Retirement Ahead – Do You Have Enough Gas? (photo credit.)

When a sign on the highway states Next Gas Station 167 Miles, the ride is a lot more enjoyable when you know there is enough gas in the tank. “I think we can make it” doesn’t quite cut it.

The 4% Rule tells us if our Retirement has enough gas, but we don’t know if we will coast into the next gas station on fumes or if we have enough to drive across the entire country without refueling.

As life expectancy continues to increase and the ERE movement sees people expecting 60+ year retirements, there is need for an improved withdrawal plan.

In this post I outline my own thinking on how to ensure our portfolio lives longer than we do.

The Trinity Study that birthed the 4% Rule defines success simply as having more than $0 in 30 years. But $1 and $100 million are both more than zero. Are both outcomes equally successful? I think not.

Clear boundaries and outcomes make it easier to assess risk and make investment and spending decisions.

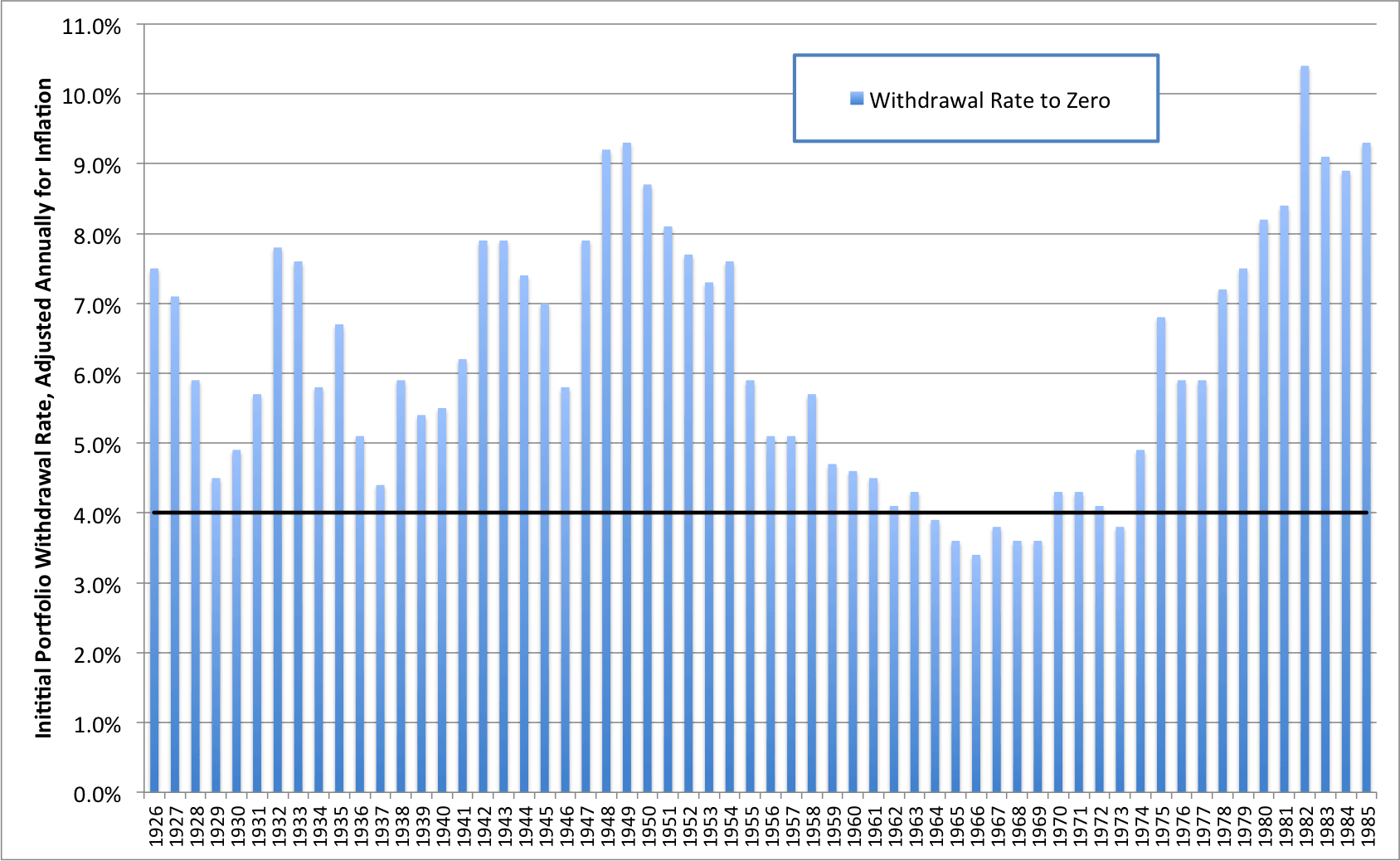

First, I sought a clear upper bound on spending, one that would guarantee the last check bounces. What withdrawal rate would have resulted in a portfolio value in 30 years of exactly $0?

In 9 out of 10 cases for a 75% stock / 25% bond portfolio, this is greater than 4%.

At lower levels of spending the portfolio would have lasted longer than 30 years. But how much longer? It isn’t clear, and in fact some of the “successful” 30 year retirement periods in the original Trinity Study would fail if the portfolio had to support an extra 10 or 20 years.

At lower levels of spending the portfolio would have lasted longer than 30 years. But how much longer? It isn’t clear, and in fact some of the “successful” 30 year retirement periods in the original Trinity Study would fail if the portfolio had to support an extra 10 or 20 years.

This is a difficult question to answer, in part because we only have about 150 years worth of data for modern stock markets. Further complicating things, for time frames longer than 30 years the data starts to lose credibility; the last consecutive 60-year period we can study began in 1955, long before anybody dreamed of Collateralized Debt Obligations or Quantitative Easing.

To address this problem, I took inspiration from Endowment Funds such as those Harvard, Yale, and MIT use to fund ongoing operations. What withdrawal rates would result in a future real value equal to the initial portfolio value? If the portfolio had a starting value of $1 million it would have a final value of $1 million when adjusted for inflation.

Short term investment returns are highly volatile and will cause frequent and significant dips in portfolio value. Even over time frames as long as 25 years, in several cases a portfolio would have lost purchasing power even with zero withdrawals. But if withdrawal rates are low enough, over a 25-30 year time frame the portfolio can recover to its initial value.

With relatively constant purchasing power over long periods, the portfolio would function like an Endowment Fund in Perpetuity and support a Forever Retirement.

In clear red and blue we can gleam a few interesting insights:

In clear red and blue we can gleam a few interesting insights:

- The gap between a 30 year and a Forever Retirement is small in most years.

- The delta gives us clear guidance for degree of austerity required if we are trending towards failure (10% for 1982, 35% for 1965)

- A case study of the Worst Retirement Ever shows what this looks like

- The delta gives us clear guidance for degree of austerity required if we are trending towards failure (10% for 1982, 35% for 1965)

- In 7 out of 10 cases, 4% withdrawal rates involve working too long. Those are much better odds than Vegas.

- Striving for a withdrawal rate less than 3% is certainly going to involve working too long

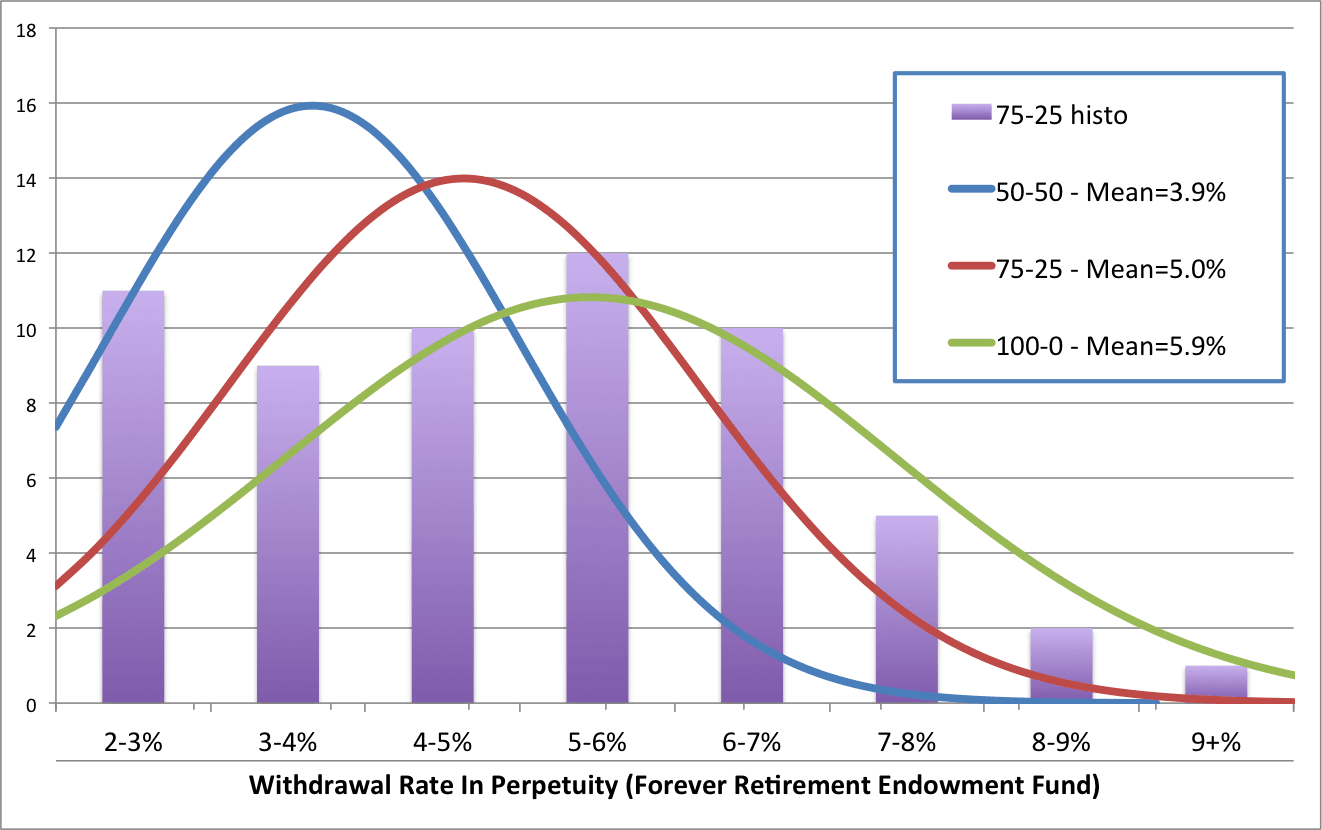

To seek further truths I dug out an old copy of How to Lie with Statistics![]() and a free license for StatPlus:mac LE.

and a free license for StatPlus:mac LE.

This isn’t a perfect normal distribution (if withdrawal rate is < 0%, it is no longer a withdrawal rate) but the distribution provided a convenient snapshot of a large amount of data. Statistics are your friend, and help reduce emotional decision making.

This isn’t a perfect normal distribution (if withdrawal rate is < 0%, it is no longer a withdrawal rate) but the distribution provided a convenient snapshot of a large amount of data. Statistics are your friend, and help reduce emotional decision making.

Stock weighting appears to significantly impact the Withdrawal Rate in Perpetuity, albeit at increased volatility (note the fatter distribution of the green line versus the blue) and even withdrawal rates above 4% can be viable with a high degree of margin (consistent with the payout data for University Endowment Funds.)

Since our withdrawal rate is below the -2sigma / 95% threshold for our current portfolio allocation (90% stock / 10% bonds – on path to 100% equities), and we are more than willing to implement austerity measures via global arbitrage, it looks like I’ve created the Go Curry Cracker Endowment Fund.

At a point in the distant future, we’ll make that a legal commitment (When it has the greatest tax benefit, naturally.)

How Do You Plan to Build Your Own Endowment Fund?

—

In future posts, I’ll use this idea of a withdrawal rate in perpetuity to predict future withdrawal rates and how long it would have taken to build an Endowment Fund in various economic environments of the past.

This is more or less how I think of our portfolio. We only spend around 3 percent so it should grow in real value over time. We could probably spend 5 or 6 percent and be fine, but we don’t want to run out of gas half way through our trip! :-)

Continuing to LBYM is a sure way to join the Forbes 400. Race you there ;)

See you at the finish line!

Great article. After all the analysis, what percentage did you come to terms with? 4%, 5%, etc.?

It depends on your tolerance to volatility and ability to implement austerity measures.

With 100% equities, historically a 5% withdrawal rate would have a 70% chance of withdrawals in perpetuity. Add some geographic arbitrage to the mix, allowing substantial spending cuts in major recessions, and you could goose that to 95%

I’m really conservative though, and spend less than 4%, which gives us a 99% chance of the portfolio growing in real value over time. I hope to leave behind a nice charity

I don’t think I understand your red/blue bar chart then? It looks like there’s like 8 instances of failure even as low at 3% perpetual withdrawal rate?

If you start with $1 million and die 40-50 years later with $500k, I wouldn’t call that failure (but not perpetual…)

This is another (better?) way to look at it: You will die before you run out of money.

Got it. Thanks. It’d be good to know at how many years in the “perpetual withdrawal rate” failures happened. I’ve got a portfolio similar to yours, 90/10, and at 31 and 3.5% withdrawal, I’m hoping this “income” lasts my lifetime.

I’m hoping too, which is about all we can do since the future is unknowable.

However, we can learn a lot by looking at the worst time to retire in the US (1965.)

If you retired in 1965 with a 90/10 portfolio and blindly/robotically spent 4%, the portfolio would have failed in 26 years. If you spent 3.5%, the portfolio would have failed in 45 years (2010) and been an unpleasant ride. If you add basic Social Security at age 65 ($1k/month) and spend 3.5%, the portfolio would still be worth ~$250k (inflation adjusted.)

If you haven’t already, experiment with cFIREsim. That is where all of these numbers come from.

Brevity may be the soul of wit, but this article could’ve used some footnotes! What exactly was the methodology for determining the “Withdrawal Rate in Perpetuity”? Is it the withdrawal rate that leaves the portfolio’s real value unchanged at the 30-year mark?

Yessir, at the 30 yr mark.

My apologies, I broke this monster piece into 3.

Gotcha. This is a great way of thinking about portfolio survivability.

Also, the gas tank analogy perfectly captures what I’ve always thought when an early retiree (using 20/20 hindsight) says they “worked X years too long.” Retiring with exactly enough gas in the tank (working zero years too long) may get you to your destination but could make for an anxiety-filled trip.

I’ve made that exact statement. I knew I worked 3 years too long (saving 100% of income) but in hindsight it was more like 7. I sleep well though, so no worries

Foot notes:

– I wanted a better way to plan for a 60 year retirement with the limited data with sequence of returns analysis. Withdraw in perpetuity provides that

– I wanted a better pass/fail test, so two boundary conditions: withdraw to zero and withdraw in perpetuity. The latter is a better upper bound than infinity

– Early retirees also say “be flexible” and “spend less in down years.” The ratio of withdraw to zero and withdraw in perpetuity provides perspective on how much less spending would be necessary

Thanks. Could you provide more details on the data behind the WR in Perpetuity bar graph? Are the results replicable in cFIREsim (or did you use a source with different underlying data)? Do these figures reflect investment fees (and, if so, what is the assumed MER?)?

I used the Shiller data, same as cFIREsim, but I did the analysis in Excel. I compared a few samples to cFIREsim, it should be fully repeatable

I use 0% fees and 0% taxes, and instead include those in total spending

Hi Jeremy + Winnie,

I really like your perspective, and I’ve got a million questions. But I think there are 2 relative to this post, and they will help me with math.

1. When you take out investment money for the year? In the beginning, all at once, or do you sell off a bit each month? (I’m not sure how the trading works, so this detail is very interesting to me)

2. What do you do when there is a likely market correction (like now, or last week) happening, or pending? Are there any smart defensive measure the will help your portfolio last longer?

The questions above might be worth separate post, as i’m sure readers would be interested. And if you’ve answered them already, please point me there. I’m so curious about your thoughts and methods, especially during bear markets. Which, might not be the case now, but certainly it can happen in the future. Thank you.

Hi Antonius

For #1, see this post: https://gocurrycracker.com/cash-flow-management-early-retirement/

Re: #2, I won’t really pay attention unless the market drops 25%. It is fun to watch the reactions on social media though

If a 25% drop happens, then I’ll move 1/2 of our bond position into VTI. If the market drops another 25%, I’ll move the other 1/2, https://gocurrycracker.com/reminiscing-about-the-glory-days-of-2008/

Also see this post about managing the portfolio through a severe recession

https://gocurrycracker.com/the-worst-retirement-ever/

Jeremy,

Thank you for the reply! I’m glad to see that you would double down. I was thinking along those lines, but for a second there I thought that I was crazy. MAYBE NOT SO.

Do you have a rule of thumb about moving back into fixed income. Would a rate greater than 5% have to be the case, or is there something else that would dictate your asset allocation?

your theory (or way of thinking about this) would be of interest, since I imagine that things can be very different 10 years from now.

You’re a genius BTW. But don’t let that go to your head. Thank you for making it happen and sharing with the world some of us hamsters on a wheel. ;)

I probably wouldn’t move back into bonds (ever) unless the government started selling TIPS or iBonds with guaranteed 3%+ real return. I just have the bonds to reduce the volatility in case we retired into a down maket

Crazy or genius… we’ll have to decide in 10 years :p

University endowment funds are continually recharged by donors (responding to those begging letters that come regularly to alums), which I suppose it like working part-time or inheriting some money – it just increases the pile.

I need to get some donors

Put a PayPal button on your site and there ‘ya go…

Maybe I should be more comfortable planning around a 4% SWR. I also have not planned to earn income once I am FI, which I actually definitely think I’ll earn at least a little. This will definitely help pad the plan and make sure I don’t run out of gas. Great perspective.

4% is pretty robust, historically. 9 out of 10 samples, it lasts longer than 30 years. 7 of those 9, the portfolio grows larger than the initial value. Add some spending cuts in severe recessions and it is as close to a guarantee as one could find

I don’t know why more people don’t talk about that. If your at all living within your “retirement means” you can certainly adjust spending up and down, or bring in some level of income if necessary.

I doubt the study has been done, but if you modulated your withdrawal between 3% and 5% depending on the market I would bet you get essentially a 100% safety level.

There are a handful of Variable Withdrawal methods that attempt to do just that.

Wade Pfau published a summary of the various methods earlier this year:

http://retirementresearcher.com/making-sense-out-of-variable-spending-strategies-for-retirees/

My portfolio generates dividends that I plan on spending in retirement. Dividends are always positive, and more stable than capital gains, which make them ideal for living off a portfolio in retirement. I will let the capital compound since I won’t be selling, and it will provide shelter/income for future DGI generations and DGI causes once I am gone.

For my endowment trust, I looked at Hershey Trust for inspiration. They own a large portion of Hershey (over one-third), and have been spending the dividends for several decades now. They are not too diversified however, but nevertheless have managed to live off that dividend income and spend it on charitable endeavors.

Thanks for the DGI perspective, DGI

Do you plan for possible dividend cuts, such as the elimination of a lot of bank dividends in 2008?

I plan on having dividend income that exceeds expenses – a margin of safety in financial independence a sort of way (i linked to it under my profile name). So if I spend $1000/month, I need income of say $1200 – $1300 before I call myself FI. My dividend crossover point will be around late 2018, so I still have the luxury of accumulating assets.

I expect cuts in the energy sector. But I also expect dividend increases from other sectors to offset the cuts.

Funny thing is that in a diversified portfolio, other sectors compensate with dividend increase for the lost income from one sector cutting dividends (like banks in 2008). Many companies that had raised dividends kept raising them in 2008 and 2009 – others just left them unchanged.

And if I sell a stock that cut dividends, and purchase another one that pays a dividend, I can end up maintaining or even increasing my dividend income in the process ( and getting a tax loss to harvest in the process).

PS As you are well aware, once you get to be in “retirement/FI”, you have plenty of free time to pursue what you are truly passionate about. For many, this results in earning incidental money in the process. You are a prime example, so is your friend MMM (I would be friends with him except that I have never met him :-( ). I have different publications that want me to write articles for them, but I have been declining that.

The Y axis on the third graph is unlabelled, making it hard to understand. Thanks.

Sorry for the confusion Professional Gypsy

There are 60 sample years in the extended Trinity Study data set for retirements starting in the years 1929 to 1985, the same years shown in Graph 1 and 2.

The y-axis in Graph 3 is the bins of the histogram (# of years that fall into each withdrawal rate bin.)

Graph 3 has me stumped too. Now that I know what the y-axis is, I’m trying to understand what the 75-25 histo data has to do with the line data. help?

Also with the 75-25 histo data, does it mean I ought to be able to find 11 instances in Graph 2 where the read line stops between 2 and 3 percent?

Thank you for your effort on this. It is of keen interest to me as I am in the second year of my early retirement and trying to wrap my brain around how best to internalize the recent mini-correction. In addition, I want to be able to understand WHEN the trigger is for pulling back on spending. That part has me stumped.

> with the 75-25 histo data, does it mean I ought to be able to find 11 instances in Graph 2 where the read line stops between 2 and 3 percent?

– Yes, exactly. Most of them are in the 1960s and closer to 3% than 2%

The line data is a normal distribution best fit to the bins, and is just another way of looking at the same data. The key takeaway is that higher stock percentages shift the mean of the withdrawal rate in perpetuity upwards, and that a 4% withdrawal rate is really conservative

As for recent short term market activity perspective:

http://www.fool.com/investing/general/2015/08/24/what-happens-next.aspx

My response to the last week is the same as it was the week before: Nothing. If anything, in a few months or so you can look back and realize that the market gyrations had zero real impact on your life. That is a good life lesson. Although at this early stage, you could even hope the market experiences a real decline. 50% off would be great, wouldn’t it?

There is no clear cut answer for if or when to cut back. I would minimize the selling of stock if there is a major decline in the first 10 years. See this post as a thought experiment on that idea:

https://gocurrycracker.com/the-worst-retirement-ever/

This is a top of mind topic for me that correlate with finding my retirement number. I too have been taking a conservative approach of considering a 3% to 4% annual withdrawal rate.

We are considering a scorched earth perspective of never working again with the possibility of our other passive income sources taking hits. The probability of those items all happening at once are remote, but evaluating the consequences helps us plan and sleep better at night.

If we can live through market corrections, real estate issues, or no other part time income to cover our living expenses with passive income, then we are ready! :)

Thanks for the article! I still need to read more about the withdraw rate and how long will the investment last.

So I just joined the long term taxable investment after being educated through your website and JLcolin’s stock series, opened the vanguard account 10 days ago. Now with today’s market plumbing, I’m in for the rough ride already!

The good news is since you are just getting started, the lower the price the better!

Unfortunately I put almost all my available savings in 10 days ago already($135K), between total stock and total bond, With yesterday’s plumbing, its down to below $134K already. That’s why I’m feeling the tough ride already!

I’m thinking of putting the little extra in since it’s good chance to buy now. I’m hesitating to invest into the same Vanguard stock/bond accounts for purely mycompany stock (GEC) as the company stock has dropped more. Do you have any input on this?

Also, I want to discuss with you about tax reduction. I have a rental property that right now bringing more rent than the expenses and mortgages interest and property tax combined. I rent right now, so no mortgage write off beside the rental property. I maxed out 401K, HSA, not qualified for deductible IRA. In searching of any way to reduce tax, I have been researching the pros and cons of home equity loan. I have probably can borrow out up to $120k from the rental property. But by running the numbers roughly, the reduction in total tax savings over the loan term may be less than the interest I pay to the bank. But if I invest this loan, it would be different. I haven’t run that number yet. Just wondering if you have run into a similar situation or have some suggestions on Home Equity loan being put into long term investment (10 year or so)?

Sorry for having too many questions! Hope all is well with all three of you!

It is a marathon not a sprint, I would just ignore the market completely if you can. See today’s post for more: https://gocurrycracker.com/exposure-therapy/

I wouldn’t have very much of your portfolio in your own company’s stock. See Enron

Don’t let the tax tail wag the dog, meaning don’t borrow $1 just to save $0.25 in taxes. If $1,000 of volatility sets off alarm bells for you, I also wouldn’t buy stocks with debt under any circumstances.

Jeremy,

Thank you for the suggestion! Definitely the tax deduction is a deceiving wagging tail. In the long run, the bank definitely gets more from the interest.

I was wondering why you said $1000 volatility, then I noticed all the typos/errors in my original post. I meant to say my total stock/bond was down over 10K, not just 1K. Sorry for all the typos and errors. I know how much I hate to read and guess things myself.

$1k or $10k, on a 30-year time frame it is all the same. Keep saving

Aside from the questionable issue of leverage on a property to invest in stocks, If I’m not mistaken, a heloc on a rental property does not qualify for tax deduction since its not acquisition debt. Check with your accountant or tax preparer.

You are right, a HELOC is not tax deductible, but a 2bd loan is.

Susan,

To my understanding, that is not correct. Interest on a loan on a rental property is only tax deductible if the proceeds of the loan are used to purchase, improve/repair the rental property, or for approved expenses on that rental property. Using the proceeds of the loan as capital to invest outside the rental property does not qualify. http://www.nolo.com/legal-encyclopedia/deducting-interest-rental-property.html

Again, be sure to check with your accountant!

That’s true, I did read on the restrictions on how to use the 2nd loan. I’m going for that route anymore, so I didn’t research more about the taxiable issue when using it as investment. Thanks!

Love this. It’s very similar to how I think about our finances. Thinking like a trust is the way to go. Of course you need a benchmark to give you an idea of how much is enough, but tweaking your spending is always an option once you pull the trigger. Flexibility is key. I saw above that this is the first post in a series. Looking forward to the next two parts.

Also, writing the above made me think of “Your father and his tweaking!!” You guys Arrested Development fans? Cheers.

I don’t think I’ve seen Arrested Development. I’m waiting for the next season of Game of Thrones and The Walking Dead

Nice.Well AD is worth your time if you want a well-written comedy sometime.

Good to see you are planning to “Give Like a Billionaire” Thanks for the link!

You might also consider following Warren Buffett’s path and giving your money to a close personal friend. In his case Bill Gates.

For what it’s worth, I’ve always thought of you as Buffett to my Gates…. ;)

I pictured more of a Cheech & Chong or Laurel & Hardy kind of relationship

Ah, man. We just gots to aim a little higher….

Thanks for considering retirements beyond 30 years, since most articles like this are silent on that rather important matter. The math is probably too complicated, but I notice that a lot of retirees on Early-Retirement.org either spend from cash reserves in downturns (meaning also that they are not 100% invested) or generate spending cash from their appreciated asset classes when they rebalance. Do you think those strategies would make a difference in portfolio longevity? Most models seem to say “spend 3-4% of your portfolio” regardless of the underlying volatility of various asset classes. Thanks for your perspectives.

Yeah, the math in this one is a bit much. Maybe the key message is that even at a 4% withdrawal rate, most of the time the portfolio will last forever

We have about 3 months in cash. Maybe that means we aren’t fully invested either. Even a year of cash would not be a big drag on a portfolio. At a 4% withdrawal rate and 2% dividend payout, a year of cash might only be 2% of the portfolio +/-. If cash reserves become much larger, it would likely have a net negative impact on longevity since the cash is losing purchasing power to inflation each year

Filling the checking account from capital gains is a fine way to go. It would be a natural part of portfolio rebalancing. And really there is no difference between spending from capital gains or from dividends in an up market

I’m always thrilled to read positive articles about the 4% rule since 99.7% of them are overwhelmingly negative. I think I saw this one last week: Why you’ll go Broke, Poop your Pants and catch the Clap if you follow the 4% Rule. Can’t seem to find it now…

One thing that all of the Negative Neds never talk about is the other risk; that you buy the farm with $10,000,000 in the bank. If that happens, it means you either have a rich uncle who left you a windfall or more likely, you worked too long.

Worst case scenario for me? I retire at one of the few times in history when the rule doesn’t hold up. Then, I have to, wait for it: go back to work for a year! The horror. The horror.*

One thing I almost never hear the Negative Neds say is that the rule assumes no future income. Despite the people who claim social security is dead, (a subset of the above 99.7%), it is a sacred cow that will be diminished, but won’t die.

Man I’m long winded today, so I’ll shut up in a moment.

I believe that frugality is far more important than income. If you can get by on 40K year in that first year of retirement, it doesn’t take much to move the needle. Spending a very small amount of time driving for Uber or renting a room through Airbnb could easily turn the 4% rule into the 3% rule. Or like you, go live in Cuba.

Stay frugal my friends.

*For those who aren’t movie buffs, this is a shout-out to a film about the failure of the 4% rule: Fincopalypse Now

.Is it Rant Thursday already? ;)

I still appreciate the Negative Neds and Debbie Downers.

Somebody has to pay the taxes, and their Estates will be nice and ripe.

I also agree about SS. The SS deficit could be eliminated by a 16.4% reduction in benefits paid to beneficiaries (Social Security Trustees 2015 Report)

ps: Thankfully the clap can be cured with antibiotics

pps: I think I saw that movie, starring Benjamins Galore and Alotta Dollars

All of this confuses me to no end. So my husband (53) and I(40) are debt free. Have a home that is worth about $600k, $150K in a savings account and about $1.2milllion in stocks/401k. We have 4 teenagers that will need some help with college. His annual income is about $175K. WIth these basic numbers could we be retired now and live the same lifestyle according to your philosophy?

Hi Kourtney

As a rough rule of thumb, you need a minimum of 25x your annual spending in invested assets. With $1.35 million, if you are spending less than $54k/year you could be Financially Independent.

See this post for more

https://gocurrycracker.com/what-is-your-retirement-number-the-4-rule/

Thank you! That would be totally doable if we didn’t have 4 teenagers to support! We will keep working and saving with the peace of mind that we are on the right track!

I would add another consideration. You have not given us any information of your retirement, which should be a major part of your consideration. You are only 40, giving you a potential 50-60 year retirement if you retired now. In my opinion, this changes the numbers a little bit because the longer the retirement term there’s a slightly higher (yet still small) chance of “failure,” or running out of money. The way most advocates of early retirement rationalize the few chances of market downturn is by being flexible, such as dramatically reducing your expenses or living in less expensive environs (i.e. Mexico, Asia, etc.), or pursuing other means of income. Even if you could live on $54k, would you have flexibility to go even lower? Would these measures be something you’re comfortable with? Have you read about GCCs lifestyle in other countries and are you confident that these kinds of choices would be right for you? If you’re not willing to significantly reduce your expenses, what skills and background do you or your husband have that can assure you that you can work if you need to (remember, during tough times in the stock market the job market is also often tight). If not, even if you have no kids and could live on $54,000/year, you still should work a few more years to give yourself more of a safety margin.