Choosing an ACA Health Insurance Plan is one of those sentimental holiday season activities we look forward to each year.

Here is the process I used to choose our plan for 2025.

Choosing Our ACA Health Insurance Plan for 2025

First things first, we need to understand the lay of the land.

We are a family of 4 living in California. Covered California provides this handy income/FPL chart (full pdf chart available here), but the concepts apply to any state exchange.

In 2024, the State of California provided their own funding for Silver Plan CSRs which eliminated deductibles on all of those plans. In 2025 that funding was increased so households with income above 250% can also choose a zero deductible Silver 73 plan. Probably worth noting here, a Silver plan typically has an actuarial value of 70% (the insurance company covers 70% of costs, you cover the rest) so a 3% bump here is nothing major – in this particular case they are using the 3% to lower deductibles.

Additionally, children in households with income below 266% FPL (~$83k/year for family of 4) will be enrolled in Medi-Cal, which provides no cost insurance and care (including dental and vision.)

Over the past few years our income has been <266% FPL so our kids have been enrolled in Medi-cal and we 2 adults have been enrolled in an ACA plan. Our premiums for a silver plan have been about $100/month and our actual costs for care have been negligible (low usage.)

Choices

Based on family size and income, the Covered California website (or the Federal exchange) shows the various plans available and their respective costs for premiums, co-pays, deductibles, etc… It can also show projected total costs based on estimated usage of doctor visits, speciality care, and prescriptions.

Ideally, this would all be displayed in a completely different way for easy comparison.

For example:

Cost of 2LCSP – $18,212.40 (2 adults), $26,839.44 (2 adults, 2 kids)

Premium Tax Credits (subsidies) are based on this cost.

Key costs of each metal level – we pay the premiums AND the cost of care, BOTH.

Premium Tax Credits reduce cost of the plan ONLY.

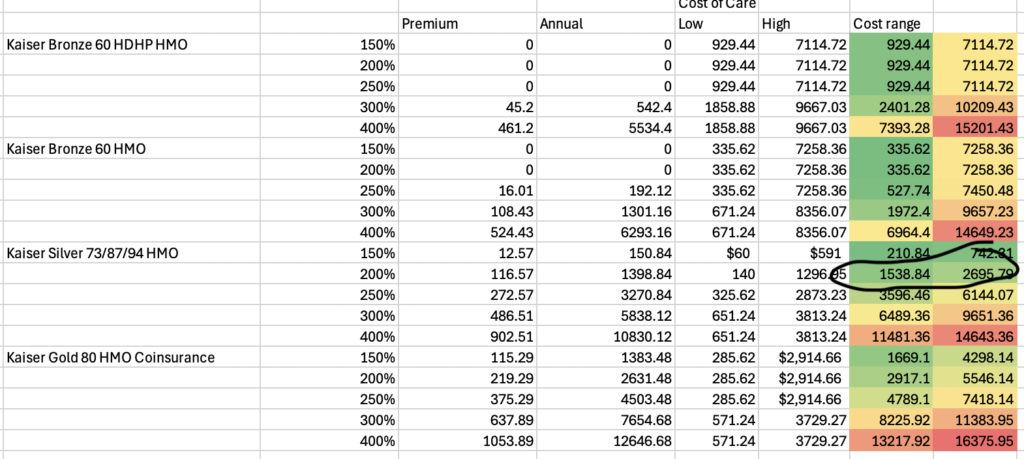

| Plan | Cost (annual) | Cost of care estimate (annual) | |

|---|---|---|---|

| AGI < 266% FPL (2 adults on plan) | Low usage | High usage | |

| Bronze 60 HDHP | $14,770 | $929 | $7,115 |

| Bronze 60 | $15,285 | $336 | $7,258 |

| Silver | $18,363 | 94: $60 87: $140 73: $326 | 94: $591 87: $1,297 73: $2,873 |

| Gold 80 | $19,597 | $286 | $2,915 |

| AGI > 266% FPL (2 adults, 2 kids) | |||

| Bronze 60 HDHP | $21,766 | $1,859 | $9,667 |

| Bronze 60 | $22,525 | $671 | $8,356 |

| Silver 73 | $27,062 | $651 | $3,813 |

| Gold 80 | $28,878 | $571 | $3,729 |

| Policy | Deductible (Individual /Family) | OOP Max | Primary care | Specialist | Prescription (generic) | ER | Urgent Care |

|---|---|---|---|---|---|---|---|

| Bronze 60 HDHP | $6500/ $13300 | $6650/ $13300 | <--- | 0% (after deductible) | ---> | ||

| Bronze 60 | $5800/ $11600 | $8850/ $17700 | $60 | $95 (after deductible) | $19 | 40% coinsurance | $60 |

| Silver | 94: $0/0 87: $0/0 73: $0/0 | 94: $1150/ $2300 87: $3000/ $6000 73: $6100/ $12200 | 94: $5 87: $15 73: $35 | 94: $8 87: $25 73: $85 | 94: $3 87: $5 73: $15 | 94: $50 87: $150 73: $350 | 94: $5 87: $15 73: $35 |

| Gold | $0/0 | $8700/ $17400 | $35 | $65 | $15 | $330 | $35 |

Because the premium cost is a function of income, I find that easiest to understand in chart form.

Decisions

With our typical income of 200-250% FPL we can have a $0 Bronze plan or a $100-$250/month silver plan, with annual premium tax credits of $15,000 – $17,500 plus free insurance and care for the kids (~$9k+ value?)

In theory I could bring our income down below 150% but this would cost us more via loss of the full child tax credit than it saved in insurance costs. Overall this would be a large net negative.

I could also increase income above 300%, even though this is not necessary to support our normal cost of living… and… has the potential to be expensive, in terms of high premiums and/or high cost of care in the high usage scenario. Interestingly enough, more income than we need puts us in the classic insurance tradeoff… should we pay $5,000 more per year in premiums to avoid potentially spending $5,000 more on cost of care. (To which the answer could be yes if we expected a high usage year – as a self-employed individual, health insurance premiums are a tax deduction whereas cost of care is not, typically.)

In the end I made a nice color coded spreadsheet to help visually compare the options, and concluded that an income of ~199.9% FPL ($62,399) would be a comfortable spot in the middle with a Silver 87 plan. We will spend more than if we didn’t need any care at all, but will spend little if something happens.

I think a fine counterargument to make is that with a Bronze HDHP plan we could $8,550 to an HSA. Since the kids are covered by Medi-cal, we could come out ahead over the year as long as care for the adults costs less than ~$2,400 (~$1,400 in premiums and ~$1,000 in tax reduction from HSA.)

I am not certain if this would be the case each of the past 3 years – our cost of care was lower than $2,400, but I can’t say that it would have been on a Brronze plan. For example, I went to the ER for a potential broken wrist and paid $150 co-pay. What would my cost have been on an HDHP plan? I dunno – what is 100% of the cost of an ER visit with X-rays? (And wouldn’t I have gone to an urgent care facility instead, even though it is a longer drive?)

Related Posts

There are a lot of concepts, words, and phrases used in the above text that may be confusing. These prior posts cover a lot of background information.

Obamacare Optimization in Early Retirement

Obamacare Optimization vs Tax Minimization

Obamacare Advanced Premium Tax Credit Repayment Limitation

Summary

We enrolled in a Silver 87 plan with income of around 199.9% FPL. This decision was made based on comparing the various plan options in our marketplace, and finding an option that provided a lot of upside expense protection for little cost. Our Silver 87 plan has no deductibles and very low co-pays / co-insurance / Max OOP.

I always get the HSA-eligible Bronze plan and treat it as catastrophic coverage. Interestingly, because we pay the insurance negotiated prices, I don’t think we’ve ever had a crazy high bill. My son broke his foot last year, and I think we paid about $200 for the urgent care visit and a little less than that for the follow-up in the orthopedic office.

I definitely understand the appeal of the HSA Bronze plans. Out of curiosity, how much more would you spend on premiums if you were on a silver plan?

I wish I had written down the numbers, but it was a sizeable jump. A couple hundred dollars a month for the cheapest silver plan in our area.

Plus, they estimate your total out-of-pocket costs based on your prescriptions and health care needs, and even with the cost-savings of a silver plan, I come out ahead with Bronze by a couple thousand.

I see Steve’s comment below about coinsurance, but my plan has a OOP cap so I know the worst case scenario is that I am paying $16k for care.

Mary, you bring up an interesting point about the negotiated price. Most providers have to also negotiate with the insurance company on what and how they will be paid. Generally speaking we will never know this information until we get an EOB, so it makes our decision making even more complex.

So far in our lifetime my spouse and I have never hit a deductible or out of pocket max. This is quite a pleasant surprise for us after going through the stress of hospital visits and treatment. This has been the same experience for pharmacy as well. I have never paid as much as I thought I would at the pharmacy and I attribute this to the contracts negotiated with the supplier for medicine.

I think it is very important to obtain insurance for your family and to keep track of what things are costing. Luckily in early retirement one has the time and energy to do this if one desires.

I’m sure people know this, but for those ineligible for subsidies, some insurers offer cheaper, off-exchange bronze ACA plans, def a better deal for those who aren’t eligible for subsidies.

Thanks for highlighting this.

I am with you on the expense protection. In my state I am able to select a Silver plan with known daily coinsurance for ER and Hospital admissions. I would rather pay the known $240 per day than the 30-50% for daily coinsurance. When you look at the most common inpatient procedure for my demographic, a hospital stay can easily cost $100K.

I do like knowing the cost of things up front. How many days of hospital care do you think it would require to hit the OOP Max? Is it way longer with the per diem?

In my experience hitting the OOP Max happens on day 1. A ride in a helicopter and going straight into surgery is not cheap.

Yes, that is why I was asking. I couldn’t get my head around how a per diem was better than daily coinsurance.

But wait… there is a story behind this for sure.

I know a few stories first hand. The best was having major surgery and staying two nights in the hospital. Total cost to me was $136. I hope God continues to bless me and my family.

I wanted to expand my answer on this a bit because I am sure that there may be a few of you who say my math does not add up. If you said that, you would be absolutely correct. For simplicity sake, I will call this insurance math.

After going back and looking at my EOB on the example above I find a bunch of terms that I don’t fully understand like allowable charges, denied charges, member discount, etc. All of this got me to thinking. Many of us may be getting care for less than we thought it would originally cost us.

I for one am getting an additional discount on my already low ACA health insurance premium because I go online to my insurers website to complete these little educational activities for points. Once my points build to a certain level I can trade points for a visa debit card that has actual money on it. I have the choice of taking this card to the provider for services or I can pay a premium with it if I want.

There are other examples I can think of where the cost of care was reduced by such things as employee discounts, military discounts, church donations, reward points, extra help and prepaid memberships.

Surely I am not the only person who gets these kinds of welcome breaks on their healthcare.

I am not aware of any non-traditional means to lower the cost of healthcare with our existing health network.

Are you using a broker or applying yourself?

No broker. I am not sure what a broker would do for me

Glad to see I’m not the only one making multi-colored spreadsheets for this.

By minimizing our capital gains, I’d managed our income down to about $46K for the past two years to take advantage of lower premiums and CSR, enjoying silver plans that cost $68(NC)-$330(SC) for a household of 3 adults.

But with our cash cushion running low from a home purchase this year, it’s time to plan for a high-income year ($120K) in 2025 and the higher premiums that come with it. The $68 silver plan we currently have will go to $1057 next year so we opted for a $893 bronze plan as we don’t anticipate as much usage.

Once our adult son moves out, our premiums will increase by by over $300/month since the higher income will be for a household of two instead of three, further reducing our premium subsidy.

The wait times were too long in England but it sure was nice not to have to worry about health insurance. If only we could find a middle ground.

ouch Stackfault, That will be a huge premium increase! Do you have anyway to borrow money with a low interest rate? Think credit card 0%. Maybe postpone this increase for another 18-21 months while your stash continues to grow.

I do love me a multi-colored spreadsheet.

I foresee a similar situation in our future. I will run out of high-basis stock to sell and have to realize a higher income within the next 5+/- years. I will probably start to pull funds from Roth accounts to compensate (still TBD.)

2025 is most likely the final year where there is an 8.5% cap on SLCSP premiums regardless of income, making it not the worst year to realize high income. It can be worth harvesting a small amount of capital gains at 0% fed tax rate as well, pushing income closer to $130k for an effective 8.5% tax rate (+ State.)

Question; if 100% of my income comes from a Roth IRA; does that count as ‘income’ against the ACA AGI?

Qualified Roth distributions are not income for federal taxes or the ACA.

Which means… you wouldn’t qualify for ACA subsidies due to low income and would forego the benefits of the standard deduction.

I see; was simplifying it; I will take out approx 40-60k from traditional IRA, then the remaining 40-50k from a roth. that would give me a taxable income of 40-60k which I could use as income to determine my ACA costs… I should be able to use my std deduction (married filing jointly as well, I assume)..

Yes, this is the way.

hi,

when will the 2025 federal income tax calculator be up and running. thank you

Today: Federal Income Tax Calculator

any chance you could make this colored spreadsheet available to others, I need it for the State of Hawaii, maybe where I could make the FPL input, but then how to I get low use/high use and premiums? I have some forced income coming due over the next few years, and can’t do all the math. :) mahalo

The premiums and low/high usage numbers come from working through the exchange options via brute force. The color coding in the spreadsheet is just Excel’s conditional formatting on that data. Minimal math involved.

Can you breakdown your statement “In theory I could bring our income down below 150% but this would cost us more via loss of the full child tax credit than it saved in insurance costs.”

I thought you would still receive $1400 refundable CTC per kid vs $2000 or a $1200 total extra cost for 2 kids to save $1300+ in premiums and care vs the 199% FPL. What am I missing here?

The ACTC increases with inflation. $1600 in 2023, $1700 in 2024/25.

Using our 2023 tax return as it is the most recent filed:

To get the maximum ACTC for 2 kids in 2023 required earned income of ~$24k. My 2023 earned income was ~$15k, so max ACTC of ~$1875 (~$940/kid.) That leaves $2,125 for the CTC.

Now looking at 2025, with income of 150% FPL ($46,800: $25k qualified, $21,800 ordinary) total tax would be $0. Thus CTC would be $0. I would also lose other credits – foreign tax credit, child and dependent care credit, saver’s credit ($917 combined in 2023.)

Overall saving $1300 in premiums costs about $3k in lost tax credits.

But let’s say it is a wash. The delta between 150% FPL and 200% FPL comes entirely from Roth conversions. A zero cost Roth conversion is a win.

Okay that makes sense. I missed the earned income piece along with the other non-refundable credits received.

I hit my FI number but still deciding on when to call it quits and still learning how to navigate all the potential credits available at that income range.

I’m also looking into a few other deductions/credits such as the potential EITC if I ever have years with <$10k in investment income, reduced lunch, energy credits, home improvement credits, reduced price broadband etc.

Nice, congrats.

It is all a bit of a mess – credits phase out, most are non-refundable, some are proportional to income type, etc…

For completeness… since my earned income is due to self-employment, health insurance premiums are also deductible. So all else being equal, there is some incentive to have non-zero premiums.

Assuming you’re retired and have your same expenses and assets but instead of self employment income you have $40k in part time W2 income for an employer but use ACA for health insurance, which of these 3 scenarios do you think is best:

1)Don’t contribute any to 401k and use your earned income to live on plus a small amount of taxable dividends + LTCG

2.) Max 401k pre-tax and use withdraw extra from taxable to cover the difference and/or do extra roth conversion/withdraws if necessary

3.) Same as #2 but do Roth 401k, which would very similar like doing 401k pre-tax then roth conversion later

I know there are a lot of individual considerations but at a high level which of these 3 options would you take?

Isn’t this the classic Roth vs Traditional question?

For ordinary income tax brackets yes its that simple, but I thought there would be implications for some of those phase outs of special tax credits, subsidies, etc that depend on where the income is sourced.

For example for the EITC, I think it would be best to just live off as much earned income as possible and try to keep investment income under $10k if you can.

I thought I’ve come across a handful of local subsidies and credits that use unadjusted gross income but maybe I’m misremembering.

Off the top of my head I can’t think of any that don’t use AGI?

I was curious if you have looked at the impact of intentionally increasing income in other areas besides ACA subsidies, such as Calfresh or other areas you get discounts based on being below an income threshold (Internet, utilities). You mention you could get below a 150% FPL so that implies you could potentially get to an income level where you qualify for Calfresh, which could be worth thousands/year. Clearly would lose the full child tax credit usage that could be gained via Roth conversions but balancing that vs actual cash savings in the current year via Calfresh/other discounts. Thanks.

I have not looked at this in depth. With the federal program we don’t qualify as there is an asset test, but (I believe) California looks only at income so in theory we could get something.

As I understand it, the program assumes 30% of household income will be spent on food. This is then subtracted from the max possible benefit ($975 for family of 4.)

Income would need to drop to <100% FPL to get the max. At 200% FPL we would get $23/month. At 150% we would get about $5k/year but $0 CTC/FTC/CDCC (but some ACTC... $600?) and future tax on IRA withdrawals since I wasn't able to do Roth conversions. Maybe a wash in the short term and a loss in the long term.

The benefits for internet and utilities are very limited. I am paying only $35/month for Internet now. With low income benefits we could get only $10-$20 month reduction in electrical bill and save 20% on our gas bill (which is typically <$30/month.)