It’s that time of year again, when the stars align and wonderful things happen. No, not the holidays. Tax time!

That’s right, before the end of the year we need to implement all of those tax minimization strategies that allow us to defer, minimize, and eliminate taxes

I just completed this process for the year, effectively completing our 2014 taxes.

Total time? 7 minutes

I have tax time down to an art. Here is how I did it

The following is a Step by Step example implementing the strategies first shared in the post Never Pay Taxes Again

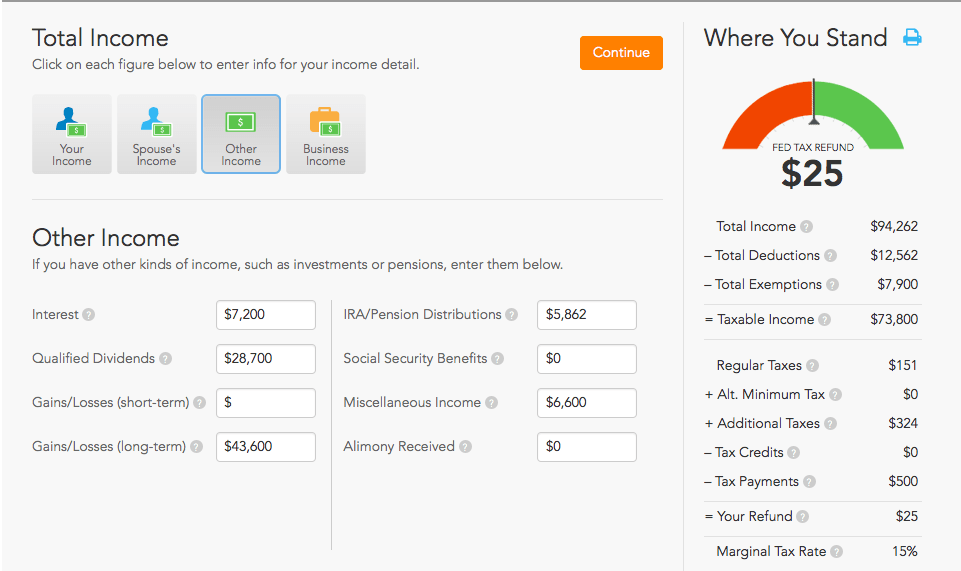

Being able to quickly and efficiently view your total financial and tax situation is key. We use Personal Capital as a foundation, allowing us to see the big picture in just a few pages.

Step 1: Check the Latest IRS Information for the 15% Tax Bracket Threshold, the Standard Deduction, and Personal Exemption values

The IRS published changes to the Standard Deduction, Personal Exemptions, and Tax Tables in Revenue Procedure 2013-35. From this document we learn:

F0r Married Filing Jointly, the upper edge of the 15% tax rate is $73,800.

This threshold is important, because when total income is below this amount, Qualified Dividends and Long Term Capital Gains are taxed at 0%

We also learn:

2014 Standard Deduction for Married Filing Jointly (MFJ): $12,400

2014 Personal Exemption: $3,950

Total deductions and exemptions (MFJ): $20,300

Step 2: Estimate Total Qualified Dividend Income

From the Personal Capital Investments page, we can see Dividend income to date. For most funds, this information will be incomplete until the end of December, so we must make an educated guess

To estimate the year end dividend payout for a fund, I compare current year dividends to last year. We do this with every fund we hold. Here is one example using Vanguard’s VTI / VTSAX:

Q3 2014 payout / Q3 2013 payout = $0.465 / $0.429 = +8.4%

Q2 2014 payout / Q2 2013 payout = $0.420 / $0.386 = +8.8%

From this I assume that the Q4 2014 payout will be ~8.5% greater than in 2013, increasing from $0.494 per share to $0.536 per share

Is that accurate? I have no idea. We will find out in a couple weeks

Step 3: Estimate Total Non-Qualified Dividend Income (and Foreign Tax Paid)

Some funds generate a different class of dividend, which the IRS calls Non-Qualified. This is the case for many funds that invest in Real Estate, Commodities, and International Stocks.

For these funds, we need to estimate the amount of both Qualified and Non-Qualified Dividends. Here is an example using Vanguard’s VEU:

Q3 2014 payout / Q3 2013 payout = $0.268 / $0.221 = +21%

Q2 2014 payout / Q2 2013 payout = $0.610 / $0.605 = +1 %

Q1 2014 payout / Q1 2013 payout = $0.394 / $0.139 = +283%

It is less clear how to estimate the payout of this fund, so I use the most recent quarter info as a default (+21%.) I could be right, I could be very wrong. Being 100% accurate isn’t possible, so we just do the best we can

Using last year’s 1099 Form (from 2013), 30% of the VEU payout was considered Non-Qualified.

Assuming the same situation in 2014, then the VEU distribution will increase by 21% to $0.468 per share, $0.328 as Qualified Dividends and $0.14 per share as Non-Qualified Dividends

For a fund like Vanguard’s VEU that holds international stocks, often tax will be withheld from the dividends before they are distributed to you. This data is shown on the same 1099 as the dividend data, so we might as well check this now

Uncle Sam will give us a tax credit for any foreign tax paid, so we should take advantage of this credit

Last year’s 1099 Form shows that Vanguard’s VEU withheld 5.5% of the total payout as tax

Assuming the same for 2014, 5.5% of the the entire year’s distributions will be paid as tax. We will receive an estimated distribution of $1.74, the net remaining after paying $0.096 in tax

Step 4: Estimate Short Term Capital Gains and Long Term Capital Gains

Some funds trade regularly. If the fund management were to hold an investment for less than 365 days before selling, it might be classified as a Short Term Gain and be subject to taxation at the marginal rate. If the investment was held, longer than a year it is classified as Long Term and taxed at the same rate as dividends

For funds that track indexes, such as VTI and VEU, Short Term Capital Gains seldom occur, and we can assume $0 for total Short Term Capital Gains

If you were actively trading, some gains may be Short Term and others Long Term. Calculate total gains here

We have not sold anything in the past year, so Total Short Term Capital Gains = Total Long Term Capital Gains = $0

Step 5: Estimate All Personal Earned Income, Business Income, and Interest

If we have truly prioritized Leisure over Labor, then there will be no Earned or Business Income. But inevitably, an early retiree will likely have some additional income trickle (or pour) in

Some of this income has not been received yet (as of Dec 13, 2014) so I estimated based on previous months

In our case, the blog generated a small amount of income

Additionally, cash reserves and a private mortgage loan generated a respectable amount of interest

Here are 2 great savings options that we use:

1. Open an online savings account with industry leading interest rates and get $20 free

2. For WA State Residents: Earn 4% on your first $500 and get a $50 signup bonus

Step 6: Determine ROTH IRA Conversion Value and Transfer Funds

From Step 1, we know that all income up to $20,300 is tax free.

From Steps 3-5, we’ve estimated our total income from Short Term Capital Gains, Interest, Earned and Business Income. We add all of these together to determine “Total Non-Qualified Dividend and Long Term Capital Gain Income”

Example:

Earned Income: $0

Interest Income: $7,200

Non-Qualified Dividends: $6,600

Short Term Capital Gains: $0

Blog & Other Business Income: $2,300

Total: $16,100 ($4,200 less than total deductions of $20,300)

Rather than let this $4,200 of tax free income go to waste, we will create it out of thin air by transferring funds from our Traditional IRA to our ROTH IRA

These funds, and any future earnings on them, are now tax free, forever. Thank you Uncle Sam!

Step 7: Determine Long Term Capital Gain Harvest Value and Execute Trade

From Step 1, we know that as long as total taxable income is less than $73,800, all Qualified Dividend and Long Term Capital Gain income is taxed at 0%

From Steps 3 and 4, we know our total Qualified Dividend and LTCG income

Example:

Qualified Dividends: $28,700

LTCG: $0

Total: $28,700 ($45,100 less than zero tax threshold)

Rather than allow this $45,100 of tax free capital gains to go to waste, we will Harvest up to this amount. How?

Using VTI as an example:

Assume we bought $383,000 of VTI shares on December 12th, 2013 for $92.46 per share. Selling these on December 13th, 2014 would yield $103.34, an increase of $10.88 (11.8%.)

Total gain are $45,068, bringing our total Qualified Dividends and Long Term Capital Gains income to ~$73,800, the tax free threshold

By repurchasing VTI, we effectively increase our basis to the new price ($103.34), and make the $10.88 gain tax free, forever.

(Some interpretations of tax law would suggest repurchasing the same asset could be classified as invalid by the IRS. They have not done so in any case today that I am aware of. This could be avoided by purchasing a fund that tracks a different index)

Conclusions

These 7 steps took me 7 minutes (which is great until somebody comes out with a 6 minute taxes post) and about 7 hours less than it took me to write this blog post)

In the process, we were able to convert $4,200 in tax-deferred funds to tax free funds, and lock in over $45k in capital gains. That is nearly 50k in tax free dollars

In the new year, I’ll share our actual 2014 tax return with final numbers to complete the example

It will probably take a bit longer than 7 minutes to complete the process the first time, but hopefully this example will help guide the way. Using a tool like Personal Capital to provide quick access to our whole financial situation helps

Bonus Points: Recover Foreign Taxes and Self Employment Taxes

Because of some blog income, we must pay some self-employment taxes. This amounts to 15.3% of total income, or about $350. Half of this is deductible, increasing total deductions by $175 to $20,475

In Step 3, we determined how much Foreign Tax was withheld from our foreign investments. This year we estimate about $500

This $500 in tax credit will wipe out the $350 due in self-employment taxes, but will leave $150 of credit on the table. Why not generate additional taxable income to create $150 in additional tax?

Long term, increasing the ROTH IRA Conversion value will provide the best ROI since this will result in tax free growth. But by how much are we able to increase our Conversion?

Any additional ROTH IRA Conversion will be taxed at 25%, and we need to reduce the Harvested Capital Gain value by the same amount or pay tax on a portion of it (at the max tax rate on LTCG’s of 15%)

After a bit of algebra… 0.25x – 0.15x = 150; x = 1500

We can increase our conversion amount by $1,500 plus the $175 in additional deductions, from $4,200 to $5,875. At the same time, we reduce the amount of Capital Gain we Harvest by $1,500

A quick check using Intuit’s Taxcaster is a great way to double check our analysis

TaxCaster: Close Enough for Government Work

Some Additional Thoughts/Concerns/Questions

“There are a lot of estimates in this process, what happens if we make a mistake? Will we suffer a big tax penalty?”

Estimates for year-end dividends and foreign tax withholding could be off by a large margin. If we attempt to harvest too large a capital gain, we will have to pay tax at a rate of 15%. If we move too much money from our Traditional IRA to a ROTH, we will have to pay tax at a rate of 25%. Fortunately, this is only on the amount above and beyond the levels we checked in Step 1

Worst case, we might pay a few hundred dollars in tax. If we are less aggressive and intentionally estimate low, we could guarantee no tax.

“Why make so many estimates? Can’t you wait until Dec 31st and use all of the year end dividend info?”

I have two reasons for doing this. The first being that it is unclear when Vanguard will publish their final and fully accurate dividend info. We may learn what the payout is with enough time remaining in the year to execute trades, maybe not. In addition, sometimes the qualified vs. non-qualified dividend info is not complete until the next year, when tax documents are released in February

The second reason is that I want the option of being able to trade these same stocks next year as a Long Term Capital Gain. This means we need to hold the fund for 365 days + 1. If we wait until Dec 31st to trade, we lose this flexibility.

“Isn’t paying No Tax in the US, and receiving a credit for Foreign Tax paid like having the US Government pay your foreign taxes for you?”

It sure is. And you didn’t even have to setup a bank account in the Caymans or a shell corporation in Ireland to do it. If Congress were to ask me for advice, I would recommend changing this particular portion of tax law. (Note to Congress: Feel free to use the Contact form at the top of this page)

“Won’t ROTH IRA Conversions and Harvesting Capital Gains impact my Obamacare subsidy?”

Yes. On the scale shared in this example, subsidies will be completely eliminated. I previously estimated this as an effective 13% tax on income up to 4x the Federal Poverty Level

In our specific case, since we don’t have health insurance in the US and have remained outside the US for more than 330 days in 2014, we are outside of Obamacare

“Why do you recommend Personal Capital?”

Personal Capital is a free online tool that consolidates all of our financial information, making it easy to view all of our investment transactions and costs on a single screen. I like it, as it is a simple way to quickly see all of our capital gains, dividends, and interest income. We also have an affiliate relationship, so if you try Personal Capital using one of our links we may receive some compensation. Feel free to give it a try and decide for yourself

Have thoughts, ideas, or questions? How long does it take to do your taxes? Please share in the comments section. In the mean time, Happy Tax Time!

Question: you guys seem to spend around $4-5,000 monthly, so around $50-60,000 annually. Where do you pull that money from? I would have assumed you cash in some investments, but you say your long tern capitol gains are still $0? How does that work? Am I missing something?

Hi Andrew

The delta comes from cash. Maybe 80% of our spending this year will come from dividends and interest, and the remainder comes from drawing down our cash account

We weren’t sure how much we would spend this year on our IVF procedures, so we started the year with quite a cash horde

re: Capital Gains. The reason Step 5 shows LTCG = $0 is because we sold no stock earlier this year. The first transaction we did was in Step 7, Harvesting Capital Gains

If our cash pile needed to be topped off to smooth our next year’s spending, I would do it as part of this year end activity

Make sense?

Jeremy

Thanks for teaching me something about taxes! I’ll have blog-related self employment taxes, too (maybe $2000?) and I was afraid my foreign tax credit would go unused. I didn’t realize it offsets the SE tax. I’m trying to keep my AGI low in order to qualify for near-max ACA subsidies, so I can’t easily convert more to Roth without suffering that effective 15% or so subsidy reduction.

Starting next year, you might be able to get a refundable child tax credit ($1000 per head). I think you have to have earned income in order to make it refundable. Theoretically, you might be able to get a $1000 check back from the government, thereby making your tax rate negative. We will probably get back a thousand or two from ole Uncle this year due to much lower income and the $3000 child tax credit. Makes tax season a little happier. :)

You are welcome :)

I think our investment income is too high to capture any credits, but… I haven’t started looking into it yet. If there is a way, I’ll figure it out :)

I’m happy to have the additional Personal Exemption next year. If we planned better, GCCjr would be born on 12/31 to give us another $3,950 in ROTH IRA Conversion potential. Although a due date of 4/15 is ironic in its own special way

What a great post Jeremy, and a wonderful education about taxes!

At this point in my life (I’m 46 and she’s 49), I don’t see a clear path to get anywhere close to where you are… Around 90% of our portfolio is invested in tax-advantaged accounts (401K, Trad. IRA, Roth IRA, and HSA new for 2015), and I have a pretty high earned income from my job.

It seems I’d have to stop investing altogether in tax-advantaged accounts, and spend the next 10 years pouring every available penny into a regular/taxed investment account before we could ever hope to prioritize leisure over labor. But investing in the tax advantaged accounts is saving me a lot in taxes each year.

If I were to retire early (in the next 10 years), I’m currently unclear what we would live on until we’d be able to start tapping into our retirement (tax advantaged) money. Our expenses are very similar to yours BTW — roughly $5K/month. I think we could fairly easily scale that back by $1000 or so if we really wanted to. :)

I apologize if my post above sounds totally unrelated to the subject at hand — taxes. It was basically a follow on thought to Andrew’s question above where he asked where $50-60K per year is coming from for living expenses. I was basically wondering the same thing. But really I was trying to imagine where in the heck I would pull ~$5K/month from to pay my living expenses if I no longer had an earned income. :)

My comment below about 72t was meant to be a reply to you – I’m not sure why that didn’t happen. But you should take a look.

Thank you! :) I’ll research 72t. I also learned you can pull contributions from a Roth IRA as long as it’s been there for 5 years minimum. Also, rather than accessing money in my 401K for living expenses at 55, I think I’d rather convert the 401K over to a regular IRA, and then to a Roth IRA. With no earned income, if I did this correctly it could be done tax free over a period of several years.

You can pull direct contributions from a Roth IRA at any time without consequence. The five year rule can come into play for when you roll over a traditional IRA to a Roth.

Hi Dave

Ervin has given you some good direction. There are several ways to access money in tax deferred accounts without penalty before 59.5. In addition:

Read through all of Jim Collin’s stock series. There are several posts on withdrawing from tax deferred accounts

One of Jim’s later posts highlights the risks of saving too much in tax deferred accounts:

http://jlcollinsnh.com/2014/07/27/stocks-part-xxiv-rmds-the-ugly-surprise-at-the-end-of-the-tax-deferred-rainbow/

Good luck

Jeremy

The foreign tax credit doesn’t specifically offset SE tax. It just offsets your tax liability. SE tax can never be fully avoided, even with solo 401k or traditional IRA contributions. In Jeremy’s case, there are only SE taxes and Roth conversions to offset, so the foreign tax credit is offseting those two things.

For the typical employed person, the foreign tax credit is mostly going to offset tax on wages (I say mostly because I don’t think it’s correct to say the foreign tax credit only offsets taxes from X if X is lower than total tax liability incurred).

Look into the 72t. You can pull out money from an IRA (you’d have to roll a 401k to get access to those funds) penalty free (but not tax free) before 59.5. There are three ways of calculating the allowable withdrawal amount. Once you start the 72t, you must withdraw exactly the amount given by the formula, no more no less.

The calculations seem like a PITA, but certainly, if that’s the only thing standing between you and early retirement, it’s worth it.

Also, if you leave your job when you are at least 55, you can access 401k money penalty free. However, this money must stay in a 401k for this to work. If it is rolled over to an IRA, the age for penalty free withdrawals is the standard 59.5

Thanks Ervin, great answers

Beautiful post again. Thanks again Jeremy. Absolute brilliance.

Thanks to you, I actually took the time to model the intricacies of the tax code in Excel. It’s about as good as Taxcaster (checks out to within a couple of bucks), though it’s better in some regards. It clearly shows effective marginal tax rates for each I actually modeled several of the complexities of the tax code.

Here’s the link to download:

https://www.dropbox.com/s/gpl4mdsmjfqrfwc/2014%20federal%20tax%20calculator%20-%20Shared.xlsx?dl=0

I wrote it for my personal use, so I think I hard coded in assumptions like married filing jointly. # kids is an input parameter.

The best thing about this spreadsheet is that it can be updated in 5 minutes from year to year, allowing me to strategically defeat that US tax code through optimal deferrals + roth conversions…..

Once you have kids, the EITC is a magical thing…..and one with screwy incentives as the credit winds down.

Unfortunately for many seeking early retirement, the EITC isn’t available. We have low enough incomes, but getting earned income in retirement is a little challenging. But the largest impediment is the limit on interest, dividends, and traditional IRA withdrawals. If you exceed about $3000 of “investment income”, you don’t qualify for the EITC.

GCC definitely has over $3k in investment income, and even our more modest size portfolio spins out about $9k in dividends and interest.

The EITC is actually a fairly well designed program since it keeps millionaires like GCC and my household from receiving what’s supposed to be low to moderate income assistance. I like free money as much as the next guy (maybe more), but I like well-designed government programs even better.

Thanks Brian.

I too did the analysis in a spreadsheet, and use Taxcaster to double check, but mine is a big gnarly mess that even I don’t understand. Thanks for sharing yours

Would the combination of any earned income (over standard deduction and personal exemption) + Long term capital gains need to stay under the $73,800 to remain in 15% marginal rate for the 0% long term capital gains?

So, would (taxable earned income + LTCG(and qualified dividends,etc) < 73,800)?

Everything is progressive, so if income exceeds any of these thresholds, you pay the higher marginal rate only on the excess

For example, if our estimates turned out to be low and we actually had an extra $10k in income, we would pay tax only on that $10k. If it was interest income, business income, or earned income, it would be taxed at 25%. If it was dividend income, it would be taxed at 15%

The only time when all dividend income will be taxed at 15% is when earned income is high, putting you in the 25% tax bracket or higher

Does this answer your question?

I guess I’m asking what are all the incomes used to determine the marginal tax rate if you want to stay at a 0% long term capital gains rate. Would the gains themselves add onto your gross income? And possibly put you into a higher marginal rate no longer giving you the 0% capital gains.

sorry I don’t know if I’m wording the question well. Thanks for the info though!

See Step 1 above. That is where I am verifying the max income levels

As for income sources, a real world example might help, particularly looking at a 1040 form. See this example: https://gocurrycracker.com/the-go-curry-cracker-2013-taxes/

Or I explain it in a slightly different way here:

https://gocurrycracker.com/never-pay-taxes-again/

Playing around with tax caster helped with my question. Awesome info!

I’m not very savvy on IRAs but isn’t there a 10% early withdrawal fee to move from Traditional IRAs to Roth IRAs? I didn’t see that mentioned anywhere in your article, did I miss something?

Hi Joe

Short answer: No, there is no penalty

Long(er) answer: If $ are withdrawn for spending, there is a penalty (except in a few specific cases.) A Conversion is a different thing altogether

This is what the IRS says in Publication 590:

“You can withdraw all or part of the assets from a traditional IRA and reinvest them (within 60 days) in a Roth IRA. The amount that you withdraw and timely contribute (convert) to the Roth IRA is called a conversion contribution. If properly (and timely) rolled over, the 10% additional tax on early distributions will not apply. However, a part or all of the distribution from your traditional IRA may be included in gross income and subjected to ordinary income tax. ”

As in the post above, as long as income is sufficiently low, the effective tax rate is 0%

Good question

Jeremy

Hey GCC, I am a tax guy by day trade. Big props for the level of detail you give when going over this each year. You do a great job of showing how to execute a great tax strategy!

Thanks man

Gosh, it’s so complicated.

Does this apply to a non-resident alien as well?

No, that is another complication. Non resident aliens are taxed differently on dividends / interest / cap gains. See here.

I wish i could find someone to pay to do these calculations for me. Any suggestions?

A competent CPA can help. I would also recommend trying to work through it yourself, it seems a lot at first but is not terribly complicated. You can look at our tax return as a reference.

Do you lose dividends by harvesting a capital gain? I understand you re-invest, but you’d have fewer shares.

Sell $10,000 worth of stock, buy $10,000 worth of stock. You have the same before and after.