Should I invest in International stocks? If so, what percentage of assets should be invested internationally?

These are important questions to answer when deciding on a target asset allocation.

This is how I thought about that decision.

Should I invest in International Stocks?

Like most investing questions, there is no right or obvious answer, except after the fact. And we can rationalize any decision we might want to make…

For example:

The United States prints the world’s primary reserve currency and is the world’s largest single market. As of Dec 31, 2018, US corporations were worth 54% of the total global market cap (source, big pdf.) California by itself is the world’s 5th largest economy, and the 10 largest companies are all American. Interesting (to me), the market cap of many US corporations exceeds the market cap of every publicly traded company in many developing countries (selling toilet paper and diapers is worth more than all of the oil in Russia, for example. Kleptocracy has a price.)

(I found this on Reddit, apparently via BoA and The Economist)

What’s more, US corporations are truly global, generating 40%+ of revenue outside the US. And growing. A lot of people use iPhones outside of Kansas and South Dakota, and I occasionally enjoy a double vente Frappuccino with extra whip here in Taipei.

(source, from 2012, big pdf. Somewhat corroborated by data from 2017.)

Furthermore, as a US person who eats, sleeps, and breaths in US dollars, investing in Euros or Pounds Sterling or Yen or Dong brings currency risk. When the USD rises, the value of International investments falls and vice versa. Do you want the poor financial choices of other countries to impact your personal inflation rate?

And last but not least, the cost of International investing is higher. International funds generate more non-qualified dividends, which are taxed at higher rates, and the expense ratio on VXUS is 13 basis points higher than on VTI.

Based on all of the above, it is understandable how many notable individuals recommend a portfolio invested 100% in the United States.

“Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.)” – Warren Buffett (in his will, as a recommendation for the money left for his wife.)

“I wouldn’t invest outside the U.S. If someone wants to invest 20 percent or less of their portfolio outside the U.S., that’s fine. I wouldn’t do it, but if you want to, that’s fine.” – Jack Bogle, himself (may he rest in peace)

“Since these companies (US corporations) provide solid access to the growth of world markets, while filtering out most of the additional risk, I don’t feel the need to invest further in international specific funds.” – JL Collins, the godfather of FU money

Simple is good, simple is nice. I fully support anybody who chooses to invest 0% Internationally.

But we don’t do this.

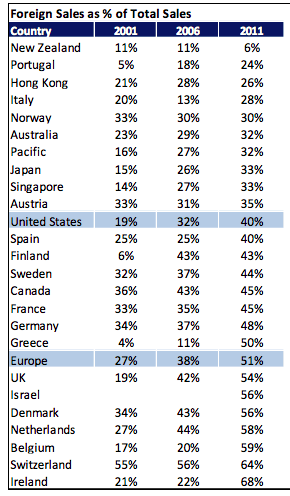

Home Bias

“Bah, you Americans are all the same… so arrogant, thinking you are the center of the universe.” – lots of people

Touché. “Home bias” is the phrase commonly used to describe being overweight your home country in your investment portfolio.

Consider:

- You own Ford and GM, but what about the companies that produce the other 70% of vehicles sold in the US?

- The world’s largest cell phone provider by subscribers is in China.

- A not insignificant portion of what you feed yourself, your baby, and your pet comes from Nestle, a Swiss company.

Anybody care for a Nespresso?

![]()

As a fan of passive index investing, we simply own the entire US stock market through index funds. Boring investing is the best investing. Wouldn’t it make a little sense to extend this philosophy to the globe?

In doing so, an investor would own about 50% US stocks and 50% non-US stocks.

Some people do just that, and I fully support anybody who chooses to invest 50% Internationally.

But we don’t do this either.

Anecdotal Evidence

Everyone has their rationalizations for a home bias. Here are some from Jack Bogle (source)

“When you look at global market capitalization it’s true that the U.S. accounts for about 48 percent and other countries 52 percent. But the top three markets outside the U.S. are the U.K., Japan and France. What’s the excitement about there? Emerging markets have great potential, but have fragile sovereigns and fragile institutions.” – Jack Bogle

“It’s hard to believe that the differences in returns (between US & International) over the long term will be huge. That’s just not what we have seen for the most part. Why take the currency risk?” – Jack Bogle

Sovereigns and institutions are important. Courts and culture that enforce contract law, low instances of corruption and bribery, transparent accounting standards, and strong shareholder rights make companies more profitable and efficient. It can be difficult to do business in countries with systemic corruption.

Our overall economic system relies on growth, doing more with less year after year. A component of economic growth comes from population growth, in large part due to immigration. Where Immigrants go, economic growth follows. (Consider: your spending is somebody else’s income.) Historically, that has been the US.

Along with strong educational institutions, this leads to strong entrepreneurial growth. Nearly half of all Fortune 100 companies were founded by 1st or 2nd generation immigrants. Some examples include Google, Intel, eBay, and Nvidia…

Many of my own work experiences also encourage a home bias…

I recall a time when I was working closely with a Japanese company. The team proposed a solution via another Japanese company (owned by an Uncle) with a cost of $200,000, a lead time of 16 weeks, and a piece cost of $1.25. We offered an alternative solution via a Taiwanese company and a Chinese tool vendor for $25,000, 3 week lead time, and piece cost of $0.25. Which option do you think they chose?

In another instance, I was supporting a project out of Korea with a target shipment date of Thanksgiving 2005. The team was still working on the project in 2008 because the corporate culture rewarded managers for finishing a project. Trying to ship a 2005 product against the competition’s 2008 product resulted in sales of 2 units, to the manager’s parents. How much does it cost to run an engineering team of 100+ people for 3 years?

I could write another 100+ examples, but Paul Midler already did that with more humor:

![]()

Are US companies perfect? Of course not. More efficient? Maybe.

Is this an irrational and emotional perspective? Most definitely.

Data

It is interesting to hear people’s reasons for why they chose a certain US/International allocation. Some think the era of US dominance is over and overweight International. Others invest only a token percentage in far off lands.

I prefer data, to counter my own anecdotal evidence.

Vanguard, the company, has a different opinion (big pdf) than their founder. It concludes, in part (emphasis mine):

In light of quantitative analysis and qualitative considerations, we have demonstrated that domestic investors should consider allocating part of their portfolios to international securities, and that a 20% allocation may be a reasonable starting point. Although finance theory dictates that an upper asset allocation limit should be based on the global market capitalization for international equities (currently approximately 58%), we have demonstrated that international allocations exceeding 40% have not historically added significant additional diversification benefits, particularly accounting for costs. For many investors, an allocation between 20% and 40% should be considered reasonable, given the historical benefits of diversification

This snippet is backed by lots of data and charts, and carefully phrased and lengthy explanations.

Literally putting their money where their mouth is, Vanguard Target Date funds invest 40% Internationally in stocks (and 30% in bonds.) Betterment seems to follow Vanguard’s lead on this. (Why Betterment has zero of our dollars.)

Another interesting (data-driven) viewpoint comes from the Bogleheads wiki, where you can find this chart:

The data shows that between 1970 and 2007, holding any International stocks resulted in a greater return than owning US stocks alone. If that isn’t an argument for diversification and rebalancing, I don’t know what is.

With allocations of 10-30%, that higher return was earned with lower volatility. That looks like the sweet spot!

We discussed this a little on the GCC forum.

But…

I enjoy using a 40-year data set to guide decisions as much as the next guy, but… why not 50 years?

And so, I reverse engineered the chart and added data from 2007-2018. US data is represented by VTI / VTSAX and International by VXUS / VGTSX (about 80/20 developed/emerging, roughly market weight.) (Data from Yahoo and this Bogleheads forum post.)

Another decade changes things quite a bit.

The original data is shown in Blue, with the extended data shown in Orange.

Between 1970 and 2007, holding any amount of International stock resulted in a greater return. Between 2007 and 2018, holding any amount of International stocks resulted in a worse return.

Which is why I get emails like this:

Email: “Like you, I have a portion of my portfolio invested in International stocks, e.g. VXUS. Over the past decade or so, my US investments (e.g. VTI) have more than doubled. The International fund is not worth much more than what I invested long ago. Are you happy with the performance of the International portion of your portfolio? I’m considering ditching it altogether.”

Me: “VXUS has tracked its target index with high correlation and low fees. It is doing exactly what it is supposed to do, perfectly. So yes, I’m extremely happy.”

PS: Please don’t chase performance or try to time the market.

Plus, with a token percentage of 10-20% International equities, volatility was lower over the entire 50-year span.

The GCC Portfolio

Long ago, I did the mental gymnastics of choosing an asset allocation. I read the opinions, looked at the data, made some spreadsheets, mixed in my personal experiences… and settled on an 80/20 US / International split.

I can balance my anecdotal evidence and the opinions of highly respected US focused investors with the logic of diversification and index fund philosophy, and then point at the historical data and pretend I was being rational about it all.

According to Personal Capital, as of mid-January 2019 our portfolio looks like this:

This was explored in much more detail here.

We have been on the path to 100% equities for some time, and recently completed our annual rebalancing to an 80/20 US/International allocation, with a roughly 75/25 Developed / Emerging split (slightly overweight emerging.

What will be the right balance of US / International going forward? Dunno. But I think our portfolio has a nice balance – too little for Vanguard, too much for Buffett/Bogle/Collins, just right for me.

What is Your US / International Allocation? Do you have some entertaining anecdotal evidence?

Hey Jeremy! Thanks for the overview of the subject. One question I was still wondering about that perhaps you could address: How does the fact that you guys are such an international family impact (if at all) your decision as to US/Int’l breakdown? With so many stamps in your passport you have a more outward-facing perspective on life than most, I would venture to say. Does that come into play at all on this issue?

Hi Sam.

It doesn’t really impact it. My overall goal is for our portfolio to perform equally (or better) to the US market in USD terms. Geographic arbitrage is our friend, as we can choose to go where the USD is strong relative to local currency. We went to the UK post-Brexit vote and to Europe when USD/EUR was at a decade low, for example. Argentina could be a good visit now.

If we were committed to one specific currency, I would probably tilt our portfolio in that direction. We are currently spending in Taiwan dollars and everything costs 10%+ more than it did a few years ago as the TWD has strengthened. It’s no big deal, but if we were planning on being here 30+ years I would consider investing some locally.

As someone who also plans to live ex-US in my post-FIRE years, I had a very similar question. In my case I know I’ll be spending about 1/2 – 3/4 of my time in Euro and CHF denominated countries, and would like to mitigate the long term currency risk. It sounds like you haven’t committed to any one country/currency, which is a solid plan. But do you have any thoughts for people who actually plan to spend a majority of their time ex-US in the long run? Many of your readers are accumulating U$D in our working years, and them plan to retire outside of the US, and long term currency risk mitigation is a topic that’s rarely discussed.

We all see that the U$D is very strong now. When I was in EU in 2010, it was 1.65 U$D/euro. Now it’s 1.10! That’s a pretty significant shift, especially when compounded with inflation, which is great for U$D holders now! But it can very easily (and will eventually) go in the other direction.

If we knew what to do with it now, we could mitigate some of that long term currency risk. Markets are up, and people are asking “The market’s overvalued! Where should I invest?”. Well, it seems to me that if someone has long term goals of living outside the US then we should be figuring out how to invest these currently high value USD into the currencies we plan to be spending post-FIRE. To clarify, this is not about ForEx or currency trading, but about long term investments outside the U$D, towards the goal of having funds invested in the country/currency of one’s retirement country choice.

This topic could very well deserve it’s own blog post ;-)

I don’t know what the right answer is (if there is a right answer.)

If I was looking to live in Argentina or Venezuela or a long list of other countries, I would still keep the vast majority of assets in USD. For a Euro focused life, I’d tilt some TBD percentage towards Euros but that might just be cash. As long as the USD is the primary world reserve currency, I’ll still keep a USD centric portfolio.

That’s it – the whole blog post.

A very balanced article, and well articulated and supported opinion. Couple of key factors from my stand point, first of which you allude to:

1) be careful chasing past performance; US has dramatically outperformed over last 10+ years, resulting in US valuations being dramatically (eg PE ratios 30 – 50%) higher. Is some of that justified for reason cited? Probably. Are US stocks valued extremely rich? Yes, based off history (see Shiller).

2) yes, there are many great, dynamic companies in America. But look at the head winds they face due to a struggling democracy/government: massive fiscal deficits, dysfunctional political system, poor and declining infrastructure, increasing social unrest (eg wealth distribution and anti capitalist rhetoric). There is a strong case to be made that the near to mid term future outlook is troubling. Clearly the US is not perfect, nor is anywhere else for that matter, But that does argue for diversification of political risk. See legendary value investor Seth Klarman’s annual letter to Baupost investors.

In conclusion I think the 100% US exposure argument is tenuous based on present and forward outlook. I think your 20 – 50% international exposure makes more sense,

Hola Jefe, solid points.

I agree on your conclusion.

Shiller’s CAPE thing is interesting, although if we used it as an investment guide everybody would have avoided US stocks since 1981. Bummer that Shiller missed out on nearly 40 years of epic investment returns, but he does have a nice pension and book sales to pad his retirement. I’ll happily pay 30-50% more for the US legal system versus Russian or Brazilian.

The US has always had a dysfunctional political system. It’s part of the core design. People plugged into the 24/7 news cycle just see more of it now.

Great breakdown of the case for owning international stocks! I see that your portfolio is almost completely tilted to stocks, do you mind me asking what your plans are in the event of a big drawdown? Would you continue to withdraw 4% or so or do you have a cash buffer? Sorey if you’ve already answered this question. New reader here.

Hey, Will.

See “Hacking the Data” and “Foundation for Long Term Success” in this post. Take a look and let me know if you have any follow up Qs.

We’ll just keep doing what we are doing, which is basically independent of current market prices. We are 6+ years into this little experiment and have yet to spend anything close to 4%. Between tax optimization and blog income, we probably own more shares of stock than we did at the beginning.

Thanks a lot for the reply, I’ll have a look at the post!

Personal situation,but often wondered about this, What if you arent from America? Should an African or Asian invest 60% into the US and 40 International? Since for them it would be basically 100% international, 0domestic? And then live with the currency risk.

Secondly if performance gets measured in usd the emerging markets and developed markets have done worse than US, but in their local currwncy may have done well. Again the US returna would be enhanced if measured in their currency, but one of the largest drivers of performance of US vs nonUS seems to have been the Dollars strength as a currency. Is it just better to be a share owner in the Worlds reserve currency, and then reassess if the Yuan ever rises to dominance or SDRs… All interesting to me as a nonUS citizen.

Hey Bob, I understand your dilemma. I’m British, live in Asia buy most of my stocks/ETFs off the London Stock Exchange, but hold them through a platform in Luxembourg. I hold a mix of USD and GBP denominated ETFs, but if you look into it, the currency of your ETF doesn’t really matter that much, but you could choose a brokerage that offers multiple currencies if you’re worried. If you’re looking for international exposure VEU is a good ETF as it tracks the whole World excluding the US. It’s recent performance has not been stellar which makes me think it could be an even better buy right now. Otherwise my go to Vanguard ETF (listed in the UK) is VWRL/VWRD. Which tracks the global stock markets by market capitalisation. It’s roughly 55% US, 19% emerging markets and the rest international developed World. It roughly follows global market capitalisation, so you don’t need to worry about small percentages!

Im more concerned about the fact that my currency in use is an emerging market currency. As such over the past 10 years as it moved from say 10 to the dollar to 20 to the dollar, it magnified the US returns thus besides VTI shooting up, we received an additional 100% in the form of currency depreciation.

However whilst it magnifies on the way up it also magnifies on the way down. The issue is we spend in an emerging currency that is more volatile than developed markets. Is the answer always to be in developed currencies? because there was a lot of issues with owning developed assets post the financial crisis when emerging market currencies strengthened significantly… It’s a far bigger impact to SWR than stock returns have been.

We’ve been using a combo of local and international stocks to try mitigate some currency issues as well as keeping shorter term money in local currency. But am always considering whether to just use USD or other developed currency as my base in order to avoid feeling rich when it was just our emerging currency plummeting in relative value.

There’s more than just raw performance involved as well. As a Canadian, the tax treatment of some of these options is different – for example, one of our tax advantaged accounts (what we call a TFSA) is not subject to our tax treaty with the US, resulting in US withholding taxes for dividends paid by US companies. Similarly, in our fully taxable accounts, qualified dividends paid by (typically Canadian) companies are taxed differently than non-qualified dividends.

All in all, I’d say that it makes sense to at least have some *domestic* assets, depending on where domestic is for you.

This is important. After-tax return is what you really get.

Hey Bob, this isn’t something I’ve thought about a lot so I’m mostly thinking out loud here…

If I were a non-US person, I would lean more towards true market weight. As a US investor I can get 0% tax rate and no withholding, something not available to others, so taxes are something to consider as well, i.e. maybe your home country has tax benefits for investing locally (thus encouraging heavier weight.)

I once met a guy who was living in Japan (afair) and had his effective rent double when the currency was hit, and I worked with a few guys who were living in Europe but being paid in dollars who were hurt when the Euro jumped circa 2001/02. So if I were committed to another currency, I would also hold investments in that currency. Probably government bonds, but maybe a personal residence.

Recently, I reduced our international holding to 20%. I think that’s about the right balance. Some years international performs better US, but that’s pretty rare over the last 10 years. More than 20% can drag down your portfolio quite a bit. Last year, we didn’t do so well because of international index funds performed so badly. Anyway, I think 20% is about right.

What did you reduce it from? Did you base that solely on performance, or did you get new info that made you think your original allocation was not the right one?

The bad performance last year pushed me over the edge. I had nearly 35% international and it was painful. This is based mostly on experience. International rarely beat US. I think only once or twice over the last 10-15 years. I need to check the numbers.

Also, I learned from Jack Bogle a few years ago. Now I’m convinced that he’s right. 20% or less. US companies are already diversified. That’s why I think the stock market isn’t going to do so well this year. The global economy is slowing down quite a bit.

“International rarely beat US. I think only once or twice over the last 10-15 years.”

This is recency bias. International beat the US as recently as the 2000s. US stocks lost money over that decade while international gained. This was mainly driven by emerging markets, but developed ex-US also beat the US. You can’t just look at the last ten years in isolation and decide, that’s it.

This goes one way and then the other. If international has underperformed for _the last_ 10 years, reversion to the mean could mean that it is likely to overperform for the _next_ 10, and that is exactly what most analysts including Americans ones from the likes of Vanguard or Schwab are predicting for the next ten. Now they may or may not be right but I can see the logic in the argument.

Surely this is the worst time to rebalance into US stocks, when they are higher, relatively? “Buy high, sell low?”

Personally, I think something around 50/50 or market weight makes sense. I’d be more comfortable piling into US stocks at lower valuations.

https://www.fidelity.com/bin-public/060_www_fidelity_com/images/Viewpoints/FF/international_investing_2018_chart_1.jpg

https://www.portfoliovisualizer.com/backtest-asset-class-allocation?s=y&mode=2&timePeriod=4&startYear=2000&firstMonth=1&endYear=2009&lastMonth=12&calendarAligned=true&initialAmount=10000&annualOperation=0&annualAdjustment=0&inflationAdjusted=true&annualPercentage=0.0&frequency=4&rebalanceType=1&absoluteDeviation=5.0&relativeDeviation=25.0&portfolio1=Custom&portfolio2=Custom&portfolio3=Custom&TotalStockMarket1=100&IntlStockMarket2=100&IntlDeveloped3=100&total1=100&total2=100&total3=100

I’m impressed you have 20% int, rare for an american. An a non-american myself, international investing has been natural to me for the past 20 years. My balance has always been 50-50% US-Int (roughly) and, although I lament the international performance of this decade, I remember the 2000’s very well and it does not cross my mind to reduce that exposure. The argument that US companies benefit from world growth is flawed, simply because international companies do too (if not even more). Yes, US is pro-business, rule of law, etc. but international companies on the other hand tend to have fewer competitors and ingenuous ways to cope with local “obstacles”. So they grow too. If they didn’t, there wouldn’t be entrepreneurs and business people outside the US. As you mentioned, my overall (20-year plus) volatility is actually lower because I own multiple countries. Currency risk? Yes, it does exist in the short term and fade in the long run (data proven). But hey, aren’t you the one promoting geographical arbitrage? Why worry, specially considering your global mobility? Since you crunched some numbers you probably saw that US multi-year out performance is usually followed by multi-year under, not to mention current CAPE valuations, price/dividend, etc. No, no, no timing here, just long term prediction of total return going forward. Let’s touch base again in 2029. PS: love your stories, you are my hero.

I definitely have less international exposure for many of the reasons cited – US companies having (oftentimes) 50% or greater of their sales overseas, the miserable performance of international stocks for the last decade, the lack of good accounting standards in many countries (think China), and the big one in my book, namely that Int’l stock funds and ETFs are so highly correlated to US stock funds and ETFs. I have seen many so-called experts claim that is not the case, but international markets have been following the US market virtually in lockstep for some time. The US markets are down significantly today due primarily to CAT and NVDA; what do you think the foreign markets will be in response? Only a one day example but from someone who has followed the market gyrations for some time, it is the way it normally is.

With their higher expense ratios the Int’l funds/ETFs already have an anchor on their performance compared to their US counterparts. Until things change count me as a person who would prefer doing their investing with good ol’ US of A companies, thank you very much.

And conversely, there is a strong argument for me to invest in local (Australian) shares to take advantage of fully franked dividends (https://en.wikipedia.org/wiki/Dividend_imputation) to minimise the tax bill. A question for you : are you comfortable with the low dividend yield from US stocks? I thought there would have been rioting in the streets by now.

Thanks for writing this and sharing your thoughts on the subject :). As always, very well written and presented!

FWIW, the following series of articles shaped my own US/xUS equity split:

https://finpage.blog/2017/03/18/investing-in-the-world-part-1/

https://finpage.blog/2017/03/25/investing-in-the-world-part-2/

https://finpage.blog/2017/03/25/investing-in-the-world-part-3/

Based on this data, I decided on the following for my equities:

2/3 World stocks, which includes U.S. (e.g. VT)

1/3 U.S. stocks (e.g. VTI, VTSAX)

With this allocation, I’m correlated to long-term global growth trends as well as domestic inflationary effects.

I implement with IXUS+VTI (instead of VT+VTI) to achieve better tax efficiency and lower overall E/R. And I lookup the global cap weighting from the Vanguard page for VT (which is updated monthly).

Thank you for the interesting post! I know there were a lot of comments on recent articles so I really appreciate teh follow up here.

My pleasure. I had planned to write a post on this way back in 2016, and the recent comments finally gave me the motivation to do so.

I also have a 20% international allocation. I decided this based on the advice in David Swensen’s book, Unconventional Success: A Fundamental Approach to Personal Investment.

I’m glad that this allocation model coincides with what you concluded.

I’m at 20% international as well. And, after spending way too much time on Portfolio Charts, I sliced and diced some into a portfolio I’m happy with (something I ignored for a long time, being heavy in real estate).

Great minds think alike?

Great article. I love that you acknowledge that there is not an obviously right answer. My impression is that correlations between the U.S. and developed foreign markets have gone up in recent decades–and that, in particular, correlations between the U.S. and developed foreign markets during times of market duress have really spiked. So I wonder how much of a free lunch the diversification will bring going forward. I enjoyed following your thought process. Thanks for this one.

It seems reasonable that the correlation between US / non-US markets would increase as the percentage of non-US revenue increases.

I don’t feel fully comfortable with the “during times of market duress” component, largely because there hasn’t been much duress since 2008. TBD. But also acknowledge that I don’t really know.

Sounds good. Happy investing, Jeremy.

I’m 50/50 US/International. Just in case the US implodes over the next 50+ years. :)

The last decade hasn’t been great as a heavy international investor. But the US component certainly did it’s thing! Maybe the next 10 years will be better for my asset allocation. Maybe not. Either way I’ll probably still be able to fund that mythical 4% (which we aren’t coming close to spending either!).

Solid choices all around. VXUS is paying 3% dividends at the moment, so no worries on the 4%.

I’m 60/40 US/int, so pretty close. Decided to just go with the Vanguard recommendation. Of course, I have about 25% of my portfolio in cash right now due to my business needs.

i am 60/40 US/Intl Stock.

I have 100% us stocks.

I believe in the Collins/Buffett/Bogle approach.

Although it’s an interesting graph (up to 2007), any of those allocation had incredible returns during that time.

I chose 100% us stocks because there’s nothing I like more than simplicity. No rebalancing and autopay into it for years to come. Spending levels are so much more important than returns.

However, if I get close to FI or especially if I decide to FIRE, I might change my tune…or not. Laziness will probably win.

Thanks for the nice post.

Agreed on all points (particularly the laziness one.) Having some international allocation has helped with lower volatility, which can be nice in withdrawal phase.

Shouldn’t one just weight US/Internationals stocks roughly in proportion to global market capitalisation rather than some arbitrary percentage? Right now the US is about 55-60%. Given that the majority of you invest in index funds that follow market capitalisation of companies why do you not do the same with geographical allocation? There’s a lot to be said for just owning one World index fund. No rebalancing would be needed (at least for equities). Here’s an excellent that article makes the case for that: https://monevator.com/why-a-total-world-equity-index-tracker-is-the-only-index-fund-you-need/

I also like the global market portfolio (which is the weighted sum of every asset in the world), but there’s not quite enough equities exposure for my liking (and no good ETF that tracks it yet).

One could do that.

If one had done so over the previous 50 years, the return would have been lower with higher volatility than US alone. Or in other words, the market was wrong. So not sure about should. (Great monevator article, btw.)

Just seen this tweet which quite relevant to your article : https://twitter.com/MebFaber/status/1090662885573853184

“Over the past 70 years the US stock market has been a darling, outperforming foreign stocks by 1% per year.

$10k invested in US stocks in 1950 turned into $14 million vs. only $8m in foreign stocks.

Want to know how much of that outperformance has come since 2009?”

All of it.

This was a recent article on the US vs International stock valuations that I read that has compelling stats on just how undervalued International equities have become compared to the U.S.

https://mebfaber.com/2019/01/25/the-biggest-valuation-spread-in-40-years/

Current PE of Russia is about 9. For the US, about 21.

Median home value in Flint, MI is about $20k. In Seattle, it is about $725k.

Is there a value disparity? Or just price.

Yes price disparity is common due to local employment market, also Russia is under sanction and quite risky

that why it is cheap, However the reverse to the mean likely to impact the US stock market in a negative trend. Just as it impact Japan Stock market after 1989s..

To which mean will it revert? When? The average S&P500 PE over the past 30 years is 24.

PE of the Nikkei in 1989 was about 70, and a lot of those earnings were imaginary.(see transparent account standards.)

I just checked, 27% international. Mostly out of laziness and lack of rebalancing. I agree that about 20-25% is ideal. I think I will just allocate future allocations in that direction instead of rebalancing. Once again, laziness wins!

I still have a bit of cash to allocate. I think it will all go into international / VXUS

Wow!!! Great post and comments! How did I miss this? Math and awesome graphs with real life examples! I definitely like the lower volatility especially in the more critical 10yr window of initial retirement(although I guess it all works out). Thanks again. 22 mo for FI. Ok now what about corporate bonds(isn’t that part of the Vanguard Target date fund package now)

I don’t really do bonds. Vanguard target date funds have US / International bonds, both government and corporate.

I’m at 70% VTSAX, 25% VTIAX, and 5% bonds. 31 years old, military job. I’ve been to 58 countries in the last 6 years. Some of them were great (Australia and Romania get a shout out) and some of them have some work to do (Djibouti, Iraq, Liberia). There is lots of potential for growth in much of the world, but also lots of challenges as well.

I think just owning US stocks is foolish. There are 7 billion people living outside the United States and 50%-ish of the world’s market cap, as you described above. The room for real growth in the rest of the developing world, not even counting emerging markets, is huge.

Just owning US stocks is like just owning the tech sector in the US. You are picking one sector to beat the market average of all the other sectors. I know I can’t pick stocks or sectors to outperform, so I just buy the whole haystack and skip looking for the needle.

I apply the same principle to international equities. Just buy the haystack because you never know where the next Alibaba or Google is going to rise.

Like you, I have no idea what the right balance of US-Int’l is. I suppose I should just call it 50-50 since that is the approximate market cap distribution. But right now I am 74-26, so my money is on the home country bias.

Since international markets have under-performed the US so much for the last ten years, I would not be surprised if they outperform the next ten years. Time will tell. Either way, I will at least capture some of the returns of both US and International stocks by owning VTSAX and VTIAX.

And I can sleep easily at night with my portfolio, which is 80% of the battle.

Totally agree that the opportunity for real growth in the rest of the world is huge. The question is who gets the benefit of that growth? Is it capital, in which case our return is positive. Or is it corruption and bureaucracy, in which case our return is less than positive.

Great article! Thanks for this. This is one of my favorite posts on this subject: http://forum.mrmoneymustache.com/investor-alley/statistics-personal-experience-and-risk-management/msg629210/#msg629210

I like that post as well. Dodge is a sharp guy. I am unable to replicate his conclusion, however.

The Portfolio Return charts in that post are from Portfolio Visualizer, which only offers international data back to 1982.

From the Trinity Study / 4% rule, the 1972 period is one that passes… so I suspect there is a greater than 4% withdrawal rate used in this analysis to get a failure (actually about 5.7%.)

If I look at a portfolio of 80% US stock / 20% US bonds with a 4% withdrawal rate, I get this chart:

Some non-US stock in this period would have improved CAGR with lower StDev, but not to the degree described.

Solid article. The world markets range around 52% US, 36% developed and 12% emerging mkts. That fluctuates a couple of points but that’s a good benchmark. In the last ten years, the US has obviously been the place to be. Not sure what demographic your readers are, but I’d remind everyone of the “lost decade” for US stocks. From 2000 – 2009 US stock lost around 9% cumulative for the decade.

International stocks have underperformed US significantly over the last ten years. However, in 2017, the EAFE index returned 25.03% and MSCI emerging markets returned 37.26%. The Russell 3000 returned 20.97% in 2017. An all US portfolio would have underperformed.

My point is not to highlight short term returns. It’s to say that having a home bias (along with a recency bias) are not helpful when investing. Most people won’t be comfortable having a total market based portfolio matching the world market percentages. Not having international can be costly. I’d ask readers to ponder this question:

Do you think expected returns going forward are better for the US or international stocks? If you believe in the regression to the mean, you’d have to say international, wouldn’t you?

Another argument can be made for overweighting value and small cap stocks. That’s a discussion for another day. 😀

Great job analyzing the data. The blogosphere needs more of this type of writing.

I’m at 20% international. Being from France but living in the US for the past 20 years, weighing how much to put in US vs. non-US has simply…cost me too much time spent on Portfolio Visualizer, Portfolio Charts, etc. Pick an allocation you are comfortable with and leave FOMO behind. Keep it simple. If you see a rose, smell it.

VTWAX for life. I admit that I know nothing so I just go with global market cap. Anything outside of that is a bet. This is all I need. I’ll add bonds later. Simple…

That map is over 5 years old and outdated. For example the total market cap of all listed Indian companies is now over $2 trillion – comfortably larger than any single company. That’s like Apple + Amazon + Facebook all of which are in the top 20 companies by market cap.

Yes. So?

As Jack Bogle has said and I think it a strong point, current US indexes already has international exposure. I favor the Vanguard Balanced Index Fund Admiral for the best all in one fund. I also like the Wellington however the Balanced Index holds 60% Total US stocks while the Wellington owns 65% consisting of of 92 stocks and that has always bothered me. 92 stocks and and the word diversification don’t add up for me. Remember the other term “Past performance is no guarantee of future results.”

Any consideration here to the rest of the world being less impacted and recovering more quickly from the pandemic? Less exposed going forward to another possible shutdown and slower recovery?

I’m not a market timer generally so no, haven’t thought about it.

Thanks for writing this great article! For someone with a long-term investment horizon, would you suggest holding international (VXUS) in a taxable brokerage account or a tax-deferred retirement account? I’m living in a high-tax state (CA) and currently in a high marginal income tax bracket. I saw on the Vanguard website that only ~65% of VXUS dividends in 2019 were eligible for reduced tax rates as qualified dividend income.

As with many things, it depends…

You will get a mix of dividends, qualified and unqualified. The former taxed by the feds at <20%, the latter taxed at <37%. California will tax both equally.

Let's say you buy $100k worth of VXUS - maybe you get $2,500 in dividends (2.5% yield.) 65% taxed at 15%, 35% taxed at 35% (for example)... total tax of ~$550 for an effective federal tax rate of 22%.

In addition foreign governments will withhold tax - what you receive in dividends is after-tax. In 2019 this was about 7% afair. You can then use the foreign tax credit (FTC) to offset your US taxes - reducing your $550 tax bill to ~$375 for a 15% effective tax rate. This is an effective annual load on the funds of about 0.4% ($375/$100k) - 4% over 10 years, 11% over 30 years.

If you hold the fund in a retirement account, you don't pay the taxes now* but you also cannot claim the FTC.

* you pay the taxes later upon withdrawal at your ordinary income tax rate (instead of the capital gains tax rate.)

If you hold the funds in a taxable account, you pay the taxes now but have use of the funds before age 59.5.

Capital gains (long-term) are taxed at the reduced tax rates instead of your earned income tax rate.

Which is better? TBD. I have VXUS in both taxable and tax-deferred accounts, but prefer to hold it in taxable accounts for FTC and the low taxes on long-term capital gains.

Thank you!