2023 was our second full year back in the US where we were subject to the 3 overlapping tax systems – Federal, State, and ACA.

In theory this could mean that we would have a high tax burden.

But in practice we paid practically zero, with more opportunities to save next year.

The Go Curry Cracker 2023 Taxes

Executive Summary

Total income from all sources was higher than last year thanks to a large tax-free Roth conversion (I learned a few things from last year.)

Ignoring health insurance and related subsidies we paid $352 in total tax for an effective tax rate of 0.5%. Including the $1,139 we paid in health insurance premiums (after $11,941 in subsidies) our effective tax rate is ~2.1%.

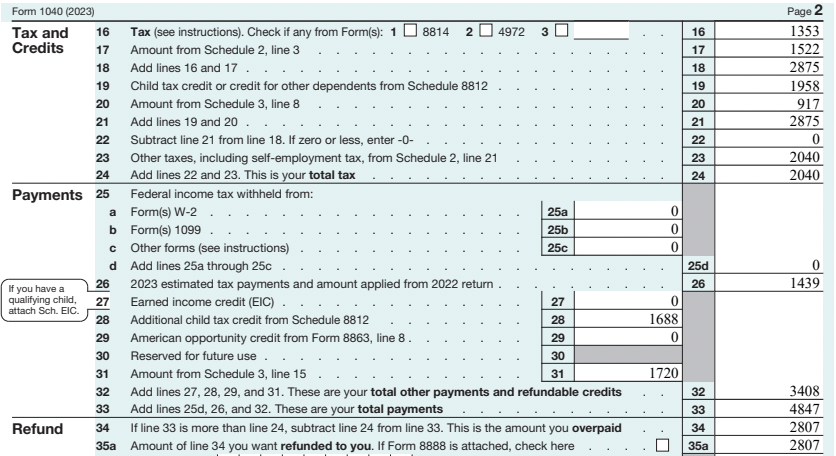

Overall we paid $0 in federal income tax (net $1,688 paid to us in refundable tax credits), $0 in California income tax, and $2,040 in self-employment taxes (which increase future SS income.)

Form 1040

- Income – $70,312

- W2: $0

- Interest: $2,512 (mostly from short-term US treasuries, using money borrowed from credit cards at 0% interest)

- Travel hacking: $0 (but used points to book ~$9,000 in flights and hotels in 2023.)

- Dividends: $31,136

- Qualified: $24,993

- Blog profit: $14,772 (down substantially from last year)

- Roth conversion: $24,892

- Capital Loss: -$3,000

- Capital Gain harvest: $0

- Federal Income Tax: -$1,688

- Income tax: $2,875 (Line 18)

- Income tax: $1,353 (Line 16)

- ACA excess tax credit repayment: $1,522 (Line 17)

- Tax credits: $917 (Line 20)

- Foreign Tax Credit: $450

- Child and Dependent Care tax credit: $67

- Retirement savings contribution credit: $400

- Child Tax Credit (Line 19): $1,958

- Additional Child Tax Credit: $1,688 (Line 28)

- Income tax: $2,875 (Line 18)

- Self-employment tax: $2,040 (Line 23)

- Retirement Contributions: $26,000 (Double Dip.)

- Solo Roth 401k: $13,000

- Roth IRA: $6,500

- Roth IRA – spouse: $6,500

- ACA – MAGI = 239% FPL

- Total premium tax credit: $11,941

- Premiums (paid by me): $1,139

- In advance: $1,139

- Form 1040:

$1,522(paid by tax credit on Form 1040)

- California: $0

- Tax: $730

- Exemption Credits: $1,180 (nonrefundable – opportunity to increase tax burden next year)

- Net: $0

This is how it all looks on the tax return: (copied from OLT, Online taxes – a free filing service)

Roth Conversions and Capital Gain Harvests

Over the past decade we have done annual Roth conversions / Capital gain harvests to minimize future taxes. The future is now.

As in years prior, I used our tax optimization calculator to get a first glance at the options, which is how I determined our Roth conversion size. The calc tells you what is possible tax free at the federal level (but doesn’t include tax credits…)

Were we outside the US, I would have definitely also harvested some capital gains ($50k+ worth!) Doing so inside the US means higher ACA premiums.

But… since we can’t fully utilize all of the tax credits available to us, it would make sense to either do a larger Roth conversion or harvest some capital gains, pushing AGI up to 265.9% (~$79,800.) This is about $13k higher than this year… it’s always a bummer to leave some money on the table.

Inability to Fully Utilize All Available Tax Credits! / Business Deductions

We are eligible for numerous tax credits:

- Child Tax Credit (and Additional Child Tax Credit)

- Child and Dependent Care Credit

- Foreign Tax Credit

- Saver’s Credit

- ACA Premium Tax Credit

Unfortunately only one of these is refundable (the Additional Child Tax Credit.) So if the amount of credits exceeds our actual tax burden then we lose the benefit of these credits… they just fall on the fall.

So it makes sense to increase taxable income via Roth conversion or capital gain harvest in order to fully utilize all of the credits available. But those need to be done before Dec 31 of the tax year or the opportunity is lost.

So I figured…. why not just not claim all of the business deductions available to me in order to have a higher taxable income… the tax bill to me is the same, but a higher income would mean more self-employment taxes paid (and therefore higher future SS income.) A similar thought might come to someone trying to fully maximize IRA contributions.

Why not? All I needed was an extra $1,000+/- in income to get the full child tax credit.

Well… after much searching and exploring, and even contacting the author of a paper from 2006, “No Thanks, Uncle Sam, You Can Keep Your Tax Break“, it seems that claiming all business deductions is REQUIRED BY LAW. Thank you Professor Maule for confirming. (Although the paper does conclude that it would be impossible for the IRS to know which deductions you were able to claim but didn’t.)

In any case… I claimed all eligible deductions, as required.

Estimated Taxes and Travel Hacking

An interesting thing, nowhere on our 2023 tax return does it show the $9000+ of travel I booked using credit card rewards points. (Flights to Taiwan, hotel on the Big Island, etc…)

If you earn award points through credit card usage or signup bonuses, the IRS just treats these points as a refund on your purchases. There is no income and therefore no taxes. (See our Award Travel Series on Transferrable Currencies.)

Ironically, we actually got a lot of these points by paying taxes – we pay self-employment taxes quarterly, and I often use that “opportunity” to meet the minimum spend on a new credit card. I paid estimated taxes of $1,439 (Line 26) to the IRS throughout the year and paid an additional $1,720 (Line 31) when filing an extension to give myself a little extra time to finish this return after April 15.

Why $1,720? Because that is what I needed to finish the minimum spend on my latest card.

If you are going to have to pay some taxes anyway, you might as well get a nice vacation out of it. Even if you are not going to pay some taxes anyway, get a nice vacation out of it :)

Related:

- Aloha Uncle Sam (paying taxes with a credit card to get a free Hawaii honeymoon)

- Award Travel Series: Getting to Hawaii for Free with Ultimate Rewards

Summary

In the US under the triple taxation system (Federal, State, ACA) the incentives are to keep income low. But at low income levels there are numerous nonrefundable tax credits… which require higher income to fully utilize.

I tried to find a healthy balance and did alright in that regard… but could do a little better.

Overall though, it was a good year – we paid next to nothing in taxes, got nearly free high-quality health insurance, and contributed $26,000 to Roth accounts. Social Security income will be higher due to the payment of self-employment taxes. Low taxes now. And low taxes later.

Am I understanding this correctly? You have less than $15,000 in earned income and put $26,000 into retirement plans?

Yes. $13k in Roth solo-401k and $6.5k into his/her Roth IRAs. Roth solo-401k contributions don’t reduce compensation for IRA contribution purposes.

I thought you can only put 20% + of your NET earned income ( $14,772 ) into a SEP/SIMPLE plan ( plus catch-up ? )

How were you able to contribute so much ?

That’s not quite right. The employeR can make such a contribution (20/25%.) The employeE can contribute up to the 401k limit ($22,500 in 2023.)

Our calc goes through the details:

Solo 401(k) Contribution Calculator

Thank you for sharing this info. so generously! I al also confused about the 26k contribution. I thought both Roth and solo 401k’s needed to be funded through earned income?

I linked this in the post also:

Double Your Roth Contributions (Without Working or Earning More)

Ahhhm got it…thank for posting the link (again). I wrongly thought you were reducing your AGI by 26k which I know understand you were not- because ROTH. We are in a position of high cap gains in 2024 due to selling a rental so I’m on high alert for ways to reduce AGI in 2024.

I will read with better attention to the details next time, thanks again for sharing so freely – we have learned so much from you over the years!

You got it, AGI remains unchanged. I’m just putting the money into those Roth accounts for the tax-free growth.

I may be about done with Roth contributions though… about 10% of our portfolio is now in Roth accounts which is probably enough.

Offsetting a rental sale is a tall order, unless you are sitting on a whole bunch of unrealized losses in a brokerage account.

I LOVE reading thru this every year…and agree with one of the posters that you could turn this into a lucrative practice for yourself…

You are a tax wizard and we all take advantage of US tax law when possible, but millionaires gaming the system for free healthcare seems icky to me. I can’t explain it and it is irrational, but that’s my opinion. This is not the intended purpose of the subsidies. Believe me, I wish we had national healthcare for all.

This is wrong. The intended purpose of the subsidies is so every household making 239% FPL will pay less than 4% of income on insurance.

What is the gaming part that inspires the gag reflex? What action would you prefer I take – please be specific.

It is disingenuous to compare a millionaire who manufactures his taxable income to meet income limits for tax purposes and benefits to the hardworking people making minimum wage. You are applying letter of law, I am applying and spirit of law. I think this is pretty obvious to most people.

>I am applying and spirit of law.

You aren’t though. The ACA isn’t for minimum wage households, it’s for everyone that doesn’t get insurance via an employer.

But let’s go with it – what action would you like me to take in order to follow the spirit of the law? (note that all of the actions I did take increased my taxable income, resulting in higher ACA premiums.)

I can think of 3 possibilities, ordered from most reasonable to least reasonable:

1. Apply for health insurance directly through the insurer rather than through the exchange so you aren’t eligible for subsidies.

2. Intentionally realize more income (capital gains, Roth conversions, side jobs) to make yourself ineligible for subsidies.

3. Go back to a full-time job that provides health insurance.

I suppose #1 isn’t too unreasonable, but I wouldn’t expect anybody to do that. Nobody is 100% satisfied with the system we have, but we all have to work within it and make our own decisions about what we are comfortable with.

Those are options for sure.

For #2 I can push income all the way up to $160k before we lose subsidies completely (because I hear the ACA is only for really low income households?)

For #3 I would still get subsidies, because employer provided insurance is some of the most heavily subsidized

Other options:

– refuse to buy insurance at all, pay all health related expenses out of pocket, and pay the individual mandate penalty (no longer at the federal level but exists in California.)

– write a check to the US Treasury to offset any subsidies

The obvious thing that is being overlooked here is the government heavily subsidizes healthcare provided by employers. The subsidies aren’t based on income or net worth, so a low level employee pays the same for their insurance as a someone earning a million dollars or that has a high net worth.

Also there is no adjustment for risk, a young employee pays the same rate as a 60 year with anchronic health condition. How are those things fair?

This idea that health insurance should be tied to your job is a crazy concept. There are pros & cons with any system. I am thankful for the ACA since I have a pre-existing condition & would never been able to get health insurance without it.

Multimillionaires & Billionaires get all kinds of tax breaks, so not sure why specifically the ACA insurance subsidies cause so much angst.

The owners and executives I know have a completely different healthcare package from regular employees. Few of them know what a premium or deductible is because all of that is paid by the corporation.

Most people support some sort of universal healthcare system that would provide affordable health insurance for high earners in addition to middle and low income earners that ACA offers big subsidies for.

Don’t hate the player, hate the game.

agreed

Would you say the same thing about rich folks who choose to send their kids to “free” public school when they could easily afford private school? Probably not, because in the US we view education as a fundamental human right, not a privilege, but we have a harder time viewing healthcare also as a fundamental right.

What about using the post office instead of UPS? Taking the highway instead of the toll road? Relying on the police instead of private security? There are many socialized services in the US that are provided to everyone regardless of income. I, too, hope someday we have national healthcare for all.

Or… are you angry that people who get health insurance via their employer get the most subsidies of all, most favorably to those with the highest incomes?

@JubilantJill, well said!

Thumbs up!

Which ACA plan are you using?

We have a silver plan via Kaiser

Congrats for paying so little! It’s comforting because all of us pay this little on income up to that point right? As a result, it’s good to know that if we end up making the same amount, that would be our tax bill as well.

It’s also comforting to know y’all can live comfortably on that income I in Sacramento. I was feeling stressed for 4-6 months after purchasing a new home last year.

But seeing you guys live on much less and doing fine is very helpful.

I blew up my passive income by about $150,000 after purchasing my house. So I look forward to pay less taxes as well!

Thanks, Sam

It is truly a wonder we poors manage to survive on so little

I know lots of people living well on less $50k a year. If it ever feels like being a millionaire just isn’t enough, it might be a sign that your social bubble could is super well off and/or you are living in super high cost of living area (cough *Bay Area*).

I would hazard a guess that he withdraws from cash accounts to supplement the taxable income to pay for the California lifestyle.

Looks pretty familiar.

We don’t get the child tax credit but did get AOTC which is partially refundable.

We also had some state tax liability because our current state taxes capital gains as regular income.

California also taxes capital gains / dividends as ordinary income, but it is a very tax-friendly state.

We have similar numbers but chose to harvest some capital gains through the 0% bracket. One add’ reason is healthcare for the kids and our ability to have them on our ACA plan. How did you manage healthcare, are the kids ACA-eligible at that MAGI level?

Kids are on medi-cal up to 266% FPL

It would be CHIP where we’re at (PA) which is somewhat restrictive as far as I know – and always subject to funding cuts by Congress. What’s your experience with Medi-Cal, work out well?

Yeah the kids go to the same medical office we do and also get dental.

It seems to work as well as our own insurance.

Interesting take on taxes, I didn’t know one could pay taxes via credit card, but I guess out tax preparer puts the “increased fee” to suggest paying by ACH.

I wish the tax system was more simple, and that tax dollars went to more tangible or visible uses to the public. Maybe then those with the ability to pay more wouldn’t put so much effort into minimizing what they pay, if they see the benefit like libraries, trails, schools, safety nets, etc like other nations have.

Financial Fives – You pay a fee to use a credit card (~2%) so it’s hard to come out ahead on an existing card. However, if you use tax payments to meet a minimum spend on a new credit card with a large bonus you’ll come out ahead.

Financial Fives – You are assuming incremental tax revenune would go towards libraries/trails/schools/safety nets. But that has not been my observation. It was Andrew Carnegie who spent part of his fortune to build 1,600 libraries. Had that being turned over the Uncle Sam in taxes, it’s very unlikely Uncle Sam would prioritize libraries.

I do agree tax laws should be simplified, and many of the complex dedcution and tax credits being eliminated so one does not have to become a black-belt to avoid paying more than the minimum of what one legally owes.

Every time I read one of your year-end tax posts, I ask myself why I’m still working…….. and have no good answer for it, except that I signed up for 20 years

And next year my 20-year obligation is met. So I guess next year it is! But I know I can leave tomorrow if I want to…. And I kinda do. SMH.

How were you able to use your Foreign Tax Credit? Did you have foreign income in 2023?

VXUS pays foreign tax.

While I am a big Vanguard fan, the VXUS ETF is a bad choice. Look at its performance over any # of windows (1 yr, 3 yr, 5 yr) and they lag badly against VOO or other better choices.

With perfect hindsight, US equities have outperformed international equities. Will that continue for all time?

My problem with international funds/ETFs is that for many years now international markets have been tightly correlated to our own, yet even with that they still continue to underachieve against US equities. I gave up on them years ago and have been the better for it, bottom line. But to each their own.

I’m always confused after reading these posts as to where your cash flow is coming from. Almost all our money is in retirement accounts so it almost all gets taxed but I still try to control it to stay in the 12% bracket and maximize the ACA subsidies as I can. If I had to do it over again I would do more of your strategy of having more outside retirement accounts for the tax flexibility. Are you sitting on large cash account balances (I guess no or you’d have more interest income) or is it mostly coming from the Roth?

More than half of our portfolio is in a taxable brokerage account (Taxable / Pre / Post-tax: ~ 57 / 32 / 10 – GCC Asset Allocation 2024)

I sell stock most years (Where the Money Comes From)

I haven’t pulled anything out of retirement accounts yet beyond regular Roth conversions.

When accumulating assets, it almost always makes sense to put money into Traditional 401k/IRA first. In theory we could have done backdoor Roths but didn’t.

Companies paid you $31,136 after 21% tax on gross which was:

= 21% * 31136 / (1 – 21%)

= $8,276.66

but the tax payment was not imputed to you.

Wage income tax would have been.

also sales tax, property tax, vehicle registration tax, airfare and hotel taxes, etc…

State company tax also not imputed to shareholder:

https://taxfoundation.org/data/all/state/combined-federal-state-corporate-tax-rates-2022/

Sounds as if you are getting closer to the FTC-frustration cut off. Something to consider.

https://thefinancebuff.com/claim-foreign-tax-credit-form-1116-hassle.html

Turbotax and OLT both did it for me with zero hassle. *shrugs*

I did a carryback to 2021 when filing our 2022 return, and that was not difficult either.

The bigger issue is that I’ll likely never be able to use all of the tax credit that I am carrying forward, and keeping total foreign tax credit at <$300/$600 (single/mfj) eliminates that issue. That is something I have considered.

Just wanted to echo others to say thanks for sharing. I just told my husband I was reading your tax article for 2023 and how I look forward to it each year! There’s always at least one nuance I learn about. Your strategies helped me set up my own plan that allowed us to retire in 2015 at age 39.

The medical discussion is always one that people get thorny about. I am on Medicaid and have been since 2015. I’ve paid zero for my medical care which is clearly a lot less than I when I worked. I do have trouble finding doctors with available appointments sometimes, specifically dentists and dermatologists in my area. But I do the same as you and plan my income each year in order to continue my eligibility. Our income is primarily interest and dividends and we fill up the rest of the bucket with Roth conversions. Medical coverage will continue to be a political discussion between those who find it unfair and those who do not. For now, I will utilize the resources available to me, and we have plenty of wiggle room in our plan if the rules change.

The reason everything is unfair is that most of the tax credits/tax breaks support the rich and those who are married or have kids (basically the government subsides kids and ends up subsidizing the parents as well, which is ridiculous in my view). Someone who is single would never be able to live off income required to qualify for Medicaid and still have a place in California and have enough for essentials. Now, when you are married, the amount of income gets to a place with 2 people where you can still get all the subsides and be ok (technically even better with kids, which is a choice). We should not be disadvantaging single people.

Assuming I am interpreting your comment correctly –

250% FPL is about the sweet spot for good ACA subsidies (low premiums and low deductibles.) For a household of 4 that is $75k. For a household of 1 that is ~$36.5k, or roughly half. The statement here is that it is not practical for a single person to live on $36.5k?

Few adults are qualifying for Medicaid – that requires income less than 138% FPL ($30k/year for household of 4, $14.5k single, 2024 numbers.)

Yes, I’m not saying for most metropolitan areas of California, it is not practical for a single person to live on 36.5k a year pretax. Let’s assume the person works at for a company and get’s a W2 because they are working for someone else (no fancy tax break situations like someone who has a schedule C). I figure that with taxes taken out of a paycheck (i’ll be conservative with about 10%), that will leave someone with 36,500 – 3650 = 2737 per month. Let’s say you find a studio for 1600 which is being generous. And you need to have a car and gas and insurance. Let’s say 250+100+100 = 450 (generous again). And then lets say you have food at 300 a month including going out. You are at 387 left and I haven’t even mentioned medical costs or other costs of just living. You are just scraping by. You are definitely not going to retire early. If you have a a partner and 75k to work with, you are WAY better off.

I typed the first line too last. I meant to say it is not practical for most single people in California to live on 36.5k pretax if they are by themselves and don’t get any extra help.

Gotcha. I agree with this assessment as it is stated.

Is this something you see a lot of or is it theoretical?

What if this is a single parent? Help should be removed in order to make things more fair?

Well, all of this is tough because maximizing for morality is a different thing than just making things more fair between class groups. In my situation, I have a lot of highly educated friends that make at least double the example of 36.5k. The issue, is that a lot of people who are single do in fact make a poor living. I actually think you have the best in intentions in trying to educate people and actively enjoy playing the game of trying to minimize what you pay to the government. I’m also 100% with you that just paying more to the government is not automatically going to help correct imbalances between class groups given how much money is mismanaged. Do I think that it is possible that someone who has a high net worth utilizing the system to get subsided is slightly subverting the original intention of the laws, yes (unless one is cynical enough to believe it was put in there to benefit those who have more money, which is possible). I’m in favor of the government mandating housing, healthcare, and a livable wage as a right, and the governments main job is defense and regulations to make sure companies don’t completely screw individuals or pollute us to death. In the single parent scenario, I believe having a child is a luxury and should be considered as such. I’m not sure how to reconcile a society giving support to an individual who needs help (who has kids and makes poor money), but I would probably do more to help them vs trying to give tax breaks to those that have a high net worth (and this is super complex because it is possible someone who has a lot of wealth is actively doing more good than someone who less). And while I believe in complete freedom of thought, I do not believe humans should be free to do whatever they want when it comes to resources. Someone who has too many kids is most likely a strain on resources and society should enact rules so that resources aren’t mismanaged. This is why you have to buy into the system of living wherever one lives.

This sounds a bit authoritarian, no? Do people need permits to have kids? IQ tests?

Across the globe governments from the full spectrum of ideologies have implemented policies to encourage people to have more children. Fewer children = fewer workers = collapsing society. You think these policies are misplaced?

I would rather see governments remove roadblocks to upward mobility that mandate livable wages, myself. Low cost of eduction, etc. Mandating higher incomes at low-skill jobs -> increased rents -> rent controls -> reduced housing -> increased homelessness… I’m open to changing that opinion if the data says otherwise (but I don’t think it does.)

>Do I think that it is possible that someone who has a high net worth utilizing the system to get subsided is slightly subverting the original intention of the laws…

This is a commonly stated belief. For it to be true we need to assume the legislators are unfamiliar with means or asset testing. But we know that isn’t the case… EITC, SNAP, multiple tax credits, … are all phased out with income or assets or both.

They did take a different approach. Multiple studies show that universal benefits cost less than means-tested benefits. It is cheaper to the government (and therefore you and me) to provide health insurance universally than to implement an administrative burden to ensure only those who qualify* are benefiting. This is also a more moral system as it removes the judgment of what qualifying means, as it has historically meant those with the “right” skin color / religion / parents / connections. Then, in addition, taxes are increased on those most able to pay to fund the system (e.g. 3.8% NIIT.)

Compare with the current Medicare system…. which tends to redistribute upwards (take from the poor and young and give to the old and rich.)

You make a lot of good points. You always have. I’m sure if you got us both in a room, we would probably agree on a large majority of points in general on the economy.

I’m definitely not an Authoritarian. I test lower left on the https://www.politicalcompass.org/test and I am closest to Anarchism with some distinct differences.

I’m partial to https://simple.wikipedia.org/wiki/Georgism and I actually think that real estate as currently practiced in the United States should be overhauled completely and taxed very differently. I’m much more in favor of individuals investing in companies that makes something vs just owning housing.

I believe that society should make it as easy as possible to make money and harder to hold onto large amounts of money over time. I know you at least agree with the first point ;)

I believe in Housing, Education, Healthcare as a right. And to coin your term, I would be universalist in taxing luxury items we purchase on the daily. I would abolish income tax if I could. I would have everything as a varying VAT tax on goods. I would exempt food and certain necessary items to live. Or minimally tax those items based on the amount of money it would bring in.

I also think we have to live in harmony with nature or pay the consequences later.

We do not have unlimited resources, but I do value the idea of things like fusion energy and and similar technologies that will really push us forward and make things easier for everyone. AI is also in that camp of technologies.

And as another example, we in society thought it was fair for those who were older to get vaccines first. How it that not in line with my thinking that we shouldn’t just willy nilly have as many children as we can have without the thought of the big picture. I’m not sure how to implement fair rules though because I wouldn’t trust a government to be fair.

To design and optimize a system that takes into account the population we have and the systems we already have in place is super tough.

The downside to GCC’s method is that it’s a throttle on wealth creation. Because he’s so focused on reducing taxes, he doesn’t focus on increasing income. This has repercussions, like having to live in Sacramento versus a more desirable city.

No giving either.

Be careful focusing on only tax minimization.

Dear Sir, we are definitely interested in removing all downsides and living in a desirable location. Please advise where we should move to and how we should spend all waking hours to create wealth. We want to make these changes immediately upon returning from our European summer vacation, so please reply post haste and with great detail.

Do you ever think about holding the short term treasuries in Roth accounts instead of taxable accounts so you pay less taxes on them?

For instance,

borrow $50k

sell $50k vtsax that you already own in Roth

use that to buy $50k in treasuries in Roth

Use $50k cash you borrowed in taxable to buy VTSAX $50k

Your treasury interest doesn’t get taxed, if VTSAX gains, it gets taxed at LTCG instead of ordinary income and if you have a loss you can write it off.

Basically all the same risks that you have now but with your treasury holdings in Roth instead of taxable account.

Smart – I hadn’t really thought about it, thanks for the idea.

One risk is I won’t be able to meet the full year holding period for a sale to qualify as long term. If I need to sell other shares I will realize more than a $2k gain. I need to harvest some gains this year if I’m to have anything at basis in 2025. Now if it goes down…

I haven’t had great success these past 2 years with this kind of granularity – I could have had income $5k+ higher in 2022 or $2k+ in 2023 and still had ~$0 tax bill… maybe I’ll do better this year.

Hi. I love reading your posts. I am unable to wrap my head around what you are able to do. You worked hard and had the ability to frontload earnings and wealth. I am a blue collar worker as a nurse so this is not a possibility for me and Financials are over my head. That said, I woke up today to hear the doom and gloom over SS and Medicare. What is the point if my contributing my whole life to just not collect? I am 62 and love my job and was going to work until I couldn’t or didn’t want to or 72….that’s exactly when they say it will not be occurring. This brings panic to me. Am I being unreasonably fearful over this? Am I just paying for current collectors yo not be able to finally collect myself? I am sorry if I am ignorant over such things so forgive me. I respect your opinions and knowledge and am looking for some sort of reassurance.

Bonnie, don’t fall for the fearmongering around SS in particular. All it means is if absolutely nothing changes then the current SS inflows will not equal outflows in about ten years or so. They will still fund something like 83% of expenditures at that point. It has happened periodically over the years SS has been in existence and Congress will do what it does best, kick the can down the road by instituting minor changes to keep it going. Think along the lines of a slight raise in the income levels that are taxable for SS, perhaps a raising of the age for full retirement benefits, and so on. No one has the intestinal fortitude to make tough decisions when it comes to SS for one reason – it is a guarantee they will lose their next election, since Americans will not give up anything in this area.

Now Medicare is a different situation since it has never been funded completely by Medicare taxes, unlike SS. Not sure what will happen there since Medicare lost some of its funding when obamaCare was instituted, when they moved some buckets of money to help fund that pet program. Unsure what is going to happen there. But regardless know that these problems are due to demographics; down the road the situation will reverse and there will be fewer people receiving these program benefits than in the past. It won’t change until after the Boomers and Millennials have moved on, though, which means most of us will not be around to see any positive from it.

There is no crisis that means you will “contribute my whole life and just not collect.”

Please turn off the television.

Focusing on what you can control is the best strategy.

You can strive to save larger percentages of income than is traditional during your final working years, which will help provide more retirement income.

Observations:

1. Always love the highly anticipated annual tax summary.

2. You are a freaking tax wizard.. i was a cpa by training (albeit not a personal tax specialist), but you blow me away with your mastery of the tax code and optimization skills.

3. IF you ever wanted to earn extra cash (and test your tax optimization skills further?) you could start a tax prep biz. I pay my tax preparer (big firm) ~$6k (Federal only), and i consider paying you as much, figuring you would come up with more tax saving strategies.. pretty certain it would be more lucrative than blogging.. ;-)

4. It is asinine and infuriating that employer health plan premiums are deductible, but individual paid are not (can you tell i am an early retiree, but income too high for ACA subsidies?). Pay $24k annually for wife and I for shite coverage, and no deduction..

Queue the haters….

I’m game. Drop me an email.

I think the main issue most pros have is that they do a tax return starting in February, but most of the planning / action has to take place by end of December.

I know this is really late. But I was curious why you did not enroll in Medi-cal for you guys as well. As far as I read, Medi-cal is based on monthly income and you would be over the limit only in the month you do Roth conversion

It’s a very interesting idea. Yes, eligibility is based on monthly income.

Related: Choosing our ACA Health Insurance Plan for 2025

We would have been ineligible in at least 5 months of the year – the 4 months when we received dividends, one of which overlaps with Roth conversion month, and a month when I had more blog income. In 2024 we would have been ineligible 6 months.

I would have then had to provide proof of income each month we were eligible, with regular interaction with the DHCS office. Which… frankly… is insanely painful, and so far I have only had to work with them 1x per year. This Oct-Nov I actually went to their office 5 times in an attempt to resolve an error on their part (still unresolved.) I have been tempted to remove kids from Medi-Cal by increasing our income to 267% FPL just to avoid having to deal with them at all. (Coverage / care is great, the annual enrollment process is broken.)

If we adults were on Medi-cal 11+ months of the year, I don’t think we would actually save much if any money. Premiums would be zero, but they are near zero now when including the child tax credit (which we wouldn’t receive in full without some APTC repayment to offset.)

I don’t have any first person experience but I understand care for adults on Medi-cal is not ideal and options are very limited. For kids it is fine, they go to the same place we do.

In summary – insignificant $ savings and significant increase in time and hassle factor.

Thank you for taking the time to reply me. I really appreciate your perspective. I have been trying to deal with them for about 45 days now to get Medi-cal and I totally get what you mean. But I am told that once enrolled, it is very smooth. I only call them and just do whatever in the hour I am waiting for someone to pick up.

Just for anybody else interested about Medi-cal in this forum, you can have a monthly income of about $3600 for a family of 4. Hoping to get it in the next few days. I also hope my income is going to be more stable given I dont have a blog and very little dividend. It is mostly going to be from sale of stock which I can do in the same month as Roth conversion.

For the most part things have gone smoothly outside the enrollment process. Re-enrollment each year has been far more painful than enrollment, and this year (the 4th) has been the worst by far. One day when I was in one of the DHS supervisor’s office for 3.5 hours we had some good talks about how they lost a lot of long-time/experienced staff during Covid (due to retirement) and have had regular staff funding cuts since then… so of course an under-staffed/trained organization will underperform.

I know it is a lot to ask, but if you remember please come back and comment about how things went for you once the year is up!