I have now submitted our 2024 tax return. Somebody (me) has exceptional procrastination skills.

The numbers this year are very nice – overall we “earned” more and paid about the same.

The Go Curry Cracker 2024 Taxes

Executive Summary

Total income was higher than last year due to realized capital gains and higher blog income (in part due to more consulting.)

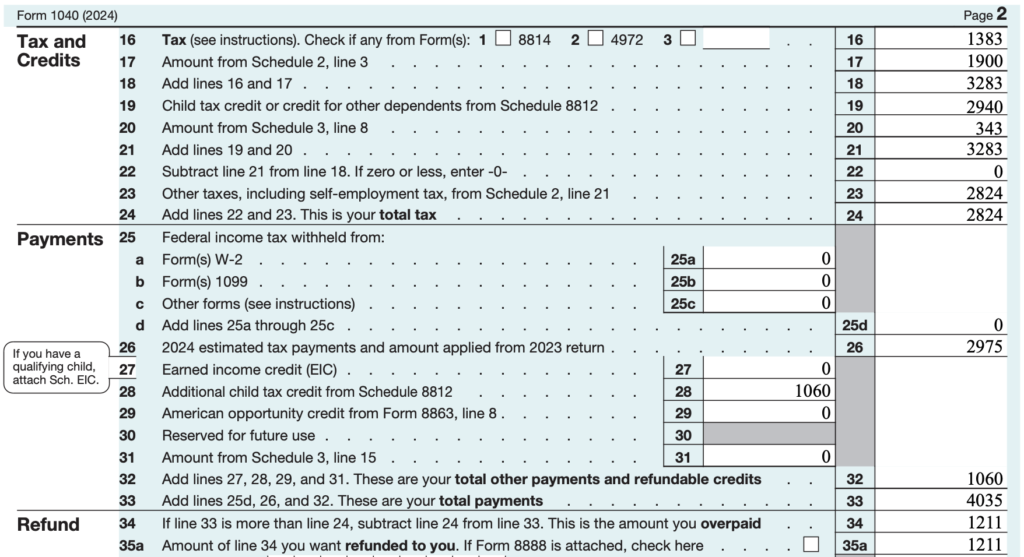

Overall we paid $0 in federal income tax (net $1,060 paid to us in refundable tax credits), $0 in California income tax, and $2,824 in self-employment taxes (which increase future SS income.) Not including all health insurance related credits, total tax burden was $1,764 or ~2% of total income.

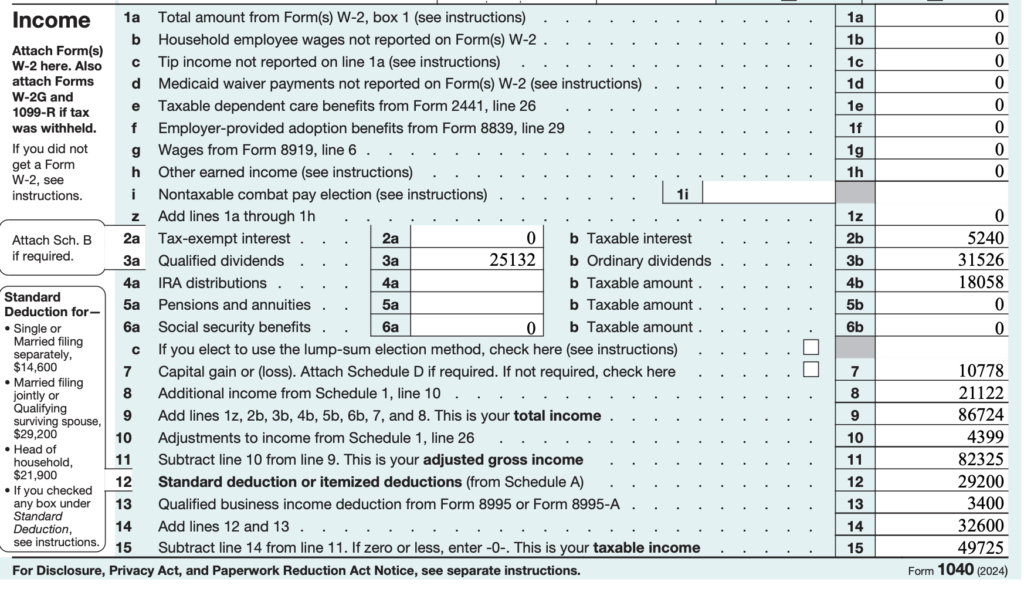

Form 1040

- Income – $86,724

- W2: $0

- Interest: $5,240 (mostly from short-term US treasuries, using money borrowed from credit cards at 0% interest)

- Travel hacking: $0 (but spent $0 on a week stay in a $1,000/night all-inclusive resort in Mexico)

- Dividends: $31,526

- Qualified: $25,132

- Blog profit: $20,322 (significant increase over prior year thanks to consulting) (Line 8, majority)

- QBI deduction: $3,400

- Credit card referrals: $800 (included in Line 8)

- Roth conversion: $18,058

- Capital Gain

harvest: $10,778

- Federal Income Tax: -$1,060

- Income tax: $3,283 (Line 18)

- Income tax: $1,383 (Line 16)

- ACA excess tax credit repayment: $1,900 (Line 17) (LIMITED)

- Tax credits: $343 (Line 20)

- Foreign Tax Credit: $276 (but paid $708 in total foreign taxes)

- Child and Dependent Care tax credit: $67

- Retirement savings contribution credit: $0 (Roth conversion reduced this to $0)

- Child Tax Credit (Line 19): $2,940

- Additional Child Tax Credit: $1,060 (Line 28)

- Total: $4,000 (the maximum value)

- Income tax: $3,283 (Line 18)

- Self-employment tax: $2,824 (Line 23) Results in higher future Social Security

- Retirement Contributions: $18,000

- Solo Roth 401k: $18,000 (placeholder value… I could have increased this another $574 before filing.)

- Roth IRA: $0 (Oops… procrastination sometimes has consequences – in theory could have contributed full amount for Double Dip.)

- Roth IRA – spouse: $0

- ACA – MAGI = 274% FPL ($82,325)

- Cost of 2LCSP: $15,275

- Cost of health insurance: $16,362 ($1,087 more than 2LCSP)

- My cost based on MAGI $4,083.32 (4.96% * 82,325) + $1,087

- Total premium tax credit: $11,192 ($15,275 – $4,083)

- Premiums (paid by me): $1,062.72 (88.56 * 12 = $1,062.72)

- In advance: $1,062.72

- Form 1040:

$1,900(paid by tax credit on Form 1040) - Not paid due to repayment limitation: $1,120 ($4.083 – $1063 – $1,900)

- California: $0-ish

This is how it all looks on the tax return: (copied from OLT, Online taxes – a free filing service)

Items of Interest

Every year when I publish our tax return I try to think of a few interesting things to highlight. This year there are 4.

Qualified Business Income (QBI) Deduction

The QBI deduction allows a business owner to deduct (up to) 20% of all (qualified) income right off the top. Of course all other/normal deductions still apply. Just based on 20% we are allowed a deduction of $3,400 in 2024.

But… and this is a very big but… this deduction cannot be applied to other qualified income, e.g. qualified dividends and long-term capital gains, or to income that is deducted / excluded in some other way.

Said another way, total ordinary income must exceed all deductions before we can even start to take advantage of a QBI deduction.

Example:

Coming into December 2024, I had yet to do any Roth conversions or realize/harvest capital gain (or do any tax optimization stuff, really.)

My total possible QBI deduction? $0.

Because the standard deduction ($29,200) and top-of-line deductions ($4,399) exceeded total ordinary income ($32,756), all business income was already excluded. I needed more ordinary income.

I got this in the form of a Roth conversion (Line 4b.)

To get 100% of the possible QBI deduction, I sized the Roth conversion such that ordinary income exceeded deductions by (at least) the amount of qualified business income.

Now my QBI deduction is the full 20% of business income, or $3,400 (Line 13.) (Or is it that 20%+ of the Roth conversion is tax free?)

In terms of value… with a 10% federal marginal tax rate, this was worth $340.

ACA repayment limitation

When enrolling in an ACA marketplace plan we pay monthly premiums based on projected / estimated income for the year. At tax time, we true up. If income is lower we get a refund of some of those premiums. If income is higher, we pay more.

If income is much higher, we also pay more… but the total is limited thanks to the ACA repayment limitation.

Based on our AGI, we were expected to pay 4.96% of income ($4,083) towards health insurance premiums. This is a great deal more than the $1,063 I paid throughout the year. In theory, I should be paying the remaining $3,020 but this is capped at $1,900. (And would have stayed at $1,900 even if I pushed income up to 300% FPL or $90k.)

Total value: $1,120

Note: Ideally this won’t happen again. Or at least not very often. It is good to estimate low, but not too low.

Maximum income

These past 3 years we have paid basically $0 in federal and state income tax. The difference this year is that income is about $15k-$20k higher.

How high could we have pushed income? Could I get a larger Roth conversion? Harvest some (more) capital gains?

What are the limits?

Well.. at $76,500 (~254% FPL) I lost the Saver’s credit. Last year this was $400, so roughly equal value to this year’s QBI deduction.

At 266% FPL or $82,992, the children are no longer eligible for Medi-Cal. (Medi-Cal uses different FPL numbers from ACA.) This has at least a few thousand dollars of value.

At 300% FPL or $90k, the ACA repayment limitation increases by $1,250

At $102,900 (343% FPL) income would exceed 80% of median income for our county, at which point we would be ineligible for the extra juicy HEERA rebates (but still qualify for somewhat smaller rebates.) I’m still hoping to get a free water heater out of this. Quotes have ranged from $5k up to “I don’t want this job.” (Without a juicy subsidy I would most likely DIY it for $2k.)

So many potential limits… but with the next topic, maybe it makes sense to break through these ceilings from time to time (even without math permitting? More analysis required.)

Limited Roth Contributions

Again this year we had the ability to double dip Roth contributions. With ~$18k in “earned income” I can contribute $18k to my Roth solo 401k, and then with the same money contribute $8k to my personal Roth and $7k to the Mrs’ Roth. Yes, I am now eligible to make catchup contributions.

But I only made the contribution to my solo 401k for a total of $18k. Why is that?

Simply stated – I didn’t have the cash. I have been unable to make ongoing capital gain harvests since being back in the US, so getting more cash requires selling highly appreciated shares. I probably could have made it work, but that might mean I start withdrawing Roth contributions / seasoned Roth conversions next year to manage cash flow (rather than a year or two later.) So the motivation isn’t exactly high.

Estimated Taxes and Travel Hacking

An interesting thing, nowhere on our 2024 tax return does it show the thousands of dollars not spent thanks to credit card rewards points. (Flights to Taiwan, all-inclusive hotel in Mexico, etc…)

Not a bad view from the room – sandy beach, pools, lazy river, water slides, and kids can get pizza & drinks whenever they want.

If you earn award points through credit card usage or signup bonuses, the IRS just treats these points as a refund on your purchases. There is no income and therefore no taxes. (See our Award Travel Series on Transferrable Currencies.)

Ironically, we actually got a lot of these points by paying taxes – we pay self-employment taxes quarterly, and I often use that “opportunity” to meet the minimum spend on a new credit card. I paid estimated taxes of $2,975 (Line 26) to the IRS throughout the year, mostly as part of new credit card spending requirements.

If you are going to have to pay some taxes anyway, you might as well get a nice vacation out of it. Even if you are not going to pay some taxes anyway, get a nice vacation out of it :)

Related:

- Aloha Uncle Sam (paying taxes with a credit card to get a free Hawaii honeymoon)

- Award Travel Series: Getting to Hawaii for Free with Ultimate Rewards

Summary

Another year, another tax return. This time with much higher income and the same low/minimal/zero tax burden.

For expats, the various US tax systems have incredible complexities and interact in numerous bizarre ways. US residence only complicates things further. But… after nearly 4 years back in the US I feel like I’ve largely worked out the most important bits. Maybe.

This year had 2 firsts – I was able to use the QBI deduction to the fullest and we hit the ACA repayment limitation.

Great work! You were saying your income was higher, so were your expenses higher?

I asked because it seems no matter what our income is, our expenses remain about the same every year.

Expenses were similar if we ignore that we are now a 2-car family.

Hi,

Is there a glitch with the federal tax calculator? I inputted numbers and it’s not working. Thanks

Hi,

I noticed the Federal Tax Calculator isn’t working. Is there a glitch?

Total realised income [9]:

= 86724

Personal Tax on income [33]:

= 4035

Personal tax refund:

= -1211

Company tax on gross dividends:

= 21% * (31526 / (1 – 21%))

= 8380

Total tax:

= 4035 + -1211 + 8380

= 11204

Total tax rate:

= 11204 / 86724

= 12.9%

My Aus total tax rate:

= 13.7%

Maybe I should have moved to Australia!

Does your tax rate include the cost of health insurance? $1900 of the tax total is health insurance premiums.

Personal tax on income is line 24 (rather than line 33.) $2824 rather than $4,035. 100% of that is because of this blog – if I had zero self-employment income and instead just withdrew from my retirement accounts then this tax would be zero. The only reason for the distinction is because this tax payment means I will get higher income from Social Security later.

All direct Commonwealth [Federal] taxes included.

Territory [local] property tax $A3,155 / y not included. Based on unimproved capital value not income.

Medicare $0 as two personal incomes total is under $A62,006 tax-free threshold [SAPTO offset] and we have sufficient private hospital insurance.

Medibank Silver Plus Advanced Hospital $500 excess premium: $A4,400.93 / y.

Cheapest couple health insurance that avoids Medicare levy surcharge is Medibank Bronze Plus Value $A1,996. Optional but could be seen as a Commonwealth tax.

Possibly redundant due to good free Territory funded public hospitals, except wife wants it.

No personal contributions to Age Pension [Social Security] which is means tested welfare for couple from 67+ of $A45,037 / y. No obvious likelihood of our receiving it.

Couple cost of living with modern ‘essentials’ ~$A25,000. Living it up >= $A40,000.

“Personal tax on income is line 24 (rather than line 33.) $2824 rather than $4,035.”: 4035 + -1211 = 2,824. Same.

If I subtract Company Tax credits which will be imputed to us personally when our company pays us dividends, our overall tax rate would be 5.5%.

Our personal capital generates income exceeding the tax-free threshold with a marginal tax rate of >= 28.5% so profits are retained in the company with a tax rate of 25%, and not paid as dividends.

We would have to spend big to empty our personal pockets to pay grossed up dividends, to the tax-free threshold, to us personally to receive the imputed company tax credits as cash refund.

How’re you liking the leased Ioniq? Any more thoughts on that after having it for close to a year now?

How are the other home electrification projects going? I’m having Hooked On Solar put in a 2.94kW array for a net cost of $9,087 after the tax credit and referral bonus. I’m thinking I should’ve gotten a quote from the company who did yours Nationwide Sun as your price/kW seemed. to be lower.

Car is great. I would get another one. I have all of the 120V circuits in the house able to run off the car, but don’t use it much because of the hassle factor of charging the car more often

The cost/kW will go down as size increases. We have 7.6 kW

“2.94kW array for a net cost of $9,087”:

$3 / kW.

All up installed price in Aus: $A1 / kW, $US 0.65 / kW.

https://www.solarchoice.net.au/solar-panels/solar-power-system-prices/

Installed over tile or steel roofing, attached to battens beneath.

‘The U.S. has recently imposed high tariffs on solar panel imports from Southeast Asian countries, specifically Cambodia, Malaysia, Thailand, and Vietnam. These tariffs, reaching up to 3,521%, are a result of an investigation into alleged subsidies and dumping of cheap solar products by Chinese companies operating in those nations.’

“2.94kW array for a net cost of $9,087”:

$3 / W.

All up installed price in Aus: $A1 / W, $US 0.65 / W.

Thanks for the post. I always look forward to reading them. You’re an inspiration for me to get to financial independence.

I cannot recommend it highly enough

You are always amazing and an inspiration to me also. Thanks!

Every year I wait for your taxes post because I learn something interesting. Thank you!

Wish I would have thought about the QBI deduction in this interesting way when we had business income but maybe it will come in handy someday when we have unexpected income.

We are fire’d and honestly couldn’t have done the taxes part without your help.

Glad to help! Congrats on the early retirement.

I was wondering about HSA reducing AGI for ACA purposes – If I have a HDHP that allows HSA, I think I can contribute without any earned income. If I do this, would it be tax deductible and reduce my AGI for ACA purpose? If yes, why don’t you or many people do it since it effectively increases AGI runway by 8000+ for family?

This seems like a good option especially since all bronze plans will be required to have HSA with the new bill. Not sure if I am missing something obvious here. Thanks!

>I think I can contribute without any earned income.

>Would it be tax deductible and reduce my AGI for ACA purpose?

Yes to both.

>Why don’t you do it?

It has value that we can measure.

A deduction is worth $X on a tax return. For us (per the tax return above), X = $0. I’m already unable to utilize all tax deductions available to us. For somebody with a greater tax burden it could be worth more.

Or if I had $8k in cash on hand to contribute to an HSA I can do an $8k Roth conversion with no tax impact. Then we have the tax free growth from both the Roth and the HSA ($16k total.) That seems nice.

But that has a cost too. I don’t have $8k in cash though so would generate some taxable income to get it, e.g. by selling stock. I would also be unable to claim the full CTC (worth about $1,900, see tax return above.) And I would pay substantially more if we had anything beyond preventative care (increasingly likely after age 50.)

For 2025 we have a Silver 87 plan that I pay about $100/month for. Our actual cost of care if something were to happen is very little.

I could instead choose a Bronze plan and pay $0/month in premiums and then pay 100% of care up to the deductible ($6500/$13300 individual family.) Estimates for cost of care for low/high usage were ~$900/$7k (but could be as high as the deductible.)

I think I could argue that there is no obviously best option.

10-20 years ago I probably would have gone with the HDHP and HSA (and did, once upon a time.) Nowadays, I’ve chosen to go with a lower cap on my health care spending as the probability of needing care is much higher.

For details on how we figured out which health plan was best, see: Choosing our ACA Health Insurance Plan for 2025

Thank you so much for this, very helpful. I follow the federal tax return, but can not figure out how you achieve $0ish on your California income tax return. Smaller standard deductible, and the qualified dividends and LT Cap Gains get taxed at ordinary rates. Can you expand on the CA return?

California is a low tax State, which helps.

On the CA tax return we itemize deductions (prop taxes and mortgage interest) and get to a total tax of about $1.2k. This is offset by the personal exemptions (2*$149) and the dependent exemptions (2*$461) on Line 32 of the 540. (2024 #s)

Thank you! Just took the leap in March of this year. Taxes in CA were not low as a highly paid W2 employee compared to other states, but now in my current situation I agree they compare pretty favorably. Perspective is everything. I really enjoyed your content as I prepared to enter early retirement, helped me work through the numbers to feel comfortable.

My pleasure. California’s marginal tax rates on higher incomes are perhaps higher than in some other places, but Prop 13 should probably be factored into total tax burden.

Dear Jeremy, I appreciate your answering my occasional questions over the years, so I wanted to see if I could point you in the direction of some useful information.

It need not be true that the probability of needing medical services is much higher at your age or after age 50. With the possible exception of traumatic injuries such as car crashes, the great majority of medical problems are under our individual control. This fact is not popularized.

You can read these books to explain what I mean: The Mindbody Prescription, and Healing Back Pain (includes many more problems than just the back) by Dr. John Sarno; The Will to Live by Arnold Hutschnecker (says something similar to Sarno in a different way). You see, the medical industry that pays us these big dividends and the ever increasing stock prices do so because they are designed to substitute one medical symptom for another at great expense. They are not designed to heal anything, or to prevent anything; rather the opposite, they are expressly designed to cause and contribute to disease on a population level, so that they can be treated profitably. You could think of it as a huge stealth tax on unconsciousness, greater than anything we pay to the IRS. But it is subtle. The books explain in detail, especially Sarno’s.

Thanks, I’ll put these on my reading list. Maybe similar to the food industry.

Np, I read another of your old articles, or maybe it was an interview, where it said you don’t care what other people think or say about you. You have that gift. I believe your wife said it. Can you elaborate on that? Like when someone says you should be doing so and so or providing such and such, acting in this way or that, having this or that status in the world, etc., what is your internal feeling reaction and thinking in response to that? Especially if the person saying it was a close family member, like a parent. Was it always that way or did you have to cultivate it? Maybe it’s too personal and if so, I understand. I’ve had this problem myself, and many people I know do too. Caring too much about appearance to others or “roles” in society.

This can probably best be summarized by the saying: No one can serve two masters. Attempting to do so (by doing what others say we should x 8 billion people) seems like a recipe for unhappiness and perhaps even psychological disorders. However the opposite could be considered sociopathy, so there is a balance.

I get this question a lot particularly from people with Asian parents or Tiger moms. If we always do what parents say without question there is no reason they will ever stop trying to control. The umbilical cord does need to be cut at some point. It is perfectly reasonable to listen to the opinions of people we respect and have a track record of good suggestions, but ultimately we have to make our own choices.

Early retirement is a perfect example of going your own way. We should work until the socially approved retirement age, they say. But I like my life better without work so that is the opinion I follow. My life is exactly the same regardless of what other people think or say about that.

Interesting!

If your earned income is $14k, could you put $7k into your traditional IRA, $7k into your wife’s traditional IRA, convert $30k from traditional to roth, and cap gain harvest $94k-$30k=$64k tax free?

More, actually.

For 2025, a married couple filing jointly could do a Roth conversion equal to the standard deduction ($31,500) and harvest gains up to an additional $96,700. All with zero federal income tax.

Separately, with $14k in earned income you could contribute $7k each to his/her IRAs. Rather than contribute to Traditional and then do a Roth conversion, it would be better to contribute directly to Roth and do a smaller conversion. If need be you can withdraw contributions at your leisure with no tax impact but must wait 5 years on a conversion for the same flexibility.

You can play with this using the GCC income tax calc.

Thanks!

Your calculators are a lot cleaner than my spreadsheets.

I’m also juggling ACA bronze plan for family of 5. There’s only a narrow $3k window where I can pay $0 for bronze health insurance and still avoid Medicaid in Georgia. Personally I think medicaid would be fine, but my wife doesn’t feel good about it.

My calculators are a lot cleaner than my spreadsheets also.

There are a lot of stigmas with Medicaid. Also consider paying more than $0 for ACA in order to increase Roth conversions, etc. And make sure you get the full CTC.

Do I have control over getting the full CTC? I thought that was just based on earned income. Does a traditional IRA contribution affect it?

This is my first year of low earned income

Yeah, you have control. The ACTC has an earned income requirement, the CTC does not.

See: Maximizing the Child Tax Credit (even without earned income)

Just as an example, let’s say you have 3 kids and can get up to $6,600 in CTC in 2025.

If you have no earned income and your tax bill is $0, you receive $0 of the $6,600. Said another way, the $0 Bronze plan can actually cost you $6,600.

In the context of doing a $31.5k Roth conversion and $96,700 cap gain harvest, it could be better to do a ~$90k Roth conversion which would give you a tax bill of ~$6,600. This would then be reduced to zero by the CTC. ACA plan costs more than $0 in this scenario, but a lot less than $6.6k. You can play with the numbers to find the balance that best meets your preferences.

As a complete aside, this is one of the things I do with tax optimization clients. See: Consulting

I think I finally get it! Thank you!

I think the CTC strategy you explain above is the same for all non-refundable credits, right? The stuff on Schedule 3 Part 1?

Thanks for pointing this out.

Yes, that is correct. Although it can be difficult to get multiple CTCs and other credits while keeping AGI low enough for reasonable ACA PTC.

I’m surprised you ultimately didn’t do any brokerage bonuses. Just not worth the bother?

4% on a large number is nothing to sneeze at.

https://www.webull.com/offers-promotions/deposit

4% is nice. It is really 0.8% per year for 5 years and you can’t touch any of those funds until year 6, but still… not bad for just parking excess funds.

I have played a bit with brokerage and bank bonuses this year. I’ve collected $11k so far and another $1,200 coming this month. It was slightly more effort due to multiple accounts but I can spend the $ now and do it again next year.

Hi, is $86k in income per year enough to support a family of 4 in California, especially with 2 children in school? The cost of living got very expensive even while cooking at home and doing only few things/trips once in a while.

It feels like enough. But we are spending more than we earn.

https://www.gocurrycracker.com/75k-lifestyle-requires-210k-income/

So how is planning for 2026 going?

Basically done. It will look very similar to 2024. Exact values of Roth conversion and realized capital gains will depend on size of Q4 dividends.

Sweet, glad to hear. Our plan is now done and feels like a smooth glide into 2026 as well. The biggest move I got for January is to close some credit cards that we don’t need or want. Perks dried up and/or fees went up. Wishing you and your family a very happy Thanksgiving.

Lots of not great changes in the credit card world this last quarter. We are ditching the CSR and replacing with an Amex Platinum. The devaluation of UR points is a bit of a bummer.

Our ideas about travel have changed and we try to stay away from airports unless there is a non stop flight to where we want to go. We also use a driver now. We can stop, eat, sleep, etc. where we want.

What are the perks of AmexP ?

Can you expand on how you use a driver? How does that work? Sounds interesting.

There are pros/cons/perks to every card, but the only one I’m really interested in for the AmexP is the welcome bonus.

Drivers are family and friends that join us on vacations, shopping trips, dining and doctor visits. We are very thankful for them.

WF is my card with 18 months 0% interest, I will ride my bicycle to the bank next November and pay off our living expenses.

When we run out of points on UE I may apply for AmeP.

What kind of trips are you planning to use your 175k points on?

We are going to Italy for the month of June. I’ll use the MR points for that… not sure how yet. Flights were booked to clean out our UR stash.

I also have a bunch of 0% cards. Still owe about $40k with payoff dates between now and May.

Very exciting plan, wish you the best. Please let us know how it all works out.

Love your blogs, and these tax posts. I had a question – I’m thinking of pulling the plug in a year or two (or earlier if the company let’s me go as part of a re-org). How would I plan for myself, for a single person, say mid-40s while also considering ACA subsidies? I’m thinking my target MAGI has to be around $30K to be in the sweet spot for ACA, and I have currently unavoidable income due to interest (downpayment for a home but currently priced out) and qualified dividends from stocks in my brokerage (I could sell down but 40%+ capital gains).

* MAGI Target = $30,000

* $10,000 interest / non-qualified dividends (from cash/short-duration bond tent position to protect against SORR)

* $10,000 qualified dividends (similar treatment to LTCG right?)

* $14,300 Roth conversion from IRA

* -$4,300 HSA contribution if I pick a plan with high deductible

Does that seem right?

Seems about right. If you are going to get a bronze plan so you can have an HSA, you can probably push your income above 200% FPL and still have $0 premium.

See chart in this post: https://www.gocurrycracker.com/choosing-our-aca-health-insurance-plan/

That could get you an extra $7500 Roth conversion at 10% – 12% federal tax. And/or realize some LTCGs at 0%.

Related calculators:

https://www.gocurrycracker.com/aca-premium-calculator/

https://www.gocurrycracker.com/federal-income-tax-calculator/

For your consulting business, do you use 1099 or do you form a LLC? Thanks.

1099. No need to complicate things

Was looking at gcc vs rmd and I’m hoping you can clarify how we can maximize tax free roth conversion. It seems to depend on standard deduction $31.5k but if our investments have says $30k in dividends and interest, does that mean we can only have 1.5k tax free conversion?

Also, tried joining mailing list but get ‘Account is cancelled and can not accept new subscribers.’ :(

Play with the tax calculator. MFJ can have $120k+ income with zero tax

https://www.gocurrycracker.com/federal-income-tax-calculator/

I see, qualified dividends are capital gains taxed. Thank you Jeremy!

I need to start moving things around to minimize ordinary income to maximize the roth conversions