2022 was our first full year back in the United States, which means we were fully in the crosshairs of the 3 US tax systems: Federal, State, and ACA.

One might think this would result in a large tax burden. But no.

Although the incentives have certainly changed.

The Go Curry Cracker 2022 Taxes

Executive Summary

We had multiple streams of income totaling $60,534. State taxes and ACA premiums incentivize low income.

I’m not completely sure how to calculate our effective tax rates in this system – we received over $16,000 in credits, receiving far more than we paid in… If I ignore health insurance and higher future SS income, we paid ~$1,200 out-of-pocket for various taxes for an effective tax rate of 2.0%.

Overall we paid $0 in federal income tax (net $3,000 paid to us in refundable tax credits), $0 in California income tax, and $4,233 in self-employment taxes (which increase future SS income.)

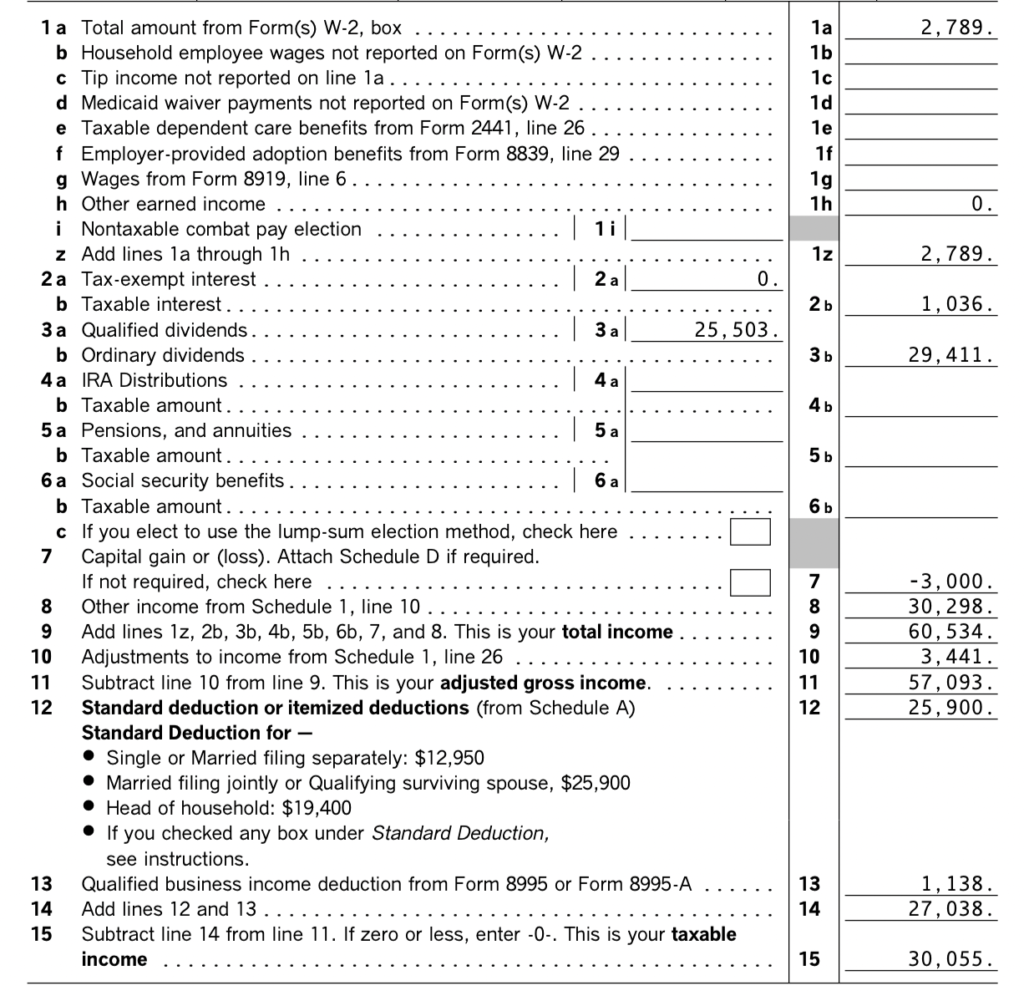

Form 1040

- Income – $60,534

- W2: $2,789 (who woulda thunk)

- Interest: $1,036 ($925 from bank bonuses.)

- Travel hacking: $0 (but just booked $7,000+ worth of travel for $0 out of pocket.)

- Dividends: $29,411

- Qualified: $25,503

- Blog profit: $30,298

- Roth conversion: $0

- Capital Loss: -$3,000

- Capital Gain harvest: $0

- Federal Income Tax: -$3,000

- Income tax: $730 (Line 18)

- Income tax: $458 (Line 16)

- ACA excess tax credit repayment: $272 (Line 17)

- Tax credits: $730 (Line 20)

- Foreign Tax Credit: $130

- Child and Dependent Care tax credit: $67

- Retirement savings contribution credit: $400

- Residential energy credits: $133

- Additional Child Tax Credit: $3,000 (Line 28)

- Income tax: $730 (Line 18)

- Self-employment tax: $4,233 (Line 23)

- Retirement Contributions: $32,500

- Solo Roth 401k: $20,500

- Roth IRA: $6,000

- Roth IRA – spouse: $6,000

- ACA – MAGI = 215% FPL

- Total premium tax credit: $12,344

- Premiums (paid by me): $1,212

- In advance: $1,212

- Form 1040:

$272(paid by tax credit on Form 1040)

- California: $0

- Tax: $636

- Exemption Credits: $1,146 (nonrefundable – opportunity to increase tax burden next year)

- Net: $0

This is how it all looks on the 1040 -> (copied from Turbotax)

Roth Conversions and Capital Gain Harvests (or lack thereof)

Over the past decade we have done annual Roth conversions / Capital gain harvests to minimize future taxes. The future is now.

As in years prior, I used our tax optimization calculator to get a first glance at the options. The calc tells you what is possible tax free at the federal level, but doesn’t include tax credits…

Were we outside the US, I would have definitely harvested some capital gains. We also left $1,000 in child tax credit on the table so a $10,000+ Roth conversion is on the table.

But now that we are in the crosshairs of the 3 US tax systems (Federal / State / ACA) I actually did nothing, thanks to the ACA.

I previously wrote about optimization of health insurance premiums.

(see: Obamacare Optimization in Early Retirement and The Obamacare Tick-Tock.)

Any additional income would have increased health insurance premiums at a marginal rate of ~14%, even without increasing federal or state tax burden.

(see: ACA Premium Calculator.) It may have also forced us into a lower tier of plans for 2023 (from Silver 87 to Silver 73), increasing our deductible and out-of-pocket max for the year (e.g. raising out of pocket max from $1,000 to $6,000.)

I could argue that we should have done a sizable Roth conversion this year (especially with the markets down.) And similarly tax-loss harvesting was maybe not worth the effort in this particular year. 14% is not an unreasonable marginal rate.

ACA Premiums and Credits

A very interesting thing happened with ACA premiums this year. First, a snap shot of Form 8962 showing advanced premium tax credits:

On Form 1040 the IRS determined that we actually under-paid our premiums throughout the year by $272 so this amount was added to our total tax (ACA excess tax credit repayment.)

On Form 1040 the IRS determined that we actually under-paid our premiums throughout the year by $272 so this amount was added to our total tax (ACA excess tax credit repayment.)

As a result, the total tax credits we were able to collect INCREASED by an equal amount.

Conclusion – for ACA purposes always take a pessimistic approach when estimating annual income

(Related: Obamacare Advanced Premium Tax Credit Repayment Limitation.)

Estimated Taxes and Travel Hacking

An interesting thing, nowhere on our 2022 tax return does it show the $7000+ of travel I just booked using credit card rewards points.

If you earn award points through credit card usage or signup bonuses, the IRS just treats these points as a refund on your purchases. There is no income and therefore no taxes. (See our Award Travel Series on Transferrable Currencies.)

Ironically, we actually got a lot of these points by paying taxes – we pay self-employment taxes quarterly, and I often use that “opportunity” to meet the minimum spend on a new credit card. I paid estimated taxes of $2,900 to the IRS and $550 to the California FTB this year on new cards,

If you are going to have to pay some taxes anyway, you might as well get a nice vacation out of it. Even if you are not going to pay some taxes anyway, get a nice vacation out of it :)

Related:

- Aloha Uncle Sam (paying taxes with a credit card to get a free Hawaii honeymoon)

- Award Travel Series: Getting to Hawaii for Free with Ultimate Rewards

Summary

In the US under the triple taxation system (Federal, State, ACA) the incentives are to keep income low. I didn’t do a Roth conversion or harvest gains as a result (and in fact harvested a loss.)

Overall though, it was a good year – we paid next to nothing in taxes, got nearly free high-quality health insurance, and contributed $32,500 to Roth accounts. Social Security income will be higher due to the payment of self-employment taxes. Low taxes now. And low taxes later.

Hi. I have always enjoyed your blog , but am a bit confused now. In last post you mention expenses or 108k, but income only 60k. Is it because you do not include any capital gains on 1040 due to tax loss harvesting strategy, I.E. income isn’t reportable to IRS? Thanks

Retirement = spending more than you earn

Cash to spend comes from selling stock

I was confused too. Did you not realize any capital gains when you sold your stock to spend last year? Thanks for being so transparent! I learn so much from your blog.

I realized at least 3k more in losses than gains.

For example:

2013 – 2021 – tax harvest a bunch of cap gains (most recent harvest at $X)

2022 – sell some shares for less than $X

I understand that you sold the stock, but why aren’t you including capital gains on 1040? Is it because of tax loss harvesting?

Let me answer this in a few different ways and see which one clicks best:

1 – capital gains are included – the amount on the 1040 is always the sum of all realized losses and gains

2 – we realized zero capital gains – every share of stock I sold, I sold for less than I paid for it

3 – the shares I sold were part of a gain harvest in 2020 before returning to the US. I originally purchased those shares in 2007 +/-. Overall I had a profit (2022 sale price was higher than 2007 purchase price) but thanks to years of gain harvesting I was able to show a loss for tax purposes.

4 – I have many shares of stock with unrealized gains. I chose to sell only those with “losses” at this time.

Great info! What company do you use for the Solo Roth 401k?

Also pays to have dependents! Really, really hard to get ACA MAGI below 200% FPL as a solo filer.

Guess it incentivizes being even less productive…the benefits of being below 200% FPL are considerable for the ACA.

Sadly, it makes Roth conversions tough.

Strong work, as always.

Etrade, but you can go with any of the big 3 (Fidelity, Etrade, Vanguard)

Thanks! Also I am wondering. 401 Contributions have to come from earned income right? So i guess the $20500 contribution come from your blog income, right? Since W2 is just 2k

Yes

Also, to make $32,500 of Roth contributions you only need to earn $20,500

Double Your Roth Contributions (Without Working or Earning More)

Thanks for sharing! In 2022 did you go with HSA, silver, or gold plan and who was the carrier? I heard in bay area a lot of doctors left ACA network, so wondering how was your experience using the insurance?

I have heard since the ACA started that lots of doctors don’t accept it. It’s still here.

We are on Kaiser Silver. My experience is we go to the doctor when we need to and insurance pays the bill minus copays and deductible.

Which network? I mean, which ACA plan has lost docs? Kaiser? Blue Shield, Anthem, CCHP?

I know that Stanford opted out of all ACA plans, but UCSF seems to accept Blue Shield, as does Hill Physicians.

Kaiser seems to accept Kaiser.

Another benefit of FI and an anti-consumer lifestyle, is low taxable income.

Not going to knock you for doing your taxes well, just crazy how the IRS doesn’t look at assets equally when considering things like subsidized health care, financial aid for college, and tax credits. Wonder if anything will change with the huge budget they now have.

With our budget I’m not sure we live an anti-consumer lifestyle…

The IRS just follows the law. The law follows the lobbyists.

Oh ok. I guess I was assuming that with $60k in income, and putting about half away to retirement funds and what not, doesn’t leave a lot of discretionary funds for a family in CA. Then again, you drive an electric car and have subsidies for health care, low housing, etc.

But there is no relationship between income and spending.

There is a relationship between portfolio size and spending.

Similarly, putting money in retirement accounts does not subtract from income per se. Sell some stock, move that cash to retirement accounts, buy stock again.

https://www.gocurrycracker.com/legal-money-laundering/

Good stuff! We are paying about $2,300 a month in unsubsidized healthcare expenses for a family of four. But at least it’s tax deductible under our business.

Do you have any advice for how to pay less taxes for households earning $500,000+? Curious what you’d do in that situation.

I’m going to a dinner with someone from Taiwan who represents the golden visa program to learn more about what that entails. Before and earn tax credit is only like $96,000 a year though right?

Thanks, Sam

I don’t know anything about the golden visa program.

At $500k I would just pay the taxes and enjoy the rest.

I think the only option to save taxes for your situation is to max out your traditional 401k contributions. A 401k Roth contribution wouldn’t make sense at your income level unless you already had have millions or 10s of millions in traditional IRA/401k accounts. Don’t forget about an HSA contribution if you have a high deductible health plan.

Hey Sam. Big fan of your blog :-) We’ve been in Taiwan since 2020 and got the Taiwan gold card which indeed provide some nice Tax breaks for people making a lot of money.

Is this the visa you are referring to? https://www.nomadnumbers.com/taiwan-employment-gold-card-application-guide/

If so, then feel free to contact us if you have follow up questions as we might be to help you out! Would you consider coming to Taiwan though to be able to tap into these tax breaks?

Do you have Kaiser or a different California ACA plan?

Kaiser

Qualified dividends: $25,503, your tax rate: 0%.

Your tax rate on your share of your companies’ profits paid as dividends: 28% (USA + CA)

Your share your companies’ profits (before tax):

= $25,503 / (1 – 28%)

= $35,421

Your share of your companies’ tax on profits distributed as dividends:

= $7,141

Had you been paid as an employee, you would have been credited with tax withheld.

Because you were paid dividends you were not credited with tax paid on your share of your companies’ profits.

My Australian company pays 25% income tax.

When it pays me dividends of $750, I am credited with proportional taxes of:

= $750 * 25% / (1 – 25%)

= $250

My taxable income being:

= $750 + $250

= $1,000

On which I pay tax at my personal marginal tax rate of 0%.

Err; Your share of your companies’ tax on profits distributed as dividends:

= 28% * $35,421

= $9,918

Yes… but effective tax rate on SP500 is generally lower than 28%

random google link: https://csimarket.com/Industry/industry_Profitability_Ratiosc.php?sp5

Statutory, marginal and effective tax rates explained:

https://www.investopedia.com/terms/e/effectivetaxrate.asp

“dividing the total tax, which is the number found on line 24, by the taxable income figure found on line 15 and multiplying the result by 100.”

= $4,223 / $30,055

= 14.0%

However, your companies earnt an additional ~$9,918 which was paid as company tax and not credited to you and is additional tax on your income. Accounting for that:

= ($4,223 + $9,918) / ($30,055 + $9,918)

= 35.4%

Dividends are not sought nor paid in USA due to the double taxation resulting in large tax rates. Just about anything else is taxed at lesser rates. A company avoids paying profits as dividends by issuing junk bonds with the interest being deductible, …, ?

Australia’s tax imputation system allows companies to tax efficiently distribute profits as dividends to tax residents, resulting in gross dividends ~9% on ASX200.

As a self-employed worker, I have been living dangerously for years by not making all my quarterly payments. However, the ACA subsidy always saved me. I estimated my income high during enrollment and then would get an extra credit at tax time when my actual income came in lower. Last year, I had a great year income-wise and ended up actually owing back some of the subsidy I received. Ouch.

Thanks for sharing your details with us!

Hi Jeremy,

With so little interest showing does that mean your asset allocation has almost no cash/bonds? I assume so and is it about the same as a year ago when you last posted your allocation? And if you are at near 100% equities do you think that you would still maintain that allocation even without any blog income? And are you at all concerned that your allocation is too aggressive and poses too much sequence risk if a prolonged severe downturn happened? No judgment implied whatsoever but it is a subject I wrestle with often myself as am I being way too defensive? So I was curious as to how you viewed it? But great post and I love your blog. Thanks.

short answer: We have minimal cash and no, that is not a scary thing.

longer answer: some old posts

There are a lot of ways to reduce sequence of returns risk in the early years. I prefer any of the ways that isn’t “have a lot of cash or bonds.”

There are few ways to reduce the risk of running out of money before you die short of having a lot of equities.

Emergency Funds are Overrated

The Path to 100% Equities

Another important factor – I am now of an age where Social Security starts to have measurable value. And it is significant.

Always enjoy your analyses and writing, Jeremy! Thank you.

Why is your QBI deduction so low? Shouldn’t it be 20% of your 1099 income? So ~6k of your ~30k blog income?

Also, any thoughts to update your tax calculator to take into effect the qbi? Especially phase out with specified services?

That to me seems like the most difficult thing to optimize regarding traditional vs Roth 401k contributions and not fall over the cliff.

The deduction is limited to the lesser of the QBI component plus the REIT/PTP component or 20 percent of the taxable income minus net capital gain. Form 8995.

https://www.irs.gov/newsroom/facts-about-the-qualified-business-income-deduction

I don’t plan to make much in the way of changes to the tax calculator. It becomes exponentially more complex to implement with every exception/feature/nuance.

Hi Jeremy. Outstanding report and work on your taxes once again!

I have 4 questions:

#1 – We just got back to Taiwan last month and are missing you here. Are you planning to come visit family/friends you have here in 2023?

#2 – Do you expect your taxes to remain as low for 2023 as you will have spent a full year in California?

#3 – Can you share more about how much your insurance covers you for a regular hospital visit?

#4 – I know you guys are focusing on your health, but if you need some long-term care (like chemo for cancer or multiple weeks at the hospital to recover from a nasty accident), how much would your ACA Silver plan cover you, and would you guys be fine to pay the out-of-pocket without risking losing the house?

1. No

2. Same. We were in California all of 2022.

3. All of it. Small ER co-pay.

4. Our out of pocket max is $1k. No coverage limit.

Wow, no matter how much I play with Covered California I can’t get the OOP max below 3k, even with CSR.

Impressed as always.

the cost sharing reduction subsidies make all the difference

Just to expand a bit on what Jeremy wrote for #4, the ACA “…stops insurance companies from limiting yearly or lifetime coverage expenses for essential health benefits.”

Source: https://www.hhs.gov/healthcare/about-the-aca/benefit-limits/index.html

And as for out-of-pocket maximums, there is a cap on those as well:

“For the 2023 plan year: The out-of-pocket limit for a Marketplace plan can’t be more than $9,100 for an individual and $18,200 for a family.”

Source: https://www.healthcare.gov/glossary/out-of-pocket-maximum-limit/

Even if Jeremy got the worst Marketplace plan and had zero subsidies, he’s still capped at $18,200 OOP for a family.

It’s slowly getting better as well. There used to be “balance billing” where out-of-network providers could charge you directly. You go in for a surgery, an OON anesthesiologist puts you under (and you have no idea who is in/out of network), and then bills you directly because your insurance doesn’t cover his service. As of 2022, the No Surprises Act gets rid of that sort of BS.

There are still plenty of things to fix, but the US is slowly moving toward a first-world healthcare system and fewer ways to “risk losing the house” due to medical issues.

Although there is Max out of pocket limit, there is also something called as ‘Covered and Uncovered’ benefit where an insurance company can deny certain services, drugs or therapies which can end up being a huge patient liaiblity. This can apply to both inpatient or outpatient.

Interesting Insurance companies do not disclose their list of Uncovered services. We will only know about them once a claim has been made and denied under these grounds.

Yep, I doubt there is any health insurance plan that covers 100% of every possible health issue.

Fortunately, each plan purchased through the Marketplace has a “Summary of Benefits and Coverage” that lists out what is covered in/out of network, what percent/dollar amount, etc. They also have a “List of Covered Drugs” to go through before you purchase a plan.

I figure it’s pretty safe to assume if it’s not on the covered list, it means it’s uncovered. But, just to make it blatantly obvious, they also specifically disclose certain uncovered services like:

Acupuncture – Benefit not covered

Infertility treatment – Benefit not covered

Private-duty nursing – Benefit not covered

Anyway, not trying to defend insurance companies — just pointing out that the coverage/benefit details are listed in the plan documents.

“Conclusion – for ACA purposes always take a pessimistic approach when estimating annual income”

I’m having trouble understanding your situation that led to this conclusion. Can you speak more on this? And let’s say you might earn anywhere from $40 to $60k next year… which end is “pessimistic”? Pessimistic from the income perspective or the tax perspective? :)

Pessimistic from the income perspective. So $40k. (Maybe 35k.)

See the repayment limitation as one example.

In our case – we are eligible for a whole bunch of nonrefundable credits that are lost because our tax burden is too low. Since underpayment of ACA premiums gets added to total tax we are able to utilize some of those credits.

Could you please expand a little more on below? Based on your reading / experience, do you automatically get bumped to a lower their plan next year when your income turns out to be significantly higher than expected? Just wondering what thresholds need to be crossed for this to happen apart from the obvious ones like subsidy cliffs. Also, I can’t find any info on repurcutions for underestimating income. E.g. if I estimate income at 147% FPL and of it turns out to be 210% FPL, apart from excess tax payment, are there any other penalties?

Any additional income would have increased health insurance premiums at a marginal rate of ~14%, even without increasing federal or state tax burden.

(see: ACA Premium Calculator.) It may have also forced us into a lower tier of plans for 2023 (from Silver 87 to Silver 73)

I do not have experience with anything being automatic. Each year we guess what income will be the following year, which is independent of anything that came before. There is some discussion in the comments in the posts, The Obamacare Tick-Tock and Obamacare Advanced Premium Tax Credit Repayment Limitation

As far as I can tell, there are no penalties and in fact no incentive at all to be accurate with income projections (within reason.)

Thank you! I have read through all the posts and comments for those two links :)

I dont think my question was clear. I am trying to better understand the line in your post. How would you be forced into a lower tier plan for next year if you are just estimating the income for next year? This is my concern for next year. I estimated to be in Silver 94 plan for 2023. If my income turns out to be higher and I end up in Silver 87 or 73, do you think it forces you into a lower tier plan for 2024?

“Any additional income would have increased health insurance premiums at a marginal rate of ~14%, even without increasing federal or state tax burden.

(see: ACA Premium Calculator.) It may have also forced us into a lower tier of plans for 2023 (from Silver 87 to Silver 73)”

Thank you for clarifying.

Technically speaking, as soon as you know that your 2023 income will make you ineligible for the plan that you are enrolled in, you are supposed to notify the health exchange and they will move you into the plan you are actually eligible for.

There are manual checks in some cases. In Oct 2022 I was called by a person who worked for Sacramento county as part of my kids’ re-enrollment in Medi-cal. Somehow this information feeds into my/spouse enrollment in our ACA plan, and the math wasn’t checking out. She wanted me to enroll in the Silver 73 plan instead of the Silver 87… after maybe 90 minutes of the computer telling her that my numbers didn’t add up, I was able to get her to adjust the numbers by saying I would make a very large IRA / 401k contribution ($30k afair.) She found this experience very frustrating, but capitulated with, “well, it’s your life… if the IRS doesn’t like it, you will have to deal with it (on 2023 tax return.)”

Now we could enroll in the Silver 87. I wasn’t forced, and it wasn’t automatic. Even though the numbers they calculated were different than mine, they deferred to my numbers.

And of course, our 2023 income will be in the range I said it would be so there is nothing to be concerned or upset about.

In theory, there are penalties for abusing the system… if a household repeatedly (and perhaps egregiously) underestimates income, the system should make sure that behavior doesn’t continue. There are penalties (up to $250k) for lying, or up to $25k for inadvertently providing false info. I personally doubt these would be applied in 99.9% of cases.

All that said, no, I don’t think exceeding your 2023 income will force you into a lower tier plan for 2024. But you may (low probability) be asked to explain why you think the large gap in income vs expectations won’t repeat.

Thank you so much! This is so helpful. Sorry you had to go through a 90 min phone call with a rep. That must have been frustrating.