The Retirement Savers Contribution Credit, aka the Saver’s Credit, is a nice incentive for households to contribute to qualified retirement accounts (IRAs, 401ks, etc…)

It’s also a nice incentive for early retirees who make a little hobby / side-hustle money to make MASSIVE Roth conversions on Uncle Sam’s dime.

The Saver’s Credit

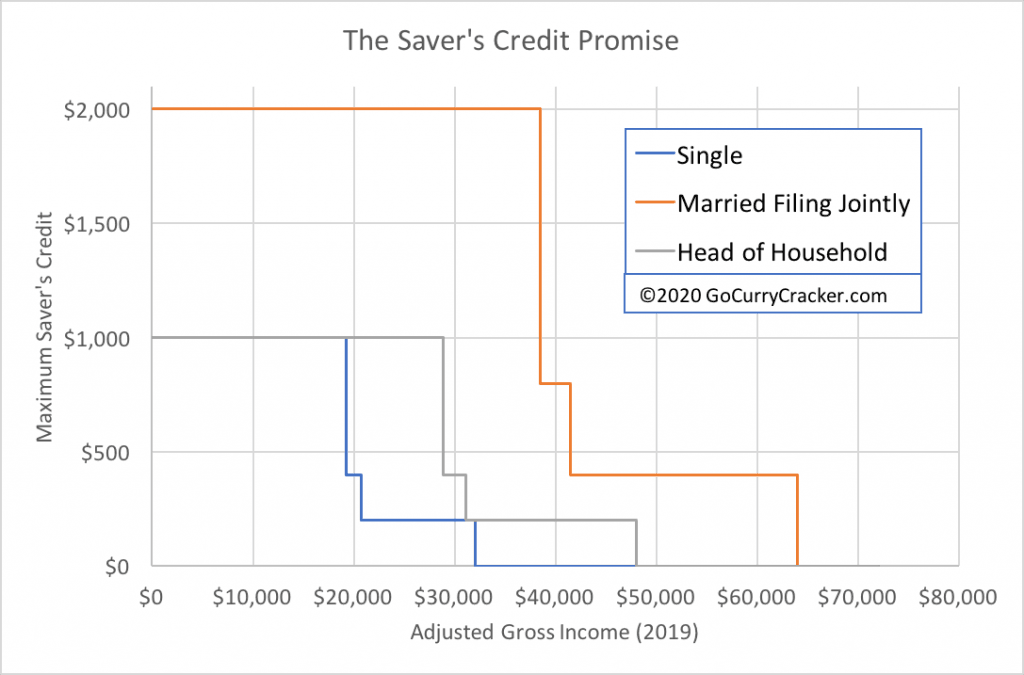

The Saver’s Credit offers great promise – contribute up to $2,000/person to a qualified retirement account and the IRS will reduce your taxes by up to $1,000. That is an immediate 50% return on investment!

Seems nice to get a 50% tax credit. It’s a virtually impossible thing to achieve, however.

As these things usually go, it’s an income-dependent credit… the more you make, the less you get.

This credit phase-out is shown in the following IRS table from Form 8880 (pdf), and then visually courtesy of my Excel spreadsheet.

Line 8 = Adjusted Gross Income (AGI)

In addition to being income-dependent, the Saver’s credit is also non-refundable.

In other words, In order to get a $1,000 credit, you must first owe $1,000 in federal taxes. Which almost never happens at Saver’s credit compatible income levels …

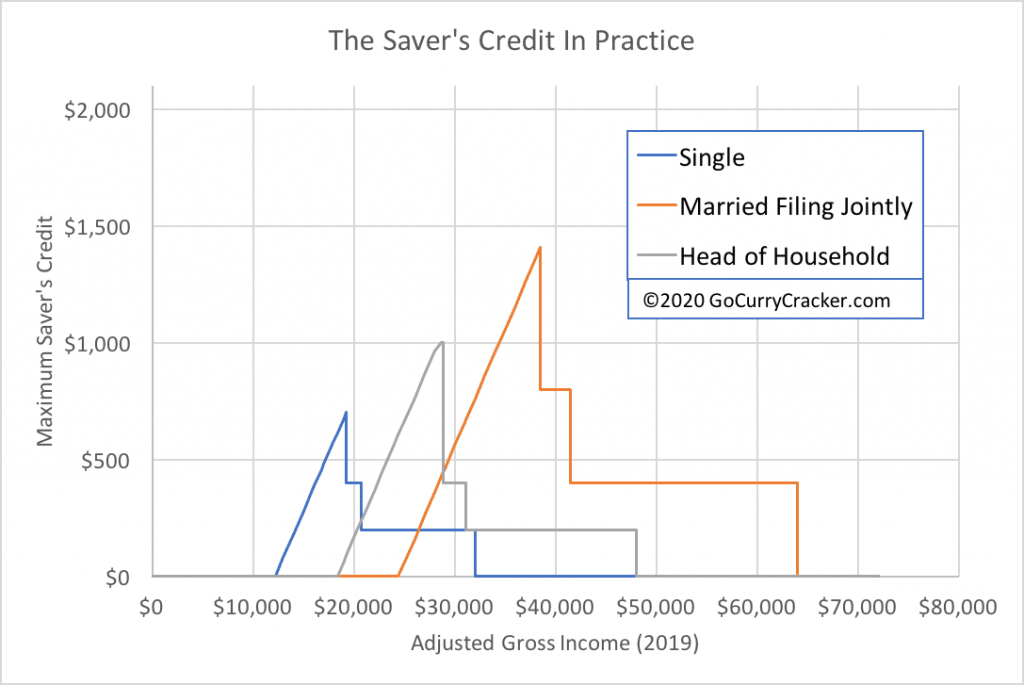

The following chart shows the saver’s credit in practice – the amount of tax credit we can get is limited to the amount of federal tax we owe. With the exception of a very small window for a Head of Household filer, the maximum Saver’s credit phases out way ahead of the federal tax tables.

Maximum achievable Saver’s Credit (2019)

Single: $705 @ AGI $19,249

Head of Household: $1,000 @ AGI $28,350 – $28,874

Married Filing Jointly: $1,410 @ AGI $38,499

Saver’s Credit in Early Retirement

Being unable to get the full credit seems like a bummer. But there is another way to look at it…

The Saver’s credit effectively eliminates all federal tax burden for incomes up to these thresholds, which is equivalent to increasing the standard deduction (aka the 0% tax bracket.) Instead of zero tax up to $24,400 for a married couple filing jointly, there is zero tax up to $38,499, for example.

Who wouldn’t appreciate a larger standard deduction? And so…

To get the maximum achievable saver’s credit, we must first contribute $2k/person to an IRA. A Roth IRA, ideally.

To make $2k – $4k of IRA contributions, we first need $2k – $4k in earned income. (Only earned income can be contributed.)

And then to get the maximum Saver’s Credit, we would need to increase taxable income by up to $34,499, but no more (2019, MFJ.)

If only there was a simple and easy way for early retirees to do that…. Oh, I know. Roth conversion!

Earn $4k. Convert ~$35k. Pay $0 federal tax. (Single filers, divide by 2.)

Things to Consider

But how will I live? Cash – from a practical perspective, this is probably only manageable in the first 1-3 years of early retirement. That said, it does lay a nice foundation as these large Roth conversions will be accessible tax and penalty-free within 4-5 years.

Can I also withdraw original Roth contributions during this phase? No – any withdrawal from a retirement account, in the current year or previous 2 years, reduces dollar for dollar the amount of IRA contribution eligible for the saver’s credit. Otherwise, you could just make a Roth contribution, get the credit, and then withdraw the contribution. (See IRS Q&A, pdf.)

Doesn’t a Roth conversion also eliminate eligibility for the Saver’s credit? No – see the text on Form 8880

“Don’t include … Distributions from your eligible retirement plan (other than a Roth IRA) rolled over or converted to your Roth IRA.”

What is a good way to earn $2k-4k/year? – retiring after 1-n paychecks in January is a good way for the 1st year. A part-time job will also work. Or a common side-hustle like blogging, monetize your hobby, whatever suits your fancy. (See: Everyone should blog!)

Will I need to pay State taxes? – If you live in one of the 43 States with an income tax, yes, possibly. My estimate for total tax burden in California with $40k/year income for our family was < $200, which is less than the $1,410 benefit from the Saver’s credit. Conversely, in Colorado, we might pay $1,850 on $40k income, making this strategy a net loss.

What about ACA subsidies, won’t this increase the amount we pay for health insurance premiums? – Indeed it may.

If, like us, you choose to spend a few years outside the US then no worries at all. It’s a good way to kickstart your retirement. Or maybe you choose to self-insure or use one of the ACA alternatives.

But if you do use the ACA, higher income means higher premiums. Sometimes. Most of the time. (For example, a quote we received for an HSA-eligible Bronze plan in California at FPL ~200% was $2/month.)

(A good way to internalize the relationship between income and insurance premiums is to experiment with our ACA premium calculator.)

At a minimum, we need 138% FPL or so in most states to be eligible for ACA subsidies. Above that threshold, the effective “tax” is now the same for ordinary income as for qualified dividends and long-term capital gains, i.e ~15%, rather than the 25-27% without the Saver’s credit. Worth it? It’s an individual choice.

Most of my income is from dividends and long-term capital gains. Can I do this too? – Probably not. This is best for people with the majority of their savings in retirement accounts, and without large unrealized capital gains in a taxable account (so no opportunity cost for not harvesting gains.)

Income from qualified dividends or long-term capital gains reduces the maximum Saver’s credit we can achieve as it increases AGI without increasing federal tax burden (taxed at 0%.) Since the saver’s credit is a nonrefundable credit, we need tax burden to offset.

Summary

The Retirement Savers Contribution Credit, aka the Saver’s Credit, is a nice tax incentive. Contribute up to $2,000/person to a qualified retirement account and the IRS will reduce your taxes by up to $1,000.

It’s (virtually) impossible to get the full Saver’s credit, but for many, it can have the effect of increasing the standard deduction by thousands of dollars. Early retirees willing to earn up to $2k/year/person can use this to do massive Roth conversions at a 0% federal tax rate.

Let the IRS pay for your Roth conversion!

This is exactly what I’ve been doing the last three years. Retired early but stayed on the payroll as a consultant for “special projects”. Make about 4K a year in earned income and been doing Roth conversions up to the max 50% level for MFJ. Someone once told me I could “never pay taxes again” and so I haven’t!

ha, nice!

This is interesting, but it seems like only a few people can do this.

I think most people would be hard-pressed to earn exactly $2-4k. If you can earn more, you’d probably try to make more. I can’t see myself stopping hobby work once I reach the $2k threshold.

I’d rather pay some tax and have more money. I’m sure most people feels this way too.

so earn $38.5k

Great idea. I’m not sure if we’ll be able to take advantage of it for our Roth conversion ladder. With two kids, we should be able to convert about $61000 per year and pay $0 fed tax, so we would be at the very top of the saver’s credit income phase-out, right? Just want to make sure I’m not missing anything.

With 2*CTC, yes you could have AGI of $61k/year and pay ~$0 tax.

If $4k of your AGI was earned income and you contributed it to his/her Roths, you would also be eligible for $400 of Saver’s credit.

With some earned income you would also be able to get the ACTC (Additional Child Tax Credit, the refundable credit.) If I remember correctly, you could get a check for up to 15% of the amount over $2,500, or $225 in this example.

So tweak size of Roth conversion to get AGI to ~$62,425.

Total tax = $4,175.

Saver’s credit = $400

Child Tax Credit = $3,775

ACTC = $225

You, Sir, are a tax code wizard…..

You are too kind

This is on our list for 2020 and depending on how the cash flow works out, we might actually pull this off. Our income is going to be substantially lower (it’s our first trial FIRE year with a tiny bit of consulting income coming in leftover from 2019). Thanks for putting this together!

Best of luck!

Ironically I discovered this just last week. My husband and I earned approximately 43K this year, which is the most we’ve ever earned, and I realized if we contribute enough to pretax accounts we can bring out taxable income down to the 50% bracket for the saver’s tax credit.

Since a lot of that was self employment on my end and those taxes are extra this can really help us. It’s a relief to see that I was correct in my discoveries!

Heidi here, long time lurker, first time commenter. Been wanting to FIRE for a while but am disabled, only well enough to work part time in the past 3 years. This year was my first ever contributing to retirement, and before the end of the year DH and I will max out our IRAs in addition to my company match to a simple IRA I’ve had going all year.

I just signed the paperwork for 50% of my paycheck to go to the SImple IRA next year. That alone won’t max out the account but it’s better than the 3% with company match I did this year.

I’m not sure we’ll ever reach actual FIRE, but I suppose everyone’s path is unconventional in their own way. We live in an RV to keep below our means and have the dream of being financially stable to have kids.

Thanks for the inspiring and informative blog!

Nicely done! Sounds like you have designed a great life.

You have it right… Traditional contributions until AGI is just below the 50% Saver’s Credit threshold, and then Roth thereafter.

FIRE or no FIRE, nobody regrets having super-sized savings.

Thanks for reminding about this before the year end! Question – if one spouse had earned income (one severance check only, nothing else) can the other spouse make a contribution to his/her personal Roth IRA and still get the saver’s credit on their joint return? In other words, the Roth IRA contributing spouse had no earned income. I think the answer is yes but wanted to confirm.

Yes, confirmed.

Fantastic post. We’ll be doing it this year. Thanks for putting out great content!

You need W2 income to qualify right? My mini job (worked for 8 weeks) this year will send me a 1099 not a W2. I guess next year I gotta look for a job that qualifies. Ugh!

1099 income is earned income. That works.

The numbers work out a little bit different because of the deduction for 1/2 of self-employment taxes, but the idea is the same. See our self-employment tax calculator for details on how that works.

Great info, thank you! Do you know if a COVID-related withdrawal from a tIRA in 2020 will make taking the savers’ credit impossible in 2021? I imagine so but can’t find any specific information.

I haven’t looked at this, but I assume not – reason being that for the saver’s credit net contributions (contributions – withdrawals) must be positive. There may be some nuance to the covid withdrawals that I don’t know about…

Related: Details on the Saver’s Credit

So here it is, December 28th, and I stumbled across your article. I made 4k in W2 income from my employer back in January. I would like to put money *today* into an IRA that would count for this credit. It appears that I can only do this through employer-sponsored IRAs- is that correct?

No, not correct – You can contribute to an IRA which is not connected to any employer.

I was single last year when I did a Roth conversion which bumped my “income” from 14k to 81k. Unfortunately it seems the IRA distribution put me out of the running for the saver’s credit. I can find nothing that alters the truth of my income on 1040 line 11 being 81k instead of my actual 14k in earnings. Am I missing something?

Roth conversions are taxable income that are included in Line 11. With an AGI of 81k you won’t qualify for the saver’s credit.

So many details and loopholes in the tax law!

Am I hearing you right that married filing jointly needs to contribute to TWO IRAs in order to get the max saver’s credit? I can’t just put 4K in mine? Husband is on Medicaid and they are not allowed to have savings over 2K in their name. I’ll just have to be satisfied with my one 1K credit.

No, you can’t just put $4k in your IRA. $2k/person max. See form 8880 line 6