You Sunk My Retirement! Photo by Rick Bennett

“What?! The IRS can take nearly 50% of my Retirement Fund in taxes?! How am I supposed to live on only half of my savings? With taxes like this, how can I ever retire, let alone early?”

There is a dangerous nuance in the US Tax Code code that is going to sink and destroy your retirement! There is nothing you can do when the Tax Torpedo strikes, taking nearly half of your income with it!

Sounds ominous, doesn’t it?

Social Security Tax Torpedo

The Social Security Tax Torpedo is the name for the phenomenon that occurs when a Social Security recipient has income from other sources, resulting in some of the Social Security being taxed.

The Tax Torpedo often strikes as people reach Age 70.5, when Required Minimum Distributions force withdrawals from 401ks and Traditional IRAs. (Jim Collins has a great article with details on the RMD) It was in this context that I first became aware of the effect, when a reader suggested that if the Tax Torpedo resulted in higher taxes, then a Roth IRA was superior to a Traditional. (You may recall I’m not a fan of the Roth)

Is this the case? I had to investigate

The implementation of this effect is complex. The various explanations I found on the internet were either sensationalist drama, overly complex, or difficult to understand. Hopefully this version is an improvement

The Tax Torpedo in Action

Remember how the US Tax Code works, from our IRS 101 example?

As a refresher, graphically it looks like this for a Married couple Filing Jointly (MFJ) using the Standard Deduction

US 2014 Tax Curve

The 1st ~$20k of income is tax free, the next ~$20k is taxed at 10%, and so on

But what if instead, it looked like this

Marginal Tax Rate for Median Income Social Security

Or even worse, what if it looked like this

Marginal Tax Rates for Max Level Social Security Income

Let’s use an example to make these graphs clear

In the Median Income case, what if you had $50k of income but need to withdraw $1k more from your IRA? Looking at the first US 2014 Tax Curve, you would correctly estimate that $1000 would be taxed at 15%, increasing total tax due by $150

But in the case of a Social Security recipient, instead of being taxed at 15% the tax rate would soar to 27.75%, with total tax of $277.50. Or in the last chart with over $100k income, an incremental $1000 could be taxed at 46.25%!

This is the Tax Torpedo in action. Yeah, I’d be pissed too

How Social Security Income is Taxed

At low incomes, Social Security Income is completely tax free. But as income increases from other sources, such as from Dividends, Interest, Capital Gains, even Municipal Bond Interest, the tax free status is phased out

To determine how much of our SS is taxable, the IRS uses what they call Combined Income. This is the sum of all income from other sources plus 50% of the annual Social Security Income

Why only 50%? During our working years, Social Security taxes are paid in equal amounts by the employee and employer. When we receive Social Security income after retirement, half of the income is in effect a return of taxes paid and the other is income received from the employer contribution.

This is where it gets a little weird

Two different thresholds are used to determined the percentage of SS Income subject to taxation

| Combined Income | Single | Married Filing Jointly | |

|---|---|---|---|

| Lower Base | $25k | $32k | Below this $ level, SS is tax free |

| Between the Lower and Upper Bases, each $1 of Non-SS Income results in $0.50 of SS being taxable, up to 50% of total benefits. | |||

| Upper Base | $34k | $44k | Above this $ level, each $1 of Non-SS Income results in $0.85 of SS being taxable up to 85% of total benefits |

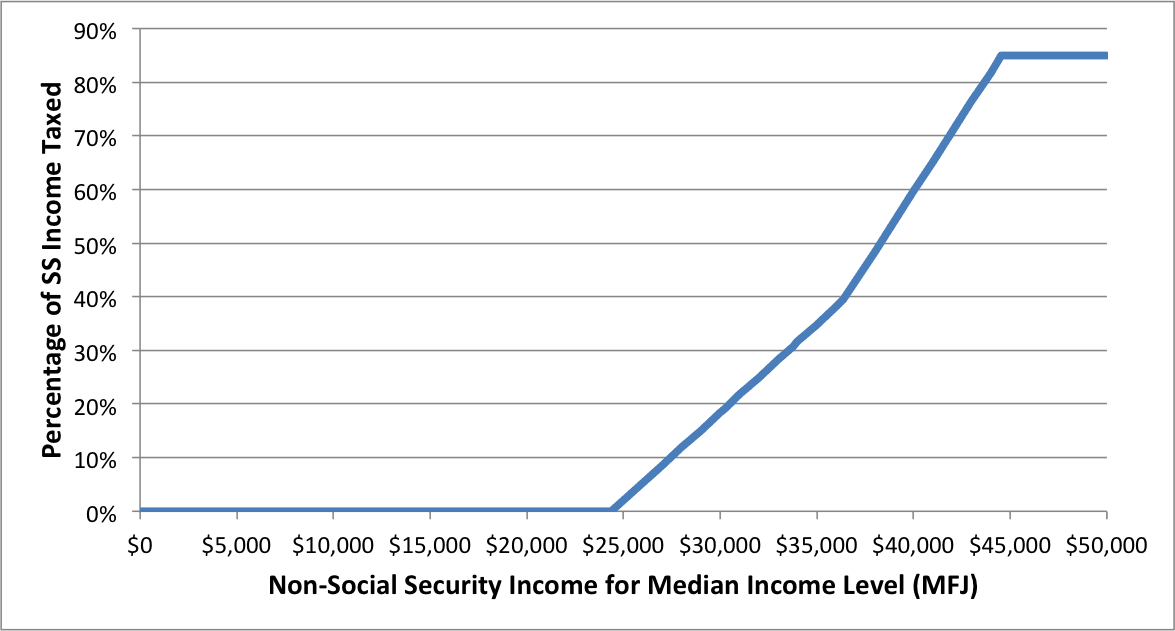

This is easiest to understand in graphic form. This graph uses the Median SS Income of $15228 per year. You can estimate your own SS income here.

Percentage of SS Income Subject to Taxation (Median SS Income = $15,228)

Will The Tax Torpedo Strike?

For an early retiree, the likelihood of having most of SS taxed is lower. And if it does happen, SS Income is lower due to many years of not working. Other income is also lower, as people Live Well for Less and choose Leisure over Labor. And thanks to years of building a Roth Conversion Ladder before receiving SS, RMDs are lower.

But for somebody with high non-SS Income, those with large pensions, and if RMDs are large, then up to 85% of SS Income will be subject to taxation. In this case, this income is added to Adjusted Gross Income

But let’s think about that in another way

If you withdraw $1000 from your Traditional IRA, what percentage of it is subject to taxation? 100%

If you earn interest on your savings account, what percentage of it is subject to taxation? 100%

If you are still working and saving for early retirement, what percentage of your income is subject to taxation? 100%

But in the worst case, only 85% of Social Security can be taxed. That is like a 15% off sale, and you don’t even need a coupon. I will take that deal any day of the week

What about a Roth IRA?

With marginal rates of 27.75% and 46.25%, it would be better to pay tax in our working years at marginal rates of up to 25% and use a Roth, right? Wrong! ;)

The argument goes: Funds withdrawn from a Roth IRA are tax free, and thus are not added to Combined Income for determining how much of SS is subject to taxation. Therefore, if we need an extra $1000 to spend, we can withdraw the funds from a Roth instead of a Traditional IRA with no impact. But there is another type of investment account with the exact same characteristics: a taxable brokerage account

But wait

Those scary 27.75% and 46.25% marginal rates are not actually real. (Some call them phantom marginal rates)

When Combined Income is greater than the Upper Base, each additional $1 of non-SS income increases taxable income by $1.85 ($1 in income and $0.85 in SS)

At the 15% marginal rate, $1.85 x 15% = $0.2775, equivalent to 27.75% tax on the $1.

At the 25% marginal rate, $1.85 x 25% = $0.4625, equivalent to a 46.25% tax on the $1.

But in practice, the taxable income is just added to Adjusted Gross Income.

The tax rate doesn’t change, the amount of income subject to taxation does

And… there is a very important distinction to point out

Subject to taxation is NOT the same as tax due.

100% of the Go Curry Cracker annual income is subject to taxation, yet we pay $0 in tax

Defusing the Tax Torpedo

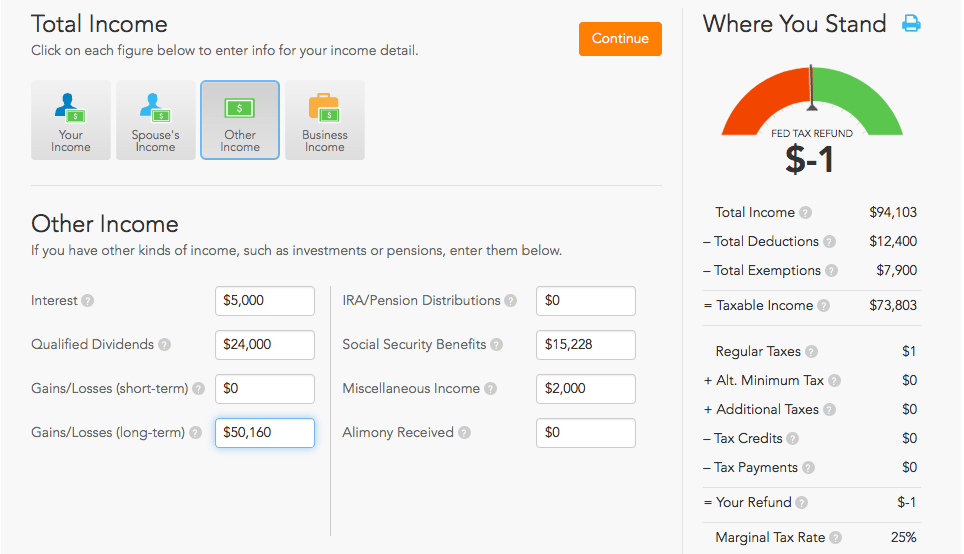

To determine the actual tax impact we can use a tool like Taxcaster

Example:

SS Income: $15,228 (The Median)

Interest: $5000

Qualified Dividends: $24000

Non-qualified Dividends: $2000

Total income: $46,228

Tax due: $0

(Long Term Capital Gains Available to Harvest: $50,150)

Despite the dangerous sounding name, the sensationalist articles about exploding marginal tax rates, and a whopping 85% of the SS income subject to taxation, we had $46k in income and the option to harvest another $50k, all without paying a single dollar in tax

Despite the dangerous sounding name, the sensationalist articles about exploding marginal tax rates, and a whopping 85% of the SS income subject to taxation, we had $46k in income and the option to harvest another $50k, all without paying a single dollar in tax

It might be a torpedo, but it’s made by Nerf![]()

The Exceptions

This isn’t to say some people aren’t impacted. SS recipients with Combined Income around the Lower and Upper Base levels may face tax bills larger than expected if they were assuming SS is tax free.

Reducing Combined Income below the Lower Base will eliminate any impact, particularly those portions taxed as ordinary income such as interest, short term capital gains, and Traditional IRA withdrawals.

This may not be possible for someone with a large pension and high social security income, or with large RMDs. So let’s look at another example for somebody with all 3

Example:

Married Filing Jointly, both over Age 70.5

Pension income: $40k

SS Income: $30kIRA Withdrawal: 30k (Age 70.5 RMD for IRA = $822k)

Total Income: $100k

Tax due (from Taxcaster): $10,016 (A 10% Tax rate)

That is an incredible tax rate on $100k of income, no matter how you look at it.

But what if instead we had this (replace SS with Interest Income):

Married Filing Jointly, both over Age 70.5

Pension income: $40k

SS Income: Zero

Interest Income: $30k

IRA Withdrawal: $30k

Total Income: $100k

Tax due (from Taxcaster): $11,044 (An 11% Tax rate, $1,028 MORE)

If you are someone you love is impacted by the Tax Torpedo, recognizing you paid less tax than if that income was from other sources might offer some small comfort. Taxcaster can help you plan for your own unique situation

The Future & Conclusions

We won’t be able to receive SS income for another 30 years or so. By that time, I assume benefit levels will be reduced

One example: the Lower and Upper Base levels are not adjusted for inflation. With 30 years of 3% inflation, that $32k Lower Base level will be equivalent to $12,800 in today’s dollars. As a result, no matter what we do I can assume 85% (or more) of any SS income received will be taxable. It’s income, after all, and the days of SS being tax free income are over

Because the SS Income is taxed as ordinary income, the size of Roth IRA conversion that can be done at zero or low tax rates is reduced or eliminated. For this reason, we will delay SS income for as long as possible (Age 70 under current law: See Jim Collins’ article for other considerations on when to start taking SS)

In the mean time, the 4 Principles to Never Pay Tax Again apply. Even with Social Security income and the maximum amount subject to taxation, we can pay zero tax

See All of Your Accounts in One Place

Track your net worth, asset allocation, and portfolio performance with free financial tools from Personal Capital

Nice work debunking the sensationalism! It’s especially ironic that, in the frugal early retirement context, the people most susceptible to the Social Security Tax Torpedo are those who grossly over-save and don’t need to rely on social security in the first place. So to complain about it is to speak out of both sides of your mouth: “I can’t count on social security income, because it will never be around by the time I’m eligible to collect! Hey, Uncle Sam is going to take an unfair cut of my social security income!”

Haha, that is funny! You can see how the system has been setup to provide for people if they need it, and for those that don’t… it is still a very tax friendly source of income

Being caught in the cross hairs in the middle zone could be unpleasant though, so good to be in the know.

I view the potential huge taxation of SS in the context of risk. If I make it to age 67 or 70 with a portfolio large enough to generate withdrawals that push my SS into nosebleed marginal rate territory, then I won. I won the game of making my money last into my old age. I won’t enjoy paying more than zero taxes, but I’ll gladly do it knowing that I won.

The alternative is depleting my taxable and tax deferred portfolios in the next 3.5 decades (between age 34 and age 70) and relying primarily on SS to get me through retirement. Sure, I won’t pay any tax but I’ll also be flirting with real poverty. That means I lost.

Great summary of the mechanics, by the way. I need to help my parents figure out optimal SS strategy since mom is a few months from retiring with a pension and they are both over 62 therefore just barely eligible.

I like your thinking.

In the short term, if one wanted to work the system and take steps to keep income below the Lower Base, it would be possible. In the long term with no inflation index, I realized we will just pay tax on 85% of SS no matter what. Better than receiving $0, and will help keep the system solvent for those that really need it

I think we will delay SS until Age 70 no matter what. I expect to live a long time, and the IRR on the delay after age 80 is hard to beat. Winnie won’t ever receive SS except as spousal benefit after I’m gone, so it’s easier to figure out than with two people. Your analysis for your parents would make a good blog post

We’re looking at age 70 SS too. I figure the higher payments after 70 would basically serve as a form of LTC insurance (since we probably won’t be buying LTC).

I think my parents are too private to want a blog post outlining their finances and SS options, but it certainly would be a good one. I might be able to do a hypothetical post that is similar enough but different enough to their actual position.

Love how you put it. It is not uncommon to hear people say that they don’t want to save too much in tax deferred account because they don’t want to pay too much tax after retirement. I mean, even people with PhD degrees in insurance, accounting, or finance.

I’m enjoying playing with TaxCaster, but am a bit confused by the data. I entered some earned income and see that we’re in the 15% bracket. Then added some qualified dividends…and the tax bill went up. Shouldn’t those be taxed at 0% if I’m in the 15% marginal bracket?

The numbers I’m playing with are for a married filing joint couple whose total income (from all sources, including the qualified dividends) is less than $50,000.

That does sound strange. If you want to send me the data you are using via the Contact form, I’ll take a look at what is going on

That was a great post! I had pretty much reached the same conclusion, coming from a different place. And that is, that it is not an issue for people who truly retire early on relatively low income, but for people like myself who retire later (even if still early) with a pension and probably higher SS check when eligible, the tax torpedo does have some effect. It is true that it isn’t as scary when you look at average rates vs. marginal rates. But if you are in the zone, it will still make you think twice about withdrawing that $1000 or $5000 from your IRA. You’ll ask yourself, “Can I wait until next year to buy that X?”

This is good timing. I just finished my spreadsheet model a few minutes ago, after having to restructure it several times to accommodate all the things I kept adding to it. LOL. Anyway, I’m now going to plug in your previous examples and compare results, then send you by email.

Definitely, if you are in the Lower to Upper Base range of income, the incremental tax burden can be severe. Delayed purchases or using capital from the brokerage account instead of the IRA would minimize the impact

With the thresholds not indexed to inflation, more and more people will just be taxed on 85% of the income, which I suspect is the point

I have been planing on starting to take Social Security at age 63, because my wife being a schoolteacher with a pension will get none of my Social Security upon my death. (She will not get social security either since there is a social security offset if you have a teachers pension.). So my thoughts were that it would be more important to preserve as much of our assets that we have – for her to use after my death. She also has a lot of longevity in her family.

I have read that to “win on delaying” you have to live beyond 80. Sure hope I live that long but one never knows.

Great content as usual. Not sure if you remember the commercial that said “when EF Hutton speaks, people listen”. That applies to you as well. Thanks for all you do!

I agree with your thinking. It would be best to preserve assets if you expect your wife to outlive you by a wide margin, and spending SS in the near term can help with that.

I’ve been working through the question of when to take SS. The breakeven point between starting at Age 62 and Age 70 is around 80 years old if you just spend it. Taxes, size of potential RMDs, and investment return on the SS are other factors I’m working through

Haha, I remember those commercials. Here is one:

https://www.youtube.com/watch?v=sc2GpmLx82k

Thank you for that awesome compliment!

Thanks for the post! Very informative and learnt a lot. How social security tax works never really bothered me as I try not to let things I cannot control get into my planning for personal finance. If I have to pay taxes on 85% of the SS income, I consider it a good problem to have.

BTW, I am tempted to get the nerf for my son. :)

I bet he would love it!

I agree, since the Lower and Upper base are not indexed with inflation, we will pay tax on 85% of SS income no matter what we do. For people already retired or retiring soon, being aware of how SS taxation works could help them avoid the phantom tax rates

When you mention Interest Income in your example, what generally would be the source? That seemed like a large amount with today’s low savings account interest rates. Just wondering if there are other sources of Interest that I’m not thinking of.

Regarding the torpedo, I agree with many of the other responses, in that it sounds like an OK problem to have.

You can replace Interest with anything taxed as ordinary income: Short term capital gains, non-qualified dividends, a part time job at Wal-mart (after full retirement age), additional withdrawals from a Traditional IRA, Rental income after deductions and expenses…

The idea there is not so much about interest, but to highlight that every other type of income besides qualified dividends and long term capital gains is taxed more than SS

Another impressive post, Mr. GCC. You’re on a roll.

Thanks for the links to my two posts. This one of yours will be an addendum to both.

Thanks Jim! Glad you liked it!

Your posts are easy to link to because they are brilliantly informative :)

As a researcher and social security specialist, I still consider the tax aspect one of the most complicated parts of the “system” to calculate and explain to people. Wonderful article! I’m thrilled I found it!

My wife and I are in our late 60’s. Our income is around $100,000 a year, from Social Security and Teachers’ pensions. Recently we depleted our IRAs of about $60,000 to purchase a condo. There was adequate money withheld. How will the social security Tax Torpedo affect us?

With 100k in income, 85% of your SS income is taxed every year. The Tax Torpedo doesn’t really impact you

Thank you for your input

I love your discussions. I recommend this website at least once a week to others.

I’ve thought about the torpedo in a different way, but, I’ve never sat down with the numbers

to see if my concerns are valid.

If we wait until age 70 to take SS, I believe we can live comfortably on SS income.

We’ve saved well, so we’ll have a healthy MRD. I know everyone is getting out their

violins to play a sad tune for me. ;-) But, here’s the concern. The savings is our Long

Term Care Insurance. My parent is costing $7000 per month right now, so I know its

good to plan for LTC, even if you plan to self-insure. So, at 70.5, we are forced to take

a pretty significant sum out of IRAs and pay up to 25% (or more) of it in tax, so there goes

a good bit of savings every year. Then, where do you put the withdrawn money? In a

brokerage account, I presume, which is taxed if your income is over $65,000, as I remember. So, the question is, will the taxes slowly eat the savings and leave much less for LTC?

I know people don’t typically live a long time in extreme care situations, but some may.

LTC is a challenge. We are helping now with LTC expenses for Winnie’s grandmother, but fortunately the costs are shared by a larger family. It is great that you are able to help your parent and be there for them

After the RMD, you will end up with more $ in your brokerage account. But you’ll only pay tax on any growth after that point in time. As a reference point, we have more than $1 million in a brokerage account and pay no tax. You may want to start doing Roth IRA conversions before Age 70 up through the 15% marginal rate, it is at least better than 25%.

Thank you for sharing GCC!

I think I disagree with the assertion that “those scary 27.75% and 46.25% marginal rates are not actually real”. The bottom line is that, if you are affected by this extra tax, you will be paying more than you would have otherwise for every extra dollar of taxable income. So instead of being taxed at 15%, every extra dollar of income you take will be **effectively** taxed at 27.75% because I will be giving Uncle Sam that much more money regardless of which money is being taxed.

Sure, if you are affected by the phaseout of tax free social security you might have effective rates as shown in the charts. In 30 years that will be 100% of us.