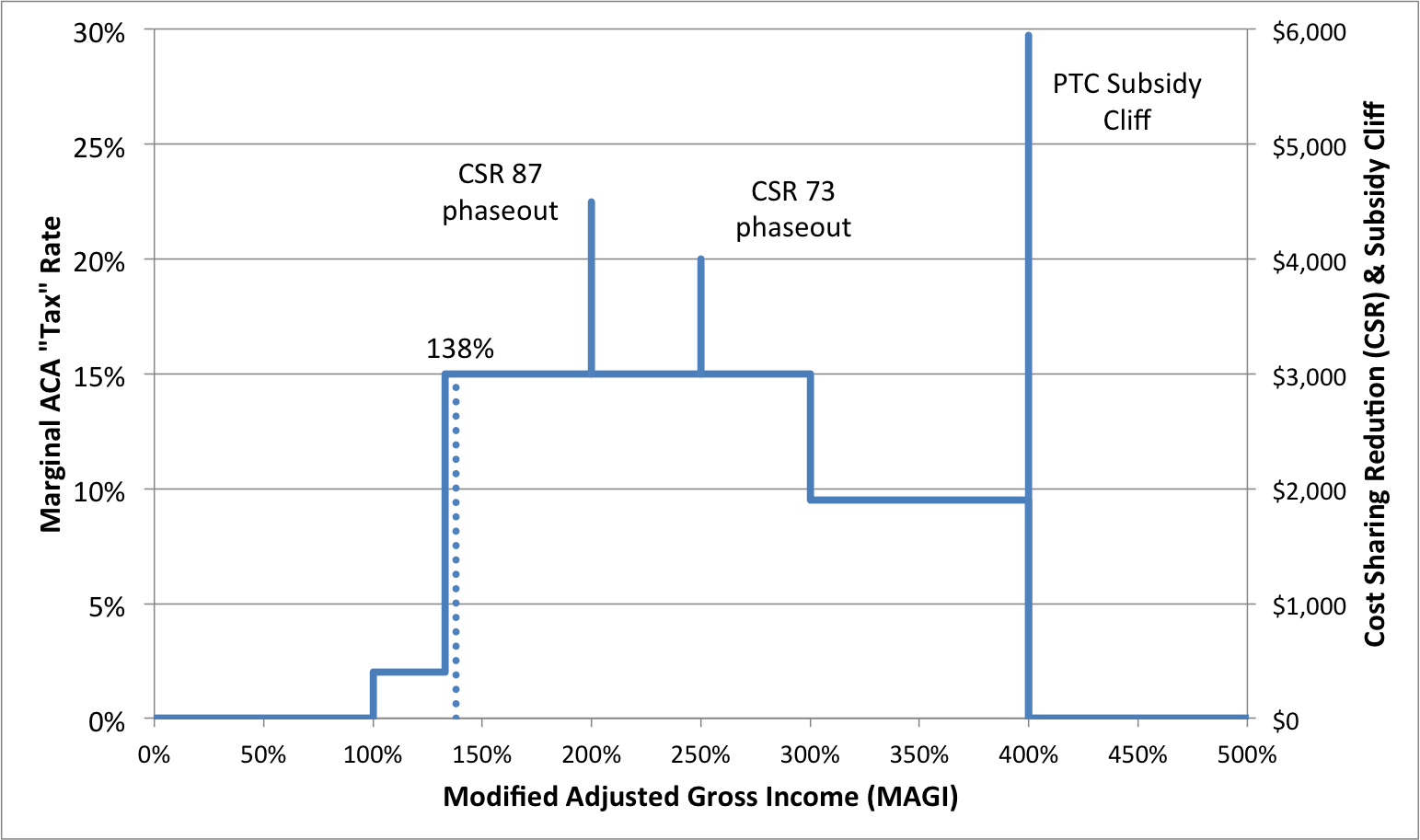

Affordable Care Act as a Tax

Affordable Care Act subsidies decrease as income increases. A marginal loss of a tax credit is equivalent to an increase in the marginal tax rate. Ergo the ACA is a tax.

Unlike the Federal Income Tax, all income sources included in MAGI are taxed against the ACA tax profile, including Roth IRA Conversions, Qualified Dividends, and Long Term Capital Gains.

Affordable Care Act Tax Profile

There are 3 taxes shown in the chart

- Premium Tax Credits are reduced using an inverse marginal taxation profile for MAGI up to 400%. Total tax is bounded; beyond 400% additional income is tax free.

- Out of Pocket Maximums may increase as income increases beyond 200% & 250%. Shown as impulses, CSR 87 & CSR 73

- A subsidy cliff may increase insurance premiums above 400%, particularly in high cost states and for older retirees. Shown as Subsidy Cliff impulse.

If any of this doesn’t make sense, background information is covered in the post Obamacare Optimization in Early Retirement.

These taxes can all be quantified, allowing us to compare against alternatives.

Note: Most states have expanded Medicaid for low income households. For those states, income must exceed 138% FPL to qualify for ACA which eliminates that cute little 2% marginal rate lobe (difference in total tax is minor.)

Federal Poverty Levels change every year. See the latest FPL data here.

Quantifying CSR Subsidies

For silver plans only, at 200% and 250% FPL the Out of Pocket (OOP) Legal Limits increase. (There is also a CSR subsidy reduction at 150% FPL that I’m excluding since it doesn’t impact OOP.)

An insurance company will implement this via higher deductibles, co-pays, and co-insurance. In a year with limited medical use, the value of this subsidy may be zero. But in a year with significant health expenses, the Out of Pocket Maximum can save thousands of dollars. These are legal limits, the actual changes may be lower.

<200% FPL – $2250 single / $4500 family

200% FPL – $5200 single / $10400 family (+$2950/+$5900)

250% FPL – $6600 single /$13200 family (+$1400/+$2800)

Quantifying Subsidy Cliff

The impact of the Subsidy Cliff is relatively easy to determine. The legal limit for cost of premiums is 9.5% of MAGI at 400% FPL. At $400% + $1, the delta to the actual premium can be zero or it can be thousands of dollars. (We previously saw examples of a cliff from -$1k to +$4k.)

Legally, older people can be charged 3x younger people, which means the subsidy cliff will grow substantially with age. As long as we stay below 400% FPL this isn’t a factor at all, the premiums are independent of age.

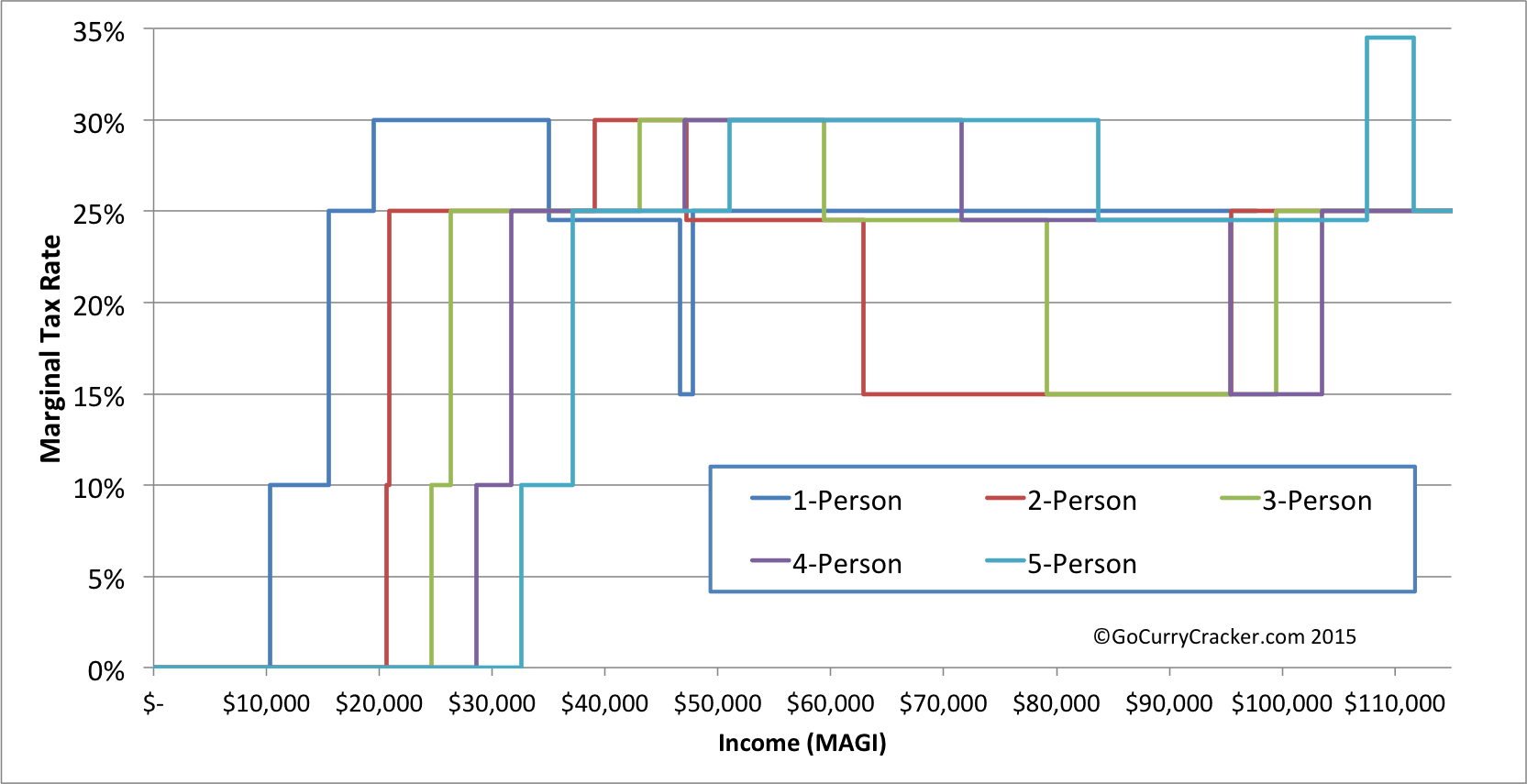

Tax Implications

When we superimpose the ACA Tax profile for a 138% State on the Federal Tax profile, things get interesting.

Combined Federal & ACA Tax Profiles

Pre-ACA, it was inconceivable to see 25%+ tax rates on income of less than ~$100k. Now, households at 138% FPL will. Non-dividend incomes above 250% FPL will see 30% tax rates.

Qualified Dividends and Long Term Capital Gains no longer see a generous 0% tax rate, and will be partially taxed at 9.5% & 15%.

The capital gains we planned to harvest at 0% tax now cause us to blow past the 400% FPL level, losing all subsidies and falling off the subsidy cliff.

This has profound implications. The opportunity space for tax minimization has been reduced significantly (highlighted in chart below.)

Opportunity Space for 10% Roth/0% Dividends and 0% Capital Gains

Further complicating matters, household size is now a major factor in tax minimization due to use of multiples of the FPL. A married couple at 400% FPL is still early in the 15% Federal marginal rate. A family of 5 would have already crossed into the 25% bracket. One Size Does Not Fit All.

Single people and large families have limited or zero opportunity to harvest tax free capital gains, whereas 2 and 3 person households have a large amount. 10% Roth space increases with family size due to personal exemptions, except for single households which have the most.

Single people and large families have limited or zero opportunity to harvest tax free capital gains, whereas 2 and 3 person households have a large amount. 10% Roth space increases with family size due to personal exemptions, except for single households which have the most.

| Household | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| FPL | $11670 | $15730 | $19790 | $23850 | $27910 |

| Size of 0% space ($) | $10300 | $20600 | $24600 | $28600 | $32600 |

| Size of 10% space ($) | $5805 | $1107 | $2710 | $4313 | $5916 |

| Percent of 10% bracket | 56% | 5% | 11% | 15% | 18% |

| 0% CG space | $1070 | $32580 | $20340 | $8100 | $0 |

Tax Minimization with the ACA

To begin, we need to at least qualify for the ACA. In most states, this requires a minimum of 138% FPL. With a combination of qualified dividends and other income, the tax bill could be $0 and insurance would cost only 3.29% of MAGI. I use this as a baseline. (In some states, 100% of FPL is the qualifying minimum. The tax delta to the 138% FPL case is small)

Households below this threshold in most cases will be on Medicaid. Some say Medicaid is the best insurance they ever had, so don’t automatically discount it. But make sure this is intentional.

Any additional income of any kind will increase tax burden. We could minimize today’s taxes / maximize ACA subsidies by keeping income at 138% of FPL, but at the expense of a potential greater future tax bill. If we can find a combination of actions that result in a low average tax rate, then it would be worth pursuing.

10% Roth Conversion / 0% Dividend Tax Space

If non-dividend/capital gain income is less than 138% FPL & total MAGI is less than 400%, we have a choice of how to use the remaining portion of the 10% Federal Tax bracket (shaded region in Opportunity Space chart.) We can either do a Roth Conversion and pay 10% tax, or leave it for tax free qualified dividends/long term capital gains.

This decision should be driven by the RMD. If we expect the RMD to result in a tax rate higher than 10%, we will minimize lifetime taxes by increasing the size of today’s Roth Conversion.

Above 138% FPL, we face an effective tax rate of 25%. If RMDs will cause 28%+ tax rates in the future, it may be worth converting more funds. Otherwise, 138% FPL is a hard stop on Roth conversion size.

0% Capital Gain Tax Space

The inverse marginal tax profile (tax rate decreases as income increases) on dividends/capital gains provides an incentive to harvest gains whenever possible. We can minimize the effective tax rate by averaging the tax over more income (Household Size = 2,3,4.)

Using 138% FPL as a base, if we only have dividend/capital gain up to 400% FPL, we would pay an effective tax rate of 12.9% (area under the ACA tax profile curve.) But if we harvest all the way to the top of the 15% federal tax bracket, we can reduce that to 7.2% for a 2-person household (excluding subsidy cliff.) A $1k subsidy cliff would increase this to 8.6%. This isn’t zero, but it is better than 15%. If we are going to push over the 400% FPL level, we should push all the way as long as the subsidy cliff is not too punitive.

Example Effective Qualified Dividend/Long Term Capital Gain Tax Rates

Some households will earn at a higher income level by default, so effective tax rates are shown for various base MAGI levels from 138% to 300%. (e.g. If a household earns 300% FPL as a minimum, that is the base upon which marginal changes take effect.)

Additional subsidy loss via CSR phaseout or the Subsidy Cliff will increase the effective tax rate. This is shown as a percentage on a per $1000 basis, e.g. if a 1 person household with a 250% FPL base loses $1,000 in subsidies due to harvesting capital gains, this will increase the effective tax rate by 5.4%, from 10.7% to 16.1%. In these circumstances, harvesting gains may not be worth it.

This table shows the effective tax rate for harvesting gains from various tax bases up to the top of the 15% marginal rate. The impact from subsidy reductions are shown in parenthesis per $1k.

| Household → ACA tax base (↓) | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| 138% (+$1k) | 12.5% (3.2%) | 7.2% (1.4%) | 9.3% (1.4%) | 11.4% (1.4%) | 13.7% (1.4%) |

| 200% (+$1k) | 11.7% (4.1%) | 6.0% (1.6%) | 8.1% (1.7%) | 11.3% (1.5%) | 13.6% (1.5%) |

| 250% (+$1k) | 10.7% (5.4%) | 4.8% (1.8%) | 6.7% (2.0%) | 9.2% (2.3%) | 12.6% (2.7%) |

| 300% (+$1k) | 8.7% (7.8%) | 3.1% (2.1%) | 4.7% (2.5%) | 7.1% (3.1%) | 11.2% (4.2%) |

| 400% Cliff Only/$1k | 93.5% | 3.1% | 4.9% | 12.3% | NA |

If We Were In the US

Accumulation

Knowing that we would face 25%+ subsidy reductions for Roth IRA conversions, I would no longer focus on a Traditional 401k and IRA to accumulate retirement savings. Instead, I would accumulate savings in a combination of Roth/Traditional/Taxable. I know making this statement will make several people very happy :)

While young and healthy, I would choose a health plan with an HSA for additional tax deferred savings.

Traditional accounts alone result in paying more taxes in retirement than while working, as an income in the 95th percentile is required to pay tax at a rate greater than 25%. And if income is greater than 400% FPL, we don’t even get an increased ACA subsidy for the contribution.

Roth accounts alone may not enable us to generate 138% FPL annually, since Roth withdrawals don’t contribute to MAGI.

Even at the 25% marginal rate while working, maxing out a Roth 401k is more appealing than paying 25% tax post retirement due to an interesting phenomenon that exists with Roths at higher tax rates. If we contribute the max to a Roth at the 25% marginal rate, we have an effective ~7% increase in after-tax purchasing power over contributing the same amount to a Traditional and investing tax savings in a brokerage account. (Harry Sit the Finance Buff explains this well. The Boglehead’s wiki also has a good overview.)

Ideally though, we would contribute to Roth accounts early in a career when income was lower, and then to Traditional accounts as income rose to higher levels.

Post Retirement

We would establish legal residence in a state with no income tax. I would do Roth IRA conversions each year to fill up the 0% tax space. Roth conversions and dividend income from the brokerage accounts would insure we were above the 138% FPL threshold.

Since total annual spending is higher, we could draw down savings that don’t contribute to MAGI, including cash, basis in stock held in a brokerage account, and Roth IRA withdrawals (Contributions only before Age 59.5.)

While young, when the subsidy cliff is not a problem I would wait until the last trading day of the year. On this day, I could harvest capital gains up to the top of the 15% tax bracket in years where it made sense, and then be sure not to do anything stupid that might require medical care until midnight on Dec 31st. In years that required a large amount of medical care, we would do no capital gain harvesting for the maximum CSR subsidies.

In this way, I could still convert all of our traditional accounts to Roths at a 0% tax rate. And we could harvest capital gains at an effective tax rate of less than 7% (with an effective negative subsidy cliff.) Over all income, it would be ~5% effective tax rate. On occasion, we could follow the same practice but while spending a year abroad, with an even lower effective tax rate.

A perpetual 7% annual tax on gains wouldn’t be ideal, so this wouldn’t be something I would do every year.

As we age, eventually the Traditional accounts will go to zero due to the Roth IRA conversions, probably before we ever see an RMD. If this appeared to be the case, we could reduce the size of Roth conversions and give a little more tax space to tax free dividends.

When the Traditional accounts were depleted, we could then harvest gains at 0% up to the 138% FPL level.

As the subsidy cliff increased in size with age, I would put a halt to any large scale gain harvesting. Or at least until we reach Medicare age and the ACA no longer applies. By the time we reached Age 70.5, we would likely be 100% tax free.

Alternatives

- Ignore all of this. We need insurance, we pay full price for it. Or do a minimal amount of Obamacare Optimization to avoid the subsidy cliff

Worst case, we pay full price for health insurance. Perhaps it is the patriotic thing to do. The full loss of subsidy is just the area under the ACA tax curve, plus any impact from the loss of CSR subsidies and the subsidy cliff. We could just include this into our target annual expenses.

| Household | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Max subsidy from 138% FPL | $3944 | $5317 | $6689 | $8061 | $9040 |

- Pay the penalty

We could choose to self-insure and pay the individual mandate penalty. In practice, for most people this would look like a 2.5% tax rate. With healthcare prices in the US, this may be like playing Russian Roulette. Some are less risk averse.

In 2016, the penalty is the higher of:

– $695/adult ($387.50/child) (max of $2,085/family)- 2.5% of MAGI above filing threshold (standard deduction + personal exemptions)

Absolute max is national avg price for a Bronze plan. For 2014, this is $2,448 per individual but $12,240 for a family with five or more members.

- Be Exempt from the ACA

The list of exemptions from the ACA is limited, and includes fun things like being incarcerated (always a frugal living option.)

PT Money has written up an example of exemption by being a member of a health care sharing ministry. It is an interesting read about an alternative to traditional health insurance.

- Live abroad, even if just for a year

If we were in the US, we would have ACA health insurance. Probably. Maybe.

But because we are outside the US for more than 330 days per year, we are exempt. Certainly living abroad isn’t for everyone. A lot of people have very good reasons to stay in the United States, and many more don’t have good reasons but are going to stay anyway.

As a family of 3, we are able to do large Roth IRA conversions and harvest large amounts of capital gains every year, saving us ~$7k in ACA tax. Subtracting the cost of international health care from that, it is enough to pay for several months of living in many countries. If/when we return to the US, we are in a stronger financial position to optimize the ACA.

Final Thoughts

The interaction between the Federal Income Tax and the ACA is one of the most complex things I’ve modeled in a long time, even more so than many engineering problems I’ve worked through. I’m sure I’ve only just scratched the surface, and my thinking will evolve as I learn more. I’ve probably even made some assumptions that won’t hold up over time.

The ACA is still new and politically unstable. The next few decades are likely to bring massive change to US healthcare, so it would be prudent to take the long view. By this I mean taking steps solely for the purpose of optimizing Obamacare or minimizing taxes is probably going to lead to disappointment. We can instead find a reasonable balance in the current environment and be prepared for change, hopefully for the better.

In many ways, I feel our current solution of a life of perpetual travel is the ideal balance. It is certainly an easier problem set. Maybe you’ll join us, even if just for a year or two.

In any case, I hope this can be the start of an interesting discussion.

Nice post! I came to a similar conclusion in my analysis and we will be aiming for the MAGI of 100-150% of FPL to get the best ACA subsidies.

For example, if we want to live on $40,000 for next year, our income for next year will look like:

$20,600 – Conversion of Traditional IRA to Roth IRA (must wait 5 years for this money)

$10,860 – Capital gains from our Taxable Investment Account

$29,140 – Distributions from our Roth IRA (don’t count towards MAGI).

Since we’re a family of two, this gives us a MAGI of $31,460, which is slightly under the 150% of FPL limit.

One thing is for sure: the ACA definitely makes tax optimization more complex!

Indeed, the ACA is a bit of a mess in this regard

Nice way to pull funds from the multiple accounts. If you have the option, I would probably take some funds from the brokerage account as well and let the Roth grow with minimum withdrawals for as long as possible.

Wow, it seems that this is just as complex as the rest of our tax laws. Thanks for a detailed explanation of the tax impacts of this.

We’re aiming to stay somewhere around 138-199% of FPL in order to get the awesome Gold Plated Silver plans with the steep cost sharing subsidies. It’ll also mean we pay relatively little for health insurance and have enough room to convert Roth to Traditional to set up our ladder long term and remove assets subject to RMD.

For my planning, I place less importance on the possibility of taxes under an RMD than I do on keeping taxes low (and subsidies high) today. A bird in the hand is worth approximately 1.87 birds in the bushes and all that. RMD’s are still 32+ years away for us, and what they look like layered on top of SS and SS taxation may be totally different than the tax laws of today.

On a different note, the complexity of the analysis in this article suggests we, as the American people, need a simpler tax/subsidy regime to provide “affordable healthcare to all”. I’d suggest ditching the subsidies, giving near-free health insurance (or alternatively, move to a single payer system) to everyone plus the cost sharing subsidies for the lower income brackets, bumping up the marginal tax rates (wouldn’t take much) to cover the insurance.

Then ditch the exemption making employer provided health insurance a tax-free benefit (this alone would generate a big proportion of the amount needed to provide near-free insurance to all). Open up the Health Exchanges to anyone, including employees who get health insurance from their employer.

A single set of tax brackets would be so much easier to implement and understand than our current double, triple, or quadruple layer of tax curves and brackets with the various phase outs, cliffs, etc.

3 different definitions of MAGI. Different tax structure for earned income, dividends and capital gains, social security. Different subsidy structures for FAFSA and ACA and EITC. It makes you wonder just how much $ is lost in the layers before anybody benefits. Not to mention the time spent trying to figure it out that could be applied to something useful. I’d say it is all kinds of fucked up. I don’t expect any improvement

Hi GCC,

Thanks for writing those past two exhaustive posts on ACC. I am lucky to have employer coverage, since I am still in the process of learning about the tax ramification of the Affordable Care Act on income from dividends, capital gains, IRA/401K conversion to Roth, 1099 income etc.

I may end up reading this post a few times ;-)

Or I may just decide to live abroad in retirement like you.

Life is great outside the US. To be fair, it is great inside the US too, but you can let the tax savings help pay for a really long vacation

Whew! This was a mind-bending read for me. I struggled to keep up with all the acronyms, concepts and what-ifs. And I’m right in the middle of this. This will be my first tax year with no W-2 income while on ACA with PTC (too damn many acronyms!). Because my health costs are under $2K a year, I chose a Bronze plan with HSA. I couldn’t do Roth conversion last year because I still had a bit of W-2 income. This year I am hoping that I can simply replace the W-2 income with Roth conversion (roughly speaking). But I don’t think I’m going to really make a dent in my traditional accounts using Roth conversions, so I’m considering not bothering with conversions as all. (Maybe I’d make a good twisted case study!) I’ll have to read this again in December.

I think most people won’t read this post all the way through. I wouldn’t :) But I was thinking through the problem for ourselves, and I figured maybe somebody else would benefit from it

It isn’t necessary to make a large dent in the Traditional accounts to have a large impact. Even $10k today would become $100k in 10 years at 7% growth, and at the top of the RMD we can see taxes as high as 39.6%.

Isn’t $10k going to be $20k in 10 years at 7%?

Indeed it is. Math is hard sometimes. Thanks for the correction.

The point to consider is that even small amounts of Roth conversions today, done at 0% or 10%, is better than larger withdrawals later at a marginal rate of up to 39.6% as RMDs require increasingly large withdrawals.

Using us as an example, we will have 35 years of growth before our first RMD. Every little bit of Roth conversion helps.

This made my head hurt. I’m very glad to see you writing these tax optimization posts, however; you’ve made me think about how to optimize my own situation.

I am currently covered under FEHB (gov’t employee) and will be able to keep this in retirement, along with the gov’t continuing to pay part of my premiums. As long as we’re healthy and keep a HDHP with HSA, this is amazingly cheap, even compared to subsidized ACA plans.

At some point though, if we’re retired with fairly low income needs and increasing health care costs, it’s conceivable that we might be better off doing the maximization you suggest above and picking an ACA plan with lower (subsidized) deductibles.

There could be many changes in the years ahead, of course. I think it’s not out of the realm of possibility that we gov’t employees will end up on the ACA or its successor plans anyway. Thanks for the reminder to analyze this in the future!

Excellent post – I’ve given up on roth conversions and am scooping up all the subsidies and gold plated silver I can.

I retired in 2008 and got my son and I nice cheap high deductible plans that worked just fine – I was paying about 200 for both of us – wife was on work coverage. But my plans became illegal.

Idiots in government want to fix things so now I pay $50 a month for gold plated silver for wife and I and $9 a month for medicaid for my kid. Govt pays well over 1K a month for gold plated silver and whatever they pay for my kid’s medicaid. $3 copays for us/nothing for kid – although we need to go to the one doctor in 50 miles that takes medicaid.

Idiots.

Also got the kid on reduced price lunch at school. And am applying for food stamps – the form still has a archaic spot for assets – but even if I put $50M there I qualify.

Waiting right now for the pg&e guy for the 30% discount I automatically get for having household with reduced price lunch; and am typing this on the $10 a month cable internet comcast was blackmailed into offering for ‘poor’ folks.

Again idiots.

Kid just got back from a school exchange program to europe but he pays 40c for his school lunch.

I hear you. Having reduced “status” for FAFSA purposes is way more important than the $300-500 saved on lunch.chac

Jeremy, this post was a tour de force of optimization analysis.

And if the analytical rigor weren’t enough to convince readers to take it seriously, the newfound use of end-of-paragraph punctuation would be ;)

I second Justin’s comment that no better evidence for the need for tax reform exists than the stunning complexity of the analysis that went into this post.

I would love a tax system that was simple and predictable, although the only thing I’ve seen with the current round of proposals is just lipstick on the pig.

Also, I assure you any use of terminal punctuation was purely unintentional

Jeremy,

I think that maybe a lesson here is that no matter what you plan for, you can count on the government to screw over your well laid plans years down the road with some piece of legislation. ACA did not exist until after you had already quit the rat race. Roth might be the best solution to allow maximum flexibility when it comes to tax planning down the road USING TODAY’s ENVIRONMENT, but who can tell us if ACA tax subsidies will always be around? Then there’s always the tradeoff between pay tax now vs pay tax later and how it affects your timeline to FI in the first place. All in all, great post and just lots to think about, and I’m sure you will continue to take on these challenges as laws change on us in the future

I have a slightly different take on this. If we were in the US, we would buy insurance anyway. The elimination of the pre-existing conditions clause is a huge boon to retirees, and there is a standard structure to all insurance plans that makes research easier. Overall, I think the ACA is the opposite of screwing us over

I’m still not a huge fan of the Roth, but there is a place for it in a retirement portfolio that consists of Traditional/Taxable/Roth. The US is one of the few 1st world countries that doesn’t have a VAT, which if (when?) we get one will make the Roth less appealing

But in any case, still retired, still happy. Life is good

I think a key factor in ACA subsidy or roth conversion is one’s future visibility of regular taxable income.

If looking at a substantial pension and/or social security than doing roth conversions is a big win – especially if you’re doing so in a window between being in a high bracket and starting that pension/SS.

For me I’ve got 15 years or so before SS and only a very small pension coming in 8 years or so. I’d rather suck at the ACA teat for now and am guessing I’ll never pay much of a tax rate on eventual IRA withdrawals. Avoiding a eventual close to 0% tax rate is no big win.

I am rolling the dice that if the govt ever ends the subsidy lunacy that the law will allow for a working high deductible insurance market again. That does worry me and may drive me to taipei or kuala lumpur someday – no big tragedy there.

I also find comforting that the correlation between health coverage and health is actually very low.

If I were to bet, I’d guess the US will move more towards single payer than to high deductible. Just like Taipei

I keep seeing comments to the effect that the ACA did away with high deductible plans, and this just isn’t so. For 2017-2019 I’ve have a high deductible HSA-eligible plan thru the ACA. Maybe insurers just don’t offer it in your state?

This comment is several years old now, but I don’t think it references the ACA doing away with HDHPs… (which of course it hasn’t)

… but more stating a preference for the HDHPs of old, where they cost $100/month instead of $1000/month (unsubsidized.)

Thanks GCC for these last two posts. Plenty to think about though it doesn’t apply to my current situation; perhaps my future one.

I would think the vast majority of folks would have no issue trying to minimize taxes. It probably get’s into a little more of a gray area IMO for early retirees to try to maximize subsidies. I guess those are the rules for all though, so why not?

However, one commentator above even spoke of reduced lunch. For some reason, that seems to cross a line. Not sure why and I realize that it might not be logical. Perhaps it’s the overt act of applying for “handouts” versus settling the bill on the 1040. Like I said, not logical.

Where do you stand? Get all you can or is there a line somewhere where those that are choosing not to work shouldn’t have their hand out?

In the grand scheme of things, I would rather pay for free lunches than bombs. At the end of the day, I just try to follow the life philosophy of “be kind.” I don’t always do a great job of it, but then I get to try again the next day.

It seems fairly common today (especially on the Internet) for people to spend a great deal of emotional energy judging others. That seems like a much higher price than a few extra tax dollars going to programs that might help a few at the margins that don’t really “need” it. If it is really important, it would be a better use of energy to work to change the incentives. Morality is fluid, but humans will always respond to incentives.

Beautifully said! Just be happy and don’t worry about other people.

This is about a thousand times more thorough than the post that we’re still working on about reverse engineering our retirement budget (and thus our retirement savings needed) based on the ACA limits! (Man, those super silver 97 plans sure look sweet, if you can stick to right around 138% FPL!) Our big hope is just that they don’t introduce any asset tests into the mix — that would throw in a major wrench. There’s been some movement in that direction on social security (in terms of taxing benefits for those earning above certain thresholds), and policy debates suggest that caps on benefits to those with high assets could be on the table. Not that we’d care — we’re not planning on getting social security when we reach that point in 30 years. But we sure as heck DO want to keep our health care costs as low as possible, and so are prioritizing getting a big subsidy now over what we might owe in taxes later — especially since we assume Medicare will stick around, beloved as it is, and we can wait to take our minimum distributions until we’re safely in the non-subsidy cliff arms of Medicare.

Thanks for this pretty incredible breakdown!

Wow that engineering degree came in handy. A little off topic but I was wondering how you are planning for RMDs considering your pre-tax stash is growing faster than you can convert it.

See this post: https://gocurrycracker.com/gcc-vs-rmd/

The reason I included “% of 10% bracket” as a metric in a table above is because I used that same metric in the GCC vs RMD post

Holy @#$%! You’re a tax-optimizing maniac! That’s some seriously complex analysis. I think my brain moved to another country after the 3rd graph with multi-layered tax curves.

Thank you, though. I can at least see a groove in the lines where I can achieve a lower tax rate.

If you made it to the 3rd graph, you probably read farther than most people. This topic is a bit heavy. But now it is something people can refer to when it is needed.

Yeah, my head was spinning. I am glad you have the last paragraph though….things may change, the important thing is to be flexible. Our current plan is to leave the US, but it does make we wonder if I should look into Roths again just in case.

Well crap GCC, now I have to rethink all kinds of things! Thanks a lot ;-)

Seriously though, this is the first time I immediately knew I was going to need to re-read an article in a long time. Awesome stuff!

Writing long, complicated, & confusing blog posts is just one of the services I provide here :)

Wow. Just wow. I read it all, three times, and I realized that I must immerse myself in the tax code. Amazing analysis! I think you should offer ACA and tax optimization consults.

A couple of thoughts on where the ACA is going. Agreed that it is insanely complicated and that we need a simpler and more cost-effective solution. I am not sure we are headed, however, for single-payer. It has worked well for Medicare, Canada and Australia, and less well in the UK. With the insane power of the insurance companies here in the US, I have a hard time seeing them pushed out of business. Curious as to why you think we are headed there as opposed to a highly regulated multipayer system like Germany or Switzerland? I do agree that we are heading for a lot of change, presumably towards a simpler and cheaper system.

I still think Medicaid is the best insurance money can’t buy, but even more than other health insurance it has never been shown to improve any health outcome. The recent study in Oregon has shown its main effect is more ED visits and higher costs. This is probably more a reflection of the current Medicaid recipients than the program itself. I am sure the ER crowd would utilize it more wisely.

I’m not sure we’ll end up at single payer. But I think the trend is more likely in that direction than towards a system that allows young healthy people to buy HDHPs.

My plan, on Medicaid from 50-54, at 55+ go on NY’s “Essential Plan”, which is exactly like Medicaid, no premiums or copays. This avoids Medicaid Estate Recovery claims on my estate.

The ACA is fantastic for ERs and low income folks. The situation was absurd prior to its passage. I hope political changes do not scrap it.

I extreme early retired at the end of August (38!) so I’ve been mashing my brains trying to figure out how much income I should shoot for to minimize taxes & out of pocket costs and maximize ACA benefits and gain/loss harvesting. It doesn’t help that I have an additional layer of complexity since the state I live in has an income tax of ~4.7%. At the moment my plan for 2016 is to estimate my income at the bare minimum to not qualify for Medicaid but get the maximum ACA subsidy, which I think is about $15,600 for states that expanded Medicaid. That will buy me 11.5 months of time to further mash my brains trying to figure it out and if I conclude having additional income and having to payback some of the subsidy makes more sense then I can just manufacture that income just before the year ends.

Your analysis is quite detailed so it’s going to take me reading it over at least 10 times to get most of it.

138 FPL is currently $16,243 yr / $1,343 mo. So you need $16,244 to avoid Medicaid.

“Since total annual spending is higher, we could draw down savings that don’t contribute to MAGI, including cash, basis in stock held in a brokerage account”

Hi, thks for an excellent post, I have a question on the comment above, do you favor any particular cost basis selection in order to optimize vanguard withdrawals. I understand they offer 3 options – Average Cost, specific identification and first-in, first-out.

rgds

I always use specific identification. That way I know exactly what my gain (or loss) will be

Very impressive analysis! I love your blog, and admire your abilities, but disagree with some of your way of looking at things. To call ACA a tax because you have too high an income (via gains harvesting) to take advantage of both ACA subsidies AND 0% capital gains tax law just doesn’t jive for me. ACA IS a tax, but not for that reason, but rather what SCOTUS said (if you force people to buy insurance or pay a fine, that’s effectively a tax). I have to agree with Steve in his post above, i.e. it may be crossing a line when people of very sizable assets take advantage of the criterion of “income” to qualify for subsidies. It’s one thing to minimize taxes, it’s another to qualify for subsidies via what is in principle a loophole. As you alluded to at the end of your post, the ACA can not survive in it’s current form, and like Social Security, congress is likely to switch to means testing as part of the qualification. A lot of the current “loopholes” are likely to disappear in the future, like back door Roth, file & suspend on SS, etc. We just can’t afford to continue with these loopholes which jeopardize the main intent of these safety net programs.

Hi Bruce

My use of the word tax is purely mathematical. If we earn $1 more in income, the government will keep a portion of it. There is nothing more to it than that.

As you know, this doesn’t even apply to us since we are outside the US. But many can benefit from at least understanding the system. Then each can choose what they do with that knowledge.

At some point, you may be in a position where you have earned $400% of FPL and have the option to earn $1 more. That $1 in income could cost you $4000 in insurance premiums due to the subsidy cliff. Maybe this is OK, and you pay the $4k. Maybe this doesn’t jive with you, and you choose to not earn $1 more.

Whichever path you choose, please vote for a system that isn’t so completely messed up. I’ll do the same.

Jeremy

So if I buy a 1.2 million dollar vacation home down the shore and finance 1 million at 5% thereby getting a 25K subsidy from the goverment in the form of a tax deduction would you be ok with that?. Also keeping in the mind that said home is likely to sit empty for 9 months of the year.

1. SCOTUS had to look beyond labels into substance to conclude that the “penalty” for violating the individual mandate is actually a tax. By contrast, the ACA tax credits (as they are called in the statute) are in fact “tax credits” (or “negative taxes”) in both name and substance.

2. The subsidization of asset-heavy taxpayers with low reported incomes is not an unintended “loophole” in the law. Congress knows how to implement an asset-based means-test when it wants to but, in the ACA, thus far opted not to. And if you think that is unfair, keep in mind that the various tax policies that promote leisure over labor that we in the early retiree community exploit (like the 0% LTGC rate you cited) actually treat passive income more favorably than earned income. The ACA, at least, treats all income equally instead of giving income from a million-dollar nest egg BETTER treatment than income earned from actual labor.

My philosophy on these matters is similar to what Jeremy just suggested — try to implement your system of choice through suffrage, but don’t hesitate to exploit whatever system is in place to the fullest extent permitted by the rules of that system.

Agree completely about sucking the teat.

Note too that asset based testing itself is very subject to exploitation. Money in a house or a IRA doesn’t count the same way for FAFSA/SNAP as other assets. Folks will work around any halfhearted attempts at means testing.

Purely speculative but I think there’s a bipartisan taste for dependency and I don’t think the very few early retirees are going to spoil that taste. We aren’t that important.

BTW, the ACA does NOT treat all income equally – I’ve got lots of savings bonds and deferred gains that sidestep the MAGI test, and with earned income the deductible ira/403/457/401k twists make earned income particularly gameable.

It is not cost effective or efficient to implement asset tests and would drive many people away from the ACA, that is why they didn’t create it with one. The goal of the ACA is to get everyone insured, the simplicity of the income test alone best suits this purpose. The number of people who have very low income and high assets is negligible.

Great analysis Jeremy! One thing I’d like to clarify: do any of your results include the benefits of the Child Tax Credit? I know it’s not as simple as saying, “3 person household = $1,000 tax offset, 4 person = $2,000, etc.” However, if the effective tax rate on a Roth conversion is 25%, couldn’t a family of 3 with $1,000 CTC coming increase the conversion by $4,000 and still still pay no tax? I’ve only read this article 3x, so it’s possible I’m still missing something! :)

I haven’t included the CTC in this analysis.

Since the CTC provides a credit on tax due, we can increase income to create a $1k tax bill per child, which would then be eliminated by the credit.

The additional income would reduce ACA subsidies however.

There is more to it than that – a large chunk of federally funded state programs have gone away from asset tests, including most medicaid, food stamp, and school lunch programs. And many other benefits key off these. Whatever the reason it certainly works to the benefits of early retirees who can manipulate their taxable income.

Note – the asset test is about the only ‘simple’ thing about ACA, otherwise it’s written to employ accountants lawyers and hr specialists. And it has patently failed at the ‘everyone insured’ metric. The expansion of medicaid has likely had more impact.

Wow, the differences in the US tax system and the Dutch are immense. But it can best be summarized as this: for people wanting to become, or people that are, financially independent are way better off in the US!

We’ve been through most of your tax deferral and tax optimization articles and recently have been working our way through the Dutch tax system, but we have far less options to do similar tax deferral/optimizations. Seems that our effective tax burden will not be able to be brought down below about 25%.

Maybe its time to relocate to another place once we are financially independent!

Have you though about the UK , it seems to implement favourable treatment of investment income, taking full advantage it would appear that a couple could have up to 80K(stg) income from investments while only having an effective tax rate in 5-6% range. Of course some planning would be needed to maximise income in different spaces – LTG’s, interest, dividends etc.

Thanks for the tip, definitely worth exploring! However, somewhere warmer/dryer is also part of the equation for country selection during financial independence ;-)

I have read this post 3 times, I’m starting to think 50% traditional and 50% Roth/taxed savings might be the way to go and hope for the best. I am wondering, similar to T-Rav, do your results include the Child Tax Credit, Saver’s Credit, Earned Income Tax Credit? I am viewing this from the accumulation phase, but I would think these apply during post retirement phase.

See my reply to T-Rav, the CTC isn’t included.

The EITC won’t apply in most cases, as even very small amounts of investment income reduce the credit to zero. Saver’s credit also doesn’t apply since we aren’t contributing to retirement accounts.

I haven’t done sufficient analysis yet to recommend a Traditional/Roth ratio, but I think it is more like 90/10 than 50/50.

Great post! This is what everyone needs to study and understand to take advantage of various tools that are available. Just a little bit of studying they can save really big $.

Thanks for sharing.

BSR

A Roth conversion in Dec will increase income at the end of the insurance plan year, and require PTC payback – but only up to a family cap of $600 – $2550, depending on income under 400% FPL. You might want to include those caps in your excellent and otherwise exhaustive analysis, or just mention it. The caps (if I understand them correctly) can blunt the cost of lost PTC for a Roth conversion.

I wasn’t aware of this cap, thanks Rebecca

http://obamacarefacts.com/advanced-tax-credit-repayment-limits/

I think the strategy of “predict a low income so you get APTC” and then “woops! i made a Roth conversion so my income was higher, yet my clawback payment is limited” may eventually backfire.

I believe that in the next years, as you apply for ACA marketplace plan, they’ll be comparing your predicted income to your actual tax records of previous year. When there’s a discrepancy that is significant, they’ll ask for documentation or reasonable explanation.

How many years do you think it will be possible to keep saying “well, last year my income was high because of a late-year Roth conversion … but this year I’m predicting I won’t do that” and yet keep repeatedly doing that?

I’m just suspecting that the approach of doing Roth conversions and hoping to convince marketplace that your lowball estimate of upcoming year’s income may fail as people see you’re gaming the system to get APTC and only have to pay back some of it because of the clawback limitation. I think instead what will happen is the marketplace will deny your attestation of very low income based on previous tax data, and so you’ll simply get less APTC in the first place. So the “taxation” effect of APTC will be real, and GCC quantifies it.

I’m single and I have earned income from self-employment, and it seems I can reduce my MAGI by maximizing my contributions to my Solo 401(k).

This will be my first year getting insurance through the federal marketplace. Does one simply estimate the 2016 income, and deductions to arrive at MAGI? And if this leads toward getting premium subsidies what if there is a discrepancy between the estimate pg 2016 income and deductions, and what actually is the income for 2016?

Yes, you estimate. Any discrepancy will be made up at tax time the following year.

Wow,

I don’t think I have the intellectual firepower to fully understand all the moving pieces but you have done a beautiful job of laying out the details. Very impressive!

I know this won’t likely apply to you personally, but for someone who owns their house, the ACA seems to throw another factor into the decision of whether or not to pay off the house before retirement. Conventional wisdom would say keep the mortgage and keep retirement money invested. Now it may make sense to pay off the mortgage, thus lowering expenses in retirement, and lowering capital gains and dividend distributions in the future (because you used that money to pay off the mortgage). This effectively reduces the amount of money you will need in retirement, lowers your MAGI, and can result in increased subsidies.

Why not add one more variable into the mix ;)

I would love to hear your thoughts on this.

My thoughts:

Imputed rent (free rent) is the term for the value you receive when living in a house with no mortgage. Some countries even tax it. Since the US isn’t one of them, imputed rent can be advantageous for those choosing to optimize Obamacare (and any other government program that uses MAGI.)

Impact to ACA subsides as a result of paying a mortgage (or rent) depends on how the $ are sourced (see Tax Implications section in the post above.)

$ source:

Cash, stock basis, Roth IRA – zero impact, since no income is generated.

Long Term Capital Gains – taxed at 15% or less.

Traditional IRA withdrawals – taxed at 15-25% (or more.)

If you were going to source the mortgage payment from cash/stock basis/Roth then I wouldn’t pay off the mortgage. If you were going to source 100% of it from Traditional IRA withdrawals, then maybe paying off the mortgage would be better. It would depend in large part on the mortgage details (P, i, t.) and relative size of total annual payment vs 400% of FPL threshold. The analysis would be more complicated than possible in a comment, but doesn’t change the fact that we will be Renters for Life.

It is also important not to let the tax tail wag the dog. 15% tax rates are fairly low, and unlikely to be a major difference in long term wealth as compared to the fundamental growth rates of housing (inflation) vs equities (7% real.)

Thanks for the reply! I think my strategy will be not to think to hard about it and to keep reading you blog for ideas ;)

Who do I see to just have THEM do all this for me?

A Financial Adviser could potentially help with the planning. Maybe.

You write: “If non-dividend/capital gain income is less than 138% FPL & total MAGI is less than 400%, we have a choice of how to use the remaining portion of the 10% Federal Tax bracket (shaded region in Opportunity Space chart.) We can either do a Roth Conversion and pay 10% tax…”

I’m really glad you made this post. However, the above argument seems flawed. I don’t think your “opportunity” space actually means you’re free to “fill up” the 0% tax bracket and 10% bracket with Roth conversion and expect to get away with a rate as low as you say. In fact, the cost is greater than that, because the Roth conversion pushes MAGI up, and health care premiums depend on the MAGI, not how much of MAGI is actually taxable.

Let me illustrate by using an example of a 1-person household taxpayer whose goal is modest: to fill up the 0% tax bracket with a Roth conversion. Let’s suppose this taxpayer has some taxable income from self-employment and interest of $3500, and nonqualified dividend income of $1800, and qualified dividend income of $13700 (that will enjoy the 0% LTCG tax rate). This taxpayer is using only $3500+$1800 = $5300 of his 0% tax bracket (i.e. the $10,300 of his standard deduction and personal exemption). So it seems like this person might want to “fill up” that 0% tax bracket (even if not filling up the 10% bracket) with a $5000 Roth conversion.

Now observe the difference between not doing the Roth conversion ($19000 MAGI) and doing the Roth conversion ($24000 MAGI).

Not doing Roth conversion:

MAGI: 3500+1800+13700 = 19000

FPL ratio: 19000/11670 = 1.628 = 163% FPL

applicable figure: 0.0462 (i.e. 4.62% is “affordable”)

affordable insurance: 19000 * 0.0462 = 878 for year

Doing Roth conversion:

MAGI: 3500+1800+5000+13700 = 24000

FPL ratio: 24000/11670 = 2.056 = 206% FPL

applicable figure: 0.0655 (i.e. 6.55% is “affordable”)

affordable insurance: 24000 * 0.0655 = 1572 for year

If the taxpayer estimated income at 19000 but then actually does the Roth conversion and income ends up at 24000, the repayment limitation is 750. The difference 1572 – 878 is 694. So this means the taxpayer does have to repay all 694, bringing total cost of insurance up to 1572.

So after all this, what is the actual “cost” of doing this $5000 Roth conversion. The $5000 cleanly sits inside this taxpayer’s $10,300 that is free of income tax. Yet the cost is $694 to do this Roth conversion. That’s an effect of +694/+$5000 = 13.88% effective “tax.”

[Even if taxpayer games the repayment limit by converting only enough to stay under 200% FPL and have a repayment limit of $300, the effective tax is still something like 300/4200, or 7%.]

This is just for someone trying to fill up the 0% tax bracket. For someone trying to fill up both the 0% and 10% tax bracket with a perfectly sized Roth conversion, the effect is even greater. Because such a Roth conversion pushes the taxpayer’s MAGI up (and this MAGI includes the qualified dividends that won’t get taxed), it does have an effective “tax” that isn’t just 10%, but a value closer to but slightly under 25%.

My conclusion is that it isn’t really possible to “make use” of filling up the 0% and 10% space with a Roth conversion unless one’s overall MAGI remains under 138% FPL after the conversion amount is included. Not simply if one’s overall MAGI is anything under 400% FPL, which is what I think your argument was implying. I think that “opportunity space” you imagine is there at the left end of your graphs isn’t really there in many cases.

Yes, you are correct and I am wrong. Thanks for pointing out the flaw and for providing a detailed explanation.

Looking at this now it is clear that if 138% < MAGI < 400%, any incremental dollar would cause a reduction in subsidy and be subject to income tax. For most US residents, it looks like the ACA killed Roth IRA conversions.

Is this true? If so, it could be useful to people if you update your post accordingly (if you haven’t already) since it seems to me that it invalidates a significant portion of the strategy for Roth conversions. I’m really trying to understand the tradeoffs here, and your posts are really valuable – thank you.

More of a miscommunication. If you have total income below 138% of FPL there is a small window of opportunity to do Roth conversions at 10% tax rate.

A second example, even more closely in line with your discussion of someone Roth converting within the “10%” space that lies below the 138% marker.

Taxpayer B has $10000 income, $5 interest, $1100 nonqualified dividends; plus $10,895 in qualified dividends. They are thinking of Roth converting $5000, which would bring their taxable income to 10000+5+1100+5000 = 16105, the 138% FPL mark you think is meaningful. All 5000 of the Roth conversion sits in the “10%” space (because it’s $11105 to $16105, and the 10% space comprises $10300 to $19525 for this Single filer).

Not doing Roth conversion:

MAGI: 10000 + 5 + 1100 + 10895 = 22000

FPL: 22000/11670 = 1.885 = 189% FPL

applicable figure: 0.0583

affordable insurance cost: 22000 * 0.0583 = 1283

Doing Roth conversion:

MAGI: 10000 + 5 + 1100 + 5000 + 10895 = 27000

FPL: 27000/11670 = 2.313 = 231% FPL

applicable figure: 0.0743

affordable insurance cost: 27000 * 0.0743 = 2006

The taxpayer doing the Roth conversion owes an APTC repayment of 2006 – 1283 = 723, or 750 repayment limitation, whichever is less. So in this case, owes 723. That 723/5000 represents a 14.46% “tax” because of the Roth conversion.

So what is the “cost” of doing this $5000 Roth conversion within the 10% “space”? It’s not just 10% of 5000.

Income tax cost: $500, or 10%

ACA related cost: $723, or 14.46%

Total cost is $1223, for an “effective” marginal rate of $1223/$5000 = 24.46%.

Thus the taxpayer B needs to think hard about whether it’s right to do this $5000 conversion even though it seems to sit in the 10% “opportunity” space you described. Even without straying higher than 138% with the taxable income, this taxpayer B pays 24.46% to take these $5000 out of traditional IRA and convert it into Roth IRA. Taxpayer B would have to presume that RMDs in future will force trad IRA withdrawals to be taxed higher than 24.46% in order to make it worth doing.

This is the first year since i lost health insurance at my part time job that my income should stay in the subsidies range. I’m invested in all index funds in my taxable accounts.(they produce mostly Qualify Dividends and LT gains) I’m focusing on limiting taxes now and getting the largest subsidies now. I work part time and changed from a Roth 401k and IRA to traditional ones. I did this to keep lower MAGI. That will just produce higher RMD in the future. I have rental properties and really need little to no investment money now and all projections are that my retirement accounts are also extra. I was planning on selling shares of taxable accounts that lost value (They would be from specific lot shares) and wait the 31 days and put that $5500 into an Traditional IRA. Lowering my income in both ways.. Wondering your thoughts on that idea and figuring out what to do when I turn 70. (currently age 48) I still am now wondering why and to what detriment my working part time is worth. I wonder if the government will tax retirement withdrawals extra to help others that didn’t save enough for their retirement?? I heard Clinton and some other politicians toying with that. Any thoughts on what I’m doing would be of interest. I like the idea of converting Trad IRA to Roth but being single I only have up to $37400 so that really limits the amount.

Any interest in (temporarily) living abroad? Eliminating the ACA requirement is a good thing for Roth conversions.

There should never be a situation where $1 of earned income results in anything close to $1 of tax. So you still come out ahead financially by working, maybe just by less than you would have liked.

Tax loss harvesting is one way to reduce current tax burden (up to $3k per year.) Any cash flow from the sale can’t technically be contributed to an IRA, but if you have the earned income even after 401k contributions you are fine. The thing to compare is current marginal rate (including ACA subsidy reductions) on those 401k/TIRA contributions vs. expected future marginal rate. The 25% marginal rate for single people goes all the way up to ~$90k.

At Age 65 you’ll be on Medicare instead of the ACA. You can do Roth conversion during those years without the ACA subsidy impact.

At age 70.5, the RMD kicks in. But the RMD isn’t substantial until at least age 80 (starts at less than 4% of tax-deferred assets.)

I like to keep the part time for now and just work a few thousand dollars over the $5500 the IRA covers. I just at the point that I don’t want to work too much that the lost subsidies mean I worked for what feels like nothing. Also if the companies don’t want to cover me anymore and thanks to Obama the government is really telling someone like me to not work or put a limit to how much. I like the tax loss selling to fund the IRA and think that benefits me currently. We shall see what changes come about with healthcare. (I’m sure there is more to come) Also no I don’t have a desire to live in any other country yet but one never knows. Thanks

Any thoughts on how you would approach this differently if you knew the following at a young age in a three-person household with a similar income profile to your own when you were working:

1) One spouse has a chronic, incurable-yet-treatable illness that requires heavy annual use of healthcare services, to the point where the annual deductible on a high deductible plan is reliably met in every year.

2) Child has Down syndrome and may require heart surgeries down the road, along with other potential medical interventions.

How open would you be to living abroad knowing these things? How would your approach to early retirement change? Thanks!

It would be necessary to budget for these expenses. Recurring annual expenses require investments of at least 25x (4% Rule.) One time expenses also need to be planned for.

In the US, ACA subsides and out of pocket maximums could reduce these costs dramatically. In order to qualify for max subsidies, you would need to keep total MAGI less than 200% FPL in retirement. This would mean zero or limited Roth IRA conversions, so it could be worth getting as much into Roth IRAs as possible while working (via mega backdoor Roth, for example.) You may essentially choose to pay more tax now to get more subsidy later.

Outside the US, if you were to live in one country as a permanent resident, you may qualify for coverage under a national health plan after a certain period. Countries with single payer health systems would be worth investigating.

Being fully nomadic may be more financially challenging, since you would have to cover more of the healthcare costs out of pocket. But you may be able to find an International health plan that phases out exclusion of pre-existing conditions after a few years. You could also pick and choose where you buy meds or have non-emergency surgery. The US may have the highest prices in the world, which is not the same as the best quality.

I will be overseas fewer than 330 days but probably more than 150 and I’d have to pay for insurance when I would not be covered anyways. I accept the ACA was a decent honest try to help a lot of people but I hate that they have a made it a one-size-fits-all solution. I am off to read about Medishare. Looks promising. There was something along those lines on the NYT last week (someone complained about havng to endorse Christian values they did not really share to get affordable coverage) but I did not connect the dots until now. Thanks for the link!

Great post. Regarding the “living outside the US” part, I wonder how you cover your health expenses abroad. Do you self-insure?

Mostly

Thanks for a thorough look at this, I’ve read through your post a few times and still find myself a bit confused. I’m an Alaskan resident, so our FPL levels are at $30,380 for a family of 4 rather than $24,600. Our unsubsidized health care costs are some of the highest in the nation $2400/month for a silver plan with a $6k deductible with no subsidies. We own a rental property with two units,personally finance a mtg on another dwelling and intend to continue to have some self employment income once we begin FI. SInce we will need health insurance it feels like we’ll need to aim to have either really low income (less than 60K) to qualify for subsidies, or really high income, so that $29,000 in premiums and $13,000 out of pocket expenses don’t feel absolutely overwhelming. We are trying to learn more about tax code, and making spreadsheets timing things out, but can you lend any insight into how little income we would need to earn in order to take advantage of low tax (10%) roth conversions and untaxed capital gains? Also, are there any tax code tutorials or resources (besides your well researched blog, of course) that you would recommend? There are so many moving parts, and we’re up to our eyeballs in spreadsheets, trying to figure out which options are financially optimal. Thanks so much!

I’m not aware of a good tax code overview. I primarily write these posts to help me figure it out for our needs.

The low taxed roth conversions and 0% cap gains are only for the first 138% of FPL +/-. After that subsidies are reduced / taxes increased.

Subsidies and cost sharing are still pretty good up to 250% of FPL (roughly $75k using your numbers) and still exist up to 400% FPL ($120k income.)

If you have no income can you take long term capital gains up to 95,000 for a 2 person household. Does rental property qualify for this amount as well? Thank you so much for opening my eyes on paying too much taxes.

Yes, long term capital gains and qualified dividends.

Rental income is neither of those, so no. But it is already favorably taxed due to depreciation and deductions.

Thanks so much for the answer. What about the Capital gain if I sell the investment property. Does that capital gain from the sale work the same way.

Yes, kind of. The gain from the sale would be a capital gain, taxed at between 0% and 20%, same as if you sold stock.

However, you also have to reclaim depreciation which is taxed at ordinary income rates.

Often in this case a landlord will use the proceeds to purchase another rental property (a like-kind exchange) which allows continued tax deferral.

I am in the accumulation phase and almost all my savings is in Traditional 401k/IRA’s. My income puts me in the 25% (now 22%) bracket but I have been using my Traditional contributions to get down in the 15% (now 12%) bracket. I am planning on retiring in a few years and using ACA health insurance. I have read your post over and over, but I still can’t decide if I should change my 401k contributions to Roth and pay the 22% tax now or continue doing what I have been doing and pay ~25% effective tax (after 138% FPL) when I retire and start my Roth conversion ladder to cover my family’s expenses (~$40,000/year). I am starting to think I should switch to Roth’s or maybe even a taxable account to have more post tax money to cover >138% FPL. Any thoughts?

40,000 rollover from 401k to a Roth does not put you anywhere near a 22% tax bracket.

Look at the Combined Federal & ACA Tax Profiles chart above

I don’t know near enough of your situation, but I’ve been on ACA health insurance for 3 years. I am single and as of 2018 premiums for my area I can earn more and 100% of the premium is covered. Before I had to watch what I earned at my PT job so I could put 100% into a traditional 401k and IRA. I also have rental properties so that adds to my cash flow which provides deductions. I have a friend and she is using Roth IRA withdrawals to keep her income just over the 138% but she is over 60. Now you can use the contributions made to Roth IRA after 5 years but not earnings if you are under 59 1/2. So maybe it would be better to use Roth 401k or IRA now? It depends on how you plan on generating income before 60?

Thanks for the replies. I live in Nebraska (no expanded Medicaid). When I retire in a few years, I plan on doing a Roth conversion ladder to 100% FPL (family of 4 = $24,600). My expenses will be $40,000/year so I have to cover the difference (~$15,400/year). I don’t have enough in my taxed accounts to cover this, especially considering the 5 year wait on the Roth conversions. Prior to ACA I was planning on doing Roth conversions for the $40,000/year. But with the ACA available, part of me is thinking I should switch to Roth 401k or taxed account and pay the 22% tax now so I don’t pay the ~25-30% “tax” on the $15,400 in the future when I retire. The other part of me is thinking it is all going to change anyways so take the guarantee and save the taxes now. Thanks again for the replies and any more input you have on this.

Yeah, it’s not a black / white decision.

Note that the charts in this post are pre-TCJA, meaning rates are now 3% lower (your 22% current marginal rate is the same as your Combined Federal & ACA tax rate later, i.e. 22%.) Same same.

Some things to consider:

– State tax. A TIRA contribution saves you 6.84% Nebraska tax now, but withdrawals will be taxed at zero to less than half that (assuming you stay in Nebraska.)

– if you max out your Traditional 401k ($18,500 in ’18) then you need to make ~$25k to contribute the same amount to Roth 401k, based on Federal 25% tax rate only. Instead, you can take that ~$6k tax savings and put it in your brokerage account (or to Roth IRA or Backdoor Roth.) You can use that $6k to help bridge the 5-year gap

– Nobody knows what the future holds – The ACA repeal & replace efforts included a fixed tax credit that was based on age rather than income, so no “ACA tax” as outlined in this post. The repeal of the individual mandate in the TCJA should bring back the option to have an HDHP, also with no ACA tax (since no subsidy.)

Sorry, no easy decision, but hopefully this helps.

How does the Trump CSR change alter this analysis?

http://abcnews.go.com/Health/wireStory/trumps-health-subsidy-shutdown-lead-free-insurance-50580570

“The Obama-era health care law actually has two major subsidies that benefit consumers with low-to-moderate incomes. The one targeted by Trump reimburses insurers for reducing copays and deductibles, and is under a legal cloud. The other subsidy is a tax credit that reduces the premiums people pay, and it is not in jeopardy.

If the subsidy for copays and deductibles gets eliminated, insurers would raise premiums to recoup the money, since by law they have to keep offering reduced copays and deductibles to consumers with modest incomes.

The subsidy for premiums is designed to increase with the rising price of insurance. So government spending to subsidize premiums would jump.”

Should be close to a wash – premiums go up, subsidies go up

I’ve found this calculator helpful in figuring out ACA subsidies. This is my family’s first year on ACA subsidized ins, and the calc accurately predicted what my health ins charged me after subsidies

https://www.kff.org/interactive/subsidy-calculator/

It shows my fam of 5 can have income up to $60k and pay $0 (get full subsidies)

Separately, I know if our income was just $60k, we would pay no income tax.

So I’m confused by the above analysis which talks about 30% tax brackets etc at $40k. Did something huge change from time of writing to present day? Or am I missing something big and in for a rude surprise?

Hey Andrew

I don’t think you’ll be surprised. The above charts are just looking at the math of income tax and ACA subsidies. Other subsidies are above and beyond.

So, for income tax – A family of 5 with MAGI of $60k would have income tax burdens of ~$3k in 2017 and ~$4k in 2018. This may then be offset by tax credits of various sorts. The Child Tax Credit would presumably pay you $3k in 2017 and $6k in 2018, so you end up with a $0 or negative tax burden.

As you say, $0 net tax, but based off another subsidy.

For ACA subsidies – A family of 5 making $60k/year is at ~200% of FPL. By definition, you would have to pay around 6-6.5% of income for the second lowest cost silver plan. So not $0. But… if you chose a Bronze plan, you could be at $0 if the premiums were lower than the allowed subsidy. That is what I see in the Kaiser Foundation calc with the State as “US average.”

Technically by choosing a free bronze plan you are leaving some money on the table (about $2500 per KFF) but if you don’t plan to use the insurance that may be cheaper than paying ~$4k for a silver plan with better actuarial value. These are just rough numbers from KFF. That’s a tradeoff to make.

From here, you could look at the charts and estimate how much a $1000 change in income would impact things. Let’s say you decided to do a Roth conversion of $1k. That’s where you would see the 30% brackets or whatever, as you would get a reduction in subsidy by about 15% and an increase in income tax of 25% on that $1k. (2017 #s.)

Thanks so much!

The crux of my confusion was your analysis is for silver while I’m on bronze.

Assuming no other big changes happen, when I leave full time work hopefully in 1-2 years I think I’ll

-fund my family’s $30k/yr life with non-reinvested dividends and long term cap gains

-fill up the $24k standard deduction with Roth conversions and ordinary dividends

-keep my MAGI around $60k to get $0 bronze premiums

As I’m writing this I think I understand better what you are explaining. If I went a little above the $60k MAGI I would still pay no direct income tax, but I would lose some aca subsidy. Luckily that leftover premium is very low compared to what I’m used to. The real wild card in the aca for me is no out of state coverage!

Thanks for all you do in explaining this stuff.

Even 3 years later, this is still the best analysis on the web! Thanks for writing it. This is my first year on the ACA, and this is exactly the information I needed (and yes, I read it all the way through).

I agree, but maybe someone could update it . . . ?

My husband and I are both 61 and semi retired. My daughter aged out of being on the ACA with us, so we can no longer claim her income. My part time job gives us about 3,000 in earned income which gets wiped out by a rental house we own. Our actual income claimed is around -3,000 with all the real estate deductions. We live in a state that did not expand Medicaid so our income threshold is lower, to qualify for the ACA. Since we now need income to qualify, would converting some traditional IRA to a Roth be a good strategy? We have enough in cash to live on for the year, so we don’t have to touch retirement accounts. I’m just not sure how much would be a safe amount to convert, so as not to mess up our ACA insurance. Would it be better to just wait until 65 and Medicare and then start converting?

In a State without Medicaid expansion, as a “childless adult household” you’ll need an AGI of at least 100% FPL to be able to get ACA subsidies. For 2021 coverage for a 2-person household that is a bit over $17k (numbers here.) A Roth conversion could help you increase income to that level. To understand your options you should contact the ACA marketplace in your State.

Sounds like a win-win, to me! Thanks so much for all the time spent educating us folks!

Thanks GCC, this and your previous post were the most helpful analysis I’ve found on this. I’d be interested on yours (and your readers’) take on my situation as we’re slowly working toward FI.

Family size of three (I’m 34, wife 33, infant daughter). I’m self-employed with some part-time W-2 work. Wife has some small SE income. Predicting about $89K-110K MAGI for 2018. 400% FPL is about $81K.

On a Silver PPO plan. Subsidy we stand to gain/loss based on MAGI is about $3K, not a small chunk.

I have a Solo 401(k) to potentially reduce MAGI to keep the subsidy, but we only have about $26K in the bank, and $20K in brokerage funds. $95K in Roth IRA’s ($60K contributions w/ basis), $80K in Traditional IRA’s.

Wife isn’t totally on board with the extreme frugality, so we’re on a less-aggressive path to FI, and I’m okay with it because I enjoy the flexibility I have now with self-employment.

To keep the subsidy, would you recommend funding the Solo 401(k) with a) savings, b) brokerage funds money, or c) withdrawing contributions from the Roth IRA?

Feels counter-productive to FI goals to draw from brokerage or Roth, but Wife wants the emergency fund beefed up, so the $26K cash savings is her least-preferred option. And selling off brokerage funds will trigger cap gains, driving up MAGI further (but beneficially cap gain harvesting).

I could file an extension to give me until 10/15/19 to contribute to the Solo 401(k) and settle up on the subsidy, but that seems like robbing Peter to pay Paul regarding keeping 2019 MAGI low enough to keep that year’s subsidy.

Probably looking at kid #2 in 2020, which would increase our 400% FPL amount a bit.

Hey Joe…

It sounds like you are doing well. Congrats on the addition to your family (and $2k/year child tax credit.)

I assume you mean the subsidy cliff is $3k? So you are just looking to keep total MAGI below 400% FPL? Any contributions to tax-deferred accounts will do this – Traditional IRA, Traditional solo 401k, HSA, 403b, whatever… There is no Peter to rob, just take it one year at a time. (Employee contributions to solo 401k typically need to be complete by end of calendar year, not tax year.)

Money is fungible. $ from cash flow, cash, brokerage account (sans gains/loss), or emergency fund are the same. Be sure both of you adults understand this completely for maximum marital harmony.

In an emergency situation you could withdraw $ from a Roth at that time if need be. Roth withdrawals should be last and done only in a true emergency (job loss and house has burned down) vs you “need” a new kitchen. .

Thanks GCC, it really helps to have additional counsel in this decision.

Yes, our subsidy cliff is $3K this year, trying to stay below 400% FPL. We were only on the exchange 8 months this year, running out COBRA from formerly both being W2’d DINK’s. How life has changed (for the better).

So theoretically, our subsidy would be about $4500 in 2019 being on the exchange for a full year, if that’s where we decide to stay. I’ve considered Medishare because our healthcare expenses are low, but it’s frustrating not to be able to deduct share payments before AGI, so I don’t think we’ll come out ahead that way.

Thanks for the fungible comment, that truly helped with the prioritization of funding sources. And definitely not doing anything that would sacrifice marital harmony.

And for the reminder on Solo 401(k) contributions. I had been thinking about the employer portion, not the employee portion.

This particular post has me rethinking our overall tax strategy. We are doing the classic Roth Conversion pipeline to cut our overall tax burden. Our spending is very low (around 20k and we could stay below the 138% fpl to qualify for Medicaid).

However, the tricky part is the first 5 years of retirement to start the pipeline. If we convert 20k from trad to Roth, then we still need another 20k to live on (possibly taxed). So, we have the potential of 40k income for a household of 3 which would qualify for subsidies but not as cheap as I would prefer. If I mix in some Roth accounts today, then we can pull directly from those in the first 5 years to reduce our MAGI (we do have some in a brokerage but very little since most savings are tied up in pre-tax accounts).

So, maybe the right strategy is to save 5 years of living expenses in cash or Roth so that I can keep the MAGI below the 138% fpl (or close). This would enable us to pay virtually no income tax or healthcare costs. What are your recommendations?

A few points that were missed above:

1. After the first 5 years, I could essentially pay no income tax since our expenses are less than the standard deduction. Convert the standard deduction of $25100 and live on $20000 per year (pulled from 5 year old Roth money). We could qualify for Medicaid or convert a little extra if we wanted marketplace coverage.

2. We have access to a 457 plan and can pull funds immediately with no penalty but this is a taxable event and increases our MAGI, so this is a potential source of money for the first 5 years but has healthcare and tax consequences.

3. We could get part time work during the first 5 years and also convert the 20k per year, but we would still run into the problem of a little higher income during these years to qualify for cheap insurance. Like you mentioned above, it sometimes makes sense to make more money even though you get additional taxes.

4. Our marginal rate right now is 12% (we also pay marginal rate of 5% for state). So, pre-tax saves us 17% today. As long as we don’t pay more than 17% for increased taxes and ACA premiums during retirement, then this makes mathematical sense.

Thanks for any input!

There are a lot of factors that could change things (age, size of IRAs, Social security income, etc…), also because household size =3, be sure you are getting the full CTC (Maximizing the Child Tax Credit (even without earned income) if applicable.)