Oops, I did it again. Another year of nearly $100k in investment income, but with a very budget friendly income tax bill of $0

Oops, I did it again. Another year of nearly $100k in investment income, but with a very budget friendly income tax bill of $0

The same as last year, income was primarily from index fund and individual stock dividends, interest from a seller-financed mortgage on a property we sold a few years ago, and interest from our cash reserves and a municipal bond fund.

This year’s tax situation was a little more complex, since I violated Rule #1: Choose Leisure over Labor. The blog made a small income, so I learned a thing or two about self employment taxes in the process

Let’s go through our actual 2014 tax return, to see how we kept taxes low this year, and took action to minimize taxes in the future

Income

Total real income for the year was $44,640, almost enough to cover our base cost of living for 2014.

All of this income was real, with checks or deposits received from varying sources shown here with their respective line on the 1040 form

Interest (Line 8a): $7,410

Tax-free Municipal Bond Interest (Line 8b): $1,455

Qualified Dividends (Line 9b): $30,166

Non-qualified Dividends (Included on Line 9a): $3,622

Blog income (Line 12): $1,987

Total income: $44,640

We also had imaginary income of $52,469, as a result of a Roth IRA Conversion of $5,744 and harvesting long term capital gains of $46,725

I refer to this as imaginary income because it doesn’t really exist in the same way that a paycheck does. I’ll explain more later in this post, but for now we include it in taxable income

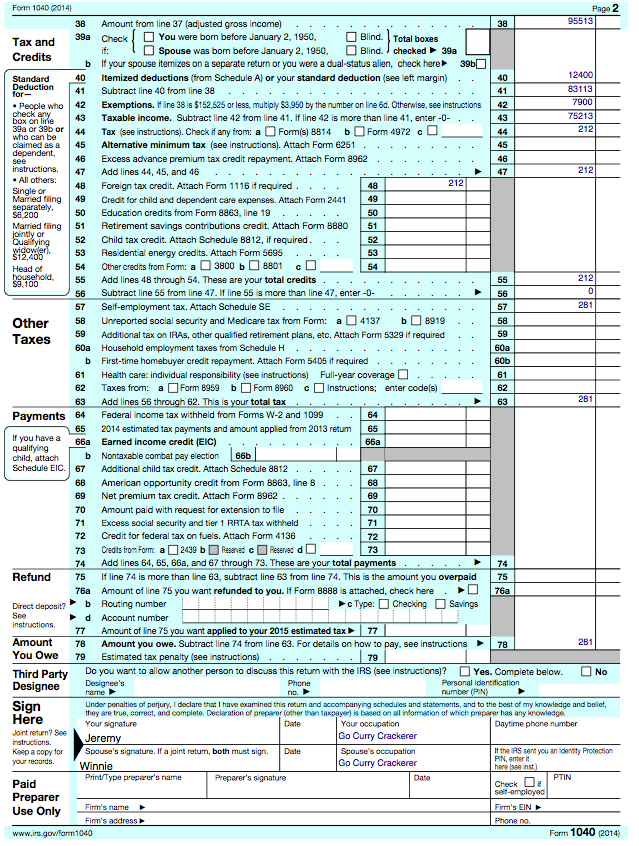

All of these sources of income appear in the Income section on Page 1 of our 2014 1040, with Total Income = $95,644

The only adjustment we have to income is the result of self-employment income from the blog. 1/2 of self-employment tax for Social Security and Medicare is a deduction shown on Line 27

Tax Due

On Page 2 of the 1040, we calculate total tax due. The first step is calculate taxable income by subtracting all possible deductions

As a married couple filing jointly, we have a Standard Deduction of $12,400 (Line 40.) Since we are a family of 2, we have 2 Personal Exemptions of $3,950 each (Line 42.) These deductions reduce our Taxable Income by a total of $20,300 to $75,213 (Line 43)

If you’ve ever done your taxes manually, you’ve probably used the Tax Tables. According to the tax tables, total tax due on $75,213 of income is $10,519.

But look at Line 44. Total tax due is only $212! Why?

When you have income from Qualified Dividends or Capital Gains, the tax tables aren’t used. Instead, we use the Qualified Dividends and Capital Gains Tax Worksheet, which I’ve included below. (If you are super interested in the details, the 1040 instructions for Line 44 explain in depth)

Qualified Dividends and Capital Gain Tax Worksheet

Qualified Dividends and Capital Gain Tax Worksheet

This is where all the magic happens when determining total tax due.

The main point of interest is on Line 8, where is shows a value of $73,800 for Married Filing Jointly. This is the amount of qualified dividends and long term capital gains we can have, tax free! We had a bit more than this, so tax is calculated at a low tax rate of 15% on the difference (Line 20) resulting in total tax due of $212

But $212 still seems like a lot of money. I want to pay $0. This is where the Foreign Tax Credit comes in. We paid over $500 in taxes to foreign governments through an index fund we own that invests in international stocks.

But $212 still seems like a lot of money. I want to pay $0. This is where the Foreign Tax Credit comes in. We paid over $500 in taxes to foreign governments through an index fund we own that invests in international stocks.

The IRS will give a credit for any foreign taxes paid, which appears on Line 48. This completely wipes out any tax liability we have for the year, resulting in a total tax bill of $0 (Line 56 of Page 2 of 1040)

Imaginary Income

Earlier I referred to some income as imaginary. This “income” appears on our 1040, but is really just the result of moving money around that we already have. Today, there is no increase in net worth as a result, but it has a great impact to long term net worth since this income will be tax free forever

Roth IRA Conversion

We moved $5,744 from our Traditional IRA to a Roth IRA this year, which is known as a Conversion. In effect, we choose to pay taxes on this money now in order to pay no taxes on it in the future, the key feature of a Roth IRA

Earlier we saw that the Standard Deduction and 2 Personal Exemptions totaled $20,300, which reducing our total taxable income. We can think of this as first offsetting all non-dividend and long term capital gain income, which is taxed separately on the worksheet we reviewed above

This other income includes interest ($7,410), non-qualified dividends ($3,622), and blog income ($1,987), for a total of $13,019. Since this is much less than $20,300 we create some imaginary income in the form of the Roth IRA Conversion

We could have transferred up to $7,281, but we didn’t have all of the information necessary before the end of 2014 so we had to estimate. We estimated low, doing a Roth IRA Conversion of $5,744.

It is unfortunate, but we left $1,537 of tax free income on the table. But we still win, because the $5,744 that we Converted into a Roth is tax free forever

Capital Gains Harvesting

We harvested long term capital gains of $46,725. You can think of this as selling some stock that has increased in value and then immediately purchasing more stock. This year I sold some individual dividend stocks and purchased more VTI.

From Line 8 of the Qualified Dividend and Capital Gain Tax Worksheet, we saw that we could have $73,800 of tax free qualified dividends and long term capital gains

Earlier we reported qualified dividend income of $30,166

If I do nothing, I leave $43k of tax free income on the table. So I generate imaginary income by selling appreciated stock.

I estimated a little high this year, generating a gain of $46,725. A few thousand of this is taxed at 15%, the maximum tax rate on long term capital gains. This is the $212 tax bill shown on the 1040 and on the Dividend worksheet (which is then wiped out by the Foreign Tax Credit)

This gain is taxed at 0% today, and is now part of our basis in new stock. That gain is locked in, which means it is tax free forever. The higher basis also increases the opportunity to harvest capital losses in the future

Self Employment Income

It turns out, if you have self-employment income you have to pay self-employment Social Security and Medicare taxes at a rate of 2x that for an employee. This year the bill was $281

I always knew this, but since this is my first year having self-employment income I made some beginner’s mistakes.

I at first assumed I could offset this with the Foreign Tax Credit. Not so. The self employment income only appears on the 1040 at Line 57, after the credit is applied. This error caused me to leave $300 in tax credit on the table, while also losing some opportunity in the size of our Roth IRA Conversion. I know better for next year

It’s not all bad though, I made an additional contribution to our Roth IRA equal to our total self employment income of $1,846 ($1,987 – 1/2 of self employment tax.) Since our tax rate is effectively 0%, this is perfect use of a Roth IRA

Conclusions

Overall, 2014 was another great tax year for the Go Curry Cracker household. We paid no tax on nearly $100k in investment income, increased the size of our Roth IRAs and increased our basis in our stock holdings which will minimize our future taxes

I also learned a lot about self-employment taxes. Yes, I left money on the table through some beginner’s mistakes. That is the price of tax education. It is by making mistakes that we learn, and past mistakes learning is how we are able to pay no taxes today

Hopefully this was useful, and will help you also Never Pay Taxes Again

If you like what you read here, please consider sharing. Everybody can benefit from learning how to minimize taxes

—-

As I do every year, I used TurboTax to process and e-file our taxes. I think its worth the price to import everything directly from our brokerage without mistakes, versus the hours it would take to enter everything manually. This year the bill was $59.99, which easily saved 3 hours of my time

—-

See All of Your Accounts in One Place

Track your net worth, asset allocation, and portfolio performance with free financial tools from Personal Capital

I learned about the Self Employment tax in 2014, too. What, they want a cut of our fun blogging income too?

Looks good – we managed $0 tax on just over $100k gross income for 2014 (Mrs. RoG is still working which is 2/3 of that income).

Next year I’ll be a little more aggressive with business expenses. We need a new laptop anyway

Congrats on your own sweet tax bill. Well done

Can someone teach me please? Lol. I have a side business and made about $90k. I get killed being in CA.

Great rundown. Did you continually harvest gains in the same way while you were employed? Or is there an income level at which you can’t take advantage of paying zero taxes on up to $73,800 of long term capital gains?

Ditto on using turbo tax

I never harvested gains while working, since other income pushed us out of the 15% marginal rate. At that point long term gains are taxed at 15%

I did harvest capital losses though

That’s kinda what I figured. Thanks for answering my question.

Wait, are you saying that the first $73,800 of long term capital gains is tax free for a married couple?

I am single so I think my number is $36,900. I have been sitting on some stock that has appreciated greatly. If I sell the stock, the first $36,900 of profit (long term capital gains) is completely tax free???

If so, wow. I need to start harvesting, too.

This statement is only true if you have no other taxable income. If you’re still working or have other substantial income you won’t benefit from the 0% tax on Long-Term Capital Gains. You have to be in the 15% bracket with all taxable income to fully benefit.

Thanks or clarifying. It sounded to good to be true.

Still good to know though. If the gains are high enough, it might even be worth taking a year off. Or if earned income isn’t too high, maybe you can harvest some of the gain

You can model this with your own income using Taxcaster

https://turbotax.intuit.com/tax-tools/calculators/taxcaster/

Can you explain this? “This gain is taxed at 0% today, and is now part of our basis in new stock, which means it is also tax free forever.” Why is it now tax-free forever? You wouldn’t pay capital gains tax in the future when you sell it again (taxing the gains on your new basis)?

The gain from 2014 will never be taxed again. It was taxed this year, it just happens that the tax rate was 0%

Maybe an example will help

You buy Fund A for $50k, and sell it later for $100k. Your gain is $50k, and like in this post’s example is tax free

You now buy Fund B for $100k. Your basis is $100k. You can only be taxed on the gain above your basis, so your $50k gain is locked in forever

If Fund B grows to $150k in 2015, you can harvest the gain again. In theory, you could increase your basis each and every year

What if you don’t buy a Fund C. Would your gains become taxable?

No

Yes but only gain from 100k not 50k.

Love it, particularly the occupation line. ; )

“There is no increase in net worth as a result” – This is a true statement, but there is a substantial retention of net worth as a result which is an important distinction. You know this, which is why you do it, I just want to emphasize it for any readers who might gloss right over that subtle little point.

On the mistakes, I guess next year you have 2 options: 1) spend more than 10 minutes on tax planning or 2) go a bit more aggressive and maybe end up paying a few hundred in tax. I’m not sure it’s worth any extra time other than a point of pride by getting it perfect. If you have to pay a few hundred in tax, at least the effective rate would still be under 1%.

Thanks to you, we have the best job title anywhere :)

I modified the post to show there is a long term benefit to net worth by locking in gains at a tax rate of 0%

Next year I will be more aggressive, partially because we will have a Child Tax Credit and another Personal Exemption. It’s ironic that GCCjr’s due date is April 15th.

Love these tax posts (and linked to an earlier version this morning).

I have what might be a stupid question but, hey, you never learn if you don’t ask.

To get the 0% tax treatment on gains, does your earned income (or a combination of earned income and investment income) have to put you in the 15% marginal tax bracket or lower?

I’d love to be able to employ these cap gain harvesting strategies, but don’t know if that’s in the cards until after we stop working.

Yes, total income from all sources would need to be below the 15% tax bracket max

You can model this in taxcaster to get a feel for how each incremental dollar changes the tax bill

You may end up being your own worst enemy when it comes to achieving your goal of never paying taxes again, assuming the blog’s income growth keeps pace with its publication rate of stellar content!

This is indeed a problem. I’ve already made more in 2015 than all of 2014, and there are a couple major media things coming that will drive some serious traffic

But I can’t let the tax tail wag the dog

Pushing this a little bit, could you have invested the blog income in a “Traditional IRA” there by increasing your “Zero Tax band”? This would have allowed you to convert more Old Traditional to Roth?

I had to think about this for a minute. I could do this, but the end result would be the same as just making a contribution to a Roth

Why not open an individual 401(k) and offset all the blog income there?

That could become an interesting option if blog income goes above $11k, as unlikely as that is, enough for Winnie and I both to do an IRA

And of course at some point we’ll have to hire GCCjr so he can open a Roth IRA at his own 0% marginal rate

“We could have transferred up to $7,281, but we didn’t have all of the information necessary before the end of 2014 so we had to estimate. We estimated low, doing a Roth IRA Conversion of $5,744.”

Wouldn’t it be better to overestimate and then recharacterize? For example, at the end of 2014 you think you might be able to do the $5,744. So, for good measure, you double that and convert $11,488. In 2015 you do your taxes and find out you can only convert $7,281 tax-free. You then recharacterize $4,207 back to your tIRA since you have up until April 15 to do so (October 15 with extensions). Now you have fully optimized your tIRA -> Roth conversion down to the last dollar. I know it’s an extra step in there, but it would help get every tax-free dollar possible.

Well… shit. Travis, you are a genius

Consider this my plan of action for 2015 (*smacks self in head*)

You actually have until October 15 of a given year to recharacterize. This is exactly what I tell my clients to do…and not to panic when they see a larger tax bill because of the additional income, as they can make adjustments to get back to within the desired tax bracket.

See http://www.irs.gov/Retirement-Plans/Retirement-Plans-FAQs-regarding-IRAs-Recharacterization-of-Roth-Rollovers-and-Conversions for more.

Thanks for reaffirming Jason

I’ve been looking into doing multiple Roth IRA Conversions with non-correlated asset classes, and then recharacterizing the loser (the Roth IRA Horse Race)

Now that I see the option of the doing a partial recharacterization to get the exact dollar amount, it seems so obvious

Thinking about this more, I now wish there was an unsell option for stocks :P

++++ for Travis being brilliant. It’s easy to do too. TurboTax walks you through the whole thing

Great work!

I have to do some homework on the capital gains harvesting that you are doing here.

Cheers!

Check out this post from the Mad Fientist

http://www.madfientist.com/tax-gain-harvesting/

What is the thought process behind determining how much of the capital gain to harvest versus how much of the Traditional IRA should be converted to Roth?

The money in a Roth IRA has the best tax profile, so that is the most important. Maximize that, and then whatever tax free space is remaining can be used to harvest capital gains

Amazing!!

Correct me if I am wrong. But will the max. amount allowed for a ROTH contribution in this case be $1846, which is the net profit from the blog business minus 1/2 of SE tax ($1987-$141)?

That is correct. I changed the phrasing in the post to make this more clear

You can max out your Roth conversion every year by converting too much, and then come tax season, recharactering a portion of the conversion retroactively.

Oh and also, once GCC Jr is born, you might qualify for the additional child tax credit on line 67 to cancel SE taxes. I haven’t read it in detail, you shoudl check it out.

The recharacterization is now part of our plan for 2015. It’s cool all of the new learning that happens each year

The child tax credit is also a sweet deal. I think in our case the full credit will be applied earlier on the 1040, so can’t be used against the SE taxes, but I still have more reading to do. In any case, this should allow us to increase the Roth IRA Conversion by up to $10k

Great run down. While I’m not familiar with the US income tax system, I think it’s very similar to Canada. It’s always interesting to know how FI ppl file their income taxes as I can always learn a thing or two. Thanks for sharing.

Thanks Tawcan. Do you think it would be possible to do a similar thing in Canada? I heard dividends are not taxed at all?

I love these posts. You guys do an awesome job of getting maximum values from the rules of the system. It’s almost crazy that this kind of thing is possible. I wonder if more people would do it if they only knew, or if they would balk at “only” being able to earn 20k from regular income. Either way, thanks for the post.

Thanks Mr Dragon. It is a bit ridiculous that the tax code makes this possible

its actually ridiculous that this needs to be done. In other countries this would not be necessary. Lets not forget yall all this savings has been taxed when he earned it…capital gains is mostly inflation and there is double taxation at corporte level on those dividends.

Sad that most retirees never can get this efficient

I wish I could get my tax bill to look that way now. Even maxing out all my tax deferred accounts my bill is 5 figures. Looking forward to getting to that tax bracket in the future.

There is only so much you can do while working for a paycheck :(

A few questions/comments:

1. Even though you are overseas, would you have considered a HSA to further subtract from your “for AGI” calculation (may come in handy as your income gets higher)? It would turn to an IRA after 65 if you don’t use the money but money goes into tax free and I don’t think you need to have earned income like an IRA. You can even contribute to the prior year like an IRA up until April 15. Let me know your thoughts on this. MF has talked about it too quite extensively

2. You probably already know that the CTC can be broken out into non-refundable (line 52) and additional child tax credit (line 67). But thought I would mention that since I didn’t see it in the comments. So if you don’t use all of GCC Jr’s CTC (because it can be limited), then you may be able to use the rest of the $1k on line 67. It may help offset your SE tax and you can get that refunded back to you too (so not only a zero tax bill, but it could be that they owe you). Be careful of MFJ phaseouts at $110K though in your planning.

3. Just wanted to also thank you for your continual posts. It has really spurred me to question my own taxes and really think through them strategically. We are still in accumulation phase and in 33% marginal tax bracket this year (ouch earned income and AMT!). We are planning on retiring here soon, but I am doing everything I can for our family to set everything up smartly. You rock! So brilliant!

Oops, to my first point…obviously, it does not “turn” to an IRA, but becomes IRA-ish.

Hi Elizabeth. First, thank you for your very kind comment. I’m very happy to hear that what you’ve read here is helping out with your own tax planning. This stuff is ridiculously complicated, unfortunately

I don’t know much about the CTC yet. Actually what you just wrote clears up some questions I had from what little I have read. Thank you. The CTC and additional personal exemption is going to make next year’s taxes extra nice

re: HSA. Every policy I’ve seen looks like a net loss for us. I self insure right now, and Winnie is (and GCCjr will be) covered by the Taiwan health system while we are here. If I bought US based insurance to get the HSA, coverage while abroad looks abysmal / useless and overpriced

Prior to the ACA, we carried an HDHP because of the small chance of developing a pre-existing condition. I looked at HSA options, and the additional price was higher than what we could save by making HSA contributions

I want to look into the self-employment health insurance deduction. I see there is a line on the 1040 for it, but need to look further. I’ve considered some non-ACA compliant international policies that might be a good fit

Ooohhhh, right. You need a HDHP plan to participate in a HSA. I forgot about that. It totally makes sense why it would be a money loser for you overseas. OK, nevermind. It’s something that I am planning on employing in our retirement budget to help get our above the line AGI down since health insurance will likely be mandatory here in the US.

In fact, I realized this morning that my husband’s employer only prorated their contribution to his HSA in 2014 (new job) and I learned that I could still send in a check to the HSA to meet the family max for the year. I entered it into TurboTax to see the effect on our tax bill and the extra $833 contribution to meet the max dropped our tax bill a few hundred. I could send $833 in receipts to the HSA provider to get reimbursed (had a baby last year) and have no effect at all on our checking account. That’s the beauty of just understanding this stuff.

And yes, very complicated. I am taking an online tax class right now to learn the fundamentals and every single area has a multitude of if/then statements.

Congrats on the baby. Hope Winnie is feeling well. Love that the due date is Apr 15. How fitting. :) My first came naturally on her due date, so you never know.

I wish you had a donate button because between you and MF and other contributors like Cheddar Stacker…it’s saved us so much since discovering this group.

Thanks Elizabeth! Your happiness and excitement is donation enough. Thank you, this is what inspires me to keep writing

Winnie is doing great, although she is ready for the birth any time now. GCCjr seems to be practicing kung fu 24/7, so she hasn’t been sleeping well

One idea for the HSA… is don’t send in the receipts. There is no requirement to get reimbursed for health related expenses in the year they happen. You could let the HSA continue to grow tax free for 30 or 40 years, and submit 4 decades worth of receipts all at once. I have a small folder of receipts in a friend’s basement in Seattle for this purpose from the 2 or 3 years we had an HSA

Question about the Roth conversions.

Is executing one of these just a simple matter withdrawing the money from your Traditional IRA account and then depositing an equal amount into your Roth IRA account within 60 days (to avoid the 10% early withdrawal penalty), or do you need to do anything special?

And then when doing your taxes you just enter the amount taken from your Traditional IRA on form 1040 line 15a/b, but nowhere do you need to report them amount added to your Roth nor do you need to fill out form 5329? That’s all?

I just clicked on the Convert to Roth IRA button in my Fidelity account, and specified a dollar amount. Everything else was done automagically.

Then I imported everything into Turbotax directly from Fidelity and was done. There is no form 5329 in the submission packet out of Turbotax

You did not pay a 10% early withdrawal penalty, correct? (By the way, I love these posts. Seeing how people maximize their real-life tax situation is energizing.)

Correct, no early withdrawal penalty

(A Conversion is not a withdrawal)

Excellent post. Thank you for sharing. You and Winnie are a true inspiration!

Thanks Weili!

Mind detailing what investments are generating that 30k of qualified dividends?

Hi Eli

I outlined our asset allocation here: https://gocurrycracker.com/path-100-equities/

Very impressive. Thank you for the thorough explanations and transparency!

Thanks FF, glad to help

Quick question for you. Since still working, we would benefit greatly from tax loss harvesting. We did not take advantage of it this year b/c only funds w/ losses were international funds. How do you figure your tax obligations on foreign index funds? Is it different harvesting gains and losses on these funds? Can you point us to any reference? I didn’t follow what you did?

Thanks in advance for clarifying and sharing. These posts are extremely helpful!

Hi EE

There are two different things at play here, capital losses and foreign taxes. They are completely independent

You can sell any stock or fund that has gone down in value, locking in the loss. Any loss is first used to offset any gains, but if the losses exceed gains up to $3k can then be used to offset other income sources (such as job income.) Be careful not to purchase the same fund within 30 days to avoid the wash rule, which disallows the loss deduction

Foreign taxes are paid automagically. If you hold some VEU, you paid foreign taxes. This is reported on the 1099 form you get from Vanguard. Turbotax will calculate this for you, or check out the instructions for Line 48 of the 1040

Does this make sense?

Jeremy

The foreign tax part we understood.

Just seems confusing that if you pay taxes to foreign govt on fund gains (dividends) you could harvest losses in US on losses.

When you sell the funds (at a gain or loss) that has only tax implications in US for harvesting purposes? When you pay taxes on dividends, it is to the country where the company of the stock is headquartered ( and then receive credit on 1040 so as to not be taxed twice)?

Am I understanding that right? Seems like a bit of a headache since our losses were small this year anyway, but could be worthwhile in future if losses are bigger so would like to make sure I’m understanding.

Thanks!

That is my understanding

Although you still owe taxes on those foreign dividends in the US. The US is the only government that taxes its citizens on all income world wide, no matter where it is earned. With some countries, there are tax treaties so the dividends just flow through to you in the US. In other countries, they take their cut first

I am curious why you are still holding municipal bond funds. I am accumulating these during my working years, but I assumed I would exchange them for taxable bond accounts once I join you in tax heaven, for the higher yields at lower risk. Do you have sizable capital gains on those bonds that makes it less advantageous to exchange them, or is there something else I am missing?

Great blog, by the way. It is inspiring to see how well all your hard work has paid off. Congratulations!

Yield on MUB is ~2.75%, which is the same as BND. But BND payout would reduce the potential size of tax free Roth IRA Conversion

I should sell the MUB and buy VTI.

Sorry didn’t read every post, so if this is already mentioned forgive me. I have a free app on my iPad called taxcaster. It is fun to see what you can get away without paying any taxes.

Taxcaster is great

I imagine the iPad version is like playing Candy Crush, but more fun

Fascinating stuff here. When I am no longer encumbered by a job perhaps I can sit down to figure this stuff out… Question, do you learn all of these tax strategies from a CPA? The fine folks on the internet? Or just reading tax codes?

Honestly I’m not totally sure. I’ve been doing my own taxes for as long as I can remember, and learn stuff each and every year. I’ve never had an accountant so I’ve pieced it all together via the internet and the school of hard knocks

You mentioned ‘qualified dividend income of $30,166’ Is there a quick and easy calculation to figure out how large your investment would have to be to get said amount.

Lets say for example I would need roughly 20k in qualified dividends during early retirement, how easy would it be for me to figure out how much of said stocks I would need (rough estimate would be great). 100k, 200k, 300k, etc…

Thanks and great post!

Quick and Easy might be to look at the current dividend yield on the S&P500

http://www.multpl.com/s-p-500-dividend-yield/

As of March 20, 2015, it is 1.87%. So yield on $100k would be $1870. For $20k in dividends you would need $1.07 million

More accurate would be to look at weighted yield of all assets (each individual fund, stocks, bonds, etc…)

When are you going to start offering tax prep services? ;)

haha, no thanks! I think that would drive me crazy

Can a single person (over age 55) have $36,900 of qualified dividends and long term cap gains tax free, or can she have $36,900 + $6,200 standard deduction + $3,950 personal exemption (+ $4300 HSA ?) qualified dividends and long term cap gains tax free, assuming no other income?

Also can you explain your comment that the Roth IRA has a better tax profile so maximize the Roth conversion first, and then use any remaining tax free space to harvest cap gains? I don’t understand, and don’t see how you did that?

Many thanks.

A single person can have $36,900 in dividend and cap gain income plus any deductions from Standard Deduction, Personal Exemption, HSA, IRA contribution, 401k contribution, etc…

This is reduced by any other income, including a Roth IRA Conversion

Because the Roth IRA funds will never be taxed again, I prioritize those. Use the tax free space from Standard Deduction & Personal Exemption to maximize the size of the Roth IRA Conversion. Any other tax free space can be used to harvest gains

I am new to the blog, so I didn’t follow your year 2014 data. However, if you lived outside of the US for the whole year (minimal vacations back don’t count) you should have been able to avail yourself of the Foreign Earned Income Exclusion to get the SE income tax free. It doesn’t help with the SE Tax, but it does allow you to eliminate the income tax.

Hi Bex, my understanding is the foreign earned income exclusion only applies if we are taxed by a foreign country. Since we are not, we still have to pay US tax

Hi GCC, that’s not the case, foreign earned income exclusion can be used even if no tax is assessed by foreign country. So if a US citizen lives in Dubai, he can exclude $99,200 (2014) from tax in the US. Of course, the first question to ask is are you qualified for this exclusion. Once you are qualified, you can exclude the income from tax.

The downside of the Foreign Earned Income Exclusion is that you can’t use the excluded income to qualify for minimum income tests (which are relevant for the Child Tax Credit, IRA contributions, and probably others). As an American living abroad, I took the FEIE to simplify reporting (no need for 1116 which is a pain) until the year my first child was born. Basically, with the FEIE, the goal is to reduce taxable income to zero, but with the CTC, the goal is to get a $1000 refund for each child.

I should note that I wasn’t fully initiated in the FI community at that stage, so I’m not sure how the FEIE would interact with Tax Gain Harvesting.

I don’t see how you say you didn’t pay any tax. Didn’t you have to pay $281 in self-employment tax? That’s what it looks like on your 1040.

We paid no tax on the investment income (line 56 = 0)

Due to some accidental blog income, we did pay SE tax (line 57)

Maybe poor wording on my part

Great read. I’m sorry I didn’t read all the comments, so if this is in there and a repeat, I apologize.

For taxes, I put the dividends and capital gains worksheet into Excel and tied it to my investment income worksheet. I do my taxes twice for each tax year. First time is late December so I can see what I can convert into our ROTH accounts. Using YTD income and a few estimates, I come within $50 of maximum tax free conversion every year. The trick is to use “goal seek” to get to the “married filing jointly” maximum.

The second time I do taxes is in April since congress has a bad habit lately of finalizing tax changes until late Feb.

We have been living off of investment income since we retired at 40 and we’re now 49. Travel half the year and just bought another home with the “interest” income we made off of the last 5 year’s ROTH investment income. Obviously, we can only draw off of the amount we deposited or converted, but you get the idea: we drew down our ROTH to pay cash for a house, and the balance is what it was 5 years ago, ergo, “free house”.

The biggest change we were forced into when we quit work was moving from our home state of TN which, actually, does have a state income tax. They claim they don’t, but the Hall Income tax is only levied on dividend and interest income. That’s OK, we like NW Florida better anyway.

Glad you’re doing this blog. Our still working friends told us to write a book describing how we did what we did and you guys are doing a great job doing just that. We never wrote a book because we know folks would buy it and never live the lifestyle necessary to get there. The coolest part is that once you’ve lived like you’re broke, it’s easy to forego luxury items later too. Yes, we occasionally splurge, but we found we are perfectly happy living simple even with loads of cash. We did a backyard patio party last night with a neighbor instead of going to a bar, club or restaurant and had a blast.

Happy travels, we’re heading South today to meet friends for a mini vacation.

BTW…. I use T Rowe Price for all my brokerage accounts and they give me a free copy of Turbo Tax every year which also allows me to roll the investment data into it and file $0 electronically every year.

Love this article! Its great to see these tax strategies…ie, Its great to have someone figure this out in advance so I dont have to! Haha…Thanks so much for posting this, it is incredibly informative, educational, and inspirational.

One tiny question: Do you access Turbo Tax through Vanguard? I read you have Vanguard accounts. If you have enough money with Vanguard, or other services (my 401k is through Vanguard for example) you can get TurboTax online at a much reduced rate. Im paying $10 for TT Premier this year.

Just a tip for anyone who is eligible…

Thank you! My husband and I just started Vanguard accounts this year and we always use Turbo Tax. I had no idea there was a discount!

Thank you for sharing so much information! I am new to your site and am rather overwhelmed by all the financial lingo and strategies. I am a single, 30-year old, self-employed music teacher with relatively low expenses but unfortunately I do have a bad habit for buying stuff I don’t need. Last year I opened a traditional IRA and this year I set up a SEP-IRA as well. I maximized my contributions to both accounts this year, but got crushed with the Social Security tax. I have a savings account with Chase bank as well, but I feel funny just sitting on it for 0.01% “interest”.

Other than my two retirement accounts, I am at a loss for what else I can do to achieve the financial independence you have.

How do you suggest I get started? Any resources you can recommend?

Hi Nicci

This post outlines on overall path to financial independence

https://gocurrycracker.com/how-to-retire-in-your-30s/

Hope it helps!

Jeremy

Haven’t seen this yet .. since you have a business and medical expenses hire your spouse and use a spousal section 105 HRA plan to reimburse your health expenses pretax. This reduces income and SE tax. Your spouse has to do legitimate work for the business though.

I just looked up the Section 105 HRA. Very nice

I’ll have to dig into it more deeply

” Since our tax rate is effectively 0%, this is perfect use of a Roth IRA”

Technically your income tax rate was exactly 0%. Your taxes of $281 paid were self employment taxes. If you worked a job to earn the $1987 you reported on line 12, your employer would have paid 7.65%, and you would have 7.65% deducted from your paycheck and this would never show up on your 1040.

If you ever exceed the IRA contribution limit with your self employed income, you can always open a self employed retirement account (SEP IRA – though I think the contribution limits overlap with personal IRAs?, SIMPLE IRA, and solo 401k)

Agreed. If the day ever comes when income is sufficiently high (>$11k), I’ll probably open a Roth solo 401k

My knowledge of the US tax code is pretty weak and this was eye-opening! I’ve been scratching my head trying to figure out how to keep our tax bill low when we reach financial independence. I guess the lesson here is to keep building those taxable investment accounts and one day you really can live off of the long term capital gains and qualified dividends. Thanks for sharing a real world example of this!

You are welcome, Spencer. Glad it helped!

For most people building the tax-deferred accounts should be the priority over the taxable accounts, to take advantage of the immediate tax deduction. Then any tax savings and other savings can be deposited into a brokerage account, for the tax free LTCGs and QDs

Interesting post, Jeremy. One thing I’d like to know is whether you are impacted by the Alternative Minimum Tax, and if not, why not. It looks like the threshold for Married Filing Jointly is $82,100 for 2014 and $83,400 in 2015. If I’m not mistaken, it is based off of your AGI on line 37 of the Form 1040. I’d like to increase my IRA to Roth conversions as well, but it looks like I bump into the AMT along the way.

We were not impacted by the AMT

It is more complicated than a simple threshold test. You have to calculate tax due the normal way (as done in this post) and also the AMT way (on Form 6251), and pay the higher of the two.

Turbotax does this automagically, but the AMT still allows for favorable treatment of Long Term Capital Gains and Qualified Dividends, so Form 6251 results in an AMT of $0

I’m not sure if this was intentional on your part, but it seems that you posted pictures of page 2 of your 1040 twice and didn’t post page 1!

I’ve seen on some browsers the preview shows page 2 twice, but if you click on the image it loads the correct page.

So as a guy still working for the man, am i better off making my yearly IRA contribution to a standard IRA, then converting to a Roth IRA once we’ve reached FI? I’ve been contributing to the Roth each year in order to minimize future taxes, but now i feel like i might be a sucker, knowing that i might be able to pay 0 tax now and 0 tax later if i’m reading this correctly. I shouldn’t need to touch either my Roth or traditional IRA funds until we’re at traditional retirement age.

If the Traditional IRA contribution is tax deductible and you invest the tax savings, then most of the time the answer is yes.

https://gocurrycracker.com/turbocharge-savings/

https://gocurrycracker.com/roth-sucks/

It somewhat depends on the marginal rate you are paying today (both federal and State.) If it is 25%+, then you are usually better off with the TIRA. If it is 0%, you are best off with the Roth. In between it is more fuzzy, but generally favors the TIRA

I’ve read your posts over the years about Trad vs Roth and worked hard to wrap my mind around your perspective many times. I get stuck though when trying to apply the reasoning to me because as I recall your examples usually use a couple (and the relevant exemptions & deductions, etc), with the occasional reference to how this applies to a single person. Would it be possible to repost your related blogs and have them specifically walk thru how this would work for a single person at various income levels? It’s hard at least for me and I assume others to really grasp your reasoning while also trying to translate the tax implications (also confusing) and do the math as it relates to singles. Thanks.

Thanks for the feedback, I will attempt to make things more clear for single vs married in future posts

With maybe a few small exceptions, everything you read here can be applied to a single person by dividing by two.

If anything is unclear/confusing, please ask and I can try to help

I am curious if there are people out there who are still working and doing the Traditional to Roth IRA conversion. My wife is working just few hours a weeks right now as we are raising kids. We have a relatively low income with AGI ~ $30K (of memory) thanks to salary minus deductions and heavy contributions to 401k and IRA. So I am well below the $73,800 threshold.

Contribute to traditional IRA and convert traditional to Roth in the same year?

Some do this when they are past the legal limit for doing direct Roth contributions

There isn’t any value in doing a deductible Traditional IRA contribution and then direct converting though, since the conversion is taxed. It would just be the same as contributing to a Roth directly

That’s what I’m starting this year: backdoor Roth contributions. I’m past the income limits for both deductible Traditional IRA contributions and direct Roth contributions, so I opened a nondeductible Traditional IRA. I’ll make my 2015 and 2016 contributions to the full limit, then convert it to Roth.

Sadly, I can’t do this for my wife without triggering taxes because she already has about $16k in a deductible Traditional IRA that we established many years ago before we exceeded the income limits for deductibility. So any Roth conversions for her would be prorated between deductible and nondeductible, and the piece deemed to have come from the deductible IRA would be taxed. Oh well – just have to put more money in the taxable account.

If your wife’s employer offers a 401k, or she were to start a small home business and open an individual 401k, it could be possible to roll the pre-tax Traditional IRA funds into the 401k. At that point all funds outside a 401k would be post-tax, and Roth IRA conversions would be tax free.

An excellent idea, and one which I will surely execute if my wife ever decides to rejoin the workforce. Unfortunately, she “retired” over 2 decades ago when we had our first child and has neither job nor 401(k) at this point.

As always awesome write-up and responses – thks.

I have a general tax question – my wife has just started working part time earning very little income but because of my high salary her wages will be subjected to a high effective rate of tax.

Anything that can be done to shelter her income?

Little info:

MFJ

Max out the 401k

Backdoor Roths his/hers.

There is little/zero that can be done, this is how marginal taxation works.

This is usually where people get sucked into buying life insurance as an investment, buying bigger houses for the tax deduction, or other questionable practices. It is important to not let the tax tail wag the dog. You are doing the right things with 401k contributions and other tax deferred accounts.

Your comment about violating rule #1 brought a smile to my face. And it seems like your punishment will be not only the SE tax you had to pay, but much more of your time in trying to optimize around all the additional variables that your earned income (particularly since it’s business income) introduces. It does look like it will take you a bit more than 7 minutes this year to do taxes :-)

The upside is that earned income does have some benefits (at least wage income – I’m not sure what the ruling is on business income, but I assume it’s similar). You mentioned the Roth contribution, but also you can qualify for the retirement savings contribution credit, the child care expenses credit (if you happen to have any expenses related to this, that were incurred so you could spend the time “working” instead of playing with GCC Jr.), and most importantly the child tax credit. As other people have pointed out, it is a “super credit” since they will pay you back up to $1000 even if you owe zero taxes. BUT that is only if you have income. (Last year, for example, I had a little too much leisure, so I only qualified for $17 of refund.) So it might not be worth it to go too crazy on the business expenses and get down to $0 of business income (though I assume that the IRS can’t force you to declare particular expenses after the fact even if they are incurred. You might be the only business owner to be interested in NOT deducting).

Technically speaking the Earned Income Credit (another “super credit”) has income minimums that you could qualify for with lower income, but it also requires less than $3000 in investment income, so that’s out.

This is turning into quite the pretty multivariable optimization problem. The goal clearly is to use the post-tax-year tools at your disposal to minimize the tax hit.

The fixed parameters (after the tax year is over) seem to be:

*Business Revenues

*Passive Income (dividends and interest)

*Capital gains (assuming you did gains harvesting based on approximations before the tax year ended). This is “fixed” after the tax year since as you noted, there is no “unsell” function.

*Foreign tax paid by your ETF holdings

The variable parameters (the “dials” you can play with to optimize) would then be:

*Roth conversion re-characterization

*Business expenses (how much you offset the income)

*IRA (or other tax-preferred SE account) contributions

*Mike mentioned 105 HRA above. I don’t know enough about it but it does sound promising

Then the goals become:

*Minimize SE tax, but keeping income up enough to qualify for all the other credits, particularly the CTC

*Get the tax liability down to zero before line 52 to preserve the full $1000 of additional CTC (some of which will go to covering your SE tax).

There might be additional grey areas here. For example, it might be worth it to get SE income down so low that you reduce the CTC but still come out ahead in the sum. It’s going to take one hell of an excel file to do this, but luckily you are (paraphrasing MMM) Mr. Go Curry-Fuckin’ Cracker, so I’m sure you’ll wow us all with some snazzy graphs a la the Social Security Torpedo or Obamacare (still haven’t managed to wrap my mind entirely around the brilliant work you did with the latter).

Thanks again for inspiring us all!

Forgot one thing that was also banging around my head: an additional goal is to maximize the use of the credits, since unused credits represent money left on the table (through Roth conversions or Capital Gains Harvesting). This includes the foreign tax credit up to the maximum of the taxes paid through your ETFS, as well as the other credits mentioned above.

I’ve just finished doing my year end tax work and spent maybe 2 hours in total. It probably could have been done in half that, but I was drinking a beer and bouncing an 8 month old kid on my knee.

I’m afraid I may disappoint you with charts and pretty pictures for 2015, but I think I did pull off some pretty sweet tricks to get total payment to the tax man at a minimum, especially considering most of our earned income was unexpected. Stay tuned for full details in the early months of 2016

Amazing blog! Many thanks. However, I have one very simple question: I am an American expat and live outside the US for many years. I still have to file (and pay) US taxes as US government is the only government in the world which taxes its citizens on the worldwide income, which is insane. I manage to exclude a significant portion of my income through the FEIE, FHE and a combination of a standard deduction and personal exemption. If you live in a relatively high cost areas, it is easy to exclude about USD 150,000 of earned income per year. Can you still do the capital gain harvesting if you claim FEIE and FHE?

You can still capital gain harvest, but all US investment income would be taxed as if the FEIE etc. didn’t exist. If you are excluding USD150k, then you are well above the range where long term gains are tax free.

btw, the US isn’t the only country that has citizenship based taxation. Eritrea also has that honor.

Am I right to assume that due to your super low taxes, you never had to make estimated tax payments? That looks like a messy quagmire in itself.

You are correct. But estimated tax payments aren’t difficult, no more than paying any other quarterly bill (property taxes, insurance, etc…)

Hi Jeremy,

Catching up on your posts one by one. I am learning so much from your site here. Thank you.

Is it correct in saying that I’m subject to a wash sale if I wanted to TLH by exchanging VTSAX with VFIAX but in my 401k my employer uses Vanguard’s 2035 retirement plan, which holds VTSMX?

Hard to say.

If you tax loss harvested as you say, and there was a purchase of VTSMX in the 401k within 30 days (before or after) of the harvest, in theory that could be considered a wash.

But in an audit, would the IRS look at the 401k? And if they did, would they recognize that a fund within a fund was substantially similar to one you traded?

Thanks for your quick reply Jeremy. I really appreciate it!

Sorry to trouble you with a few more questions on this topic as I’m fairly new to this.

If I were to move forward with the TLH as described above:

1. In my taxable account, do I simply do a “exchange” from VTSAX to VFIAX and switch back to VTSAX in 31 days given that there’s no significant increase in VFIAX? (or is it 61 days?)

2. Is the above all I need to do, and does TurboTax automatically recognize these 2 transactions as TLH when I do taxes next year?

Keep up the excellent work and I hope to meet you someday in one of your meetings. You two are truly inspirations for me and my fiancee!

I only trade once a year in December (if at all) so I would just leave it in VFIAX until the end of next year. That way we ensure gains are always long term and dividends are always qualified.

Turbotax doesn’t know about tax loss harvesting. You just enter or import all transactions, and it adds all the gains/losses. If losses exceed gains, you’ll get a net loss on the 1040.

Read through this Vanguard summary for info on loss harvesting, things to look out for, etc.. The Boglehead’s wiki is also good.

hmmmm…. we are selling our rental property this year, with sizable capitol gains. Maybe its a good year to take off work to finish some home projects?

Maybe. It’s generally a good idea to not let the tax tail wag the dog.

If you earn $1 and pay $0.50 in tax, you still have $0.50 more than you had before.

But obviously taking a year off has its own value.

Hello and thank you for the continuously excellent, thought-provoking information in your posts and replies.

A quick question, which I didn’t see exactly covered earlier.

If (as US citizens), my wife and I work abroad but pay no tax in US due to the foreign earned income exclusion – are we able to undertake a Roth conversion of up to the aggregate of (standard deduction + 2 personal exemptions) per year with no additional tax? If so – when might it make sense to do a larger conversion even if it means getting into the 10% or 15% bracket?

I believe this should work.

The standard deduction / personal exemptions stack with the FEIE, per comments here.

Any Roth conversion beyond the standard deduction / personal exemption will be taxed at your highest marginal rate however. The conversion is taxed as if the FEIE doesn’t exist.

If you are a tax resident of another country, be sure they won’t consider the Roth conversion to be a taxable event.

If we retire and my husband has a pension of 54k what strategy would be the priority — harvest capital gains or convert funds in the 401k to a ROTH even if that would result in a 12% tax?

We have about 2 million in tax advantaged accounts, and wondering if there’s way to decrease it over time before RMDs required (we are 52 so that would be about 20 years)

The way I am calculating it is as follows: If we count on 24k deduction for married couples, the pension would yield 30k taxable earned income each year.

Option 1: harvest capital gains of 50k each year, which keeps us below 80k income and pay zero tax.

Option 2: Convert 50k into the ROTH each year. That would keep us below 80k income, so the marginal tax rate is 12%. The conversion of 50k would cost approx $6k taxes/year but save RMD later. But you lose the opportunity to tax capital gains now. So am thinking the former is better?

It depends… annual spending, health insurance, State taxes, possible tax law changes, and your estate plan all are factors to consider.

If you are on the ACA, additional income will reduce your subsidies for an effective tax rate of 10-15% (or more.)

Obamacare Optimization in Early Retirement.

For RMD, you will need to think about what tax rate you will pay in 30-40 years. That is unknown, but using current rates maybe you are paying 22-24%(or more.) Better to pay 12% now than 22% later.

Upon death, your heirs will get a step-up in basis on the brokerage account (zero tax) but will have forced withdrawals on the IRAs (probably high tax rates.)

No one right answer, but here is my overall thinking on it: Roth Conversions vs Capital Gain Harvesting

PS — thanks for your awesome website and advice on these issues. It strains the brain but is really great to think about in advance!