A Conservative Weekend (Photo credit)

Some people thrive on jumping out of airplanes, climbing untamed mountains, or riding wild rapids. These same activities would stop the heart of many an avid Scrabble![]() player and crochet aficionado. Perception of risk varies widely… as every extreme sports fan knows, more than one person has died with knitting needles in hand.

player and crochet aficionado. Perception of risk varies widely… as every extreme sports fan knows, more than one person has died with knitting needles in hand.

This same risk spectrum exists in finance. Even the words we use belie our assumptions. Someone whose preferred method of saving for retirement is to hoard cash under their mattress may be labeled as “conservative”, whereas an investor with 100% of their assets in equities might be called “aggressive.”

These word choices are unfortunate. Obviously if I don’t enjoy jumping out of airplanes into the rapids of a high mountain river in a kayak, then I must be conservative… I wonder how many investors have been led astray by nomenclature.

This is all vary strange, because I enjoy jumping out of airplanes and riding wild rapids. But when it comes to our retirement I’m extremely risk averse.

I’m not alone. Nobody wants to be destitute in their old age, so like bad television news we focus on the negative, the failures, the worst case.

“Is the 4% Rule unsafe?” “What does safe mean anyway?” “Should I work One… More… Year…?” “Should I go for a 3% withdrawal rate?” “Do all of the very vocal & very risk averse people in some online early retirement forums know something I don’t?”

Probably not.

Instead of focusing on all of the potential failures, just for fun let’s look at what happens when everything goes right. What would have happened if we had retired in 1982?

Accumulation and Preparation

As we explored previously, the decade or so before 1982 were financially challenging. High inflation, high unemployment, an oil embargo, price controls, the “death of equities”…

Stock prices moved sideways for over a decade, losing significantly to inflation. Although bond yield was at an all time high and stock dividends were at a peak, inflation was eroding purchasing power by the minute.

For somebody in the accumulation phase, this was a mixed blessing. Certainly, low prices provided incredible buying opportunities; the Shiller PE10 ratio has not been lower since. But this economic environment provided little in the way of real return, making it more difficult to accumulate 25x annual spending in total assets.

This would be an emotionally difficult environment in which to retire early. Little positive has happened in the economy for too long and many have lost faith.

Not wanting to endanger your family’s future by retiring without sufficient assets, of course you do some research. You spend many evenings simulating portfolio longevity in cFIREsim. You seek out like minded people online and get a 2nd and 3rd opinion, and discuss your concerns about health insurance, raising a child, and paying for college. You even share all of your personal financial information with a random person on the Internet for a detailed Reader Financial Review.

And of course you discuss important topics with your spouse such as personal risk tolerance, margins of safety, and contingency plans.

Willing to bet on history and your analysis, you take the plunge and start spending 4%.

Best Retirement Ever

Interestingly enough, all of the worrying and planning was a colossal waste of time. 1982 was the best time to retire ever.

Spending 4% is surprisingly easy from any asset allocation. Income on a portfolio of 80% stock / 20% bonds is over 7% of assets.

S&P500 dividend yield is over 5.5%. 10-year bond yield is an amazing 14.6%, due to inflation averaging more than 10% per year.

It is hard to say if the Volcker-led fight on inflation is having an effect. Members of both political parties are calling for his impeachment, claiming he is destroying the small businessman, destroying the American dream, and destroying Middle America. Throughout 1982 the stock market continues its decline. Everything is a mess. Was retiring early really a good idea?

As summer comes to a close, the Fed announces it is lowering interest rates and President Reagan announces the recession has bottomed. Shortly after, the stock market takes off like a rocket. It ends the year up 23%.

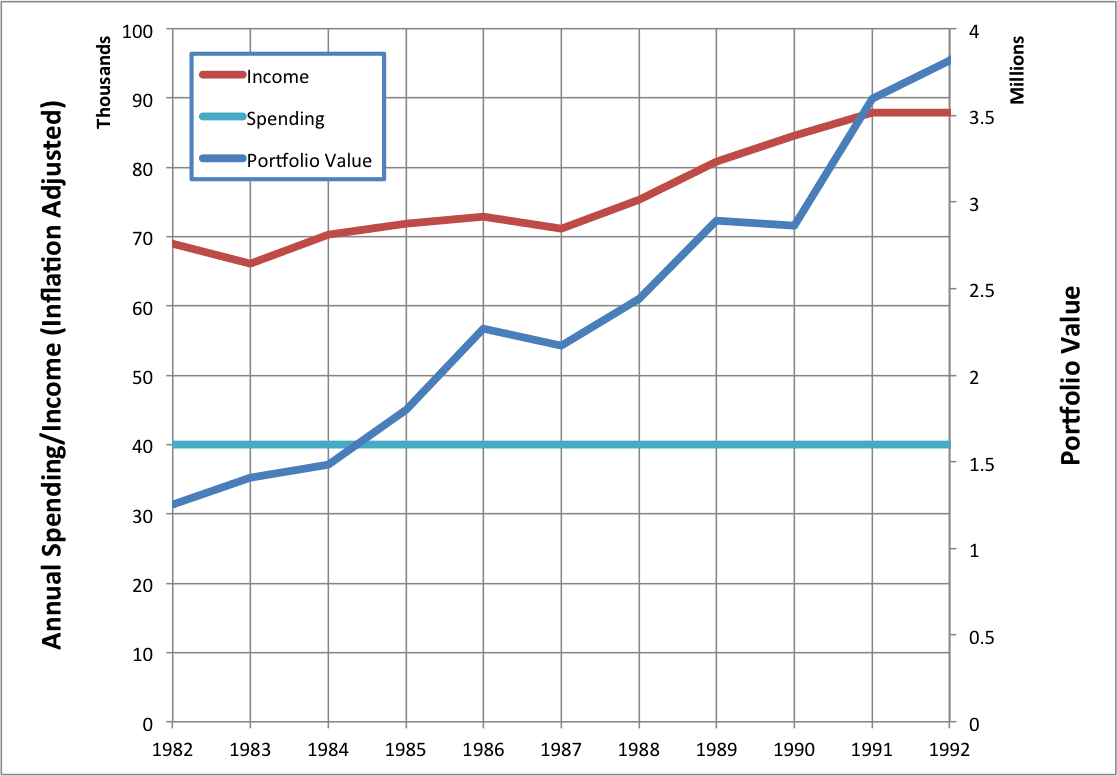

And thus begins one of the most powerful bull markets in history. Over the next 5.5 years the stock market rises 280%. Despite spending 4% per year, our portfolio has exploded to nearly 3x the starting value. Inflation appears to have been defeated, averaging less than 4%/year. Our target withdrawals are now just slightly more than 2% of the portfolio.

A few months later, on Black Monday, the stock market dropped 22% in a single day. Had we retired with $1 million in 2014 dollars, we would lose more than $500,000 dollars in a single day. Yet our total assets are still worth over 2.5x what they were 6 years ago, and we stay the course

2 year later, Savings & Loans Associations across the country start to fail. Thousands of these banks go out of business, costing taxpayers over $100 billion. The Doomers predict total economic collapse (again.)

And yet we would end our first decade of early retirement with nearly 4 times as much money. Income each year is much greater than spending, and we continue to accumulate assets.

The 1st 10 Years – $1 million 1982 starting value (Equivalent to $396k in 2014 $)

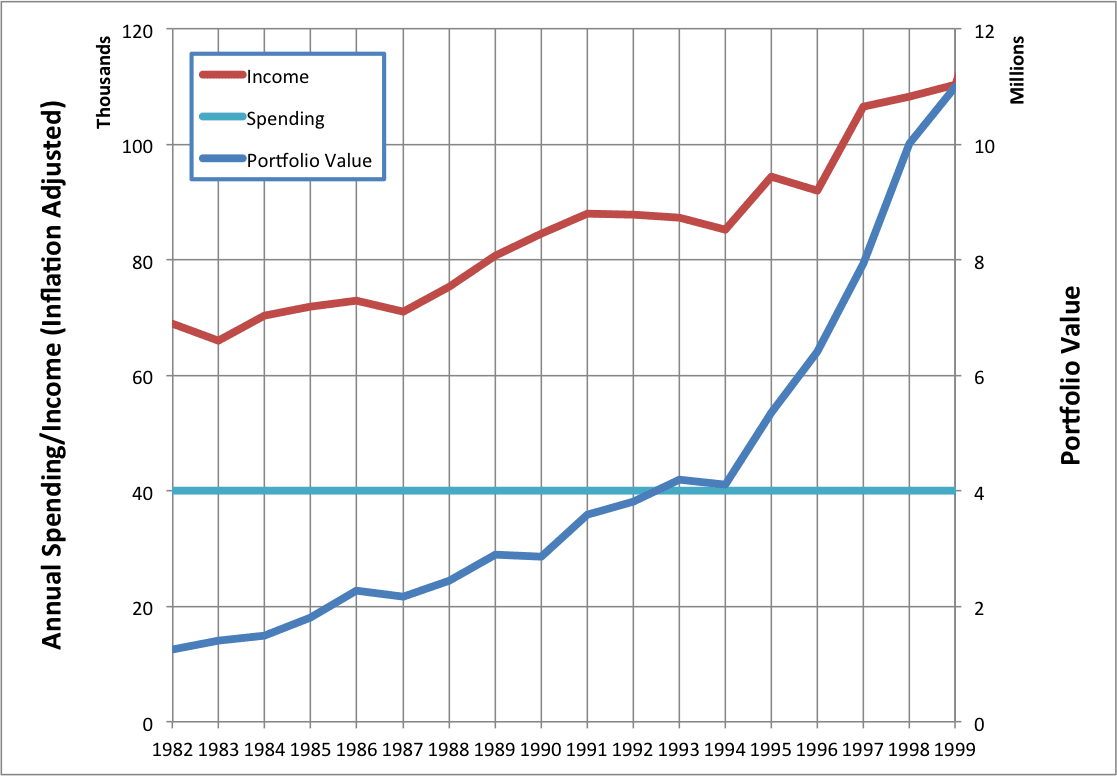

Over the next 7 years, despite increasing trade and budget deficits, hurricanes/floods/earthquakes/terrorist attacks, the death of Dr. Seuss, and yours truly graduating from high school and college, the portfolio nearly triples. Income from bond interest and dividends is nearly 2.5x our target spend

Things go south from here. The Internet bubble brings the lost decade in stocks. Interest rates plunge which brings the housing and mortgage bubble. Yield chasing charlatans

Things go south from here. The Internet bubble brings the lost decade in stocks. Interest rates plunge which brings the housing and mortgage bubble. Yield chasing charlatans![]() start selling collaterized debt obligations, laying the foundation for the stock market collapse of 2008. But with a withdrawal rate of less than 1%, we’ve long since stopped paying attention. And yet, our net worth continues upwards to unprecedented levels. Up, up, and away.

start selling collaterized debt obligations, laying the foundation for the stock market collapse of 2008. But with a withdrawal rate of less than 1%, we’ve long since stopped paying attention. And yet, our net worth continues upwards to unprecedented levels. Up, up, and away.

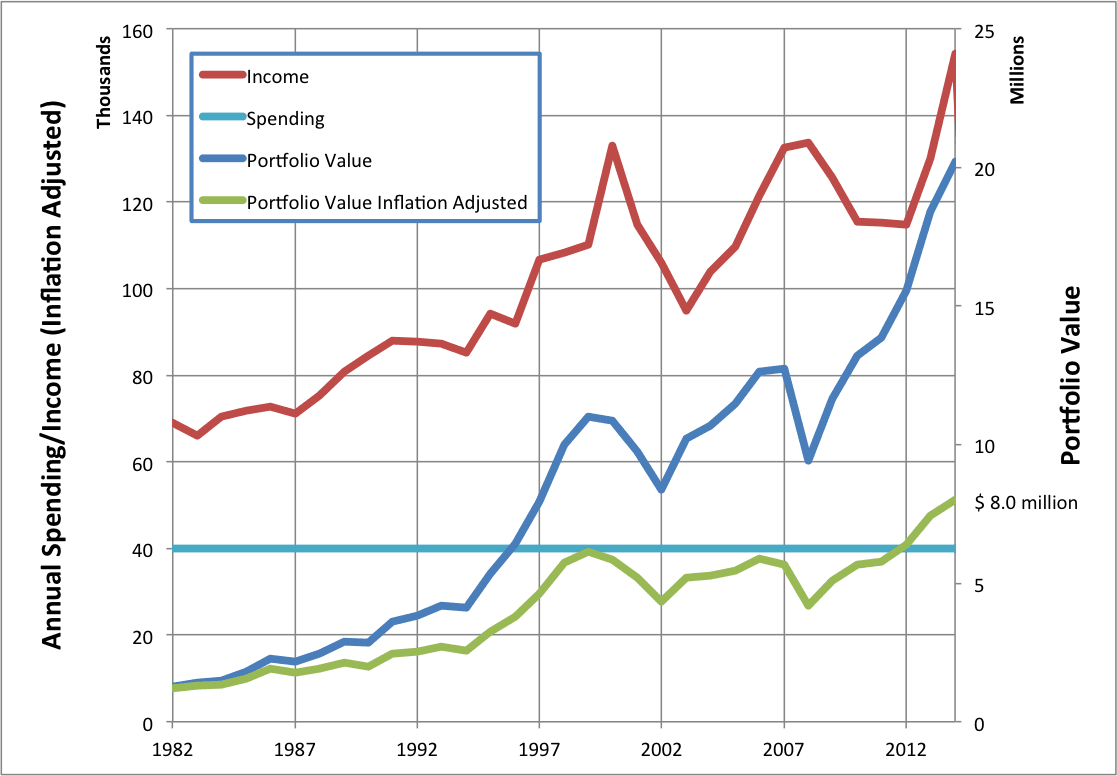

Sometime soon we’ll need to start thinking about how to benefit our fellow humans with this ridiculous pile of cash.

Sometime soon we’ll need to start thinking about how to benefit our fellow humans with this ridiculous pile of cash.

What if…

Investment returns were so strong over the past 33 years, that we could have spent an inflation adjusted 9.5% of the starting portfolio value, and still have the same purchasing power as when we first retired.

There isn’t much to worry about when everything goes your way, much like being born the son of Frederick Trump. That advantage is HUUUUGGGEEE.

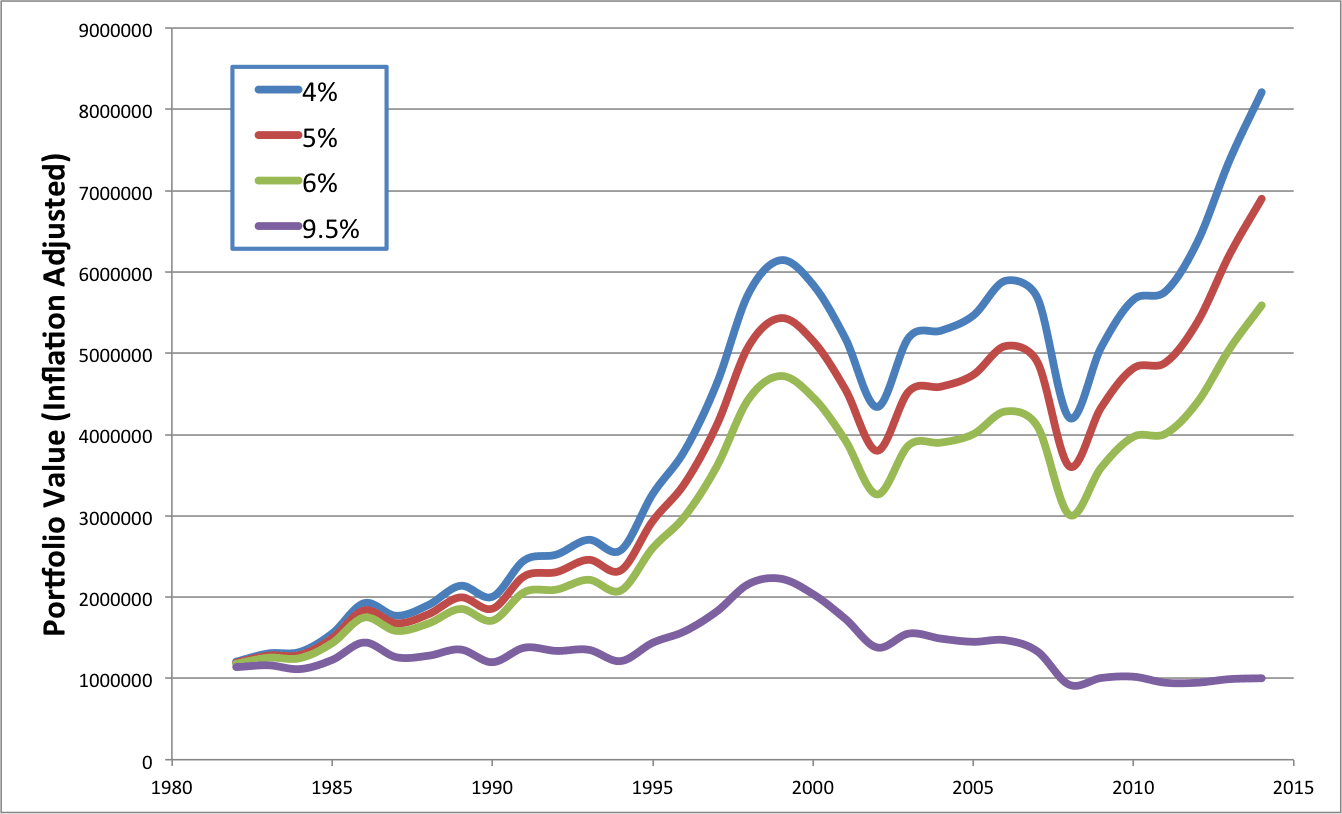

Inflation Adjusted Terminal Value with Withdrawal Rates from 4% to 9.5%

Maybe the opportunity to spend more is an exciting prospect. Or the alternative… you could have stopped working with less than half as much savings. Wild!

Conclusions

Although spending 9.5% was something that worked only once in recorded history, I’m sure some aggressive souls may be willing to give it a try.

I’m not so bold. But imagining what it was like to live through the extremes… what happened in the worst case and what happened in the best… helps me feel comfortable in the middle.

And being comfortable with the plan is really what makes for the best retirement ever.

See All of Your Accounts in One Place

Track your net worth, asset allocation, and portfolio performance with free financial tools from Personal Capital

It’s very tempting to live on that 9.5% spending line but I’m feeling a lot safer (and smarter! and good looking!) gliding along the 3-4% line, knowing I can increase it over time without blowing up the ER portfolio.

When I run the FIREcalc and cFIREsim calcs, I always like dreaming of those huge upward deviating lines like the one starting in 1982 where I end up with many millions or tens of millions more than I ever need. Although I know the median is closer to where we’ll end up. That’s still not a bad spot, with the portfolio tripling or quadrupling in real terms over 40-50 years in spite of spending 3-4% of it each year.

Similar to Justin, I operate under the assumption that the upside will take care of itself. It is up to me to manage the downside. I ask myself – What Could Go Wrong -) and I create a plan to address various scenarios. I also operate under the assumption that the future results will be and could be different than the past. Hence why I think exclusively off a 3% yield in my world ( or a 3% withdrawal rate in your world) is safer today.

On a side note, Gillete Edmunds wrote a book in 2000 where he discussed how he retired in 1981, and has spent something like 10%/year since then.

How To Retire Early And Live Well With Less Than A Million Dollars

Since 2000 he has written several books, and I think manages money now.

He did discuss getting divorced, which is equivalent to selling after a 50% drop in the market.

Yes the Edmunds book is the best ever treatment of early retirement and practice of money management. I have read and reread that book 5 times with 5 different high light colors.

We’ve decided that no matter what all the calculators say, or how much other people agree that we should be ok, it all comes down to how comfortable we are with choosing to live this lifestyle, when we “retire early.” We also found that flexibility is king, because even with minor tweaks to our allowances, or adding in even $5k/yr part time income, we’re batting 1000! That’s all in our scenarios of course and they could all fail just the same, but we’re not above seeking part time work, and expect we will both have some sort of work with income coming in to supplant our savings.

Even with Mrs. SSC most likely getting laid off in 3 weeks we think we should still be able to pull the trigger around 2018 if other things stay the course. It’s all about flexibility though.

Love your detailed chart posts, and this is no exception. It’s definitely fun to think about all of our portfolios exploding, but I suspect most of us are like you: more conservative in what we’re willing to spend. Those who want to spend like crazy are not well-suited to saving up a million bucks or more at a young age. :-)

Great post. People let fear stop them from living the dream they saved so long for. Bad things aren’t going to stop happening, but if you stay the course and stay flexible on your spending and ability to earn some extra cash, people should be just fine.

I agree with all these comments on being flexible but for the FIRE crowd this is going to be the most problematic.

Most of the FIRE folks are frugal with their spending so there is limited areas to cut spending.

I think even the most frugal people can explain how they plan to reduce spending if necessary. I don’t know anybody that has zero extra stuff in the budget… maybe go hiking and camping near home for vacation instead of flying somewhere, etc…

On the other side, people who spend 100% or more of their income have even fewer options

No need to cut spending as its already very very low. Mind you the standard of living is very high and the stress level is very low. Just dont buy anything you cannot pay for in cash.

Stay flexible, like you have said many times before. Key to Early Retirment.

As someone – at 44 years old & with 2 young children – with a decent pile of assets saved up, I feel the pull of both the joy of an early retirement and the never ending desire to add to that pile of assets. The “one more year” syndrome is quite powerful and it’s really difficult (at times) to envision retiring from a lucrative career at the peak of one’s earning power.

Lately I’m trying to think of this exercise as not the daunting task of planning for every contingency & spending decision in a single 40 or 50 year retirement, but rather as a series of 1 year retirements. By giving myself the permission to re-enter the work force, if necessary, at whatever level of employment is required, I feel I can give myself the permission to pull the trigger sooner. By thinking in terms of a 1 year sabbatical that can be renewed as long as things are going well, perhaps I can finally overcome the “one more year” syndrome and pull the trigger.

I’d love to hear other’s thoughts on this.

Maybe we can turn that “one more year” syndrome around to mean “…of retirement.” I’ve got awhile to get to that point but it’s definitely something I’m going to keep in mind from here on out while working that way. I’m an RN and hope to get to the point where I can take a travel-nurse gig for about 3 months of the year (aka paid to travel the country with family) and then enjoy 9 months of retirement at a time.

This is my first post on this site but I just have to say that I love it and find every post even more inspiring than the last. Dave Ramsey got my family on track, then I started reading MMM earlier this year, stumbled onto this site, and we’ve gotten on the FIRE train ever since. THANK YOU!

Choo choo! Full steam ahead!

My Mom and sister are both RNs, and they have both done well with travel nursing. There are some great opportunities there

The fallacy to this is that you might not find work after a big gap.

Is that a fallacy? Even $100/month increases the terminal value of a portfolio by over $100k. It isn’t necessary to return to an old career

It is in that the times one need the money is correlated with the bad economy. One might not be able to find minimal wage jobs when one needs the money.

I’m not worried at all. I’m beginning work on my Masters degrees in nursing and business and, as a licensed professional, I am required to stay up to date on continuing education to maintain my licenses. A nine month gap in working wouldn’t render my knowledge base useless. There are dozens of travel agencies all across the country (and even overseas) with dozens of job postings at any given time. As I write this, Fastaff has a posting for a Labor & Delivery nurse in Alaska for $60 per hour = $40,560 for 13 weeks of work. These assignments even cover living expenses, transportation, etc. One can quickly see how that can drastically cut down on the nest egg necessary for early retirement. Nursing is an incredible career with endless possibilities of paths to follow. And you could quite literally throw a dart at a map and find a hospital nearby that is hiring. Additionally, hospitals also have what are known as PRN (“as needed”) positions that essentially allow you to pick a shift or two per month to work. The opportunities are, quite literally, endless.

Jeremy,

While we don’t have cable and I wouldn’t watch The View even if we did, I hope your mom and sister wear their “costumes” and “doctor stethoscopes” proudly just like me…lol.

The most important period for predicting portfolio longevity is the first 5 to 10 years. If the stock market does well in those years, your portfolio balloons. If it doesn’t, then you are probably still OK but depending on personality it might be emotionally challenging

It is this idea that inspired me to write the Best and Worst retirement posts, as a way of thinking about how I would respond to the different environments. Giving yourself permission to work for an income is a fine way to move forward. I explored that a bit in this post.

I love this idea. I think this may be my new way of thinking.

Mike, I feel you are on the right track. Just dont buy anything that you cannot pay in cash. Get your kids into good public schools and colleges close to home

( to avoid costs) and save enough to pay for the same.Hope your house and car is paid for….

I’m recently FIREd and I like that mindset – renewed one year sabbaticals!

Jeremy you seemed to have forgotten the word “Just” in your statement: “Should I work ____One… More… Year…?” :)

We are struggling with this very subject, becoming comfortable with a 3% to 4% withdrawal from our retirement accounts. I know the math and history tells us that we should be fine, but fear does rear its ugly head!

My plan is to actually be at a point where we can live comfortably off only our passive real estate income, and everything else is a bonus. Essentially a 0% Rule. I know this is way too conservative approach, yet it is something we can do next year. We should be able to survive anything except a nuclear attack!

So I did. What was I thinking!? ;)

It sounds like your plan is about as robust as they come. But what if there is a nuclear attack followed by a zombie apocalypse?

D’oh! Now I have to prepare for the zombie apocalypse! I had completely forget about that possibility. There is probably a calculator out there on the internet that will help me with that one….. :)

If one looks at the online retirement calculators, such as the one provided by Fifdelity: https://www.fidelity.com/calculators-tools/retirement-quick-check, or the new calculator from Personal Capital, it appears that they prescribe a safe withdrawal rate way less than 4%. I think it is closer to 2%. Any thoughts on that?

I haven’t used either calculator, and can’t say what assumptions are being made

I think another little element here is as you are going along to continue to increase your accumulation phase, particularly when the market goes down. Holding a little powder back for those times (e.g. putting a little in cash in your 401k or Roth IRA) can create even greater PPP later on. Love the post though. Excellent dose of reality.

I think most studies show that holding cash reduces total return. You get to buy more shares at an unknown point in the future, but you lose all potential gain before that date.

This was a fun read. A 9.5% SWR is crazy. I’m certainly not going to plan on 9.5%, but ending the first decade with 4x the money would be really nice :)

Statistically speaking, having more $ at the end of the first decade is more likely than having less. History is on your side :)

You are totally right. So many people fret about the “what ifs” but they forget one of the what ifs is their portfolio continues to grow at a rapid rate even with 4% WR. Take these scenarios and then the couple of scenarios where the plan fails, and I’m happy sitting in the middle (once I get there).

Most of the Trinity Study 30-year periods with 4% withdrawals have terminal values greater than the starting value. 4% is super conservative

I think a key takeaway for me was that even in the “best” period to retire, a lot of seemingly bad thing happened, markets fluctuated, etc.

This is one reason I don’t watch television

Great read. The funny thing, we drive ourselves crazy worrying about things that never come to pass. It was the same way when I was building my business. I sweated lots of things and it all worked out great.

Only if I had all those hours of worry back… :)

Love your focus on the upside, as we risk-averse humans are typically hyperfocused on the possible downside.

I think the biggest possible downside comes from dying at the office. How is that for being positive?

“I think the biggest possible downside comes from dying at the office.”

I’m going to remember this quote every time I start to worry about my funds lasting!

You guided Tunnel Shoot on the MoFo? For real? Financial Independence and a Class IV Boater? Mind blown over here.

I have done class V, V+ on the Gauley River in WV, but this photo is not of us.