Flowing that Cash

When you are accustomed to saving a high percentage of income every month, quitting your job and living off your portfolio can be intimidating. It was for us, at least

Now instead of receiving a steady stream of paychecks, making big contributions to a 401k and depositing healthy sums into a brokerage account each month, suddenly money is flowing out of those accounts!

And unlike a paycheck, income is inconsistent. Some months, dividends and interest cover all of our expenses. Most months, it doesn’t.

To further complicate things, there is a mix of 401k/IRA, Roth, and Brokerage accounts with different rules and tax treatment for withdrawals, as well as typical checking and savings accounts.

Should we spend the money in our taxable Brokerage account now, allowing the money in the 401k/IRA to continue to grow? What if we need a lump sum for a large expense? Should we keep a large cash buffer? Should dividends be automatically reinvested or deposited as cash? Does it make sense to harvest capital gains for cash spending?

I’ll share how we manage our Cash Flow, and hopefully answer these questions and more

2014 was one of our most expensive years to date, even more than our cost of living in the United States. When we started the year we had no idea how much we would spend, since it was unclear how much our IVF treatments would cost or how long they would take. This combination of unknowns, volatility, and large expenses provide for a great Cash Flow management example

The chart below shows our 2014 Expenses, Income, and Cash Buffer. Expenses varied significantly from month to month, as did income. Our cash buffer started the year at at a healthy sum, and declined throughout the year

I’ll explain the how and why

Cash Flow Management in 2014

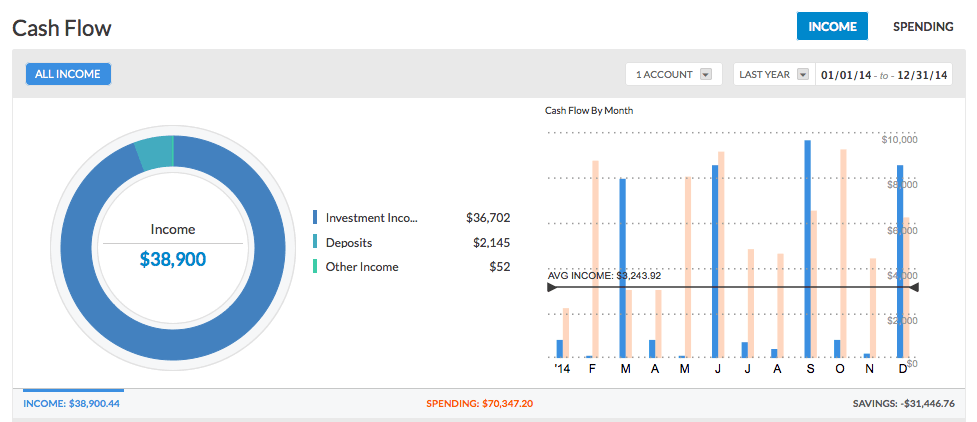

Income

We have multiple sources of income: a seller-financed private mortgage, a few individual dividend stocks, and large holdings in equity funds.

As shown in the Cash Flow Management graph (Red columns), income is very inconsistent. Sometimes our private mortgage is paid on time, but often it is late. Sometimes it will not get paid one month, and then the following month we will receive 2 payments

Dividends are also cyclical, with the majority of income received quarterly in March, June, August, and December. December is a big month, as some funds only pay out at the end of the year

Cash Buffer

Because of the income volatility, we keep a Cash Buffer in our Capital One 360 account (Free $20 when you open an account.) This pays much better interest than our Brokerage account reserve.

All of our dividends are received as cash, which is deposited directly into our Brokerage account. When the cash account exceeds a few thousand dollars, I transfer it to the Capital One 360 account. I prefer to receive dividends as cash as opposed to automatically reinvest, as it simplifies tax time and eliminates any risk of a wash sale if/when harvesting capital losses

The size of our cash buffer varies. Because most of our income is received quarterly, I’ve typically held 3 months of expenses in cash. This year because of IVF expenses, I increased that significantly. You can see we started the year with nearly $40k in cash and it reduced steadily through the year

Cash Flow Smoothing

Rather than just hit the ATM every time we make a purchase or have a meal out, we make every purchase possible with a credit card. (See how we use credit cards to travel for free.)

With a No Foreign Transaction Fee card that offers either cash back or rewards points, we are able to save for our next airplane ticket or reduce our balance due.

Because credit card payment terms allow us to pay for a purchase up to 60 days later, we effectively get a short term loan with zero interest. Purchases made in February can be paid with March dividends instead of with cash on hand.

Year End Asset Management and Capital Gains

December is when we do our tax planning and adjust asset allocation. This involves our Roth IRA Conversion and Capital Gain Harvesting as part of our long term tax minimization strategy. I went through the process in just 7 minutes this year.

Last year in December 2013, because our IVF expenses were unknown I put an extra $25k +/- into our cash account. This year I estimated our spending to be much less, so I returned some of our cash hoard to index funds.

Some retirees prefer to have a larger cash buffer. Jim Collins prefers to carry almost none at all. This preference for a large cash reserve is generally based in the idea that in a major stock market decline, the cash reserves & income would be sufficient to fund years of expenses, preventing stock sales when prices are down. This is a fine strategy for sleeping better at night, even though it historically has reduced total return.

I prefer to keep most of our assets invested. In a market decline, we could quite easily reduce our spending to a level below our income. We could also take advantage of our location independence to reduce total spending substantially. We can continue to harvest capital gains in an up market, and avoid selling them in a downturn except to harvest capital losses.

401k / IRA / Roth

We currently don’t access any of the funds in our 401k / IRA / Roth accounts except as part of building our Roth IRA Conversion Ladder. There are methods to access these funds prior to Age 59.5 without penalty, but we prefer to allow those funds to continue growing tax free.

As discussed here, when saving a high percentage of income it is inevitable that we would accumulate savings in a taxable account. Our strategy is to primarily fund our early retirement years from the Brokerage account, and then access the tax-deferred accounts later in life if necessary.

Large Purchases

Were we to expect a large purchase in the future (a home, a boat, another baby), we would build up a larger cash reserve in the previous year or years to use for that purpose.

If the case of a large emergency expense, in an up market we would sell stock in our taxable account. In a down market, we have our cash buffer, credit cards to smooth out the expense, and worst case we can sell some stock or access the contributions to our Roth or even pay a penalty and access the 401k/IRA, whichever is the most advantageous at the time.

Easier Cash Flow Tracking

After a couple hours playing with Excel to make the above graph, I took a look at our investment account in Personal Capital. And there it was, our income and expense graph with no work at all.

Personal Capital Cash Flow Screen

I’ve used Personal Capital for at least the last year to track our investments, but never linked our cash or credit cards. As a result, some of our fund transfers appear as expenses and others as income, so the chart isn’t 100% correct. I just linked those accounts so instant access to our full spending picture is now a lot easier

Why not give Personal Capital a try yourself. It’s free.

Summary

For funding early retirement, we primarily drawn down our taxable Brokerage account along with our private mortgage, which allows our tax-deferred accounts to continue to grow tax free.

We manage our cash flow using a Capital One 360 savings account as a cash buffer, and top it off as based on estimates for next year’s spending as part of our annual tax and asset management process.

We use a No Foreign Transaction Fee Credit Card with a Rewards Program as a way to build up points, but also as a short term interest free loan that smooths out our cash flow.

It is our intent to follow this process for as long as the Brokerage account has a positive balance, which ideally is forever.

Jeremy,

Thank you for sharing this, it made my day. So helpful. I now have the habit of checking your blog daily as you are pumping out clever and fun blog posts at the speed of light, and to my delight this particular morning, you had posted this one. the timing is perfect. Sincere thanks.

Great, thanks earlyfi! I have a long backlog of post ideas written down, and now that I’m done with my Chinese classes for awhile I’ve been writing daily instead of weekly. Thanks your letting me know you like it!

Wow, you’ve turned into a posting machine! Another excellent article. While I agree that holding a large cash buffer is a fine strategy (and it provides psychological benefits), the research shows that your strategy of using a smaller buffer and remaining mostly invested is actually the optimal approach because there is less of a cash return drag on your portfolio’s performance.

See, for example, the research discussed in this Kitces article:

https://www.kitces.com/blog/research-reveals-cash-reserve-strategies-dont-work-unless-youre-a-good-market-timer/

Very timely topic, because we were just (and still are) discussing this in depth in the MMM forums.

I set some aggressive growth goals for GCC this year, and if I’m going to get nominated for some blogging awards and garner the attention of mainstream press I need to get some great content out there. Plus, writing and thinking through all of this stuff is a lot of fun

A lot of the recent articles are inspired by direct questions I’ve received either in comments or via email, and I’ve got a lot more to cover.

The Kitces article and others like it are a big reason why we don’t keep a lot of cash on hand. Starting 2014 with a big cash hoard was an exception. The next time the market goes into a big decline, we have other ways to ride out the storm. Thanks for the link, it was a good read

While I am not there yet, my vision/plan is to have 1 year’s worth of potential expenses in a checking account, using this money only for expenses. During that year the multiple income streams will build up, so in essence you are working 1 year ahead for your budget.

That will work. We just shorten that period to 3 months, except when we have big expenses planned

My strategy when I reach FI is to generate enough dividend income to live off of from taxable accounts. This is ready cashflow that is always positive, and has grown above the rate of inflation over the past 80+. If I earn less than $36K in qualified dividends ( or less than 72-73K as married), those dividends will be tax free. The rest of the money should be in tax-deferred accounts, which will hopefully grow forever, and I would never have to touch them.

You also get the standard deduction for tax free income, so you can increase that dividend income by ~$10k/single – ~$20k/MFJ and still pay no tax. Nice little bonus, that one

That is, unless your using that space for a Roth IRA Conversion ladder? You’ll have to touch the funds in the tax-deferred accounts starting at Age 70.5 for RMDs, so good to get the funds out if you can

Eschewing dipping into capital should allow you to leave behind a nice sized estate.

Hi GCC,

That is a very good point on the standard deduction on singles-married of $10K – $20K. The goal is to do some 401K/IRA conversion to a Roth slowly over time. Plus, I might also do some tax-gain harvesting if I have room, in order to bring my cost basis higher.

I totally get the idea of putting as much as possible in tax-deferred accounts today, and getting tax breaks today,and then potentially rolling that amount over to Roths, and hopefully paying limited amount of taxes. Rmd’s, coupled with SS and dividend income will be expensive when/if I get to be 70.

Of course, it might be “cheaper” to get a part time gig at Wal-Mart greeting customers at age of 70, and put my 401K that hasn’t been rolled over there, since that would mean no RMD’s.

I am also recently warming to the idea of doing more tax-loss harvesting. It is easier with individual securities, rather than indexes to do it, in my opinion.

I actually really like your site, and Mad Fientist. You bring some very good points about tax planning and paying as little in tax as possible. If only I had maxed out all tax-deferrals options all those years, I would have shaved off at least 2 years from my FI journey.

Either way, I had read somewhere that you wanted to get EU citizenship. I don’t know much in terms of actual details, but it seems that if you invest 500K Euro in Bulgaria ( by buying government bonds for 5 years), you will obtain a passport. Since Bulgaria is part of the EU, this could give you and your kid access to another developed region ( Europe that is). It’s a lot of money though..

I’ve read some things also about purchasing a home in Spain or France can at least provide permanent residency. With the Euro on the way down (or out) this is starting to look more interesting

I don’t know if you’ve seen it, but our tax return shows a clear example of how we did both a Roth Conversion and Capital Gain Harvesting

It sounds like you’ve got a good plan put together. Thank you for reading and for the compliment, I really appreciate it!

Thanks for sharing this, GCC. It sounds like our approaches are pretty similar. I’m holding about a year’s worth of expenses in cash and plan on replenishing that as necessary in up markets and eating away the cash balance during down markets.

Other than that, it’s going to be year by year depending on what big expenses we have coming up. I can see a new(er) car, possibly a minivan, sometime in 2016-2020. Possibly braces for the kids. A new HVAC might happen by 2022 or so.

The plan is to look ahead as best we can and harvest some gains from the taxable account in good times to fund those liabilities that will come due within the next few years. I might start “paying” for that new(er) car today, for example, even though I might not buy it for 3-4 years. I’d hate to have to sell $10k worth of investments in a major market downturn to fund a car purchase or face the alternative of driving an unreliable car (our current 2 cars are 15 years old now but running awesome).

Sounds like an excellent plan, sir.

Your comment made me think of all of the “emergency expenses” some people seem to run into when their roof or HVAC has a problem. A little advance planning goes a long way

Yeah, I laugh at those “emergency expenses” that others seem to have. 99% are rather predictable. Especially routine things like HVAC and roof replacements. Sure, they might only last half the time you expect, but they aren’t all going to fail at the same time.

“Unexpected” might include a tornado or flood or earthquake that destroys your house and you either are uninsured or the insurance company defaults. There’s no point to predict a specific expense like that, which is why it pays to remain flexible in your plans.

I have a slight advantage in that I was responsible for forecasting 40 years of repairs, replacement, and operating/maintenance costs for a billion dollar toll road my last couple years of working. We had a financial model very similar to what many of us FIREee’s have to forecast future income and spending and make sure we can repay our bonds. Many coworkers couldn’t really wrap their heads around the point of forecasting for our project, and I think that ignorance carried over into their personal lives (they are still working hard to finance those cars, boats, and lake houses!).

Thanks for sharing this, it’s great for me to understand how you guys manage your cash flow and how everything works with the regular and tax-deferred accounts. I envision something similar as what you’re doing once we start our early retirement journey.

My pleasure Tawcan. This methodology has been working great

Another great post, thanks! Have you only been living off of the dividends and private mortgage income, or have you also been selling some stock from the brokerage account? Also, as GCCjr gets older, are you expecting to increase your annual spending, and does that concern you at all?

Thanks OK

We’ve been primarily living off dividends and mortgage income, but sold some stock in Dec 2013 to build up our IVF cash buffer. But to date maybe 95% of our expenses sans IVF are from direct income

I thought through the GCCjr cost question a bit here:

https://gocurrycracker.com/how-much-does-it-cost-to-raise-a-child/

We will have child expenses, but I don’t expect it to be a large impact. He’ll need some necessities like clothes and a bicycle, but there will also be reductions in spending as we avoid taking a toddler to restaurants and bars. That said, we’ve never had a kid before so we’ll see how it goes

Cheers

Jeremy

Im assuming that way your overall balance is still increasing, which has to feel good. Regarding child expenses, I think I’d read that one before, but gave it another look. I guess I was thinking mostly around travel expenses and possibly some other essentials. With slow travel and the other ideas you mentioned I think you will be right. A lot of spending is truly optional, you just have to frame it that way.

Hi Jeremy,

I love your blog and love hearing about your adventures! I was wondering if you could reveal what kinds of investments you hold to kick off the serious amount of dividend income. Hubby and I are shooting to semi-retire in a couple of years but would love to hold some more dividend paying investments to help with monthy expenses. Thanks!

Hi Goldendog, thank you for reading and your very kind compliment

Most of our dividends come from VTI & VEU, Vanguards’s broad market stock fund and international stock fund. We also have a few other dividend paying stocks, but I’m slowing merging those into VTI & VEU

See Dividend Growth Investor’s site (He commented above) as an example of selecting dividend paying stocks for income. I prefer the index fund route because I’m lazy and I never have to think about it, and I expect the broad diversification to have better long term return

Jeremy,

Very cool to see how you guys manage your cash flow. It’s a very interesting subject for many of us, especially those who are nearing financial independence.

I personally plan on a strategy similar to DGI above. I plan to live solely off of the dividend income the portfolio provides, and I suspect the income will grow faster than expenses, thus leading to a healthy margin of safety over time. However, I also like the idea of keeping a little cash on the side in case something big comes up or something unforeseen occurs with the dividend income.

I hope to still be blogging by then, showing budgets for more than a decade leading up to FI and then after FI. Should be fun. :)

Thanks for sharing!

Best regards.

Thanks Jason

It will definitely be cool to see income and expense statements over such a long period and pre/post FI.

I hope to still be blogging in 10 years too, it will be cool to look back at income & expenses for us in different times and locations, pre/post GCCjr, etc…

Interesting article, and an important subject for those planning early retirement.

I’m pretty much financially independent now, but still working to add some margin of safety. To get used to the idea of living off my investments, I’ve started doing that while still working. I pay off my bills with the dividends from my taxable brokerage account. Earnings from work go into a separate savings account (and are sometimes used to make stock purchases).

I’m still trying to figure out the optimal amount of cash reserves to balance peace of mind with opportunity cost.

Hi JD

We did something similar our last few years, depositing my whole paycheck into the Brokerage account. The margin of safety goes up substantially when you can save 100% for a few years

How much cash to keep on hand is definitely a balance. We aim on the low end (3 months worth) to keep most of our investments at work, knowing we can reduce expenses below income if need be.

You are a financial whiz! When I see all those numbers, rules and everything, my eyes glaze over. Where did you learn all this stuff? Can you recommend a good book or website for those that are math and finance dumb? Thanks!

Normally I just say I’m a finance geek, but I like how you said it better! ;)

Funny you should ask, I’m writing a book. I’m on page 1, so it will be awhile.

In the mean time, there are a lot of posts that I’m proud of on this site, and also check out my blog roll for a list of some of the sites I really like

:) Page 1? Well pick up the pace, after all, time is money and I’m not getting any younger! I’ve already put off investing too late. I need a finance and investments book that puts it out there in plain English for me.

I will start from page 1 of your blog to look at all the posts. I’ve already read quite a few (and enjoyed them immensely!) but once again, the finance ones had jargon that eluded me.

Thanks!

Art can’t be rushed :p

Have you read Jim Collins’ stock series?

http://jlcollinsnh.com/stock-series/

If anything doesn’t make sense, just ask. I’m always happy to help

This is a great explanation of expenses in retirement and strategies to manage it! I’ve been trying to focus more on creating a game plan for when we are FI in a few years, reading up on different strategies and such, now that we’ve gotten to a 50+% savings rate and have that part of our plan lined up. I had been thinking of keeping more cash on hand – but maybe I’ll have to rethink keeping less around!

Hi Mrs SSC

There is a psychological benefit to keeping more cash for some, but I feel better knowing most of our cash is playing the game rather than sitting in the bleachers. 3 months of cash on hand has been working well for us

Congrats on your great savings rate!

Jeremy

Thanks for sharing! Another nice post! Do you increase your cash buffer when you are in a country that is not credit card friendly?

Noticed that my comment is the shortest one. Felt pressured to add a sequel. I wonder why comments on finance blogs tend to be long and on fashion blogs are often short? :p

Taiwan isn’t the most credit card friendly country, but 3 months of spending in cash is enough. The cash flow smoothing is a bonus, not a requirement

I think you just have the gift of eloquent speech, and don’t rattle on like some of us :)

Haha… I guess there are more right-brainers on fashion blogs and more left-brainers on finance blogs.

I love the frequency of your posts lately – as always, your blog is SO helpful because you’re way more in depth and technical than so many other PF bloggers. Keep it up!

Thanks Emma! I have a lot more coming

Exactly. It’s all about the cashflow cashflow and cashflow that matters at the end of the day. Networth does provide the base there but what we need for our daily working capital is cashflow.

I see a lot of financial bloggers are early retirees or aspire to it. It’s inspiring to me, but I don’t see us being able to do that anytime soon. We’re looking more into working at something we enjoy and having more free time to enjoy life. My spouse is getting a career in teaching, which we think will allow us to have more free time than other careers (with all the 3 day weekends, holidays and summers off), and I am working towards quitting my day job and being a business owner. I hope to eventually pay off our mortgage and add more rental properties to our portfolio, to at least partly pay for our expenses. It’s nice to follow your journey and it’s amazing how you’ve managed to retire and live off of savings and investments.

Hey Felix, that sounds like a good plan.

The cool thing is, after financial independence choices are plentiful. Some people blog, some choose early retirement, and others continue working in some way

Even cooler is none of these choices are permanent

I agree. Having choices is great. And hopefully, if we decide at one point to completely retire early, we’ll be able to. We’ll see next year how we like our new lives (a teacher and a business owner) and if we decide it’s not for us long term, we might work harder towards early retirement :)

your quarterly payout making it unstable, but I see bloggers that have 50 Dividend paying companies, and the dividend seems to be smooth out by then. And with steadily rental income, factor in the maintenance, and vacant. hopefully it would take care of this issue for me in a couple year when I pull the trigger.

Quarterly payouts are fine, I don’t think our lives would change if income was more regular. As long as you know the pattern, it is easy to plan for

Thanks for another great post Jeremy! I’ve been trying to keep up on all your latest posts, so I’m a little late reading this one. Anyway, I love all the detail you get into and how you really break down the nitty-gritty of what you guys are doing. Very helpful!

For some reason, with all the Early Retirement/FI blogs I read, I keep getting stuck on this one point…. How the heck do I save enough in my taxable brokerage and/or cash account to live off of that? I’m mid-40’s and in my prime earning years at my job. I max out my 401K every year and I max out my and my wife’s ROTH IRA every year. Starting this year, I’m also trying to make out my new HSA.

After all that, it doesn’t leave much to save/invest into a taxable brokerage account since we still have regular living expenses too! In a situation like mine, would you recommend stopping all the tax advantaged investments and just pouring every cent into a taxable brokerage so I have an appropriate amount in the next 10-15 years without having to tap my retirement accounts?

The idea of paying any of my bills right now from the dividends my taxable brokerage account is throwing off is laughable! :) I’m mostly invested in Schwab broad market ETF’s, both in my taxable and non-taxable accounts. I currently have a diversification across domestic & international stocks, real estate, commodities, and bonds. About a 70/30 stock/bond split right now, but have recently started moving closer to 90/10. But my taxable brokerage is 100% invested in equities (SCHB, SCHD, SCHH, and SCHA). I’m pretty heavy into SCHB and SCHD, and I honestly think I could get rid of SCHD completely since there is so much overlap between the two ETFs.

I can’t even imagine how much you must have invested in your taxable brokerage to be throwing off so much in dividends each month! Cudos to you!

No, I wouldn’t stop saving in the tax-deductible accounts. Tax the tax deductions now

There is nothing wrong with having the majority of your funds in tax-deferred accounts. If you are mid-40s, plan to work another 10-15 years, you are approaching Age 59.5 where you have unrestricted access to those accounts. There is no need to have a lot in a taxable account

Hi Jeremy,

I echo Dave M. In order to live off dividends only without touching your 401k/traditional/roth, the amount in your taxable accounts must be a lot. I read in one of your articles that to sustain your annual expenses of $39,000 a year, your net worth is $947,000. Would all of the $947,000 be money that you’ve saved in your taxable brokerage accounts since you don’t withdraw from the non-taxable ones?

The $39k to $947k relationship is just based on the 4% rule

https://gocurrycracker.com/what-is-your-retirement-number-the-4-rule/

The funds can be split across any number of accounts, of both the taxable and tax-deferred variety. It is much like if you have a checking account and a savings account, it doesn’t really matter which you use to pay a $100 expense. Instead of checking / savings, think of 401k / Taxable. The result is much the same

You mention that you set up your equity accounts to receive dividends as cash. How do you set capital gains? Cash or reinvest?

I have all distributions distributed as cash in the brokerage account, and reinvested in the 401k/IRA

The last few years I haven’t seen much of anything in the way of cap gain distributions

Jeremy, great stuff as always. What are your thoughts on replacing a “cash buffer” with a “bond buffer” as a sort of middle ground? In that way, you can have your money growing moreso than if it were in cash (albeit at a rate lower than equities in the long run), and that can be something to cash out in a downturn. Looking at Vanguard’s total bond index, it did appreciate during the 08-09 recession.

I would look at it this way:

If you want bonds in your asset allocation, then have bonds. Then do normal re-balancing on a schedule. I wouldn’t hold bonds solely for the potential future opportunity to transfer them to stocks.

There is no guarantee that bonds will return greater than cash. In times of rising interest rates, bonds will potentially perform worse than cash

I recently left a job for a new opportunity and have a 401K decision to make. My new company requires me to wait a year to start making contributions to their 401K account so I have my old one just sitting there with no ability to contribute to it. My wife has a 401K account of her own. I’m trying to weigh my options. I can leave my 401K account sit for a year and then roll it over to the new company account. I can roll my existing 401k into an IRA of my own, or can I possibly roll my 401K into my wife’s IRA? Any advantages you see to any of these options? I’m inclined to just let it sit and start making my own contributions to my wife’s account in the meantime, then roll it over into the new company 401K next year. Is there any advantage to having those funds altogether in the new company’s 401K account rather than starting that account from scratch in a year?

Hi Jeff

Your wife’s 401k is hers and hers alone, you can’t commingle nor contribute. You can only contribute to your own 401k and your own IRA. So for this year, you only have the IRA option (weird practice for a company to not allow contributions, kind of flies in the face of conventional wisdom)

Rolling your old plan to new company or to IRA is a separate decision, one I would base solely on investment options and fees. There is no real advantage to having them together. I left my old 401k with my employer, because it has a 0.03% e/r index fund which is better than the 0.05% I would pay with VTI. If that fund wasn’t available, I would roll it to my own T-IRA. Based on your new company not allowing you to invest the first year, I’m going to assume the plan sucks and you would be better off not rolling it to them

Hi GCC,

Thank you for providing this detailed post on how you manage your cash flow. This has been on my mind a lot lately since we’re less than 3 years away from early retirement and are building our asset allocation accordingly. So you keep a 3 month cash buffer. I think MMM keeps less than 3 months and Justin at Good of Root keeps about a year. I’m guessing that a good strategy for us will be to keep 3 months to a year based on income streams other than dividends. It’s great to be able to compare notes with you guys.

Meant to say Root of Good!!!

Root of Good, Good of Root, no biggie!

I will eventually put together a post on my own cash flow management. I have about a year’s worth of cash right now, but it’ll actually last possibly 3-4+ years since I’ll be collecting dividends each year equal to about 1/3 our spending and if blog income continues at the same pace, it will make up almost 2/3 our spending. Add that to a bond maturing in Jan 2018 and our cash flow spreadsheet makes it look like we won’t even need to sell any taxable investments till 2019-ish. Lots of variables in the cash flow model though… :)

Awesome, I’ll be looking forward to that post! I’m glad to see that your cash flow is doing better than expected. :)

Thanks for writting. I really like your blog. All the technical details of saving and investing process is outstanding but what I learn from most is your phylosophy. One doesn’t have to spend money to be happy. This is really powerful ideal since it forces me to really examine what trully makes our family happy and inspires me start changing my family life style to center around happiness, not spending ( with a vague idea that it might make us happy)

We save most of our income ( own house, own cars, no mortgage, no car payment, no debt, max 401Ks, have college fund for kids and investment accounts) but I never could quite clearly put into words the reasons for doing it like you have articulated so to some degree I was still confused spending with happiness. (Deep down, I knew it wasn’t.) I see my path more clearly now after reading your blog. I will put my $ into purchasing the most expensive commodities: Time and Freedom.

To be more specific, after reading your blog, on Saturday, I took my family to the playground to play hide and seek instead of going out to eat as we often do. The kids loved it and we got some excercise in fresh air. We saved money and gained health. We will start biking next weekend and I plan to walk more. We can walk to the mall, library, recreational center, cinema, a lot of playgrounds and bike to the beach. We live in one of the finest city in the country but I have yet taken advantage of all the free beauty that it offers.

So keep writting. It’s very inspiring to read your blog.

All the best.

Awesome! Way to take action!

It is amazing how quickly these changes become habit and feel normal, and how easily the savings build up as a result. Congrats!

Hi Jermey,

Great article! I had a question on you graph. The “income” shown from seller private mortgage is mixed with principal and interest, correct? If yes, shouldn’t it be split and only interest should be shown as true taxable earnings or income? Just curious…

Hi Kevin

This is just cash flow. We can spend principal just the same as interest as long as the checks keep coming. Cash flow is what pays the bills in the short term.

When filing our taxes, only the interest would be taxed (see 2014 example.) Any principal is just return of capital, although overall I think we still have a net loss on this “investment.”

In short, a cash flow statement and a profit/loss statement would show different numbers.

Make sense?

Jeremy

You might want to check out Fidelity’s Cash Management account. No ATM fees anywhere in the world. And maybe still use capital one for credit since there are no foreign transaction fees.

Fidelity is who we use for ATM withdrawals, but I keep a minimum of cash in that account since interest is ~0%.

See this post.

This blog is really inspiring! I love following you guys! I had a question for you. I am working toward fi. I am 45 my husband is 50. He just retired from the military with a $4000 a month pension; I will get about $2000 a month when I turn 64. I am currently maxing out a 403b that has about $250,000 in it. My husband contributes to a Roth which is worth about $70,000. At the moment I am pouring all left over savings in a taxable brokerage account which is worth about $170,000. I keep wondering if I should be contributing to an IRA as well as the brokerage account. I plan on working another 5 years and was thinking I should focus on the taxable account which I’d like to get to $500,000 and could access well before my pension kicks in. Your thoughts? Thank you for all your wisdom!!!

Stacey

Thanks Stacey.

The thing to look at is the marginal tax rate you are paying now vs. the marginal tax rate you would be paying in the future.

If your future tax rate will be higher, which it might with two pensions, then paying taxes now would be better (save in the brokerage account.) If the future tax rate is lower, save in the IRA to save taxes now.

Also, you can access the Roth contributions anytime without restriction, and you can access the IRA via a SEPP or Roth IRA Conversion. No need to wait until Age 59.5 or for the Pension.

Thanks for referring us to this. I think we’ve thought about carrying a larger cash buffer (up to 2 years) in retirement by default, assuming that our best bet was to avoid having to sell low. But you’re right that we are then subject to inflationary risk at a minimum, and major lost gains worst case. We need to crunch some numbers to see how much we can expect in dividend cash flow in retirement, and how that impacts the rest of our cash situation. Lots to ponder…

I am still suffering paycheck withdrawal syndrome. It is hard for me to see a capital gain as income (spendable income), it would be easier if I had enough dividends as I do see them as income. I am due a mental switch. I use a credit card for everything and pay it off each month with proceeds from stock sold, keeping about a one-month spend at hand. I have rental income but is mostly going to equity. Hardly perfect but I am still transitioning and learning and adapting.

Read through this discussion on the MMM forum. The discussion is interesting, and links to some worthwhile material.

One of the best quotes imho is from a Couch Potato post (links from original):

Yeah, I kind of knew it’s a mental trap but, wow, there is so much written about it. At least I am not the only one with the problem… I guess we all go through the same phases. Thanks for the links. Maybe the only “advantage” of dividends is that the holding period of the stock, for the dividend to be qualified, is shorter than for the long term capital gain (apparently), but it would be likely putting the cart before the horse. And then maybe selling stock as I need the money is not such a bad idea anyway, if I take a constant amount every month would it be like dollar cost averaging? I just sold a bigger chunk to increase my cost basis, something I think I learned here (thanks).

Thanks for this one. It is useful to see how someone else thinks this stuff through.

Hi! Do you have a post for exactly how you withdraw money from your portfolio? Thanks to you, my hubs and I finally started saving properly and we’re just wondering (yes, because we’re idiots), when we would know we’ve hit our savings/withdrawal goal (40k per year) and how exactly we’re supposed to ‘withdraw’ the 40k from everything if we manage to retire early (before 59.5). We’ve ‘verbed’ you btw. When we talk about finances, we refer to you often saying, ‘doing it the gocurrycracker’ way. Many thanks!

Oops, found JLC’s post, lol: http://jlcollinsnh.com/2014/08/25/stocks-part-xxvi-pulling-the-4/

Thanks again :)

They say you haven’t made it until you have been verbed. Thank you! The JLC post is a good one – withdrawing isn’t so complicated.

What is the advantage of doing the cost basis rest versus just selling a portion of shares that would be less than $75k/year? Wouldn’t you still get the benefit of 0% tax?

If you spend only $25k per year then you are unlikely to ever pay tax on those withdrawals. The advantage is in the long game.

Maybe 20 years from now you need to make a large lump-sum withdrawal, perhaps because you find your dream house or maybe you need a new treatment for a rare form of cancer.

What would be better, having a brokerage account with a basis of $X or $X+$1,000,000? (20 years x $50k/year.)

I wouldn’t decline the opportunity to guarantee a future withdrawal is also tax free.

But wait, there is more. Most people have funds in a Traditional account of some type, either a 401k or an IRA. You also get a Standard Deduction of $24k (2018 MFJ.) Why not use that allowance to do a Roth conversion? This guarantees that $24k + growth is also tax free for life.

See our tax return for an example of both cap gain harvesting and Roth conversion.

Thank you very much for the clarification!. Much Appreciated.

Just to provide additional clarity/assumptions on my question above – There is no other income besides my dividends and LTCG. I am at or less than 15% tax bracket. I plan to live on $25k/year (married, filling jointly) for rest of my life (inflation adjusted $25k). Why would I be okay to just sell some portion of the MF/Shares versus resetting by whole position? Thank you!