2019 was our 2nd tax year under the Tax Cuts and Jobs Act (TCJA), 3rd year using the Foreign Earned Income Exclusion (FEIE), and 7th year of paying ~$0 in income tax on dividends, interest income, and blog revenue.

But… this year I also realized a massive long-term capital gain which resulted in a massive tax bill.

Our 2019 tax return has some good examples of the FEIE, the long-term benefits of capital gain harvesting, and tax and travel hacking synergies.

Here are all the fun details.

The Go Curry Cracker 2019 Taxes

We had multiple streams of income again this year: interest of both the taxable and tax-free varieties, qualified dividends, non-qualified dividends, long term capital gains, blog earnings, and a ton of Ultimate Rewards points earned by parking some assets in a new brokerage account with JP Morgan.

Ignoring capital gains, income for the year was $104,854. As I’ve shown again and again (and again), at this income level we would pay zero income tax. Blog income of $56,838 generates self-employment taxes of $7,979. (See self-employment tax calculator.)

Including capital gains, total income comes to $206,113. Those gains also come with a tax bill of $10,288. This is a marginal tax rate of 15% and an effective tax rate of 5.0%. Including self-employment taxes, the effective tax rate rises to 8.9%. Including tax paid on international dividends, the effective tax rate comes to 9.5%.

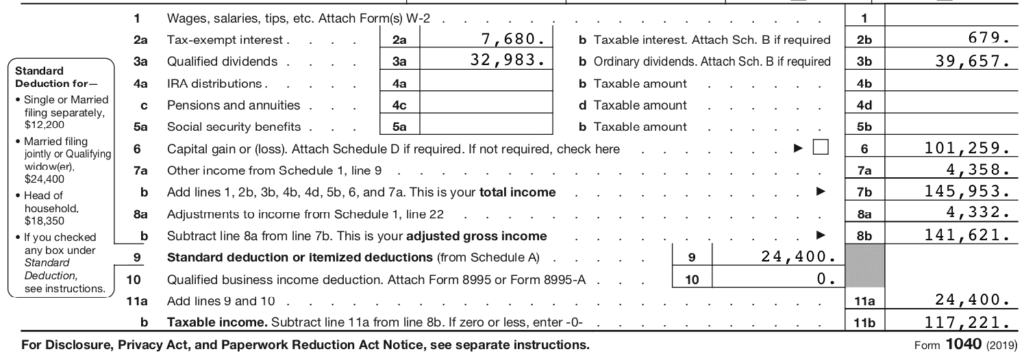

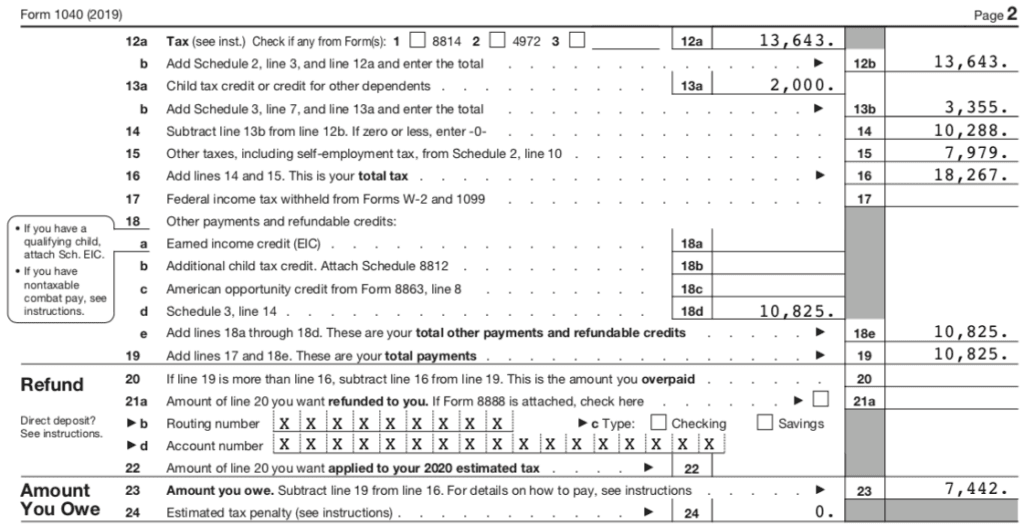

Form 1040

Here are the highlights:

- Income

- Taxable interest: $600 for 60,000 Ultimate Rewards points and $79 of interest on minimal cash

- Tax-exempt interest: $7,680 (~$5k increase over 2018 due to change in asset allocation)

- Dividends: $39,657 (a ~7% increase over 2018)

- Capital gain: $101,259

- Other income: $4,358 of blog income after excluding $52,480 of foreign earned income (Total: $56,838.)

- Gross Income: $206,113

- Adjusted Gross Income: $141,621 (Line 8b)

- Taxable Income: $117,221 (Line 11b)

- Tax

- Income tax: $13,643 (Line 12a)

- Self-employment tax: $7,979 (Line 15)

- Tax Credits: $3,355 (Line 13b)

- Child Tax Credit: $2,000 (Line 13a)

- Foreign Tax Credit: $1,281 (included in line 13b) (this is from taxes withheld on International equity dividends)

- Credit for child and dependent care expenses: $74 (included in line 13b)

- Income tax after credits: $10,288 (Line 14)

This is how it all looks on the 1040.

Form 1040 Page 1

Form 1040 Page 2

In the days of old all income and adjustments were on 1 page where it was easy to digest in one glance. Now, business income (Schedule C) and the Foreign Earned Income Exclusion (Form 2555) are reported on Schedule 1, as well as deductions/adjustments for 1/2 of self-employment taxes and self-employed health insurance premiums. These numbers bubble up to lines 7a and 8a, respectively, on the 1040.

Schedule 1 Part 1

Schedule 1 Part 2

A deduction is always nice, but in this case we had to pay $7,979 in Self-Employment taxes to get one. (This could be eliminated through the use of an Overseas Corp, but since we will probably be moving back towards the US I’ve been content to accept a larger future SS income instead.)

Foreign Earned Income Exclusion

100% of income from GoCurryCracker.com is foreign earned income, which can be excluded from taxation. We qualify for the FEIE via the objective Physical Presence Test because we spent 0 days in the US in 2019, and we also probably qualify under the subjective Bonafide Residence test.

To determine the benefit from the FEIE, taxes are calculated first as if we are in the US. Then, the tax that would apply to the excluded income is subtracted from total tax to yield our actual tax due. This is done on the Foreign Earned Income Tax Worksheet, shown below.

Using the Schedule D Tax Worksheet, total tax due is calculated to be $19,552 (Line 4c).

Next, the tax on excluded foreign income is determined from the 2019 tax tables (pdf.) For Married Filing Jointly with taxable income of $52,480 (Line 2c) the total tax due is $5,909 (Line 5.)

Subtracting these numbers yields the actual tax burden of $13,643 (Line 6 and Form 1040 Line 12a)

Foreign Earned Income Tax Worksheet –> Form 1040 Line 12a

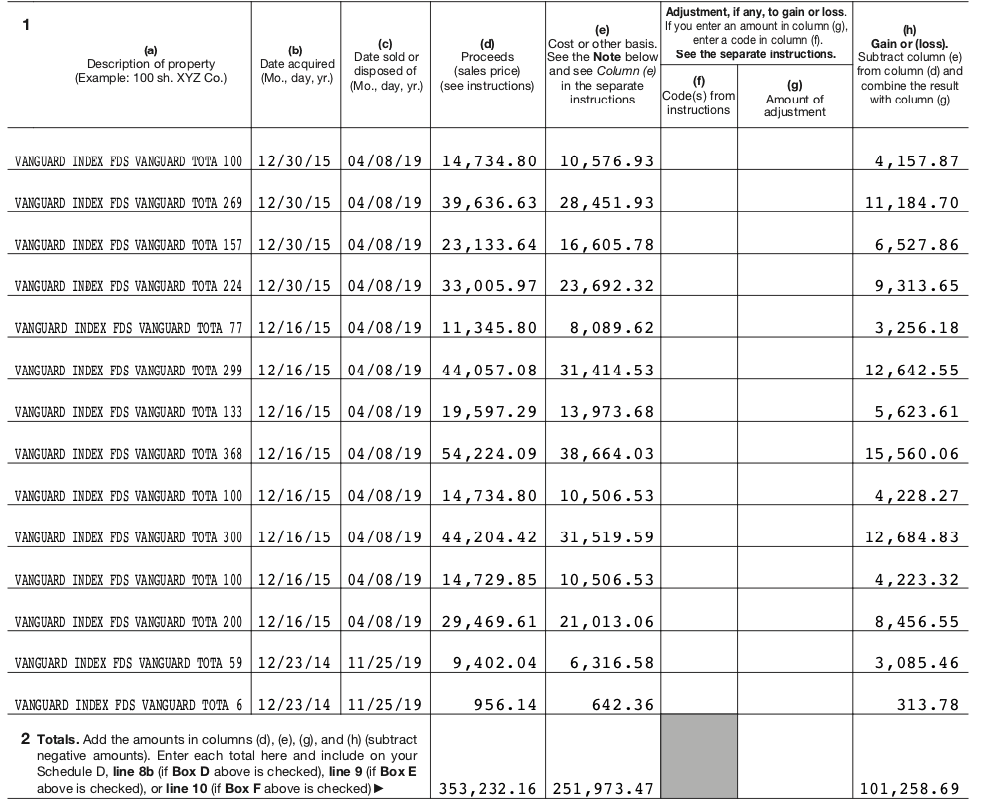

$100,000 of Long-Term Capital Gains

In 2019, I sold $353,232.16 worth of VTI (Vanguard Total Stock Market Index ETF) realizing a long-term capital gain of $101,258.69. This started as a massive capital gain harvest but ended as a shift in our asset allocation.

Schedule D Form 8949 Long-term transactions

$90,951 of this sale was taxed at 15% for a tax burden of $13,643 (100% of our 2019 tax burden.).

All of the individual shares sold were purchased in late 2014 and late 2015 as part of previous capital gain harvests that increased our basis in these shares by $114,659.

Without those previous capital gain harvests, these transactions would have realized a gain of $215,918 resulting in an additional $17,199 tax due.

Capital gain harvesting works wonders.

Want to know more? Plug your email address in here and I’ll send you our capital gain harvesting template with the actual transactions from a harvest I made in 2016.

Taxation of Award Points

If you earn award points through credit card usage or signup bonuses, the IRS just treats these points as a refund on your purchases. There is no income and therefore no taxes. (See our Award Travel Series on Transferrable Currencies.)

Not so when earned in other ways, such as through referrals or bonuses for depositing funds in a bank or brokerage account. I did this in late 2018, depositing $75,000 into a new You Invest by JP Morgan account to get 60,000 Ultimate Rewards points. (As part of 2018’s cap gain harvesting – just move cash to the new account.)

This was shown on the bank 1099 as non-cash rewards of $600.00.

These points were converted into $900 of airfare for flights to Bali, Indonesia in August 2019.

This “income” pushed $600 of long-term capital gains into the 15% tax bracket, so those flights actually cost $90 in taxes.

Tax Payments for Award Points

Throughout 2019 I made quarterly estimated tax payments of $10,825 (Form 1040, Line 19.) When filing 2019 taxes, I also owe an additional $7,442 (Form 1040, Line 23.) This is all due by July 15th, 2020.

100% of this $18,267 in tax payments have been / will be made with credit cards, as I apply for at least 1 new card per quarter. We have 3 cards ready to go for the coming $7,442 in payments (United Explorer card, IHG Premier card, and Alaska Airlines card.) (See the full details on how and why to do this.)

Making tax payments requires a fee of 1.87%, so on $18,267 I will pay fees of $341.59. Thanks to the welcome bonuses that generates over $3,500 in travel value with $0 in tax. I’ll gladly pay $1 to get $10 in return. (Someday, when we can travel again.)

Summary

In 2019 we paid zero income tax on dividends, interest income, and blog revenue. This is due to the generous 0% tax brackets for qualified dividends and the Foreign Earned Income Exclusion on blog income (but $7,979 in self-employment taxes.)

However, a massive capital gain resulted in a massive tax bill (actually $10,288 after tax credits.) This started as a supersized capital gain harvest to minimize taxes when we move into a “high-tax” State, but ended as a shift in asset allocation. This also marks a shift in attitude from “never pay taxes again” to “lifetime tax minimization” – we could have paid $0 in income tax again this year but chose to pay some taxes now vs more taxes later.

Some of the main takeaways include:

- substantial tax benefits of being physically outside the United States (saved more than $5,000 in taxes.)

- long-term benefits of annual capital gain harvests (this year’s tax bill was reduced by more than $17,000.)

- financial benefits of travel hacking even when taxed ($900 in flights for $90 in taxes.)

- HUGE travel benefits for using credit cards for tax payments ($3,500+ value for $350 in fees.)

Overall it was another good year, with small tax burden for a high quality of life.

Until next year…

Sounds like you had a pretty good year! I hope I get to that level of blog income eventually. These things can be so lucrative!

I’m not sure if my tax situation is fully optimized which probably means it’s not lol

I expect blog income to be less than half this year, and probably never as lucrative again. Thanks coronavirus.

I’m curious why you didn’t have to recognize a capital gain on the reward points since they weren’t a refund on purchase? They were reported as $600 but you actually “sold” them for $900.

Great info as always. Just a word of warning to any readers looking to file via FEIE if living abroad but are married to a non-US citizen (I’m a dual US/Canadian citizen, my partner is a Canadian citizen only, and we have been residing in Canada since 2015). Depending on you and your spouses income (and if your spouse is able to apply for a SSN or ITIN) you likely will be filing as Married Filing Separately or Head of Household – both of which do not come with as juicy of tax benefits compared to Married Filing Jointly.

This is us – I’m married to a non-US citizen but she has a SSN from the green card days and we elect for her to be taxed as a resident (so MFJ.)

There are some juicy benefits here also for down the road – technically I can gift her stock worth $175k (afair) per year, which she can sell with zero capital gains tax (but need to file as MFS at that point.)

Very interesting! Do you have a post on this specific niche topic any chance? My partner too has a SSN from working in the States for a few years and is no longer working so I was considering making the switch over to MFJ this year. Does your wife need to file a FBAR and Form 8938?

I don’t have a post on that (yet.) Google “gift appreciated stock to non US spouse” for some reading material.

We don’t need to do a FBAR or 8938 because we don’t have any non-US accounts with more than $10k.

You can just file a US return MFJ with a statement that your spouse wants to be treated as a US person for tax purposes.

I think it’s the same as if you buy a $900 thingy at Wal-mart that is 33% off

I find detailed posts like this very helpful. Thank you for sharing your specifics. Your blog has been instrumental in increasing my knowledge of tax planning strategies.

My pleasure, thank you.

Hi Jeremy, thanks as always for an informative post!

I was wondering though about your strategy on credit cards. Specifically: how do you manage doing multiple credit cards a year when you live outside the US? Do you just have a family member or someone you trust give you the card details when the physical card comes to their address?

I ask because I’m also an expat, but have limited my applications to the one or two cards I can get every year in the few weeks when I’m back in the US. Just haven’t figured out yet how to maximize cards the way you have…

Thanks and all best!

I live in the basement of a friend’s house in Seattle, so I have a US physical address.

I also have a mailing service that processes all mail, including credit cards. I now have everything routed through this, so I can’t even remember when the last piece of physical mail arrived at the physical address. It’s amazing and I can’t recommend it enough – if/when we end up back in the US, I will continue to use this service.

I’m an expat as well and doing something similar to Jeremy. I have my mailing address set up at my dads in FL, apply for US cards, get approved, have the card sent to his house, he takes a picture front and back so I can start using it for online/recurring purchases, and then mails it up to me. We’ve been able to continue our normal cc churn this way.

I do this too – get a scan of front and back of card so I can activate it, and then add it to my Apple Pay or use for online purchases. Sometimes I just never bother to get the physical card.

Wow Jeremy, great job. Your tax return is not too dissimilar from mine albeit different paths. Similar income and cap gains, albeit, the cap gains was for downsizing and buying all cash condo and some Roth conversion. No child credits since we are empty nesters, however, alimony payment deductions (ouch!, only 3 years left). End result: 6.99% effective tax rate.

That’s one of the elements of my retirement puzzle that I still have to figure out: most US banks and brokerages want to cut ties with expats and I don’t have family (or good enough friends) that could allow me to use their US residential address. Mail services seem to be hit and miss with the likes of Chase or Schwab… For that reason alone I almost want to purchase a rental real estate in US.

7% is a sweet tax rate. I’ll take that

Well done! always jealous of the huge tax breaks US citizens get (not even including FEIE here). The low divi tax is phenomenal, compared to the flat 20% divi tax we have here.

CGT is ok here, as then its on inclusion rates of 40% with the max marginal tax rate of 45% only kicking in at $78k so that’s definitely a nice way to fund income needs as opposed to pure dividends.

The US tax system is extremely generous to the investor class and retirees.

Share of company tax on profits to pay dividends:

= (21% / (1 -21%)) * $39,657

= $10,548

Personal tax:

= $7,442

Total tax:

= $17,990

“The low divi tax is phenomenal, compared to the flat 20% divi tax we have here.”

USA taxes company profits at 21% – which is thus the minimum tax on USA shareholder’s share of profit.

Aus company tax is 30% with that tax being credited to shareholder dividend recipients (dividend imputation) – so the minimum tax on shareholder’s share of profit is 0% (for tax residents).

Essentially the Aus tax on profits is 0% and gross dividends (dividend + tax credit) is added to dividend recipient’s taxable income.

Useful to a pre-RE FIREe expecting a low income when FIREd.

nice. Our corporate tax rate is 28%, then when shareholders receive dividends it’s 20%. So being a shareholder of my own company becomes a total tax burden of 43% on any distributions. I can of course write off business expenses or pay myself a salary, but overall it’s very expensive to make profits in our country, compared to US or your Aus example.

Unfortunately, we don’t get anything for our taxes either, we’re not a developed market where it goes to social services I can use, but unfortunately goes to mostly fund an inept government.

Which jurisdiction?

“write off business expenses or pay myself a salary”:

Could you lend to (or buy bond from) your company which then pays you interest at commercial corporate unsecured rates and deducts interest as an expense? Typical Aus and USA rate ~5% – 10%.

Capital to lend could be withdrawn shareholder equity or recycled after tax dividends.

South Africa. Yes you can do shareholder loans, which we’re currently doing. It shifts the tax then to the holders to add to marginal income. We’ve done this and you can earn high rates of around 15%.

You need to give the business the money, which was fine but then the cash is trapped there and can only be invested into rand-based investments (so no Vanguard) and will take around 6 years of interest before its paid back and you are able to start getting some of the business’ income out at the lower tax rate.

Also to consider is whether the interest in the hands of individuals is lower than 20% dividend rate since marginal tax rate already hits 26% at $10k and rises rapidly to 45% at $75k.

At this stage I’m considering whether a BVI corp isnt better than supporting a government I disagree with.

SA:

>= 18% tax on personal income on >= ~R 120,000 / y (= ~$USA 6,600 / y) is ‘limiting’.

On top of corporate tax of 28%, total (1 – (1 – 28%) * (1 – 18%)) = 40.96%, is ‘crushing’.

Worse with 45% marginal tax rate on personal income >= R1,577,301. 60.4% rate is ‘Repressing’.

Aus:

>= 19% on >= $A 30,000 (= ~$USA 20,000) for seniors.

Actually it’s just depressing =)

Coupled with currency depreciation of $1/R7 to $1/R19 in the space of 12 years, it’s surprising any of us ever achieved the $1m net worth mark or FIRE, lol

What is your moderately thrifty cost of living for where you are in SA?

We run 4 bed house on 1,000 m^2 with 4×4 car, good neighbours (and SA friends), in low crime Canberra with no bad neighbourhoods on ~$A 33,000 (+ depreciation + international travel). Means tested Age Pension welfare is ~$A 40,000 for which we are ineligible due to assets.

These comparisons don’t tell the whole story, especially for FIREes:

https://www.nationmaster.com/country-info/compare/Australia/South-Africa/Cost-of-living

Purchasing power is more useful for workers, not so much for FIREes:

https://www.numbeo.com/cost-of-living/rankings_by_country.jsp?title=2020&displayColumn=5

Using R10/1A$ here, which had been the rate for a while. Since the global corona economic crash it’s around R12 to A$1 now.

Average is tricky because we have such a huge range of wealth scale here (Gini). I read that 14% of the population owns 90% of the assets, so frugal living could be super cheap. I consider our lifestyle middle class by first world country standards (I think).

I recently sold our 1250 m^2 home for R1.2m (A$ 100k), which was in a reasonable suburb.

Currently we’re in an expensive suburb so our 140 m^2 3bed townhouse is around R1.6m (A$160k).

Average expenses have been around R420k per annum excluding international travel, say A$42k, versus R600k (A$60k) when we did travel to Europe and ski.

So monthly at A$3.5k, that’s with a paid off home (as interest rates at 9% are too

high and houses are cheap), 1 car (8 years old), levies (A$500 per month), eat out occasionally (2x month,cheap but we prefer home cooked), medical cover (A$600 per month), domestic help, no kids, but have pets, groceries (A$1000 per month).

I think we could reduce a little, since now in lockdown we’re approaching closer to A$2.5k per month but we’re frugal compared to most of our family and friends (although they also have kids which require private schooling then and that’s an extra A$100k per annum per kid), but we’re super wealthy compared to most South African working class.

“Average is tricky because we have such a huge range of wealth scale here”:

Not many poor here.

“Sold our 1250 m^2 home for R1.2m (A$ 100k)”:

Where? Median 4 bed house ~$800,000 here. Property tax ~$A 2,000 / y.

“140 m^2 3bed townhouse is around R1.6m”:

Median 140 m^2, 3 bed 2 bath, 2 garage townhouse / flat ~$A 600,000.

“interest rates at 9%”:

Mortgage rate 5 year fixed ~3%.

“medical cover”:

Free. Top hospital insurance ~$A 2,500 / y.

“domestic help”:

Rare to never – gov subsidies for visiting age assistance in home. Aged fail use Age Hostels capital cost ~$A 700,000 per individual + ~$40,000 / y. Would be comforting to have good, and cheap, help in own home.

“groceries (A$1000 per month)”:

Perhaps you mean R 1,000 / mth. Our expenditure $A 60 / wk, $A 260 / mth. Then I must walk > 1 hour a day to avoid ‘disfiguring’ myself.

“private schooling then and that’s an extra A$100k per annum per kid”:

(R or $A ?) Here gov subsidises private schools to similar extent to public schools – fees ~$A 10,000 / child y.

“we’re super wealthy compared to most South African working class”:

We are top 2%ers in wealth – and ‘work our expenditure’ harder than the ‘working class’.

Groceries at A$1000 per month, ie R10k per month. That’s not too unusual for us. Yeah, messed up on the private schooling, meant A$10k per annum. It’s the thing that’s been crushing the middle class in South Africa, having to pay so much just for school fees and all other amenities on top of that.

The public schools became a failed system around 10 years ago (they weren’t free then either), it was fine when my wife and I went to school, but has since had too many new students that cannot afford to pay and many of the decent teachers moved to private schools.

It looks like housing is super expensive there, but much of the other things would work out both ways. I noticed the same when we went to Switzerland before, that some of our costs would reduce over there, but our home wouldn’t be affordable.

“looks like housing is super expensive there … our home wouldn’t be affordable”:

Aus: no capital gains tax on ‘Primary Place Of Residence’. Interest and other expenses ‘Negatively Gearable’ – deductible from non-related profits. Demand from strong immigration and decreasing interest rates – future may differ.

SA: Capital gains tax on > R 2M gain on ‘Primary Residence’. https://www.bizcommunity.com/Article/196/568/197887.html

“Interest and other expenses ‘Negatively Gearable’”: on ‘Investment Property’.

Home affordability; (Mortgage_Rate * Price / Income):

SA:

= 10% * 1,000,000 / 360,000

= 28%

Aus:

= 3% * 800,000 / 81,531

= 29%

Roughly the cost of housing in portion of hours worked is similar.

South African mortgage rates are higher due to inflation and high rates of tax on the interest yield.

Renting consumes similar portions of income.

(I always ensured I paid less than 10% of income.)

Great post, super informative. Question: How did you earn Ultimate Rewards points with your JP Morgan brokerage account? I can’t find an offer like that online. Thanks.

I linked to the JP Morgan press release in the post, but I believe the offer has expired. They replaced it at one point with either a $750 or $1,000 cash bonus (which is better) but I think that expired as well.

Nice, as always. How are you getting tax free interest? I’ve never seen a way to do this which is why I’ve been slowly moving cash from interest accounts into dividend paying stocks.

Nicely done! I How were you able to set up the Invest by JP Morgan account as an expat?

I have a US physical address, but route all mail through a mailing service.

Muni bonds would be a guess. Vanguard has an ETF: VTEB.

Municipal Bonds. I own some VTEB (Vanguard) and some MUB (iShares)

Definitely need to add some municipal bonds once I get to the point where I want to start buying bonds. Still sticking to a more aggressive strategy of buying stock alone. Asset allocations of 100% stock are certainly more volatile, but still working and earning an income means I don’t have to pay attention to that. Having a job can be a great thing.

Great article as usual Jeremy!

Question… how do you get new credit cards abroad? The companies are reluctant to send the card initially overseas

Use a US address. See my responses to the other similar questions for more details.

Would you mind sharing how much you pay in local income taxes? FEIE is great for not paying US, but aren’t your tax payments just going to country of residence?

$0

Move yourself to a country with no income tax or a territorial tax system (only tax locally sourced revenue.)

See: Nine Tax Friendly Countries We Have Explored

Or if it is a high-tax country you desire, use the Foreign Tax Credit instead of the FEIE

Jeremy, I just want to thank you personally for publishing your annual taxes. I found you in early 2019 and have read all the tax posts. 2019 was the first year that I really was able to master my taxes. I am 59 and FIRE. Last year I got 11K in free Obamacare, harvested over 30K in capital gains and converted 6K into my Roth. All with a zero tax bill. My accountant was stunned. For the first time since retiring three years ago I feel like I am in control! Thanks for all you do, it is appreciated more than you will ever know.

Woop woop! Well done, James! 👍

Wonderful! Congrats!

>My accountant was stunned.

This always makes me laugh. I love it when accountants are surprised by things from a random guy on the Internet

Curious why you didn’t claim any Qualified business income deduction on line 10, due to holding VTI / VTSAX ?

owning some ETFs or Mutual Funds isn’t a qualifying business activity

Both H&R Bock and TurboTax take the dividends in box 5 of my 1099-DIV, Section 199A dividends, and put that amount on line 6 of form 8995 and calculate a QBI.

Ahh, sorry I missed the connection to the REIT dividends

The reason there is no QBI deduction on Line 10 is in part because of the FEIE. Technically, we could get up to a $10,800 deduction – $10.5k for the blog business and $300 for the 199a divs.

However, there is a ceiling on the deduction based on taxable income and net capital gains (qualified divs + cap gains.) Since our taxable income of $117,221 (Line 11b) is greater than net capital gains of $134,242 (Line 3a + Line 6), our deduction is capped at $0. Without the FEIE our taxable income would be higher and we would qualify. This is all done on Form 8995.

For the blog income, the QBI deduction requires US income and we have none due to FEIE.

Overall, better to exclude 100% of blog income than to get a $10.8k deduction, so FEIE wins.

First you turn your back on 100% Equities. Then you turn your back on Never Pay Taxes Again? How come your comments aren’t full of cries of hypocrisy?!?!?

Seriously, good on you for making rational decisions with changing conditions and new information.

Some in the public eye* will stick to actions and advice just so they can preserve the purity of their brand.

*Dave Ramsey is recommending that struggling small businesses turn down the PPP because it’s technically a loan and his brand is “DEBT IS ALWAYS BAD”.

*People that name their blogs something like “Dividend Investor” or “Real Estate Investor” or whatever will argue their way is superior to any alternative even if there is strong evidence that they should at least diversify.

Haha, perfect

I also turned my back on preferring brokerage account over Roth, so hypocrisy is my new brand ;)

How are you getting tax free interest? I’ve never seen a way to do this which is why I’ve been slowly moving cash from interest accounts into dividend paying stocks. Couldn’t find any reference to this in the linked article.

Municipal bonds

These weren’t even on my radar.

Are you worried about municipalities going bankrupt with investors holding the bag like Detroit?

Ain’t nobody got time to worry about all the things that could happen

“I made quarterly estimated tax payments of $10,825” So you paid almost 44 grand in taxes already and now you’re paying an extra 10 grand?

Sorry if the question is weird, I’m not american so idk how that works exactly.

~$2500/quarter so $10,825 total.

Ah not 10k a quarter like it reads. Ok it makes more sense now.

Research Section 199A dividends. Line 10 on the 1040 should not be zero since Vanguard Total Stock Index includes REITs.

Probably not worth filing an amended return for 2019, but don’t miss out next year.

Our QBI deduction nets out at $0 because of the FEIE. See details in this comment.

Hey GCC!

For the traveling mailbox, can this be used for those folks who would like to legally claim that they live in an income tax free state? I have heard of RV’ers doing this legally (claiming their state of residency is in Texas, Washington, etc.) but wasn’t sure if someone had early retired through the FIRE movement and are living through mostly investment income, if they could claim this using the traveling mailbox service as their state of domicile.

Thanks!

-Sean

Having a mailbox / mailing address isn’t sufficient to be a resident of a State.

International taxation is all new to me since I only recently married a woman from another country and she still lives overseas. I’m curious to know if you get help from a professional in filing your returns or do it all yourself. I’ve been searching for CPAs or EAs with the the right experience. There are none in my immediate area. Only Boston, NY, etc. Do you know of any reasonably priced firms who can assist me?

I do it all myself but I’m a tax geek.

The people at Taxes for Expats could be a good option – their online articles are quite good

https://www.gocurrycracker.com/tax-services/

I’m new to taxes. For long term capital gains when filing taxes – how do you figure out what the basis and the gains are when you sell those stocks? If I sold my stocks from Vanguard, does Vanguard figure all that out for you?

Thanks. I’m learning a lot from your posts.

Yes, your brokerage has/reports that information. If you sell “specific shares” you can select which shares you want to sell based on their purchase price (basis.)