This week, a fairly common question from the inbox:

Hey Jeremy, thanks for the great blog! I’ve read all of your stuff. Like you, I’ve put a lot of our retirement portfolio into VTI / VTSAX. VTI pays about 2% which is only half of what the 4% rule allows us to spend. How can I live off just dividends? What about the other 2%?

The answer is simple: don’t live off just dividends.

“How do I live off of just dividends?”

Living solely off of dividend income is an interesting idea. The general thinking behind this approach is that dividend income can be a regular and predictable income stream, just like a paycheck, thereby making our retirement somewhat immune to market fluctuations.

The current approximate dividend yield on the S&P500 is about 2%. If we want to spend twice that amount, as the 4% Rule allows, we can:

- spend less

- double the size of our portfolio so we can meet our target budget on dividends alone

- have a more concentrated portfolio – own fewer stocks that pay little to nothing and more stocks with higher yields

- spend some of the principal each year

- some combination of all of the above

Doubling our portfolio is pretty straight forward – just work another decade or so. Easy.

If we want a less diversified / higher yielding portfolio, Vanguard has an option – VYM / VHYAX currently pays 3.39%.

(It does so by holding 396 stocks with higher yields, versus the 3514 stocks in VTI / VTSAX.)

Spending principle is also easy – we simply spend the 2% dividend and then realize some capital gains worth another 2%.

Spend Some Principal

Well, I don’t really want to work longer… and having a less diversified portfolio sounds a little risky. Are you sure it is OK to spend some principal?

Let’s find out.

Using a 4% withdrawal rate, using Portfolio Visualizer I compared Portfolio 1 (100% VYM) with Portfolio 2 (100% VTI) for the Go Curry Cracker retirement years. Assuming a starting value of $1,000,000 and $40,000/year spending, as of today, the lower yielding portfolio is worth $95,000 MORE.

VYM vs VTI at 4% withdrawal rate

But that is because we would be spending some principal in both cases, right? Nope.

Using a 3% or 2% withdrawal rate has the same results. The more diversified / lower yielding portfolio has a greater CAGR.

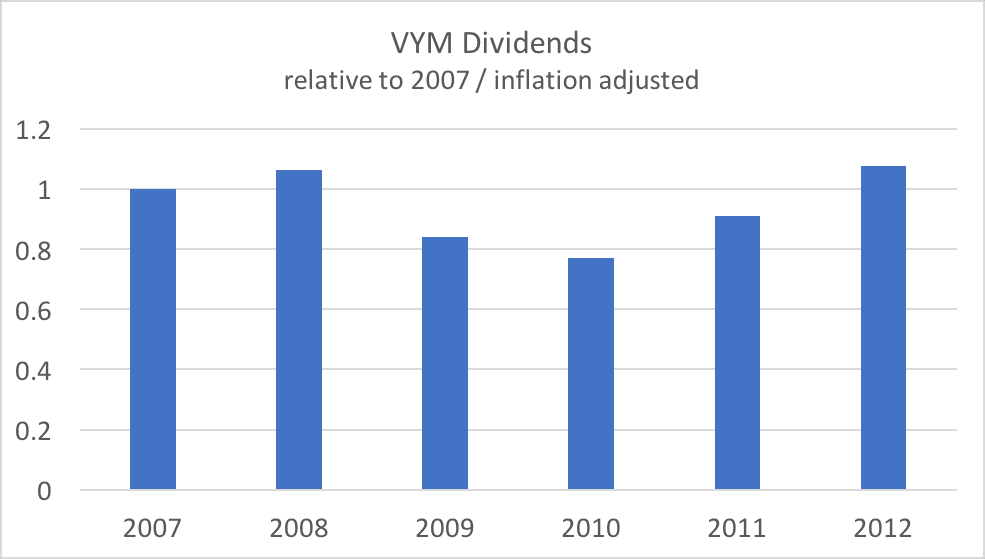

But this has been through only good times; the stock market has trended upward throughout our retirement. Surely a VYM portfolio would perform better during a market disaster like 2008?

Nope. The high yield portfolio fell harder and recovered more slowly. It’s dividend payouts were also cut more aggressively, dropping nearly 25% over 2007 value at one point.

Selling stock to recover some of your principal for spending works just fine.

Taxes

Now that we’ve decided that spending some principal is OK, let’s look at taxes.

Maybe we have a $1,000,000 portfolio that spits out $20k per year in dividends and we get another $20k from selling stock.

If that were a pure dividend portfolio, we might have $40k of taxable income. But with a hybrid dividend/capital gain portfolio, assuming our stock has increased in value by 25%, we have taxable income of only $24,000.

If you are following the Never Pay Taxes Again approach to life, maybe you pay zero Federal income taxes on all of this income regardless.

But in one potential future home base, this difference in taxable income could cost us between $2,400 and $10,000 in combined ACA subsidy reduction and State income tax. Ouch.

Choosing when and how much money we want to pull from the portfolio is more tax efficient than having the portfolio decide for us.

Summary

Companies can return value to shareholders in a number of ways, of which dividends are one form. Investing in future company growth, share buybacks, and acquisitions are a few other options, which we would expect to result in price appreciation.

Companies that pay out high dividends tend to be in more established low-growth industries, and they often grow more slowly. By concentrating our portfolio in this subset of the market, we lose the growth potential of small-cap and mid-cap stocks. A lower yield fund with greater diversification, as shown above, can have greater price appreciation.

Additionally, long term capital gains are more tax efficient than a pure dividend portfolio. It’s the main reason why I wouldn’t mind having fewer dividends.

In summary, planning on spending some principal is a fine solution to generating the full 4% that history says we can spend.

Do you plan on spending principal?

Do you invest any of your money is in gold or silver?

Only what is in our teeth.

Ha! :D

Great post great research great work !! Thank you I had this very question for a long time and your researched based answer is very good

Excellent article. I have been spending more time reading about dividends and how I can use them in retirement and this definitely helped

You left out option 5 which is a great one.. never spend any of your equity proceeds and use a blog to cover your costs =)

On a serious note, great stuff, there’s lots of options and working another decade ain’t one of them. You need to have a bit of faith in the math when you’re spending 2x your cash yield and that selling shares doesn’t lead to eventual depletion.

That is also a solid approach ;)

Throughout the Trinity Study / 4% Rule research, principal was part of normal everyday spending. So there is something to base the faith on.

Working part time is a great option for early retirees. That has always been my plan. A little active income goes a long way in retirement. Once we’re 55, then I will spend down the principal if needed. For now, I have active income to supplement my early retirement.

Planning to work a bit is a solution – income of $100/month increases the terminal value throughout the Trinity Study by about $150k on an initial $1 million portfolio.

I didn’t plan on having any “active income” but my blog hobby kind of took off.

What about those times when the stock market goes into bear market territory and down 40% and you don’t have supplemental income (like your blog income) and there are no capital gains to harvest at that time?

From 2000 to 2002 the stock market went down 46.55% and it took it 3,5 years till 2006 to get back to the point where the portfolio was before in 1999. That’s 6,5 years of not making any returns/capital gains and making withdrawals from your principal each year for retirement.

When you are 65, that can be quite nerve racking, don’t you think?

Then in 2008 the market was down 38.49%. It took two years to recover that and then 2011 there was 0 return on the stock market. That’s another 4 years without having growth in your portfolio, just getting it back where it was before.

If you were retired at the end of 1999 and till the end of 2011 the market was down 85.04% total and up 91.75% total. So in 11 years you would have made 6.71% divided by 12 years you got a lousy 0.55% return. In reality you would have lost money because you would need to withdraw 2% each year to supplement your income at a price that was way less than what you had paid for stocks, especially during 4 years of bear markets. I would not feel comfortable with my portfolio allocation and would probably be looking for a job at that point.

I know a person who retired on around 2 million dollars and invested it in money market account, various 15% tax rate preferred stocks, some common stocks and bonds. He has been leaving on that dividend/interest income for 20 years and not only could live off at least 5-6% off dividends/interest income but also had capital gains every year as well. His portfolio was never down 40% during bear markets and he did not have to sell principal because his dividend/interest income of 5-6% a year was sufficient to live off. Plus if some of your money is in Roth IRA, you end up paying 0 taxes.

What are your thoughts on that? Would you still be invested in 100% stock if you did not have supplemental income and were 65 years old?

A lot of what you are describing is called “sequence of returns” risk. Tilting to dividend paying stocks doesn’t help with that, and in fact could make it worse. There are better ways of dealing with the sequence risk, and many of them involve holding high quality fixed income as a portion of your portfolio. You can withdraw from the fixed income portion during down years and give your equities time to recover. If reabalancing to a target allocation, then this will happen automatically.

Use the ‘Vanguard 500 Index Investor’ as the middle between VYM and VTI and using the longest series available, from 2006 to 2019 and selecting ‘Inflation adjusted’ the ‘Portfolio Visualizer’ reveals $1M growing to $1.1M.

That is compound annual growth rate (CAGR) of::

=(1,100,000 / 1,000,000) ^ (1 / (2019 – 2007)) – 1

=0.8%

It has taken 13 years to maybe ‘recover’.

Gold ($USA):

=(1,300 / 600) ^ (1 / (2019 – 2007)) – 1

=6.66%

Money in the bank in Aus did 2.29% inflation adjusted compound annual growth rate.

Gold ($A) 6.48%

Best adjust gold for inflation for comparison!

dqydj has a good gold calculator

Well… the 4% rule is called the 4% rule (and not the 5% rule) because spending 4% survived the worst times in economic history. And they all involved spending principal. So unless you believe the future will be worse than the worst we have ever seen, then you will be fine, mathematically speaking.

The worst time was actually 1965.

2000 and 2008 work too (see Kitces.)

Seniors have supplemental income – Social Security.

Remember though that the 4% rule was designed to accept a drawdown to zero over 30 years. If your retirement will last longer than 30 years the 4% rule and the research backing it does not apply to your situation.

But it does. I get what you are saying, but disagree with the conclusion.

At 4% your portfolio will likely last forever, increasing in value over time. That’s directly from the research.

Debating whether somebody could spend 4% or 3.92973% is fun and all, but statistically speaking successfully using a 5% withdrawal rate is more likely than running out of money while spending 4%. Focusing on the worst time to retire ever misses the big picture:

The strongest retirement failure mechanism is death (“the human body is designed to draw down to zero.”)

Check this out visually (click here):

Retiring at 35, 4% withdrawal rate, 80/20 stock/bond, SS at 65 (25% of COL)

so with the 4% rule – does that include the dividens and capital gains that are “spit” out? what happens if you dont touch the principle and only live on the divides and capital gain….

Good job breaking the myth that high yield is “better”. If you are afraid of spending principal maybe you are not really ready to FIRE just yet. “Spending principal” can certainly play with your head at the beginning. My SWR is CAPE-based (1.5/0.5) which involves selling principal. I sleep well at night.

Sleeping well at night is almost as good as sleeping well during nap time (isn’t retirement great?!)

Great points and I can relate to the “Choosing when and how much money we want to pull from the portfolio is more tax efficient than having the portfolio decide for us”. Considering your analysis is fairly recent (less than 15 years of performance), how does this all compare to the well established conclusion that, over the long run, value stocks will outperform growth stocks?

Is that conclusion well established? Check it out in portfolio visualizer.

I’ll just own the whole market.

I’ve read it from a few sources that crunched some data for longer periods. Below is one of them. I also own a mix of all, but lately tilting towards value… Never tried portfolio visualizer. I will.

https://www.fidelity.com/learning-center/trading-investing/trading/value-investing-vs-growth-investing

Couldn’t agree more. People waaaay over-index on dividends at the cost of long-term performance. Some even start messing with preferred shares etc that are super volatile and have iffy returns long-term. This is good advice.

Thanks! I mean, I like dividends. I just don’t see a reason to prefer them over appreciation, and definitely, see negatives to over-indexing.

You should be “living off corporate profits” instead of just dividends. Living off your dividends might be way too conservative at times when corporations pay out only a fraction of their profits and reinvest the rest. Why ignore that? You’d never be able to retire if holding BRK.B. I’ve written about that approach, i.e., gearing the withdrawal rate to the Shiller CAPE:

http://earlyretirementnow.com/2017/08/30/the-ultimate-guide-to-safe-withdrawal-rates-part-18-flexibility-cape-based-rules/

I think your link says spend more than dividends but less than corporate profits, so principal is OK it is just a question of how much.

Current #s from multpl:

Earnings yield: 4.7%

CAEY: 3.3% (will get goosed when 2009 numbers fall off)

CAPE 1.5/0.5 = 3.1%

1Y Trailing earnings are indeed close to 5% yield now, but I suggest not using that earnings definition because during bear markets, EPS occasionally drops by 80+%. During 2008/9, some countries saw negative EPS. It’s hard to build a withdrawal rule based on that. CAPE is smoother but also has the 2009 issue. But even crossing our fingers and hoping for continued economic expansion it will take a while for the CAPE to drop to 25.

The CAPE-rule SWR of 3.1% is built for folks with an equity share around 70-80% (rest in bonds). The bond portfolio can’t sustain the same SWR as equities, given today’s low real interest rates.

But not all is lost: The 3.1% SWR can be adjusted upward to account for two factors:

1: rolling out 2009/10 as you mentioned

2: capital depletion (the CAPE rule parameters were geared toward capital preservation)

With that, you’re probably north of 3.5%, maybe even close to 3.75%. That’s certainly not ALL of corporate profits but significantly more than purely dividend yield.

Sorry if I wasn’t precise enough in the initial comment! :)

Now add Social Security and you are at 4%

I know I’ve done this as well, but I enjoy the implied precision of 3 significant digits on the withdrawal rates in your post ;)

Social Security (and don’t forget pensions) make(s) a huge difference for early retirees in their late 40s and will likely push the SWR even way above 4%. Especially in two-income households! I’ve done some case studies where I recommended folks go for SWRs>5%. But Social Security has a pretty small impact on retirees in their early 30s.

The number of significant digits and precision: I personally think that 1.00% steps in the SWR (see Trinity Study) are way too wide. For a $3m portfolio that’s $30,000 steps in the annual budget. Even 0.25% steps (and now we’re at 3 significant digits) produces $7,500 steps.

Also, just because outcomes (future market returns) are uncertain doesn’t mean we shouldn’t use input parameters with whatever precision we see fit. When I was still working I used to write programs using statistical tools and I would input the parameters with whatever precision Matlab allows; 16 digits, I presume. I never claimed that I had any precision in predicting outcomes. Only the distribution of outcomes. Subtle difference!

But that’s all getting too philosophical and too far away from your original post, which I enjoyed very much, by the way! Keep up the great work! :)

I definitely plan on spending principal but I will admit that it scares the hell out of me. I just hope that at some point after my 5 year conversion ladder is complete I will hit the point where I might be able to start running a surplus of shares with reinvested dividends. I do have one question regarding VTSAX. After talking with Personal Capital they showed me that my investments are way more Technology heavy and definitely have a higher percentage of Apple, Google, etc. I pretty much have everything in VTSAX or the S&P 500 in my crappy company retirement plan. But since you mentioned the benefits of having more small and mid-cap stocks above. Do you think there is a better fund that has a better diversity/balance than VTSAX during the accumulation phase of FIRE? Always a pleasure reading your blog.

The problem is that in order to know what you are asking, one has to be able to predict the future (ie what sector or factor will outperform). Nobody knows this. Thus, most feel that holding the market is the best bet. I think you are doing the right thing with holding S&P 500 and total market index. You could add a little international as well. You’ll likely do much better than any financial advisor over the long term, especially net of fees

Thanks for the input. Yeah, I was not impressed with Personal Capital. They only use about 100 different companies and charge .83% fee. Based on the data they showed me, they have historically returned about 1% more than VTSAX. I think that is with tax loss and gain harvesting which won’t apply to me since all of my investments are tax deferred. Also, that was only looking at the last 10 years of this wonderful Bull Market.

> Do you think there is a better fund that has a better diversity/balance than VTSAX during the accumulation phase of FIRE?

No, that is the one.

Thanks for the response and letting me know I’m on the right track. Leave it to a financial planner to plant that grain of doubt even though following your advice for the last 6 years has allowed me to kill 6 figures worth of debt and get me half way to FIRE. I’m so thankful for being able to interact with this you, the FIREstarters, and this community. It’s a life saver.

VTWAX

Another great post on this subject GCC, and the second of yours to now be an Addendum to this one of mine:

https://jlcollinsnh.com/2011/12/27/dividend-growth-investing/

:)

Wow, thank you sir!

You’ve addressed a natural, but misguided, desire that people have. They want the stock market to work like a rental home, pumping out income without affecting the underlying asset. But sometimes you have to take off some of the shingles and siding and sell it off. The neighborhood is always improving though, so the home value tends to increase anyway.

My favorite part about the stock market is that it doesn’t act like a rental property – no crappy tenants, no leaking roofs, no vacancies

Life Shrinks or expands in proportion to one’s courage. I have been following MMM, JLCollins FIREcracker and now Curry Cracker. It is nice to see the FI bloggers commenting on each others posts. It gives me peace of mind knowing they are auditing each other. My wife and I have done a life makeover since finding the FI community, we quit our career jobs making money for others and started a small business. We now work part time and still save 75% of our income into S&P 500 Index and VTSAX!!! Unfortunately the business has doubled and we expect it to quadruple. We are now looking for employees to work for us. Thank you FI community.

Congratulations :)

What’s your company about just out of curiosity ?

Agreed on all parts.

I don’t like high dividend stocks and I especially don’t like the lack of diversity/tax efficiency.

I think because I’m planning for a 4% full retirement in the us in a high cost of living area, I likely will spend mainly dividends.

I very much enjoyed my time in Mexico and love the weather, food, people and cost of living. If I spend the first few years in a low cost of life bing area, with a little cooperation of the market, I’ll likely spend mainly dividend percentage (based on today’s total stock market return) but sell principle in the taxable account and reinvest the 401k.

How do you bridge the gap between 2% S&P500 yield and spending the full 4% in your US example?

The initial years of retirement would be low cost of living so likely spending 1-2% and reinvesting the rest.

Depending on how long I did that with growth the withdrawal rate could lower to 2% although doing the math, it would take a while.

Realistically, I’ll just sell some of the principle of vti and not worry about it much.

On an unrelated note. When you did medical tourism for a dentist, how did you choose which to go to? Next time I’m in Mexico I’d love to try it out.

Ahh, makes sense now. That is more or less what we did.

We just asked local friends if they had a dentist they liked. Basically the same as at home.

This is a nice, concise explanation of a complicated topic. The logic and reasoning of the index/4 percent perspective are unassailable.

Having said that, in my case I have an emotional aversion to spending principle (it took so long to build up, its painful to spend it down!). I have tried to “have it both ways” by maintaining both a dividend stock account and a separate index fund account.

Most of my money goes into the index funds, but I indulge my “never touch the principle” emotions with the dividend account. So far so good, but I am still in the accumulation phase. We will see how it goes when it’s time to start spending.

Thank you very much for this excellent piece!

Have you thought about investing in a notes fund which yields 10% and is backed by 1st position and some 2nd lien mortgages? Check out (link removed) . Caveat this is only for accredited investors but if you have 1mm in cash lying around then you are good.

Nope

Joseph, this kind of “financial gymnastics” is not necessary for those of us who want to live off VTSAX. It’s simply not necessary. That’s the beauty of a 3-4% withdrawal rate on VTSAX; the simplicity… really straightforward and easy for anyone to manage and understand.

Something that comes to mind often when considering living off dividends/gains is that the logic presented here is easier to apply when markets are trending up, like it’s been. What would you do to your gain portion of income if, after say a multi-year bear market, you simply ran out of gains to tap? (Assume your income comes from investing only.)

Easier for whom?

I think the best way to hedge is to keep at least 20% of your savings in cash, say in your ROTH or IRA, that way if you have to spend down your investments in your taxable account in a multi-year bear market, you won’t really lose anything because you turn around and buy the investment back with your cash. What’s your take on this Jeremy?

Wade Pfau has done some interesting work around debunking the 4% withdrawal rule. It might be of interest to people considering that strategy: https://www.barrons.com/articles/retirement-rules-time-to-rethink-a-4-withdrawal-rate-1428722900

We use real estate and online business income to cover current expenses and let our paper assets compound in the background as a safety net. Since we’re in our 40’s we’d prefer not to tap the paper till later on in life — to reduce sequence of returns risk and shorten the draw period.

Yup.

In one of his more widely distributed critiques, he uses portfolio fees of 1% and concludes around 3% spending is OK.

In another, he starts from the premise that future returns will be much worse than in the past. And then proceeds from there.

Hi, does it ever make sense to have all dividends reinvested and just withdraw principle in intivals when you want to receive same. Not sure if this makes sense tax wise or is even possible.

Money is fungible so this is six of one, half dozen of the other. Same same.

Hi. Thanks for writing this. I completely agree with your conclusions after heavily using portfoliovisualizer over the last year. As you point out this is obviously very starting capital dependent. If someone has say 4million starting cap then the dividend approach with a bond split might be a good route. That person might not ever have to touch their capital as they are getting close to 150k pretax in dividends/interest.

yeah OK but BUYBACKS will and should have for long be consider ILLEGAL. It’s a scam companies use to inflate share prices so CEOs can get fat checks. This is going away soon.

You should really ready the book “All about dividend investing”. It might change your mind

uh, no.

I live in Australia and this subject of “living off just dividends” is one of the most talk about topic in the Financial Independence community forums here e.g. https://www.reddit.com/r/fiaustralia/.

The Vanguard Australian Shares Index (ASX:VAS) dividend yield is 4.45%(http://www.etfwatch.com.au/funds/VAS/) so that could easily meet the 4% rule. And to quote an article in Vanguard below:

“And because of the imputation system here in Australia, this ETF is very tax efficient for Australian companies pay franked dividends, those franking credits are paid to the ETF, which are entirely passed through to ETF investors. Each quarter, the ETF distribution contains details of the amount of franking credit and the percentage of dividends that were franked”. (credit to https://www.vanguardinvestments.com.au/retail/ret/articles/insights/research-commentary/etfs/ETFs-can-help-to-minimise-tax.jsp)

So our 4.45%dividend yield could be around 5.45 because of the franking credits.

So if I me and my wife have a combined 1,000,000 in ETF, we could easily live off 44,500-54,500 in dividends gross before tax. If we hold the account 50-50, that means our taxable income is 22,250 each (before franking credits). 18,200 is tax free so that means only 4,050 is only taxable (https://www.ato.gov.au/rates/individual-income-tax-rates/) which is tax at 19%.

Now please let us know, for us who live in the land down under, why is it that living off just dividend is not a good idea?

P.S. I would like to ask permission to post your answer on our reddit forum https://www.reddit.com/r/fiaustralia/, if that’s OK with you.

Living off dividends can be a good idea. It just isn’t necessary.

Australia is <2% of global GDP. It would be a good idea to own more than just Australian equities.

I want to ask a really mundane question. How do you physically pay for things? For example, do use a credit card for most day-to-day purchases, big one-time expenses, etc.? And then how do you pay off that credit card? Do you directly transfer funds from your investment account to pay off the card? If you are paying from the investment account, you are withdrawing from the principal amount of one of your funds?

If you need to withdraw actual cash, where do you do that? Do you keep a cash reserve anywhere or do you keep everything in your various investment accounts? Is rent automatically paid from a bank account? Maybe you posted about this at some point in other posts that I have yet to come across. I feel like I am missing some silly fact that will help me better understand how early retirees get on with the day-to-day.

Cash Flow Management in Early Retirement

I am just now learning how much dividends are effing over my income control strategies I learned from you. I sold a business last year along with my primary residence, netting me 3MM net worth after tax. My plan was to jam all this all into VTSAX in a taxable account, but at 3MM invested and ~2%/year dividend that puts me at a mandatory 60k taxable income.

I’m single so this completely fills my 0% bucket of $51,575 ($39,375 + $12,200 standard deduction). Exposing $8425 to 15% federal tax and leaving me no room for Capital Gains Harvesting, Roth IRA Conversions or any other great strategies I learned from your blog to “Never Pay Taxes Again”. Not to mention, I plan to live off more like $80,000 per year so any realized gains from shares I have to sell are immediately exposed at 15% taxes as well. Any crafty ideas for someone who shares your dividend woes?

Hey Danny, congratulations on your successful entrepreneurial efforts.

If you are in the US, you may not be able to (efficiently) use a lot of these tax minimization strategies anyway (cuz: ACA.)

Some things you could try:

– invest in VTCLX and VTMSX instead of VTSAX (slightly lower yield but higher fees…)

– buy your primary residence for cash – double “benefit” of imputed rent (lower expenses) and fewer dividends

– put a portion of your portfolio into Berkshire Hathaway – no dividends at all, sometimes tracks overall market

– don’t let tax tail wag the dog – accept a $2k/year tax bill on $80k cost of living (2.5% effective tax rate)

– get hitched

Basic question here since I’m not familiar with the 4% “rule”. Do you count dividends as part of your 4% ? Or can you “safely” take out up to 4%/year AND all dividends offered?

You don’t get to withdraw 6% (4% plus current ~2% yield on SP500.)

Become familiar with the 4% rule by reading this.

Hi Jeremy,

Great article; this is my approach, up to and including the capital gains harvesting in the 0% bracket to Never Pay Income Taxes again. I like the idea of dividends as I don’t have to do anything, but at the same time, if I had less taxable dividend income, I could use that space for Roth conversions. I think this is right on; thanks for the number crunch on how the two portfolios perform over time in good and bad market conditions.