We will never have the experience of receiving an inheritance, but GCC Jr will.

In my role as fiscal steward, I would like to ensure that he, along with our other beneficiaries, receive the largest amount possible. (After we are done spending as much as we want, naturally.)

But Jr only gets what the IRS doesn’t take, so I’m taking my tax efforts to the next level: multi-generational tax minimization.

Note: The ability to withdraw funds over the beneficiaries lifetime was eliminated in the SECURE Act. Check out the details here.

Multi-Generational Tax Minimization

Much of what I’ve seen with regards to multi-generational tax minimization/wealth preservation is focused on avoiding/minimizing the impact of the Estate Tax, often by companies or persons with a vested interest in selling you a Trust (“Hey little kid, would you like to buy a trust?” said the Big Bad Wolf.)

Trusts have their place, but I have a simple and guaranteed solution to avoiding the Estate Tax altogether and it costs a lot less – just die with less than $22 million in assets. It’s so easy, almost anyone can do it.

With each adult able to pass ~$11 million to their heirs without taxation (at the Federal level), for most of us, the Estate Tax is a non-issue. But it is an incredible opportunity to build a family dynasty. The Kennedys, the Rockefellers, the Curry Crackers…

Even with the Estate Tax out of the way, there is still a lot to consider.

Gifting

There are pros and cons of providing gifts to your adult children. In the book The Millionaire Next Door they call it Economic Outpatient Care, and it is highlighted as a way parents prevent their children from becoming economically successful in their own right. Dependence is a helluva drug.

Our family gifts flow in the opposite direction, but regardless there is a right and wrong way to do it, tax wise.

You may have heard the recommendation to gift appreciated stock to a charity, rather than sell it, pay taxes, and then donate the remaining cash. The charity is able to benefit from the full amount rather than the reduced after-tax value.

There are similar considerations when gifting to individuals.

When a gift is made, the recipient’s basis in the asset is equal to the lower of the original owner’s basis and the current market value.

Unlike a charity, a person has tax obligations, so we need to consider Jr’s tax status – if we gift appreciated shares, when he sells will he have to pay more or less tax than if we sold the stock and gifted cash? Maybe we have a 0% capital gain tax rate whereas he is in his prime working years and would have to pay 15-23.8%.

If we’ve raised our basis over the years and are thus able to sell stock at a loss, are we better off doing so than gifting the stock directly?

Probably. But we should also avoid getting to that point…

Stepped up basis

The basis on inherited assets is stepped up to the market value at the time of death. Unrealized gains on these assets are thus never subject to income tax. It’s the ultimate capital gain harvest, in both senses, and provides a new context for prioritizing Roth conversions vs Capital Gain Harvesting.

Bought some stock or a house for $1 and it is now worth $10 million? No taxes, now or ever.

Got some rare artwork in the basement from a recently discovered star? No taxes.

Antiques, coins, gold, baseball cards…. all no taxes.

It is easy to take advantage of this incredible opportunity – simply do nothing.

And there’s the rub…

I’m a big fan of doing nothing, but this isn’t always possible or the best option.

It can be worth paying some tax now to pay less tax later. This is a good choice if/when we decide to move back to California – I can pay some tax at 15% now to avoid paying some tax at 17-23%+ later.

But with everything being stepped up in basis upon death, harvesting more than we might spend results in paying 15% rather than our heirs paying 0%.

We need to take the Goldilocks approach… not too much, not too little. This seems more of an art than a science.

The exception: Retirement accounts.

Retirement Accounts

The ability to withdraw funds over the beneficiaries lifetime was eliminated in the SECURE Act. Check out the details here.

401ks, IRAs, etc… are tax-deferred vehicles, the key word being “deferred.”

Beneficiaries of an inherited retirement account are required to withdraw those funds, as a lump sum, over 5 years, or with Required Minimum Distributions (RMDs) over the beneficiaries’ lifetime. Upon withdrawal, those funds are subject to taxation, although there is no 10% early withdrawal penalty. (RMDs still apply if the inherited account is a Roth. Roth conversions are an option on inherited IRAs only for a spouse.)

For lifetime tax minimization, the RMD route gives us the greatest number of years to work with, but the 5-year approach could make sense if account values are low and we know those 5 years will be low-income years (e.g. college, sabbatical, etc…)

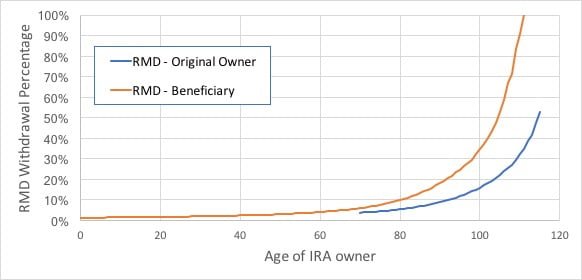

Standard advice says bequeathing a retirement account to the youngest possible beneficiary is a good way to maximize deferral benefits.

And that is kind of true – the RMD for a 10-year-old is only 1/4 that of the RMD for an 80-year-old IRA originator and only 1/3 for a 40-year-old. However, they ramp up much more aggressively. (The result being the inherited IRA value approaches zero about 15 years earlier than it would have had the original owner lived.) Note the word “minimum” in the acronym RMD.

RMDs & Tax-Deferred Growth

Presumably, a larger RMD will be taxed more heavily, but that isn’t necessarily the case – a large withdrawal by a retired couple with minimal other income may face a lower tax rate than a small withdrawal by a single person during their peak earning years. (Due to single filer brackets being half the size of married couples’.)

This makes multi-generational tax minimization a difficult game. We must not only predict the rate at which withdrawals will be taxed during our own lifetime but also during our children’s or grandchildren’s.

For the original IRA owner, RMDs begin at Age 70.5. With 7% annual growth, even with required withdrawals, the IRA will continue to grow well into our 80s, eventually fading towards zero as we become a centenarian. The RMD accomplished what it was designed to do.

This chart shows the outflows and IRA value based on an arbitrary amount of $1 million at age 70.5 with 7% real annual growth.

Now, if the IRA owner passes at Age 85 (for example) and bequeaths the retirement account to a beneficiary 40 years younger, the IRA can benefit from an additional 60+ years of growth. (A “stretch” IRA.)

RMDs for the beneficiary will start immediately, albeit at a lower percentage, and the IRA will continue to grow well past traditional retirement ages. By the time the beneficiary reaches their own normal RMD age of 70.5, the IRA could have tripled… even after 30 years of minimum withdrawals.

Multi-Generational Tax Minimization, GCC Jr Edition

I’m unlikely to predict our own taxes over the coming decades, let alone Jr’s over the next seven.

But we can give it a shot. Here is a simple enough thought experiment:

I’ll be 45 this year. Jr just turned 4.

If I earmark ~$200k in my IRA as Jr’s inheritance, invested for future real growth of 7%/year, then it will be worth ~$1 million when I hit RMD age in 25 years or so.

My life expectancy is somewhere around 85 years old. I’ll live much longer because I’m a crotchety old bastard, but it’s as good of a target as any for illustrative purposes.

Even with RMDs, the original $200k will grow to about $1.3 million by the time I reach age 85, as shown in the first RMD chart above.

If I pay tax on those RMDs (if any) out of my own pocket, and let the RMD funds continue to grow 7% in a taxable account, then they will grow to an additional $1.3 million.

Jr’s total inheritance: $2.6 million around age 40, $1.3 million in a Traditional IRA and $1.3 million in stocks in a taxable account. (The Economist was right about this one – The simplest way to become rich is to be born to the right parents.)

Based on the 4% Rule, this could sustain a cost-of-living of $104,000/year.

Dividends of 2% would pay $26,000/year.

The RMD the following year would be ~$36k (2.58%.)

Now, what would his tax situation look like, assuming the tax code of the future resembles that of today?

If he were married with no other income, spending 4% (withdrawing additional funds from IRA), taxes would be about $6,500 with a top marginal rate of 12%. (If he instead withdrew basis from the stock in the taxable fund, taxes would be ~$2k, but greater in the future.)

If he were single, taxes would be about $14,000 with a top marginal rate of 22%.

If he were married and earning a median income (single income household), all of the RMD would be taxed at 12% and all of the dividends at 15%, for a total inheritance related tax bill of ~$8,000.

Which of these situations is most likely to apply?

Probably all of them at various points, but as the RMD levels increase rapidly… these tax rates are likely to be the lowest that will ever be paid… by the time Jr is 60 years old, the RMD will be more than $100,000/year.

Hence, if we have the opportunity to pay 10% on Roth conversions anytime between now and our ultimate demise, then we should probably do so…. and maybe even a little at 12%.

Mathematically speaking, choosing to pay 10% now on a Roth conversion is equivalent to paying 10% on a larger withdrawal 60 years from now (associative property of multiplication.) But doing so could guarantee that the future rate isn’t much greater than 10%, a real possibility considering the aggressive RMD rate increase for an inherited IRA (as well as our own potential to pay a very real death tax.)

But can we be more specific? It’s hard to take action when things are a little vague. But such is the future…

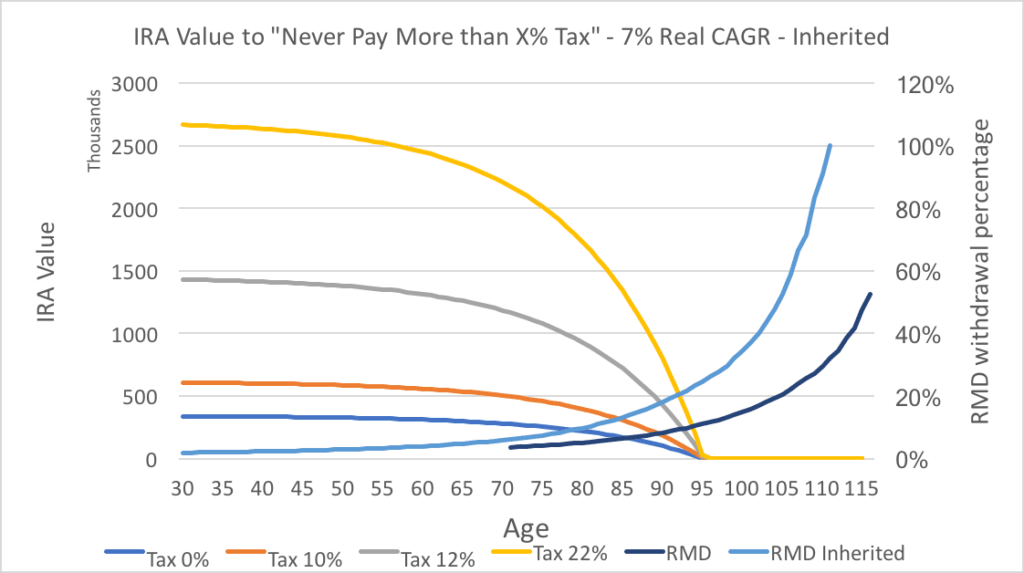

Although, I could use the same methodology that I used to analyze Is Your 401k Too Big? to get something a little more precise. (This chart modified to use the more aggressive RMD for Inherited IRAs.)

For a married couple, with no other income, if the IRA value exceeds any of the thresholds in the chart then tax rates will exceed a specific marginal rate. Example: if the IRA exceeds ~$1.4 million for a 40-year-old then taxes will need to be paid at a rate above 12% (see Tax 12% gray line.)

If other income (like a job) fills the standard deduction (Tax 0%) and 10% bracket (Tax 10%) (slightly below median incomes) then thresholds are lower, and we need to reduce our allowed IRA values by roughly $600k (the Tax 10% line) to $800k-$900k to avoid paying tax above a 12% rate.

Or stating it differently, if Jr’s inherited IRA is on track to exceed about $800k-$900k in value (which it will), we should do Roth conversions at rates <12% to get the size back below those levels.

Conclusions

It’s good to be born to parents with a head for $$$, but planning for tax minimization over multiple lifetimes is still a real challenge.

The very generous exemptions to the Estate Tax, combined with gifting, stepped-up basis upon death, and “stretch” IRAs, mean that it is easier than ever to build a dynastic portfolio.

Tax laws may change, and so much of the tax code is situational (married/single, other income/no other income, dividend income or earned income), that no matter what we do we are still only guessing what will result in multi-generational tax minimization. The future is very cloudy.

As such, it is probably best to err on the conservative side (don’t pay tax now if you don’t have to) and take the Goldilocks approach… not too much, not too little.

For the purposes of the Curry Cracker Dynasty, when looking beyond our own lifetime’s battle with the RMD, we will need to be a bit more aggressive… it looks like RMDs will require Jr pay 12% tax rates through much of his adult lifetime.

This tax rate would be a new reference point for tax minimization efforts. If we have the option of doing Roth conversions at a lower rate then we should seize the opportunity.

Note: The ability to withdraw funds over the beneficiaries lifetime was eliminated in the SECURE Act. Check out the details here.

With the Taiwanese checkups you’ll live quite long. Also make sure to have the website as part of your foundation so I can reread it when I’m at a more appropriate age with children.

As for me, still thinking of minimizing my personal

taxes and growing retirement funds, but will keep these considerations in mind.

Focusing on our own lifetimes is priority #1.

I retired with a pension that keeps me in the 22% tax bracket for life (until tax laws change again). This year I am starting Roth convertions up to the max 24% bracket (I have 15 years before my RMD’s). I figure I have 6 years until my tax bracket goes back to 25%. But once in the Roth my tax liability is over. This still will not empty my tax deferred account so all I can hope for is taxes not changing. I wish I could pay less taxes but as you say we don’t know the future for taxes. But I don’t think they will go lower. The good part my kids will not have to worry about paying taxes on the inherited Roth IRA.

Yeah, I think we are at a low in terms of taxes.

There are several bills under consideration by Congress currently that would eliminate stretch IRA’s and set the withdrawal period at a maximum of five years in exchange for raising the RMD a year or two. In your shoes, I would make an alternate plan that considers the modification or elimination of the stretch IRA.

In addition, there are currently proposals in the California legislature to impose a state estate tax. Washington and

Oregon already have estate taxes at the state level. The most egregious proposal is to reinstate the old federal rate at the state level for estate values between the old federal limit in the three million range to the current $11.4 million limit. That won’t likely pass, but I would expect to see an estate tax comparable to Washington and Oregon in the next few years.

There is always legislation. When it becomes law I’ll make adjustments.

Jeez, that’s complicated. I’d probably try to get most of the money out of the retirement funds before we go. That way our son won’t have to deal with that piece of it.

The only complicated part is predicting the future.

The only way for our children to not have to deal with it is to inherit 100% Roth (will still have RMDs.) But at what cost?

I’d rather inherit the largest after-tax value.

Bookmarking this for future reference. I can picture a kid (40 year old like your example) without the right financial know-how landing with a big inheritance windfall, not knowing what to do with it, and turning it all over to Edward Jones so they don’t have to worry about it (while grieving). Ideally if the parents went thru all the hoops to minimize taxes, the child would also be sharp enough to avoid the investment management fee haircut.

I should have mentioned the most important inheritance at all – financial knowledge.

I think you are right to highlight the “economic outpatient care” angle. Being supported by one’s parents deep into adulthood can really mess people up. I’ve seen in with some of my relatives. Best solution is for you and the Mrs. to live such a long life that Jr. has to step up and build his own self-sufficient life. If he inherits all the assets at 50, he’ll be mature enough to handle it by then and not be debilitated by the lack of needed to ever make a dime…..

Thanks for this post, btw. It’s something I’ve been thinking about quite a bit as well. The great news is the $22 mill threshold, the step-up in cost basis at death for taxable accounts, and the zero taxes on inherited Roths. Basically, the order of preference for passing on assets to heirs would be Roth Account, then taxable, then traditional IRAs and 401Ks. Cheers!

I think the preferred way to inherit assets is based on the largest after-tax value. That may or may not be the same order that you listed.

Fair enough.

Are you familiar with any similar strategy for Canadian?

Sorry, I’m not familiar with Canadian law at all.

My brother and I each inherited a million from our parents, zero taxes since most of it was in taxable accounts. But we were already millionaires and did not need it. My three kids will likewise receive seven figure inheritances from us. But, like us, they won’t need it and will hand it down to their kids. A nice family tradition.

Money, the gift that keeps on giving.

Slightly different animal (but still in the spirit of multi-generational tax minimization) are you about to open a Roth for junior in his own name? His earning potential is a bit limited (get to work, junior!), but he’s already been a model here, and the possibilities for him to have earned income will just increase in the years ahead.

Yes.

You’re thinking of moving to California? Cool. We live in SF. We couldn’t make it to your SF meet up in Dolores Park last time but looking forward to a chance to meet up in the future.

Considering it… maybe in a few years.

I’m always up for a coffee if you are in the neighborhood!

Thoughts? https://www.forbes.com/sites/leonlabrecque/2019/04/23/new-proposed-stretch-ira-rules-will-have-a-big-effect-on-iras-and-it-could-cost-your-kids-thousands/#687804fa2233

I’ll wait until infrastructure week is over before really thinking about it. There is always new legislation…

Reducing the stretch to 5 or 10 years means higher marginal rates.

Very roughly, the present value of tax paid if you inherit a $1KK Traditional IRA at age ~40 and follow the withdrawal approach in the “never pay more than X% tax” graph above, with no other income:

current law: X

10 year withdrawal period: 2X

5 year withdrawal period: 4X

So, I might choose to do Roth conversions in my lifetime at a higher rate to get lower rates in Jr’s lifetime, paying more than X but less than 2X.

As an aside… I suppose an unintended consequence of eliminating the stretch is that you might see a lot more mid-career breaks.

I like the mid-career break incentive:) Or more folks applying for disability- who knows?

It’s pretty sneaky, though, and it would certainly make retirement accounts less valuable to the many people who use them for estate planning, and would have alocated differently. Definitely see the advantage of making sure kids have their own Roths.

But, let’s see what happens, as you say.

If you are going to raise taxes on a large number of people, especially after major tax reductions for the uber wealthy, it is probably best to do it in a sneaky way. It’s kind of like how the TCJA changed how inflation was calculated, thereby likely resulting in the bottom 2/3 of the country paying more taxes in 10 years than before the TCJA…

Overall, elimination of the stretch is probably a good thing… what percentage of people die with massive IRAs?

Some random data says that the avg 401k for people ~age 70 is $200k (median: $60k.) Maybe 2x that for married couples? I think the Senate’s version had an exclusion for IRAs less than $400k… The people most impacted by this are well above average.

Dude, I’m hiring you as my tax/financial manager. Let’s discuss your hourly rate…

How do you put a price on art?

sotheby’s auction?

Next up on the auction block is an hour of Jeremy’s time…. let’s start the bidding at $10,000. Do I hear $10k?

Art is selling for quite a bit these days: https://www.latimes.com/business/hiltzik/la-fi-hiltzik-koons-artwork-20190517-story.html

Thanks for the discussion. Hope to hear more when/if this becomes law.

survivorship bias?

Another great tax post GCC! I think that’s your strong suit and what’s keeps readers coming back.

I agree that predicting future tax laws is anyone’s guess. It’s hard to plan properly when there’s no concrete answer. I like your thinking though for optimizing the stepped up gift exchange of inherited assets to avoid a lot of taxes.

From what I concluded, it seems most prudent to leave Roth accounts alone indefinitely and to spend down tax sheltered accounts but do it smartly while living.

The best thing is to keep income zero after retirement. Seems like a catch 22 though since the standard advice of the wealthy is to have multiple streams of income.

What to do?

>The best thing is to keep income zero after retirement.

Would you rather get a dollar and have $0.75 or so after taxes, or get no dollar and have zero/nada/zilch?

https://www.salon.com/2019/06/23/congress-targets-middle-class-retirement-savings_partner/

“The difference is instead of your kids having $2 million, your kids will be broke because the income tax acceleration reduces the IRA so much.”

So… a 100% tax. Or too much drama.

Thanks for this very useful analysis. Most FI people with children see financial planning through the perspective of their children, not their own.

Unfortunately the article is already becoming obsolete as the (ominous) tax code of the future is already here:

The “secure act” that is about to pass Congress would disallow your children from stretching RMDs over their lifetimes, requiring them instead to withdraw all IRA funds in 10 years.

Bottom line: Your (our) IRAs will grow too big much faster.

I have not worked out the numbers yet (perhaps an updated article from Curry Cracker may help) but I suspect that for many many of us it would be better to stop traditional IRA contributions immediately.

Another planning corollary may be: Don’t bother too much making your children capable of earning high salaries (i.e. too productive). It’s not worth it, as the pitchforks will come after any “excess” excellence.

Are Roths indeed safe from taxation? Who promises that? Democracy?

>I have not worked out the numbers yet…

Dude.

Even before working out the numbers… it is pretty obvious that the impact will be huge:

For those interested in a little more detail on the pending “Secure Act” legislation regarding Retirement Accounts:

https://www.forbes.com/sites/leonlabrecque/2019/04/23/new-proposed-stretch-ira-rules-will-have-a-big-effect-on-iras-and-it-could-cost-your-kids-thousands/#7c29867f2233

…actually will likely cost our kids hundreds of thousands…

But this also has further reaching implications regarding future returns from the US economy. Upending three decades of assumptions regarding saving into Retirement accounts with what turns out to be “bait and switch” tax laws is a great way to destroy societal trust. So seems like America is becoming a Pitchfork Democracy. A Banana Republic and a Greek economy are the likely outcomes! I think that investors should seriously take this long term national trajectory into consideration when it comes to long term financial guidance. In more practical terms, long term assumptions about future 7% investment returns in US securities seem quite unlikely in such an environment.

Mathematics before histrionics.

…or logic before slogans?

I saved in my 401K all my working life. The Secure Law has put a dent in my plans. I am thinking of leaving a small percentage of my 401K to each grandchild. I can not get an answer to this question: How much can each minor earn before he has to pay income tax on the earnings?

The kiddie tax is something to be aware of. Minor children have to pay tax at their parents’ tax rate on non-earned income over ~$2200.

You may see some conflicting info when reading about the kiddie tax – The TCJA applied estate and trust (much higher) tax rates, and the SECURE Act repealed that change so it is now back to being taxed at parents’ tax rates.

Also, see my analysis of the SECURE Act.