The end of the calendar year is quickly approaching, and that means it is time to run through our year-end tax checklist. The simpler the better.

Here are a few important items to review and actions to take.

Year-End Financial and Tax Checklist

Re-Subscribe to Go Curry Cracker!

I am ending my email distribution list. It costs $100+ per month. Many months each year this goes unused.

Since you certainly want to continue receiving all of this financially and mentally stimulating content, be sure to subscribe in another way, e.g. RSS, etc…

I use the feeder.co Chrome extension

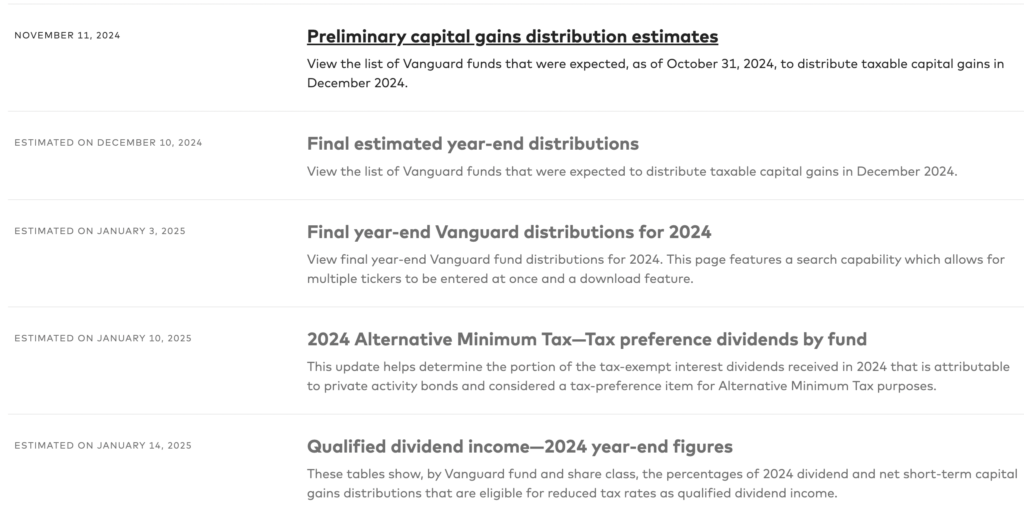

Estimate total annual income

Q4 dividends, interest, and capital gains are not yet on the books, but Vanguard (and others) usually publish an estimate in November / December.

For 2024 Vanguard has shared this calendar:

With a preliminary year-end fund distribution estimates out on Dec 10, 2024, I can start my 2024 tax calculations for total income, qualified dividend income percentage, and US / Foreign earned income split, and then adjust as necessary / as new information is available.

The actual distributions come in the last week of the year so there are still a few days to adjust before the ball drops.

Determine Your Marginal Tax Rate

From income, we can quickly determine our marginal tax rate. (See our full overview of the federal tax brackets.)

The marginal tax rate is what guides us in most decisions related to tax optimization.

For 2024 we will have a low marginal tax rate, so aggressive Roth contributions and conversions would normally be in order.

Income Tax Calculator! (reports marginal tax rate)

For assistance with tax calculations, be sure to check out our simple yet powerful tax calculator!

Ensure SEPP and RMD distributions are complete

SEPP / 72(t) IRA withdrawals and Required Minimum Distributions have rather unpleasant penalties if the necessary withdrawals are not completed accurately and timely. Review SEPP and RMD distributions to avoid this unpleasantness.

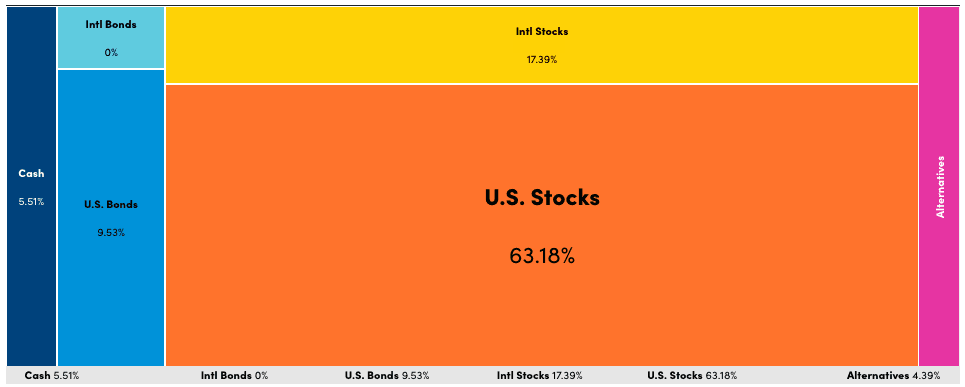

Review Asset Allocation & Rebalance

A good asset allocation stands the test of time through periodic rebalancing. I include Roth Conversions, Capital Gain / Loss harvesting, and cash flow management as part of the rebalancing process.

Our target asset allocation has been about 90% stocks / 10% bonds and 75% US equities / 25% International for as long as I can remember, even with the cash accumulation I did as part of pandemic response.

Our 202x asset allocation chart

Now is a good time to review and rebalance if necessary. I use a combination of a spreadsheet and Personal Capital (affiliate link) for this process.

Finish All Roth Conversions

Any Roth conversions must be completed by Dec 31st. Since Roth conversions can no longer be recharacterized post-TCJA, I will schedule these after I know our “final estimated” total income and amount of unqualified dividends (taxed as ordinary income.)

The actual distributions and qualified dividend income percentage of Mutual Funds / ETFs may be different from the early-December estimate, so some educated guesswork is sometimes necessary.

- Our tax calculator also helps estimate appropriate Roth conversion size.

Harvest Capital Gains / Losses

Similar to Roth conversions, all capital gains/losses must be realized by Dec 31st. I will schedule these after I’ve completed a Roth conversion (if applicable), although I already realized some capital losses earlier this year (This is a good time to remember why to harvest capital losses.)

Related: see thoughts on how to prioritize Roth conversions or Gain harvesting.

- Our tax calculator also helps estimate appropriate capital gain harvest value.

Make final 401k contributions

Ideally, 401k contributions are on auto-pilot and you are able to contribute at least enough to receive a full match from an employer (if applicable.) See the current and past year 401k contribution limits.

Verify all is well, and make necessary adjustments including desired Roth / Traditional allocation.

If you make solo 401(k) contributions manually (like me) be sure you know the due dates for both employer and employee contributions. These dates are set by the plan administrator.

Our solo-401k contribution calculator can help with the math.

Plan for IRA and HSA contributions

IRA and HSA contributions need to be completed by the tax deadline, often April 15th of the following year.

See IRA contribution limits and HSA contribution limits.

If we haven’t already made full contributions for the year, I plan to ensure we have the cash available. This might mean selling stock now or Q1, realizing a capital gain in whichever tax year is more favorable.

Be Sure to get the Full Child Tax Credit

With the expiration of the wonderful child tax credit enhancements that came during the pandemic, it may be necessary to jump through some hoops to get the full child tax credit.

A portion of the Child Tax Credit (CTC) is refundable, but only if you have earned income. If you don’t, it is necessary to ensure a positive tax burden and use the CTC to bring total tax back to zero rather than get a refund. A Roth conversion or capital gain harvest can solve this problem easily but must be done by Dec 31st.

For more details, see Maximizing the Child Tax Credit (even without earned income)

We likely won’t get the full Child Tax Credit this year because increasing our taxable income (via Roth conversion, for example) would result in higher ACA premiums and State taxes that would actually cost us more than the CTC benefit. Bummer.

Schedule Healthcare, Enroll in ACA coverage for next year

Most ACA and employer health insurance plans have a deductible. If you are close to hitting it for the year, December is a good time to schedule Doctor visits and planned care. Free knee surgery in December is possibly preferred to expensive knee surgery in January (or it may be better to meet the deductible in January. The key is planning ahead.)

FSA and HRA dollars may also need to be spent.

For ACA enrollment, results from these end-of-year health checks can inform what level of health insurance coverage we may want for next year. Healthy as an ox? Bronze with HSA. Something isn’t quite right? Silver plan with high CSR subsidies combined with income optimization for the year.

ACA Premium / Subsidy Calculator!

For assistance with ACA planning, be sure to check out our simple yet powerful ACA premium calculator!

Make Tax-deductible Purchases & Donations / Shift Income to Next Year

For business owners / self-employed, December can be a good time to make necessary purchases. Or it can be a good time to shift income into the future if you expect lower income next year (e.g. bill you clients with a due date of Jan 15 instead of Dec 31.)

Last year I purchased a new laptop as a Christmas gift to myself because our marginal tax rate in 2021 was higher than it will be in 2022. Were it the other way around, I would have gotten myself a Januarymas gift instead.

If you are itemizing (rather than claiming the standard deduction) you can also deduct charitable donations (also by Dec 31st.) Gifting appreciated shares means no capital gains taxes for the gifter or beneficiary.

Alas, the above-the-line charitable deduction changes during the pandemic have expired (can only deduct charitable contributions if itemizing.)

Consider getting an (almost) free vacation for paying your taxes

Either through paycheck withholding or via quarterly estimated tax payments, the IRS collects their money upfront.

For the self-employed, it is a simple process to pay those taxes with a credit card (or four) to get free vacations. (See how Uncle Sam paid for our Hawaii trip. I paid $56 in fees to get over $1,000 in free hotel nights and free breakfast with beach view.)

For employees, you can reduce withholding with an updated W4, and then make quarterly payments as the self-employed do to square up.

Consult with your CPA or Tax person

Tax and investment management are superpowers that anyone can develop, but it takes some time and experience to get there. I learned it all one step (and mistake) at a time.

A good CPA or tax guy/gal who also enjoys the role of educator can really help. December is a good time to meet with them for the first or umpteenth time. You can even bring this list.

I’m sometimes asked if I can help – I do my best to take on that educator roll through this blog and also on the forum. I created a consulting page for those who want something more.

Also this year (2024 tax year), in addition to volunteering for tax assistance for low-income households, I am considering personally helping a few GCC readers do their taxes for a competitive fee. Drop me an email if that sounds of interest.

Summary

- Re-subscribe to GCC!

- Estimate total annual income

- Determine your marginal tax rate

- Ensure SEPP and RMD distributions are complete

- Review Asset Allocation & Rebalance

- Finish All Roth Conversions

- Harvest Capital Gains / Losses

- Make final 401k contributions

- Be Sure to get the Full Child Tax Credit

- Schedule Healthcare, Enroll in ACA coverage for next year

- Make Tax-deductible Purchases & Donations / Shift Income to Next Year

- Consider getting an (almost) free vacation for paying your taxes

- Consult with your CPA or Tax person

Use online tax calculators to help:

- Federal Income Tax Calculator

- ACA Premium Calculator

- Self-Employment Tax Calculator

- Solo 401(k) Contribution Calculator

Enjoy the Holidays

We may spend a lot of time thinking about money and taxes on this blog, but they are small topics in the grand scheme of things.

Have a great holiday season with friends and family, wherever you may be.

We will having Thanksgiving dinner with friends, spend the Black Friday weekend in Tahoe (snowboarding), travel to Taiwan for a few weeks over Christmas and New Years.

Happy Holidays!

Actual photo of me in our hot tub.

You blog is my favorite – never used RSS feed and don’t rally understand the linking that is happening. Sorry to be so tech lame, but your blog is my favorite and I hope to Keep getting notified when you publish some way. (No need to publish this comment)

Same here!

Nice list! I’ll be taking some of this advice.

Man, it’s been so long since I used an RSS feed, I don’t even know what to use. Does Android have functionality for that or do you have to download an app?

I was excited to see you have a forum but looks like it hasn’t been used in a couple years. Going to try to get it going again?

Dang can’t figure out on my iPhone either. It opens up in my Activity Tracker when I click the downloaded feed icon.

You can use the Feedly app, which is free for the basic version.

Do a web search for an RSS to email service, there are plenty of free ones. I don’t have a recommendation as I’ve just started looking into this myself. I already have an IFTTT account….so I’m starting out with that one.

I killed the forum a couple years ago due to excessive spam. Bots love spamming forums.

I use the feeder.co Chrome extension, works great.

Not sure how to subscribe now?

Help please

Hi,

When I click on the Re-subscribe to GCC link it brings up code.

What is best way to get alerts when you post content?

Thanks,

Matt

RSS? No thanks…

How about posting more consistently on X?

No worries. Thanks for commenting.

We have been busy with our year end list as well doing many of the things on your list with maybe the addition of a visit to the bank to renew/restructure cds, money markets and move interest needed for next year’s living expenses to checking account. Also planning car purchase to take advantage of 0 percent deals, end of year inventory and avoidance of any additional tariffs that may surface during the new year. Also trying to plan trips for new year in order to get rid of some of accrued credit card points. Busy times but we are also prioritizing holidays with family during all this time. We wish you and your family the best holiday season. We are so thankful for your help and advice that you so freely share on your page. Thank you.

Not sure if this will work for you, but instead of going to the bank and CDs, typically short-term Treasuries pay more than CDs and the interest is not taxable at the State level

You are right that short term Treasuries would maximize our interest income. Our current need is to minimize and/or defer income for as long as possible.

Perhaps my comment wasn’t clear, my apologies.

Instead of CDs (which you have now, which means you are not minimizing or deferring income) buy short term treasuries. Let’s assume that interest is the same as on CDs.

Your interest is the same as your current situation, but your State tax bill is potentially lower (if applicable) and you saved yourself a trip to the bank.

No I should be the one apologizing. Your comments have always been very clear and accurate. I try to be brief and leave out too many details sometimes. My end game is to minimize taxes, maximize healthcare subsidies and defer excess income so that I can have my spouse in this house for as long as possible.

I am looking for the best way to accomplish these goals and I greatly appreciate your comments.

The details that I have left out are mainly that I am lazy. Also my house is less than a mile from the bank and easily accessible on my bicycle. I go once a year to talk cd’s and add the interest accumulated to the checking account and money market for use in the new year as expenses. So far the expenses are less than 1 percent of portfolio and expenses in the last two years include a new custom built house, new car and multiple vacations with extended family with no balances.

Our cd’s are paying more interest now than treasuries, we legally pay no state income taxes, we are well diversified and our only child is doing better than we are, but they will still get a large chunk of money upon our demise.

I would go to Treasuries now but I only see another spreadsheet and I honestly don’t want that kind of work. What would you do for the long term?

I respect laziness. No more needs to be said :)

I am a little surprised that your CDs are yielding more than ST T-bills

I was surprised by the cd rate as well. It could be that we use a small locally owned bank down the street who we were referred to by extended family members when we moved here recently (2 years ago). Said family members use a ton more banking services than we do. It could be that we are getting some type of teaser rate. I will keep an eye on these rates and dip my toe in treasuries when an opportunity comes up.

Good tips! Assuming there aren’t any major changes for 2024 (big if, I know) if I have zero earned income is the only way to get the child tax credit to generate $2000 in tax through Roth conversions? I’m tax resident in Spain and they don’t recognize Roth status so there’s never been any incentive for me to convert to Roth. I’m trying to figure out how I can get any sort of refundable credit from the US without earned income in 2024. Then use that credit to pay part of my ginormous Spanish tax bill. Ha!

You can’t get a refundable credit from the US

Hi Jubilantjill. I am a Spanish resident too, and with an IRA. I am thinking of doing Roth conversion when I take my early retirement, to at least reduce (or even cancel) my US tax bill on the IRA assets. Doesn’t it make sense to you also ? then of course, still would have to pay the Spanish tax bill….

Marc-

A Roth conversion would mean you’d pay Spanish income tax on that money which would probably cancel out the lower US tax bill. Then you’d later pay capital gains on any Roth distributions. If you just left the money in the IRA and withdrew as needed you’d still have the higher Spanish tax bill. I don’t see an advantage to doing a Roth conversion as a Spanish tax resident. Spanish taxes are brutal compared to the US. Although, it’s worth it in my mind for the higher quality of life.

Hello Jeremy – I am a long time reader of your blog and very much appreciate your depth and clarity on complex issues. We have three kids and have been living solely on passive income past few years. In order to maximize ACA subsidy, I have made our AGI a few dollars above 138% of FPL via Roth conversion. With that said, I have a slight concern that I am leaving $ on a table by not calculating/targeting the most optimal AGI (whereby child credit and ACA subsidy are “synced” and maxed out). Would you speak to how you come up with you AGI level as it relates to that “sweet spot” and if you target more than 138% of FPL in your situation. Thank you!

I typically target 200-250% FPL, see: The Obamacare Tick-Tock

With ~$50k of income (138% FPL family of 5 in 2024) you have about $2k in Federal income tax. The CTC reduces this to $0.

Assuming all 3 kids are <17, you have $4k of CTC that goes unclaimed. With no earned income, you get no ACTC.

Related: Maximizing the Child Tax Credit (even without earned income)

Marginal tax rate at this income level is 12%. If you did a Roth conversion of ~$33k ($4k / 0.12) you could claim the CTC in full.

But this increases income to ~250% FPL and ACA premiums by about 15% ($33k * 0.15 = $5k.) 15% tax rate on a larger Roth conversion is not too bad. If that is worth it depends on your future expected tax rates.

Alternatively, you could enroll in the ACA with an honest assessment of your annual income of 138% FPL. Then in December you think hard about if more income is better for your long-term tax situation. Deciding yes, you make a large(er) Roth conversion.

You are now responsible for repayment of some of the PTCs, which is added to total tax on your 1040. As such, it can be offset with the CTC.

If, for example, you made a December Roth conversion of ~$15k (income now ~150% FPL) you would pay some extra tax to the IRS and some to the ACA, for about $4k total which is reduced to zero with CTC. Or the same as you pay today, but with an extra $15k moved into Roth. In some cases, PTC repayment may be capped: Obamacare Advanced Premium Tax Credit Repayment Limitation

State taxes may change the calculus a bit.

If anybody thinks this kind of analysis is valuable, I do some consulting for a low fee that is a fraction of the $4k gain in just this one example.

Receiving your updates by email works best. Would you consider a substack with paid subscriptions instead, since that service sends emails when new articles are published. Or maybe patreon and let us pay to receive email notifications? I only use RSS for podcasts and am not interested in using it for blogs. Thanks for all the great content!

I agree updates via email work best. No worries at all.

I’m not terribly interested in other platform options simply because I don’t want to invest the time.

Aren’t “RMD distributions” redundant?

Try to avoid doing them twice

Is the bond part of your asset allocation still mainly muni bonds similar to https://www.gocurrycracker.com/gcc-asset-allocation-2020/ ? Thoughts on using BND + BNDX for that? Also how do you strategize freeing up funds for the mortgage while keeping AGI low for taxes? Thanks so much!

No, I sold almost all bonds a few years ago when buying a house. See: GCC Asset Allocation 2024. BND, etc.. are find choices if you want to hold bonds.

Most of our cash flow comes from low income and low tax sources – e.g. long-term capital gains & qualified dividends. If your mortgage is a small percentage of your total annual expenses, it doesn’t change your tax planning.